Independence of Auditors and Financial Report Reliability of Listed Deposit Money Banks in Nigeria

- Kolawole Olayemi Babatayo

- Onajero Kensinton Ohwo

- Ibrahim Solomon Audu

- Jamiu Adewale Arogundade

- 223-231

- Mar 28, 2025

- Accounting and Finance

Independence of Auditors and Financial Report Reliability of Listed Deposit Money Banks in Nigeria

Kolawole Olayemi Babatayo1*, Onajero Kensinton Ohwo2*, Ibrahim Solomon Audu3*, Jamiu Adewale Arogundade4*

1Department of Accounting, Babcock University, Ogun State, Nigeria

2UCEE Micro Finance Bank, Lagos State, Nigeria

3Department of Accounting, Finance and Taxation, Caleb University, Lagos State, Nigeria

4Department of Finance, Babcock Business School, Ogun State, Nigeria

*Corresponding author

DOI: https://doi.org/10.51584/IJRIAS.2025.10030016

Received: 23 February 2025; Accepted: 27 February 2025; Published: 28 March 2025

ABSTRACT

Reliable financial reports are vital for maintaining the confidence of the relevant stakeholders. Challenges such as aggressive earnings management, regulatory pressures, and systemic corruption can compromise the reliability of financial reports, raising questions about the effectiveness of existing audit mechanisms and the independence of auditors. Hence, this study examines the influence of the independence of auditors and financial report reliability of the listed deposit money banks in Nigeria. The ex-post facto research design was used, and secondary data was collected from the audited financial reports of the banks. The data was covered over a time span which ranged from 2014 to 2023. The multiple regression model was used. The result shows that audit fees and audit firm size jointly do not have any significant effect on the level of faithful representation of listed deposit money banks in Nigeria. Also, both the audit fees and audit firm size have an inverse influence on the level of reliability of financial reports of listed deposit money banks in Nigeria. It was concluded from the study that auditors’ independence does not have any significant influence on the reliability of the financial report of the listed deposit money banks in Nigeria. It was recommended that banks should focus on broader corporate governance mechanisms beyond just auditors’ independence.

Keywords: Independence of auditors, financial report reliability, faithful representation, relevance.

BACKGROUND TO THE STUDY

The reliability of financial reports is fundamental to the functioning of modern economies, as these reports serve as the cornerstone for decision-making by investors, creditors, regulatory authorities, and other stakeholders. In the banking sector, the reliability of financial reports is particularly critical due to the pivotal role banks play in financial intermediation, resource allocation, and economic stability. However, the credibility of financial reports is directly linked to the independence of auditors, who serve as gatekeepers to ensure the accuracy, transparency, and fairness of financial disclosures.

The independence of auditors is a cornerstone of financial report reliability, particularly in the banking sector, where trust and transparency are paramount. Given the persistent challenges and regulatory gaps in Nigeria, there is a pressing need to examine the factors influencing auditor independence and their implications for financial reporting quality. This study aims to provide a comprehensive analysis of these issues, contributing to the broader goal of enhancing corporate governance and financial accountability in Nigeria. This study is significant for several reasons. First, it contributes to the ongoing discourse on corporate governance and financial reporting quality in Nigeria. By examining the relationship between auditor independence and financial report reliability, the study provides empirical insights into the effectiveness of current audit practices and regulatory frameworks. Second, the study has practical implications for policymakers, regulatory authorities, and audit practitioners. It highlights the need for stringent measures to safeguard auditor independence, such as mandatory audit firm rotation, restrictions on non-audit services, and enhanced regulatory oversight. Finally, the study addresses a critical gap in the literature by focusing on the banking sector, which has unique characteristics and risk profiles that differentiate it from other industries. The findings of this study have the potential to inform policy reforms aimed at strengthening the financial reporting ecosystem in Nigeria.

In the context of listed banks in Nigeria, reliable financial reports are vital for maintaining the confidence of depositors, investors, and regulators. The regulated nature of the banking industry, coupled with its exposure to credit, market, and operational risks, necessitates a robust financial reporting framework underpinned by effective external auditing. However, challenges such as aggressive earnings management, regulatory pressures, and systemic corruption can compromise the reliability of financial reports, raising questions about the effectiveness of existing audit mechanisms and the independence of auditors. In Nigeria, concerns about auditor independence have gained prominence in recent years, particularly considering corporate failures, financial scandals, and allegations of fraudulent financial reporting. These events have highlighted the critical need to examine the factors influencing auditors’ independence and their impact on the reliability of financial reports, particularly in the banking sector, where financial irregularities can have far-reaching economic consequences.

Scholars have carried out several studies of auditors’ independence and financial report reliability in both developed and emerging economies. Findings from these studies have been conflicting. While some of the findings revealed positive effects of auditors’ independence on financial report reliability, some of the findings revealed negative effects of auditor’s independence on financial report reliability. The current study therefore aims to bridge the identified gap in the identified studies.

Main Objective

The primary objective of this research is to investigate the impact of auditors’ independence on the reliability of financial reports in listed deposit money banks in Nigeria. The study seeks to understand the extent to which auditors’ independence influences the accuracy, transparency, and trustworthiness of financial reports, thereby contributing to enhanced financial decision-making and corporate accountability.

Specific Objectives

- To examine the effect of auditors’ independence on the faithful representation of financial reporting of listed deposit money banks in Nigeria.

- To assess the effect of auditors’ independence on the relevance of financial reporting of listed deposit money banks in Nigeria.

LITERATURE REVIEW

Conceptual Review

This section shows insight into the meaning of the two main variables adopted in this study.

Financial Report Reliability

The reliability of financial reports refers to the extent to which financial information faithfully represents the economic activities and conditions of an organization, free from material misstatements, errors, or bias. Reliable financial reports are essential for fostering trust among stakeholders, promoting market efficiency, and ensuring regulatory compliance. According to the International Financial Reporting Standards (IFRS), financial reports must meet qualitative characteristics such as relevance, faithful representation, comparability, verifiability, timeliness, and understandability (IASB, 2018). According to Okezie and Egeolu (2019), the reliability of financial reports refers to a condition, in which investors and other stakeholders interested in a company’s business affairs, consistently find the audit reports and opinions about a company’s financial statements and position to be dependable and credible.

Nattawut and Sirilak (2018) defined “financial reporting reliability as the published financial statements that are being prepared reliably in order to provide information useful to users in making economic decisions (Tontiset & Kaiwinit, 2015; Socea, 2012; Shahwan, 2008; Marriner & Nuseiben, 2004)”. In this study, we focused on financial reporting reliability in two-dimensional variables that are rooted in the fundamental qualitative characteristics of faithful representation and relevance (IASB, 2018).

Auditors’ Independence

Auditor independence refers to the ability of auditors to perform their duties impartially, without undue influence from the management or stakeholders of the organization being audited. DeAngelo (1981) opined that “independence is often categorized into two dimensions: independence in fact and independence in appearance. Independence implies that auditors are free from any biases or conflicts of interest that could compromise their judgment, while independence in appearance relates to how third parties perceive the auditors’ impartiality”. The erosion of either form of independence can undermine public confidence in financial reports and the auditing profession. Ndubuisi and Ezechukwu (2017) believed that “the immediate role of audit independence is to serve the audit by making it more effective in providing assurance that the auditor will plan and execute the audit objectively”. The auditors’ independence is sometimes described as adding credibility to the timeliness of financial reports which is an important ingredient of auditing though management’s cooperation is also needed (Carmona, Momparler & Lassala, 2015). This study focused on auditors’ independence using audit fees and audit tenure as the two independent variables to measure financial report reliability.

Theoretical Framework

There have been several theoretical perspectives adopted by several researchers about the influence of auditors’ independence on the financial reports’ reliability. Some researchers such as Nattawut and Sirilak (2018) adopted the stakeholders’ theory as the underpinning theory for their study. On the other hand, Okezie and Egeolu (2019) adopted the signaling theory in their study. The current study however adopted the agency theory as the underpinning theory for the study. The agency theory provides a theoretical basis for understanding the relationship between auditor independence and financial report reliability. According to Jensen and Meckling (1976), the agency theory posits that the separation of ownership and control in organisations necessitates external monitoring mechanisms, with auditors serving as agents tasked with mitigating agency conflicts. It is believed that conflicts of interest may arise between the management and shareholders, necessitating mechanisms such as external audits to align their interests and reduce information asymmetry. Auditors’ independence is critical in this context, as it ensures the credibility of financial reports and enhances stakeholders’ trust.

Empirical Review

Kabiru and Abdullahi (2012), carried out empirical research into the quality of audited financial statements of deposit money banks in Nigeria. They employed the use of primary and secondary data extracted from a sample of 5 listed banks in Nigeria. The study revealed that the independence of an auditor does significantly improve the quality of audited financial statements of money deposit banks in Nigeria.

In the study conducted by Okezie and Egeolu (2018) on audit independence and reliability of financial reports: empirical evidence from Nigerian banks, four banks were considered. The study employed the use of an ex-post facto research design with data extracted from the published annual reports of these banks using a multivariate linear regression method. The study’s findings showed that audit independence had a significant effect on the value relevance of the banks under study using earning per share as the proxy for financial report reliance. The study further revealed that audit independence has an insignificant effect on the timeliness of financial reports. The first findings of the study affirmed the findings of Kabiru and Abdullahi (2012) while the second findings disproved the results of Kabiru and Abdullahi (2012)

Nattawut and Sirilak (2018) examined the factors affecting financial report reliability: through empirical research of publicly listed companies in Thailand. A descriptive survey research method was used with data collected with the use of a questionnaire. The study employed the use of an accountant’s professional ethics, accounting information system quality, audit committee effectiveness and audit firm quality as antecedents for financial report reliability. The study results revealed that an accountant’s professional ethics, accounting information system quality, audit committee effectiveness and audit firm quality have a positive significant effect on financial report reliability.

Thien and Gerald (2019) assessed the audit quality inputs and financial statement reliability using Amiram, Bozanic, and Rouen’s (2015) measures of the conformity of a firm’s distribution of financial statement line items’ leading digits to the Benford distribution. The study examined whether different constructs of audit quality inputs are related to financial statement reliability. The study results showed that financial statement reliability increases with audit fees, non-audit fees, and audit report lag, and decreases with audit firm tenure. The study also found that audit quality inputs are more strongly associated with income statement reliability than with cash flow statement reliability.

From the review of existing literature, it shows that findings from the studies are mixed. The current study thus, intends to bridge this gap by carrying out a multivariate regression to determine the effect of auditor’s independence on financial reports reliability of listed deposit money banks in Nigeria.

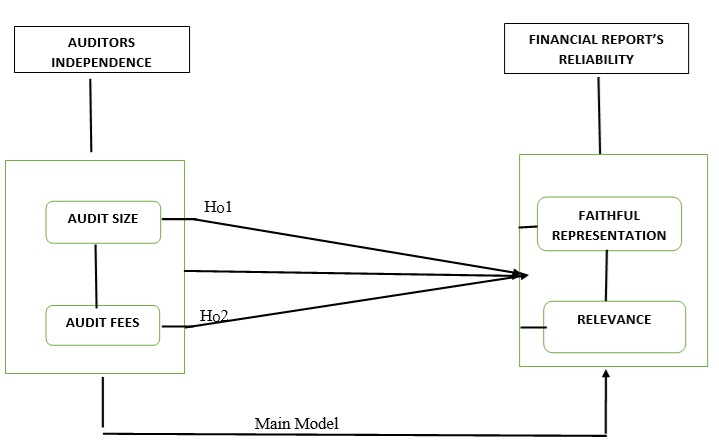

Conceptual Model

The conceptual model was developed to establish the effect of auditor’s independence and financial report’s reliability in listed deposit money banks in Nigeria.

Source: Research work (2025)

Figure 1. Research model of audit independence and financial report’s reliability

METHODOLOGY

In this study, the ex-post facto research design is used, and secondary data is extracted from the audited annual reports of the selected samples in this study. The study population is made up of all the listed deposit money banks in Nigeria which according to the Central Bank of Nigeria sums up to thirteen as of December 31, 2024. The purposive sampling method is used to select seven banks based on their size and in proportion to the total number of listed banks in Nigeria. The panel regression is used to analyze the effect of auditors’ independence (independent variable) on the reliability (dependent variable) of financial reports of listed deposit money banks in Nigeria. The content analysis is used to extract data from the audited financial reports of the selected listed banks used in this study over a time frame ranging between 2014 and 2023. Beest et al (2009) measurement scale of the quality of the financial report is used to extract the proxies of the dependent variables in this study. The model is specified as below:

y = f(X)

Where:

y = Financial report reliability

x = Auditor’s independence

Mathematically, this is specified as:

FR = a + β1Feei + β2Szei + Ƹi …………..…..……Model 1

RL= a + β1Feei + β2Szei + Ƹi …………..…..………Model 2

Where:

a = intercept where the independent variable is zero

FR = Faithful Representation (Dependent Variable)

RL = Reliability (Dependent Variable)

β1Feei = Audit Fee (Independent Variable)

β2Szei = Audit Firm Size (Independent Variable)

Ƹi = Error Term

ANALYSIS AND DISCUSSION OF FINDINGS

The results of the data analysis are presented below:

H01: Auditors’ independence does not have a significant effect on the faithful representation of financial reporting of listed deposit money banks in Nigeria

Table 1. Hypothesis One Result

| Estimation Techniques | Regression Result | |||

| Dependent Variable: FR | Coeff. | Std. Err | T-Stat | Prob |

| Constant | 0.7860924 | 0.0837709 | 9.38 | 0.000 |

| Fees | 1.40e-08 | 5.89e-08 | 0.24 | 0.812 |

| Size | – 0.0005799 | 0.0166215 | -0.03 | 0.972 |

| Adjusted R2 | -0.0308

0.0009 |

|||

| R-Squared | ||||

| Number of Obs | 66 | |||

| F-Stat | (2, 63) 12.57 | |||

| Prob > F | 0.9715 | |||

Source: Researcher’s Computation (2025)

Table 1 reveals that audit fees and size independently do not have a significant effect on the faithful representation of listed deposit money banks in Nigeria’s financial report. However, audit fees have a positive effect on the faithful representation of financial reports. This means that the higher the audit fee, the higher the level of faithful representation even though it is not significant. On the other hand, audit firm size has an inverse influence on the level of faithful representation. This means that the larger the size of the firm, the lower the level of faithful representation even though it is not significant.

The result further reveals that the regression model explains a very minute portion of the faithful representation of financial reports. This is represented by -3.08%. Therefore, other variables outside the scope of this study influence the level of faithful representation of financial reports of listed banks in Nigeria.

Finally, the result shows that auditors’ independence does not have a significant effect on the faithful representation of financial reporting of listed deposit money banks in Nigeria. Hence, the null hypothesis is retained, and the alternate hypothesis is rejected in this study.

H02: Auditors’ independence does not have a significant effect on the relevance of financial reporting of listed deposit money banks in Nigeria

Table 2. Hypothesis Two Result

| Estimation Techniques | Regression Result | |||

| Dependent Variable: RL | Coeff. | Std. Err | T-Stat | Prob |

| Constant | .5727825 | .0749568 | 7.64 | 0.000 |

| Fees | -1.08e-07 | 5.27e-08 | -2.04 | 0.045 |

| Size | -.0157145 | .0148726 | -1.06 | 0.295 |

| Adjusted R2 | 0.0491

0.0784 |

|||

| R-Squared | ||||

| Number of Obs | 66 | |||

| F-Stat | (2, 63) 2.68 | |||

| Prob > F | 0.0764 | |||

Source: Researcher’s Computation (2025)

Table 2 shows that audit fees do have a significant inverse influence on the level of relevance of the financial report of listed deposit money banks in Nigeria. Audit fees on the other hand do have a non-significant inverse influence on the level of relevance of financial reports of listed deposit money banks in Nigeria. This means that the higher the audit fee, the relevance of the financial report reduces significantly. In addition, the larger the size of the audit firm, the lower the level of reliability of the financial report, which is not significant.

Overall, the model used in this study explains only a few of the factors that influence the reliability of financial reports of listed deposit money banks in Nigeria. This is represented by the adjusted r-square of 4.91%.

Lastly, the result of the test of hypothesis 2 shows that auditors’ independence does not have a significant effect on the relevance of financial reporting of listed deposit money banks in Nigeria. This means that the null hypothesis is retained, and the alternate hypothesis is rejected.

DISCUSSION OF FINDINGS

The result of this study shows that audit fees do have a positive influence on the level of faithful representation of financial reports of listed banks in Nigeria. On the other hand, it also reveals that audit size has a significant effect on the level of faithful representation of financial reports of listed deposit money banks in Nigeria. In summary, audit fees and audit firm size jointly do not have a significant effect on the level of faithful representation of listed deposit money banks in Nigeria. This is contrary to the position of Kabiru and Abdullahi (2012) who opined that auditors’ independence does significantly influence the quality of financial reports positively. A possible reason for the variation in results might be the timeline. Kabiru and Abdullahi’s (2012) study was carried out much earlier, but today, there are lots of complexities that arise such as increased cross-border activities and, an increase in the level of technology among others.

Using agency theory to explain the rationality of the result, shows that auditors alone might not be sufficient to ensure accurate financial reporting at such a time like this. Other actors and variables such as forensic accounting might need to be put in place to enhance the level of faithful representation of financial reports among listed deposit money banks in Nigeria.

The result from this study also shows that both audit fees and audit firm size have an inverse influence on the level of reliability of financial reports of listed deposit money banks in Nigeria. While audit fee is significant in its influence, audit firm size is not significant. Jointly, audit fees and audit firm size do not have a significant influence on the reliability of financial reports. The position of this study is at variance with the views of Nattawut and Sirilak (2018); Thien and Gerald (2019) who posited that auditors’ independence significantly influences the level of reliability of financial reports. The reason for the variance might be due to the difference in geographical location of the studies with varying laws and the increasing complexities in contemporary times. Hence, the reliability of financial reporting is not enhanced by auditors’ independence as corporate governance mechanisms are comprised of varied parts to narrow the reliability of financial reporting to only auditors’ independence.

Based on agency theory, monitoring cost is not limited to auditing fees. It means that to enhance the reliability of financial reports of listed deposit money banks, other variables are involved beyond auditors’ independence.

CONCLUSION AND RECOMMENDATIONS

Results from the study reveal that auditors’ independence does not have a significant effect on either the faithful representation or the relevance of financial reporting of listed deposit money banks in Nigeria. Audit fees and audit firm size independently have non-significant effects on faithful representation, although audit fees show a positive relationship while audit firm size shows a negative relationship.

Based on the foregoing, the following recommendations are made to enhance the financial report reliability of deposit money banks.

- Since auditors’ independence alone may not be sufficient in ensuring financial report reliability, forensic accounting practices should be incorporated to help ensure the accuracy and faithful representation of financial reports.

- Given that higher audit fees are associated with better faithful representation, policymakers should ensure a fair and transparent audit fee structure to incentivize high-quality financial reporting.

- Banks should focus on broader corporate governance mechanisms beyond just auditors’ independence to enhance the reliability and relevance of financial reports. This includes improving oversight and accountability measures.

- Professional audit firms should encourage continuous professional development for auditors to keep them updated with the latest standards and practices in financial reporting and auditing.

- Deposit money banks should engage more with stakeholders to understand their needs and concerns regarding financial reporting. This engagement will help in aligning financial reporting practices with stakeholders’ expectations.

Policy Implications

Since the result of the study showed that auditors’ independence does not have a significant effect on either the faithful representation or the relevance of financial reporting of listed deposit money banks in Nigeria, this gives room for policy overhaul. Regulatory bodies in Nigeria should consider revising current regulations to incorporate more comprehensive corporate governance mechanisms that go beyond auditors’ independence.

Also, the relevant regulatory bodies should establish a robust system for monitoring and evaluating the quality of audits conducted by firms, ensuring adherence to high standards and transparency. Although there are guidelines set by individual audit firms in terms of audit fees, the relevant body (FRCN) could develop general objective guidelines on audit fees that are measurable and commensurate with the complexity and scope of audit work, thereby promoting better quality audits.

Considering the complexities arising from cross-border activities, Nigerian regulators should collaborate more with international bodies to harmonize audit standards and practices. This will entail the adoption of advanced auditing tools and technologies to improve the accuracy and reliability of financial reporting.

By implementing stated recommendations and policy implications, the quality of financial reporting among listed deposit money banks in Nigeria can be significantly enhanced, ensuring greater transparency and accountability in the financial sector.

REFERENCE

- Abbot L J., Parker. S., & Peter,G.F.(2004). Audit committee characteristics and restatements auditing. Practice and Theory, 69-87.

- Amiram, D. B. (2015). Financial statement errors: Evidence from the distributional properties of financial statement numbers. Review of Accounting Studies, 20 (4), 1540-1593.

- Carmona, P. M. (2015). The relationship between non-audit fees and audit quality: dealing with the endogeneity issue. Journal of Service Theory and Practice, 25 (6), 777-795.

- L.E. (1981). Audit size and audit quality. Journal of Accounting and Economics, 183-189.

- Jensen, H & Meckling, W.(1976). Theory of the firm: Managerial behaviour, agency costs, and ownership structure. Journal of Financial Economics, 305-360.

- International Accounting Standards Board (2018). Conceptual frameworks for financial reporting

- Kabiru, I.D., & Abdullahi, S.R., (2012). An Examination into the Quality of Audited Financial Statements of Money Deposit Banks in Nigeria. International Journal of Academic Research in Accounting, Finance and Management. 4(1), 145-156.

- Marriner, S. N. (2004). Quality of financial reporting: Evidence from the listed Saudi nonfinancial companies. The International Journal of Accounting, 21(2), 461-491.

- Ndubuisi, A. &. (2017). Determinants of audit quality: Evidence from deposit money banks listed on Nigeria Stock Exchange. International Journal of Academic Research in Accounting, Finance and Managerial Sciences, 7(2), 117-130.

- Nattawut, T., & Sirilak, K. (2018). The factors affecting financial reporting reliability: An Empirical Research of Public Listed Companies in Thailand. Journal of Modern Accounting and Auditing 14(6) 201-304

- Okezie, S. O., & Egeolu, D. U. (2019). Audit independence and reliability of financial reports: Empirical Evidence from Nigerian Banks. International Journal of Economics and Business Management, 5(3), 44-55

- S. & Fagbemi, T. (2010). Audit quality, corporate governance, and firms characteristics in Nigeria. International Journal of Business and Management, 169.

- Shahwan, Y. (2008). Qualitative characteristics of financial reporting: A historical perspective. Journal of Applied Accounting Research, 9(3), 192-202.

- Socea, A. (2012). Managerial decision-making and financial accounting information. Procedia-Social and Behavioural Sciences, 58, 47-55.

- Tontiset, N. (2015). Internal control system effectiveness of Thai-listed companies: An empirical research of its antecedents and consequences. Review of Business Research,15(1), 95-110.