International Journal of Research and Innovation in Applied Science (IJRIAS) | Volume III, Issue II, February 2018 | ISSN 2454-6194

A Study on Impact of GST on Indian Economy

Esha Bansal

Assistant Professor, IEC University, Himachal Pradesh, India

Abstract: – Goods and Service Tax is an indirect tax levied on the supply of goods and services. GST Law has replaced many indirect tax laws that previously existed in India.GST is one indirect tax for the entire country. There are 3 taxes applicable under GST: CGST, SGST & IGST. GST will mainly remove the Cascading effect on the sale of goods and services. Removal of cascading effect will directly impact the cost of goods. This paper gives an understanding about GST in India & its impact on the Indian Economy. The Evolution of GST in India is also discussed in this research paper. The research objectives focus around the evolution of GST, how it works & how different sectors are affected by GST.

Keywords: GST, Goods and services tax, Dual GST, Indian economy and value added tax.

I. INCEPTION

Goods & Services Tax Law in India is a comprehensive, multi-stage, destination-based tax that is levied on every value addition. In simple words, Goods and Service Tax is an indirect tax levied on the supply of goods and services. GST Law has replaced many indirect tax laws that previously existed in India. Earlier, various indirect taxes were levied and collected at different point in the supply chain. The centre and the states were empowered to levy respective taxes as per the Constitution of India. The Value Added Tax (VAT) when introduced was considered to be a major improvement over the pre-existing Central excise duty at the national level and the sales tax system at the State level. But now, GST would be levied with the propaganda of “One Nation One Tax” and is collected at each stage of sale or purchase of goods and services. Purpose of GST in India is efficient tax collection, reduction in corruption, easy inter-state movement of goods etc.

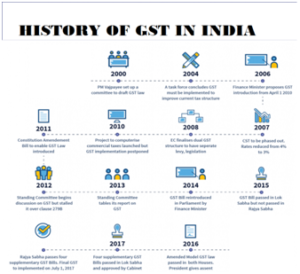

In India, the idea of adopting GST was first suggested by the Atal Bihari Vajpayee Government in 2000. A task force that was headed by Vijay L. Kelkar the advisor to the finance ministry, indicated that the existing tax structure had many issues that would be mitigated by the GST system. In 2005, The finance minister, P. Chidambaram, said that the medium-to-long term goal of the government was to implement a uniform GST structure across the country, covering the whole production-distribution chain. In 2009, Pranab Mukherjee, the new finance minister of India, announced the basic skeleton of the GST system. In February 2015, Jaitley, in his budget speech, indicated that the government is looking to implement the GST system by 1 April 2016.In May 2015, The Lok Sabha passes the Constitution Amendment Bill.

IMPACT OF GST ON INDIAN ECONOMY

Positive Impact of GST in India:

1. GST brings in uniform tax laws across all the states spanning across diverse industries. Before GST was implemented, tax was calculated and paid by every purchaser including the final consumer which is called Cascading Effect of Taxes.