An Analysis of Personal Financial Literacy among Teachers in Secondary Schools

- Marvin Kapenda

- 226-240

- Sep 22, 2023

- Education

An Analysis of Personal Financial Literacy among Teachers in Secondary Schools

Marvin Kapenda

Department of Educational Psychology, Sociology and Special Education, University of Zambia, P.O. Box 32377, Lusaka, Zambia.

DOI: https://doi.org/10.51244/IJRSI.2023.10818

Received: 13 July 2023; Revised: 15 August 2023; Accepted: 19 August 2023; Published: 22 September 2023

ABSTRACT

The aspect of literacy in the education sector has been aligned to the ability to read and write. Therefore, scholars have suggested that teachers are the most endowed professionals in relation to academic literacy, but there are a few studies conducted to determine teacher’s financial literacy. The main objective of the study was to analyse personal financial literacy among teachers in secondary schools. The study sampled 354 secondary school teachers from ten government secondary schools between the ages 24 and 55 years. Using qualitative and quantitative methods (Mixed method) and a questionnaire/interview guide to collect data, the results of the study revealed that financial literacy levels among secondary school teachers demonstrate that teachers in areas of long term planning attitude shows high or positive results while the aspects of saving, spending behaviour and tracking finances through record keeping was low or negative results. However, some teachers demonstrated some considerable financial knowledge on the concept of financial literacy with a percentage of 44% and also performed below par on the segment of spending and keeping financial records. Therefore, the study recommended, strengthening of financial literacy in the teacher education curriculum, various teacher organisations and unions provide seminars on financial literacy for their members to ensure that they are financially secure and the need for a collaboration between the Ministry of Education and the Ministry of Finance to develop mechanisms of disseminating information materials on financial literacy to teachers. This study is significant as it could be used as an evaluation tool for the national strategy on financial education (NSFE II) for Zambia (2019 –2024) which sets out the framework for improving financial education in Zambia.

Keywords: Finance; Literacy; National strategy on financial education; financial planning; financial education.

INTRODUCTION

Discussions of financial literacy have gained prominence in all sectors around the world. The education sector is no exception to such a topic, especially that many governments have put deliberate policies to promote financial inclusion among their citizens. The global average score of financial literacy is 61%, [1] indicating that many people lack the information and abilities necessary to make wise financial decisions, which could result in instability and insecurity in one’s financial situation. By virtue of being prominent people in society, teachers are expected to have the capacity to apply knowledge and skills and to properly manage financial resources for long-term financial well-being. Financial literacy is the process through which people get a better knowledge of their financial position and learn how to improve it over time by developing financial habits like as saving, budgeting, and planning, and so making the best financial decisions possible [2].

Concerns regarding the financial literacy of their citizens have been voiced by nations all over the world. According to numerous academics worldwide, the general public pays a large price for low financial literacy [2], [1], [3]. The public’s inadequacy or lack of awareness of financial problems can be attributed to major concerns including poor retirement planning and a lack of savings [4]. Insights from the standard and poor’s ratings services global financial literacy survey provide information on financial literacy around the world, in their report of the country-by-country breakdown of adults who are financially literate, Zambia was rated at 40% compared to the 33% worldwide [5].

In the modern world, being able to manage personal finances is becoming more and more crucial. People need to make long-term plans for their investments in retirement and children’s education. Additionally, they must choose between making short-term savings and borrowing money for a trip, a down payment on a home, a vehicle loan, and other significant purchases. They also have to take care of their own health and life insurance requirements [6]. Financial planning, which is crucial to a person’s financial wellbeing, is another area that is mostly influenced by financial literacy.

Planning for the future financially enables people to manage their financial situation. People must identify and establish their priorities in order to accomplish this. The degree to which financial requirements and goals will be satisfied depends on having a strategy for spending, saving, and investing money. Financial planning that takes into account all facets of finances, including budgeting, managing taxes, obligations, buying decisions, managing insurance, managing investments, retirement, and estate planning, is necessary to achieve those goals [7].

Understanding fundamental financial concepts and how to apply them is essential for one’s financial well-being. “Unfortunately, a lot of people don’t understand the fundamentals of personal finance. Concerning attitudes exist in regards to both saving and spending. Information is not the problem; the problem is the ability to understand the information” [8]. On the other hand other scholars pointed out that the interconnectedness of financial markets on a global scale, the advent of increasingly sophisticated new financial products, and the risks that go along with them pose new difficulties for all participants on a personal, institutional, social, and international scale [9]. Nowadays, when a wide spectrum of people have easy access to increasingly complex financial goods, financial literacy is especially crucial. For instance, the number of people with bank accounts and have access to credit products is expanding quickly as governments in many countries try to increase access to financial services. Furthermore, people who previously relied on their jobs or governments for their financial stability after retirement now bear the burden for making decisions [1].

Financial literacy is low in high-income countries and significantly worse in middle- and low-income countries, according to surveys conducted all over the world. In the UK [10], Austria [11], Poland [12], Fiji [13], and Ireland [14], surveys on financial literacy have been undertaken. These surveys’ findings typically confirm that there is little worldwide financial understanding. In the Africa region, Fin Scope surveys—which primarily examine financial access and activity but also gauge a few elements of financial literacy—have been frequently used.

Zambia is not the only country in the world that is making strides through policies to promote financial literacy. Since the last ten years, all the regulatory organisations in India have been working to increase financial literacy [15]. Financial literacy is also being improved by banks and AMCs. After promoting investor awareness campaigns throughout India, they now understand the value of promoting financial literacy education at the secondary school level [15]. This makes it possible for future generations to manage their money wisely and avoid issues when investing [15].

A policy named the National Strategy on Financial Education (NSFE II) for Zambia, 2019 –2024 was adopted by the Government of the Republic of Zambia in response to this realisation that financial literacy in Zambia has become more crucial in recent years [16]. The strategy sets out the framework for improving financial education in Zambia. The main objective of the strategy is to empower Zambians with knowledge, understanding, skills, motivation and confidence to help them to secure positive financial outcomes for themselves and their families.

There seemed to have been a few studies that analyse how this strategy has affected teachers in the education sector. Especially with regards to personal financial literacy. According to [17], a lack of financial literacy skills can result in unwise spending decisions, greater debt, and a wealth gap between generations. For instance, according to the centre for trade policy and development (CTPD), teachers were the majority among 60, 000 civil servants who were burdened by financial debt of which most of them fell victims which resulted to financial challenges and prompted the government to enforce a debt swap as a relief [18].

In the Zambian context such information was attributed to over borrowing by teachers who in the process disturbed their financial income flow at household level. In most cases, fiscal discipline is attributed to financial literacy [19]. General attitudes regarding spending and conserving are also concerning among teachers. It is not so much a dearth of information as it is a lack of capacity to understand it. Many people appear to be unaware of the future financial load they will face as a result of borrowing at exorbitant interest rates. It’s difficult to estimate how many teachers are making poor judgments without knowing all of the details of each instance. However, given a major section of the population’s apparent lack of financial understanding, high rates of consumer bankruptcy, and a big share of the population ill-prepared for retirement, there are causes for concern [8].

In the educational sector, the Financial Education Working Group (FEWG), the Ministry of General Education (MoGE), and the Curriculum Development Centre (CDC) identified what Zambian pupils needed to know about personal finance at all grade levels from kindergarten to grade twelve. As part of a broader assessment of school curricula for primary and secondary schools, MoGE and CDC incorporated financial education into chosen topic syllabi. For all school grades, teachers’ and students’ guides have been written [20].

Furthermore, financial education has been introduced into Grades 7, 9, and 12 examinations. Practicing teachers have received orientation training, and the Ministry of Education has introduced financial education into the syllabi of trainee teachers attending institutions of education. Other school-based initiatives include the formation of financial education clubs by various non-governmental organizations (NGOs); financial education for children through the media (such as television and radio shows and newspaper articles); and the Securities and Exchange Commission’s Capital Markets Schools Challenge, which has reached over 1,000 students [21].

Despite the accomplishments listed above, much less progress was accomplished than predicted in the National Strategy on Financial Education (NSFE). There seem to be factors that imped the progress of financial literacy among secondary school teachers, which this study has analysed. In addition, financial literacy research is becoming increasingly crucial to conduct. It is owing to the fact that financial literacy in Zambian society is still relatively hypothesized, as indicated by the Securities and Exchange Commission’s (SEC) financial study, which found that only 32.5 percent of Zambians knew how to save [21].

In analysing personal financial literacy among teachers in secondary schools, the study acknowledged financial literacy according to [22] as financial decision-making and eventually achieving individual financial well-being depend on having the awareness, information, experiences, attitudes, and behaviours.

Objectives of the Study

This study analysed personal financial literacy among teachers in selected secondary schools of Lusaka District in Zambia. The major objectives of this study were to: to assess teachers’ levels of financial knowledge, to determine how teachers financial literacy affected their financial behaviour, to evaluate how secondary school teachers use financial planning attitude as a strategy for achieving financial goals, to identify challenges which impede enhancement of financial literacy and personal financial planning among secondary school teachers.

Scope of the Study

The research was carried out in five school zones in Zambia’s Lusaka District which were purposively selected. Out of all the ten educational zones in Lusaka as categorized by the District Education Board (DEB), the study in five zones made up 50% above the thumb rule of 30% in terms of sample representation of the entire sample whose results could be generalized to some extent. The study therefore used random numbers method to choose Chilenje, Lusaka central, Kaunda Square, Munali, and Chibolya zones. The division of physical regions such as low densely inhabited areas, peri-urban, and medium densely populated areas was observed by the choosing of the five zones. The study mainly assessed teachers’ personal financial literacy by focusing on teachers’ understanding of budgeting and spending habits, short-term and long term planning attitude.

METHODOLOGY

Research Approach and Design

In order to determine the links among the planning constructs under consideration, including attitude, saving behaviour, spending behaviour, and tracking funds through record keeping, this study was conducted utilising a quantitative and qualitative research paradigms. The study employed explanatory sequential design. An explanatory sequential design consisted of first collecting quantitative data and then collecting qualitative data to help explain or elaborate on the quantitative results.

Participants

Financial education has been incorporated into examinations for Grades 7, 9, and 12. Orientation training for existing teachers has been developed, and Ministry of education has incorporated financial education into syllabi for trainee teachers who attend colleges of education. The reason for selecting teachers is that they are the implementers and key stakeholders for the Ministry of Education and Curriculum Development Centre who incorporated financial education into school curricula for a few subjects in primary and secondary schools. This study used them as a sample because they can serve as role models for their pupils and support their development as financially and socially responsible citizens by having a strong understanding of personal finance and handling it responsibly.

These teachers willingly responded to a questionnaire and answered to interview questions to assess their own level of financial literacy (FL). Examined are the connections between their financial behaviour, financial awareness, and financial literacy and aspects of their professional backgrounds. Lusaka District has the total of 57 government secondary schools and a total number of 4362 secondary school teachers at the time of the study. Therefore, with a population of 4362 as calculated by Rao Soft [23] sample size calculator; at 5% significance level and a confidence level of 95% the representative sample size for this study was 354 secondary school teachers from ten (34 subject teachers and one head teacher from each school) government secondary schools in five zones of Lusaka District making the total number of 10 Headteachers who were the key informants. According to biographical data, respondents in this study were between the ages 24 and 55 years. All schools in the study were purposively selected because they were government schools that were under the FSDP Financial Education Working Group which are part of the Ministry of Education (MoE), and the Curriculum Development Centre (CDC).

Data collection Instruments and Procedures

This study used a questionnaire for 344 teachers and an interview guide for the 10 Headteachers to gather information from the 10 secondary schools in the Lusaka District about their experiences with financial literacy, their knowledge and how their knowledge on financial literacy affected their financial behaviour such as planning, spending and saving. The questionnaire was also utilized to solicit for information regarding their spending behaviour, long term and short term planning attitude, saving and levels of financial knowledge. Closed-ended questions were included in the questionnaire while open ended questions were included in the interview guide. To guarantee that all respondents answered the same questions, standardized questions were utilized in the questionnaire. On the other hand, open ended questions were utilized in the interview guide to elicit replies that were compelled by exploratory, explanatory, and comprehension of aims.

The responses were scored using various types of -point Likert scale, with “never”, “rarely” and “always”. The other scale included “high”, “moderate” and “low”. Before being analysed with SPSS and displayed in the form of tables, the acquired data was assessed and checked for errors. It was done using descriptive statistics including frequencies, percentages, means, and standard deviation. Additionally, factor analysis is used to identify the important components of a few chosen variables that are crucial to analysing financial literacy, spending behaviour, saving and long term personal finance planning attitude. Interview responses made up qualitative part of the data and were analysed using recurring themes.

RESULTS OF THE STUDY

Respondents’ Demographic Characteristics

Financial literacy is influenced by factors like gender, education, income, type of employment, and place of employment. Financial literacy often rises with education level and personal assertiveness [24]. The two factors that have potential to have the biggest an impact on financial capabilities and behaviour are age and employment status [25].

In general, 127 (36 percent) of the 354 people who responded were male, while 227 (64 percent) were female. The age categories were represented as follows: the age group between 20-29 years made up five (5) percent of the total sample size and included eight (8) male and 10 female. In addition, the age group between 30 and 39 year was represented by 177 (50%) participants who included (40) male and 137 female. In addition, age was another important factor that the survey results clearly link to risk. The age group between 40 and 49 years indicated that (54) were male while their female counterparts were 72. Those in the age range of 50 and 59 revealed that (30) were female while (21) were male.

The dominance in the distribution of female teachers was due to a high employment of female teachers by the ministry of education. This observation was also noted by the national statistics which reported that 35.5 percent of teachers are male while 64.5 percent are female [26] compared to the distribution of teachers observed at district level which constituted 1325 (30.4%) male while 3037(69.6%) are female secondary school teachers. The biographic data further suggest that the majority of teachers fall under the age group between 30 and 39 which suggests that middle-aged teachers are financially engaged, as evidenced by their capacity to get loans from various microfinance organizations for both income and non-income producing activities.

Educational Levels of Respondents

For this study, the level of education included a four-category nominal variable namely, diploma, Bachelors, Masters and PhD. Respondents’ educational background was believed to play a major influence in financial literacy and personal financial planning. According to the survey’s findings, male teachers possessed the following education qualifications; (70) were bachelor’s degree holders, (26) had diplomas and (31) had attained master’s degree. The female teachers on the other hand had 107 degree holders, 67 diploma holders and (53) master degree holders. Out of the total number of 354 teachers in this study, 50% possessed bachelor’s degrees, 26% were diploma holders and 24% had attained master’s degree. The findings on the education level of respondents in this study’s illustrate that these individuals were well-read enough to make sound judgments regarding the usage of their finances. Because of their high educational levels, teachers were also capable of comprehending basic fundamental principles and practices of financial literacy.

Work Experience of Respondent

The study anticipated that, the longer a teacher served, the more financially literate. In analysing this view, work or duration of service was solicited from respondents. Contrary to this assumption, the results on work duration indicated that, although the difference in responses was not significant, unexpectedly, participants with more years of service in the teaching fraternity were observed have limited knowledge on financial literacy than those with few years of service in the ministry of education. This was observed from their responses to questions to measure their saving, planning, spending behaviour, long and short term planning attitude suggested which compared the scores of the three groups. The findings are not in tandem with the findings of [27] and [28] who also suggested that people’s financial literacy was associated with work experience. In terms of involvement, participants who had between 5 to 10 years of experience made up (40%) while those had between 11 to 15 years’ experience were (50%), the other (10%) was for those with more than 15 years work experience.

Self-Reported Financial Literacy Levels

The ability to compare financial products and services and make sound, well-informed financial decisions is a crucial part of financial literacy for people. Consumers can handle financial affairs more confidently and respond to news and events that could affect their financial well-being if they have a basic understanding of financial concepts and the ability to apply math abilities in a financial context. The levels of fundamental financial knowledge were examined in this section, with a particular emphasis on the answers provided to five questions meant to assess various facets of information that are frequently seen to be crucial for people making financial decisions.

Participants were asked to rate their level of financial literacy. This question was used to determine how confident teachers were in their own financial literacy, which may have caused them to engage in riskier behaviour in addition to more active financial planning, budgeting, and saving. The research questions sought information regarding the level of financial literacy among secondary school teachers. This was measured using five questions with the scale of ‘I don’t know’, ‘low’, ‘average’ and ‘high’. The first question asked them to explain the concept of financial literacy while the second question asked about simple interest calculation. Question three asked about understanding interest paid on a loan while question four budgeting and the last question asked about calculating price discounts. The results revealed that the majority (44%) of teachers had ‘high’ financial literacy knowledge and understood the concept of financial literacy while (20%) scored average, 30% was for ‘low’ score on the knowledge of financial literacy.

On the other hand, an interview guide question number one aimed at finding out if the (10) key informants had knowledge of what financial literacy was. In responding to the question, teacher One (1) defined financial literacy as;

In my view, financial literacy is the knowledge about the uses of money by an individual or organization.

The other key informants (Headteachers) commented on the issue by stating that financial literacy involved the management of finances such as the personal income and other external financial sources. From the definitions of financial literacy by all the 10 key informants, it showed that they had theoretical knowledge about the concept.

When asked if they had undergone any training in finance, only (43); 12% out of the total of 354 secondary school teachers in the study confirmed to had taken some courses at university level that had a component of financial literacy. The participants further revealed that there was no deliberate policy in their work place which supported financial literacy among teachers, nether was it included in their continuous professional development (CPD) activities.

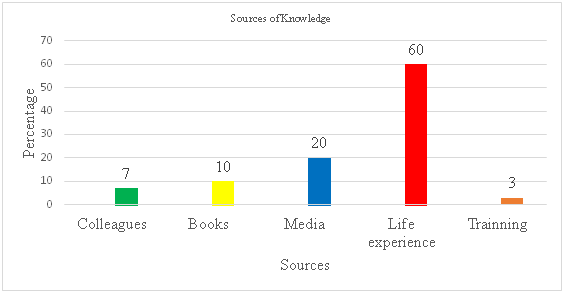

The study further sought to inquire about the sources of knowledge regarding management of personal finances and the results revealed that most teachers acquired finance management knowledge through personal experiences (trial and error) which involved planning and budgeting on a daily basis and management of personal small businesses. Other teachers responded that they had acquired knowledge about management of personal finances from sources such as media, books, colleagues and formal training.

The summary of these findings have been tabulated in figure 1 and shows that the majority (60%) of respondents stated that they acquired knowledge on finance management from life experiences while (20%) of the participating got it from the media. In addition, 10% of the teachers obtained their personal finance management information from reading books while 7% attained from their colleagues through social interactions. There were 3% of the teachers who had formal training in relation to financial management.

Fig 1: Sources of Knowledge of Personal Finance of Teachers

The information from the respondents in the study gives it an impression that the concept of the national strategy on financial education (NSFE II) for Zambia (2019 –2024) which sets out the framework for improving financial education in Zambia has not fully achieved its objective to disseminate financial literacy information among teachers as observed by the high number of teachers who have used their own understanding of the concept of financial literacy. Respondents responses suggest that financial literacy was an abstract to many and not pragmatic. Therefore the results of the study suggests that the sources of information and knowledge of financial literacy among secondary school teachers were limited as there was no organised framework that guided its distribution.

Financial Literacy: Effect on Financial Behaviour among Secondary School Teachers

In order to analyse financial literacy and its effect on financial behaviour among secondary school teachers, four key ideas in making sound financial decisions were assessed using a questionnaire to gauge financial literacy: aspects of earning, saving and investing, spending, borrowing, and protecting. The study adopted the 2018, Organisation for Economic Co-operation and Development (OECD)/ International Network on Financial Education (INFE) Toolkit which incorporates various questions to determine three potentially prudent financial behaviours, such as: Saving and long-term planning: a set of questions look to understand if people are actively saving, if they borrow or prevent unnecessary borrowing to make ends meet in case of a short-term financial emergency.

Making thoughtful purchases: questions explore whether people have sought independent information or advice when thinking about buying (financial products and services), whether they consider multiple options when choosing, and whether they try to make informed choices by shopping around rather than buying the most readily available good or service as wee as Cash flow management: Questions were designed to determine whether respondents maintain a close eye on their finances, pay their bills on time, and avoid falling behind on payments. Collectively, the financial behaviour questions provide insight into people’s financial behaviour that, if practiced, may enable people to live lives with little financial stress.

Planning ahead and setting aside money helps guarantee that people have a safety net in case of emergency or abrupt disaster. People can make their money “go a long way” by only buying what they really need, refraining from extravagance, and living within their means. Debt can also be avoided by doing all of these things. It is also possible for people to prevent getting into debt by keeping track of their financial inflows and expenditures and prioritising their critical expenses. Teachers have the capacity to apply knowledge and skills to properly manage financial resources for a lifetime of financial well-being by knowing these abilities, as financial literacy is achieved via financial education.

The results of financial literacy and its effect on financial behaviour among secondary school teachers was analysed through personal expenses during their main spending activities. In the quest of finding out if teachers took time to compare price of commodities or seek information about the product before purchasing, 13 % never, 14% rarely and 25% often while 48% always compared prices. The majority of teachers had the ability to compare prices implying a certain degree of financial discipline and literacy. In order to find out if teachers used budgets as their guide with regards to their expenses, the results indicate that, 77% on the total sample always made sure to use a budget as a guide for their shopping activities while the other 26% indicated that they often used a budget. This aspect shows significant financial literacy as budgeting is one of the financial literacy skills that allowed them to track their expenses.

Furthermore, in order to assess secondary school teacher’s personal use of financial planning as a strategy for achieving financial goals, the research probed the aspect of teacher’s ability to keep financial records which involves income and expenditure. The study discovered that 64% never kept financial records, 20% rarely kept financial records whereas 16 % always kept their financial records. The implication of not keeping goods personal financial records includes; inability to dealing with the bank and creditors as well as not tracking financial losses and gains. A summary of the results on financial literacy and its effect on financial behaviour among secondary school Teachers has been presented in table I.

TABLE I Teacher’s Financial Behaviour

| f & % | Never | Rarely | Often | Always | |

| Regularly set aside money each month for saving and future needs | f | 240 | 50 | 34 | 20 |

| % | 68 | 16 | 10 | 6 | |

| Compare prices when shopping for main expenses | f | 44 | 49 | 85 | 166 |

| % | 13 | 14 | 25 | 48 | |

| Use spending plan or Budget | f | 0 | 0 | 80 | 264 |

| % | 0 | 0 | 23 | 77 | |

| Keep track of expenditure and income | f | 220 | 69 | 0 | 55 |

| % | 64 | 20 | 0 | 16 |

Long-Term Financial Planning Influenced by Financial Attitude.

Financial literacy is defined by the OECD/INFE as “a combination of awareness, knowledge, skills, attitudes and behaviour necessary to make sound financial decisions and ultimately achieve individual financial well-being.” [29] This definition acknowledges that even if a person has the knowledge and skills to act in a financially prudent manner, their attitudes will affect that decision.

The current study, which examined teachers’ personal financial literacy, adopted and domesticated elements from the OECD/INFE Toolkit, including three attitude statements to assess respondents’ perspectives on money and future planning. Respondents who displayed more favourable attitudes toward the future and saving received better scores. Teachers were asked to rate their attitude and practiices with the following assertions that are listed in table II using a scale.

TABLE II Respondents’ Attitudes Towards Money and Planning for the Future

| Response | Never | Rarely | Often | Always | Total |

| Statement | |||||

| I usually focus on the now and let the future take care of itself (long-term). | 296 | 2 | 0 | 46 | 344 |

| I find spending money more pleasurable than long-term investing (saving and the long-term). | 266 | 10 | 4 | 64 | 344 |

| Money is available for spending (long-term and saving). | 283 | 4 | 7 | 50 | 344 |

Teachers’ responses to each item centered on short-term choices such as “living for today” and spending money. Preferences of this nature are likely to prevent actions that might increase financial resilience and wellbeing. The statements were designed to measure the degree to which teachers demonstrated attitudes that were more financially knowledgeable, or the degree to which they frequently perceived the claims.

On the other hand, the analysis to analyse the attitude of teachers towards money and planning for the future, their responses were as follows:

“I normally focus on the now and let the future take care of itself”, indicated 46 of the 344 teachers who were interviewed in the sample of 10 schools who participated in the study, while 296 indicated that they never focused on the now and let the future take care of itself. To the statement “I find spending money more enjoyable than long-term investing,” however, 64 indicated that they “always” and 266 responded with “never”. Additionally, 50 people indicated “always” with the assertion that “Money is available for spending,” whereas 283 teachers responded with “never”.

Despite variations in the percentages of respondents who disagreed with the three claims, the overall picture reveals that teachers have positive views toward attitudes of financial literacy in financial planning.

Secondary School Teacher’s Personal use of Financial Planning as a Strategy for Achieving Financial Goals.

The current research discovered that all the teachers who participated were employed by the government and were on full time government salary. This status of employment gave a full monthly salary at the end of each month. According to the information obtained from key informants, the salary was to carter for all their personal expenses such as rental payment for some teachers, groceries, education school fees for their dependents and in some cases to fund their own education, transport to work, medical expenses as well as remit the other share to relatives and other family members. When asked if their personal financial planning met their budget demands, some head teachers stated that their monthly salary did not satisfy their personal needs. For instance, Head Teacher one (1) said;

My financial planning does not always correspond with my salary. This has prompted me on several occasions to seek external financing such as getting a loan from the bank or microcredit institutions.

In adding the voice to the question of whether their personal financial planning met their budget demands, Head teachers (2, 3 and 4) shared a similar view by stating the following;

The salary is not enough to carter for all my personal expenses. As I plan, there are many things that I have to exclude from my budget due to personal financial deficit. Therefore, it is difficult to plan.

As part of their financial planning, some teachers revealed that they had established contingent financial sources apart from the salary such as small business. On the other hand, about seven (7) (70%) of the key informants who had identified loans as an opinion and were in affirmative with the view that loans from financial institutions provided an option for better financial planning and reported as follows;

The loan provided capital for my poultry farming since my salary could not allow as it was limited. It’s up to an individual to find an opportunity in a loan because microfinance institutions work is just to give money and they don’t even want to know what you will do with it.

Contrary to the above assertion, key informant five (5) mentioned that she did not think that borrowing money from the financial institution was a better strategy for financial planning.

The strategy of getting a loan only favoures financial institutions because they are the ones who benefit from the entire process as they make extra interest such that it further encourages individuals to top up an amount on their existing loans which affect their salary and ultimately the planning process.

The study further probed levels of one’s financial knowledge which was assumed to influence very key financial management practices that ensure financial discipline. This was on the premise that personal financial management practices of the teacher with regards to some key important decisions about their daily life. This was assessed by considering savings culture of the teachers which were categorized as ‘never’, ‘rarely’, ‘often’ and ‘always’. For instance, 64% said they never reserved money, 20% stated they rarely set some money aside, 10% reported that they often set aside money and 6% suggested that they always saved for future requirements to sustained their plan for their impending.

Respondents in this study had varying views concerning their personal use of financial planning as a strategy for achieving financial goals. Since they had limited financial literacy the implications of these results are that most of the respondents reported that there financial goals could not be fulfilled due to limited financial literacy strategies. Although respondents had different opinions with regards to the subject, most of them almost two third of the total responses were not in affirmative with the idea of teacher’s personal use of financial planning as a strategy for achieving financial goals due to various reasons which will be mentioned in the next section covering factors which arise in financial planning influenced by strategy.

Challenges Which Hinder Enhancement of Financial Literacy and Personal Financial Planning Among Secondary School Teachers.

Respondents reported numerous challenges which hindered them from accessing financial literacy and achieve personal planning. The results revealed that among challenges faced in enhancing financial literacy were, limited financial awareness among teachers, no deliberate policies which could allow teachers to be oriented at the beginning of their career, limited income and bad spending habits.

On the aspect of limited financial awareness, respondents reported that many financial institutions conduct financial literacy sensitisation during the financial literacy week which only targeted pupils and neglected teachers. In addition to this revelation, respondents further stated that there was limited information material such books, magazines and other pamphlets contributed to the enhancement of financial literacy among teachers.

The majority of the teachers questioned made poor choices when faced with hypothetical financial difficulties. For instance, lack of financial management orientation was also reported by respondents as a hindrance to enhancing financial literacy among secondary school teachers. All the teachers revealed that they were not subjected to any orientation as it was not a deliberate policy in the ministry of education.

The majority of the teachers in the study suggested that their salary was not enough to carter for their needs but the other teachers opposed the suggestion and attributed financial management to bad spending habits by their counterparts. Challenges faced by teachers that were believed to have hindered the enhancement of financial literacy included; limited financial awareness among teachers, no deliberate policies which allows teachers to be oriented at the beginning of their career, limited income and bad spending habits.

DISCUSSION

Generally, the financial literacy levels among secondary school teachers demonstrate that teachers in areas of long term planning attitude shows high or positive results while the aspects of saving, spending behaviour and tracking finances through record keeping was low or negative results. However, some teachers demonstrated some considerable financial knowledge on the concept of financial literacy with a percentage of 44% and also performed below par on the segment of spending and keeping financial records.

In terms of demographics, the study’s findings show that age and years of experience are not predicting factors in personal financial literacy among teachers, as it was observed that teachers with many years in service in service made many bad financial decisions which led them in debt unlike the new teachers who seemed to be financially organized in their decisions. This conclusion further contradicts [30] findings, which showed that individuals with more years of job experience are more knowledgeable than those with less experience, regardless of age or work experience.

The finding regarding work experience of respondents in the current study also contradicts the findings of [31] who reported that the highest levels of financial literacy were demonstrated by those of 35-50. The discovery of this study moreover agrees with the findings of [32] who demonstrated that financially literacy was not influenced by age. The difference in the level of financial knowledge is also accounted for by years of experience in teaching. Teachers with more years in the teaching field (more than 6 years) are relatively less knowledgeable financially than those with less than 6 years of teaching.

The findings revealed some differences in financial literacy (knowledge) among teachers were attributed to a variety of factors. Teachers with master’s degrees, for example, were found to be more knowledgeable than their counterparts with diplomas and bachelor’s degrees. Gender differences among participants, on the other hand, indicated that female teachers were better competent in several elements of financial management than their male counterparts. This finding contradicts the findings of [27] and [32], who found that male teachers had higher financial management skills than female teachers.

Individuals who make budgets, according to [33], spend within their means and thereby control their personal money. As a result, impulsive spending is avoided, and budgeting is approached with optimism. This was supported by research conducted by [34], who argued that more informed groups control their spending habits and decisions by keeping detailed financial records. Another study by [32] also finds that increases in financial literacy prompts a more continuous production of financial statements of which was not the case with the current study among teachers.

Resonating with the current study, [4] identified some key competencies of financial literacy: money basics, budgeting, saving and planning, borrowing and debt literacy. Money fundamentals identify with the knowledge, skills and comprehension needed for the most basically regular calculations. Examples include numeracy and money management skills. This study found that financial literacy had a favourable impact on teachers’ financial behaviour, which was broken down into four categories: saving behaviour, shopping behaviour, long-term planning, and short-term planning.

Empirically, this study has demonstrated that financial literacy significantly improves financial behaviour for all forms of behaviour that are studied. In general, prior research that have demonstrated a strong favourable influence of financial literacy (or financial knowledge) on financial behaviour confirm these findings [35], [36], [37], [38]. This study was backed by some research by [39] and [40] that particularly evaluated the effect of financial literacy on saving behaviour. As a result, according to the present study, three important elements – financial control, earning a good livelihood, and how to cope with financial management – have an influence on money management abilities.

Budgeting, maintaining records, and learning about everyday living expenditures and the ability to pay are all examples of financial control. Making ends meet refers to a person’s ability to foresee financial difficulties and take steps to alleviate them. This also includes assessing one’s ability to keep up with spending and duties. Financial management methods address impulsive spending, the use of credit rather than cash, and general spending patterns that result in the use of more money than is available.

In addition, this study is in agreement with [41] who argues that budgeting and living within one’s means entails being educated about one’s money and limiting unnecessary expenditure. Saving and planning entails putting money aside for an emergency through savings and insurance, as well as mental states related to financial planning, such as saving and planning for retirement and saving and preparing for anticipated costs. The study further contends in line with [42] that the proper use of financial knowledge aids households in meeting their financial responsibilities by allowing them to plan ahead and allocate assets with the greatest ease.

CONCLUSION AND POLICY IMPLICATION

This study aimed at analysing personal financial literacy among teachers in secondary schools. The results obtained from the sample of 354 teachers reveal the majority of secondary school teachers, according to a study, have a poor level of personal financial literacy, but they are aware of different areas of personal financial planning and are capable of making their own plans regardless of their degree of expertise.

This lack of appropriate financial knowledge has far-reaching repercussions for teachers in the long run, as it has been noted that teachers’ understanding of budgeting and spending habits is not excellent or encouraging, which will restrict participants’ financial decision-making and planning in the long run.

The findings of this study is suggests a mismatch between practice in teachers’ personal finical literacy and the aims of the national strategy on financial education (NSFE II) for Zambia which sets out the framework for improving financial education in Zambia.

RECOMMENDATIONS

Based on the study findings and their interpretations as well as the conclusions, the findings were limited in the contextual scope due to the sample size, time and therefore recommends the following:

- Serving teachers and student teachers, regardless of their field of study, should be taught on some basic financial concerns and best practices during their studies or training in order to avoid future personal financial crisis that has the potential to affect their work performance.

- The study also suggests that various teacher organisations and unions provide seminars on financial literacy and investment options for their members in order to ensure that they are financially secure.

- In conjunction with the Ministry of Education, the Ministry of Finance should enhance methods and information to be included in media and other materials sent to teachers. Stakeholders in the education sector must work to change teachers’s attitude toward money and boost the proportion of people who actively save. In the short term, work toward developing a culture of financial caution, planning, and seeking to attain long-term financial objectives.

In the first instance, using straightforward tools with demonstrated efficacy may inspire consumers to behave in financially literate ways. Digital tools could support people in planning and assist them in focusing on their longer-term priorities, such as online calculators, simulators, reminders, and commitment devices. Given the differences in financial literacy and the sources of information between people who use media like social media and those who do not, financial education may be combined with digital education in these situations.

REFERENCES

- Klapper, L, Lusardi, A & Oudheusden, V.P. (2023). Finncial literacy around the world: insights from the standard & poor’s ratings services global financial literacy survey. FINLIT.

- Lerman & Bell (2006). Financial Literacy Strategies Where Do We Go From Here? Opportunity and Ownership Project Report No. 1, Center on Labor, Human Services and Population.

- Capuano, A. and Ramsay, I., (2011). What Causes Suboptimal Financial Behaviour? An Exploration of Financial Literacy, Social Influences and Behavioural Economics. (March 23, 2011). U of Melbourne Legal Studies Research Paper, (540).

- Fernando, J. (2023). What Is Financial Literacy?.Investopedia.

- Van Rooij, M., Lusardi, A. And Alessi, R., October (2007). Financial literacy and stock market participation, National Bureau of Economic Research, Working Paper 13565, pp.1-46.

- Chen, H & Volpe, R. (1998). An Analysis of Personal Financial Literacy Among College Students. Financial Services Review. 7. 107-128. 10.1016/S1057-0810(99)80006-7.

- Kapoor, J. R., Dlabay, Hughes R.J. (2014). Personal Finance. New Delhi: Mc Graw Hill Companies.

- Lerman & Bell (2006). Financial Literacy Strategies Where Do We Go From Here? Opportunity and Ownership Project,1, 1-10. Doi:10.2139/ssrn.923448

- Kovács, Levente & Terták, Elemér 2016. Financial Literacy (Panacea or placebo? – A Central European Perspective). Verlag Dashöfer, vydavateľstvo s.r.o., Železničiarska 13 Bratislava 814 99 Slovakia

- Atkinson, M., Wilkin, A., Stott, A., Doherty, P. and Kinder, K. (2002). Multi-agency Working: a Detailed Study (LGA Research Report 26), Slough: NFER

- Fessler, P., M. Schürz, K. Wagner and B. Weber. 2007. Financial Capability of Austrian Households. Monetary Policy & the Economy Q3/07. 50–67.

- Horska, Elena & Szafrańska, Monika & Matysik-Pejas, Renata. (2013). Knowledge and financial skills as the factors determining the financial exclusion process of rural dwellers in Poland. Agricultural Economics (AGRICECON). 59. 29-37. 10.17221/9/2012-AGRICECON.

- Sibley, J. (2010). Financial Capability, Financial Competence and Wellbeing in Rural Fijian Households.UNDP Pacific Centre.

- O’Donnell, N and M Keeney, 2010, ‘Financial Capability in Ireland and a Comparison with the UK’, Public Money and Management, 30 (6): 355–362.

- Surendar, G & Sarma, S.V .V. (2018). Financial Literacy and Financial Planning among Teachers of Higher Education – A Comparative Study on Select Variables. Amity Journal of Finance 2(1), (31-46).

- GRZ (2019). The National Strategy on Financial Education (NSFE II) for Zambia, 2019 –2024.

- World Bank, (2009). The Case for Financial Literacy in Developing Countries, Washington: World Bank, DFID and OECD

- Centre for Trade Policy and Development (2021)

- Dwiastanti, A. (2015). Financial Literacy as the Foundation for Individual Financial Behavior. Journal of Education and Practice www.iiste.org. ISSN 2222-1735 (Paper) ISSN 2222-288X (Online) Vol.6, No.33.

- GRZ (2019). The National Strategy on Financial Education (NSFE II) for Zambia, 2019 –2024.

- Atkinson, A. & F. 2013. “Promoting Financial Inclusion through Financial Education: OECD/INFE Evidence, Policies and Practice”, OECD Working Papers on Finance, Insurance and Private Pensions, No. 34, OECD Publishing. http://dx.doi.org/10.1787/5k3xz6m88smp-en

- Agarwal, S., Gene, A., Ben, I. D, Souphala, C & Evanoff, D. D. (2015). Financial Literacy and Financial Planning: Evidence from India. Journal of Housing Economics, 27, 4–21. doi:10.1016/j.jhe.2015.02.003

- Raosoft (2023). http://www.raosoft.com/samplesize.html.

- Taylor, M. (2011). Measuring Financial Capability and its Determinants Using Survey Data. Social Indicators Research. 102. 297-314. 10.1007/s11205-010-9681-9.

- Government of the republic of Zambia. Ministry of education (2020) Bulletin.

- Cude, B.J., (2010). Financial Literacy, the Journal of Consumer Affairs, 44(2).

- Oppong-boakye, P. K., & Kansanba, R. (2013). An Assessment of Financial Literacy Levels among Undergraduate Business Students in Ghana. Research Journal of Finance and Accounting, 4(8), 36-49.

- OECD (2018), OECD/INFE Toolkit for Measuring Financial Literacy and Financial Inclusion

- Chen, H. and Volpe, R.P., (1998). “An Analysis of Personal Financial Literacy among College Students”. Financial Services Review, Vol. 7, No. 2, pp. 107-128

- Almenberg, J. and Säve-Söderberg, J., (2011). Financial Literacy and Retirement Planning in Sweden. CeRP Working Paper, No. 112, Turin (Italy).

- Bhushan, P. and Yajulu, M., (2013). “Financial Literacy and Its Determinants,” International Journal of Engineering, Business and Enterprise Applications, Vol. 4, No. 2, pp. 155-160.

- Fonseca, R., Kathleen, M., Gema. Z., and Julie Z., (2009). What explains the gender gap in financial literacy? The role of household decision-making. Journal of Consumer Affairs 46 (1) (Spring): 90-106.

- Kidwell, B. and Turrisi, R., (2004). An examination of college student money management tendencies. Journal of Economic Psychology, 25(5):601– 616.

- Wise, S., (2013). The impact of financial literacy on new venture survival. International Journal of Bus and Man, 8(23): 30-39.

- Fernandes, D., Lynch Jr, J. G., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviours. Management Science, 60(8), 1861-1883.

- Kumar, S, Watung, C, Eunike, J.N, Liunata, L. (2017). The Influence of Financial Literacy Towards Financial Behavior and its Implication on Financial Decisions: A survey of President University Students in Cikarang – Bekasi. Journal of manangement studies, 2 (1).

- Nicolini, G, Cude, BJ and Swarn Chattejee, 2013, ‘Financial Literacy: A Comparative Study A Cross Four Countries’, International Journal of Consumer Studies, 37, pp. 689 – 705.

- Jamal, A, Azlan, A & Ramlan, Kamal, W & Mohidin, Rosle & Karim, Mohd & Osman, Zaiton. (2015). The Effects of Social Influence and Financial Literacy on Savings Behavior: A Study on Students of Higher Learning Institutions in Kota Kinabalu, Sabah. International Journal of Business and Sosial Science. 6. 110-119.

- Lusardi, A., Mitchell, O. S. and Curto, V.(2010). “Financial Literacy among the Young”, Journal of Consumer Affairs. 44, 358–380.

- Rooij, M. V., Lusardi, A. and Alessie, R.. (2011). Financial Literacy, Retirement Planning and Household Wealth. DNB Working Paper, Working Paper No. 313. August 2011.

- Lusardi, A. and Olivia S. M., (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature 52 (1): 5- 44.

- Mwangi, I. W. and Kihiu, E. N. ( 2012). Impact of Financial Literacy on Access to Financial Services in Kenya. International Journal of Business and Social Science Vol. 3 No. 19; October 2012.