Study of the Effect of Fintech on The Financial Efficiency and Productivity of Omani Commercial Banks

- Zainab Mohammed Alsariri

- Marya Hassan Al-Balushi

- Ahad Nasser Almalki

- Zamzam Ismail Al Tubi

- 105-115

- Jun 30, 2024

- Economics

Study of the Effect of Fintech on The Financial Efficiency and Productivity of Omani Commercial Banks

Zainab Mohammed Alsariri, Marya Hassan Al-Balushi, Ahad Nasser Almalki, Zamzam Ismail Al Tubi

Oman College of Management and Technology, Oman

DOI : https://doi.org/10.51584/IJRIAS.2024.906009

Received: 08 April 2024; Revised: 28 May 2024; Accepted: 01 June 2024; Published: 30 June 2024

ABSTRACT

Progress in the use of financial technology has become an important matter in the development in the use of digital technology and the revolution that has occurred in the field of financial transactions in recent years. As financial technology makes people easier and faster. Therefore, through this research, discuss the impact of financial technology on the financial and productive materials of Omani banks. This study is analyzing cum exploratory in nature as it assessed the information and data obtained from the financial statements of the five banks in the Sultanate of Oman, which are the Bank of Muscat, Dhofar Bank, Sohar Bank, Bank Nizwa and Oman Arab Bank. The financial statements for the banks list that was chosen for the year 2018 to 2022. From the research and through the previous technologies It was noticed that the banks used are seeking to provide easy and quick experiences that facilitate the customer to do his transactions without the need to do several operations, as all previous technologies all seek to be all safe and secret transactions and this indicates Financial technology is safe and does not threaten the impact of financial technology on improving the productivity and financial efficiency of Omani banks plays an important role in improving the productivity and financial efficiency of Omani commercial banks. It has helped streamline operations, enhance customer experience and provide innovative solutions. security of the banks and the entities that it uses.

Key words: FinTech, efficiency, productivity, and banks.

INTRODUCTION

Background of the study

FinTech, short for Financial Technology, a type of software or mobile application that makes it easier for consumers or businesses to conduct financial transactions, is the use of technology to provide new and improved financial services. When FinTech emerged in the 21st century, the term was initially used to refer to technologies used in the backend systems of established financial institutions such as banks. Between approximately 2018 and 2022, there was a change towards consumer-facing services. Fintech now encompasses a variety of sectors and industries such as education, retail banking, fundraising and non-profit organizations, and investment management, to name a few (Radixweb, 2022).

Banks are using Fintech for back-end processes – like monitoring account activity behind the scenes – and for customer-facing solutions, like the app you use to check the account balance. Banks also use Fintech to secure loans. Individuals are using FinTech to access a range of banking services, including paying for purchases with their smartphone and receiving investment advice on their home computer. Fintech also automates many services used by businesses, such as lending and property valuation. Artificial intelligence, combined with great amounts of consumer data, is helping FinTech companies understand their customers and advance their marketing campaigns, product development and underwriting. This innovative concept entails a new financial model, by which technology serves as the carrier to provide various financial services, which includes financial management, and financing through online platforms, mobile payments, cloud computing, and other emerging technological means. In addition, it reduces the banks operating costs and improve the banks work efficiency. It strengthens the banks risk control and promotes the intelligent and digital transformation of traditional banks. Therefore, the use of financial technology by traditional banks can improve competitiveness and profitability. (Hanna Shnaider, 2023).

Problem Statement

Financial innovations have contributed to raising the efficiency of the banking sector by improving Services provided to customers, besides financial technology it can be able to change traditional concepts for the banking sector to financial technology. Most important thing is to know how financial technology can affect the Omani commercial banks productivity and efficiency. It is important to use financial technology to help in building a better economy so that the Omani banks need to adapt this kind of financial technology to achieve better results. As well as follow up on risk and fraud that the facility may face through Fintech platform. Furthermore, it helps to achieve faster growth of financial organizations and expand business by providing new services to customers. Also, Fintech is a cost-effective alternative by utilizing technology and its prospects. In doing so, it helps to avoid spending money on labor costs. Moreover, to maintain high operational efficiency in for banks and other financial institutions is to enhance the business growth and expansion of the organization by Fintech it helps in managing resources efficiently and find effective ways to utilize financial accounting information (Muia, S.W. 2017).

Study questions.

Q1: What is the effect of the two elements of FinTech (application and Deposit and transfer machines (on the that Omani commercial banks?

Q2: Will FinTech contribute to enhancing the security aspects of Omani commercial banks?

Q3: What are the most important products that financial technology can provide?

Objectives of the study

The primary objective of this research is to study whether technology will help increase productivity and contribute to developing financial efficiency in Omani commercial banks and seek to develop the Omani economy and market.

The specific objectives of the study are:

- Study the elements that enable Omani commercial banks to use FinTech.

- Evaluate whether FinTech contributes to enhancing the security aspects of Omani commercial banks.

- Analyze the most important products that financial technology can provide.

LITERATURE REVIEW

- Mohammed Almashhadani1 & Hasan Ahmed Almashhadani2 1Department of industrial Engineering, University of Houston, United States (2023), Searching for them (Return on Assets and Return on Equity) revealed the results and statistics of the banks. A high correlation level was developed in the banks to deal with the distinct validity after the criteria were applied and the banks’ validity was assessed. We have received positive and remarkable hypotheses and outcomes for the Fintech of Banking performance. This study found that the use of fintech has improved the banking performance of foreign banks in the UAE. This study also discovered that as the number of electronic financial services offered to customers’ increases, sodoes the performance and quality of banks.

- According to, Nashwa Ibrahim Muhammad (2022), this study aims to evaluate the effects of financial technology on the operational effectiveness of commercial banks in Egypt using data envelopment analysis for 20 banks, which are broken down into 7 government banks, 3 Islamic banks, and 10 mixed banks (private, Arab, and foreign). According to the three models used in this study, commercial banks had the best efficiency, followed by Islamic banks, and mixed banks due to their low relative efficiency.

- Kwee KimPeong, Kwee Peng Peong2, Kui Yean Tan3 (2021). This study’s objective is to understand how bank clients behave to better apply financial technology to the financial services sector. Understanding predictions that can affect consumers’ decisions to adopt FinTech services and enhance loyalty to the service is vital for both FinTech businesses and commercial banks. Four hypotheses were created and investigated in the current study. All the hypotheses were verified by the findings. In the Malaysian context, the most important characteristics that affect behavioral intention to utilize FinTech services are trust, social influence, cybersecurity concerns, and privacy threats.

- MeikangQiu, A survey on FinTech , (2017) in the financial sector, the term FinTech has gained widespread popularity as it refers to innovative technologies adopted by financial service institutions. This encompasses a broad range of methods, from ensuring data security to enhancing the delivery of financial services. There is a pressing need for both academics and professionals to possess an accurate and up-to-date understanding of FinTech. This study aims to provide a comprehensive overview of FinTech by gathering and assessing recent advancements, culminating in the proposal of a theoretical data driven FinTech framework. The investigation delves into five key technical aspects: security and privacy, data techniques, hardware and infrastructure, applications and management, and service models. The primary findings underscore the foundational elements essential for the development of dynamic FinTech solutions.

- Ferdinando Giglio, Fintech: A Literature Review, 2021. This study analyzes financial technology and explains some of the main definitions in the field of financial technology at the international and national levels. The study also analyzed six financial technology business models implemented by many financial companies, includingwealth management companies, payment companies, crowdfunding companies, and others.

- PatrickSchueffel, Hochschule für Wirtschaft Fribourg, 2017, through this study, reveal the complexity of financial technology and seek to define it by reviewing more than 200 scientific articles that refer to financial technology and cover more than 40 years. The aim of this study is to provide a clear and concise definition of financial technology. The definition lies in extracting the fundamental goal of financial technology by using the two fields together. It has been concluded that financial technology is one of the modern industries in which technology is applied to improve activities in the financial field. And discuss the effects resulting from its use.

- InLee and Yong Jae Shin, Fintech: Ecosystem, business models, investment decisions, and challenges, 2018, Financial technology provides a good and new model in which information technology is used in the financial field. Financial technology is described as an innovation or invention that changes the rules of the game and brings about a radical change in the financial market. This study presents and presents a historical theory about financial technology and discusses the ecosystem in the financial technology sector. This study also discusses and uses the real and correct option in investment decisions.

Introduction

Considering the technical and financial development taking place today. All financial institutions and companies, such as banks, are constantly searching for modern methods and technologies that help facilitate their operations, which leads to increased productivity. One of these methods and tools that help them increase effectiveness and productivity is financial technology, through which it improves its operations and enhances productivity. Contributes to creating new opportunities. Through this chapter, we will test the research method that has been used on the financial strength of banks.

The goal of this chapter is to identify the information and data used that are collected from several sources that will be analyzed and then will discover how financial technology enhances growth and productivity, which helps banks to flourish and develop in the technical age.

Research design.

The research questions will be answered using a quantitative research methodology, and the results will be evaluated using an exploratory analytic technique. Utilizing an operational perspective, the exploratory design is frequently utilized to provide precise answers.

By Study of the effect of FinTech on the financial efficiency and productivity of Omani commercial banks analyzing the performance of the bank in terms of interbank factors such capital adequacy, asset quality, management quality, liquidity, and size, this technique will be utilized to comprehend and assess the bank’s performance. Aside from assessing financial instruments and performance, quantitative analysis is also utilized to explore the correlations between pertinent variables in quantitative research. This study will make use of secondary data.

Data collection

Secondary data is data that has already been collected through primary sources and is readily available for researchers to use in their own research. It is a type of data that has already been collected in the past. Primary sources could be banks’ financial statements and statements.

Secondary Data

The idea behind secondary data is that it is readily available, and that the researcher uses it in accordance with the needs. The study paper’s primary source of secondary data is a bank’s account books and yearly reports.

Researchers must also make every effort to obtain comprehensive and sufficient information. The researcher uses all the correct methods.

DATA COLLOCATION METHOD

Data collection is the methodical process of collecting and analyzing information from various sources to gain a clear picture or understanding of a particular topic. This process helps individuals and companies get the answers they need, evaluate their performance, and predict trends and opportunities. The type of data a researcher uses in their study has a significant impact on how the data is collected. Secondary data are collected by one or more other people and on which the statistical process is based, secondary data collection depends on the collection techniques This study analyze and work on discussing the information and data obtained from the financial statements of the five banks in the Sultanate of Oman, which are the Bank of Muscat, Dhofar Bank, Sohar Bank, Bank Nizwa and Oman Arab Bank. The financial statements for the banks list that was chosen for the year 2018 to 2022. In order to get the required ratios for those years’ data from multiple sources.

Data Analysis

The quantitative research methodology was used for this investigation. The population of this research was banking who are currently in Oman with a sample size of 5 banks. Based on these, it will show the impact of Fintech on banking performance in Oman is investigated in this research.

Data analysis and interpretation

To assess the impact of Fintech, it’s crucial to consider the bank’s investments in technology. In this fourth chapter, this study analyzes and work on discussing the information and data obtained from the financial statements of the five banks in the Sultanate of Oman, which are Bank of Muscat, Dhofar Bank, Sohar Bank, Bank Nizwa and Oman Arab Bank. Return on Assets and Return on Equity laws were used, as this chapter is used as a link to the relationship between the study goals and the results that have been analyzed to ensure the impact of financial technology on the productivity of banks.

Variables measurements:

| Measurement | Variables |

| Net income after tax / Total assets | Return on Assets |

| Net income after tax / Total Equity | Return on Equity |

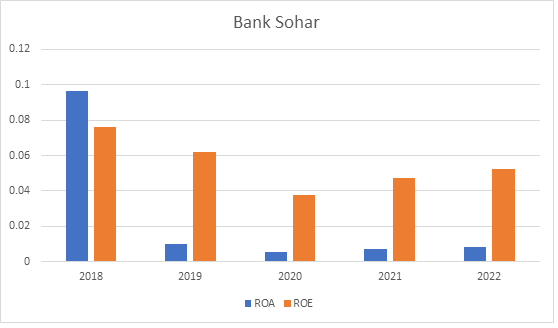

Bank Sohar

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| 0.00844 | 0.00685 | 0.00554 | 0.00981 | 0.09639 | Return on assets |

| 0.05240 | 0.04750 | 0.03763 | 0.06186 | 0.07619 | Return on equity |

Through verification and investigation, and through annual reports collected for five years between 2018 and 2022, the results showed. It turns out that financial technology is of great importance in terms of the return on assets, as after the economy was affected by the Corona pandemic, the return on assets in the bank was affected, so the bank resorted to using financial technology more, as the return on assets was 0.00981 in 2019, but because of the pandemic. The return on assets decreased significantly in 2020, reaching 0.00554, which made the bank focus heavily on financial technology, and this made the return on assets rise in 2022 to reach 0.00844.

On the other hand, financial technology had a positive role in the return on equity, according to the numbers resulting from the verification, as after the Corona pandemic, the return on equity increased between 2020 and 2022 by a value of 0.01477. This indicates an increase in the number of customers and satisfaction from Services provided by the bank.

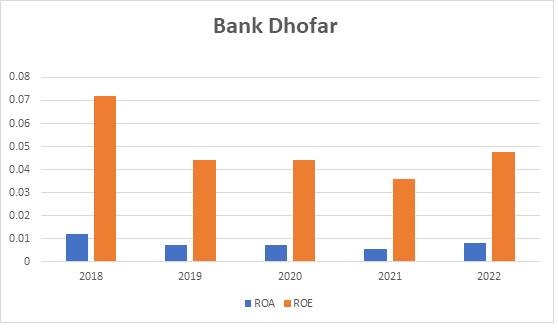

Bank Dhofar

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| 0.00790 | 0.00565 | 0.00718 | 0.00699 | 0.01193 | Return on assets |

| 0.04761 | 0.03596 | 0.04395 | 0.04407 | 0.07201 | Return on equity |

Through the previous results, and through studying the annual reports of Bank Dhofar during the five years from 2018 to 2022. It was found that the return on assets was increasing until the Corona virus swept the world in the year 2020, which led to a decrease in the return on assets, as it decreased by a value of 0.00475 from the year 2018 to the year 2020. While the use of financial technology after the Corona pandemic increased, the return on assets began to rise, reaching 0.00790 in 2022.

From the other side. Financial technology also helps in raising the level of return on equity, as it decreased due to the pandemic that swept the world, as it reached in 2021 to 0.03596, while it rose in 2022 it reached 0.04761.

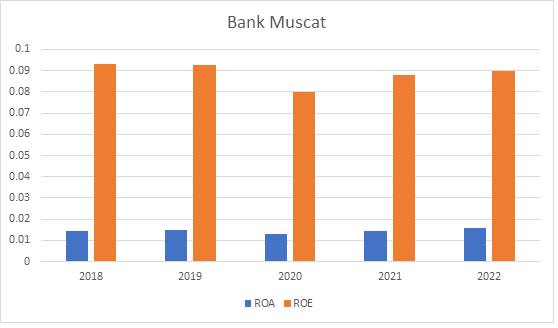

Bank Muscat

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| 0.01571 | 0.01450 | 0.01311 | 0.01509 | 0.01461 | Return on assets |

| 0.08993 | 0.08816 | 0.07993 | 0.09265 | 0.09318 | Return on equity |

The increasing trend in ROA from 2018 to 2022 indicates that Bank Muscat has been more effective in generating profits relative to its assets. A higher ROA suggests better asset utilization and efficiency so we can found that the return on assets was increasing until the Corona virus affected the bank in the year 2020, which led to a decrease in the return on assets, as it decreased by a value of 0.01311 from the year 2018 to the year 2020. While the use of financial technology after the Corona pandemic increased, the return on assets began clearly to rise, reaching 0.01571 in 2022.

The ROE figures indicate the return the bank in 2022, the ROE increased, suggesting that the bank was more profitable for its shareholders compared to the previous years. However, financial technology helped in raising the level of return on equity, as it decreased due to the pandemic that swept the world, as it reached in 2020 to 0.07993, while it rose in 2022 to 0.08993.

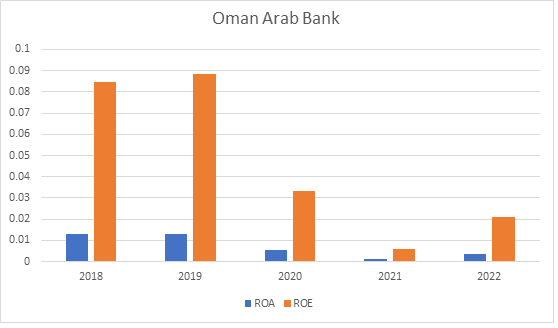

Oman Arab Bank

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| 0.00377 | 0.00117 | 0.00560 | 0.01303 | 0.01294 | Return on assets |

| 0.02098 | 0.00584 | 0.03316 | 0.08826 | 0.08445 | Return on equity |

The ROA figures show some volatility, with a significant decrease in 2021 with 0.00117 because of pandemic followed by a slight increase to 0.00377, in 2022. The impact of Fintech on ROA can be observed in how the bank adopts and integrates technological advancements to enhance operational efficiency and cost-effectiveness. Fintech could contribute to improved asset utilization through automation and digitalization of banking processes.

Similar to ROA, ROE experienced a dip in 2021 with 0.00584 and a subsequent increase to 0.02098, in 2022. Fintech innovations, such as digital banking services, can influence ROE by attracting more customers, reducing operational costs, and enhancing overall profitability.

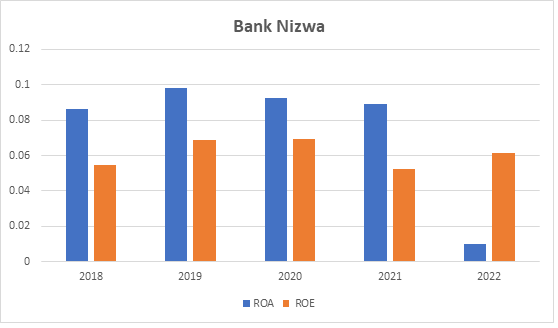

Bank Nizwa

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| 0.01013 | 0.08916 | 0.09274 | 0.09839 | 0.08612 | Return on assets |

| 0.06118 | 0.05222 | 0.0693 | 0.0688 | 0.05474 | Return on equity |

Through the annual reports that appeared during the five years from 2018 to 2022, results were shown. We find that the assets ratio increases and is more effective. Which showed a decrease in the assets ratio in the year 2022 until it reaches 0.01013. Bank Nizwa has witnessed remarkable development.

Numbers on shareholders’ equity indicate that the return on shareholders’ equity increased in 2020, which indicates that the bank provided diverse and innovative services to customers and witnessed an increase in the percentage of shareholders’ equity.

FINDINGS AND CONCLUSIONS

In conclusion, the examination of the impact of FinTech on the financial efficiency and productivity of Omani commercial banks has provided valuable insights into the transfor mative influence of technological innovations in the financial sector.

The findings of this research can be summarized as follow, the integration of FinTech solutions has played a pivotal role in driving efficiency within Omani commercial banks. Automation of processes, streamlined workflows, and the adoption of advanced analytics have collectively contributed to enhanced operational efficiency. FinTech has empowered Omani commercial banks to deliver more customer-centric financial services. The introduction of digital platforms, mobile banking, and personalized financial solutions has not only improved customer satisfaction but has also fostered a deeper engagement between banks and their clients. The regulatory framework in Oman has played a crucial role in shaping the integration of FinTech within the commercial banking sector. Regulatory bodies have shown a proactive approach in creating an environment that fosters innovation while ensuring compliance. Collaborative efforts between traditional banks and FinTech entities have also been instrumental in navigating this evolving landscape. Furthermore, the future prospects for the financial efficiency and productivity of Omani commercial banks appear promising with continued advancements in FinTech. Embracing emerging technologies, fostering a culture of innovation, and investing in the ongoing development of digital capabilities will be key factors in sustaining and expanding the positive impacts observed in this study.

In essence, the effect of FinTech on the financial efficiency and productivity of Omani commercial banks is not just a technological shift; it represents a fundamental redefinition of the banking landscape. As the sector continues to evolve, embracing the opportunities presented by FinTech will be imperative for Omani banks to remain competitive and resilient in the global financial landscape.

Below are some of the product of financial technologies that banks have produce:

- Bank Sohar:

1- Smart phone banking application.

2- The unified digital platform for online banking.

Whereas Bank Sohar received the award for the best bank in digital banking in the Sultanate of Oman during the year 2023 presented by the World Economy Magazine, as this award is presented as a result of accurate evaluations carried out by this magazine under many criteria, including digital transformation in the bank. The technological innovations offered by the bank and the diversity of digital products and services provided by the bank.

This award demonstrates the firm commitment to investing in technical fields, innovation, and providing digital solutions that improve the digital banking experience for customers.

- Bank Dhofar:

1- “Mujib Prepaid” card

This card is linked to the Thawani virtual wallet. This card provides a safe and reliable solution for users to complete payments and transactions, whether inside or outside the Sultanate. Bank Dhofar launched this card in cooperation with “Visa”. It is a global leader in the fields of digital financial technology.

This card allows it to be used in all stores that provide electronic payment inside or outside the Sultanate of Oman.

- Bank Muscat:

1- Payment bracelet “Youth bracelet”

This bracelet works in a smart way as it is linked to the bracelet holder’s account and then he can wear it in his hand and allows him to pay by placing the bracelet on the payment machine, which facilitates the payment process and keeps it from being lost.

- Oman Arab Bank:

1- Contactless technology

This technology provides the ability to carry out transactions easily, quickly, and with greater safety for users without the need for the card to be inserted into the ATM in the traditional way. This technology will help customers access their accounts and complete their transactions faster and easier and will also help them complete banking transactions securely by swiping the card.

- Bank Nizwa:

1- Pay bills from the Bank Nizwa application

This feature enables customers to pay all bills through this feature, such as paying study fees or internet fees. This feature provides customers with a modern and advanced digital banking experience and helps customers carry out transactions without resorting to the concerned authority. This feature not only facilitates payment operations but is also secure. from the research and through the previous technologies It was noticed that the banks used are seeking to provide easy and quick experiences that facilitate the customer to do his transactions without the need to do several operations, as all previous technologies all seek to be all safe and secret transactions and this indicates Financial technology is safe and does not threaten the security of the banks and the entities that it uses.

RECOMMENDATIONS

The impact of financial technology on improving the productivity and financial efficiency of Omani banks plays an important role in improving the productivity and financial efficiency of Omani commercial banks. It has helped streamline operations, enhance customer experience and provide innovative solutions.

- Improving customer experience: Digital financial technologies provide innovative and flexible interfaces for customers to conduct financial transactions easily and quickly. Customers can access their accounts and make transfers and payments via mobile banking apps and websites.

- Improving internal operations: Digital financial technologies help simplify and improve the internal operations of Omani commercial banks. These technologies include artificial intelligence, machine learning, big analytics, cryptography, and big data manipulation, which help improve efficiency and reduce errors.

- Providing innovative financial services: FINTECH provides an innovative solution to Omani commercial banks by providing serviceses.

- Financial technology works to enhance the security aspects of banks through the modern technologies that banks use and launch to provide a safe and smooth experience for users

- The application of financial technology and the use of deposit and transfer machines has significant implications for Omani commercial banks. These developments have simplified banking processes, making them more efficient and convenient for customers. Through FinTech apps, customers can easily access their accounts, make transactions and even apply for loans or credit cards directly from their smartphones. Deposit and transfer machines provide a self-service option for customers to deposit or transfer funds without the need for human assistance. This reduces waiting times and enhances the overall banking experience. Overall, these elements of financial technology have revolutionized the way Omani commercial banks operate, making banking easier and more convenient for customers.

- FinTech may play a crucial role in enhancing the security aspects of Omani commercial banks. With advances in technology, banks can implement strong security measures to protect customer data and prevent fraudulent activities. For example, biometric authentication methods such as fingerprints or facial recognition can be integrated into mobile banking applications, ensuring secure access to accounts. In addition, encryption techniques can be used to protect sensitive information during online transactions. By leveraging fintech solutions, Omani commercial banks can enhance their security protocols and provide customers with peace of mind when it comes to their financial transactions.

REFERENCES

- Business, G. and Research, M. (2022). The Impact of FinTech on the Profitability of Traditional banks. An International Journal, [online] 14(3s). Available at: http://www.gbmrjournal.com/pdf/v14n3s/V14N3s-33.pdf.

- Muia, S.W. (2017). The Effect Of Financial Innovations On Financial Performance Of Commercial Banks In Kenya. 89.49.13. [online] doi:http://41.89.49.13:8080/xmlui/handle/123456789/1243.

- Baker, H., Kaddumi, T.A., Nassar, M.D. and Muqattash, R.S. (2023). Impact of Financial Technology on Improvement of Banks’ Financial Performance. Journal of Risk and Financial Management, 16(4), p.230. doi:https://doi.org/10.3390/jrfm16040230.

- Radixweb. (2022). What is Fintech? Definition, Importance and Examples. [online] Available at: https://radixweb.com/blog/what-is-fintech.

- Hanna Shnaider (2023). Impact Of Fintech On The Banking Industry – FortySeven. [online] Available at: https://fortyseven47.com/blog/impact-of-fintech-on-the-banking-industry/.

- Economics Observatory. (n.d.). Is fintech disrupting the banking sector? [online] Available at: https://www.economicsobservatory.com/is-fintech-disrupting-the-banking-sector.

- The University of Bath (2021). How fintech is changing the future of traditional banking. [online] The University of Bath. Available at: https://online.bath.ac.uk/articles/impact-of-fintech-on-banking.

- Santosdiaz, R. (2022). Oman and Its Fintech Environment in 2022. [online] The Fintech Times. Available at: https://thefintechtimes.com/oman-and-its-fintech-environment-in-2022/.

- SPDLOAD (2022). FinTech Disruption in Banking: Overview of Key Innovations. [online] Available at: https://spdload.com/blog/fintech-disruption-in-banking/.

- gov.om. (n.d.). Central Bank Of Oman – Fintech. [online] Available at:https://cbo.gov.om/Pages/FinTech.aspx.