Effect of Big Data on Accounting Information Quality in Selected Firms in Nigeria

- Falana, Gbenga Ayodele

- Igbekoyi, Olusola Esther (PhD)

- Dagunduro, Muyiwa Emmanuel

- 789-806

- Apr 14, 2023

- Accounting & Finance

Effect of Big Data on Accounting Information Quality in Selected Firms in Nigeria

Falana, Gbenga Ayodele1, Igbekoyi, Olusola Esther (PhD)2, Dagunduro, Muyiwa Emmanuel3

1,3Department of Accounting

Afe Babalola University Ado-Ekiti, Ekiti State, Nigeria

2Department of Accounting

Adekunle Ajasin University, Akungba-Akoko, Ondo State, Nigeria

Received: 10 March 2023; Accepted: 20 March 2023; Published: 14 April 2023

ABSTRACT

Nigerian Firms have mostly been facing the challenge of disseminating accounting information that would be readily available to users at the expected time. This situation has posed challenges to the quality of accounting information. This study, therefore, investigated the effect of big data on accounting information quality in selected firms in Nigeria. The study specifically focused on data volume, data variety, and data velocity as it affects the timeliness of accounting information. The study adopted a survey research design. The population of the study comprised 157 firms listed on the Nigeria exchange group as of 31st December 2021. A sample size of 20 firms was selected using the purposive sampling method. The study used 100 respondents which represented 5 respondents from each firm. Data were collected from primary sources using a well-structured questionnaire. Data collected were analysed using descriptive statistics and regression analysis. The results revealed that data volume, data variety, and data velocity have a positive significant effect on the timeliness of accounting information. The study concluded that the attribute of data used by firms significantly affects the timeliness of accounting information disseminated. The study recommended that firms should prioritize the management of big data to improve their accounting information.

Keywords: Big data, Data velocity, Data variety, Data volume, Quality of Accounting Information, Timeliness.

JEL Classification: L86, M41

INTRODUCTION

Globally, the demand for quality accounting information by stakeholders has led to the development of essential attributes that are useful in accounting. To meet this demand, accountants must adhere to the standard of relevance and timeliness in financial reporting (Chartered Finance Analyst [CFA], 2022). While relevance is the most fundamental, timeliness further enhances its importance (Ahmet, 2019). Based on this, regulatory agencies such as the Securities and Exchange Commission (SEC) of the United States of America (USA) and the New York Stock Exchange (NYSE), emphasize the need for the timely release of corporate financial reports (Efobi & Okougbo, 2014). In Nigeria, a total of 44 firms quoted on the Nigerian Exchange Group may face sanctions for failing the timeline in a rendition of 2020 audited financial results (Nnorom, 2021). While current academic studies (e.g., Mailafia & Adamu, 2021; Ohaka & Akani, 2017) have focused on other areas that might impact accounting information quality, little research has been done on the role of big data in improving the quality of accounting information, especially timeliness in financial reporting. This study attempts to bridge this gap in the literature. Accounting information quality is directly related to accounting data and methods (Kanakriyah, 2016). One peculiar feature of accounting data is that it is structured. This makes it rigid and less accessible, while difficult to use for estimations such as depreciation, risk assessment, and budgeting (Ibrahim et al., 2021). This above peculiarity has been its limitations. However, real-time access to data through the use of big data might improve the quality of accounting information. Ibrahim et al. (2021) opined that big data is much more than accounting and financial data. It includes all digital data which become available in massive amounts, in different formats, and in real-time (Bag et al., 2020). Data has value and it is intrinsic, so more data has more value (Eaker, 2021). These values lie in the information generated and the insight gained from its analysis. Therefore, this study’s broad objective is to examine the effect of big data on the quality of accounting information. The quality of accounting information can be measured by assessing how relevant and timely it is to stakeholders in making decisions. Putri (2018) opines timeliness is the period between presenting the desired information and the frequency of information reporting. Reschiwati (2020), Putri (2018), and Srimindarti (2008) argue that financial statements should be presented at a time intervals to explain changes in firms that will affect users in making decisions. However, the use of big data can enhance the timely rendition of accounting information. Big data is characterised by velocity, volume, and variety. Ghasemaghaei (2021) explains volume as the size of the data, which is increasingly growing; velocity as the speed of processing data; and variety as the types of data, which range from unstructured to structured data. Cockcroft and Russell (2018) opine that big data can improve data quality by increasing accuracy, completeness, and real-time availability. Consequently, the second objective of this study is to investigate the effect of big data’s characteristics on timeliness, which may eventually, impact the quality of accounting information. Accordingly, this study uses a sample of Nigerian firms to assess the effect of big data on the quality of accounting information. The study examines the effect of data size on the timeliness of accounting information. Meiryani et al. (2020) state that big data when used in the accounting process, provides ease and speed of access to transaction data flow and reduces physical document storage costs. Qiongge (2020) opines that big data improves availability and reliability, and overcomes the adverse effect of subjective judgment to a certain extent. Herath and Woods (2021) suggested real-time access to accounting data can create error-free reports as well as save time and money. This study examines the effect of data types on the timeliness of accounting information. This study provides valuable insight to policymakers, regulators, and researchers in recognizing the effect of big data on accounting information quality, and understanding whether its basic features could be an antecedent of the quality of accounting information. The study is broken down into sections. The following section is a discussion of theories and concepts related to big data and accounting information. This section also contains a review of relevant literature to explain various works that have been done on big data and areas that this study addresses. The third section discusses the data collection, analysis, and methods used in the study. The fourth section also discusses the recommendations, findings, conclusions, and limitations of the study.

LITERATURE REVIEW

Conceptual Review

Big Data

Benbrahim et al. (2020) refer to big data as non-traditional technologies that make available large datasets. Gartner (2016) opines big data as big, various, and fast-flowing information that requires economically feasible and innovative processing methods with the aim of developing decision-making methods and automation of processes. Zaki et al. (2020) defined big data as data that occurs in real time. Awotomilusi et al. (2022) suggest big data as datasets that are large, diverse, and rapidly changing, making it challenging to manage them with conventional tools. Based on this, big data is a form of digital data that contains different varieties, arriving in large volumes and with more velocity. Younis (2020) stated that the increase in the amount of data is not new, but its rate of growth is unprecedented, and that data analytics is not new, as accountants frequently employ analytical techniques like ratio and time series analysis. Big data does not only refer to large volumes of data since businesses like banks have been using big data in the past (Jia, 2020). The relative difference between big data and data used by an accountant lies in volume, velocity, and variety. Warren et al. (2015) suggested big data can be used in financial accounting where new data types can be integrated with accounting data into the accounting systems. Qiongge (2020) stated that big data is not only reflected in large numbers, but the value contained in the data is large, which has high value for the development of enterprises. These large numbers, high value, lot of variety, and data arriving timely with high velocity present new concepts for accounting information which is the focus of this study. Lancey (2001) opined that volume, velocity, and variety are the basic dimensions of big data management, while Shafer (2018) has expanded these dimensions by 42 new qualities.

Accounting Information Quality

Callen et al. (2013) stated that accounting information quality is the precision with which financial reporting informs investors about future cash flows. Here, the quality of accounting information is based on accurate prediction of future cashflows for investors to make decisions. The emphasis is on the reliability or accuracy of accounting information when used for prediction. Hribar et al. (2014) explained accounting information quality as the extent to which accounting information accurately reflects the company’s operating performance, is useful in predicting future performance, and assesses firm value. The central concept of accounting information is that some are better than others at communicating what it purports to communicate (Pounder, 2013; Achim & Chis, 2014; El-Hewety, 2019; CFA, 2021). These variations in the definition of accounting information quality, according to Pounder (2013), serve the same purpose: to enable people to evaluate the value of accounting information (CFA, 2022). A value judgment is the assessment of the course of action about other standards or priorities. In this regard, accounting information quality is the feature that makes up relevant and useful accounting information. Good accounting information is characterized by reliability, relevance, timeliness, and comparability to be useful for decision-making (Ehijiele, 2019). However, this study uses timeliness to measure the quality of accounting information. Timeliness points to the need for a timely rendition of accounting reports as required by law (Odesanya et al., 2020). Accounting information must be produced as and when due, as old information will not benefit users in making decisions (Ladewi et al., 2017; Qatawneh & Bader, 2020). All accounting information must be reported on time to ensure that it is of a high standard (Appelbaum et al., 2017). Timeliness means having information available to decision-makers before it loses its capacity to influence decisions (Obaidat, 2007; Putri, 2018). Information lacks relevance and becomes useless if it is either not available as and when required or becomes available later than expected. Timeliness alone cannot make information relevant, but a lack of timeliness reduces the relevance it might otherwise have had (FASB, 2001). In this study, timeliness is the expected time for the availability and accessibility of accounting information to various users. The achievement of timeliness can be enhanced through the use of big data. Mehdi (2022) stated that the computerization of accounting systems has a significant impact on the quality of accounting information. Information loses value if delayed because speedy provision with a degree of accuracy is better than a high degree of accuracy with delay (Qatawneh & Bader, 2020).

Data Volume and Quality of Accounting information

The volume refers to the amount of data that is produced by big data technologies and the rate at which it is growing, which is enormous (Nasrizar, 2014; Hareth & Woods, 2021). McNeely (2015) opined that the world contains an unimaginable amount of digital information which is getting bigger and the effect is felt everywhere. In this regard, data volume refers to the size and growth rate of data. The volume of data forms the major part of big data (Patgiri & Ahmed, 2016). Every human created about 1.7 megabytes of data per second in 2020 and more than 3.7 billion humans are using the internet (Carter, 2022). The amount of data available for analysis is growing at an exponential rate. Ogi (2020) stated that there were 79 zettabytes of data generated worldwide in 2021, and this number is expected to double by 2025. Firms have begun to collect and analyse large data to enhance their knowledge and make better decisions (Ghasemaghaei & Calic, 2019; Larson & Chang, 2016). The increasing use of digital devices has led to an unprecedented rate of data generation, which motivates firms to process data in a real-time and provide evidence-based decisions (Gandomi & Haider, 2015). For the accountant, there is a huge amount of data available to work with (Crookes & Conway, 2018). Owais and Hussein (2016) categorized volume as processing data while Ahmad et al. (2020) linked the data processing stage to the completeness of accounting information. Ghasemaghaei (2021) showed that data volume does not improve data veracity and value. The volume of data presents data sources for accounting measurement and budgeting.

Data Variety and Quality of Accounting information

Dimmick (2017) refers to data variety as collecting data from multiple sources to understand a problem and make smarter, more informed decisions. Brown (2022) states that big data is the diversity of sources, types, and formats of information. Based on this, data variety refers to the complexity, diversity, and heterogeneity like data. Big data comes in different forms, natures, or types. It includes structured (e.g., numbers) and semi-structured (e.g., log data, XML data), and unstructured data (e.g., videos, pictures, and customer reviews) (Lam et al., 2017; Bazzaz et al., 2021). The variety of data increases as more data is gathered from various sources (Marr, 2016). Diverse data is created not only internally but also from external sources (Grover et al., 2018). Variety in big data is considered a fundamental aspect and refers to variety as the diversity of data in data collection (Spacey 2017). Unlike in the past, when structured data could only be gathered, data is now available in different formats, including emails, PDFs, photographs, videos, audio and social, media posts (Rai, 2020). Though accountants are used to structured data, unstructured data abounds. Technological advancements give firms access to data beyond the firms’ business transactions (Yaqoob et al., 2016). Lukoianova and Rubin (2014) suggest that collecting and integrating data from various sources reduces the bias and errors that stem from analysing limited amounts of data. Ghasemaghaei and Calic (2019) argue that firms that constantly collect data from various sources may improve the quality and certainty of data by reducing bias and errors stemming from a limited amount of data. Firms that are capable of processing different formats of data can generate profound and valuable insights (Erevelles et al., 2016; Ghasemaghaei, Ebrahimi et al., 2017). Wang et al. (2016) argue that processing different types of data reduces uncertainty for firms in making decisions.

Data Velocity and Quality of Accounting information

The proliferation of digital devices has enhanced the rate of data generation, leading to a growing need for analysing data in real time (Ghasemaghaei & Calic, 2019; Gandomi & Haider, 2015). Brown (2021) refers to big data as the speed at which data is generated and processed by organisations to keep pace. This study refers to data velocity as the rate at which data is received and acted on in real time. Big data is being generated more rapidly than data from traditional methods, so it flows heavily because of active interaction with the topics of individuals, clients, and beneficiaries (Younis, 2020). Almost immediately, data becomes available. This affects all areas of the company, including accounting. The timeliness of presentation and preparation of accounting information can be enhanced if data is available in real-time. While prompt usage of data enables real-time processing to solve issues continuously (Manyika & Roxburgh, 2011; Saboo et al., 2016), its effect on the timeliness of accounting information abounds. The higher the velocity rate, the faster the data can be acquired and processed, and the more valuable and long-lasting the data collected will be in terms of value (Indicative Inc., 2022). Velocity forms part of the processing stage (Owais & Hussein, 2016), and it has a profound positive effect on the timeliness of accounting information (Ahmad et al., 2020). Therefore, the impact of velocity can be assessed directly on the timeliness of accounting information.

Theoretical Review

This study is anchored on decision-usefulness theory as propounded by George Staubus in 1961. It assumes that users of accounting information are rational and the main objective of financial reporting is to provide useful information in making investment decisions. However, to make proper decisions, the information being provided needs to be relevant (Kareem et al., 2017) and the vital ingredient of this is timeliness. The quality of accounting information in terms of timeliness enhances its usefulness. Davern et al. (2018) showed that financial reports remain consistently relevant over time and that investors view non-GAAP and other non-financial information as complements, rather than substitutes, to financial reports. In the conceptual framework, the IASB and the FASB identify decision usefulness as the main objective of financial reporting. Jonas and Young (1998) suggested that decision usefulness should be the criterion to measure the quality of accounting standards. Decision-usefulness means that accounting information must have characteristics that can potentially affect the decisions of the user. Beest et al. (2009) said if financial statements are to be produced, higher quality financial information should have fundamental characteristics underlying decision usefulness. Jabbar (2017) opined that qualitative attribute was needed to produce higher-quality financial information. The awareness of this broadens accounting data sources, enabling the use of big data in accounting processes. However, this theory has been criticized based on variations in the needs of users, which affect the prominence of individual qualities.

Empirical Review

Researchers have been conducting studies to explore the effect of big data on accounting and various ways accountants can leverage such technology. Awotomilusi et al. (2022) assessed the adoption of cloud computing on the efficacy of accounting practices in Nigeria. To achieve this, the study distributed a well-structured questionnaire among deposit money banks in Nigeria. The data were analyzed using frequency and ordinary least square regression. From the findings, the study discovered that cloud computing exhibited a significant positive relationship with the efficacy of accounting practices in Nigeria. In addition, other variables employed in the model also revealed that technological advancement and security efficiency depicted a significant relationship with the efficacy of accounting practices in Nigeria. Cost-effectiveness revealed a significant negative relationship. Awad et al. (2021) examined the convergence of big data and accounting. In their exploratory research, they described areas where big data could overcome data limitations of accounting issues. The study found that big data and data analytics should be incorporated into the accounting profession because of their potential effect on numerous areas of accounting. Bose et al. (2022) assessed big data, data analytics, and artificial intelligence in accounting. The study found that accounting professionals could only leverage big data, data analytics, and artificial intelligence to stay ahead of the competition in a rapidly changing business environment. Herath and Wood (2021) investigated the impact of big data and data analytics on accounting. The study adopted a literature review methodology to examine the effect of big data on accounting. The study found that big data could improve risk analysis, improve the quality of accounting information, and provide real-time information to assist in decision-making. Also, Cockcroft and Russell (2018) studied big data opportunities for accounting and finance practice. The research addressed the major themes in existing research on big data and the resulting gaps in the accounting and finance literature. The study pointed out six areas of big data that received little attention from researchers. This included risk and security, data visualization, and predictive analytics, data management, and data quality. Again, Ramasamy and Chowdhury (2020) investigated big data quality dimensions. The study focused on a review of the literature. The study found that the fundamental quality of big data included accuracy, completeness, consistency, uniqueness, and timeliness. The study also found new dimensions that are relevant to big data such as trust, credibility, and, confidentiality, and that data quality is dependent on data types, data sources, and applications. Wamba et al. (2019) researched turning information quality into firm performance in the big data economy linking business value, user satisfaction, and firm performance. Data were collected from 302 respondents across various organisations in France and the USA. The study found that information quality contained completeness, currency, accuracy, and information quality have a significant positive impact on firm performance. Idil and Destan (2018) investigated the impact of big data analytics on financial reporting and accounting within the institutional framework. The study based on in-depth interviews of accountants analysed the potential uses and effects of big data analytics in financial reporting and accounting. The study found that traditional accounting practices were changing, but accounting and financial reporting’s nature remained the same. Younis (2020) evaluated the effect of big data on the future of the accounting profession. In their exploratory survey, in-depth interviews were done. The study found that big data would have an impact on the roles of accountants and the accounting profession in the future. The study also stated that big data analysis would improve the quality of accounting information. Meiryani et al. (2020) investigated the impact of big data on accounting information systems in Indonesia. The study reviewed the literature and found that big data is useful in providing ease and speed of access to transaction data flow; can increase the effectiveness and efficiency of physical document storage costs and changes in forensic audit and accounting techniques. Using bibliometric analysis, Varma et al. (2021) analysed the current state of knowledge on big data in the accounting domain. Through visual analysis, the study highlighted that big data was an innovation to be managed in the accounting domain to stimulate firms’ competitive advantages and an accounting tool that required new skills and capabilities for its value to be fully realised. Younis (2020) researched the impact of big data analytics on financial reporting quality. The study surveyed experts’ opinions in Saudi Arabia. The study found that big data analytics would improve organisation competitiveness and accounting information quality and provide stakeholders with relevant information for decision-making. Ahmad et al. (2020) investigated the impact of big data on accounting information systems and accounting information quality. This study developed links between data collection stage to the reliability, data processing stage to the completeness, data storage to the timeliness, information generation stage to understandability and accessibility quality of accounting information. Wongsim et al. (2021) investigated factors influencing the adoption of big data analytics in accounting. The study used two organisations as a case study and obtained data from 156 respondents using questionnaires. The study found that five factors (information technology strategists, top management commitment, skills development, technology capability; and competitive environments) ensured the use of big data. A review of the above literature provides insufficient empirical evidence and information on how big data affects accounting. However, big data is a new technology and the risks of data ownership, agility, and privacy invasion are still under-investigated. There is a need for further applied research on big data to understand its impact on sustainability of accounting profession. An immense amount of data is required to make accurate decisions and only a few organisations have the datasets necessary. Different studies (e.g., Awad et al., 2021; Younis, 2020; Meiryani et al., 2020 etc) examined the effect of big data on accounting as a whole while specific areas affected received little attention. Based on the foregoing, the following hypotheses generated are stated below:

Ho1: high volume of data does not have a significant effect on the timeliness of accounting information of selected firms in Nigeria.

Ho2: high variety of data does not have a significant effect on the timeliness of accounting information of selected firms in Nigeria.

Ho3: high velocity of data does not have a significant effect on the timeliness of accounting information of selected firms in Nigeria.

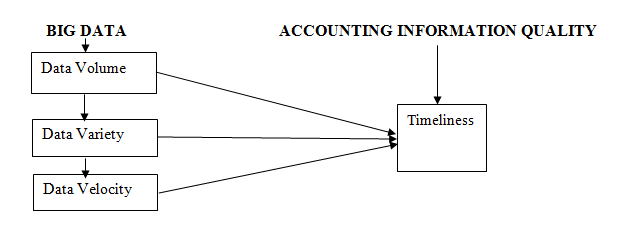

Conceptual Framework

The diagram below portrays the relationship that can be explored between big data and the quality of accounting information. Big data can be broken down into different dimensions. The study examines the effect of three dimensions on the quality of accounting information. The volume, velocity, and variety of data can impact the quality of accounting information. While various dimensions of big data can contribute to each quality of accounting information in different ways, the extent of such contributions is the aim of this study.

Source: Author’s Concept (2022).

DATA AND METHODS

This study adopted a survey research design. The population for this study covered all the listed firms (157 in total) on the Nigerian Exchange Ltd as of December, 2021(Nigeria Exchange Group [NGX Group], 2022). Adopting purposive sampling method, 20 firms that used big data in their operations were selected. Five respondents representing each firm were selected due to the relative size of the population. Respondents selected were accountants with knowledge about utilizing big data within their firms. Data were collected through a well-structured questionnaire. The study used descriptive statistics and regression analysis to analyse the data collected from respondents.

Reliability Test

Table 1 revealed the reliability test on big data and the quality of accounting information among selected firms in Nigeria using Cronbach Alpha. Seven (7) questions on the quality of accounting information were asked and the Cronbach Alpha is 0.707. For data volume, the Cronbach Alpha is 0.831 with a total of 12 items. Data variety of 11 items revealed a Cronbach Alpha of 0.704 while data velocity on items of 10 revealed a Cronbach Alpha of 0.772. Based on this, all the variables tested were reliable.

Table 1 Cronbach Alpha Test Results

| S/N | Variable | No. of Items | Cronbach’s Alpha |

| 1 | Quality of Accounting Information (QAI) | 7 | 0.707 |

| 2 | Data Volume (DVM) | 12 | 0.831 |

| 3 | Data Variety (DVY) | 11 | 0.704 |

| 4 | Data Velocity (DVCT) | 10 | 0.772 |

Source: Author’s Computation (2022)

Model Specification

The model for this study was developed in line with the study conducted by Ghasemaghaei (2021) on understanding the impact of big data on firm performance: the necessity of conceptually differentiating among big data characteristics. Ghasemaghaei (2021) used a resource-based view to analyse the effect of big data characteristics on firm performance and the mediating roles of data value and data veracity. This study digressed from the study based on the removal of some variables such as data value, data veracity, financial performance and inclusion of quality of accounting information and timeliness respectively. Hence, the model of the study is stated as follows:

QAI = f (DVM, DVY, DVCT) …………………………………….Eqn (3.1)

From equation 3.1, the model can be stated in econometric form as follows:

QAI = β0 + β1DVM+ β2DVY+ β3DVCT + µ …………………. Eqn (3.2)

Where: QAI = Quality of Accounting Information,

DVM = Data Volume, DVY = Data Variety, DVCT = Data Velocity

β0 = Parameter to be estimated

β1, β2, β3 = Unknow coefficient of the independent variables

µ = Error Term

It is expected that β1, β2, and β3 will be greater than zero based on the literature reviewed and the theory used in the study.

DATA ANALYSIS AND DISCUSSION OF FINDINGS

Descriptive Statistics

Reported in Table 2 are the descriptive statistics for the analysis of big data and the quality of accounting information of selected firms in Nigeria. The result revealed that the mean value of quality of accounting information is 4.8500. This implies that accounting information quality among Nigerian firms brings about positive value which is quite high when compared to the scale of five employed. The standard deviation of 0.50000 is far from its mean and this implies a high variability rate to its average. Data for the variable is negatively skewed and can be described as a long-left tail since the value stood at -5.238. The kurtosis value of 35.627 is higher than the benchmark of 3; hence, known as leptokurtic. More so, the average value of data volume is 3.9900 while its standard deviation stood at 0.33318. The result of the standard deviation showed a low variability from its average value. The Skewness of -6.875 can be described as having a long-left tail due to its negative sign while its Kurtosis value of 68.326 is greater than 3, thus referred to as leptokurtic distribution. From table 2 also, data variety has an average value of 4.5700 with a standard deviation of 1.08484, indicating there is high variability. The minimum value is 1 and the maximum is 5. It has a long-left tail since it is negatively skewed with -2.654 and a kurtosis value of 5.933 is described as leptokurtic because the value exceeded 3. Lastly, data velocity has an average value of 4.6900. This is quite high when compared with the highest scale of measurement which is 5. The standard deviation stood at 0.58075. This implied a higher variability from its mean. Data velocity is negatively skewed and can be described as a long-left tail since the value stood at -2.998. The kurtosis value of 15.039 is higher than the prescribed benchmark of 3. This can therefore be referred to as leptokurtic because the Kurtosis value exceeded 3.

Table 2 Descriptive Statistics

| Variables | QAI | DVM | DVY | DVCT |

| Obs | 100 | 100 | 100 | 100 |

| Mean | 4.8500 | 3.9900 | 4.5700 | 4.6900 |

| Std. Deviation | 0.50000 | 0.33318 | 1.08484 | 0.58075 |

| Minimum | 1.00 | 1.00 | 1.00 | 1.00 |

| Maximum | 5 | 5 | 5 | 5 |

| Skewness | -5.238 | -6.875 | -2.654 | -2.998 |

| Kurtosis | 35.627 | 68.326 | 5.933 | 15.039 |

Source: Author’s Compilation (2022)

Test of Variables

Multicollinearity Test

To ascertain the regression outcome, a multicollinearity test needs to be carried out. For this purpose, the study employed the Tolerance value and Variance Inflation Factor (VIF). The tolerance value for data volume, data variety and data velocity are 0.627, 0.868 and 0.570 respectively. All three variables have tolerance values above 0.10 showing the absence of multicollinearity among the variables. Also, the Variance Inflation Factor (VIF) for data volume is 1.594, data variety is 1.152 and data velocity is 1.754. The Variance Inflation Factor (VIF) for the three variables were all less than 10. Conclusively, there is no multicollinearity in the model.

Table 3: Multicollinearity Test

| Tolerance | VIF | 1/VIF |

| .627 | 1.594 | 0.627 |

| .868 | 1.152 | 0.868 |

| .570 | 1.754 | 0.570 |

| Mean VIF | 1.50 |

Sources: Author’s Computation (2022)

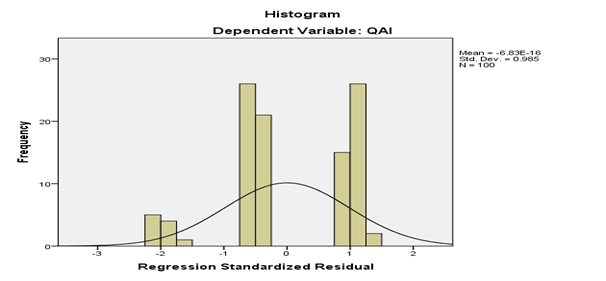

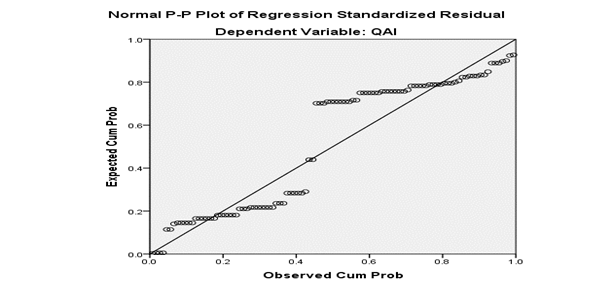

Normality Test

The study employed a histogram coupled with a P-P Plot for the normality distribution of the variables. The outcome in Figure 1 showed that data employed in the study are normally distributed. This can be ascertained from the response of the respondents in figure 1 which lies within the bean-shape of the histogram. The P-P Plot in Figure 2 also revealed that all the small shapes do not deviate too far from the regression standardized residual line.

Figure 1 Histogram with Normal Curve

Source: Author’s Computation (2022)

Figure 2 P-P Plot of Regression Standardized Residual

Source: Author’s Computation, (2022)

Table 4 Post-Estimation Test Results

| Tolerance and VIF Value | ||

| Null Hypothesis | VIF | 1/VIF |

| There is no multicollinearity among the variables (1/VIF >0.10) | 1.50 | |

| Test for the Overall Significance of the Whole Model (F-Statistics) | ||

| Null Hypothesis | Statistics | Probability |

| There is no overall significance in the research model (P<0.05) | 99.747 | 0.000 |

Source: Author’s Computation (2022)

Correlation Matrix

Table 5 revealed the correlation matrix employed in the examination of big data and the quality of accounting information. The result showed that data volume (DVM) is positive and significant, with a coefficient of 0.719. This revealed that an increase in data volume will lead to a rise in the quality of accounting information of firms in Nigeria. More so, data variety is significant and positive with a value of 0.550 implying that as data variety increases by a unit will lead to a 0.550 unit increase in the quality of accounting information among Nigerian firms. Conversely, the data velocity (DVCT) is positive, with a coefficient of 0.743, which indicates that as data velocity increases, the quality of accounting information will also increase. In the same vein, the coefficient of other explanatory variables in the model is positive. For instance, data volume exhibited a significant positive relationship with data variety with a value of 0.212 and its probability stood at 0.035 which is significant at 5% level. Also, data volume and data velocity exhibited a significant positive relationship of 0.610 while data variety and data velocity indicated a significant positive effect. The result of all these explanatory variables indicated the absence of multicollinearity as the recorded values of the explanatory variables were not above the threshold of 0.7.

Table 5 Correlation Analysis of Study Variables

| QAI | DVM | DVY | DVCT | |

| QAI | 1.0000 | |||

| DVM | 0.719** | 1.0000 | ||

| 0.000 | ||||

| DVY | 0.550** | 0.212* | 1.0000 | |

| 0.000 | -0.035 | |||

| DVCT | 0.743** | 0.610** | 0.363** | 1.0000 |

| 0.000 | 0.000 | 0.000 |

Source: Author’s Computation, (2022)

Big data and quality of accounting information in selected firms in Nigeria

The regression model summary in Table 6 explained the joint effect of big data and the quality of accounting information among Nigerian firms. The table revealed the coefficient of determination R Square (R2) and the adjusted value (R2) is 0.757 and 0.750 respectively. The result showed that about 75% variation in the independent variables (data volume, data variety and data velocity) jointly explained the dependent variable (quality of accounting information in Nigerian firms). The remaining 25% represents the error term. In the same manner, Table 7 explains the analysis of variation where the statistical significance of the whole model is revealed. The table revealed the extent to which the independent variables jointly explained the dependent variable. This is provided by the value of the F-statistics given as 99.747. This value is significant at a 1% level thus revealing that the model jointly put together is significant. It also implied that all the explanatory variables significantly predict the power of the dependent variable as the F-statistics stood at 99.747. Table 8 revealed the individual analysis of the variables. It explained the statistical significance of each parameter in the model given by the T-statistics, the beta coefficient, and their probabilities (p-value). Data volume (DVM) has a significant positive coefficient on the quality of accounting information with a value of 0.642; t-statistics of 6.741, and a p-value of 0.000. It implied that as data volume increases by a unit, there will be a 0.642 unit increase in the quality of accounting information among Nigerian firms. Similarly, data variety (DVY) has a positive and significant coefficient of 0.151; t-statistics 6.076, and a p-value of 0.000 with quality of accounting information. The result implied that a unit increase in data variety will lead to a 0.151 unit increase in the quality of accounting information among Nigerian firms. Data velocity (DVCT) has a significant positive coefficient on the quality of accounting information with a value of 0.312; t-statistics 5.437, and, a p-value of 0.000. The result showed that a unit increase in data velocity will lead to a 0.312 unit increase in the quality of accounting information among Nigerian firms. Many policy implications can be deduced from the empirical analysis and statistical results of this study. For instance, data volume revealed a significant positive relationship with the quality of accounting information among Nigerian firms. This positive relationship supports the a priori expectation stated in this study and the findings of Carter (2022), Hareth and Woods (2021), Bose et al. (2022), Ghasemaghaei and Calic (2020), Qiongge (2020), Ogi (2020), Idil and Destan (2018) among others. The positive relationship implied that as firms began to collect and analyse large data, the quality of accounting information improves. However, this positive relationship negates the findings of Ahmad et al. (2020) and Elgendy and Elragal (2014). Likewise, data variety has a significant positive relationship with the quality of accounting information among Nigerian firms. This agrees with a priori expectation and the findings of Ahmad et al. (2020), Wang et al. (2016), Ghasemaghaei and Calic (2019), Larson and Chang (2016), Patgiri and Ahmed (2016), Marr (2016) and Nasrizar (2014) who argued that firms that constantly collect data from various sources may be able to improve their quality and certainty of data by reducing bias and errors stemming from a limited amount of data. According to Rai (2020) also, the availability of data in a variety of formats improves the quality of accounting information. However, Tiron-Tudor and Deliu (2021) disagree with this, as their study hinged on the cost implication of using different means of data. Lastly, the relationship between data velocity and the quality of accounting information among Nigerian firms is significant and positive. This result concurred with a priori expectation and the work of Bose et al. (2022), Herath and Wood (2021), Rai (2020), Qiongge (2020), Dimmick (2017), Lukoianova and Rubin (2014), Ahmad et al., (2020), Ghasemaghaei and Calic (2019) among others that advocated that data velocity improves data veracity generation. Therefore, the impact of velocity can be gauged directly on the timeliness of accounting information. This contradicts the findings made in the work of Tiron-Tudor and Deliu (2021), and Elgendy and Elragal (2014) among others.

Table 6 Regression Model Summary

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | |||||||

| 1 | .870a | .757 | .750 | .25024 | |||||||

a. Predictors: (Constant), DVM, DVY, DVCT

b. Dependent Variable: QAI

Table 7 Analysis of Variance

| Model | Sum of Squares | Df | Mean Square | F | Sig. | |||||||

| 1 | Regression | 18.738 | 3 | 6.246 | 99.747 | .000b | ||||||

| Residual | 6.012 | 96 | .063 | |||||||||

| Total | 24.750 | 99 | ||||||||||

a. Dependent Variable: QAI

b. Predictors: (Constant), DVM, DVY, DVCT

Source: Author’s Field Survey, (2022)

Table 8 Coefficient of Variation

| Unstandardized Coefficients | Standardized Coefficients | |||||

| Model | B | Std. Error | Beta | t | Sig. | |

| 1 | (Constant) | .133 | .306 | .436 | .664 | |

| DVM | .642 | .095 | .428 | 6.741 | .000 | |

| DVY | .151 | .025 | .328 | 6.076 | .000 | |

| DVCT | .312 | .057 | .362 | 5.437 | .000 | |

a. Dependent Variable: QAI

b. Predictors: (Constant), DVM, DVY, DVCT

Source: Author’s Field Survey, (2022)

DISCUSSION OF FINDINGS

The regression analysis revealed that data volume, data variety and data velocity showed a significant positive relationship with the quality of accounting information in Nigerian firms. This outcome is also supported by the correlation test as all the variables are positively correlated with the dependent variable. The result connotes that big data assists in improving the quality of accounting information of Nigerian firms. The outcome derived from this study as explained by Qiongge (2020) is that big data is not only reflected in large numbers, but more importantly, the value contained in the data is very large, which has high value for the development of enterprises. These large numbers, high value, lot of variety and data arriving timely with high velocity present new features and concepts for improving accounting information quality among Nigerian firms.

CONCLUSION AND RECOMMENDATIONS

In an attempt to investigate big data and the quality of accounting information among selected firms in Nigeria, the study employed ordinary least square method coupled with correlation analysis. From the findings, the study concluded that big data proxy by data volume, data variety and data velocity significantly influence the quality of accounting information in Nigerian firms. This implied that big data can be used in financial accounting and reporting to enhance the quality of accounting information. The study, therefore, highlighted the following recommendations for policy decision-making:

- Organisations should integrate unstructured data from different sources in real time into accounting systems to enhance accounting information quality.

- There should be adequate investment in big data, its management, personnel and technology to improve the quality of accounting information.

- Organisations should prioritize the right and reliable data type and volume while keeping pace with data velocity to improve the quality of accounting information.

REFERENCE

- Achim, A. M., & Chiş, A. O. (2014). Financial accounting quality and its defining characteristics. Sea: Practical Application of Science, 2(3).

- Ahmad, I., Ahmed, G., Shah, S. A. A., & Ahmed, E. (2020). A decade of big data literature: analysis of trends in light of bibliometrics. The Journal of Supercomputing, 76(5), 3555-3571.

- Awotomilusi, N., Dagunduro, M.E., & Osaloni, B.O. (2022). Adoption of cloud computing on the efficacy of accounting practices in Nigeria. International Journal of Economics, Business and Management Research, 6(12), 194-205.

- Bag, S., Wood, L. C., Xu, L., Dhamija, P., & Kayikci, Y. (2020). Big data analytics as an operational excellence approach to enhance sustainable supply chain performance. Resources, Conservation and Recycling, 153, 104559.

- Bazzaz Abkenar, S., Haghi Kashani, M., Mahdipour, E., & Jameii, S. M. (2021). Big data analytics meets social media: A systematic review of techniques, open issues, and future directions. Telematics and informatics, 57, 101517. https://doi.org/10.1016/j.tele.2020.101517

- Beest, F. V., Braam, G. J. M., & Boelens, S. (2009). Quality of financial reporting: measuring qualitative characteristics.

- Benbrahim, H., Hachimi, H., & Amine, A. (2020). Deep transfer learning with Apache spark to detect covid-19 in chest x-ray images. Romanian Journal of Information Science and Technology, 23(S, SI), S117-S129.

- Bose, S., Dey, S. K., & Bhattacharjee, S. (2022). Big Data, Data Analytics and Artificial Intelligence in Accounting: An Overview. Handbook of Big Data Methods, Forthcoming.

- Brown, Terry. (2022). https://itchronicles.com/big-data/who-is-using-big-data-in-business/

- Callen, J. L., Khan, M., & Lu, H. (2013). Accounting quality, stock price delay, and future stock returns. Contemporary Accounting Research, 30(1), 269-295.

- Carter, R. (2022). 21 Surprising big data statistics, trends & facts for 2022. https://findstack.com/big-data-statistics/

- Certified Finance Analysts, Accounting information quality. https://www.cfainstitute.org

- Cockcroft, S., & Russell, M. (2018). Big data opportunities for accounting and finance practice and research. Australian Accounting Review, 28(3), 323-333.

- Crookes, L., & Conway, E. (2018). Technology challenges in accounting and finance. Contemporary issues in accounting (pp. 61-83). Palgrave Macmillan, Cham.

- Davern, M., Gyles, N., Hanlon, D., & Pinnuck, M. (2018). Decision-usefulness in financial reports: Research Report No. 3: The effect of industry on the relevance of financial reports for investor decision making.

- Dimmick, M. (2017). How the variety in big data works as an Advantage – OpenGov Asia. https://opengovasia.com/how-the-variety-in-big-data-works-as-an-advantage/

- Eaker, C. (2021). The curation process adds value to primary research data and is key to its usability by against the grain comments. Against the Grain, 33(1).

- Efobi, U., & Okougbo, P. (2014). Timeliness of financial reporting in Nigeria. South African Journal of Accounting Research, 28(1), 65-77.

- Elgendy, N. and Elragal, A., (2014) Big data analytics: a literature review paper, Computer Science, Springer International Publishing pp. 214-227.

- El-Hewety, A. E. (2019). The impact of the accounting quality and information risk on the time of earning announcement. Journal of Environmental Studies and Researches, 9(2), 45-51.

- Erevelles, S., Fukawa, N., & Swayne, L. (2016). Big data consumer analytics and the transformation of marketing. Journal of business research, 69(2), 897-904.

- Gandomi, A., & Haider, M. (2015). Beyond the hype: big data concepts, methods, and analytics. International journal of information management, 35(2), 137-144.

- Gartner (2016). Survey analysis: big data investments begin tapering in 2016. Retrieved August 13, 2018, from https://www.gartner.com/doc/3446724/survey-analysis-bigdata-investments.

- Ghasemaghaei, M. (2021). Understanding the impact of big data on firm performance: The necessity of conceptually differentiating among big data characteristics. International Journal of Information Management, 57, 102055.

- Ghasemaghaei, M., & Calic, G. (2019). Can big data improve firm decision quality? The role of data quality and data diagnosticity. Decision Support Systems, 120, 38-49.

- Ghasemaghaei, M., Hassanein, K., & Turel, O. (2017). Increasing firm agility through the use of data analytics: The role of fit. Decision Support Systems, 101, 95-105.

- Grover, V., Chiang, R. H., Liang, T. P., & Zhang, D. (2018). Creating strategic business value from big data analytics: A research framework. Journal of management information systems, 35(2), 388-423.

- Herath, S. K., & Woods, D. (2021). Impacts of big data on accounting. E-Business & Administration Review, 12(2), 186-193.

- Hribar, P., Kravet, T., & Wilson, R. (2014). A new measure of accounting quality. Review of Accounting Studies, 19(1), 506-538.

- Ibrahim, A. E. A., Elamer, A. A., & Ezat, A. N. (2021). The convergence of big data and accounting: innovative research opportunities. Technological Forecasting and Social Change, 173, 121171.

- Jabbar, A. A. (2017). Decision usefulness approach to financial reporting: A case for employees. International Journal of Advanced Engineering, Management and Science, 3(5), 239841.

- Jia, Z. (2020) The impact of the arrival of the big data era on accounting work. In IOP Conference Series: Materials Science and Engineering 768(5, p. 052092). IOP Publishing.

- Jonas, G. J., & Young, S. J. (1998). Bridging the gap: who can bring a user focus to business reporting? Accounting Horizons, 12(2), 154.

- Kanakriyah, R. (2016). The effect of using accounting information systems on the quality of accounting information according to users’ perspective in Jordan. European Journal of Accounting, Auditing and Finance Research, 4(11), 58-75.

- Ladewi, Y., Susanto, A., Mulyani, S., & Suharman, H. (2017). Effect of organizational commitment on the quality of accounting information systems and their impact on the quality of accounting information. Journal of Engineering and Applied Sciences, 12(24), 7649-7655.

- Lam, S. K., Sleep, S., Hennig-Thurau, T., Sridhar, S., & Saboo, A. R. (2017). Leveraging frontline employees’ small data and firm-level big data in frontline management: An absorptive capacity perspective. Journal of Service Research, 20(1), 12-28.

- Laney, D. (2001). 3D data management: Controlling data volume, velocity and variety. META group research note, 6(70), 1.

- Larson, D., & Chang, V. (2016). A review and future direction of agile, business intelligence, analytics and data science. International Journal of Information Management, 36(5), 700-710.

- Mailafia, L., & Adamu, J. (2021). Board features and timely disclosure of audited accounts of listed deposit money banks in Nigeria. Journal of Accounting Research, Organization and Economics, 4(1), 1-13.

- Manyika, J., & Roxburgh, C. (2011). The great transformer: The impact of the internet on economic growth and prosperity. McKinsey Global Institute, 1(0360-8581).

- Marr, B. (2016). Big data in practice: how 45 successful companies used big data analytics to deliver extraordinary results. John Wiley & Sons.

- McNeely, C. L. (2015). Big data analytics and workforce issues: Prospects and challenges in the information society. Journal of the Washington Academy of Sciences, 101(3), 1-10.

- Meiryani, Y. L., Heykal, M., & Wahyuningtias, D. (2020). The usefulness of accounting information systems for businesses. Systematic Reviews in Pharmacy, 11(12), 2054-2058.

- Nasrizar, M. M. (2014) Big data and accounting measurements. Advances in Computer Science and Information Technology (ACSIT), Print ISSN: 2393-9907; Online ISSN: 2393-9915; 2(3); January-March 2015 pp. 295-305

- Nnorom, N. (2021). 44 companies to face NSE’s sanctions over default filing. Vanguard News. https://www.vanguardngr.com/2021/04/44-companies-to-face-nses-sanctions-over-default-filing/

- Obaidat, A. N. (2007). Accounting information qualitative characteristics gap: Evidence from Jordan. International Management Review, 3(2).

- Ogi, D., (2020). Big data statistics: how much data is in the world? https://firstsiteguide.com

- Ohaka, J., & Akani, F. N. (2017). Timeliness and relevance of financial reporting in Nigerian quoted firms. Management and Organizational Studies, 4(2), 55-62.

- Owais, S. S., & Hussein, N. S. (2016). Extract five categories CPIVW from the 9V’s characteristics of the big data. International Journal of Advanced Computer Science and Applications, 7(3).

- Patgiri, R., & Ahmed, A. (2016). Big data: The v’s of the game changer paradigm. IEEE 2nd international conference on data science and systems (pp. 17-24).

- Pounder, B. (2013). Measuring accounting quality: the SEC is developing a software model to measure the accounting quality of its registrants’ filings. Accounting professionals should be aware of the implications. Strategic Finance, 94(11), 18-21.

- Putri, D. A. (2018). Analysis of the factors that influence timeliness of financial statement submission in consumption industrial companies listed in Indonesia stock exchange (IDX). International Journal of Public Budgeting, Accounting and Finance, 1(4), 1-12.

- Qatawneh, A. M., & Bader, A. (2020). Quality of accounting information systems and their impact on improving the non-financial performance of Jordanian Islamic banks. Academy of Accounting and Financial Studies Journal, 24(6), 1-19.

- Qiongge, L., (2020). Research on the impact of big data era on accounting development. International Journal of Scientific Engineering and Science, 4(6), 44-47.

- Rai, A. (2020). What is big data – characteristics, types, benefits & examples 2019. https://www.upgrad.com/blog/what-is-big-data-types-characteristics-benefits-and-examples/

- Ramasamy, A., & Chowdhury, S. (2020). Big data quality dimensions: a systematic literature review. JISTEM-Journal of Information Systems and Technology Management, 17.

- Reschiwati, R. (2020). Canonical correlation analysis: Effect of earnings management on firm values and timeliness of financial reporting. International Research Association for Talent Development and Excellence.

- Rubin, V. & Lukoianova, T. (2013). Veracity roadmap: Is big data objective, truthful and credible? Advances in Classification Research Online, 24(1), 4.

- Saboo, A. R., Kumar, V., & Park, I. (2016). Using big data to model time-varying effects for marketing resource (re) allocation. MIS quarterly, 40(4), 911-940.

- Shafer, T. (2018). The 42 V’s of big data and data science. Retrieved June 4, 2018, from https://www.kdnuggets.com/2017/04/42-vs-big-data-data-science.html.

- Spacey, John. (2017). https://simplicable.com/new/data-variety.

- Srimindarti, C. (2008). Timeliness of financial reporting, 7(1), 24451.

- Tiron-Tudor, A., & Deliu, D. (2021). Big data’s disruptive effect on job profiles: management accountants’ case study. Journal of Risk and Financial Management, 14(8), 376.

- Varma, A., Piedepalumbo, P., & Mancini, D. (2021). Big data and accounting: A bibliometric study. International Journal of Digital Accounting Research, 21.

- Wamba, S. F., Akter, S., Trinchera, L., & De Bourmont, M. (2018). Turning information quality into firm performance in the big data economy. Management Decision.

- Wang, Y., Kung, L., Wang, W. Y. C., & Cegielski, C. G. (2017). An integrated big data analytics-enabled transformation model: Application to health care. Information & Management. Retrieved from http://www.sciencedirect.com/science/article/pii/S0378720617303129.

- Warren Jr, J. D., Moffitt, K. C., & Byrnes, P. (2015). How big data will change accounting. Accounting Horizons, 29(2), 397-407

- Wongsim, M., Nilniyom, N., Sompong, A., Kaiwinit, S., & Satchawatee, N. (2021). Factors influencing the adoption of big data analytics in accounting: A Study of Energy Companies.

- Yaqoob, I., Hashem, I. A. T., Gani, A., Mokhtar, S., Ahmed, E., Anuar, N. B., et al. (2016). Big data: From beginning to future. International Journal of Information Management, 36(6), 1231–1247.

- Younis, N. M. M. (2020). Big data and the future of the accounting profession. Indian Journal of Science and Technology, 13(08), 883-892. https://doi.org/10.17485/ijst/2020/ v013i08/149808

- Younis, N. M. M. (2020). The impact of big data analytics on improving financial reporting quality. International Journal of Economics, Business and Accounting Research (IJEBAR), 4(03).

- Zaki, N. D., Hashim, N. Y., Mohialden, Y. M., Mohammed, M. A., Sutikno, T., & Ali, A. H. (2020). A real-time big data sentiment analysis for Iraqi tweets using spark streaming. Bulletin of Electrical Engineering and Informatics, 9(4), 1411-1419.

Dear Respondent,

REQUEST FOR THE COMPLETION OF THE QUESTIONNAIRE

We are currently conducting research on big data and the quality of accounting information of selected firms in Nigeria. This study will help the government and business organisations focus more on how to integrate big data to better improve accounting information. I hope to have a few minutes of your time to fill out this questionnaire as all information provided will be treated as confidential and responses will be analyzed as a block.

SECTION A

Background information:

Kindly tick (ѵ) on that which agrees with your opinion.

1) Employee position/designation in your organisation: Manager ( ) Accountant ( ) Auditor ( ) others ( )

2) Employee years of working experience: Below 5 years ( ) Between 6-10 years ( ) Between 11-20 years ( ) above 21years

3) Employee years of proficiency in information technology/ICT: Below 5 years ( ) Between 6-10 years ( ) Between 11-20 years ( ) above 21years ( )

4) What is your organisation’s method of data storage? ……………………………………..

5) What is the volume of your organisation’s transactions in a day? Below 1 thousand ( ) Between 1-10 thousand ( ) Between 11-20 thousand ( ) above 21 thousand ( )

6) What is the range of your organisation’s customers? Below five thousand ( ) Between 6-10 thousand ( ) Between 11-20 thousand ( ) above 21 thousand ( )

7) What is the range of your organisation’s turnover? Below 500 million ( ) Between 501-700 million ( ) Between 701-999 million ( ) above 1 billion ( )

SECTION B

This section contains sets of questions or statements raised in respect of big data and the quality of accounting information in selected firms in Nigeria. Please indicate the extent to which you agree or disagree with the following under the listed statements.

Code: SA-Strongly Agree, A-agree, UD-Undecided, D-Disagree, SD-Strongly Disagree

Bi) To assess the effect of the volume of data on accounting information.

| S/N | QUESTION/STATEMENT | SA | A | UN | D | SD |

| 5 | 4 | 3 | 2 | 1 | ||

| 1 | Do you agree that data used for accounting includes data from external sources like audio, video, web-based, mobile-based, and sensors-based data, etc.? | |||||

| 2 | Do you agree that an increase in the quantity of external data (web-based, mobile-based, and sensors-based data) increased the accuracy of financial reports? | |||||

| 3 | Do you agree that an increase in the amount of external data increased the number of items in the financial report? | |||||

| 4 | Do you agree that an increase in the size of big data makes financial reports up-to-date and readily available? | |||||

| 5 | Do you agree that an increase in the bulk of data from external sources enhances the quality of accounting information? |

Bii) To assess the effect of a variety of data on accounting information.

| S/N | QUESTION/STATEMENT | SA | A | UN | D | SD |

| 5 | 4 | 3 | 2 | 1 | ||

| 1 | There is the use of data from a multitude of sources such as web-based, mobile-based, and sensors-based data, the internet of things, and wireless technology for accounting purposes. | |||||

| 2 | There is a process for these sources of data in the preparation of financial reports and it improves the completeness of accounting information. | |||||

| 3 | Do you agree that the usage of different types of data improves the reliability of financial information? | |||||

| 4 | Do you agree that the usage of different types of digital data improves the relevance of financial reports? | |||||

| 5 | Do you agree that the use of different sources of data in the financial report improves the timeliness of accounting information? |

Biii) To assess the effect of the velocity of data on accounting information.

| S/N | QUESTION/STATEMENT | SA | A | UN | D | SD |

| 5 | 4 | 3 | 2 | 1 | ||

| 1 | Do you agree that financial reports are being processed in real-time with up-to-the-minute or second data capturing and it has improved the relevance of financial information? | |||||

| 2 | Do you agree that your organisation uses data especially web-based, mobile-based, and sensors-based data speedily and it has improved the completeness of financial reports? | |||||

| 3 | Do you that your organisation uses data especially digital data as soon as it is received and it has improved the quality of financial reports? | |||||

| 4 | Do you agree that your organisation explores data rapidly in preparing financial report to increase reliability? | |||||

| 5 | Do you agree that your organisation takes real-time action on different data sources and it has improved the timeliness of financial reports? |

Biv) To assess the effect of big data on accounting information.

| S/N | QUESTION/STATEMENT | SA | A | UN | D | SD |

| 5 | 4 | 3 | 2 | 1 | ||

| 1 | Do you agree that the quality of accounting information has improved as a result of large data? | |||||

| 2 | Do you agree that a large quantity of data has improved the timeliness of financial information? | |||||

| 3 | Do you agree that a huge amount of data has improved the completeness of financial information? | |||||

| 4 | Do you agree that large data has improved the reliability of financial information? | |||||

| 5 | From when massive data is being used in your organisation, do you agree that it has improved the relevance of financial information? |