Sign up for our newsletter, to get updates regarding the Call for Paper, Papers & Research.

-

Trending Articles

Editor IJRISS

Skills Development and Economic Welfare among the Youth in Kisoro District Uganda

Skills Development, Economic Welfare, Youth in Kisoro District Uganda

Editor IJRISS

The Effect of Monetary Policy on Economic Growth in Nigeria (2004 – 2022)

The Effect of Monetary Policy on Economic Growth in Nigeria (2004 – 2022)

Adeneye Olawale Adeleke (Ph.D)1, Moses O. Anuolam (Ph.D)2 & Florence I. Ezeilo (Ph.D)3

1Admiralty University of Nigeria, Faculty of Art, Management & Social Science, Department of Accounting, Business Administration and Economics, Economics Programme

2Admiralty University of Nigeria, Faculty of Art, Management & Social Science, Department of Accounting, Business Administration and Economics, Accounting Programme

3Admiralty University of Nigeria, Faculty of Art, Management & social Science, Department of Accounting, Business Administration and Economics, Business Administration Programme

Publication Information

Journal Title: International Journal of Research and Innovation in Social Science (IJRISS)

Author(s): Adeneye Olawale Adeleke (Ph.D), Moses O. Anuolam (Ph.D) & Florence I. Ezeilo (Ph.D)

Published On: 08/03/2023

Volume: 7

Issue: 2

First Page: 566

Last Page: 577

ISSN: 2454-6186

Cite this Article

Adeneye Olawale Adeleke (Ph.D), Moses O. Anuolam (Ph.D) & Florence I. Ezeilo (Ph.D), The Effect of Monetary Policy on Economic Growth in Nigeria (2004 – 2022), Volume 7 Issue 2, International Journal of Research and Innovation in Social Science (IJRISS), 566-577, Published on 08/03/2023, Available at https://www.rsisinternational.org/journals/ijriss/articles/the-effect-of-monetary-policy-on-economic-growth-in-nigeria-2004-2022/

ABSTRACT

Arguments against and in favor of the effect monetary policy of Central Bank of Nigeria have on economic growth in Nigeria is inconclusive with mixed outcomes. Therefore, this study investigates the effect of monetary policy on the economic growth in Nigeria between 2004 and 2022. The study employed ex-post facto design with time series data covering the period of 19 years. Econometric technique of Auto-regressive distributed lag was used to analyzed the study data. Findings of the study revealed that the entire explanatory variables in the study namely; Monetary Policy Rate (MPR), Money Supply (MS), and Lending Interest Rate (LNR) at level equation and period of lag one were statistically significant. In terms of the magnitude, finding of the study revealed that the ARDL coefficients of MPR, MS and LNR are 1861.613, 5.091207 and -3778.871. This suggests that both MPR and MS have positive impact on economic growth while LNR has negative impact on economic growth. More so, one percent increase in MPR and MS leads to approximately, 186 and 509 percent increase in economic growth. In the same vein, one percent increase in LNR will effect -3778 percent decrease in economic growth. As manifested from the findings of this study, the following recommendations are suggested: that monetary policy authority should ensure that status quo should be maintained on both MPR and MS while adjustment should be made on lending rate (LNR) by reducing the rate to encourage investors to borrow for the purpose of investment and subsequently, economic growth.

Key Words: Monetary Policy, Monetary Policy Rate, Money Supply, Lending Interest rate and Economic Growth

INTRODUCTION

According to Central Bank of Nigeria (2021) monetary policy is an arrangement or a purposeful measure which is designed to regulate the value, supply and cost of money in an economy in consonance with the expected level of economic activity. However, monetary authority via central bank uses various monetary policy instruments which include; monetary policy rate, money supply, lending interest rate, cash reserve ratio, discount rate, open market operation among other instrument in targeting at controlling volume of money in circulation either directly or indirectly.

However, monetary policy instruments understudy in this study is limited to most commonly employed namely; monetary policy rate, money supply and lending interest rate. The role of monetary policy on the economic development and the changing in an aggregate economic activity depends on how monetary policy is conducted and the independence of the central bank to choose the appropriate monetary tools to formulate the monetary policy of macroeconomic objectives (Alavinasab, 2016). Conceptually, the monetary policy rate also refers to policy interest rate is an interest rate that the monetary authority (i.e. the central bank) sets in order to influence the evolution of the main monetary variables in the economy (e.g. consumer prices, exchange rate or credit expansion, among others). The policy interest rate determines the levels of the rest of the interest rates in the economy, since it is the price at which private agents-mostly private banks-obtain money from the central bank. These banks will then offer financial products to their clients at an interest rate that is normally based on the policy rate. Different countries have different policy interest rates. The most common are the overnight lending rate, discount rate and repurchase rate (of different maturities).

Normally, central banks use the policy interest rate to perform contractive or expansive monetary policy. A rise in interest rates is commonly used to curb inflation, currency depreciation, excessive credit growth or capital outflows. On the contrary, by cutting interest rates, a central bank might be seeking to boost economic activity by fostering credit expansion or currency depreciation in order to gain competitiveness. Thus, monetary policy plays a stabilizing role in influencing economic growth through a number of channels such as monetary policy rate, money supply and lending interest rate. These aforementioned variables is been measured by time series data released annually by monetary policy authority headed by Central Bank of Nigeria.

Understanding the significant impact of monetary policy on economic growth is inevitable because any monetary policy alteration in any nation is expected to change the level of stock money in circulation thereby influences the rate at which productivity take place and subsequently affects economic growth. Particularly, monetary policy aiming at controlling the level of money in economy in order to checkmate raising inflation, increase in unemployment and economic stability.

However, with current dismal economic outlook of Nigeria as a nation the extent to which monetary policy via monetary policy rate, money supply and lending interest rate impacts economic growth is debatable which called for empirical research. It is against this background that this study examines the impact of monetary policy via monetary policy rate, money supply and lending interest rate on the economic growth in Nigeria between 2004 and 2022.

Statement of the Problem

Despite, the Central Bank of Nigeria (CBN) effort through application of monetary policy measures Nigerian economy is still faced with mirage of problems which is linked to stock of money in circulation. This is because the volume of money in economy determines its economic stability and subsequently, increases or declining in economic growth. Theory and empirical evidence in the literature suggest that sustainable long term growth is associated with lower price levels. In other words, high inflation is damaging to long-run economic performance and welfare. Monetary policy has far reaching impact on financing conditions in the economy, not just the costs, but also the availability of credit, banks’ willingness to assume specific risks, etc. It also influences expectations about the future direction of economic activity and inflation, thus affecting the prices of goods, asset prices, exchange rates as well as consumption and investment.

However, the impact of monetary policy on economic growth in Nigeria and elsewhere is inconclusive with mixed outcomes in both empirical and theoretical literatures. Some studies argue that monetary policy have positive and significant impact on economic growth while others opinion were on the contrary. Studied like Ajibola and Oluwole (2018); Lacker (2014); Lashkary and Kashani (2011) were of the opinion that monetary policy through increase in money supply have adverse effect on economic growth via inflation.

While, studied like; Anowor and Okorie (2016); Chipote and Makhetha-Kosi (2014); Fasanya and Onakoya, (2013) concluded that monetary policy has positive and statistically significant impact on economic growth. These empirical literatures outcomes suggest inconclusiveness. Therefore, the need to ascertain the exact impacts monetary policy has on economic growth in Nigeria between the periods spanning from 2004 to 2022.

LITERATURE REVIEW

Conceptual Review

Conceptually, monetary policy consists of those actions designed to influence the behavior of the monetary sector (Ajibola & Oluwole, 2018). According to Thomas (2022) monetary policy is a set of tools that a nation’s central bank use to promote sustainable economic growth and controlling the overall supply of money that is available to the nation’s banks, its consumers, and its businesses. In other words, monetary policy is a policy employ by Central Bank of a nation to control the supply of money in circulation (Simon & Elias, 2021).

According to CBN (2021), monetary policy is a tool of general macroeconomic management, under the control of the monetary authorities, designed to achieve government economic objectives such as economic growth, price stability, employment generation and balance of payment equilibrium among other. Furthermore, Adigwe, Echekoba and Justus (2015) posited that monetary policy is a major economic stabilization weapon which involves measures designed to regulate and control the volume, cost, availability and direction of money and credit in an economy to achieve some specified macroeconomic policy objectives. In sum, monetary policy is the policy employed by the monetary authority of a nation to checkmate either the interest rate payable for short-term borrowing by banks from each other to meet their short-term needs or the money supply, frequently as an effort to reduce inflation or the interest rate, to ensure price stability and general trust of the value and stability of the nation’s currency. In Nigeria, according to Simon and Elias, (2021) among other several objectives, monetary policy is designed to achieve price stability, balance of payment equilibrium and high rate of economic growth.

Similarly, in macroeconomics, the money supply (or money stock) refers to the total volume of currency held by the public at a particular point in time. There are several ways to define “money”, but standard measures usually include currency in circulation (i.e. physical cash) and demand deposits (depositors’ easily accessed assets on the books of financial institutions) According to Adeneye (2021) lending interest rate is the price a borrower pays for the use of money they borrow from a lender. It is what banks charge each other for overnight loans. Interest rate is the proportion of a loan that is charged as interest to the borrower, typically expressed as an annual percentage of the loan outstanding. Interest refers to the cost of borrowing money or the reward for saving (Banton, (2020) cited in investopedea.com, 2021). Also according to Marco and Hernandez, (2021) an interest rate is the cost of asking for a loan or saving money. It is calculated as a percentage of the amount that was delivered by a bank, financial institution, or individual. An interest rate is a percentage charged on the total amount one borrows or saves. It is the amount charged on top of the principal by a lender to a borrower for the use of the lender’s assets (Central Bank of Nigeria, 2021).

Theoretical Review

Quantity theory of money propounded by Irving Fisher (1911) and Milton Friedman (1963) as well as Keynesian theory (1936) on money and interest was adopted in this study. The quantity theory of money expresses the relationship between the quantity of money and the price in the form of an equation called “an equation of exchange. The quantity theory of money states that the quantity of money is the main determinant of the price level or the value of money. Any change in the quantity of money produces an exactly proportionate change in the price level. Fisher, stated that all things remaining unchanged, as the quantity of money in circulation increases, the price level also increases in direct proportion and the value of money decreases and vice versa. Thus, the quantity theory of money says that the level of prices varies directly with quantity of money (Ahuja, 2011). This equation of exchange is as follows

PT = MV …………………………………………………………….. (1)

Where: P =Average price level; T =Total amount of transactions; M =Quantity of money

V =Transactions velocity of circulation of money. Thus, T and V are fixed. The quantity theory of money simply indicates that the level of price is a function of the supply of money. For Walras, Marshall, Wicksell and Pigou (the Classical school) this can be expressed as:

M = KPY …………………………………………………… ………..(2)

Where: K = Fraction of income; M = Quantity of money; P = Price level; Y = Value of goods and services. The K is related to velocity of circulation of money V in Fisher’s transactions approach

In Keynesian theory (1936) monetary theory explains the effect of variation in money supply on the level of economic activity through its effect on the rate of interest which determines investment in the economy. Keynes does not agree with the older quantity theorists that there is a direct and proportional relationship between quantity of money and prices; rather the effect of a change in the quantity of money on prices is indirect and non-proportional. Keynesians propose that “money does not really matter to determine the price level, hence unable to significantly impact on economic growth. Keynes in principle believes that velocity of circulation was volatile and there often existed underemployment of resources due to recessionary conditions in the economy. Therefore, Keynesian economics believe that there was no strong automatic tendency for output and employment to move towards full employment levels (Keynes, 1936).

Empirical Review

Henry and Sabo (2020) examine the impact of monetary policy management on inflation in Nigeria between the periods of 1985- 2019. Autoregressive distributed lag analysis was employed. Finding of the study showed that while monetary policy rate and foreign exchange rate impacted negatively on inflation; broad money supply impact positively on it. Kayode, Isreal and onyuka (2020) examine the impact of money supply on savings and investment in developing countries between the period of 1999 and 2016. The study employed multiple regression technique. Finding of the study revealed that money supply have significant impact on savings and investment.

Abiodun and Ogun (2019) studied investigated the asymmetric effect of positive and negative monetary policy shocks on output and prices in Nigeria with a view of ascertaining the impact of monetary policy on sustainable output growth and price stability in Nigeria from 1986 to 2016. Non-linear Autoregressive Distributive Lag (NARDL) was employed. The study results showed that monetary policy shocks have asymmetric effects on output and prices in Nigeria both in the short and long run period. Ajibola and Oluwole (2018) examined the impact of monetary policy on economic growth in Nigeria between period of 1981 and 2016. The study adopted Johansen Co-integration test and Vector Error Correction Mechanism (VECM). The finding of the study revealed that, two variables (money supply and exchange rate) had a positive and insignificant impact on economic growth. Furthermore, the interest rate and liquidity ratio on the other hand, have a negative and significant impact on economic growth.

Inam and Ime (2017) investigate the impact of money supply on the economic growth in Nigeria between the periods of 1970 and 2012. The study employed Ordinary Least Square (OLS) techniques and the granger causality test. Findings of the study revealed a positive and insignificant relationship between money supply and economic growth. Khaysy and Gang (2017) examine the impact of monetary policy on the economic development in Lao People’s Democratic Republic between the period of 1989 and 2016. The study employed Johansen Cointegration and Error Correction Finding of the study reveal that money supply, interest rate and inflation rate have negative effect on the real GDP per capita in the long run while real exchange rate has a positive effect.

Alavinasab (2016) examines the impact of monetary policy on economic growth in Iran using, time series data between the period of 1971 and 2011. The study employed Multiple Regression Method and Error Correction Model (ECM). The findings of the study reveal that in the long run money supply, exchange rate and inflation rate have insignificant impact on economic growth while in the short run, money supply and exchange rate have significant impact on economic growth. Chipote and Makhetha-Kosi (2014) examine the role of monetary policy in promoting economic growth in the South African economy between the period of 2000 and 2010. The study employed Johansen co-integration and the Error Correction Mechanism. Findings of the study reveal that a long run relationship exists among the variables. Furthermore, findings of this study show that money supply, and exchange rates are insignificant monetary policy instruments that drive growth in South Africa whilst inflation is significant. Several empirical researches have been conducted to investigate the impact of monetary policy on economic growth in various countries. However, findings of these studied suggest inconclusiveness and mixed outcomes thus, suggesting that there is still a gap in literature.

Theoretical Framework

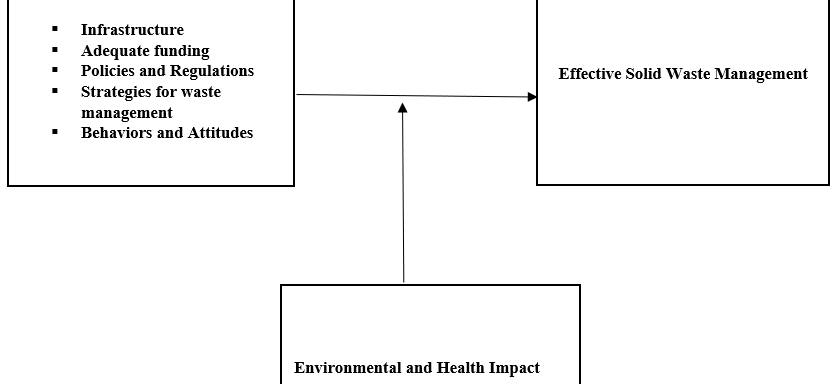

Figure 1: Theoretical Framework of this study

Source: The researchers concept (2022)

Figure 1 above depicts the impact of monetary policy via monetary policy rate, money supply and lending interest rate on economic growth. Each arrow pointed to economic growth simply suggests that any changes in any of these aforementioned variables will causes changes in economic growth.

RESEARCH METHODOLOGY

This study is ex-post facto research design also known as quasi-experimental study or after-the-fact research. Secondary data from Central Bank of Nigeria (2022) on variables which includes; monetary policy rate, (MPR), money supply (MS) and lending interest rate (LNR) and economic growth proxy by (GDP) in Nigeria, between 2004 and 2022 were sourced. Thereafter, econometric techniques analysis of autoregressive distributed lag (ARDL) was employed to analyze the data sourced in model specified. Eview 10 was used to generate and analyzes descriptive as well as inferential statistics for the study. However, the analysis includes both residual and coefficient diagnostics tests in order to satisfy certain econometric assumptions.

Model Specification

ARDL models are linear time series models in which both the dependent and independent variables are related not only contemporaneously, but across historical (lagged) values as well.

Although ARDL models have been used in econometrics for decades, they have gained popularity in recent years as a method of examining cointegrating relationships. ARDL models are especially advantageous in their ability to handle cointegration with inherent robustness to misspecification of integration orders of relevant variables. This study adopts the unrestricted autoregressive distributed lag model developed by Pesaran, Shinb and Smith (2001) by introduced different variables as oppose original model developed by Pesaran, Shinb and Smith (2001) as follows;

Where GDPt is a proxy for economic growth at time t; MPRt stand for monetary policy rate at time t; MSt represents money supply at time t; and LNRt is lending interest rate at time t. furthermore, Δ is a difference operator, t is time, β0 is an intercept term, β1, β2, and β3 𝛿1to 𝛿3 are the coefficients of their respective variables and ps are the lag lengths. To examine the existence of long-run relationship following Pesaran et al (2001), the study first test, based on Wald test (F-statistics), for the joint significance of the coefficients of the lagged levels of the variables, i.e. Ho: 𝛿1= 𝛿2 = 𝛿3 = 0 and H1: 𝛿1 ≠ 𝛿2 ≠ 𝛿3 ≠0

The asymptotic critical values bounds, which are tabulated in Pesaran et al (2001), provide a test for cointegration with the lower values assuming the regressors are I(0), and upper values assuming purely I(1) regressors. If the calculated F-statistics exceeds the upper critical value, the null hypothesis is rejected, implying that there is cointegration. However, if it is below the lower critical value, the null hypothesis cannot be rejected, indicating lack of cointegration. If the calculated F-statistics falls between the lower and upper critical values, the result is inconclusive. Once cointegration is established, the conditional ARDL long-run model can be estimated as:

In the next step, we obtain the short-run dynamic parameters by estimating an error correction model associated with the long-run estimates. This is specified as follows:

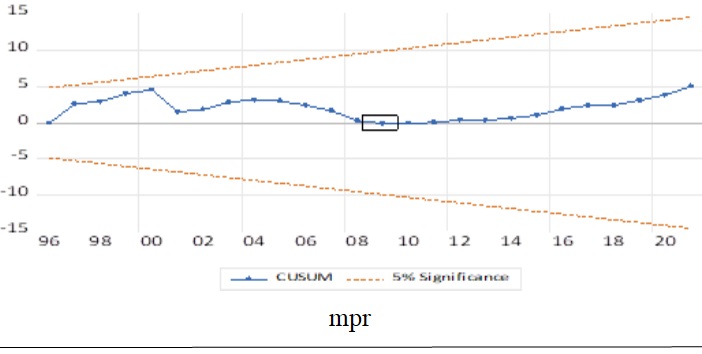

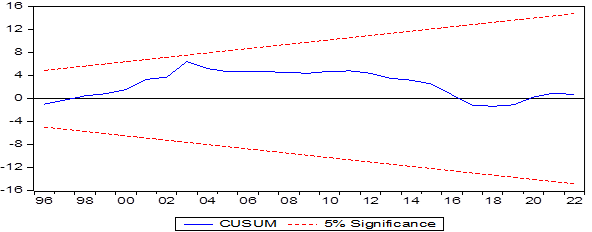

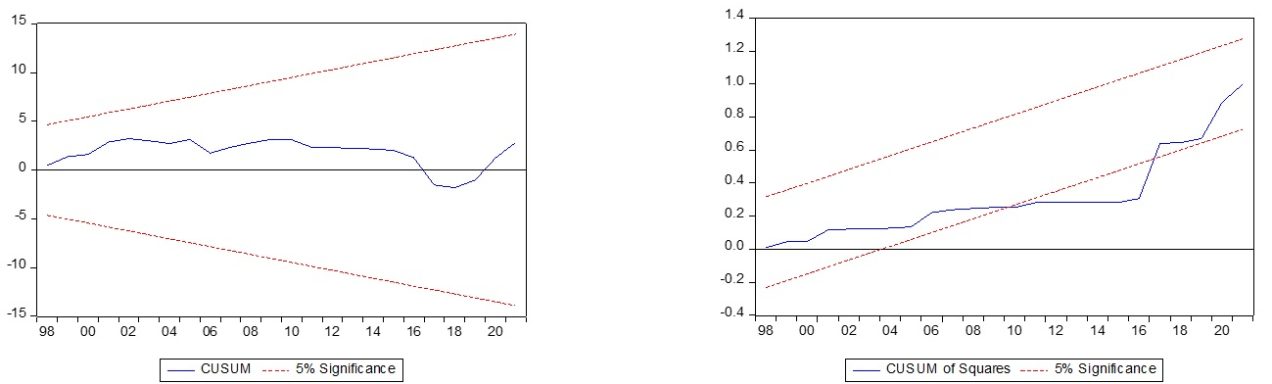

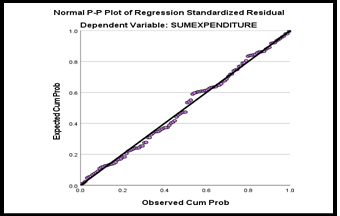

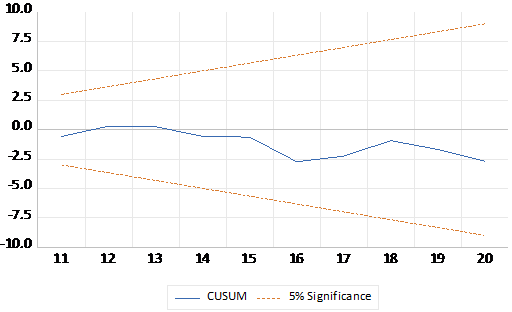

Where 𝑒𝑐𝑚 is the error correction representation of equation (2) and 𝜗 is the speed of adjustment. Where 𝜗 is the speed of adjustment parameter and ECM is the residuals that are obtained from the estimated co-integration model of equation. Peseran et al., (2001) suggested applying the cumulative sum of recursive residuals (CUSUM) and the cumulative sum of squares of recursive residuals (CUSUMSQ) tests whose equation is detailed in Brown et al., (1975) to assess the parameter constancy of the model. The justification for co-integration and error correction model is to add richness, flexibility and versatility to the econometric modeling and to integrate short-run dynamics with long-run equilibrium. Hence, accurate predictions can be more confidently made on the economic relationship between the variables.

DATA ANALYSIS AND RESULTS PRESENTATION

The results of data analysis are reported in the following subsections.

Table 1 Descriptive Statistics

| GDP | MPR | MS | LNR | |

| Mean | 85737.05 | 11.31579 | 19635.48 | 16.43737 |

| Median | 81009.96 | 11.50000 | 18743.07 | 16.85000 |

| Maximum | 176075.5 | 16.50000 | 48518.73 | 19.33000 |

| Minimum | 18124.06 | 6.000000 | 2131.820 | 11.55000 |

| Std. Dev. | 49736.07 | 2.663855 | 13678.58 | 2.147109 |

| Skewness | 0.326522 | -0.293590 | 0.483920 | -0.897546 |

| Kurtosis | 1.871503 | 2.825350 | 2.230436 | 3.183389 |

| Jarque-Bera | 1.345811 | 0.297098 | 1.210414 | 2.577655 |

| Probability | 0.510224 | 0.861958 | 0.545961 | 0.275594 |

| Sum | 1629004. | 215.0000 | 373074.2 | 312.3100 |

| Sum Sq. Dev. | 4.45E+10 | 127.7303 | 3.37E+09 | 82.98137 |

| Observations | 19 | 19 | 19 | 19 |

Source: Researcher Computation using Eview 10

Table 1 presents the descriptive statistics which describes the characteristic of the data used in the study. The study observation is 19. The result shows that both GDP and MS the distribution skewed toward right while MPR and LNR are skewed toward left. In the same vein, kurtosis distribution shows that the entire exhibited relative to normal skewness and leptokurtic. If the kurtosis exceeds 3, the distribution is peaked (leptokurtic) relative to the normal; if the kurtosis is less than 3, the distribution is flat (platykurtic) relative to the normal. The Jarque-Bera test statistic which measure the difference of the skewness and kurtosis of the series with those from the normal distribution show that all the variables understudy were all significant with the probability that a Jarque-Bera statistic exceeds (in absolute value) the observed value under the null hypothesis – a small probability value leads to the rejection of the null hypothesis of no normal distribution.

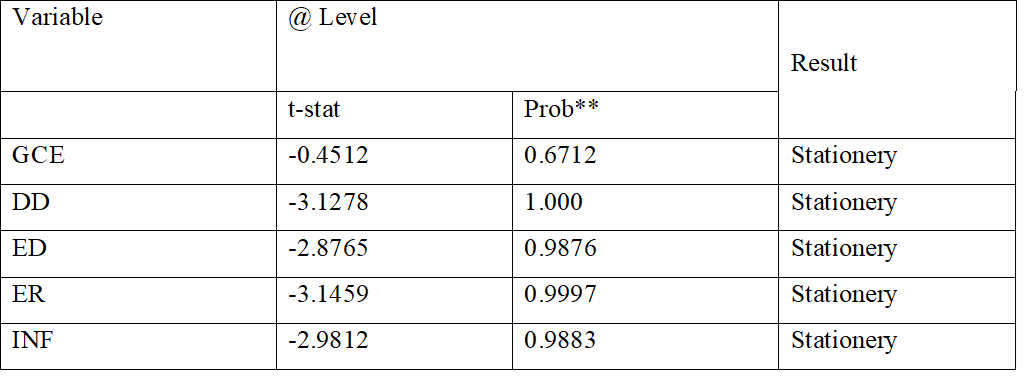

Table 2 Series of Augmented Dickey-Fuller Test (ADF) Output Results

| Coefficients | Critical Values at 5% | ADF Values | Probability | Comments |

| D(GDP) | -3.081002 | -2.011339 | 0.2792 | I(I) |

| D(MPR) | -3.052169 | -3.809911 | 0.0116 | I(0) |

| D(MS) | -3.052169 | -2.059567 | 0.2614 | I(I) |

| D(LNR) | -3.052169 | -4.063274 | 0.0071 | I(0) |

Source: Researchers Computation Using (Eviews 10.0 Output)

Table 2 present the series of unit root tests of (ADF). The results show that all the variables are not stationary of order I(0) in first differencing, there is evidence of mixed unit root test result. GDP and MS are not stationary while, MPR and LNR are stationary.

Table 3 Autoregressive Distributed Lag Estimate.

| Dependent Variable: GDP | ||||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob.* | ||

| GDP(-1) | -1.713435 | 0.724132 | -2.366192 | 0.0422 | ||

| MPR | 586.8843 | 856.6960 | 0.685055 | 0.5106 | ||

| MPR(-1) | 1861.613 | 784.9044 | 2.371771 | 0.0418 | ||

| MS | 0.244062 | 1.146691 | 0.212840 | 0.8362 | ||

| MS(-1) | 5.091207 | 2.176705 | 2.338951 | 0.0441 | ||

| MS(-2) | 4.906794 | 1.248084 | 3.931460 | 0.0035 | ||

| LNR | -3778.871 | 1376.144 | -2.745985 | 0.0226 | ||

| C | 89512.51 | 26453.66 | 3.383747 | 0.0081 | ||

| R-squared | 0.993565 | Mean dependent var | 93397.53 | |||

| Adjusted R-squared | 0.988559 | S.D. dependent var | 46795.03 | |||

| S.E. of regression | 5005.223 | Akaike info criterion | 20.17954 | |||

| Sum squared resid | 2.25E+08 | Schwarz criterion | 20.57164 | |||

| Log likelihood | -163.5261 | Hannan-Quinn criter. | 20.21851 | |||

| F-statistic | 198.5046 | Durbin-Watson stat | 1.850292 | |||

| Prob(F-statistic) | 0.000000 | |||||

| *Note: p-values and any subsequent tests do not account for model selection | ||||||

Source: Researcher Computation using Eview 10

Table 3 presents, ARDL regression estimation, the first part of the output gives a summary of the settings used during estimation. The dependent variable lag is 2 while the regressor is fixed at C including observation 17 after adjustment. However, the coefficient of Gross Domestic Product GDP(-1) at period of lag 1 is approximately -1.71 relatively low but, statistically significant with the probability value of 0.04 at 0.05 level of significance. This implies that other independent variables remain constant a one percentage increase in GDP at period of lagged 1 translates to approximately -171% decreases in its present value. More so, the coefficients of the monetary policy rate (MPR) at current level and period of lag 1 are 586.88 and 1861.61 positively assigned with probability values of 0.51 and 0.04 respectively. MPR at current level is statistically insignificant while at period of lag 1, is statistically significant at 0.05 percent level of significance. This result suggests that monetary policy rate (MPR) period of lag 1 has positive and statistically significant impact on economic growth. One percent increase in monetary policy rate (MPR) effect an approximately, 1861% increase in economic growth (GDP).

In the same vein, money supply [MS, MS(-1) and MS(-2)] that is, at current, period of lag 1 and 2 respectively, have coefficients of 0.24, 5.09 and 4.91 positively assigned with probabilities of 0.84, 0.04 and 0.00 the result suggests that money supply have positive and statistically significant impact on economic growth both period of lag 1 and 2 respectively. This result indicates that both MPR and MS move in the same direction with economic growth.

On the contrary, the coefficient of the lending interest rate (LNR) at current period is -3778.871 negatively assigned with the probability value of 0.02 statistically significant at 0.05 level of significance This suggests that one percent increase in LNR causes about -3778% decrease in economic growth. The result indicates that LNR and economic growth move in opposite direction.

Coefficient of fixed variable that is, constant (C) also known as the intercept is the value of economic growth when other independent variables have a value of zero is 89512.51 statistically significant with probability value of 0.00 at 0.05 level of significance. This result simply suggests that increase in economic growth in Nigeria is associated with other factors which are not explained by any of the explanatory variables stated in the model.

More so, the R-Square which is the coefficient of determination and also known as a measures of the goodness-of-fit, is 0.99, approximately 99%. This means that 99% of the changes in economic growth (GDP) at time t, are explained by the changes in the explanatory variables while, the remaining 1% could be explained by factors outside this model represented by error term. Similarly, adjusted R-squared, value is 99% which explained the variation in the dependent variable that is explained by only those independent variables. The overall model measured by F-statistics is 198.5046 with probability value 0.00 indicating that the model is good fit. More so, Durbin-Watson statistic (DW) is 1.8 approximately 2 shows there is no serial autocorrelation.

Table 4 below presents ARDL Long Run Form and Bounds Test on which decision to conduct ARDL Error Correction Regression is based

Table 4a ARDL F-Bounds Test

| F-Bounds Test | Null Hypothesis: No levels relationship | |||

| Test Statistic | Value | Significance. | I(0) | I(1) |

| Asymptotic: n=1000 | ||||

| F-statistic | 9.626231 | 10% | 2.37 | 3.2 |

| K | 3 | 5% | 2.79 | 3.67 |

| 2.5% | 3.15 | 4.08 | ||

| 1% | 3.65 | 4.66 | ||

Source: Researcher Computation usingEview10

Table 4 present the F-bound test of null hypothesis of no cointegration regression estimation in order to confirm the no long-run cointegration status. The calculated F-statistics of 9.626231 exceeds the lower and upper critical values of 2.79 and 3.67 respectively at 5% significant level. Therefore, the null hypothesis of no cointegration is rejected, implying that there is cointegration thus the long run relationship estimate is justified.

Table 4b ARDL Long Run Form and F-Bounds Test

| Conditional Error Correction Regression | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 89512.51 | 26453.66 | 3.383747 | 0.0081 |

| GDP(-1)* | -2.713435 | 0.724132 | -3.747156 | 0.0046 |

| MPR(-1) | 2448.498 | 1053.992 | 2.323070 | 0.0453 |

| MS(-1) | 10.24206 | 2.626533 | 3.899462 | 0.0036 |

| LNR** | -3778.871 | 1376.144 | -2.745985 | 0.0226 |

| D(MPR) | 586.8843 | 856.6960 | 0.685055 | 0.5106 |

| D(MS) | 0.244062 | 1.146691 | 0.212840 | 0.8362 |

| D(MS(-1)) | -4.906794 | 1.248084 | -3.931460 | 0.0035 |

| * p-value incompatible with t-Bounds distribution. | ||||

| ** Variable interpreted as Z = Z(-1) + D(Z). | ||||

Source: Researcher Computation usingEview10

Table 4b results shows that at period of lag 1 the entire variables understudy were statistically significant at 0.05 levels of significance and were positively related exception of LNR which has negative sign. However, Conditional Error Correction Regression consequently produced levels equation alongside the conditional error correction regression outcome. The result at level equation is presented in table 4c as follows.

Table 4c Levels Equation

| Case 2: Restricted Constant and No Trend | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| MPR | 902.3610 | 321.4065 | 2.807538 | 0.0205 |

| MS | 3.774575 | 0.093380 | 40.42146 | 0.0000 |

| LNR | -1392.652 | 315.3940 | -4.415595 | 0.0017 |

| C | 32988.64 | 5384.375 | 6.126735 | 0.0002 |

| EC = GDP – (902.3610*MPR + 3.7746*MS -1392.6523*LNR + 32988.6377 ) | ||||

Source: Researcher Computation using Eview10

Table 4c, levels equation shows that all the entire explanatory variables are statistically significant based on the probability values of 0.00 less than 0.05% level of significance. This result at level equation simply reveals the directions and magnitude of the relationship between dependent and independent variables. Finally, table 5 present the error correction regression as follows;

Table 4c ARDL Error Correction Regression

| ECM Regression Case 2: Restricted Constant and No Trend | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| D(MPR) | 586.8843 | 563.7345 | 1.041065 | 0.3250 |

| D(MS) | 0.244062 | 0.570185 | 0.428040 | 0.6787 |

| D(MS(-1)) | -4.906794 | 0.983748 | -4.987858 | 0.0008 |

| CointEq(-1)* | -2.713435 | 0.325429 | -8.338032 | 0.0000 |

| R-squared | 0.782582 | Mean dependent var | 7972.575 | |

| Adjusted R-squared | 0.732409 | S.D. dependent var | 8050.764 | |

| S.E. of regression | 4164.598 | Akaike info criterion | 19.70895 | |

| Sum squared resid | 2.25E+08 | Schwarz criterion | 19.90500 | |

| Log likelihood | -163.5261 | Hannan-Quinn criter. | 19.72844 | |

| Durbin-Watson stat | 1.850292 | |||

Source: Researcher Computation using Eview10

The result shows that, the CointEq(-1) coefficient of the error correction term which measures the speed of adjustment towards long-run equilibrium is negative and statistically significant at 5% level. The ECM has the expected negative sign which stands at -2.71. This implies that the rate at which changes in GDP at time t, adjusts to the single long-run co-integrating relationship is different from zero. The coefficient of the ECM revealed that the speed with which changes in GDP at time t, adjusts respond to regressors is about -27% in the short-run. This is in conformity with this study aprior expectation.

CONCLUSION AND RECOMMENDATIONS

This study examines the impact of monetary policy via monetary policy rate, money supply and lending interest rate on economic growth in Nigeria between 2004 and 2022. Autoregressive Distributed Lag Regression Estimate (ARDL) was conducted to analyze short-run and long-run impacts of these aforementioned variables on gross domestic product as a proxy for economic growth.

Findings of the study revealed that the entire explanatory variables in the study namely; Monetary Policy Rate (MPR), Money Supply (MS), and Lending interest rate (LNR) at level equation and period of lag one were statistically significant. In terms of the magnitude, finding of the study revealed that the ARDL coefficients of monetary policy rate, money supply and lending interest rate are 1861.613, 5.091207 and -3778.871. This suggests that both monetary policy rate and money supply have positive impact on economic growth. That is both monetary policy rate and money supply move in the same direction with economic growth while lending interest rate has negative impact on economic growth. Meaning that, lending interest rate is moving in the opposite direction with economic growth. More so, one percent increase in monetary policy rate and money supply leads to approximately, 186 and 509 percent increase in economic growth. In the same vein, one percent increase in lending interest rate will effect -3778 percent decrease in economic growth. As manifested from the findings of this study, the following recommendations are suggested: that monetary policy authority should ensure that status quo should be maintained on both monetary policy rate and money supply while adjustment should be made on lending interest rate by reducing the rate to encourage investors to borrow for the purpose of investment and subsequently, economic growth.

References

- Abiodun S. O. and Ogun, T.P.(2019). Asymmetric effect of monetary policy shocks on output and prices in Nigeria. African Journal of Economic Review,7(1), 238-248.

- Adeneye, O.A. (2021) Interest Rate and Exchange Rate Volatility on the Performance of Industrial Sector in Nigeria. Lafia Journal of Economics and Management Sciences, 6(1), 1- 12: ISSN: 2550-732X. Published by Department of Economics, Federal University of Lafia, Nigeria

- Adigwe, P. K, Echekoba F.N, and Justus B.CO.(2015).Monetary policy and economic growth in Nigeria: A critical evaluation. IOSR Journal of Business and Management, 17(2),110-119. e-ISSN:2278-487X, p-ISSN: 2319-7668 (www.iosrjournals.org)

- Ahuja, H. L. (2011). Macroeconomics Theory and Policy, 7th Revised Edition. S. Chand. & Company Ltd, New York

- Ajibola, A and Oluwole, A. (2018). Impact of monetary policy on economic growth in Nigeria. Open access library journal, 5( e4320): ISSN print: 2333-9705, ISSN online: 2333-9721.

- Alavinasab, S.M. (2016).Monetary policy and economic growth: A case study of Iran. International journal of economics, commerce and management, 6(3),2016 ISSN 2348 0386.

- Anowor, O.F., and Okorie, G.C. (2016). A reassessment of the impact of monetary policy on economic growth: Study of Nigeria. International journal of developing and emerging economies, 4(1):82-90, february 2016.

- Banton, C. (2020). What is an interest rate? https://www.investopedia.com/terms/i/interestrate.asp

- Central Bank of Nigeria (2021) Monetary Policy Review, CBN, Abuja

- Chipote, P and Makhetha-Kosi, P.(2014). Impact of monetary policy on economic growth: A case study of South Africa. Mediterranean journal of social sciences, MCSER publishing, Rome-Italy. 5(15):76-84. ISSN 2039-9340(Print) ISSN 2039-2117(Online)

- Fasanya, I.O. and Onakoya, A.B.O. (2013) Does monetary policy influence economic growth in Nigeria? Asian economic and financial review, 3,(5) 635-646.

- Henry, E.A and Sabo, A.M.(2020).Impact of monetary policy on inflation rate in Nigeria: Vector Autoregressive Analysis, Bullion. 44(4),6. https://dc.cbn.gov.ng/bullion/vol44/iss4/6

- Inam, U. S and Ime, B. S. (2017). Monetary policy and economic growth in Nigeria: Evidence from Nigeria. Advances in social sciences research journal, 4(6) 41-59

- Kayode O. B, Israel O. U.and Onyuka F. M.(2020). The impacts of monetary policies on savings and investment in developing economies: A case study. halid: hal-02520027 https://hal.archives-ouvertes.fr/hal-02520027 Preprint submitted on 26 Mar 2020

- Khaysy, S and Gang, S.(2017).The impact of monetary policy on economic development: evidence from Lao PDR. Global journal of human social science (e),17(2):1

- Lacker, J.M. (2014). Can monetary policy affect economic growth? Johns Hopkins Carey business school, Baltimore, Maryland.

- Lashkary, M., and Kashani, B. H. (2011). The Impact of monetary variables on economic growth in Iran: A monetarists’ approach. World applied sciences journal, 15(3), 449–456. Retrieved from http://idosi.org/wasj/wasj15(3)11/22.pdf.

- Marco, A and Hernandez, C.(2021).Interest rate Definition; https://study.com/academy/lesson/what-is-interest-rate-definition-types-history.html

- Pesaran, M.H., Shin, Y., and Smith, R.J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16, 289–326. /(ISSN)1099-1255

- Simon N.N and Elias I.A.(2021). Effects of monetary policy measures on Nigeria’s economic growth. Journal on banking financial services & insurance research. 11(5), ISSN:(2231-4288) www.skirec.org.

- Thomas, B. (2022) in Investopedia Team. (2022). What is monetary policy https://www. investopedia.com/terms/m/monetarypolicy.