Synergistic Effects and Financial Performance of Kenya Agricultural and Livestock Research Organization.

- Okuku Washingtone Oluoch

- Dr. Fredrick W.S. Ndede

- 2213-2223

- Jun 22, 2024

- Agriculture

Synergistic Effects and Financial Performance of Kenya Agricultural and Livestock Research Organization.

Okuku Washingtone Oluoch*, Dr. Fredrick W.S. Ndede

Department of Accounting and Finance, Kenyatta University

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2024.805163

Received: 14 May 2024; Accepted: 21 May 2024; Published: 22 June 2024

ABSTRACT

This paper explores the synergistic effects and financial performance of KALRO, which is one of the State Corporations in Kenya. It envisaged finding out whether there is a strong relationship between operating and financial synergies and KALRO’s financial performance using primary and secondary data. A sample of 32 respondents were selected using stratified random sampling from key management personnel. Structured questionnaires were administered to gather information, which was analyzed on SPSS Statistics version 25. A pilot study was used to test for the validity of the study to know whether the questions were aligned with the study hypotheses. The findings revealed that synergy gains had a bigger influence on the performance of KALRO. The operating synergy was found to have a significant positive influence on KALRO’s performance (Adjusted R2 = 0.695; p = 0.024), while financial synergy had an insignificant negative influence on KALRO’s performance (Adjusted R2 = 0.185; p =0.218). Government policy was found to have a significant mediating effect between synergistic gains and performance of KALRO. The limitation of this research was the smaller sample size, thus, a comprehensive research was recommended to determine the synergy spread in all 16 KALRO institutes and centers.

Keywords: Synergy, Operating synergy, financial synergy, KALRO, State corporations, Parastatals.

INTRODUCTION

Mergers have become crucial strategies for firms in private and public sectors to increase their efficiency and financial performance. The perceived synergistic gains in terms of operating, financial and managerial synergies drive companies to engage in merger deals. Kalsie and Nagpal (2017) defined as a business combination that brings together assets or resources of different firms under the control of one entity for economic benefits, which could not be achieved by individual firms working alone.

In Kenya, the merging of state corporations gained momentum after the release of The Presidential Taskforce on Parastatals Reform (PTPR) of 2013, which pointed out critical factors that cause inefficiency in the operations of State Corporations in Kenya (GOK, 2013). The aim of the merger deals was to align State Corporations (SCs) to the national agenda and reducing their overdependence on government funding through the Exchequer. In this regard, the Kenya Agricultural and Livestock Research Organization (KALRO) was formed by merging four state corporations. KALRO was formed by merging KARI, KSF, CRF, and TRF under the KALR Act, 2013. The aim of the merger was to promote the growth of the agriculture and livestock sectors by providing coordinated research as well as regulations through technology and innovation, in addition to resource transfer and use of agricultural research findings.

The influence of synergistic gains on the financial performance of companies has been discussed in many studies, with the results showing mixed findings. The results from some studies showed that mergers improved operating, managerial, and financial synergies, leading to greater financial performance (Garzella and Fiorentino (2017), Oroh (2016) and Ogada et al. (2016)). On the other hand, Sirower (2010) maintained that the perceived synergistic gains are dead on arrival and hence do not exist. The performance of the business is affected by the prevailing market forces, and therefore merger deals can have very little consequence on an enterprise’s operational outcome. This creates a further discussion on the synergistic gains and performances of a company. Most of the studies on mergers in Kenya are in the private sector, a few on state corporations found some improvements in the performance after the mergers. This paper explored the relationship between the synergistic gains and the financial performance of KALRO.

LITERATURE REVIEW

Theoretical Review

Various research works identify some critical theories that support merger deals. The main theories examined in this paper include synergy theory and efficiency theory. According to Garzella and Fiorentino (2017), synergy theory maintains that the crucial promoter of merger deals is to achieve greater synergies. Oroh (2016) cited that the mathematical expression of synergy is 2+2=5, where 2 and 2 represent the performance of individual firms working independently while 5 is their overall performance when working together. It implies that the overall performance in the merger deal should be higher than individual companies working independently. Many research works identified operating, managerial and financial synergies as key parameters for measuring synergistic gains. Although some critics dispute the existence of synergy gains, others found that companies can leverage the created economies of scale, scope, and pricing strategies in order to realize the expected synergy.

Further, efficiency theory exists where one or some of the companies in the merger deal are efficient, thus, the efficient companies use their skills to improve the inefficient firms (Leepsa and Mishra, 2016). By leveraging the economies of scope and scale, the merger can result in cost-savings for consumers and better performance of the organization.

Empirical Theory

Several studies on mergers and acquisitions measured the synergistic gains resulting from mergers in terms of operating, financial and managerial synergies using different proxies. For instance, Kimetto (2019) found that the merger of Sidian Bank resulted to increased liquidity, leverage and management efficiency, resulting to greater after-merger financial performance. These findings confirmed an earlier study by Ogada et al. (2016) in the financial sector, which found that there was a significant increase in after-merger performance of the firms in the merger deal. In China, Wang (2018) studied the effects of mergers using China Zhonghua Geotechnical Engineering Company, which is a state corporation, and found that the merger deals improved operating synergy measured by profitability and growth potential of the company with insignificant improvements in financial and managerial synergies. A comparative study by Zhou et al. (2015) on private and state owned companies’ performance revealed that state companies as acquirers performed better than private companies as acquirers.

A study by Mwasaa (2018) on cost reduction as a result of mergers of state corporations to form Agriculture and Food Authority (AFA) revealed a significant cost reduction after mergers, leading to better performance of the company. Ombaka and Jagongo (2018) also investigated the impact of operating synergy of Kenya’s financial institutions and found a similar result that there is a positive correlation between financial performance and operating synergy. These two research works confirmed earlier findings which revealed that operating synergy is a critical determinant of financial performance in mergers.

Further, Florio, Ferraris and Vandone (2018) found that over 60% of state corporations’ mergers are driven by increasing managerial efficiency in terms of increased market power and diversification to maximize shareholders’ wealth. The transfer of knowledge across the merged companies improves management efficiency, leading to higher organizational performance. Benassi and Landoni (2019) considered state corporations as Knowledge Explorer Agents with the ability to achieve the desired managerial synergy by organizing the knowledge of competency integration through collaborations and partnerships for better financial outcomes. In this regard, mergers are the quickest way to transfer such knowledge.

Since the operations of state corporations are significantly influenced by the government decisions through the Acts of Parliament, it was crucial to examine the mediating effect of government policies such as financing policy and regulation on the performance of SCs. Ireri (2016) found a relatively weak legal framework in financial control and politicization, which affect the performance of SCs in Kenya. Mutegi and Ombui (2016) reiterated that excessive regulation and control and political interference adversely affect the operations of state companies, hence affecting their performance.

Research Objectives

The objectives of this research paper are:

- To find out whether operating synergy has a substantial influence on KALRO’s financial results.

- To explore whether financial synergy strongly influences KALRO’s financial results.

PROBLEM STATEMENT

State corporations play an invaluable role in the Kenyan economy by providing essential public goods, revenues through taxes, employment creation, and GDP growth. However, the PTPR report 2013 pointed out the inadequate performance management framework of SCs that has failed to link the institutional and individual performance to the nation’s goals, leading to their poor performance (GOK Report, 2013). Although most state corporations are not for profits, their positive gains or surplus income can be ploughed back into the business to reduce over reliance on the Exchequer. Besides, the appropriate use of resources in SCs can help save public money for other developments. Therefore, understanding the influence of synergistic gains resulting from the mergers of state corporations is important to add knowledge to the existing literature. Healy, Palepu and Ruback (2012) stated that mergers could create a positive or negative organizational performance. For this reason, the public, the government, investors, and other stakeholders would be interested to know the performance achievement of KALRO by observing the synergistic gains.

Some of the few studies on the effects of state corporations’ mergers on their performance include Mwasaa (2018), who observed after-merger cost reduction on AFA performance and found a positive reduced cost among some units of AFA, whereas the overall performance was limited. Osege (2013) found a positive relationship between KALRO’s adoption of new reforms through change management and its performance. These past studies provided a noble ground for this research to explore the synergistic gains as a result of mergers of state corporations in Kenya and the influence on performance. This research envisaged to explore the synergistic gains and their contributions to the financial outcomes of KALRO. The aim was to arrive at a generalized deduction on whether mergers could be an effective strategy to increase and maintain the higher financial performance of SOEs in Kenya.

Study Hypotheses

The two hypotheses of this study were:

- There is a positive correlation between operating synergy and financial synergy gains resulting from the mergers of state corporations and KALRO’s financial results.

- There is a strong mediating effect of government policies on the operating and financial synergy gains and KALRO’s financial performance.

METHODOLOGY

This paper envisaged to examine the influence of synergistic gains on KALRO’s performance. The study used a sample of 32 participants from senior and middle-level managers randomly selected from the four merged state corporations in different parts of Kenya. Quantitative primary and secondary data was gathered using structured questionnaires and secondary data collection template developed by the researcher. A pilot study was done to test for reliability on SPSS Statistics version 25 using Cronbach Alpha at a 70% threshold. The results of the Cronbach Alpha are shown in Table 3.1

Table 3. 1 Research Questions Reliability

| Cronbach’s Alpha | No of Objects | |

| Operating Synergy | 0.834 | 6 |

| Financial Synergy | 0.855 | 6 |

| Performance | 0.890 | 3 |

Since the questions in the questionnaire had an Alpha greater than 0.7 or 70%, the questionnaire passed the internal consistency; thus, it guarantees reliability.

To test for the validity of the research questions, the researcher incorporated input from some KALRO key personnel collected during the pilot study to develop straightforward questions that meet the research objectives. The panel of professional lecturers provided me with constructive feedback to improve the research questions to help meet construct and content validity.

Correlation analysis and regression analysis were used to determine the relationship between the synergistic gains and KALRO’s financial results as well as the degree of influence of independent variables on the dependent variable. The growth in revenues from exchange transactions was used as a proxy to operating synergy, while liquidity was used as a proxy to financial synergy in secondary data.

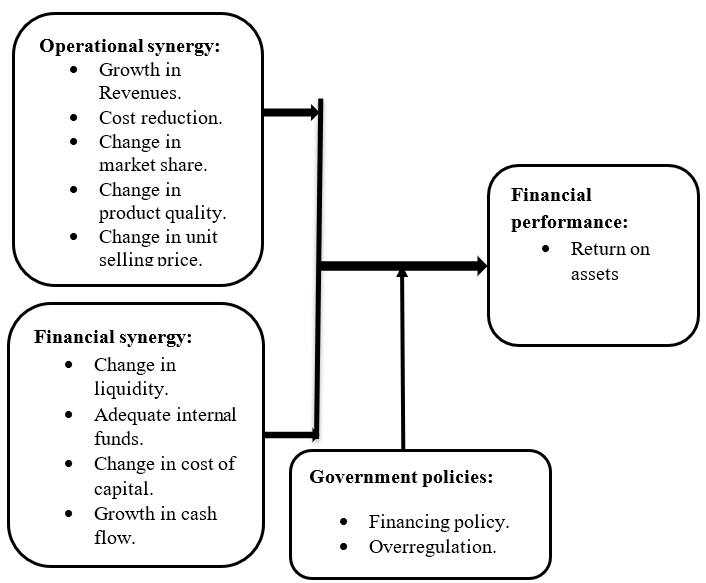

Conceptual Framework

DATA ANALYSIS

The response rate was 93.75% (30 people) consisting of 50% from crop section and 50% from livestock section.

Distribution of Respondents by Institutes

Respondents’ Distribution

| Frequency | Percent | Cumulative Percent | |

| Tea RI | 5 | 16.7 | 16.7 |

| Coffee RI | 3 | 10 | 26.7 |

| Sugar RI | 5 | 16.7 | 43.3 |

| Veterinary RI | 6 | 20 | 63.3 |

| Biotechnology RI | 8 | 26.7 | 90 |

| Food Crop RI | 3 | 10 | 100 |

| Total | 30 | 100 |

Sixteen of the respondents were men (53%) while 14 (47%) were women. The majority had more than 20 years of work experience in the institutions under KALRO. This mixed demographic enhanced the reliability of the data to support the generalization.

Testing Hypothesis 1 (Primary Data) Operating Synergy

The hypothesis was tested by applying correlation analysis using Model 1 below.

Performance = α0 + α1X1 + α2X2 + α3X3 + ε ……….. Model 1 (Without mediating variable)

Correlation of Operating Synergy and Performance

| Operating Synergy | Performance | ||

| Operating Synergy | Pearson Corr. | 1 | .690** |

| Sig. (2-tailed) | 0.000 | ||

| N | 30 | 30 | |

| Performance | Pearson Corr. | .690** | 1 |

| Sig. (2-tailed) | 0 | ||

| N | 30 | 30 | |

| ** Corr. is sig. at the 0.01 (2-tailed). | |||

Source: (Survey, 2022)

The results found a substantial positive association between operating synergy and KALRO’s performance since r = 0.690 or 69% and the sig. of 0.000 is below 0.01.

Regression Coefficient for Operating Synergy

| Coefficientsa | ||||||

| Model | Unstandardized Coeff. | Standardized Coeff. | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | 0.567 | 0.396 | 1.431 | 0.163 | |

| Operating Synergy | 0.72 | 0.143 | 0.69 | 5.05 | 0.000 | |

| a Dependent Variable: Performance | ||||||

Source: (Survey, 2022)

The regression coefficient analysis of operating synergy revealed that when the operating synergy is kept constant, the performance would be at 0.567 intercept. However, any unit rise in operating synergy would result in a 0.720 increase in KALRO’s performance. The results confirmed the findings by Ogada et al. (2016) and Ombaka and Jagongo (2018) on the positive correlations between operating synergy and financial performance of companies.

Financial Synergy

Correlation Analysis of Financial Synergy and Performance

| Financial Synergy | Performance | ||

| Financial synergy | Pearson Corr. | 1 | .872** |

| Sig. (2-tailed) | 0.000 | ||

| N | 30 | 30 | |

| Performance | Pearson Corr. | .872** | 1 |

| Sig. (2-tailed) | 0.000 | ||

| N | 30 | 30 | |

| ** Corr. is sig. at the 0.01 (2-tailed). | |||

Source: (Survey, 2022)

The findings indicated a strong positive association between financial synergy and the performance of the organization, with an R-value of 0.872 or 87.2% and a p-value of 0.000 below 0.01.

Regression Coefficient Analysis for Financial Synergy

| Coefficientsa | ||||||

| Model | Unstandardized Coeff. | Standardized Coeff. | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | 0.396 | 0.234 | 1.694 | 0.101 | |

| Financial synergy | 0.891 | 0.095 | 0.872 | 9.423 | 0.000 | |

| a Dependent Variable: Performance | ||||||

Source: (Survey, 2022)

The regression coefficient of the two variables shows that when financial synergy is kept constant, the outcome would be at 0.396 intercept. A one-unit rise in financial synergy would result in a 0.891 increase in the organization’s financial outcome.

Testing Hypothesis 1

The hypothesis was tested using Model 2 as shown below using PROCESS procedure version 4.1 by Andrew F. Hayes on SPSS Statistic 25 with government policies as the intervening variable.

ROA = α0 + α1X1 + α2X2 + α3X3 + Z(α6X1X2X3)+ ε ….. Model 2 (With mediating variable)

Mediating Effect of Government Policies on Operating Synergy

| Total effect of operating synergy on financial performance | ||||||

| Effect | se | t | p | LLCI | ULCI | c_cs |

| 0.7203 | 0.1426 | 5.0498 | 0 | 0.4281 | 1.0125 | 0.6904 |

| Direct effect of operating synergy on financial performance | ||||||

| Effect | se | t | p | LLCI | ULCI | c_cs |

| 0.7892 | 0.1385 | 5.6971 | 0 | 0.5049 | 1.0734 | 0.7564 |

| Indirect effect(s) of operating synergy on financial performance: | ||||||

| Effect | BootSE | BootLLCI | BootULCI | |||

| Government Policies | -0.0689 | 0.0682 | -0.2381 | 0.0117 | ||

Source: (Survey, 2022)

The total effect of 0.7203, the direct effect of 0.7892 and the indirect effect of -0.0689, with a p-value of 0.000, show that the connection is statistically significant with a negative indirect effect.

Total, direct, and indirect moderating effect of government policies

| Total effect of financial synergy on financial performance | ||||||

| Effect | se | t | p | LLCI | ULCI | c_cs |

| 0.8911 | 0.0946 | 9.4227 | 0.000 | 0.6974 | 1.0849 | 0.8719 |

| Direct effect of financial synergy on financial performance | ||||||

| Effect | se | t | p | LLCI | ULCI | c_cs |

| 0.9099 | 0.0894 | 10.1778 | 0.000 | 0.7265 | 1.0934 | 0.8903 |

| Indirect effect(s) of Financial synergy on financial performance: | ||||||

| Effect | BootSE | BootLLCI | BootULCI | |||

| Government Policies | -0.0188 | 0.0368 | -0.1041 | 0.0526 | ||

Source: (survey, 2022)

The results show that total effect of 0.8911, direct effect of 0.9099, and indirect effect of -0.0188, with a p 0.000, indicate a statistically substantial association exists between financial synergy and performance of KALRO.

Using Secondary Data Correlation Analysis

Operating synergy was proxied using growth in revenue from exchange transactions, while performance was measured using ROA. The correlation results were as follows:

Correlation for Synergy and Financial Performance

| Operating Synergy | Financial Synergy | GOK | ROA | ||

| Operating Synergy | Pearson Corr. | 1 | -0.734 | .966** | .870* |

| Sig. (2-tailed) | 0.097 | 0.002 | 0.024 | ||

| N | 6 | 6 | 6 | 6 | |

| Financial Synergy | Pearson Corr. | -0.734 | 1 | -0.737 | -0.591 |

| Sig. (2-tailed) | 0.097 | 0.095 | 0.217 | ||

| N | 6 | 6 | 6 | 6 | |

| GOK | Pearson Corr. | .966** | -0.737 | 1 | .953** |

| Sig. (2-tailed) | 0.002 | 0.095 | 0.003 | ||

| N | 6 | 6 | 6 | 6 | |

| ROA | Pearson Corr. | .870* | -0.591 | .953** | 1 |

| Sig. (2-tailed) | 0.024 | 0.217 | 0.003 | ||

| N | 6 | 6 | 6 | 6 | |

| ** Corr. is sig. at the 0.01 (2-tailed). | |||||

| * Corr. is sig. at the 0.05 (2-tailed). | |||||

Source: (Survey, 2022)

The results found that operating synergy and ROA had a significant positive relationship with an r=0.870 or 87.0% and sig. 0.024. The analysis shows a negative relationship between financial synergy and ROA performance, with an R-value of -59.0%. This infers that an upsurge in financial synergy would result in a reduction in the financial outcome of KALRO. However, the relationship was found to have an insignificant influence on performance (Sig. = 0.218). The correlation analysis was conducted with government spending as a proxy. The findings were that government policies influenced KALRO performance positively and significantly (r= 0.953 or 95.3%; p=0.003).

Regression Analysis

Operating Synergy

Regression Coefficient for Operating Synergy

| Model | Unstandardized Coeff. | Standardized Coeff. | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | -0.047 | 0.010 | -4.905 | 0.008 | |

| Operating Synergy | 4.439E-11 | 0 | 0.870 | 3.531 | 0.024 | |

| a Dependent Variable: ROA | ||||||

Source: (Survey, 2022)

The performance equation would be ROA = -0.047 + 4.431E-11*Operating synergy. It implies that at constant operating synergy, the performance was at -0.047 intercept. However, unit increase in the operating synergy increased the financial performance of KALRO by 4.439E-11 times.

Financial Synergy

Table 4. 38: Regression Coefficient for Financial Synergy

| Coefficientsa | ||||||

| Model | Unstandardized Coeff. | Standardized Coeff. | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | 0.005 | 0.013 | 0.374 | 0.727 | |

| Financial synergy | -0.003 | 0.002 | -0.59 | -1.461 | 0.218 | |

| a Dependent Variable: ROA | ||||||

Source: (Survey, 2022)

The regression coefficient analysis found that when financial synergy was kept constant, the performance KALRO would be at a 0.005 intercept. A unit growth in financial synergy contributed to 0.003 times decrease in KALRO performance financially.

CONCLUSION

The aim of this research was to explore the synergistic effect of mergers on the financial performance of KALRO. The research hypothesized that operating and financial synergies strongly correlate with an organization’s performance. The findings of this research revealed that the merging of state corporations under KALRO improved operating synergy, leading to an improvement in the financial outcomes (r = 0.690, sig. = 0.000). This results confirmed the findings of other studies by Kimetto (2019), Wang (2018), and Ogada et al. (2016) that there is a positive correlation between operating synergy and performance of a firm in a merger deal. Thus, the research accepts hypothesis 1. On the other hand, the research hypothesized a significant association between an organization’s performance financially and financial synergy. However, the findings show that despite having a positive association for financial outcomes and financial synergy of KALRO, the relationship was insignificant in influencing the performance (R2 = 0.348; p = 0.218. This finding supports Wang (2018), who found insignificant improvement in financial synergy after mergers to improve performance. Further, the research revealed a significant mediating effect of government policy between the synergistic gains and performance of KALRO. Therefore, the research accepts hypothesis 2 and rejects the null hypothesis.

LIMITATIONS OF THIS RESEARCH

The absence of pre-merger financial statements hindered the researcher from exploring the pre-merger performance of the organization for comparison. Therefore, only post-merger performance data were analyzed to explore the after-merger performance trends. This affects the accuracy of the responses given by the participants. In addition, the sample size of 32 was relatively small compared to the size of the organization. The sparse distribution of KALRO institutes and lack of adequate resources hindered the researcher from using a larger sample size, thus, the information provided by the small sample may not be a representative of the entire organization.

REFERENCES

- Benassi, M., & Landoni, M. (2019). State-owned enterprises as knowledge-explorer agents. Industry and Innovation, 26(2), 218-241.

- Florio, M., Ferraris, M., & Vandone, D. (2018). Motives of mergers and acquisitions by state-owned enterprises: a taxonomy and international evidence. International Journal of Public Sector Management, 31(2), 142-166.

- Garzella, S., & Fiorentino, R. (2017). Synergy value and strategic management: Inside the black box of mergers and acquisitions.

- Government of the Republic of Kenya (GOK). Report of The Presidential Taskforce on Parastatal Reforms (October, 2013).

- Healy, P.M., Palepu, K.G. & Ruback, R.S. (2012). Does corporate performance improve after mergers? Journalof Financial Economics, 31(1992), 135–175.

- Ireri, E. N. (2016). Assessment of problems facing state-owned enterprises in Kenya. International Journal of Business, Humanities and Technology, 6(4), 40-45.

- Kalsie, A., & Nagpal, A. (2017). Identification of Financial Synergy: A Case Study of Merger of UltraTech Cement with Samruddhi Cement. International Journal of Management Research, 8(2), 42-60.

- Kimetto, M. (2019). Effect of Synergy through Mergers and Acquisitions on a Firm’s Financial Performance in Kenya: A Case of Sidian Bank (Doctoral dissertation, United States International University-Africa).

- Leepsa, N. M., & Mishra, C. S. (2016). Theory and Practice of Mergers and Acquisitions: Empirical Evidence from Indian Cases. IIMS Journal of Management Science, 7(2), 179-194

- Mutegi, M. F., & Ombui, K (2016). An Investigation of the Factors That Cause Poor Performance of State Corporations in Kenya.

- Mwasaa, N. (2018). The Effect of Strategic Mergers on Operational Cost Reduction and Performance of Parastatals in Kenya. A Comparative Analysis Across Directorates of Agricultural and Food Authority. International Journal of Social Sciences and Information Technology. ISSN 2412-0294. Vol IV, Issue II.

- Ogada, A., Achoki, G., & Njuguna, A. (2016). Effect of synergy on the financial performance of merged institutions. American Journal of Finance, 1(2), 126-144.

- Ombaka, C., & Jagongo, A. (2018). Mergers and acquisitions on financial performance among selected commercial banks, Kenya. International Academic Journal of Economics and Finance, 3(1), 1-23.

- Oroh, A. N. H. (2016). Does synergy mentality mediate between strategic planning relationship and a firm’s performance? An empirical study of manufacturing companies in Indonesia. Pertanika Journal of Social Sciences and Humanities, 24, 125-138.

- Osege E. N. (2018). Change Management and Organizational Performance of Kenya Agricultural and Livestock Research Organization.

- Sirower, M. L. (2010). The Synergy Trap. Simon and Schuster.

- Wang M. (2018). Analysis on the Synergistic Effect of M&A from the Perspective of Finance-A Case Study of China Zhonghua Geotechnical Engineering Co.,Ltd. Advances in Social Science, Education and Humanities Research (ASSEHR), volume 184.

- Zhou, B., Guo, J., Hua, J., & Doukas, A. J. (2015). Does state ownership drive M&A performance? Evidence from China. European Financial Management, 21(1), 79-105.