Value Chain Mapping and Market Survey for Dairy Cattle and Goat on the Copperbelt Province, Zambia.

- Dennis Kuyenda Lembani

- 2997-3018

- May 25, 2024

- Agriculture

Value Chain Mapping and Market Survey for Dairy Cattle and Goat on the Copperbelt Province, Zambia.

Dennis Kuyenda Lembani- Ph.D.

The University of Zambia- MAD- IDE-21106213. Department of Development Studies.

Board Member: African Institute of Leadership & Governance- Durban, South Africa.

Research Associate: Community Aid Zambia.

Former Program Manager- Heifer International Zambia.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804280

Received: 17 February 2024; Accepted: 15 March 2024; Published: 25 May 2024

ABSTRACT

The main objective of the study was to identify possible entry points into the dairy cattle and goat meat value chains for small holder farmers, by clearly highlighting opportunities open to them in their respective catchment districts. The study was meant to also identify key challenges surrounding the two value chains and propose effective mechanisms of addressing them. In order to achieve the above objective, the study was meant to analyse and document the dairy and goat value chain on the Copperbelt Province considering different dairy & goat production systems, cost of production by system and the existing dairy cattle & goat marketing channels to the end markets. It was meant to generate necessary primary data from selected districts in Heifer International Zambia (HIZ) SLMEP project domiciled and operational areas collate and analyse available secondary data to meet the study objectives. The study was basically intended to identify key areas of interventions in dairy and goat value chain by development institutions to enable smallholders to become one of the most significant actors capable of receiving benefits and proportionate share of the trade margins across the value chain in selected districts of Ndola, Kitwe, Kalulushi and Mufulira of the Copperbelt Province of Zambia. The data collection methods employed by the researcher were; Desk Review, Focus Group Discussions and Key Informant Interviews respectively.

Keywords: Dairy Value Chains, Smallholder Farmers, Producers, Input Suppliers, Service Providers, Livestock Producers, Milk Collection Centres.

INTRODUCTION

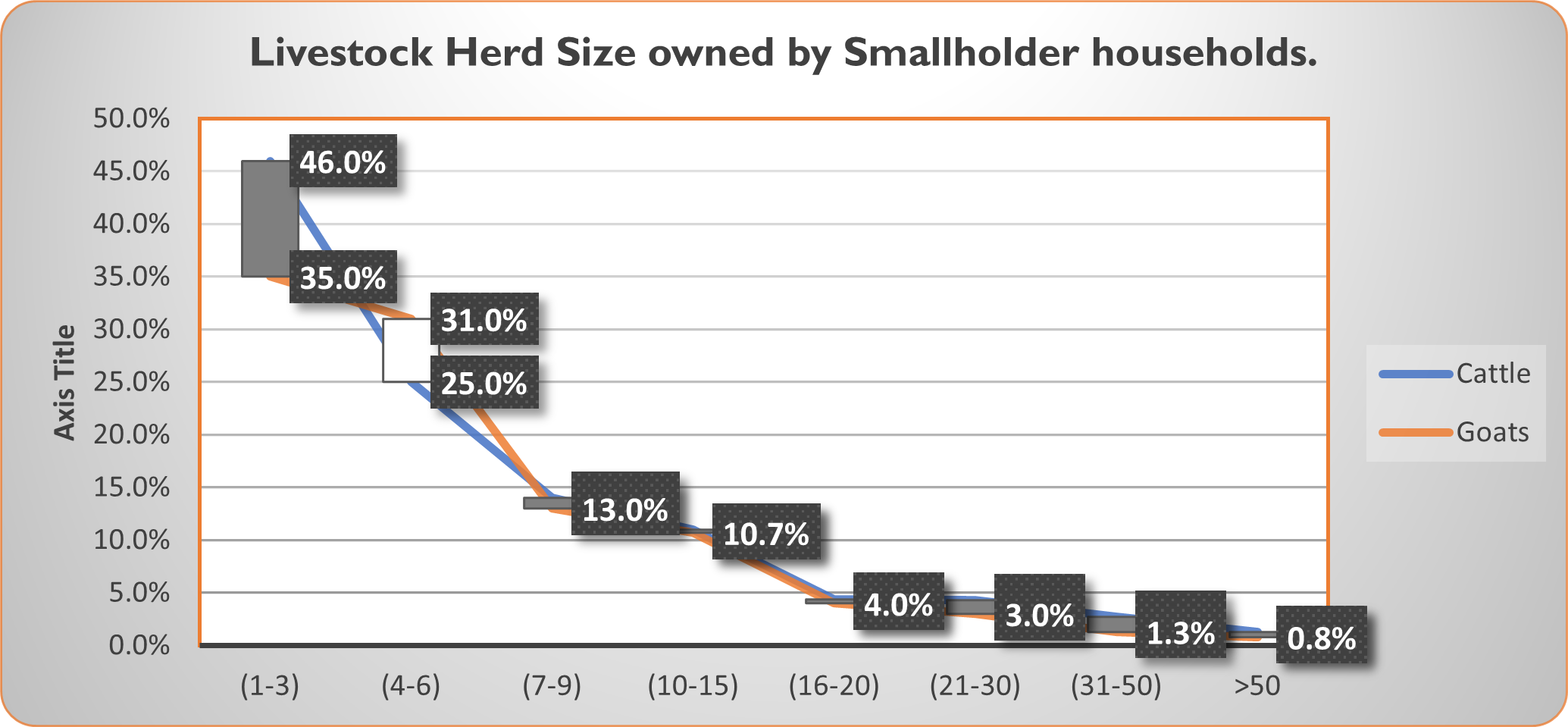

There are about 3,050,000 cattle in Zambia (FAOSTAT, 2014). In 2010, live cattle exports were estimated at $150,000, ($1,297,000 for Zimbabwe) (Rhoda Mofya, 2013). Exports mainly go to Angola and DRC. There are no livestock exports to EU due to failure to meet EU livestock standard requirement. Commercial sector in Zambia holds only 20% of total livestock population. Smallholder sector hold more than 80% of livestock population. According to Rural Agricultural Livelihood Survey (RALS, 2012), majority of Cattle and Goats farmers own between 1 to 3 animals as illustrated below.

Fig. 1. Livestock Herd Size owned by Smallholder households.

Source: (RALS, 2012)

Total milk production in Zambia is estimated to be 263,494,107 litres and only 26% of this is sold to the markets with an average price of 2.4 Kw per litre (RALS, 2012). The major constraint to cattle and goat production is slow growth rate and mortality rates for young animals. The slow growth rate for cattle is estimated to be 1.2% and 7.7% for goats. (MAL et al 2012). In Copper Belt region the mortality rate for cattle is 80 out of every 1000 cattle and 98 out of every 1000 goats (RALS, 2012).

There are about 3,050,408 goats in Zambia (Republic of Zambia, 2012). There are very few commercial goat farmers in Zambia and more than 90% are small scale farmers clustered around the rural and peri-urban communities in the country. There are no formal organized markets for goats and smallholder farmer groups are also fragmented (Lembani, 2022). However, livestock Associations seem to stabilize the marketing of goats in Zambia. An example of such association is (SLAZ). The association is able to provide holding facilities in different areas in Zambia such as Kasumbalesa, Choma, Kalomo etc. Most of goats are traded in Kasumbalesa which is considered as the ‘hub market’ for goats in Zambia. It is bordering town to Democratic Republic of Congo (DRC). Traders go around in Zambia looking for goats from smallholder farmers and then are transported using trucks to Kasumbalesa. Smallholder Farmers also organize themselves and collectively and transport the live goats to Kasumbalesa town.

VALUE CHAIN STUDY APPROACH AND METHODOLOGY.

Value Chain Study is the process for understanding the systemic factors and conditions under which a value chain and its primary actors can achieve higher levels of performance (GLiPHA., 2013). Typically, the aim of value chain analysis is to understand all the major constraints to improved performance or competitiveness – with a focus on end market opportunities. Using a gender sensitive and pro-poor lens, the Goat Value Chain analysis process employed a participatory approach and methodology involving all actors in the value chain.

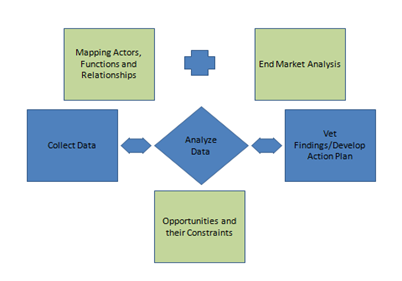

The value chain study entailed three interconnected steps: (1) data collection and research, (2) value chain mapping, and (3) analysis of opportunities and constraints.

The figure on the right illustrates in a simple way the analysis process and components. The mapping process is the mostly important in organizing the data, and highlights the goat value chain market segments, its participant/actors, and their functions and linkages. The collected data was analysed using the value chain framework to reveal constraints within the chain that prevent or limit the exploitation of end market opportunities and participation of poor farmers.

Desktop Research

The desk research involved a rapid examination of readily available material to help familiarize the research team with the goat value chains, the market and the business environment in which it operates, as well as to identify sources for additional information. The team reviewed previous studies in the target area, government publications, policy documents, internal documents, records from private sector players and service providers and other related literature. Information such as statistics on exports/imports, consumption reports, global trade figures, etc, were gathered from the internet (FAOSTA, GLiPHA), phone calls and documents from trade, commerce and industry ministries, professional and trade association newsletters. An initial value chain map was drafted to provide a basic overview of the value chain and to guide the full value chain analysis. The basic map was subjected to further refinement during the primary research phase.

Key informant interviews (KII)

In order to mount an effective quantitative and qualitative data collection process, the key actors in the goat value chain were identified and mapped, and their information analyzed. The key respondents included local government technical officers, actors from all functional levels of the goat value chain such as goat producers, input suppliers, traders and other buyers, value chain supporters and service providers. They were interviewed using checklists and questionnaires designed to gather information on the following: Current capacity of goat value chain actors to learn and innovate; Level of information sharing among value chain actors and where they learn about new production techniques; New markets and market trends for live goats and goat products; Gender dynamics that affect value chain performance; Opportunities and constraints to effective participation of poor goat producers (including women) in the live goat and goat products value chain; The extent of trust that exists among the chain actors; Opportunities and constraints for upgrading the value chain; Missing or inadequate provision of services necessary (such as financial, AI, animal health, abattoirs, cold storage, market information, transport etc), to move the value chain to the next level of competitiveness.

Focus Group Discussions (FGDs).

Focus Group Discussions (FGDs) were applied to generate ideas, to determine differences in opinion between stakeholder groups and triangulate with other data collection methods. The groups consisted of 7-10 people (at least 50% women) performing the same or a similar function in the value chain. The qualitative data gathered by these methods revealed dynamic factors of the goat value chain such as trends, incentives and relationships. To complement this, a quantitative analysis of the chain was performed to provide a picture of the current situation in terms of the distribution of value-added, profitability, productivity, production capacity and bench-marking against competitors. Analyzing these factors highlighted inefficiencies and areas for reducing cost. At least one FGDs was conducted in each of the district. In the markets, the participants included goat producers, suppliers, vendors, consumers and employers (the participation of women was prioritized where possible). In villages, separate FGDs were conducted with women and men (three with women and two with men) and the participants were of mixed gender. The group for FGDs consisted of between 7 to 10 participants.

The Researcher employed the information derived from key informant interviews and FGDs to refine the initial basic map developed from desk research and knowledge at the outset of the data analysis.

Analysis of Opportunities and Constraints Using the Value Chain Framework:

The Researcher also employed the value chain framework as a lens through which the gathered data was organized, analysed and systemic chain-level issues identified to enable a firm-level to a chain-level perspective.

The Value Chain Framework

SOURCE: USAID, Enterprise Development Resources.

The influencing factors affecting performance of the goat & Dairy value chain were subjected to further analysis in terms of offering opportunities for upgrading and the constraints to take advantage of the opportunities. These factors are:

- End markets

- Business enabling environment or chain context

- Vertical linkages

- Horizontal linkages

- Supporting markets (Business services and finance)

- Value chain governance

- Inter-firm relationships

- Upgrading

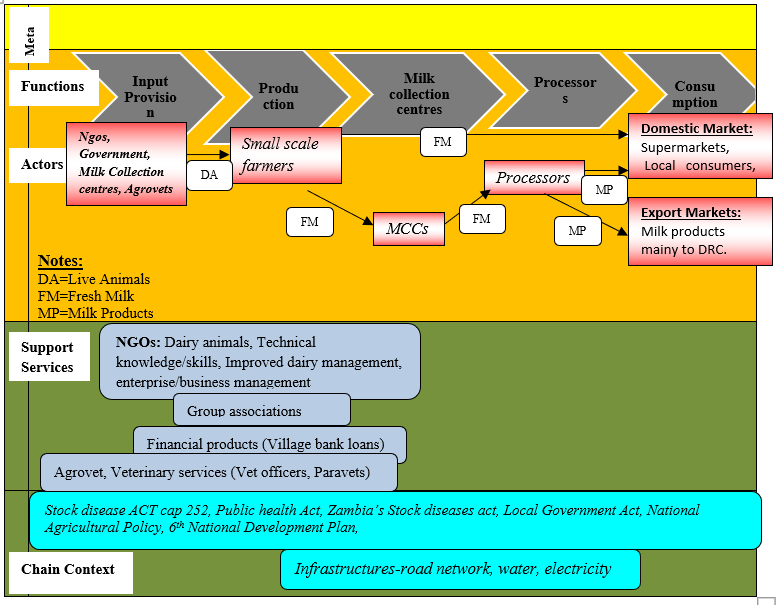

DAIRY VALUE CHAIN (DVC).

The Dairy Value Chain (DVC) study focused on Copperbelt Province focusing mainly on two predominant districts namely; Kalulushi and Mufulira. It was discovered that the dairy industry in Zambia is characterized with processing industries, producing the following products; liquid milk products (pasteurized, UHT, and flavoured milk), fermented milk products (Yoghurt, Lacto – Mabisis), butter, cheese, ice cream and dairy blend fruit juices. Zambia has about 2,500 smallholder dairy farmers affiliated to dairy cooperatives in milk marketing whose capacities in smallholder dairy are being strengthened by resource persons, including materials and financial support mainly from NGOs in collaboration with the Government of the Republic Zambia (GRZ). The per capita milk consumption in Zambia is estimated to be 24 litres per person per year against the recommended level by FAO which is about 200 litres per person per year. In Copperbelt region, the key players in dairy value chain include; Input Providers, Producers, Milk collection centres, local Retailers, Processors and final consumers.

This section analyses key actors across dairy value chain in Copperbelt Province. In each actor, the analysis focuses on; relationships and governance, markets and transactional data, support services, competition, challenges, opportunities and recommendations.

Input providers (IPs) range from NGOs, government line ministries and agrovet shops. Major types of inputs to dairy farmers include; heifers, Antibiotics, de-wormers, Ear tags, Sprayers, Milking salve, tick grease and services from extension workers. There are two major NGOs supplying dairy animals in Copperbelt Province, these include; Heifer International Zambia (HIZ) through Sustainable livelihoods Enhancement project (SLMEP). The main role of HIZ & SLMEP was providing primary input, technical and business development support to the dairy producers in area of operation of Heifer international Zambia play the role as input providers of providing dairy animals, drug kits, milking buckets, milk cans, Social Capita Development and other capacity building related activities etc. They also play the role of service providers, that is training and extension servicers.

Additionally, other input providers include Milk collection centres (MCCs), they are involved in providing: Feeds at subsidized prices to farmers, Bicycles to farmers as a strategy to reach more dairy farmers Aluminium cans, Credit facilities to farmers, Farming equipment and Market information to farmers. Agrovets mainly deal on drugs and feeds. There is no pronounced competition among input providers. In Copperbelt, most of the employees working at these agrovet shops have Grade Twelve (12) certificate plus experience in agriculture or certificate in agriculture. Support services provided to Agrovets include veterinary advice from vet officers. They receive financial support through bank loans. However, they require more business development services such as training on drug administration and financial management.

Input providers constraints

- Unable to reach to far distant smallholder farmers in rural & remote areas of the districts.

- The best dairy breeds are very expensive for the rural smallholder farmers to procure.

- Expensive drugs at the market and few prominent and viable suppliers.

- Lack of technical skills in dairy production among the smallholder farmers.

- Poor information dissemination to livestock producers in the districts.

- Poor road network in some rural- remote areas.

Dairy farming in Copperbelt Province is still low. This has largely been affected by the main activity of the province which is mining. Dairy farming is not common to many smallholder farmers in Copperbelt Province; however, NGOs like; HIZ and SLEP project have come in to supply dairy animals in the region as a step to promote milk industry in the province. This has seen smallholder farmers organize themselves into groups & cooperatives to receive and manage the dairy animals. As a result, smallholder farmers are the first beneficiaries of fresh milk from these dairy animals in the respective districts.

Due to engagement and successful impact of NGOs such as HIZ through SLEP in dairy industry in the region, smallholder farmers were positive and willing to participate in dairy production especially with the current demand of milk in Copperbelt Province. There is also a lot of interest of new emergent smallholder farmers to join the existing cooperatives or groups, for instance, during an interview with Kalindini Dairy farmers in Mufulira there were 31 individuals of whom 7 were non-members. Though many of these farmers are willing to participate in their capacity in terms of management and quality production is still very low. They need advanced training on good animal husbandry management practices, quality handling of milk, safer ways of transporting the milk etc.

However, grazing land for dairy animals is in abundance. No grazing restrictions. Breeds like Jersey and Holstein Friesian are the most predominant in the Copperbelt Province. In some areas such as Mufulira, dairy animals never existed until NGOs like HIZ moved in and introduced the livestock production development projects. Major type of production system is semi-Intensive. Animals are fed with commercial feeds mixed with chicken manure and sunflower cake, and later released to graze freely in the field. Dairy farming in Copperbelt Province is still at its initial stage and most farmers own between 1 to 3 dairy animals. This calls for the reason why employment at production stage is still non-available. The employment is in other cropping activities in the farm and the exchange of payment is giving a few litters of milk to the casual- workers. This presents how milk is treasured by communities in the Copperbelt Province of Zambia.

Support Services

Dairy farmers in the Copperbelt Province purchase services such as; vaccinations, Brucellosis testing, veterinary services, and buy drugs such as de-wormers and Dips. Smallholder Farmers have also received good and suitable management trainings from NGOs and World Vision Zambia (WVZ) such as; HIZ and social development. Some smallholder farmers have been trained as Community Health workers (CAHWs) and these trainings are free services in Copperbelt Province so as to enhance livestock production in the region.

Services required but not yet provided to dairy producers:

- Financial services

- Milk collection services instead of farmers transporting the milk to far located MCCs.

- Linking of smallholder farmers to the viable market in the province.

- Rural electrification (to establish cooling centres specially to reduce spoilage of evening milk).

Market & transactional data.

Milk production per dairy animal ranges as low as 5 litres and as highest as 25 litres per day. The difference depends mainly on degree of management practices applied by different dairy smallholder farmers. The major buyer(s) of milk in the Copperbelt Province is Parmalat. Farmers deliver their milk-to-Milk collection centres (MCCs) where Parmalat collects the milk and transport to their processing plant in Copperbelt Province.

Current trends and developments.

There is one big player in the Copperbelt region and this is the Parmalat Limited. Smallholder farmers have been selling their milk to this company which pays after every one month. This has compelled the smallholder farmers to target the emerging local retailers and traders who have started local business of raw milk in nearby trading centres and towns. This is because they pay smallholder farmers immediately milk is supplied. This has reduced amount of milk supplied to MCCs by farmers and consequently to processors.

Constraints of Smallholder Dairy Producers.

- The major constraints in the Copperbelt region is lack of access to clean water for the livestock and for household use. Smallholder Farmers try digging shallow wells which are collapsing at high rate (soil structures are weak especially in Mufulira District).

- Lack of enough capital for the dairy producers to commence and inject into dairy projects.

- Poor road networks in some parts of Copperbelt Province.

- Dairy feeds too expensive for an average smallholder farmer.

- Transporting of milk from the farms to MCCs with bicycles is also a challenge, sometimes milk pours due to uneven roads.

- Smallholder Dairy Farmers mainly benefit from morning milk. Evening milk most of the times get spoiled (turn into sour- milk) due to poor storing facilities and long distances to MCCs. Morning milk and Evening Milk are transported on different containers. Most of the time Evening milk is rejected by the MCCs in all the districts.

- The pass on program limits ‘potential milk’ that can be supplied by ‘an individual farmer’. Heifer animals delivered by Dairy animals (Supplied by NGOs) are supposed to be passed on to other farmers before the primary farmer could benefit from them. Bulls are not passed on, as compared to heifer animals. This reduces number of ‘milking animals’ per individual farmer.

- Another main challenge which is related to above is biological reproduction of heifers in Copperbelt Province. More bulls are being reproduced compared to number of Heifer animals in the region.

- Lack of sufficient food supplements especially concentrates due to few suppliers.

- Poor veterinary care services in some places such as Mufulira District. There are only three qualified veterinary personnel in Mufulira District.

- Access of dairy animals at an individual level is unaffordable. One has to be a member of a farmer group or a farmer cooperative to benefit through such programs such as Pass On. This is taking too long to increase the number of dairy animals in the province.

Milk Collection Centres (MCCs).

There are six (6) MCCs in Copperbelt Province and these are the following; Fisenge MCC in Luanshya District, Mpatamatu MCC also in Luanshya District, Kwashama MCC in Kitwe District, Chibote MCC in Kalulushi District, Sunridge MCC in Mufulira District, Mtenda MCC in Chingola District. There is one MCC coming up in Ndola District. However, this depicts positive developments in Milk industry in the Copperbelt Province. Milk Collection Centres receive milk deliveries from the smallholder farmers. They do not process or pasteurize milk; their main role involves providing cooling services before milk is delivered to processing and chilling plants. Some of these MCCs were formed by women groups e.g. Fisenge MCC. One MCC unite different cooperatives of farmers. For instance, Fisenge MCC houses 13 different cooperatives. The payment is done on monthly basis. This is because processing plants pay on a monthly basis to MCCs, the same model used by MCCs to pay the smallholder farmers.

The main Off-Takers or buyers of milk from MCCs is Parmalat in the Copperbelt region. Parmalat pays ZMW 2.99 per litre to the MCCs. Smallholder Farmers are paid 2.5 kw per litre. 0.49 remains to run the activities of MCCs, e.g. electricity, staff salary, maintenance etc. MCCs are also obligated to pay some certain amount to Dairy Association of Zambia (DAZ). Some bigger MCCs such as Fisenge handles between 52,000 and 53,000 litres every month. The butter content is examined as per group of smallholder farmers and not per individual smallholder farmer, this locks out serious smallholder farmers in the Copperbelt Province. This is considered unfair as levels of know-how and skills are not equal to all smallholder farmers in a group or cooperative. Some smallholder farmers could be practicing proper animal management practices and quality production of milk from their animals could be higher than others, but this is absorbed away when milk is mixed into one container. The butter content is categorised into 3 grades, and each grade has its own selling price.

Fig. 2. Grade & Selling Price.

Source: field data.

Other Services offered by MCCs in the Copperbelt Province.

The following are other services provided by the Milk Collection centres in the region:

- Feed services to small farmers as most farmers deliver milk through bicycles. They buy the feeds at subsidized prices from the service providers and carry them back home using the same bicycles. The MCCs collaborate with millers to be able to sell the feeds at a lower price than the feeds suppliers.

- Bicycles to smallholder farmers. MCCs are trying to reach as many smallholder farmers as they could. One of their strategies includes providing bicycles dairy farmers, targeting those benefiting from pass on HIZ programs in each respective district.

- Aluminium cans. MCCs are aggressively involved in a campaign to sensitize farmers on good quality handling and better ways of transporting the milk. Plastic containers used by farmers are replaced by aluminium cans.

- Credit facilities to smallholder farmers in the province to enhance their dairy businesses in districts.

- Farming equipment for farm management which includes livestock production in their respective districts.

- Market dissemination information to smallholder farmers. Currently, smallholder farmers go through MCCs, if they want to buy farming equipment to seek market prices before they purchase.

Constraints encountered by the MCCs on the Copperbelt Province:

The following were discovered to be the main challenges experienced by the MCCs in the districts:

- It is difficult to measure butter content per individual farmer due to mixture of milk per group of farmers before being delivered to the MCC. The butter content is therefore measured per group of farmers and not per farmer.

- Farmers who benefit from other services such as Feed services are those located near an MCC. Those in far places are left out.

- There is only one main buyer of milk from MCCs in the Copper Belt region, the Parmalat ltd. This has seen prices of raw milk remain constant for so long in the region.

- MCCs depend on the processing companies to supply the chilling machines. The charges are deducted from the money paid to MCCs. Mostly the supplied machines are of low capacity and of poor quality leading to high maintenance costs, which becomes a huge cost to the farmers.

- Some farmers are located into far distant areas and MCCs have not yet managed capturing all farmers in Copperbelt Province.

- MCCs mainly depend on morning milk as it is delivered when it is still fresh. Evening milk is mostly rejected due to sourness.

Trends of the Value Chain Actors in Copperbelt Province.

- Retailers

Milk retailers include local restaurants & hotels who buy raw milk directly from farmers and local traders who sell raw milk in the streets, trading centres and in towns. They buy milk directly from farmers and this poses challenge to bigger processors who also depend on the same milk from these farmers. This is a developing trend in Copperbelt Province as farmers prefer selling to these vendors due to their timely payment. These buyers may be buying milk at a lower price than the bigger processors but farmers still supply to them as they pay immediately.

The major processor in the Copperbelt Province is a sub branch of Parmalat which headquarters are based in Lusaka. The plant employees around 50 permanent employees. Currently the company handles between 18,000 – 20,000 litres per day which is below their target (25,000 – 30,000 litres per day). The deficit is mainly linked to insufficient supply of milk in the region and that some farmers are located far away from the Milk Collection Centres. The main products from the processor include; Yoghurt, fruit drinks (Cabana), processed fresh milk (morning fresh) etc. As they process products, they take into considerations consumer concerns which include; packaging, prices and expiry dates.

Around 90,000 litres of milk are transported to Lusaka every week. 40,000 litres remain in the Copperbelt Province plant for processing. Part of the milk may be delivered back as finished products e.g. cheese and butter which currently are not produced from Copperbelt branch. They get raw milk from six Milk Collection Centres and some few individual farmers. The company buy milk depending on the butter fat content; the best price is ZMW3.00 per litre (class A). Smallholder farmers through MCCs have an agreement with the company, a 5 years deal. The agreement stipulates the requirements such as: Cows must be free from diseases e.g. TB & Brucellosis, Butter content to be above 3.2%, No adding of water to milk delivered to the MCCs etc.

- Cross-Border Trade (CBT).

The processing companies export their products to countries such as Democratic Republic of Congo (DRC). Parmalat (Z) Limited exports about 1 billion valued products directly from Copperbelt Province every year. Major products exported come from Lusaka Province.

KEY COMPETENCIES:

- Production of the dairy quality products on the Copperbelt Province

- The company name is self-selling (which is Parmalat (Z) Limited).

- Use of Parmalat agents in all towns and trading centres to maintain availability of Parmalat products to all customers. Use these agents to reach small markets

- Constant supply to major supermarkets

Current trends and developments on the Copperbelt Province.

In Copperbelt Province, there is lack of sufficient milk supply. The emergence of local trading in raw milk has seen reduction of milk delivered to MCCs. There are also other more companies coming in to the milk industry such as Pepsi & ZaMilk. These developments have seen increased competition on milk delivered from the smallholder farmers. Since processing companies such as; Parmalat pay farmers on a monthly basis, local traders who deal on raw milk are winning the competition by paying farmers immediately milk is delivered to the selling points.

Products distribution.

Milk is delivered by smallholder farmers to the MCCs. Parmalat (Z) Limited collect milk using tankers. The raw milk is transformed into finished products such as Yoghurts, fruit drinks, fresh milk etc. The plant has a packaging store where the products are stored before taken to the distribution centre. Bigger markets such as supermarkets make their orders from the distribution centres. From the distribution centres, the products are supplied to agent containers in different towns. These agent containers are strategically placed to target populated areas. These kinds of product distribution channels ensure that the milk products are taken closer to customers, reaching all kind of buyers small or bigger buyers. The distribution has its own challenges such as;

- Sometimes the refrigeration systems of the trucks fail which affects the recommended temperature during transport, which should be at 40

- Break down of trucks during transport leading to delay in delivering the products

Competition.

In the past competition in milk industry in the Copper belt was docile. Currently, the emergence of companies such as Pepsi & ZamMilk which are also interested in the milk industry and local trading on raw milk has seen some competition in the region. However, Parmalat (Z) Limited still controls more than 75% of the market share in Copperbelt Province. This is because they operate on contracts and this contracts limit farmers from diverting the milk to the street and to the competitors. There are Cooperative Boards in all MCCs that oversee the milk deliveries in their respective districts.

Processors Challenges.

- Lack of sufficient power back up that can support the plant processing during power black outs.

- The breakdown of machines is rampant as many of them are old. They were shifted from older plant of Lusaka.

- Insufficient milk supply.

Potential of Dairy Sector in the Copperbelt Province.

- The number of dairy animals in the region is still low presenting an opportunity for both small scale and commercial farmers.

- The region is located at the border between DRC & Zambia. The lawlessness in the neighbouring DRC, see no farming activities and they depend largely on Copper Belt for food.

- There is high demand of Milk in the Populated town of Lubumbashi in DRC around 40 kilometres from Chililabombwe and as well in Copperbelt Province.

- The emergence of local trading in raw milk and coming up of companies such as Pepsi & ZamMilk present a huge opportunity in demand of milk in Copperbelt Province.

Fig. 2: Dairy Value Chain Mapping.

GOAT VALUE CHAIN.

Background.

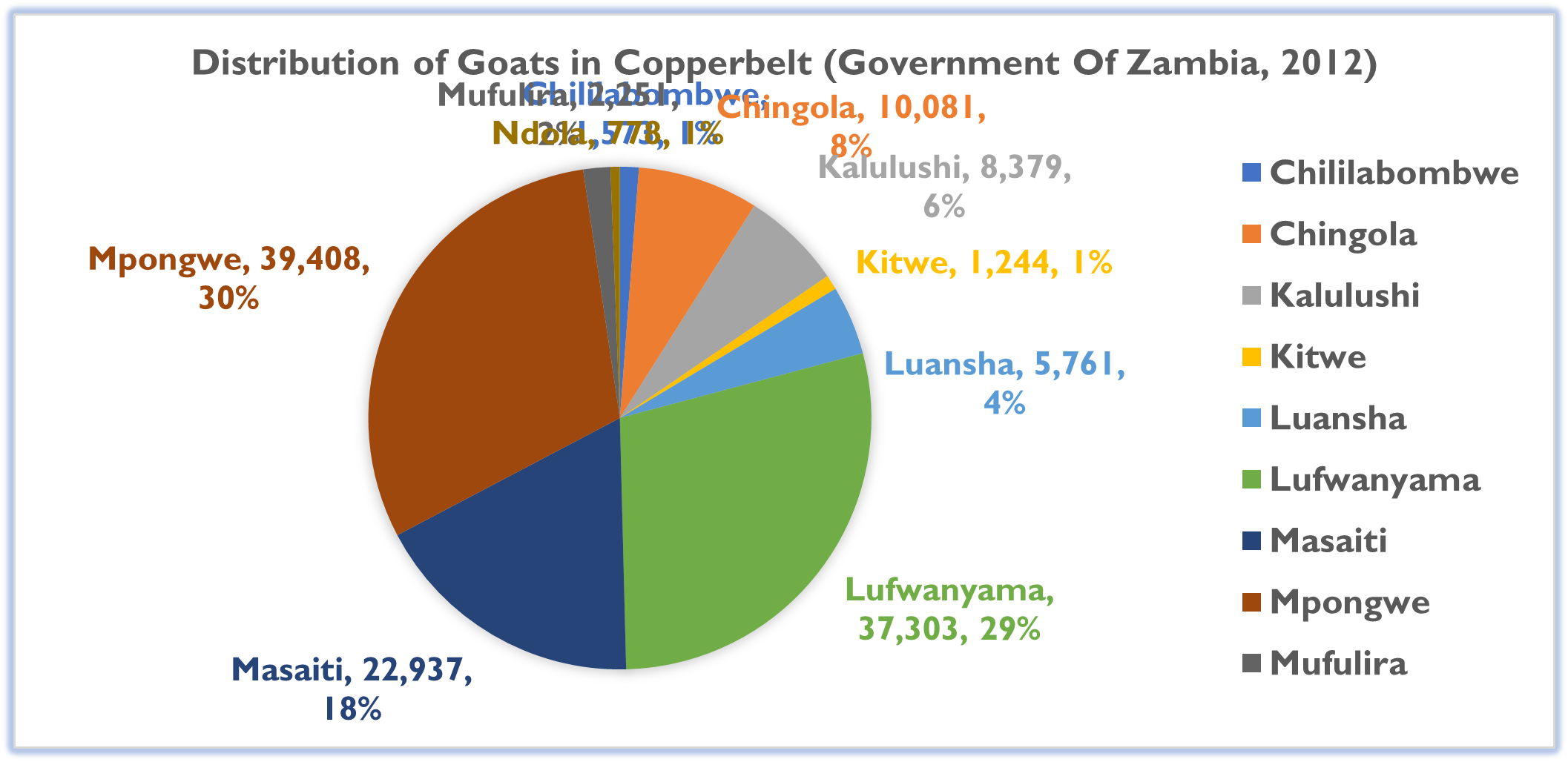

In Zambia there are about 3,023,585 goats. Goat production in Copperbelt Province is still low, sharing only 4.3% of total goats produced in Zambia. Copperbelt Province is among the least goat producers in Zambia with a total of around 129,715 goats (Government of Zambia, 2012), second lowest after Western Province. Goats can play a major role in improving the economy of rural households if the production and marketing is supported but usually, there is less consideration given to the goat subsector by the farmers, government and other stakeholders. Despite the industry being faced with a number of challenges including inadequate expertise in processing, goat has vast potential of contributing to not less than 40% as a source to the rural population in the country.

Fig.3. Distribution of goats on the Copperbelt Province.

Results & Findings.

This section analyses key actors across goat value chain in Copperbelt Province. In each actor, the analysis focuses on; relationships and governance, markets and transactional data, support services, competition, challenges, opportunities and recommendations.

Input providers in goat value chain are similar as those in dairy value chain involving; NGOs, Government and agrovets. Goat industry is new in Copperbelt Province, therefore the input provision especially from Agrovets is seasonal which include; dips, de-wormers, etc. Farmers buy these inputs mainly between September to November in each year. Major challenges to Input providers in goat value chain include; Unable to reach to far- flung or distant smallholder farmers, drugs overstaying on shelves, low- drug technical know- how of the smallholder farmers, lack of better follow ups on diseases occurrences (farmers seek help only when animals are unwell or have contracted diseases), low capital, some smallholder farmers may be unaware of an existing veterinary shop, lack of better business development services among others.

Goat farmers are mainly organized into groups, especially women groups. Most of these groups were formed during receivership programs from Ngo’s such as Heifer International. These groups later were retained and registered by registrar of societies in Zambia. Some groups went ahead to include all members of a family, such that membership is in terms of a family and not in terms of individual members. For instance, “Go Women Go” group in Mpongwe District has 20 family members with an average of 8 to 13 goats per family. The group has got around 450 goats in the area.

Land ownership is facilitated by government. Most farmers receive land permits from Traditional Leaders who are chiefs, that is, given by government. Most small-scale farmers own between 20 ha – 50 ha. Grazing is done freely with no restrictions. Fodder preservation is prepared from ground nuts husks, maize stock, preserved grass etc. The major types of breeds are the boar crosses and the local Zambian goats. Semi Intensive type of production system is the most common, where goats are fed in cages and later released to graze freely in the field.

Support Services.

The common services that smallholder farmers seek for are drug administration for their goats. The common drugs bought from agrovet shops include; antibiotics, dips and de-wormers. The farmers pay ZMW 2.50 per goat on drug administration. The smallholder farmers receive financial support from their own village banking and credit facilities. Others services required by farmers include; training on feed supplementation, marketing, entrepreneurship and efficient veterinary services.

Markets and Transactional Data.

Farmers have no definite plan on goat production. They sell randomly when in need and if the goats are ready for sale. Major costs of production include; buying drugs, salts, drug administration costs etc. One goat can sell as high as ZMW 750 at agricultural shows and as low as ZMW 150 when sold to local traders and smallholder farmers desperate to sell their goats to would be clients.

Currents trends and developments.

The prices of goats from farmers are increasing. Events such as Agricultural shows are now the best opportunities for goat farmers in Copperbelt Province. Smallholder farmer groups such as; ‘Go women Go’ have already started taking advantage of such market opportunities.

Relationships & Group or Cooperative Governance.

Most smallholder goat farmers or producers in Zambia are organized into cooperatives or groups; however, there are those who operate individually in various communities. Lack of formal contracts between the buyers (Off- Takers) and the smallholder farmers present challenges to the farmers as they lack market information services. Mostly, they do not know at what price to sell their goats. Goat industry in Zambia does not have stiff competition (Lembani, 2022).

Structure of Producer Groups.

| STRUCTURE: | ROLES &RESPONSIBILITIES: |

| Chairperson (Group CEO) | Organize members and oversees all activities in the group |

| Vice chairperson | Assist the chairperson of the group |

| Group Secretary | Records group activities, minutes preparations |

| Vice- Secretary | Assist Secretary in the day to day note taking of the meetings. |

| Group Treasurer | Group financial management |

| Works Committee | Supervise construction of sheds |

| Disciplinary Committee | Conflict resolutions, and ordering punishment in terms of fines |

| Social Committee | General welfare of the group members |

| Finance committee | Mobilise funds and organize sources of capital to new members |

| Animal Health Committee | Paravets – in collaboration with government extension officers, they look after the health status of goats in a group |

| Group Members | There are no threshold limits to numbers of members who can join a group |

Goat Production Challenges.

- Goat diseases and high infestation levels in diverse communities.

- Inbreeding is high due to open grazing unable to trace mating (There is no control of inbreeding).

- Treatment challenges. Veterinary personnel are not readily available. Paravets officers in the communities are just volunteers and lack of incentives makes them inefficient.

- Lack of bulking or aggregation, due to insufficient number of goats to sell to distant markets.

- Input suppliers located in distant areas and mostly in urban or peri-urban areas (Not in rural areas.

- Fragmented smallholder farmer cooperatives in the districts and this results into lack of strong bargaining power or voice during goat sales to Off- Takers.

- Lack of enough capital to start viable goat farming as a business in the region.

- Other farming activities reduce concentration time needed in goat farming.

- Poor husbandry practices. Poor nutrition to goats, lack of feed supplementations (Poor animal management).

- The traditional mindset of farmers, where they still believe in large animals such as cattle as a way to value their wealth and also smallholder farmers still keep goat for prestige purposes.

- Many scale farmers are yet to realise the potential in small ruminants such as goats among others.

- Poor housing structures in rural areas or villages (Mostly goats spend nights outside the structures).

- The flow of market information to farmers is non-available in most of the rural districts even in peri-urban areas.

- Visual determination of prices leads to unhidden losses to both the smallholder farmer and the trader (or the buyers).

TRADERS & TRANSPORTERS:

There are two categories of traders in Copperbelt Province and these are; Local traders and Bigger Goat Traders.

Local traders: are also referred here as small traders. They sell as low as less than 10 goats per week and these local traders target local markets, butcheries, and restaurants. They also supply to bigger traders who target big goat markets in the province.

Bigger traders: Bigger traders handle large number of goats more than 500 to 1000 in a week. Majority of bigger traders in Copper Belt transport live goats from various parts of the country to Kasumbalesa town. Some of these bigger traders are also goat farmers and easily mobilise other small-scale farmers to sell to them.

MARKET AND TRANSACTIONAL DATA.

Bigger traders are able to sell live goats at a profitable price than small traders. They are able to sell between ZMW 600.00 to ZMW 1500.00 per live goat, while small traders sell between ZMW 150.00 to ZMW 250.00 per live goat. Bigger traders are able to sell goats from far distant areas e.g. Kasumbalesa in DRC around the corridors, while local traders depend on the local butcheries, restaurant, retailing areas as their main market.

Current trends and developments

The market for goat milk is growing especially in Copperbelt Province where main economic activity is mining and the supply milk from other sources such cattle is still low. Kasumbalesa town has grown to be the market hub of goats in Copperbelt. There are lucrative prices at Kasumbalesa as most of the buyers are from the DRC.

Cross-Border Trade (CBT).

In Copperbelt Province, CBT mainly takes place in Kasumbalesa a border town with DRC. This town presents a huge opportunity for the region. Bigger traders transport the goats to this town by use of Lorries after buying goats within and outside the Copperbelt Province.

Goats being ferried to Kasumbalesa town

The main reason why Kasumbalesa town is the major hub for goat market is because of the highly populated town called; Lubumbashi town just around 25 kilometres from Kasumbalesa. Due to lawlessness that has existed over the years, farming in DRC has been docile and this transformed Kasumbalesa as the main Hub for food entry into DRC. Thousands of goats are entering into DRC every day through this town. Traders and business persons from DRC come to this town to buy live goats and transport them to Lubumbashi town. The prices of live goats are quite lucrative, a live goat can fetch up to ZMW 850.00 per goat and above.

Small livestock association of Zambia (SLAZ), has built a holding facility in Kasumbalesa town, where goat traders offload their animals and feed them as they wait to be crossed to DRC for slaughter. The goat market is normally flooded between November to February every year. At this period the demand of goats from DRC are accomplished. The supply of goats to Kasumbalesa goes down between May and July annually. This is because, at this time, smallholder goat farmers have harvested other food crops and are not willing to sell goats from their farms. They see no need as they have money. At this period the demand of goat meat to Congo increases and the prices shoots to over ZMW1000.00 per goat.

Competition.

Competition is mainly between local traders. They compete with each other to sell to restaurants, hotels, retail centres. They also receive stiff competition from retailers who own butcheries as they also source the goats from the same farmers.

Support services: Traders have no access to business development services.

Trader constraints.

- High transport costs.

- Police harassment during transport despite having proper documents.

- Lack of organised formal goat markets in the Copperbelt Province.

- Insufficient capital especially for local traders.

- Middle men who exploit local traders and have no bargaining power to negotiate for better prices.

- The small sizes of goats are attracting poor prices and this is mostly a loss to the smallholder farmer.

- Local traders cannot dictate the selling price especially when selling to butcheries.

- Poor road network in some areas. Difficult to transport goats especially during rainy season.

- Unable to detect actual health of an animal before transport. Some found dead after transport though looked healthier before being ferried.

- Local traders sometimes make losses as the carcass weight weighs less than expected due to visual determination of prices when buying from farmers.

- There is lack of transparency and poor flow of information in the goat value chain. Traders have no idea what happens to other products such as skins after they sell the live goats to off-takers.

There are many retailers that own butcheries in most of the towns of Copperbelt Province. Others operate roadside roasting of goat meat. Retailers source goats from local traders, but some link up with producers to supply them with goats. They mainly deal in goat meat. Other products such skins are seen as of no value to many traders in Copperbelt Province.

Markets and transactional data.

The retailing business picks in Copperbelt Province during the harvesting season when cash flow is high unlike traders whose business go down when cash flow is high as many farmers are not willing to sell their goats. What is worth noting is that some retailers in Copperbelt Province does not sell goat meat per Kg, rather in pieces. Measuring of meat is only done by those retailers who own butcheries in towns. Thus, the competition among retailers is still very low.

Support services

Business Development Services (BDS) such as; technical, communication, and financial support are not available to many retailers in Copperbelt Province.

Retailer challenges

- Lack of goat abattoirs, slaughtering is mainly done in backyards

- Lack of access to larger markets e.g. supply to institutions.

- Some of the retail centres are not to standard, they lack refrigeration facilities etc.

- Shortage in goat supply when demand is high. During harvesting season.

Goat processing is not common in Copperbelt Province. The existing meat processors concentrate mainly on beef, for instance Zambeef. Other products such as goat skins are sold to bigger processing companies such as ZamLeather unit, though at a small scale as large quantities of goat skins are thrown away.

Potential of Goat sector in the Copperbelt Province.

Copperbelt Province has a competitive advantage when compared to other regions especially on cross border trading as it houses Kasumbalesa town, ‘the hub of live goats trading in Zambia’. According to (Government of Zambia, 2012) Copper Belt region produces only 4.3% of total goat production but more than 90% cross border trade are carried through Copper Belt.

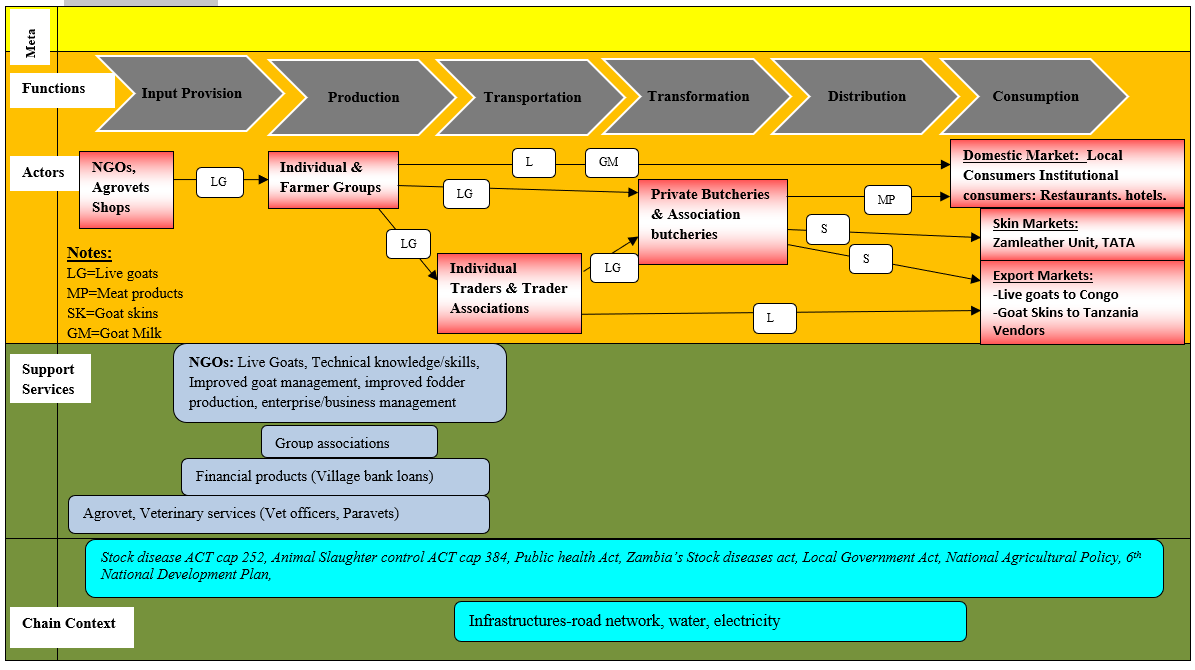

Fig. 4. Goat Value Chain.

PRIVATE SECTOR STRATEGIES, CONCLUSION & RECOMMENDATIONS

Strategies for Attracting Private Sector to Invest in Dairy & Goat Value Chain.

- Raising awareness that there exist opportunities in goat value chain through organising business opportunity seminars where private sectors are invited for engagements.

- Deliberate efforts to link small scale producers to private sector (Market linkages).

- Increasing goat population to meet thresholds orders from private sectors.

- Introducing dairy mapping where private investors will be able to track location of farmers, collection points, delivery routes, and nearest MCCs.

- Improvements in meat quality through cross breeding and proper nutrition.

- All actors in value chains should understand the private sector’s position and why they operate that way before rigorous engagement.

- Private sector participation in programs targeting small scale sector to be able to understand their concerns/issues way before program implementation. This will ensure the sustainability even after the donors withdraw their support.

- Establishing the entry points for them. For instance, Private processing an entry point for private sectors to goat value chain in Zambia.

- Increasing the competition by value addition on products would attract more private sectors.

- Organising farmers into groups would increase the trust and confidence of the private sectors on production sustainability.

- Facilitating value chain information to business minded groupings and developing business plans.

- Putting up high standards for goat slaughtering facilities in the districts.

Goat and dairy value chains face various challenges in Copper Belt as outlined in the results & findings sections. This is attributed to lack of experience, awareness and proper skills of the players more so at production level, as these ventures especially dairy value chains are completely new to some of areas in Copper Belt region. In some areas such as Mufulira, no dairy animals existed before NGOs intervention in distributing through pass on programs. Both goat and dairy value chains are highly appreciated ventures with more farmers willing to participate in the pass on programs. Heifer International Zambia and SLEP have sent positive impacts to the communities in Copper Belt and these has seen a growing interest to the new farmers who are willing to form producer groups or join the existing groups. Though many of these farmers are willing to participate their capacity in terms of management and quality production is still low. They need advanced training on good management practices (GMPs), quality handling of milk, safer ways of transporting the milk, live goats etc.

Competition in both dairy and goat value chains is still silent in Copperbelt Province. However, the upcoming of other companies in the milk industry such as Pepsi & ZamMilk and emerging local traders, has provoked the sector. These developments have seen increased competition on milk delivered from farmers to processors. Local traders who deal on raw milk are winning the competition by paying farmers immediately milk is delivered. However, Parmalat (Z) Limited still controls more than 75% of the market share in Copperbelt Province. In goat value chain, competition is mainly between local traders. They compete with each other to sell to restaurants, hotels, retail centres. They also receive stiff competition from retailers who own butcheries as they also source the goats from the same farmers. The competition among retailers is still low. Most of key actors in both dairy and goat value chains operate on individual basis with no bound relationships. This presents a huge gap in flow of information, and Business Support Services (BSS). Only producer relationships seem to exist with farmers operating in a group. These groups are motivated by pass on programs facilitated by NGOs where farmers form groups to receive goats and dairy animals. The producer group structures involve; Chairperson, Vice chairperson, Secretary, Vice secretary, treasurer, committee members, and members.

The actors in the value chain purchase different products and services. Input providers seek veterinary advices and diseases occurrence info from vet officers. Producers are more interested with drugs, feeds from agrovets and training on good management practices from NGOs. Traders and retailers purchase products such as bicycles, transport services, ingredients for value addition such as tomatoes, cooking oil, plastics, chilli, pepper, onions etc, & electricity, they access these services and products from wholesalers and retailers. Processors have the highest capital-intensive products and services they purchase. They range from manufacturing machines to purchase of human manpower. These services and products are paid inform of cash. Only processors mentioned credit form of payments.

The potential risks in dairy and goat production in Copperbelt Province include; livestock theft, disease outbreaks and lawlessness in the border between Zambia and DRC. Operating in producer groups and community policing in collaboration with government police would control livestock movements and consequently reduce livestock theft. Producers need to work closely with veterinary and agrovets in frequent health checks of their animals to reduce disease outbreaks. The lawlessness in the border between Zambia and DRC especially in Kasumbalesa town where most of livestock trading takes place is difficult to predict due to political mutation in DRC. Since this is the major point of CBT of livestock from Zambia to DRC, farmers and traders in Zambia need to establish an “intelligent network” between the buyers in DRC to be sending signals of such lawlessness to reduce deaths reported as animals especially goats die due to prolonged delays in transport. This calls for trader associations or to work with already established associations such as SLAZ.

Consumers’ quality concerns are diverse. In dairy value chain the quality issues revolve around well packaging to avoid contamination, they are also concerned with fair prices and most importantly expiry dates of milk products. In goat value chain, consumers are more concerned with the places where slaughtering is done, the standard of the butcheries where goat meat is sold, some are highly infested with houseflies. The handling of meat is also another major concern. The other critical concern is how the meat is kept if not sold within the first 24 hours, some of places lack refrigeration and this shrinks loyalty of buyers to these butcheries.

The demand of milk in Copperbelt Province is far much high than the current supply. For instance, Parmalat (Z) limited are supplied with only 18,000 – 20,000 litres per day which is below their target (25,000 – 30,000 litres per day) a deficit of more than -30.9%. The emergence of local trading in raw milk has seen reduction of milk delivered to MCCs. There are also other more companies coming in to the milk industry such as Pepsi & ZamMilk. These developments have seen increase in demand of milk in Copperbelt Province. In goat value chain the supply-demand system is different. The market is normally flooded between November to February every year. At this period the demand of goats from DRC are met. The supply of goats to Kasumbalesa goes down between May and July annually. This is because, at this time, farmers have harvested other food crops and are not willing to sell goats from their farms. They see no need as they have money. At this period the demand of goat meat to Congo increases and the prices shoots to over ZMW1000 per goat.

| DAIRY VALUE CHAIN | |

| Input Providers |

|

| Dairy Production |

|

| Milk Collection Centres (MCC’s) |

|

| Retailers |

|

| Processors |

|

| GOAT VALUE CHAIN | |

| Input Providers |

|

| Goat Producers |

|

| Traders/ Transporters |

|

| Retailers |

|

| Processors |

|

REFERENCES:

- D.H. Hill. (1983). History, epidemiology and economic significance of PPR in West Africa and Nigeria in particular. Retrieved April 04, 2014, from Peste Des Petits Ruminants (PPR) in Sheep and Goats: http://ilri.org/infoserv/Webpub/fulldocs/Peste_des/History.htm

- Ensminger M.E, R. P. (1986). Sheep and Goat Science, Fifth Edition. Danville, Illinois: The Interstate Printers.

- FAO. (2005). LIVESTOCK SECTOR BRIEF, MALAWI. Food and Agriculture Organisation of the United Nations.

- FAOSTAT. (2014). Food and Agricultural commodities production, by countries. . Retrieved January 12, 2014, from Livestock Primary: http://faostat.fao.org/site/569/default.aspx#ancor

- FAOSTAT. (2014). Food and Agricultural commodities production, by countries. Retrieved January 12, 2014, from Livestock Primary: http://faostat.fao.org/site/569/default.aspx#ancor

- GLiPHA. (2013). Global Livestock Production and Health atlas. Retrieved 01 12, 2014, from http://kids.fao.org/glipha/

- Government of the Republic of Zambia. (2012). Zambia’s Livestock Population 2012 census.

- Kaumbata, W. (2009). ANIMAL DISTRIBUTION, PRODUCTION AND CONSUMPTION TRENDS OF ANIMAL PRODUCTS IN MALAWI.

- Livestock in Malawi. (n.d.). Livestock in Malawi – Livestock regulation. Retrieved April 05, 2014, from http://livestockinmalawi.page.tl/Livestock-regulation.htm

- Mahmoud Abdel Aziz. (2010). Present status of the world goat populations and their productivity. Lohmann Information , Vol. 45 (2) Page 42.

- RALS. (2012). Rural Agricultural Livelihoods Survey. REPUBLIC OF ZAMBIA Central Statistical Office.

- Republic of Zambia. (2012). Zambi Livestock Population Census. Ministry of Agriculture and Livestock, Department of Livestock.

- Rhoda Mofya, M. L. (2013). THE LIVESTOCK SECTOR IN ZAMBIA PRODUCTION TRENDS, CONSTRAINTS AND POLICY RECOMMENDATIONS. LUSAKA: IAPRI.

- SADAFF. (2011). Profile Of The South African Goat Market Value Chain.

- Wilson Kaumbata. (2009). ANIMAL DISTRIBUTION, PRODUCTION AND CONSUMPTION TRENDS OF ANIMAL PRODUCTS IN MALAWI. .