Effect of Financial Inclusion on Agricultural Farm Performance in Rwanda: “ A case study of COMSS cooperative.”

- KARERWA Carine

- 641-688

- Jan 3, 2024

- Agriculture

Effect of Financial Inclusion on Agricultural Farm Performance in Rwanda: “ A case study of COMSS cooperative.”

KARERWA Carine

Department Master of Arts in Microfinance, Faculty of Economics Social Sciences and Management, Institut D’enseignement Supérieur De Ruhengeri

DOI: https://dx.doi.org/10.47772/IJRISS.2023.7012051

Received: 11 November 2023; Revised: 28 November 2023; Accepted: 02 December 2023; Published: 02 January 2024

ABSTRACT

Financial inclusion services are an important elements in agricultural farming operations. It makes it possible for producers to cover the cash requirements resulting from the agricultural industry’s unique production cycle, which typically occupies several months and generates very little cash income while necessitating spending money for materials, input purchases, and consumption. Access to financial services is one of several concerns that have an influence on smallholder farmers. Access to adequate, appropriate, and reasonably priced formal financial services for smallholder farmers, however, is a problem that frequently arises in Rwanda. Many rural residents continue to be practically cut off from the financial services required to maintain their survival and enhance agricultural farm performance . The general objective of the research was to find out how financial inclusion affected the performance of the agricultural farms in Muyumbu and Masaka sector . The study was additionally motivated by three specific objectives: to determine the effect of access of micro credit on the performance of the agricultural farm,to examine the effect of access of micro saving on the performance of the agricultural farm,to determine the effect of access of mobile money services on the performance agricultural farm . The target population was the smallholder rice farmers in Muyumbu and Masaka sector. To attain these objectives simple random sampling was employed .The information was given by 186 smallholder rice farmers in Muhazi and Masaka sector. A researcher employed quantitative method for data collection where structured questionnaires instrument was used, descriptive as well as correlative research design were used. Descriptive and inferencial statistics were applied for data analysis. Descriptive statistics employed were frequencies ,standard deviation, and mean. Correlation and multiple regression model were employed for inferencial statistics to show the link among variables ,and SPSS version 20 were also utilized for analysis of data.the findings were presented using tables. The results of this research demonstrated that there is a significant effect and positive contribution of access of micro credit, micro saving and mobile money services on the performance of the agricultural farm in Rwanda as shown by the coefficient of.609*, which is regarded as a high and positive correlation according to the table’s Pearson correlation. The null hypotheses that financial inclusion has no significant effect on the agricultural farm performance was rejected. The study recommends that MFI should expand financial inclusion through access of micro credit, micro saving and mobile money services which significantly uplift agricultural farm performance. The researcher also suggests that different MFIs and government agencies should provide financial training as well as awareness programs for small-scale farmers on how to access micro savings, micro credit, and mobile money services, MFI should Explore the potential for linking micro savings programs with micro credit opportunities. This can create a holistic approach to financial inclusion, allowing farmers to not only save but also access credit when needed for investments in their agricultural activities.

INTRODUCTION

Background of the study

Financial inclusion is seen like a powerful weapon for ending poverty and promoting equitable development. Financial inclusion, or the usage of official financial services, gained a significant effect on economic expansion. The provision of basic, freely accessible banking and financial services to consumers who are in need but are not eligible for conventional services is known as financial inclusion, often referred to as inclusive finance (Tambi, 2018).

In another hand financial inclusion services are an important elements in agricultural production systems and food security . It enables producers to meet the cash requirements brought on by the agricultural industry’s unique production cycle, which typically occupies several months and generates very little cash income while necessitating spending money for materials, input purchases, and consumption. A little while after harvest, cash is received. Farmers would need to keep cash on hand in the absence of micro credit in order to support production and spending during the following cycle. Credit is readily available, which encourages consumption and the usage of purchased inputs, improving agricultural performance and farmer welfare. (Menkeh, 2021).

The majority of the world’s active adults more than 2.5 billion people are currently ineligible for official financial services. As result of not having access to these products, about 80% of the impoverished in emerging and developing nations experience hardship.People in developing countries’ rural areas have had difficulty receiving financial services because of their poverty and lack of education.(Birch, 2018) . Stone et al.( 2018) noted that because rural areas don,t have access to banking services, they are categorized as being financially disadvantaged . There is an absence of knowledge about financial institutions in these places since traditional banks prioritize serving the needs of highly populated urban areas than those of rural communities.

The African development bank(2017) reported that in Africa just 20% rural people on the continent have the ability to access financial services including credit and savings accounts . A rural population’s inability to obtain financial services has an unfavorable effect. For instance, in poor countries where farming is the primary provider of revenue for rural families, not having a loan availability has a significant impact because they lack the funds necessary to increase production.

Globally, 500 million small farms are run by about 2.5 billion individuals who work in smallholder agriculture either full- or part-time (Pylypiv, 2017) . Rural populations suffer when financial services are unavailable. People are unable to invest in order to boost production and ensure their own survival due to a shortage of financing. Fowowe (2020) indicated that having access to financing promotes farmer incomes and agricultural output. The poor experience less hunger as a result, and they are able to stay out of poverty and deal with unplanned stress.

In East African, To improve the quality of life for farmers, farms’ agricultural productivity must be raised. As agricultural productivity rises, so will the demand for inputs, yet most farmers lack the resources to adopt agricultural technologies. Utilizing rural financial services in the form of loans, cash, or goods is the last viable option for farmers to enhance their business operations (Lloyd-Ellis et al., 2021).

In Rwanda, the micro credit program has significantly aided in national advancement. Since the creation of its 2020 vision, the Rwandan government has tried to put policies into place through micro credit initiatives targeted at the economic development of rurally impoverished people (Mbago-bhunu, 2021). Farmers, who typically reside in rural areas, work mostly in agriculture. Micro credit initiatives increase agricultural productivity (Berhanu et al., 2021).

According to Faith (2018) Household participation in micro credit initiatives has improved living conditions and reduced unemployment. Rural households are helped by the availability of financing for investing in agricultural output in order to improve their outside of agriculture income. (Eularie, 2017).Stone et al.(2018) stated that farmers in Rwanda still have very restricted access to financial services and products, despite a growth between 2016 and 2020 as shown in the Fins cope 2020 Agriculture Finance Thematic Report. According to the survey, from 21% in 2016 to 26% in 2020, the proportion of farmers in Rwanda who had access to formal banking services increased from 44% to 47% during the same time period. Although the use of informal financial products has decreased from 23% to 19%, proving that governmental attempts to promote financial inclusion are having a beneficial impact, farmers continue to be under served relative to the rest of the population.

Problem statement

Due to the large range of financial services available, disadvantaged rural residents can manage their household finances, begin new agricultural projects, and start small businesses .If people in rural areas with low incomes earn more money and have safe places to deposit it, they can pay for medical care and schooling as well as make plans and investments for the future (Akanbi et al., 2020).A problem that affects smallholder farmers across sectors is access to financial services (Siaw et al., 2023) . Farmers require access to funding in order to purchase the required supplies, employ or engage in after-harvest preservation and market connectivity technology, as well as mechanization operations. For small-scale producers, access to sufficient, suitable, and fairly priced formal financial services, however, is a problem that frequently arises in Rwanda (Analytics, 2017).

Note (2022) stated many rural residents are still effectively cut off from the financial services they require to strengthen their resiliency and expand their possibilities for employment.

Stone et al.( 2018) said that in Rwanda, a degree of financial services and products accessibility by farmers is still relatively low despite the increase recorded between 2016 and 2020 as reflected in the Fin scope 2020 Agriculture Finance Thematic Report. The report shows an increase in Rwandan banked farmers from 21% in 2016 to 26% in 2020, while the proportion of farmers using other types of formal financial services slightly increased from 44% to 47% over the same period. The usage of informal financial products has decreased from 23% to 19% and this suggests that policy efforts focused on promoting financial inclusion are yielding results, though farmers remain under served compared to the rest of the population.

Therefore, The primary problem addressed by the research is that Lots of farmers within the area to be blocked out of popular banking services due to owing to a difficulty obtaining access to institution of finance as well as security to gain advantages caming from the normal banking sector, Regarding the growth of the worldwide banking system and the focus on promoting financial inclusion.The loan’s size and term are insufficient, the interest rate is unfavorable, the security demands are excessive, or you weren’t expecting it could be authorized(Fin scope, 2016).

Studies on this subject (the effect of financial inclusion on agricultural farm performance ) are still scarce in Rwanda because none of the studies mentioned have been a dressed in Rwanda where this study will be carried out. There is still insufficient supporting evidence, and little scientific evaluation has been done on it. According to the information provided above, The study’s primary purpose is to ascertain how Fiscal inclusion affect agricultural farmers’ capacity to increase the productivity of their farms in Muyumbu and Masaka sector of Rwamagana and Kicukiro district.

Previous investigations on the effect of fiscal inclusion on agricultural farm productivity , have been given very little consideration, this subject need in-depth investigation in Rwanda. This study was differed from the above reviewed studies, they only considered one aspect of its variables which is (micro credit) and none of them looked at micro saving and mobile money services as it influence agricultural farm performance . Therefore, this study filled this literature gap.

Objectives of the study

The investigation’s structure included both general and specific objectives.

General objective

The general objective of this study was to find out the contribution of financial inclusion on the performance of agricultural farm in Muyumbu and Masaka sector.

Specific objectives

i)To determine the effect of access of micro credit on performance of the agricultural farm in muyumbu and masaka sector sector .

ii) To examine the effect of access of micro saving on performance of the agricultural farm in Muyumbu and Masaka sector.

iii)To determine the effect of access of mobile money services on performance of the agricultural farm in Muyumbu and Masaka sector .

Research questions

i)Does access of micro credit have effect on performance of the agricultural farm in Muyumbu and Masaka sector ?

ii)Does access of micro saving have effect on performance of agricultural farm in Muyumbu and Masaka sector?

iii)Does access of mobile money services have effect on performance of agricultural farm in Muyumbu and Masaka sector?

Research hypotheses

H01: Access of micro credit has no significance effect on performance of agricultural farm .

H02: Access of micro saving has no significance effect on performance of agricultural farm .

H03: Access of mobile money services has no significance effect on performance of the agricultural farm .

Delimitation of the study

Primary focus of this investigation was the effect of fnancial inclusion on agricultural farm performance in Rwanda. Conserning geographic focus: The research was carried out in Muyumbu and Masaka sector where COMSS is located as a self establised cooperative in order to better understand the effect of access of micro credit, micro saving and mobile money services on agricultural farm performance. Concerning time scope: Significant long term study was not included because the focus was on understanding the current situation and the immediate impact of financial inclusion efforts on agricultural farm performance.

Organisation of the study

This study covered 5 chapters mentioned below:

Chapter 1; General introduction; Under this chapter, the general introduction was explained in details the background of the study, problem statement, Objectives of the study, research questions, research hypothesis, justification of the study, significance of the study, delimitation of the study, and the organizational framework.

Chapter 2: Literature of Review; In this chapter, the definitions of essential terminology, the theoretical review, the review of the literature corresponding to the objectives, the empirical review, plus the research gap were all carefully clarified.

Chapter 3: Methodology; this chapter explained in details about the subject matter, the investigation’s restrictions, the study’s population, the sample size, the sampling technique, the data sources, the data collection tool, the data analysis, the validity and reliability of the findings, and the research design.

Chapter 4 : Results as well as discussion, this chapter explained the results obtained by a researcher from respondents by analyzing them by using Inferential and descriptive method, SPSS 20 Software and Multinomial regression model

Chapter 5: Conclusion and recommendations; this was a final chapter of this study, whereby it explained what a researcher concludes about the study according to the findings and discussion, furthermore it explained what a researcher recommended.

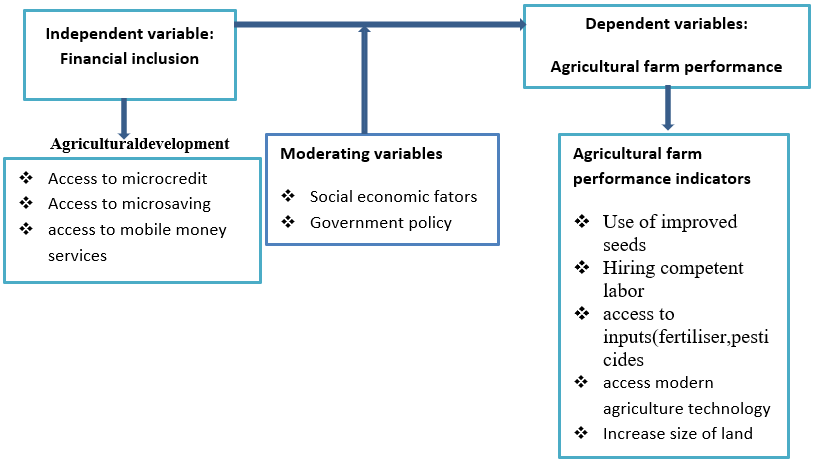

Conceptual framework

Independent and dependent variables are interrelated in the conceptual framework. The research’s independent variable was: financial inclusion which has positive effect on agricultural firm perfomance. The dependent variable will be the agricultural farm performance that are intended to increase farm production and intervening variables that have influence on the dependent variables.

The independent and dependent variables for the study topic are stated below:the effect of financial inclusion on agricultural farm performance in Rwanda

Figure 1: Conceptual framework

(Source:Researcher,2023)

LITERATURE REVIEW

Introduction

Important terminology like theoretical review, empirical review, review of related literature, conceptual framework, and research gap are defined throughout this chapter The definition of the study topic’s key terms was followed the list of important phrases.Under the definition of key terms, the key concepts related to the study problem was defined.

The theoretical review describes many theories that previous authors have used in relation to this research issue and demonstrates ideas that they haven’t utilized but might have used to develop their study. The literature related to objectives, The objectives of various authors in this field of study were contrasted. The objectives of other researchers who did research in this area, the techniques they used for data analysis, the importance of their findings, and other topics were covered along with the empirical review.

Definition of key terms

The key terms from the research topic of the study were defined as follows: Farm performance, financial inclusion, and agriculture..

Financial inclusion

Financial inclusion is the technique of ensuring that those with limited resources and economically disadvantaged people have equitable access to the required financial goods and services from major institutional entities (Mustafa et al., 2022).

The supply of banking facilities to the vast majority of disadvantaged and low-income people at a fair price is another definition of inclusion in finance. The easy access and availability of basic banking services to all members of the population is known as financial inclusion. Financial inclusion refers to the availability of practical financial services and products at reasonable prices that satisfy people’s needs in an ethical and sustainable manner (Peterson & D, 2020).

Agriculture

Agriculture is the type of land use that shows humans repeatedly grow, care for, and give domestic plants more attention. Agriculture is also the most general phrase for all of the different ways that domesticated animals and crop plants support the global population by providing food and other stuff (Harris & Fuller, 2020).

Agricultural farm performance

The agricultural farm performance refers to the efficiency as well as effecacity in generating agricultural produce for consumption. It is a measure of how well the farm utilizes its resources, such as land, labor, capital, and technology, to achieve its goals(Ngong & Fonchamnyo, 2022).

Theoretical review

Because theories and models were utilisedd in this research , the investigator could comprehend the problem’s concept better and obtain knowledge about the ideas of other academics from a global as well as a local point of view.

Public good theory of Financial Inclusion

Providing formal financial services to every member of a society should be viewed as a service to the public that benefits the whole population, based on to the public good principle of inclusion in finance. According to the aforementioned principle, every farmer may easily access financial services. The article in question highlights how farmers can get financial services through mobile money. The only need is that each person have a official account. Furthermore, a government is permitted to make a one-time deposit into every citizen’s account with a bank. This implies that farmers who are unable to provide for their basic needs locally would have the chance to become economically empowered (Kamal et al., 2021).

However, there are a few problems with this concept. First off, the true reasons of financial exclusion are concealed by focusing solely on financial inclusion as a public good Secondly, by representing financial inclusion as a benefit for the community requiring public expenditure, funding from other key public programs may be diverted to support financial inclusion projects(Xiao & Tao, 2022).

Because idea suggests all individuals enjoys financial inclusion, no matter their position or level of earnings,the hypothesis has significance for the study. This means that financial inclusion will benefit farmers of all income levels. Second, establishing financial inclusion as a benefit for the public would need public financing versus private capital since investors anticipate a larger return on private equity investments, which is exceedingly costly when using private money. And last but not least, as it is a public service, the state is obligated to promote financial inclusion(Ozili, 2020a).

Vulnerable group theory of financial inclusion

The vulnerable group theory of financial inclusion states that a country’s financial inclusion initiatives or schemes should focus on assisting the most vulnerable elements of society, such as the underprivileged, children, women, and elderly who are most impacted by economic hardship and natural catastrophes. The idea makes reason to integrate vulnerable persons into the formal financial system since they usually suffer the most from financial emergencies and recessions in the economy. One method to accomplish this is by social financial transfers from the government to the individual (G2P) into the underprivileged people’s official accounts(Tanguay-Renaud et al., 2018).

Cash payments made via a peer-to-peer social network and put into government accounts of the less fortunate, youth, the female, and older people was increased the degree of financial inclusion for vulnerable populations. By encouraging additional economically disadvantaged children, women, and older individuals to participate individuals to register official accounts and engage in the regulated banking system in order to gain access to the benefits of community transfers of money, the percentage of vulnerable populations that have access to financial services will rise(Ozili, 2020b).

Furthermore, when social financial assistance are effective and additional money are made accessible to those in society who are financially excluded, it can give those people a feeling that their present level of inequity is being taken into account for, offering them an opportunity to catch up with other categories in society as a whole. The notion implies that some demographic segments are identified as being susceptible, and that actions intended for boosting financial inclusion should concentrate on such persons. The principle of financial inclusion offers the vulnerable population certain benefits the most vulnerable people in our communities may be more economical than attaining financial inclusion for the whole community (Demirguc-Kunt et al., 2017).

There are a few limitations to the vulnerable group theory. First of all, The notion does not give a lot of weight to establishing equitable financial inclusion. Second, it ignores individuals who are secure beyond the limits of authorized banking. Access to the regulated banking system is necessary for even those who weren’t at risk. Thirdly, it contends that because males do not fall into the vulnerable group, women do. Given that men and women fight for the same opportunities in modern societies, this idea is crucial. Therefore, excluding men while classifying women as disadvantaged groups might have unintended consequences for their capacity to participate in social and economic advantages (Omar & Inaba, 2020).

The concept of vulnerable group has broad application to the rearch being conducted and will aid in placing the research in the right setting. The hypothesis firstly relates to the farmers under consideration because they might be categorized as a vulnerable group. According to the hypothesis, they are vulnerable because of a number of caracteristics, such as economic level, degree of academic achievement , and place of living. A system of classifying people’s incomes that can discriminate between the rich and the poor exists. As was said above, poverty may be a factor in exclusion. Furthermore, farmers earn little revenue. Because of this, their ability to manage money may be limited to the necessities of existence (Ozili, 2022c) .

When it is realized or believed that financial inclusion can be expensive, these farmers may therefore be financially excluded. However, it has been shown that supplying specialized goods to the poor is not economical, particularly in the region known as Sub-Saharan Africa. The substantial number of financial institutions, primarily in metropolitan areas, provides evidence of this.The research does not distinguish between vulnerabilities.This eliminates any gender bias by treating men and women equally in every circumstance. Since the research is not immediately presume that a male and female remote producers are distinguished, I think this circumstance is preferable (Peterson & D, 2020)

Despite all of this, rural farmers today have access to additional easy forms of financial inclusion. In fact, mobile banking has experienced rapid growth and is widely regarded as the continent’s future of financial inclusion.

Collaborative intervention Theory to financial inclusion

The collaborative intervention theory states that several stakeholders need to work together to achieve financial inclusion. The concept suggests that for the excluded groups to be integrated into official financial institutions, collaboration among many stakeholders will be required. This hypothesis has some validity. it promotes an integrated approach to funding for starters. According to this hypothesis, several stakeholders can work together to support farmers’ financial inclusion. partners including the government, non-governmental organizations, and private investment.Second, collaborative stakeholders feel proud of their significant contribution to a public effort(Menkeh, 2021).

However, the concept of a collaborative intervention has several limitations. To begin with, The ideal number of partners required to advance a financial inclusion agenda may be difficult to ascertain. Second, some people could decide to cease taking part, leaving the responsibility to the few people who are still actively engaged. The third issue is that the probability of achieving financial inclusion does not necessarily rise with the number of partners. This suggests that even when enough partners are collaborating to achieve financial inclusion, their efforts might not be sufficient.The investigator may better understand the numerous stakeholders who would be engaged in evaluating how financial inclusion will impact agriculture with the use of this theory(Fowowe, 2020).

Review of literature related to objectives

This section covers the objectives of other researchers who carried out studies that were connected to this one, particularly those who looked at the effect of mobile money services, micro credit, and micro savings on agricultural farm production.

Effect of access of micro credit on agricultural farm performance

Poliquit, n.d.( 2016) examined the small farmers’ access to rural credit in the Philippines. Four local informants and 45 farmers were the two groups of respondents who were interviewed. The emphasis was on how rural farmers perceived rural finance, their preferences, their reasons for borrowing, and their difficulties in obtaining rural credit. A qualitative analysis of the data gathered was done. The result showed that farmers’ preferences were not satisfied because there was little access to financing. It was recommended that access to rural loans be broadened by putting innovative financing ideas into practice.

Ayegba & Ikani (2013) evaluated the effects of agricultural financing on Nigerian farmers in rural areas. A total of 500 questionnaires were sent, and data was collected from primary data. The results revealed that the bulk of credit sources (53.33%) originate from unregulated independent loan providers, which is bad for an expanding economy. It was also clear that the desperately needed rural banks were mostly found in urban areas, which had a negative impact on rural farmers’ productivity by denying them access to formal credit.

Iderawumi( 2020) In the rice-based businesses in Nigeria’s Niger State’s Lavun Local Government Area, the relative technical efficacy of credit and non-credit users was assessed. 60 rice farmers out of a sample of 120 respondents had used credit, whereas 60 had never had access to it. The technical efficacy of the farmer teams was compared using the method of additive multiple substitute variables. According to the study, producers who accessed loans were more technically knowledgeable than those who did not. The study focused on both credit beneficiaries and non-beneficiaries’ production effectiveness.

Missiame et al.( 2021) undertook study to evaluate the impact of rural and community banks’ (RCBs) technical efficiency and access to financing on smallholder cassava producers. The study evaluated the technical effectiveness and impact of RCB credit availability on a sample of 300 smallholder cassava farmers in the Fanteakwa District of Ghana using the stochastic frontier and endogenous switching regression models. The results show that the cassava farmers in the District are 70.5 percent technically efficient, which suggests that cassava yields might increase by 29.5 percent further without changing the existing input levels.

The findings also demonstrate that the key elements that favorably influence farmers’ capacity to acquire loans from RCBs are household head gender, proximity to the bank, and participation in farmer associations. Since, on average, farmers who received loans from RCBs have considerably higher technical efficiencies than farmers who did not, it seems that access to finance from RCBs has a positive influence on the technical efficiency of small-holder cassava farmers.

In a research undertaken by Vincent et al. (2015), information on five banks and ten agricultural firms in Delta State was obtained from both primary and secondary sources to analyze the bank’s credit and agricultural growth. Basic random sampling was used in the study to choose the people who took the survey. To assess the various assumptions, the research collects data using percentages, mean scores, standard deviation and Pearson product-moment correlation. They observed that borrowers of bank loans for agricultural enterprises boost agricultural production.

Prior studies on the link between micro credit and agricultural farm performance have focused mostly on micro credit recipients and non recipients, socioeconomic characteristics that affect access to micro credit, and success as measured exclusively in terms of agricultural output. In contrast to other studies, the current investigation was focused on how micro credit affects farmers’ performance in terms of out pout, techniques used in farming , and yield from the farm in addition to how it influences the production of agricultural goods.

Effect access of micro saving on agricultural farm performance

Pamuk et al. (2021) in her dissertation examined the Effects of VSLs on Maize Productivity: The Uluguru Mountains in Southern Tanzania.Cross-sectional design was chosen. To provide a representative sample, 120 respondents-both VSL members and non-members-were randomly selected. Methodologies that were both qualitative and quantitative were employed. Focus group discussions and observation were utilized to gather data under the qualitative approach, while a questionnaire with both closed and open-ended questions was employed under the quantitative methodology.

Data analysis was done using the Statistical Package for Social Science (SPSS). The results showed that VSL had failed to raise the agricultural performance of its members. The study showed a negative relationship among the variables in study, this calls for conducting other studies to test if there is a positive significant relationship.

(Ribaj & Mexhuani ,2021) In order to put further light on such a connection, the study in question examines the situation in Kosovo utilizing both qualitative and quantitative research techniques. The data, which covered the years 2010 to 2017, were assessed using the improved Dickey-Fuller tests, the Johansen cointegration tests, and the Ganger causality tests. Deposits have a strong beneficial influence on Kosovo’s economic growth, according to the regression findings and the unit root test, which both demonstrate stationarity. This is because savings encourage investment, output, and employment, which in turn leads to more enduring economic growth.

Batista & Vicente( 2020) did research to find out how Using mobile money to increase savings access: These results suggest that farmers might not have faced financial difficulties due to a scarcity of substitute savings options, ranging but rather because fertilizer relevance in the compensation savings intervention may have been necessary to direct farmers’ (limited) attention toward reserving part of their produce earnings. Our findings also imply that the system assistance, in which friends who were farmers had utilization of unpaid mobile payment user accounts, reduced the incentives to set money aside for and purchase agricultural supplies.

Because there are fewer costs involved with transfer inside the network, this decline in incentives is most likely caused by network free-riding. This study shows, in general, how specialized mobile money products can be utilized to enhance the adoption of innovative agricultural technologies in nations like Mozambique that have extremely low agricultural production.

Ksoll et al. (2016)stated that over the course of two years, the impacts of VSLAs in Northern Malawi were investigated using a cluster randomized trial. The findings show that a variety of variables, including how frequently meals were taken each day, how much money was spent on housing according to the USAID Poverty Assessment Tool , and how many rooms were in the house, had positive and substantial intention-to-treat effects. The increase in credit and savings made possible by VSLAs, which has increased agricultural investments and small company revenue, is to blame for this outcome.

Dawuni et al .(2021) stated that the impact of VSLA on agricultural value productivity was studied in Ghana’s Northern Region. The majority of the study’s cross-sectional data were gathered using a semi-structured questionnaire. Propensity score matching (PSM) was employed in this study to examine how VSLA influences the production of agricultural value. The PSM findings show that chatting to VSLA members, contract farming, owning a television, taking part in “Planting for Food and Jobs,” and extension contact all help farmers decide better whether to join VSLA. On the other side, because of their older age, larger household size, and greater distance from the market for their goods, farmers in the Sagnarigu Municipality have a lower level of VSLA involvement. Propensity score matching calculations showed that VSLA members generated agricultural value.

Asamoah & Amoah (2015) presented a Case Study of Micro credit Schemes as a Means of Promoting Rural Banking Capacity Between Vulnerable Farm Families in the Eastern Region of Ghana). Utilizing approved questionnaires, 212 participants in registered cocoa producer associations have been surveyed since 2010 The findings demonstrated that the micro financing techniques allowed those surveyed, the majority of whom were smallholder cocoa farmers, to a mass significant savings in a practical and targeted way.

The campaigns also made use of group guarantees, peer support, and social capital built via the expansion of organizations in order to allay members’ concerns about obtaining credit from companies with a high (above 95%) rate of payback. They now have easy access to agricultural items like fertilizer to help their cocoa yields because of the money they were able to save .Microfinance is a powerful tool for promoting a saving culture.

It is crucial to get the conclusion that the variable has not been fully examined from the evaluations above. The study also looked at demographic traits that influence how micro savings are assessed, how MFIs help mobilize savings, and how savings impact investments. There was a negative correlation found in other investigations as well. examining the relationship between micro savings and small farmers’ output is crucial. In contrast to past studies, this one examined saving habits and how they affect the agricultural farm performance.

Effect of mobile money services on agricultural farm performance

Kilombele et al. (2023) studied how mobile money affected household happiness and maize output. The study’s data were gathered from a sample of 1310 households that were randomly selected utilizing a two-stage selection process from a target demographic of 130 Village Community Banks (VICOBAs) members. Data from a randomly selected sample of 1310 residences was examined using the endogenous switching regression (ESR) model. The homes were selected from seven local districts.

The ESR estimation’s findings show that MM consumption is significantly and favorably correlated with the household head’s level of education, asset ownership, credit availability, input access, and social networks. The usage of MM is directly correlated with decreased risk of poverty, increased production of maize, or both. When using the indicator for progression out of poverty, farmers who elected to use MM services saw an improvement in maize output of over 124 kg/acre and a decrease in their likelihood of living in poverty of more than 25%. In order to increase maize yield and reduce the likelihood of poverty, our results indicate the necessity for a special approach to reach out to and support the adoption of MM among households with limited utilization of conventional financial institutions.

Rahama(2022) carried out a research to determine the potential effects of mobile money adoption on input utilization and farm production. The results demonstrate that using mobile payment technologies improves both the amount and quality of agricultural production. The techniques,s adoption increases farm output and pesticide and fertilizer use. Smallholder farmers are encouraged to invest in agricultural inputs for greater farm output by the adoption of mobile payment technologies. This suggests that the use of aggressive fertilizer and herbicide applications could be encouraged by mobile payment technology, enhancing agricultural output.

Kikulwe et al .(2016) Kenyan researchers examined the effect of mobile money on the productivity of small-scale agricultural producers and homeowners. Information on household human capital, demographics, banana output, other farm businesses, and agricultural inputs that can raise productivity and, consequently, household income was gathered using a standardized questionnaire.The survey has a special question about possessing a cell phone and using mobile cash services,descriptive statistics was used .

The findings show that mobile cash users outperform non-users in terms of using more farm inputs purchased, selling more of their produce, and overall performance. The 640 observations on the balanced panel came from the 320 houses that were contacted during the course of the two survey sessions.Most of the diversified smallholder households in the sample had farms that aren’t much bigger than 5 acres. Every home in the sample raises bananas, both for domestic consumption and for local markets. The results demonstrate that people that use mobile money use significantly more inputs, such as hired labor, insecticides, and fertilizer, and sell a greater percentage from their harvest on the market. Mobile money, in one way or another, promotes more commercial farming. The results back up the idea that mobile money services can increase productivity and revenue in households.

Empirical review

Menkeh (2021) conducted a research to determine how financial inclusion will change the growth of farming in the Ngoketunjia area in northwest Cameroon. Results clearly demonstrated the detrimental and useless nature of the financial inclusion variable. Due to their limited access to credit facilities and the absence of traditional banking institutions, farmers are virtually shut off from financial services. Most of the local farmers are unable to access the limited number of microcredit organizations that do exist due to their high interest rates and collateral requirements,

Florence* & Nathan**(2020) undertook study to ascertain the effect of agricultural financing from commercial banks on the growth of agriculture in Uganda.The results show that financial support considerably raises agricultural production. Credit to processing and marketing has a much less effect on agricultural output than credit to production, it has been shown.The findings show that short-term agricultural output is not directly affected by bank funding.The research shows that commercial banks’ agricultural financing makes a considerable economic contribution to Uganda’s agricultural economy.

Ngegba et al.(2016)investigated how VSLA reduces agricultural output in the Moyamba District of the Banta Gbangbatoke (Lower Banta) Chiefdom of Sierra Leone. A multi-stage stratified random sampling procedure was used to choose the chiefdom, VSL groups, and group participants.350 farmers were polled using a certified, pretested, highly structured questionnaire(There are 100 non-beneficiaries and 250 beneficiaries).

It was found that VSLA affected farmers’ income (60.0%), access to storage facilities (61.0%), ability to save (64.0%), and ability to plant a variety of crops (57.6%). It was demonstrated that farmers experienced VSLA effects on agricultural productivity in varied degrees, which began to improve family food security. This demonstrates how VSLA may help with family food security as well as community development and poverty alleviation.

Tuesta et al.(20 15) examined the variables affecting financial inclusion.The findings indicate that among the Muslim populations under investigation, there is a significant disparity between financial access and financial usage. The researchers stressed the shaky connection between loan availability and financial inclusion once more.

Ouma et al.(2017) carried out research to evaluate the connection between mobile financial services and financial inclusion. Does it help to mobilize savings? The findings show that families are more likely to save money if they have access to and use mobile devices for financial services . Access to mobile financial services not only expands the possibility of saving but also significantly affects the amounts saved due to how often and easily such transactions may be completed using a mobile phone. The findings also showed that low-income families in Sub-Saharan Africa benefit from mobile banking increasing savings.

According to (Wang & Fu, 2022) inclusion of digital finances Farmers that participate in the digital economy and use digital financial services are less susceptible. However, the extent to which farmers can manage risk will determine these outcomes.

Olaniyi(2017) She has out study to assess how Nigeria’s agricultural environment might be affected by financial inclusion. The results show how utilizing financial services has an impact on agriculture both now and in the future. To ensure the long-term success of rural agriculture, financial inclusion must be improved . On the other hand, the amount of cash available had minimal impact on agricultural productivity. Even while providing financial assistance to rural farmers has many benefits, it’s more important to consider how the monies are allocated and how they impact rural outcomes.

Siaw et al .(2023) conducted analysis of the empirical evidence regarding the impact of financial inclusion on agricultural .The results demonstrated that family income is impacted in a number of different ways by access to financial services. As a result, there were different quantile-specific impacts of financial service accessibility on income . Programs that improve rural families’ access to financial services must be adopted in order to raise income in order to eliminate poverty.

Singh(2019) investigated how financial constraints affected US agricultural cooperatives.The results demonstrate that the capital expenditures of agricultural cooperatives are significantly influenced by the availability of internal finances. .

Javed et al. (2022) did a research to evaluate determinants of agricultural credit utilization among small farm holders. The results show that agricultural credit has a significant influence on agricultural output since there is a direct relationship between agricultural credit and farm productivity.

Fowowe (2020) did research on effect of financial inclusion on agricultural productivity in nigeria .Regardless of the method used to measure it, the data demonstrate that financial inclusion has favorably and statistically significantly impacted Nigeria’s agricultural productivity. Therefore, financially included families generate more from their agricultural activities than financially excluded ones.

Galang( 2020) examined the accessibility of agro-credit to farmers in Kaduna, Nigeria. The study’s survey research approach covered all three of the subject area’s agricultural zones. To achieve the study’s objective, five research questions and a hypothesis were developed. The hypothesis was investigated using the Chow test model. The gathered data was examined using multiple regression and a 4-point Likert scale. The results of the study demonstrated that several elements, such as age, educational attainment, experience, and financial accessibility, have an effect on farmers’ output.

Villarreal( 2020) did a research on financial inclusion of small rural producers. The findings indicate that increased financial inclusion has favorable effects on agriculture productivity at the household and macroeconomic levels.

Peprah et al( 2020) examined how the usage of mobile money affected agricultural out pout. A sample size of 379 was chosen using the Krejcie and Morgan’s (1970) determination of sample size table for a population of around 40,000 people, which was spread evenly across the three districts on purpose. Simple random sampling was used to choose the respondents. Since the District Agricultural Offices furnished a list of respondents, the study’s lottery methodology was applied. 460 surveys were ultimately collected, despite the fact that 550 questionnaires were distributed to cover non responses The chance of using mobile money was calculated using the probit model.

According to the research, farmers who utilize mobile money produce more than those who do not. The t test demonstrates a statistically significant 10% difference in production between m-money adopters and non-adopters. The use of m-money by more farmers is the reason why over 60% more farmers use fertilizer than those who do not. The usage of m-money by households to manage savings accounts, obtain loans, send and receive payments, and buy insurance products might all improve their agricultural activity, according to the Pearson chi-square test of association. Farmers who use financial institutions are more inclined to use financial services since greater income levels are a predictor of increased agricultural production.

Javed et al .( 2022) performed study on how access to financial services affects Ghanaian farmers’ income The loan interest rate, a proxy for farmers’ access to financial services, had a considerably positive influence on the expansion of agriculture.

Florence* & Nathan**,( 2020) undertook a research to assess the effect of agricultural financing by commercial banks on Uganda’s agricultural expansion. The study provides evidence that the influence of commercial banks’ agricultural loans on Uganda’s agriculture sector’s GDP is considerable. The data showed that commercial bank loans and contributions to agriculture GDP were strongly positively and significantly negatively correlated.

(Parlasca et al.;( 2022) conducted study to determine how often African farmers utilize mobile finance services, The findings demonstrate that mobile financial services (MFS) are widely regarded as a practical instrument to assist smallholder farmers in their search for agricultural finance especially those who are often underserved by traditional banks. However, there is a paucity of empirical information about the actual usage of MFS by agricultural households.

Seng( 2017) conducted study on how mobile phones affect money inclusion in Comodia. The study discovered that because of cellphones, households are far more inclined to borrow money from microfinance firms., especially if they want to start an agricultural enterprise. Mobile technology reduces business risk by providing clients with access to a variety of information, notably over the phone about the credit application process and financial understanding. Users are invited to borrow money using this information so they can get involved in profitable enterprises, particularly in agriculture.

Chinelo (2022) investigated how microloan credit affected Nigerian agriculture. The results demonstrated that microloans had little to no impact on agricultural or livestock productivity. The findings of this research indicated that microfinance loans in Nigeria had no effect on the production of either crops or animals. This shows that livestock farmers and Nigerian agriculture are self-sufficient. This suggests that they are unable to use the money that the government has allocated for farmers through government agencies. Once more, the poor farmer is not eligible for microloan financing. This addresses the issue of the nation’s exorbitant food prices, which is related to insufficient food production

Ngoongeh & Bime( 2023) conducted study on the factors influencing financial inclusion among cocoa producers in Cameroon’s southwest. The study reveals that just 16.6% of farmers were financially included due to the negative impact. Additionally, the results showed that at a 1% level of significance, bigger family sizes, farm training, proximity to formal financial institutions (FFIs), small-scale output, and more years of farming experience significantly improve financial inclusion. Furthermore, the absence of collateral security, far-off FFIs, and low income accounted for 51.3% of the key barriers to financial inclusion.

Kingdom (2015) did a research to find out how microfinance affects the production of agriculture in developing countries. The results showed that agricultural production was favorably connected with microfinance and that output levels were considerably impacted by it.The study discovered that microfinance significantly increases agricultural output. In addition, it was found that despite a huge need for agricultural loans, industry participants encounter challenges because of things such as a lack of property as collateral and a lack of knowledge of the loan acquisition procedure.

According to Demirguc-Kunt et al.(2017)Since women and older make up the majority of those working in agriculture and are all at risk of losing their jobs owing to the economy, this methodological insight is essential for this study. It could be required to integrate these disadvantaged groups into the current financial system in order to boost the local agricultural sector.

Langwenya(2019) established a statistically significant correlation between the usage of financial services and agricultural development in South Africa, corroborating the notion that financial integration affects agricultural output. Galang( 2020) examined the accessibility of agro-credit to farmers in Kaduna, Nigeria. The study’s survey research approach covered all three of the subject area’s agricultural zones. To achieve the study’s objective, five research questions and a hypothesis were developed. The hypothesis was investigated using the Chow test model. The gathered data was examined using multiple regression and a 4-point Like rt scale. The results of the study demonstrated that several elements, such as age, educational attainment, experience, and financial accessibility, have an effect on farmers’ output.

(FAO, 2015) found that increasing financial inclusion is a essential to achieving agricultural growth, which is necessary to reduce rural poverty. However, a significant factor in the delayed investment in agriculture and rural growth is smallholders’ lack of access to credit. According to (Batista & Vicente, 2020) Mobile banking networks have significantly benefited the promotion of financial inclusion of formerly unbanked communities in East Africa. Ghanaian agriculture benefited greatly from the proxy for lending interest rate used to gauge farmers’ access to credit.

Research gap

This section explains the methodological, theoretical, and empirical problems of the work and the research gap. The investigator’s methods are contrasted with those used by other authors that did research relating to this topic due to the methodological gap. ,empirical gaps highlight conflicts between the goals and conclusions of earlier studies that were related to this particular study and the goals and conclusions of the current investigation. Theoretical gaps evaluate the theories employed by the researcher of this study with those employed by other researchers who conducted research related to it.

This study indicated a research gap since no one has precisely Studied on this subject (the effect of financial inclusion on agricultural farm performance ) are still scarce in Rwanda because none of the studies mentioned have been adressed in Rwanda where this study was carried out. It still lacks enough documentation, and little scientific analysis has been done to assess it. The effect of financial inclusion on Rwandan agricultural farm performance has not yet been studied.

Microsavings and mobile money services have received relatively little attention in previous studies on the impact of financial inclusion on agricultural farm performance; this topic requires in-depth exploration in Rwanda. This study was differed from the above reviewed studies, they only considered one aspect of its variables which is (microcredit) and none of them looked at microsaving and mobile money services as it influence agricultural farm performance .Therefore, this study filled this literature gap.

Methodological gap

According to the review of methodologies used by other researchers, various researchers used different methods on their data collection and their data analysis. Many researchers used Secondary sources of data collection whereby they used instruments like Government publications, articles, public records, reports and journals while some few used Primary sources of data Such as questionnaires and focus group discussion . Furthermore, different researchers used various methods, models and software for their data analysis such as STATA Software SPSS version 22 to analyze data (Menkeh, 2021; mohammad Aifujjaman, 2007; Parlasca et al., 2022; Kilombele et al., 2023; Kikulwe et al., 2016; Atakli & Agbenyo, 2020) .

This study used primary source of data collection whereby Questionnaire instrument was applied. Descriptive statistics, correlation, multiple regression modeling, and SPSS version 20 software were all used in the study to evaluate the data.

Theoretical gap

According to the theoretical review on the theories used by various researchers on financial inclusion ,most of the researchers used various theories and modals such as Dissatisfaction theory of financial inclusion, The special agent hypothesis, community echelon financial inclusion, and financial inclusion ,The financial literacy concept of financial inclusion, and endogenous growth theory .Theory of collaborative financial inclusion intervention Theory of financial inclusion in public services; ignore other viewpoints (Wang & Fu 2022; Tambi 2018; and Villarreal 2020). The public good theory of financial inclusion, the vulnerable group theory of financial inclusion, Collaborative intervention Theory to financial inclusion were the theories employed in this study that were not often used by other researchers.

Empirical gap

Numerous research on the impact of financial inclusion on agricultural farm performance have been undertaken globally,none of them explained in details how financial inclusion particularly access of micro credit, micro savings and mobile money services affect the agricultural farm performance in a way of increase agricultural out pout. For instance, According to previous authors they have been trying to write on how micro credit affect agricultural performance on farms but most of the studies looked at the beneficiaries and non beneficiaries of micro credit, socioeconomic determinants of accessing micro credit and also, the studies looked at agricultural output alone (Chinelo, 2022; Churchill et al., 2016; Berhanu et al., 2021; Iderawumi, 2020; Umugwaneza & Barayandema, 2021).

This study distinguished itself from these studies in the sense that it looked at access of micocedit, accesss of micro saving,and access of mobile money services in terms of farm output .others studies looked at how savings influence investment, how MFIs helps in mobilizing savings and demographic determinants of assessing micro savings. Some studies also assumed a negative relationship (Microfinance,2019;David Danjuma,2018;Kingdom, 2015; Girabi, 2013) Therefore, it is crucial to examine the connection between access of micro savings and small farmers performance. This study differed in that it examined the how easy access micro saving are and how it affects agricultural farm performance.Furthermore, many researchers tried to explain about how mobile money services can affect agricultural farm out pout (Kilombele et al. 2023;Rahaman, 2022 ; Peprah et al., 2020; Seng, 2017) but they didn’t explain in details on how access of mobile money services can influence the agricultural farm outpout and performance of farmers.

RESEARCH METHODOLOGY

Introduction

The following section provides a broad review of the subject investigated and the research design outlining how data was gathered, the study population, which focuses on the population that was particularly targeted, and the sample design, which details the methods used to choose the study’s sample. This chapter also includes data collection techniques that show the tools used to collect data, data analysis techniques that demonstrate how data were analyzed, variability and reliability that concentrate on the accuracy, the quality and consistency of the data, and finally ethical consideration that governs the researcher’s behavior was deeply covered in this chapter.

Description of the specific area of the study

Muyumbu Sector is a subdivision of Rwamagana District in Rwanda. Rwamagana District and Muyumbu Sector are two of the subdivisions of Rwanda’s Eastern Province.It is a rural location with rolling hills and fertile ground that is suitable for agriculture. The sector is well known for its support of the local economy and engagement in agriculture.

The main source of income for those who live in Muyumbu Sector is agriculture. The economy of the Muyumbu Sector is mostly centered on agriculture. Farmers engage in both subsistence farming, growing crops for their own consumption.

Muyumbu Sector is predominantly rural, characterized by beautiful landscapes and rolling hills that are typical of the Rwandan countryside. Agriculture is the primary economic activity in the sector, with residents engaged in farming, livestock rearing, and other related activities. The fertile land supports the cultivation of crops such as maize, beans, potatoes, vegetables, and various fruits(de Bruyn & Wets, 2006).

Research design

The methods used to gather and assess measurements of variables are known as research designs.To assess and discuss the study’s subject, this investigation employed a descriptive and correlative research strategy to gather data .To learn more about the issues presented by this research, Farmers in the region got specially created questionnaires. The data was assessed using SPPS version 20.multiple regression analysis was used .

Using a quantitative approach, the data for this investigation were gathered. Field data was collected using questionnaires, and results were then assessed using a descriptive, inferencial statistics ,correlative research design as well as multiple analysis of regression were employed . The investigation used a quantitative methodology since it included characteristics that could be quantified and statistical analysis could be used to test if financial inclusion has an impact on agricultural farm performance.

Study population

Shukla( 2020) defines the population as a collection of all individuals who share the variables and characteristics that have been studied, and to whom the study’s generalizable conclusions may be applied. The population for each study is determined by the topic under investigation.

To examine how Rwandan agricultural farm performance is affected by financial inclusion, target population( total population) for this study was 349 small holder rice farmers, which included rural women, men, and young adults from the 2 sectors( Muyumbu and Masaka sector) who formed a cooperative of farmers( COMSS).These small holder farmers are registered with self established cooperative. This demographic made it possible for the researcher to gather the study’s required data.

Sample size

A sample size is a group of individuals selected from a population who often utilized in research to represent the population in research (Elmasri, 2017). Examining a sample and extrapolating the findings to the complete population is the primary objective of research. Representativeness of the sample determines how accurately we can generalize the findings to every body.

Using the Yamane formula, the sample size was determined. The following Mathematical expression was employed :

where the study size is n

Total population is N,

And error margin is e

Thus ,N= 349,e=0.05,and n=?

n=349/(1+349(0.05)2) =

n=349/1.8725 =186

Using the Yamane formula n =186 rice farmers were selected as sample ,therefore this study was collected data on 186 smallholder rice farmers.

sampling procedures

To choose respondents, the researcher used a simple random sampling technique.Data was gathered among 186 respondents chosen at random among the rice farmers in the Muyumbu and Masaka sectors who were members of COMSS, a farmer-owned. Considering that 186 questionnaires were handed out, all had been received , the response rate was 100%. The field assistants’ contribution to the data gathering procedure was responsible for the Satisfactory response rate. Seeing that all respondents that all of the respondents were farmers from the COMSS cooperative, a random sample methodology was adopted in the study.Random selection was used to choose participants from the general population.

Sources of data

According to Ajayi (2017) ,The term “primary data” refers to information that has been collected directly by the researcher. Primary data are information obtained directly from a source and used in further analysis to address the issue at hand.This study used primary source of data collection whereby a researcher collected data by visiting directly the (COMSS) cooperative formed by farmers from Muyumbu and masaka sector.

Data collection instruments

Questionnaires were used in this study to retrieve firsthand data coming from those surveyed.The approach was chosen due to its cost-effectiveness in surveying participants and its feasibility for quickly gathering information. Respondents were needed to utilize x to fill in the blank areas supplied against each question or tick one of the responses that suited her/his opinion .The researcher in this study uses well-organized, closed-ended questions written in simple language to make it simple to get exact data.

Using a five-point scoring system, the closed-ended questions were assessed in this way: Strongly Disagree = 1, Disagree = 2, and Neutral = 3 4. Agree and 5. strongly agree depend on the the respondent’s judgment . It facilitated the researcher in acquiring information directly with the help of surveyed participants since she personally distributed the questionnaire and collected data there. The method made it possible to quickly gather data from a lot of responders.

Data analysis

Using descriptive statistical methods like mean and standard deviation, the data was evaluated, collected, and accurately interpreted. The original data gathered was evaluated using quantitative methods. Statistical software for social scientists called SPSS version 20 was used to analyze the quantitative data.Tables were used to display the results.A association between financial inclusion and agricultural farm performance was examined using Spearman’s correlation and multiple linear regression. Both descriptive and inferential methods were employed to assess the findings. Means, standard deviation, percentages, and frequency were employed as descriptive statistics for the data analysis.

The respondent’s age, gender, marital status, and degree of education were all described by the researcher using a descriptive methodology. Using this method, a researcher was able to deduce the data’s distribution, locate mistakes and outliers, and identify connections across different variables. The relationship between the variables was evaluated using multiple linear regression and Spearman’s correlation for inferential statistical analysis.

The statistical analysis of data

The data gathered through the replies of the survey participants was processed using SPSS version 20, and the findings was presented in chapter four using tabulated formats.”. To analyze research findings ,To analyze the data, SPSS’s frequencies, descriptive, and regression analysis tools have been used.

A popular and often used indication of the middle of a distribution of a quantitative variable is the mean. The term “mean” refers to the “average or mathematical average of the values

Table 1: Evaluation of mean

| Mean | Evaluation |

| 1.00-1.99 | Strong disagree |

| 2.00-2.99 | Disagree |

| 3.00-3.99 | Agree |

| 4.00-5.00 | Strongly Agree |

Standard déviation (σ)

Deviation from the mean is a figure that represents how variable the data are. It shows how closely the data resembles the mean. The researcher is informed of the distribution of the data. Greater variability is reflected in higher values of S; when S equals zero, all observations share the same value stands for typical deviation from the mean.

Table 2: Evaluation of standard deviation

| Standard Deviation | Level Spreading |

| SD ˂0.5 | Homogeneity |

| SD≥0.5 | Heterogeneity |

| Source: (López-Romero et al., 2003) |

Two objects are considered homogeneous when they share an identical appearance or texture. Any two comparable items, entities, or persons can be said to as homogeneous.

In data analysis, heterogeneity refers to the diversity or variability of data points within a dataset. It suggests that the data is not uniform and may contain different values, categories, or characteristics(López-Romero et al., 2003).

Correlation

(Schober & Schwarte, 2018) ,states that using correlation analysis, a researcher may study and quantify the statistical association among more than one variable. Bivariate Correlation emphasizes the statistical relationship between two variables, whereas the term “multiple correlations” refers to the measurement of the link among more than two variables.” The goal of correlation analysis is to assist the researcher in evaluating the significance and the strengh of closeness between variables.

Table 3: Evaluation of Correlation

| Coefficient of Correlation | Label: Positive/ Negative |

| r=1 | Perfect linear correlation |

| 0.9 < r < 1 | Positive strong correlation |

| 0.7 < r < 0.9 | Positive high correlation |

| 0.5 < r < 0.7 | Positive moderate correlation |

| 0 < r < 0.5 | Weak correlation |

| r =0 | No correlation (no relationship) |

Source (Agresti & Franklin, 2009)

Model specification

X = Independent Variable

Y = Dependent variables

Y = f(x)

Where

X = (X1= Access of micro credit (AM), X2= Access of micro saving (AS), X3= access of mobile money services (AMM)

While the

Y= (y1= Agricultural farm performance (AFP)

FI=f(AM,AS,AMM)f1

AFP=f(AFP)f2

The subsequent multiple regression models were created using these tools:

FI=β0+β1AM+β2AS+β3AMM+Modal 1

AFP=β0+β1AFP+Modal2

Validity and reliability

This section addressed the reliability and validity of research instruments. validity and reliability were extensively evaluated and assessed by the researcher to exclude any chance of obtaining inaccurate answers.

Validity of research instruments

Before implementation in the field, the supervisor designed and authorized the research instrument (questionnaire) for evaluation. To guarantee validity, the researcher made sure that multiple factors were examined in the questionnaires. Every variable in the study was covered by the questionnaire, along with every potential item in the research topic. The researcher made sure the tools were appropriate and accurate and that they matched the study’s objectives and research questions.

The experts assess the test’s face validity. Additionally, content validity made it straightforward for the expert to judge if the study’s content was appropriate; with the expert’s direction, unclear or ambiguous questions were revised, and unrelated questions were removed.

Reliability of the research instruments

Reliability was used to assess consistency, as well as how effectively the approach and methodology was being used, while choosing instruments for data collecting. Inter-rater reliability will be utilized to guarantee that the questionnaires are equally assessed by several experts and that the evaluations are equal There will be relationships between the adjustment and the personal expert inputs. The consistency with which raters or observers make judgements is referred to as inter-rater reliability.Charter (2006), implies that there should be consensus among the observers as to what defines being present

Table 4: Reliability test

| Cronbach’s Alpha | N of Items |

| .836 | 51 |

The 0.836 reliability result in the table above indicates that the questions were accurately asked and answered because Cronbach’s Alpha value between 0.7 and 1 is commonly regarded as reliable.

Ethical consideration

Conducting research requires transparency and trustworthiness in addition to expertise and passion This is being done to safeguard people’s rights. For this study to be ethical, the rights to autonomy, privacy, secrecy, and informed consent were all followed.Before contacting the individuals responding to the survey, their permission is requested. The respondents were made aware of their options to willingly accept or refuse, as well as their freedom to stop taking part at any moment without facing consequences.

Those who took part received information on the research’s goals, how the data would be collected , and were given guarantees regarding confidentiality and the absence of any risks or espenses. Before responses from responders, They were made aware of the study’s objective , and the questionnaires were to be written so that participants do not have to give their personal information. Since respondents are free to supply additional details or consent, they were more comfortable and capable of speaking up without fear as a result of this.

Limitation of the study

A few difficulties were faced by the researcher while doing this investigation, which occasionally made it challenging for her to act as was intended. These issues include some of the following:

The researcher was unable to cover a larger group because of the study’s severe timing constraints. The vast majority of respondents used to often complain their lack of time to finish the survey. The researcher was passionate about the study and patiently waited for all of the questions to be resolved, even though this was a standard practice.

Another limitation is:

This research was restricted to the small-holder rice farmers’ cooperative.It simply is focused on the masaka and myumbu sectors. Despite the above-mentioned restrictions, it is considered that the sample picked is reasonably representative. The sample is believed to contribute to a logical analysis and conclusion on how financial inclusion effects agricultural farm performance.

RESULTS AND DISCUSSION

Introduction

This chapter presents the analysis and discussion of the field data. The goal of the study was to find out how financial inclusion affects performance of agricultural farms. Based on the replies from the research respondents who were chosen throughout the data collecting procedure, the results are given as tables. According to respondents,s identification and the study’s objectives which were established in chapter one of this study, A review of the findings was prepared.This chapter also tested the hypotheses that were presented in chapter one.

Table 5: Questionnaire response rate

| Questions distributed in number | Tota number | Percentage |

| given out questions | 186 | 100% |

| Responded questions | 186 | 100% |

| Missing question | 0 | 0% |

Source: Computed by the researcher,august (2023)

The respondents’ percentage of responses is shown in the table ahead from the sampled farmers from Masaka and muyumbu sector who formed the COMSS cooperative( Cooperative des Multiplicateur de semences selectionnees ) as the cooperative of farmers from those 2 sectors Out of 186 questionnaires given to the selected farmers, the findings revealed that all were returned .The high response rate was due field assistant with each respondent to complete questionnaires and collect information for the questionnaires.

Profile of respondents

The respondent’s profile was regarded as significant to this study by the researcher, The respondents were questioned about their sex, education level, age group, marital status, and length of time working in agriculture in order to learn more about them.In order to investigate the respondents’ profiles, descriptive statistics were employed to collect information on the respondents’ gender, age group, education level, marital status, as well as longetivity in agriculture.

Table 6: Description of respondents by demographic variables

| Frequency | Table N % | ||

| Gender of participants | Female | 104 | 55.9% |

| Male | 82 | 44.1% | |

| Total | 186 | 100.0% | |

| Education level | No formal education | 21 | 11.3% |

| Primary education | 107 | 57.5% | |

| Secondary | 54 | 29.0% | |

| University | 4 | 2.2. % | |

| Total | 186 | 100.0% | |

| Age group of respondents | Between 18-25 | 16 | 8.6% |

| between 26-35 | 43 | 23.1% | |

| between 36-45 | 95 | 51.1% | |

| between 46-64 | 32 | 17.2% | |

| Total | 186 | 100.0% | |

| Marital status of respondents | Single | 10 | 5.4% |

| Married | 163 | 87.6% | |

| Divorced | 5 | 2.7% | |

| Widowed | 8 | 4.3% | |

| Total | 186 | 100.0% | |

| Longevity in COMSS | 0-5 years | 50 | 26.9% |

| 5- 10 years | 90 | 48.4% | |

| 10 years and above | 46 | 24.7% | |

| Total | 186 | 100.0% | |

Source: Primary data (2023)

For ascertaining the gender of the respondents, the findings show that 104 farmers representing 55.9% of respondents were females and 82 respondents representing 44.1% were males.This implies that the study findings were influenced by female responses.

The results from education level of respondents have proved that out of 186 (100%) of respondents , 11.3% of those asked had never attended school , Of those surveyed, 57.5% had completed primary school , 29% of those surveyed had completed high school, 2.2% respondents had university. The majority of respondents who contributed to this study were in primary with 57.5%. Education is an opportunity For development which enables people to acquire knowledge and skills which they employ in activities and thereafter improve performance in their activities .The study concludes that most people engaged agriculture have secondary education and primary

The results from age group of respondents have proved that 8.6% of surveyed fell within the age bracket of 18 and 25; 23.1% of surveyed fell within the age bracket of 26 and 35; 51.1% of surveyed fell within the age bracket of 36 and 45; and 17.2% of surveyed fell within the age bracket of 46 and 64.The study concludes that most people engaged agriculture were aged from 36-45 because the age from 36-45 belonged to the group of people who have major responsibilities in the family. Age is an important element which influences decision making in development activities. According to Demirguc-Kunt et al.(2017)Since older make up the majority of those working in agriculture, this methodological insight is essential for this study. It could be required to integrate these disadvantaged groups into the current financial system in order to boost the local agricultural sector.

For ascertaining the marital status of respondents where 10 respondents with 5.8% were single, 87.6% were married, 2.7% were divorced, 2.7% were window. According to the research findings,the majority who contributed in this study were married. Because married people have more charges and different familial burden which can stimulate them to engage in agriculture to satisfy their family needs.