Determinants of Biological Asset Disclosure Moderated Biological Asset Intensity

- Fatimah Zahra

- Muhammad Wahyuddin Abdullah

- Nur Rahmah Sari

- 270-281

- Feb 22, 2024

- Economics

Determinants of Biological Asset Disclosure Moderated Biological Asset Intensity

Fatimah Zahra, Muhammad Wahyuddin Abdullah, Nur Rahmah Sari

Faculty of Islamic Economics and Business, Alauddin Islamic State University Makassar

DOI: https://doi.org/10.51584/IJRIAS.2024.90125

Received: 12 January 2024; Accepted: 24 January 2024; Published: 22 February 2024

ABSTRACT

This study examines the determinants of growth, company size and international level variables on biological asset disclosure with biological asset intensity as a moderating variable. The gap in this study lies in the biological asset intensity variable as a moderating variable. This study is quantitative research with secondary data sources obtained through annual reports of agricultural companies listed on the Indonesia Stock Exchange for the 2018-2022 period. The purposive sampling method was used as a sampling technique. Testing of this research data uses multiple linear regression analysis and moderation analysis tests using an interaction test approach with the help of SPSS 25 software. The results of research using multiple regression analysis tests show that growth and company size influence the disclosure of biological assets. Meanwhile, international level variables have no effect on biological asset disclosure. Then, the results of the moderation regression analysis test using the interaction test approach show that biological asset intensity moderates the growth, company size and international level variables on biological asset disclosure. The limitation of this research is that it only covers agricultural companies in the plantation sub-sector. Therefore, future researchers are expected to expand the scope of research and develop other variables related to the disclosure of biological assets, such as foreign ownership and government policy.

Keywords: Growth; company size; international level; biological asset intensity; biological asset disclosure.

INTRODUCTION

As the largest archipelagic country in the world, located on the equator with a tropical climate and high rainfall, Indonesia has enormous natural resource potential. Almost all plants can live and develop well in Indonesia, making this country called an agricultural country (Santoso & Handayani, 2021). Based on data from the Central Statistics Agency (BPS), when the country’s economy experienced a recession due to the Covid-19 pandemic in 2019-2021, the agricultural sector still stood strong and was able to maintain positive agricultural growth rates (BPS, 2023).

However, there are several crucial problems that hamper agricultural development so that the contribution of the agricultural sector to agricultural growth in Indonesia is not optimal. The problems that occur come from the market and politics. Economic and political policies often hamper the welfare of farmers and society, food security and agricultural efficiency. One example of political policy that inhibits the growth of the agricultural sector is development policy that is more inclined towards the industrial and construction sectors. This causes the availability of agricultural land to become narrow and limited. From these facts it can be concluded that the Indonesian government needs to take steps to develop the agricultural sector, as a form of effort to maintain national food security. The agricultural sector must be developed because it is one of the backbones of national economic development (Yurniwati et al., 2018).

Development carried out in the agricultural sector must be supported by the availability of accurate information (Sa’diyah et al., 2019). The availability of this information is presented in the form of financial reports or annual reports which will be used by stakeholders in the context of decision making. Agricultural companies have biological assets as their main assets, therefore it is important to provide complete disclosures in financial reports. Standards require more disclosure of biological assets, in order to produce reliable and accurate information, so as not to mislead information users.

Based on PSAK 69 (2018), entity disclosures are recommended to make quantitative descriptive disclosures of biological assets which are divided into biological assets that can be consumed and productive assets, or mature and immature biological assets. Biological asset disclosures are disclosures made regarding management activities carried out by the company, in the form of changing or processing these biological assets. The extent of disclosure of biological assets is influenced by the intensity of biological assets, company growth, company size, profitability, leverage and managerial ownership (Aliffatun & Sa’adah, 2020; Duwu et al., 2018; Hayati & Serly, 2020). This research examines the influence of growth, company size, and international level on biological asset disclosure with biological asset intensity as moderation. Therefore, agricultural companies should be able to increase disclosure of biological assets in connection with the enactment of amendments to PSAK 69. Also as a form of accountability and meeting stakeholder satisfaction, as well as reducing information asymmetry and maintaining reputation.

Several theories explain the disclosure of financial report information related to the disclosure of biological assets, including agency theory and stakeholder theory. Agency theory states that as a mechanism, disclosure is able to reduce costs resulting from conflicts between managers and shareholders as well as from conflicts between companies and creditors (Jensen & Meckling, 1976). This is because biological transformation allows the information presented by agricultural companies to be more biased than companies in other sectors, because the actual value of assets tends to change along with the transformation of these assets (Eltanto, 2014). In stakeholder theory, it is also explained that financial reporting is one way to manage the trust of stakeholders (Duwu et al., 2018). The importance of disclosing biological assets as a form of confirmation regarding the reasonable value of biological assets in accordance with their contribution in generating economic benefits for the company (Kusumadewi, 2018).

OBJECTIVE OF THE RESEARCH

The specific objective of the research is to test empirically the influence of growth, company size, and international level on biological asset disclosure moderated by the intensity of biological assets in agricultural companies in the plantation sub-sector.

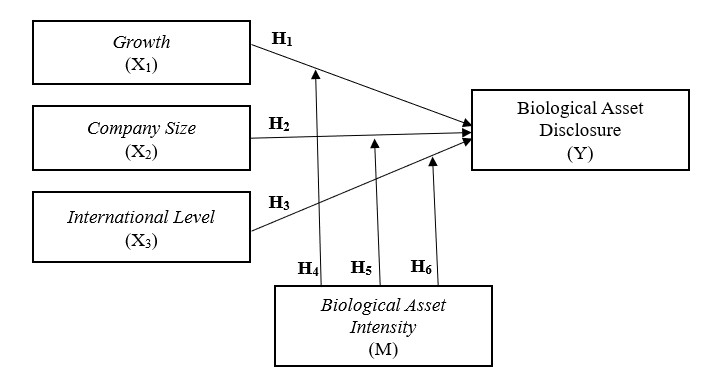

HYPOTHESIS OF RESEARCH

Figure 1. Conceptual Framework

The Effect of Growth on Biological Asset Disclosure

Growth is a growth ratio that describes the percentage growth of company posts from year to year (Harahap, 2011). Companies that have a high growth rate will tend to receive more attention, so these companies will make wider disclosures regarding the financial and non-financial information they have. Based on stakeholder theory, companies will disclose biological assets in their annual reports to inform stakeholders about the company’s ongoing growth (Alfiani & Rahmawati, 2019). Companies with high growth will make more extensive disclosures and can reduce their political costs. Thus, the hypothesis proposed is as follows:

H1: Growth has a positive effect on biological asset disclosure.

The Influence of Company Size on Biological Asset Disclosure

Company size is a description of the size of the company. According to Jensen & Meckling (1976), large companies tend to have a larger percentage of capital and agency costs, thus requiring disclosure of information to stakeholders. The bigger a company, the company will face high agency costs (Nuryaman, 2009). Company size shows that the larger the company, the higher the demand for information disclosure compared to smaller companies (Duwu et al., 2018; Sa’diyah et al., 2019; Zulaecha et al., 2021). In other words, the larger the company, the more biological assets it can disclose. Thus, the hypothesis proposed is as follows:

H2: Company size has a positive effect on biological asset disclosure.

The Influence of International Level on Biological Asset Disclosure

International level relates to the level of foreign activity in a company (Daske et al., 2013). According to Diphayana (in Hayati & Serly, 2020) international companies are companies that have begun to develop their business activities abroad, including marketing activities, factory development and other activities, but are still domestically oriented. The level of internationalization of a company is also closely related to the disclosure of financial reports, this is because companies that are already in an international position will be required to increase the disclosure of their financial information, bearing in mind that large companies with a high level of activity complexity will definitely have more stakeholders (Sa’ diyah et al., 2019). Thus, the hypothesis proposed is as follows:

H3: International level has a positive effect on biological asset disclosure.

The effect of Growth on Biological Asset Disclosure is moderated by Biological Asset Intensity

Companies with high growth have the potential to be profitable in the future so they tend to be more closely scrutinized by outside parties. Thus, companies with high growth will disclose more information (Cindy & Madya, 2018). In accordance with PSAK 69, biological asset intensity in agricultural sector companies describes the proportion of investment in the company’s biological assets. Companies will disclose biological assets in their annual reports to inform stakeholders about the company’s ongoing growth (Alfiani & Rahmawati, 2019). The greater the biological asset intensity a company has, the higher the company’s growth. As the company’s growth increases, disclosure of its biological assets will also increase. Thus, the hypothesis proposed is as follows:

H4: Biological asset intensity moderates the effect of growth on asset disclosure biological.

The influence of Company Size on Biological Asset Disclosure is moderated by Biological Asset Intensity

Company size is an important thing. Company size is a reflection of the company’s selling power (Rokhimah & Nurhayati, 2021). Company size shows that the larger the company, the higher the demand for information disclosure compared to smaller companies (Duwu et al., 2018; Sa’diyah et al., 2019; Zulaecha et al., 2021). Larger companies have larger assets and smaller companies generally have smaller total assets (Riski et al., 2019). In other words, the higher the biological asset intensity, the greater the size of the company. So the larger the company size, the wider the disclosure of its biological assets. Thus, the hypothesis proposed is as follows:

H5: Biological asset intensity moderates the influence of company size on disclosure of biological assets.

The influence of International Level on Biological Asset Disclosure is moderated by Biological Asset Intensity

Agency theory states that there is a contractual relationship between the principal and the agent. Managers as agents who manage the company know more about the company’s condition compared to the principal (Jensen & Meckling, 1976). Thus, companies that have an international position are required to increase the disclosure of their financial information, bearing in mind that large companies with a high level of activity complexity definitely have more stakeholders (Sa’diyah et al., 2019). Information regarding biological assets will be useful for stakeholders to find out what proportion of the company’s investment is in the biological assets within the company. Therefore, the company’s level of internationalization will influence the disclosure of biological assets, especially supported by the amount of biological asset intensity the company has. Thus, the hypothesis proposed is as follows:

H6: Biological asset intensity moderates the influence of international level on disclosure of biological assets.

METHODOLOGY

This research is quantitative research which aims to test the hypothesis that has been established. The population in this research is all agricultural companies listed on the Indonesia Stock Exchange (BEI) for the 2018-2022 period. Sampling used purposive sampling with the following criteria:

- Agricultural companies listed on the Indonesian Stock Exchange starting from the 2018-2022 period.

- Agricultural companies that publish consecutive complete annual reports.

- Agricultural companies that have positive profits.

Based on the aforementioned criteria, there were 35 research data obtained from seven agricultural companies which were the research samples. The type of data used is documentary data and the data source is secondary data obtained through the company’s annual report on the official website of the Indonesia Stock Exchange.

Table 1. Research Sample

The data analysis technique uses SPSS 25 software. The relationship between the independent variable and the dependent variable is explained through multiple regression analysis testing. Based on the proposed hypothesis, the form of the multiple linear regression analysis equation is as follows:

Y = α + β1X1 + β2X2 + β3X3 + e (I)

Where:

Y : Biological Asset Disclosure

α : Constant

β1, β2, β3 : Regression Coefficient

X1 : Growth

X2 : Company Size

X3 : International Level

e : Error Term

Meanwhile, the relationship between the independent variable and the dependent variable with the moderating variable is explained through Moderated Regression Analysis (MRA) testing with an interaction test approach. Based on the proposed hypothesis, the form of the moderated regression analysis equation is as follows:

Y = α + β1X1 + β2X2 + β3X3 + β4X1Z + β5X2Z + β6X3Z + e (II)

Where:

Y : Biological Asset Disclosure

α : Constant

β1, β2, β3 : Regression Coefficient

X1 : Growth

X2 : Company Size

X3 : International Level

Z : Biological Asset Intensity

e : Error Term

Operational definitions are used to avoid multiple interpretations, namely by providing limitations to the variables in this research. The variables used in this research are as follows:

Biological Asset Disclosure (Y)

In this research, the Wallace index is used to measure the amount of disclosure presented by the company. If each item is disclosed in the financial report, it is given a score of 1 (one) and a score of 0 (zero) if it is not disclosed.

Indeks Wallace = n/k x 100%

Where:

n : Number of completeness items fulfilled

k : The number of all items that may be met

Growth (X1)

To measure company growth, this research uses the profit growth ratio because it can describe the company’s good condition.

Profit Growth =![]()

Where:

Net Profit t : Net profit for the current year

Net Profit t – 1: Last year’s net profit

Company Size (X2)

To measure the size of the company, it can be measured using the natural logarithm of total assets. The use of total assets is based on the consideration that total assets reflect the size of the company and are thought to influence timeliness.

Company Size = Ln (Total Assets)

Where:

Ln : Natural logarithm

International Level (X3)

To measure the level of internationalization of a company, use the ratio between foreign sales and total sales.

International Level = Foreign Sales/Total Sales

Biological Asset Intensity (M)

The moderating variable used in this research is biological asset intensity. Biological asset intensity provides an overview of the investment value of biological assets in a company.

Biological Asset Intensity =![]()

RESULT AND DISCUSSION

Multiple Linear Regression Analysis

Multiple linear regression analysis was used to test hypotheses H1, H2, and H3 in this study. The test results can be seen in the table below:

Table 2. Multiple Linear Regression Analysis Test

| Coefficientsa | ||||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | -161.919 | 39.862 | -4.062 | .000 | |

| Growth | .065 | .302 | .277 | 2.070 | .047 | |

| Company Size | 7.442 | 1.331 | .848 | 5.593 | .000 | |

| International Level | -39.150 | 6.486 | -1.014 | -6.036 | .000 | |

a. Dependent Variable: Biological Asset Disclosure

Based on the t test results in the table above, the estimation model can be analyzed as follows:

Y = -161,919 + 0,065X1 + 7,442X2 – 39,150X3 + e (I)

Growth has a positive effect on disclosure of biological assets

The significance value of the growth variable (X1) on the disclosure of biological assets (Y) is 0.047 < 0.05. And the tcount value of 2.070 is greater than the ttable value of 1.696 (df = 35-3-1). Based on the significance value and tcount which is greater than ttable, H1 is accepted. Thus, growth has a significant positive effect on biological asset disclosure. The results of this research show that the disclosure of biological assets moves in line with the level of company growth, the higher the growth of agricultural companies, the higher the disclosure of the company’s biological assets, this is in line with agency theory about information asymmetry where management has information related to the company including the growth rate rather than the company owner himself. Financial reporting is one way to overcome agency problems so that company owners are able to evaluate their funding. Wide disclosure will make it easy for the company to attract investors and convince creditors to increase their funding for the company.

The results of the data analysis that has been carried out show that growth has a significant positive effect on the disclosure of biological assets. The results of this research are in line with research by Aminah et al., (2023), Hayati & Serly (2020), and Amelia (2016) which shows that company growth has a positive effect on the disclosure of biological assets. Supported by research by Munsaidah et al., (2016) which states that companies with high growth will make wider disclosures and can reduce their political costs.

Company size has a positive effect on biological asset disclosure

The significance value of the company size variable (X2) on the disclosure of biological assets (Y) is 0.000 < 0.05. And the tcount value of 5.027 is greater than the ttable value of 1.694 (df = 35-3). Based on the significance value and tcount which is greater than ttable, H2 is accepted. Thus, company size has a significant positive effect on biological asset disclosure. The results of this research indicate that company size is assumed to be capable in terms of resource availability in meeting the costs associated with disclosing biological assets. Based on stakeholder theory, it is also explained that the larger a company, the greater the percentage of capital and costs that it tends to have, so it is very necessary to disclose complete and detailed information to stakeholders. According to Joulanda & Wahidahwati (2021), disclosing information, especially about a company’s biological assets, is also very useful for stakeholders when making stock decisions.

The results of the data analysis that has been carried out show that company size has a significant positive effect on the disclosure of biological assets. The results of this research are in line with research conducted by Rokhimah & Nurhayati (2021); J. Santoso & Handayani (2021); Istutik & Navisha (2021); Zulaecha et al., (2021); Aliffatun & Sa’adah (2020); Mirović et al., (2019) show that company size influences the disclosure of biological assets where large companies tend to provide more disclosure in their financial reports, including regarding the intensity of the biological assets owned by the company.

International level has a positive effect on biological asset disclosure

The significance value of the international level variable (X3) on the disclosure of biological assets (Y) is 0.000 < 0.05. And the tcount value is -6.036, you need to know that in the ttable negative symbols can be ignored so it is known that the value is 6.036 > 1.696 or tcount is greater than ttable. Meanwhile, the coefficient value of -39.150 indicates a decrease in the dependent variable, so H3 is rejected. Thus, the international level has a significant negative effect on biological asset disclosure. The results of this research show that biological assets are not the main priority of stakeholders, this is contrary to stakeholder theory which states that all stakeholders have the right to know any information from organizational activities that can affect their position. Based on this theory, agricultural companies that are already in an international position should be able to increase their disclosure of financial information, bearing in mind that large companies with a high level of activity complexity definitely have more stakeholders (Sa’diyah et al., 2019). The more stakeholders there are, the more detailed the information that must be conveyed to meet the needs of the stakeholders.

The results of the data analysis that has been carried out show that the international level has a significant negative effect on the disclosure of biological assets. The results of this research are in line with research conducted by Hayati & Serly (2020) and J. Santoso & Handayani (2021) which shows that the international level has a negative and insignificant effect on the disclosure of biological assets because the higher the international level owned by an agricultural company, the lower the disclosure regarding biological assets in the annual report.

Moderated Regression Analysis (MRA)

Moderated Regression Analysis (MRA) is a special application of multiple linear regression, where the regression equation contains elements of interaction (multiplication of two or more independent variables). This analysis is used to test hypotheses H4, H5, and H6 in this study. The test results can be seen in the table below:

Table 3. Moderated Regression Analysis (MRA) Test

Coefficientsa

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | -160.673 | 1.248 | -128.722 | .000 | |

| Growth | .032 | .002 | .137 | 20.034 | .000 | |

| Company Size | 7.434 | .044 | 2.683 | 170.839 | .000 | |

| International Level | -36.035 | .169 | -7.464 | -212.798 | .000 | |

| Biological Asset Intensity | 6.420 | .029 | 6.079 | 225.095 | .000 | |

| X1.M | -.002 | .001 | -.019 | -2.655 | .013 | |

| X2.M | -.211 | .002 | -1.449 | -121.414 | .000 | |

| X3.M | .086 | .013 | .053 | 6.769 | .000 | |

a. Dependent Variable: Bological Asset Disclosure

Based on the t test results in the table above, the estimation model can be analyzed as follows:

Y = -160,673 + 0,032X1 + 7,434X2 – 36,035X3 + 6,420M – 0,002X1.M – 0,211X2.M + 0,086X3.M + e (II)

Biological asset intensity moderates the effect of growth on biological asset disclosure

The significance value of biological asset intensity (β2) is 0.000 > 0.05, so biological asset intensity has a significant effect on the disclosure of biological assets. Furthermore, the significant level of the moderating variable X1.M (β3) is 0.013 < 0.05 indicating a significant position. Because β2 and β3 are both significant, biological asset intensity is included in the quasi-moderation category, which means that the biological asset intensity variable is a moderating variable in the relationship between growth and disclosure of biological assets and is also an independent variable.

The results of the interaction test show that the moderating variable smaller than 0.05. A negative coefficient indicates that biological asset intensity weakens the relationship between growth and biological asset disclosure. Thus, the biological asset intensity variable is able to moderate the influence of growth on biological asset disclosure, so H4 is accepted.

The findings of this research clearly prove that biological asset intensity is able to moderate the influence of growth on biological asset disclosure in agricultural companies. Thus, increasing biological asset intensity influences growth on biological asset disclosure. Companies will disclose biological assets in their annual reports to inform stakeholders about the company’s ongoing growth (Alfiani & Rahmawati, 2019). The smaller the biological asset intensity a company has, the higher the company’s growth. As the company’s growth increases, disclosure of its biological assets will also increase.

Biological asset intensity moderates the influence of company size on biological asset disclosure

The significance value of biological asset intensity (β2) is 0.000 > 0.05, so biological asset intensity has a significant effect on the disclosure of biological assets. Furthermore, the significant level of the moderating variable X2.M (β3) is 0.000 < 0.05 indicating a significant position. Because β2 and β3 are both significant, biological asset intensity is included in the quasi-moderation category, which means that the biological asset intensity variable is a moderating variable in the relationship between company size and biological asset disclosure and is also an independent variable.

The results of the interaction test show that the moderating variable unstandardized is -0.211 and the significance level of 0.000 is smaller than 0.05. A negative coefficient indicates that biological asset intensity weakens the relationship between company size and biological asset disclosure. Thus, the biological asset intensity variable is able to moderate the influence of company size on biological asset disclosure, so H5 is accepted.

The findings of this research clearly prove that biological asset intensity is able to moderate the influence of company size on biological asset disclosure in agricultural companies. Thus, increasing biological asset intensity has an influence on company size on biological asset disclosure. Larger companies have larger assets and smaller companies generally have smaller total assets (Riski et al., 2019). Companies with large total assets show good prospects over a long period of time. The larger the size of the agricultural company, the higher the demands for information disclosure. The larger the company size, the smaller the biological asset intensity, and vice versa.

Biological asset intensity moderates the influence of international level on biological asset disclosure

The significance value of biological asset intensity (β2) is 0.000 > 0.05, so biological asset intensity has a significant effect on the disclosure of biological assets. Furthermore, the significant level of the moderating variable X3.M (β3) is 0.000 < 0.05 indicating a significant position. Because β2 and β3 are both significant, biological asset intensity is included in the quasi-moderation category, which means that the biological asset intensity variable is a moderating variable in the relationship between international level and biological asset disclosure and is also an independent variable.

The results of the interaction test show that the moderating variable smaller than 0.05. A positive coefficient indicates that biological asset intensity strengthens the international level relationship with biological asset disclosure. Thus, the biological asset intensity variable is able to moderate the influence of the international level on biological asset disclosure, so H6 is accepted.

The findings of this research clearly prove that biological asset intensity is able to moderate the influence of the international level on biological asset disclosure, this is because the more biological asset information a company discloses, the higher the quality of the company’s financial reports. Based on agency theory, disclosure will also make it easier for users of financial reports to understand and compare the information presented, especially for biological assets, thereby minimizing conflicts that may arise.

Agricultural companies that have carried out an internationalization process have more stakeholders so they are required to increase the disclosure of their financial information. Therefore, the higher the level of internationalization of a company, the wider the disclosure of its biological assets. This is in line with stakeholder theory, which states that every management in a company will try to gain support and trust from each of its stakeholders, namely by presenting the data needed by stakeholders in financial reports.

CONCLUSION

Based on multiple linear regression analysis and interaction tests, it shows that during the five year research period with a total of six hypotheses proposed, five hypotheses were accepted and one hypothesis was rejected. Multiple linear regression testing shows that growth and company size influence biological asset disclosure. Meanwhile, international level variables have no effect on biological asset disclosure. Moderation testing using an interaction test approach shows that biological asset intensity can moderate the growth, company size and international level variables on biological asset disclosure. This research contributes to the development of agency theory which explains how company managers can provide relevant information to stakeholders to overcome information asymmetry. Apart from that, this research is also based on stakeholder theory which states that all stakeholders have the right to know any information about organizational activities that can affect their position. The limitation of this research is that it only covers agricultural companies in the plantation sub-sector, so it is not able to represent the conditions that occur in other sub-sectors. Therefore, future researchers are expected to expand the scope of research and develop other variables related to the disclosure of biological assets, such as foreign ownership and government policy.

REFERENCES

- Alfiani, L. K., & Rahmawati, E. (2019). Pengaruh Biological Asset Intensity, Ukuran Perusahaan, Pertumbuhan Perusahaan, Konsentrasi Kepemilikan Manajerial, dan Jenis KAP Terhadap Pengungkapan Aset Biologis (Pada Perusahaan Agrikultur yang Terdaftar di Bursa Efek Indonesia Periode 2014-2017). Reviu Akuntansi Dan Bisnis Indonesia, 3(2), 163–178.

- Aliffatun, A., & Sa’adah, L. (2020). Pengaruh Intensitas Aset Biologis, Ukuran Perusahaan dan Konsentrasi Kepemilikan Manajerial terhadap Pengungkapan Aset. JIATAX (Journal of Islamic Accounting and Tax), 3(1), 1–8. https://doi.org/10.30587/jiatax.v3i1.1525

- Amelia, D. (2016). Pengaruh Profitabilitas, Leverage, Pertumbuhan Perusahaan, Tipe Industri, dan Kepemilikkan Saham Publik terhadap Corporate Social Responsibility Disclosure (Pada Industri Pertambangan yang Terdaftar di Bursa Efek Indonesia Periode Tahun 2010-2014). Universitas Esa Unggul.

- Aminah, Khairudin, & Dunan, H. (2023). Pengungkapan Aset Biologis Perspektif Internal dan Eksternal. Jurnal Akuntansi & Keuangan, 14(1), 132–141.

- (2023). Badan Pusat Statistik.

- Cindy, & Madya, S. (2018). Faktor yang Mempengaruhi Pertumbuhan Perusahaan, Kinerja Keuangan, dan Pembiayaan Eksternal terhadap Pengungkapan Sukarela beserta Implikasinya terhadap Kualitas Laba. BALANCE: Jurnal Akuntansi, Auditing Dan Keuangan, 15(1), 1–33.

- Daske, H., Hail, L., Leuz, C., & Verdi, R. (2013). Adopting a Label: Heterogeneity in the Economic Consequences Around IAS/IFRS Adoptions. Journal of Accounting Research, 51(3), 495–547.

- Dewan Standar Akuntansi Indonesia. (2018). Pernyataan Standar Akuntansi Keuangan (PSAK) No. 69: Agrikultur. Jakarta.

- Duwu, M. I., Daat, S. C., & Andriati, H. N. (2018). Pengaruh Biological Asset Intensity, Ukuran Perusahaan, Konsentrasi Kepemilikan, Jenis KAP, dan Profitabilitas terhadap Biological Asset Disclosure (Pada Perusahaan Agrikultur yang Terdaftar di Bursa Efek Indonesia Periode 2012-2016. Jurnal Akuntansi Dan Keuangan Daerah, 13(2), 56–75.

- Eltanto, D. P. (2014). Perlakuan Akuntansi dan PPh atas Industri Agrikultur. Tax & Accounting Review, 4(1), 1–8.

- Harahap, S. S. (2011). Analisis Kritis atas Laporan Keuangan. Rajawali Pers.

- Hayati, K., & Serly, V. (2020). Pengaruh Biological Asset Intensity, Growth, Leverage, dan Tingkat Internasional terhadap Pengungkapan Aset Biologis (Studi pada Perusahaan Agrikultur yang Terdaftar di BEI Tahun 2015-2018). Jurnal Eksplorasi Akuntansi, 2(2), 2656–3649. http://jea.ppj.unp.ac.id/index.php/jea/issue/view/22

- Istutik, & Navisha, A. (2021). Biological Asset Intensity, Company Size, Growth, Ownership Concentration, and Type of Public Accountant Firm Against Biological Asset Disclosure. Jurnal RAK (Riset Akuntansi Keuangan), 6(2), 195–204.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm: Managerial Behavior, Agency Costs, and Ownership Structure. Journal of Financial Economics, 3(4), 305–360.

- Joulanda, R., & Wahidahwati. (2021). Pengaruh Karakteristik Perusahaan terhadap Pengungkapan Aset Biologis Perusahaan Agrikultur. Jurnal Ilmu Dan Riset Akuntansi, 10(2), 1–20.

- Kusumadewi, A. A. (2018). Pengaruh Biological Asset Intensity dan Ukuran Perusahaan terhadap Pengungkapan Aset Biologis (Pada Perusahaan Perkebunan yang Terdaftar di BEI Periode 2017). Universitas Pasundan.

- Mirović, V., Finance, I., Milenković, N., Jakšić, D., Mijić, K., Andrašić, J., & Kalaš, B. (2019). Quality of Biological Assets Disclosures of Agricultural Companies According to International Accounting Regulation. Custos e Agronegocio, 5(4), 43–58. custoseagronegocioonline.com.br

- Munsaidah, S., Andini, R., & Supriyanto, A. (2016). Analisis Pengaruh Firm Size, Age, Profitabilitas, Leverage, dan Growth Perusahaan terhadap Corporate Social Responsibility (CSR) pada Perusahaan Property dan Real Estate yang Terdaftar di Bursa Efek Indonesia pada Tahun 2010-2014. Journal of Accounting, 2(2).

- Nuryaman, N. (2009). Pengaruh Konsentrasi Kepemilikan, Ukuran Perusahaan, dan Mekanisme Corporate Governance terhadap Pengungkapan Sukarela. Jurnal Akuntansi Dan Keuangan Indonesia, 6(1), 89–116. https://doi.org/10.21002/jaki.2009.05

- Riski, T., Probowulan, D., & Murwanti, R. (2019). Dampak Ukuran Perusahaan, Konsentrasi Kepemilikan, dan Profitabilitas terhadap Pengungkapan Aset Biologis. Jurnal Ilmu Sosial Dan Humaniora, 8(1), 60–71. https://doi.org/10.23887/jish-undiksha.v8i1.21355

- Rokhimah, Z. P., & Nurhayati, I. (2021). Biological Assets Disclosure dan Faktor-faktor yang Mempengaruhi (Studi pada Perusahaan Agrikultur yang Terdaftar di BEI Periode 2017-2019). Jurnal Aktual Akuntansi Keuangan Bisnis Terapan, 4(1), 44–54.

- Sa’diyah, L. D. J., Dimyati, M., & Murniati, W. (2019). Pengaruh Biological Asset Intensity, Ukuran Perusahaan, dan Tingkat Internasionalisasi Terhadap Pengungkapan Aset Biologis (Pada Perusahaan Agrikultur Yang Terdaftar Di Bursa Efek Indonesia Periode 2013-2017). Progress Conference, 2, 291–304. http://proceedings.stiewidyagamalumajang.ac.id/index.php/progress

- Santoso, J., & Handayani, S. (2021). Pengaruh Ukuran Perusahaan, Growth, Leverage, Profitabilitas dan Tingkat Internasionalisasi terhadap Pengungkapan Aset Biologis. SOSAINS (Jurnal Sosial Dan Sains), 1(3), 140–154. https://sosains.greenvest.co.id

- Yurniwati, Y., Djunid, A., & Amelia, F. (2018). Effect of Biological Asset Intensity, Company Size, Ownership Concentration, and Type Firm Against Biological Assets. The Indonesian Journal of Accounting Research, 21(1). https://doi.org/10.33312/ijar.338

- Zulaecha, H. E., Rachmania, D., & Amami, A. S. (2021). Pengungkapan Aset Biologis pada Perusahaan Agrikultur di Indonesia serta Faktor yang Mempengaruhinya. Competitive Jurnal Akuntansi Dan Keuangan, 5(1), 122–129.