The Sustainability Model of Microfinance Institutions

- Mila Rose D. Javellana

- Melecio A. Sy, Jr.

- 241-253

- Mar 8, 2024

- Business Management

The Sustainability Model of Microfinance Institutions

Mila Rose D. Javellana and Melecio A. Sy, Jr.

University of the Immaculate Conception

DOI: https://doi.org/10.51244/IJRSI.2024.1102019

Received: 16 January 2024; Revised: 05 February 2024; Accepted: 10 February 2024; Published: 08 March 2024

ABSTRACT

The sustainability of microfinance institutions is crucial in fostering financial inclusion and economic development, particularly in developing countries. The purpose of this study is to establish the best-fit model for the sustainability of Micro Finance Institutions. Thus, it is important to look into the sustainability of MFIs. This quantitative study employs a structural equation model to assess the relationships among the exogenous and endogenous variables and establish the best-fit model as its purpose. The respondents were 300 MFI managers and employees with supervisory positions. The study found the best-fit model through various goodness-of-fit models. The findings reveal a robust and statistically significant relationship between independent variables, digital transformation, entrepreneurial orientation, and knowledge management, and the dependent variable, sustainability within MFIs. On the best-fit model, digital transformation exhibits a strong and statistically significant positive influence on sustainability. At the same time, knowledge management and entrepreneurial orientation do not show significant direct effects on sustainability in the specific analysis.

Keywords: Sustainability, digital transformation, knowledge management, entrepreneurial orientation, Microfinance institutions, SOCCSKSARGEN, Philippines

INTRODUCTION

The sustainability of a microfinance institution is its ability to cover all of its costs for its continued operation and the provision of financial services to people experiencing poverty. To serve the people experiencing poverty was the mandate of MFIs; however, reaching the poor clients is more costly than other segments in the market. Hence, MFIs strive to attain sustainability to continue serving people experiencing poverty. Kaur (2014) pointed out that they need to increase profits by raising interest rates to achieve sustainability.

The Micro Finance Institutions (MFI) and its sustainability depends largely on a range of issues, including the business mission, level of indebtedness, regulatory environment, funding sources, access to funding, and governance and management structures (Lopatta et al., 2017; Sematele & Dlamini, 2020). The first challenge in MFI sustainability is mission drift referring to the situation where MFIs deviate from their original goal of serving people experiencing poverty and instead focus on maximizing profits (Muhammad et al., 2015). In some countries, the lack of proper regulation and supervision of MFIs led to problems such as excessive interest rates, lack of transparency, and inadequate consumer protection, according to Armendariz and Morduch (2010). Another sustainability issue of MFIs is the limited access to funding from commercial sources due to their small size and lack of collateral, leading to insufficient funds to meet operational expenses (Lee, 2021). In addition, the weak governance and management issues led to the mismanagement of funds, corruption, and lack of accountability, says Chun (2016). Finally, many MFIs globally are experiencing over-indebtedness. Guermond et al. (2022) pointed out that over-indebtedness refers to consumers’ over-indebtedness to the MFI, which may not be repaid, consequently causing bankruptcy among MFIs.

It is a critical role among Microfinance Institutions (MFIs) to promote financial inclusion and economic development, particularly in developing countries, as highlighted by a report by the World Bank (2014). MFIs help reduce poverty and inequality by allowing access to people, specifically low-income individuals and small businesses, for their financial needs. These people are often excluded from the formal financial system services. In addition, a study by International Finance Corporation (2015) found that MFIs can contribute to economic growth by financing small and medium-sized enterprises (SMEs), which are important drivers of job creation and innovation.

Furthermore, the International Fund for Agricultural Development (IFAD) in 2019 found the important role played by MFIs in rural development by providing access to finance for small farmers and rural entrepreneurs, who often need more collateral or credit history. Finally, the Asian Development Bank (2020) also posited the role of MFIs in promoting financial inclusion and reducing income inequality, particularly in countries with high poverty levels and informal employment. The gap in literature found was that most studies focus on the sustainability of large MFI organizations, leaving the micro and small relatively least reviewed. Empirically, since the Philippine businesses including MFI’s are largely micro and small enterprises by a whooping 80% of the businesses, it is thus, important to conduct a study on how MSME MFIs establish sustainability.

Thus, the study of sustainability among microfinance organizations (MFOs) is important for several reasons, including ensuring long-term viability. The sustainability of MFIs is essential for ensuring their long-term viability and ability to continue serving the customers’ needs (Maes & Reed, 2014). It also enhanced social impact. MFIs did it by reaching more clients to provide a wide range of products and services in the financial context. According to Ghatak et al. (2016), sustainable MFIs serve clients better based on their needs and contribute to poverty reduction and economic development. Finally, the significance of studying MFIs has something to do with meeting stakeholder expectations. It was highlighted by the study of Bosch-Badia et al. (2021) that the study of sustainability could help MFIs meet the expectations of their stakeholders, including investors, regulators, and customers. The objective of this study is to establish a structural equation model for the sustainability of microfinance institutions.

The objectives of the study include investigating the relationship between digital transformation, entrepreneurial orientation, and knowledge management to sustainability within Micro Finance Institutions (MFIs) in the SOCCSKSARGEN Region. Specifically, this study determined the levels of digital transformation, entrepreneurial orientation, knowledge management, and sustainability within MFIs in the SOCCSKSARGEN Region. In addition, it also assessed the existence of significant relationships between the endogenous (sustainability) and exogenous (digital transformation, entrepreneurial orientation, and knowledge management) variables, as well as between the exogenous variables themselves. Finally, the study also identified and established the best-fit model for predicting sustainability within MFIs in the SOCCSKSARGEN Region.

The researcher hypothesizes that there is no significant relationship between Digital transformation and sustainability, Knowledge management and sustainability, Entrepreneurial orientation and sustainability, Digital transformation and knowledge management, Digital transformation and entrepreneurial orientation, and Knowledge management and entrepreneurial orientation. It also hypothesizes that the model does not support the significant contribution of the structural equation of the predictor variable toward sustainability.

METHODOLOGY

This study used a quantitative research approach employing a Structural Equation Model (SEM) to create a sustainability model for MFIs involving the variables of digital transformation, knowledge management, and entrepreneurial orientation. A quantitative research approach is concerned with collecting and analyzing structured data presented numerically, which aims to build accurate and reliable measurements for statistical analysis (Goertzen, 2017). A Structural Equation Model (SEM) is a set of statistical techniques for estimating the magnitudes and directions of presumed causal effects in quantitative studies based on cross-sectional, longitudinal, experimental, or other research designs (Kline, 2023). It is a second-generation multivariate data analysis technique that simultaneously models and estimates complex relationships among multiple dependent and independent variables (Hair et al., 2021). Typically, the concepts under consideration in this model are not observable and indirectly measured by multiple indicators.

In addition, Structural Equation Model, as pointed out by Cole and Preacher (2014), obtains a more precise measurement of theoretical concepts of interest since it accounts for measurement error in observed variables in estimating the relationships. Also, Deng et al. (2018) state that the variables are measured by multiple indicators subject to measurement errors. SEM is an analytical process involving model conceptualization, parameter identification and estimation, data-model fit assessment, and potential model re-specification, and ultimately this process allows for the assessment of the fit between correlational data obtained from experimental or non-experimental research and one or more competing causal theories specified a priori (Mueller & Hancock, 2018)

The study was conducted among 293 banks and financial institutions that offer microfinance services regulated by the Bangko Sentral ng Pilipinas in Region XII, also known as SOCCSKSARGEN Region, located in the central part of Mindanao. Provided on figure 6 is the map of the region which comprises four provinces and one city, South Cotabato, Cotabato, Sultan Kudarat, Sarangani, and General Santos. Based on the Department of Supervisory Analytics, Financial Supervision Sector of the Bangko Sentral ng Pilipinas, there are 928 BSP-supervised financial institutions in the SOCCSKSARGEN region composed of 293 banks and 635 non-bank financial institutions. Among the banks present in Region XII, there are 135 Universal and Commercial Banks, 66 Thrift Banks, and 92 Rural and Cooperative Banks. At the same time, the Non-Bank Financial Institutions are composed of 4 Financing Companies, 8 Non-stock Savings and Loan Associations, and 623 Pawnshops. The study of Mylenko, N., & Iqbal, Z. (2016) in Muslim Mindanao has emphasized the need for Southern Mindanao region to be studied on the financial practices of the various institutions operating in the area. In addition, the researcher choose this region because of the diversity of the financial institutions present in the area, aside from the convenience of the researcher to survey the region.

The researcher covered 300 respondents composed of managers at all levels or those holding supervisory positions in microfinance institutions. The 10-time rule by Hair et al. (2021) can be used to determine the sample size, meaning that the minimum sample size should equal ten times the number of independent variables in the most complex regression in the PLS path model. Further, when applying multivariate analysis techniques, the technical dimension of the sample size becomes relevant; thus, adhering to the minimum sample size guidelines ensures that the results of a statistical method, such as PLS-SEM, have adequate statistical power.

A stratified random sampling technique was used to select the respondents. A stratified random sampling method is a probability sampling method that enables the calculation of the sampling error (Iliyasu & Etikan, 2021). The selection inclusion criteria include respondents who are regular employees of the MFI, employees who are managers or holding supervisory positions of the financial institutions at any level, and the financial institution may be banks or financing companies regulated and registered by the Bangko Sentral ng Pilipinas. In addition, the respondents must be Filipinos at a legal age.

The survey questionnaire has five parts, including a demographic profiling section and four sections of a formal questionnaire of the four variables of the study. These questions were adapted from different authors. The questionnaire for Sustainability was adapted from Tasleem et al. (2019). It is a study on the impact of technology management on corporate sustainability performance which is a mediating study on the role of TQM. The tool has three indicators composed of 16-item questions that determine the respondents’ agreement or disagreement concerning the firm’s sustainability performance. Reliability is determined using Cronbach alpha which produces a value of 0.708. Digital Transformation questionnaire was adapted from Hajishirzi et al. (2022) study, which includes the dimensions of data-driven, business process innovation, customer engagement, organizational resilience, and competitive advantage. This tool contains a 22-item construct using a 1 – 5-point Likert scale ranging from 5- Strongly Agree to 1- Strongly Disagree. Reliability is determined using Cronbach alpha which produces a value greater than 0.830.

In addition, Knowledge Management. The questionnaire was adapted from a validated questionnaire developed by Darroch’s (2003) study entitled “Developing a Measure of knowledge management Behaviors.” This tool contains three indicators with 16 questions and uses a 5-point Likert scale which ranges from 5-strongly agree to disagree to 1-strongly. Reliability is determined using Cronbach alpha which produces a value greater than 0.71. Finally, Entrepreneurial Orientation questionnaire was adapted from the Herlinawati et al. (2019) study entitled “The Effect of entre entrepreneurial Orientation on SMEs in business performance in Indonesia.” This tool has four indicators containing 16 questions and uses a 5-point Likert scale from 5- Very High to 1- Very Low. The indicators include innovativeness, proactiveness, risk-taking, and aggressiveness. Reliability is determined using Cronbach alpha which produces a value greater than 0.70.

The data gathered in this study was classified, analyzed, and interpreted by using appropriate statistical tools such as the Mean was used to measure the level of financial institutions’ digital transformation, knowledge management, entrepreneurial orientation, and sustainability performance. The Standard Deviation (SD) measures the dispersion of a data set from the mean. The higher the distribution of variability, the greater the SD, and the more significant the magnitude of the deviation of the mean’s value. Likewise, Pearson Correlation helped determine the significant relationships among the independent variables, digital transformation, knowledge management, and entrepreneurial orientation dependent variable, sustainability performance. Finally, the Structural Equation Model (SEM) determined the best-fit model. To qualify as the best-fit model, the values must fall within the acceptable range of all the test indices. First, the Chi-Square/ Degrees of Freedom Value must be above 0 but not higher than 2. In addition, the Normed Fit Index, Goodness of Fit Index, Tucker-Lewis Index, and Comparative Index value must be greater than 0.95. Also, the Root Mean Square of the Error Approximation value must be less than 0.05. Lastly, the P-close value must be greater than 0.05. A Structural Equation Model (SEM) as a set of statistical techniques will be used to estimate the magnitudes and directions of presumed causal effects in quantitative studies based on cross-sectional, longitudinal, experimental, or other research designs.

RESULTS AND DISCUSSION

Level of Digital Transformation, Knowledge Management, Entrepreneurial Orientation, and Sustainability of Micro Finance Institutions. Sustainability. The variable Sustainability of Micro Finance Institutions has an overall mean score of 4.27 revealing very high level of sustainability of the firms and it is interpreted as the sustainability of the firms is very evident. The standard eviation is .58 which means that, on average, the data points for sustainability are relatively close to the mean and there is relatively little variability in the data. The indicators social and environmental sustainability were both rated very high with means of 4.42 and 4.22 respectively which is interpreted as the indicators are very evident based on the perceptions of the respondents. However, rated least is the indicator economic sustainability described as high with a mean core of 4.17 and interpreted as sustainability is evident. The standard deviation of all indicators of sustainability ranges from 0.62 to 0.67 indicating that there is low variability in the responses of the respondents as the responses were relatively close to the mean. All the data on the levels of the variables is provided on table 1.

The overall high mean score of 4.27 in Sustainability suggests that microfinance institutions of SOCSARGEN Region exhibit a very high level of sustainability. This result of the study is a positive sign for the financial stability and long-term viability of the MFIs. The low standard deviation of 0.58 indicates that responses about sustainability are relatively consistent among the respondents, suggesting a shared perception of sustainability among stakeholders. The indicators within sustainability, including social and environmental sustainability, were also rated very high, indicating that these dimensions are particularly strong within MFIs. However, it’s worth noting that economic sustainability was rated slightly lower at “High” (4.17), indicating some room for improvement in this aspect.

The result on sustainability is consistent with the findings of Serrano-Cinca et al.(2016) which shows that MFIs are giving emphasis on social and environmental issues in its decision system of the organization. Furthermore, the result of the study indicating a much lower level of economic sustainability showed that MFIs need to maintain positive attitudes towards the economic environment of the organization.

This result is similar to the result of the study by Atahau et al. (2020) indicating that the economic environment brings sustainability too to institutions. In addition, in the study by Ashraf et al. (2022), MFIs from nations with greater levels of socioeconomic independence adhere to superior ESG policies. The result of the said study and this study is in parallel believing that sustainability is important to MFIs’ success.

The study by Garcia-Perez et al. (2018) also finds that the economic, social, and environmental sustainability areas of microfinance institutions is not always in equilibrium. Some areas in an organization are always better than the other factors. As such, the disparity in the results of this study on the very high levels of social and environmental sustainability while the level of economic sustainability is high is like the results of the study by Garcia-Perez et al. (2020).

Digital Transformation. Digital transformation was rated with an overall mean of 4.24 described as very high. It is interpreted as Digital Transformation of the firm is very evident. Its standard deviation is 0.6 indicating low variability in the responses where the scores are near the mean 4.24. The indicators of Digital Transformation specifically Customer Engagement, Data Driven , and Competitive Advantage were rated very high with mean scores of 4.36, 4.27, and 4.22 respectively. These ratings are interpreted as indicators of digital transformation of the firm which are very evident. However, the indicators Business Process Innovation and Organizational Resilience were rated high with mean scores of 4.19 and 4.17 respectively which both are described as high. It is interpreted as interpreted as these indicators of digital transformation of the firm are evident. The standard deviation of the variable and the indicators range from 0.60 to .72 indicating a minimal variation of the responses and are near to the means.

The result of this study showed that there is a very high mean score of 4.24 for Digital Transformation which indicates that this aspect of the MFIs in SOCSARGEN Region is also very evident in microfinance institutions. The low standard deviation of 0.60 suggests that respondents generally agreed on the extent of digital transformation within the MFIs. Specific indicators of Digital Transformation, such as Customer Engagement, Data Driven, and Competitive Advantage, were rated very high, underscoring the importance of these elements in MFIs. However, indicators like Business Process Innovation and Organizational Resilience, while still rated as “High,” suggest potential areas for further development in the digital transformation journey of MFIs.

The result of digital transformation is consistent with the findings of Mujeri (2020) that MFIs embrace digital transformation and improve their ability and knowledge to stay up with the swift advancement of technology and integrate digital financial services in their microfinance operations. As a result, the adoption of digital transformation can help MFIs improve operational efficiency and improve access to financial services (Pal et al., 20221).

Entrepreneurial Orientation. The Entrepreneurial Orientation Micro Finance Institutions of the study was rated high with a mean score of 4.11. All indicators including Innovativeness, Proactiveness, Risk Taking, and Aggressiveness likewise were also rated high with mean scores of 4.12, 4.10, 4.04, and 4.17 respectively. This is interpreted as entrepreneurial orientation of micro finance institutions is evident. The standard deviation of the variable and the indicators of Entrepreneurial Orientation range from 0.62 to .72 indicating minimal variation of the responses and that the responses are near the means.

The high mean score of 4.11 for Entrepreneurial Orientation reflects a positive perception of this aspect in microfinance institutions. The indicators, including Innovativeness, Proactiveness, Risk Taking, and Aggressiveness, were all rated high, indicating that MFIs are generally seen as proactive and innovative in their approach. The low standard deviation (ranging from 0.62 to 0.72) suggests that there is a consistent view among respondents regarding entrepreneurial orientation in MFIs.

The MFIs in SOCCKSARGEN region reveals a high level of entrepreneurial orientation which influences the performance of microfinance institutions and this result is consistent with the findings of Wainaina (2017) that entrepreneurial orientation positively influences the growth of MFIs and further supported by Panda (2018) which states that the key factor in the success of MFIs is the entrepreneurial orientation of the key personnel managing the operation.

Knowledge Management. The Knowledge Management of the MFIs has an over-all rating of 4.13 described as high and interpreted as the Knowledge Management of the firm is evident. The indicator Responsiveness to Knowledge was the only variable rated very high with a mean score of 4.20 and interpreted as very evident. The other indicators including Knowledge Acquisition and Knowledge Dissemination were both rated high with mean scores of 4.15 and 4.04 respectively. The standard deviation of the variable and the indicators of Knowledge Management range from 0.67 to 0.75 indicating low variability of the responses and the ratings are near their respective mean scores.

Knowledge Management within MFIs also received a high mean score of 4.13, indicating that it is evident within these institutions. The indicator “Responsiveness to Knowledge” stood out with a very high mean score of 4.20, implying that MFIs are particularly adept at leveraging and responding to knowledge. The other indicators, Knowledge Acquisition and Knowledge Dissemination, were also rated high, although slightly lower. The standard deviation values (ranging from 0.67 to 0.75) suggest relatively low variability in responses, indicating a shared perception of knowledge management practices.

The high-level result of the study indicates that Knowledge Management is an important tool in microfinance institutions. The result is consistent with the findings of Shea (2023) and Hesniati et al. (2019) that knowledge management can positively and significantly enhance overall organizational performance. In addition, knowledge management help organization achieve competitive advantage (Hesniati et al., 2019) and influence organizational innovation through organizational learning and culture (Hussain et al., 2022).

Correlation of Variables. The correlation test is needed to test the relationship of variables as a requisite to test regression analysis. Table 2 presents the correlation of the variables of the study. The result shows that all independent variables– digital transformation, entrepreneurial orientation, and knowledge management are statistically correlated with sustainability at the r-values of 0.87, 0.77, and 0.75 respectively, which is statistically significant (p<0.05). The r-value measures the strength and direction of the linear relationship between the variables. Thus, in this case, an r-value of 0.87, 0.77, and 0.75 suggest a strong positive correlation between digital transformation, entrepreneurial orientation, and knowledge management with sustainability. The p-value is used to assess the statistical significance of the observed correlations, and a p-value of 0.05 indicates a 5% chance of observing such strong correlations between the variables by chance alone, assuming there is no true correlation in the population. Therefore, the correlations are considered statistically significant (p<0.05).

The correlation results confirm the findings of El Hilali (2020) and Esses et al. (2021) that digital transformation has significant correlation with the component of sustainable development and created an impact on company’s quest for sustainability. Digital transformation is a driver and predecessor of sustainability and that, companies need to enhance their digital capabilities and balance their economic, environmental and social impacts (Gomez-Trujillo & Gonzalez-Perez, 2021). Additionally, Feroz et al. (2021) finds that digital technologies causes transformations in different areas particularly in the area of environmental sustainability. According to Guandalini (2022), several studies profoundly address digital opportunities for sustainability as part of a business strategy in the era of technological progress. The result of the study shows that digital transformation influences the sustainability of microfinance institutions.

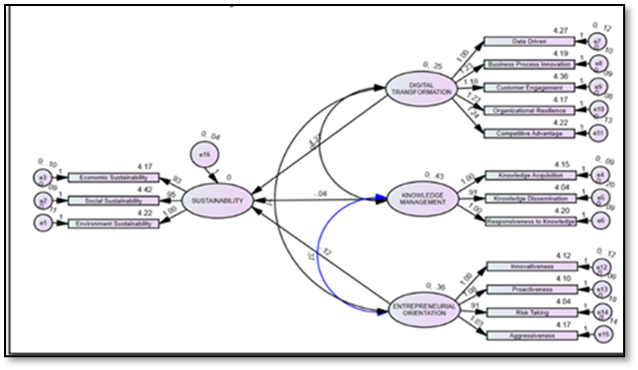

Best Fit Model. The Best Fit Model was identified using multiple indices as standards earlier provided in Chapter 1. A comparative account of the five hypothesized models were obtained using several indices as measures of SEM. The comparative table indicates that among the five hypothesized models, only hypothesized model number 1 has completely satisfied the criteria. The model shows that it possessed values that fit the criteria falling within the acceptable range of all the test indices used in this study. Thus, the hypothesized model 1 was deemed best fit. Figure 1 presents the best fit model. the best fit model structure of the sustainability of micro finance institutions. The figure shows that the latent variables digital transformation, knowledge management, and entrepreneurial orientation have causal relationships with the endogenous variable sustainability of the MFIs and with each of the exogenous variables studied. Moreover, all the observed variables in hypothesized model number 1 showed that they represent and measure the latent constructs within the structural equation model (SEM).

Figure 1 Best Fit Model of Sustainability of MFIs

The study also provides the direct and indirect effects data of independent variables on sustainability in the best-fit structural equation model (SEM). The “Direct Effect” shows the immediate impact of each independent variable (Digital Transformation, Knowledge Management, Entrepreneurial Orientation) on Sustainability. In this case, Digital Transformation has a positive direct effect of 1.267, indicating that it directly contributes positively to Sustainability, while Knowledge Management and Entrepreneurial Orientation have negative direct effects, implying that they have a direct negative impact on Sustainability. The zeros in the “Indirect Effect” column suggests that there are no indirect effects through mediated pathways in this model. The “Total Effect” column represents the sum of the direct and indirect effects, where Digital Transformation has a total effect of 1.267, while Knowledge Management and Entrepreneurial Orientation have total effects of -0.043 and -0.119, respectively. These values provide insights into the overall impact of each independent variable on Sustainability in the context of the model.

The result of the best fit model provides an understanding on how sustainability is achieved among MFIs. The selection of the best-fit model is essential as it ensures that the SEM adequately represents the relationships between variables through the favorable values of the test indices. The results on the direct and indirect effects of the independent variables (Digital Transformation, Knowledge Management, Entrepreneurial Orientation) on Sustainability showed that Digital Transformation is found to have a significant positive direct effect on Sustainability (1.267), emphasizing the importance of technology adoption for improving sustainability.

The result of this study on the positive direct effect of digital transformation of MFIs on sustainability had been proven true in various studies as early as 2015 by Chandola (2015) including those by Feroz et al. (2021), Gomez & Gonzalez (2021), and Martinez-Pelaez et al. (2023) among several others. The authors all positively confirmed that digital transformation significantly impacts the sustainability of the MFIs. It implies that MFIs must integrate digital transformation to be sustainable. These studies also confirm that the adoption of digital technologies drastically improves entrepreneurial activities influencing economic sustainability.

Conversely, Knowledge Management and Entrepreneurial Orientation exhibit negative direct effects on sustainability. However, the non-significant direct effects of Knowledge Management and Entrepreneurial Orientation do not necessarily diminish their importance. Knowledge Management refers to the practices and processes that organizations use to create, capture, store, and distribute knowledge effectively. In the context of MFIs, Knowledge Management may involve how well an institution manages and utilizes its institutional knowledge and expertise. The negative direct effect of Knowledge Management on Sustainability suggests that, in this specific SEM, as Knowledge Management practices improve or become more sophisticated, it does not necessarily lead to a direct and positive impact on sustainability. This result may imply that other factors or variables not considered in the model could be mediating or moderating the relationship between Knowledge Management and Sustainability. For example, the way knowledge is disseminated, applied, or integrated into decision-making processes within the organization might play a crucial role in determining its effect on sustainability. In this study knowledge management was indicated by how knowledge was acquired, disseminated, and how responsive knowledge is for the MFIs as posited by Darroch (2003). In several studies this result on the relationship between knowledge management and sustainability is supported by Kivits & Furneaux (2013) and Torres et al. (2017). However, various studies showed that knowledge management may impact the sustainability of the firms through many other ways. The study by RaghuRam & Prabhu (2014) on knowledge-based micro-finance indicated that knowledge management involves the creation of a knowledge ecosystem involving knowledge development process until organizations become knowledge self-sustaining. In the context of the said study, the indicators used in this study is limited which exclude knowledge self-sustenance indicators. In another study by Kayembe et al. (2021), the authors also highlighted that knowledge management also includes the personal characteristics of leaders that foster knowledge management. The said study found that the specific knowledge management system among other variables used by the MFIs also influence sustainability. Finally, the study by Nkurunziza et al. (2018) pointed out that the specific elements of knowledge management such as the ability and adaptability of the MFIs to use knowledge and implement business process reengineering to improve the internal processes and customer services is valuable knowledge management activities leading to sustainability.

In similar fashion, the negative direct effect of Entrepreneurial Orientation on Sustainability suggests that, in the context of the SEM, being more entrepreneurial in nature does not directly result in higher sustainability for MFIs. In this study, Entrepreneurial Orientation was viewed from the perspective of the study by Herlinawati et al. (2019) which refers to an organization’s strategic orientation characterized by traits such as innovation, proactivity, risk-taking, and aggressiveness. It reflects an organization’s willingness to take calculated risks and pursue new opportunities.

CONCLUSION

The results and discussion provided yielded the following conclusions related to the levels of the variables studied, the correlation, and the best-fit model in the structural equation model. The result exhibits a very high level of sustainability of MFIs in the SOCCSKSARGEN Region, which means that the level of sustainability is very evident. This indicates a positive outlook for these institutions’ financial stability and long-term viability. Likewise, Digital Transformation is evident within the MFIs, as indicated by a high mean score. This underscores the significance of embracing digital technologies and practices within MFIs to enhance operational efficiency and broaden access to financial services. More so, the MFIs demonstrate a high level of Entrepreneurial Orientation, indicating that it is evident among the MFIs. This highlights the proactive and innovative nature of MFIs in pursuing growth and opportunities. In addition, the Knowledge Management of MFIs in SOCSARGEN Region is high and is evident. This underscores the importance of fostering a learning and knowledge-sharing culture within MFIs.

The strong positive correlation between the variables reveals a robust and statistically significant relationship between the independent variables (Digital Transformation, Entrepreneurial Orientation, and Knowledge Management) and the dependent variable (Sustainability) within microfinance institutions. Thus, the null hypothesis is rejected. The correlation result implies that Digital Transformation, Entrepreneurial Orientation, and Knowledge Management influence the sustainability of MFIs.

The best-fit model is Model 1 as seen in Figure 7. After using the multiple fit indices, the model shows the values that satisfy the criteria for the Structural Equation Model. Digital Transformation exhibits a strong and statistically significant positive influence on Sustainability, emphasizing the importance of technological investments for improving sustainability. In addition, Digital Transformation has a significant positive direct effect on Sustainability, reaffirming its role as a crucial driver of sustainability within microfinance institutions. Knowledge Management and Entrepreneurial Orientation do not show statistically significant direct effects on Sustainability in this analysis. However, this does not diminish their potential importance, as other unaccounted-for variables may mediate or moderate their impact.

Furthermore, Knowledge Management and Entrepreneurial Orientation have negative direct effects on Sustainability in this model, indicating that the relationships between these variables and sustainability are more complex and may involve other mediating or moderating factors not considered in this analysis that could influence these relationships. The study’s findings reveal complex relationships between Knowledge Management and Entrepreneurial Orientation with Sustainability. Knowledge Management and Entrepreneurial Orientation exhibit negative direct effects on Sustainability, suggesting that further exploration or refinement is required to understand how these factors can positively impact sustainability. This complexity emphasizes the need for a more nuanced examination of these relationships and consideration of additional variables and contextual factors.

The best-fit model of this study shows a direct causal relationship between Digital Transformation, Entrepreneurial Orientation, and Knowledge management to Sustainability, which supports the Resource-based View (RBV) Theory and Dynamic Capability Theory. The MFIs with high levels of digital transformation, entrepreneurial orientation, and knowledge management are indicated to have dynamic capabilities and competitive advantage, contributing to their long-term sustainability.

The results of the study confirm the Resource-Based View (RBV) Theory, which further emphasizes the significance of unique and valuable resources within microfinance institutions (MFIs). It underscores that MFIs possess distinct resources and capabilities, such as organizational culture, digital technologies, and knowledge assets, which competitors do not easily imitate. These unique resources are essential for building sustainable competitive advantages and achieving long-term success – sustainability.

The result also confirms the Dynamic Capability Theory (DCT), which emphasizes the need for MFIs to adapt, integrate, and reconfigure their resources and capabilities in response to a dynamic environment. It highlights that MFIs must continuously sense and seize emerging opportunities, build and restructure capabilities, and engage in learning and knowledge integration to remain competitive and sustainable in the evolving microfinance sector. Moreover, MFIs must be able to arrive at knowledge self-sustenance.

REFERENCES

- Armendáriz, B., & Morduch, J. (2010). The economics of microfinance. MIT press.

- Ashraf, D., Rizwan, M. S., & L’Huillier, B. (2022). Environmental, social, and governance integration: The case of microfinance institutions.

- Asian Development Bank Annual Report (2020). https://www.adb.org>multimedia>ar2020

- Atahau, A. D. R., Huruta, A. D., & Lee, C. W. (2020). Rural microfinance sustainability: Does local wisdom driven-governance work?. Journal of Cleaner Production.

- Bosch-Badia, M. T., Torrent-Sellens, J., & Sánchez-García, J. C. (2021). Work–family conflict and its effect on the use of flexible work arrangements and job satisfaction: Does culture and gender matter?. Journal of Business Research,

- Chandola, V. I. K. A. S. (2015). Digital transformation and sustainability: Study and analysis. Cambridge, Massachusetts.

- Chun, J-h. 2016. “Can CAMPUS Asia Program be a Next ERASMUS? The Possibilities and Challenges of the CAMPUS Asia Program.” Asia Europe Journal.

- Cole, D. A., & Preacher, K. J. (2014). Manifest variable path analysis: potentially serious and misleading consequences due to uncorrected measurement error. Psychological methods.

- Darroch, J. (2003), “Developing a measure of knowledge management behaviors and practices”, Journal of Knowledge Management

- Deng, L., Yang, M., Marcoulides, K.M. (2018). Structural equation modeling with manay variables: A systematic review of issues and developments. https://doi.org/10.3389/fpsyg.2018.00590

- De Quidt, J., Fetzer, T., & Ghatak, M. (2018). Commercialization and the decline of joint liability microcredit. Journal of Development Economics.

- El Hilali, W., El Manouar, A., & Idrissi, M. A. J. (2020). Reaching sustainability during a digital transformation: a PLS approach.

- Esses, D., Csete, M. S., & Németh, B. (2021). Sustainability and digital transformation in the visegrad group of central european countries.

- Feroz, A. K., Zo, H., & Chiravuri, A. (2021). Digital transformation and environmental sustainability: A review and research agenda. Sustainability.

- García‐Pérez, I., Muñoz‐Torres, M. J., & Fernández‐Izquierdo, M. Á. (2018). Microfinance institutions fostering sustainable development.

- Goertzen, M. J. (2017). Introduction to quantitative research and data.

- Gomez-Trujillo, A. M., & Gonzalez-Perez, M. A. (2021). Digital transformation as a strategy to reach sustainability. Smart and Sustainable Built Environment, 11(4), 1137-1162.

- Gomez-Trujillo, A. M., & Gonzalez-Perez, M. A. (2022). Digital transformation as a strategy to reach sustainability. Smart and Sustainable Built Environment.

- Guandalini, I. (2022). Sustainability through digital transformation: A systematic literature review for research guidance.

- Guermond, V., Parsons, L., Vouch, L. L., Brikell, K., Michiels, S., Fay, G., … & Picchioni, F. (2022). Microfinance, over-indebtedness and climate adaptation: new evidence from rural Cambodia.

- Hair Jr, J. F., Hult, G. T. M., Ringle, C. M., Sarstedt, M., Danks, N. P., & Ray, S. (2021). Partial least squares structural equation modeling (PLS-SEM) using R: A workbook (p. 197). Springer Nature.

- Hajishirzi, R. et al., (2022). Boosting sustainability through digital transformation’s domains and resilience.

- Herlinawati, E., Ahman, E., & Machmud, A. (2019). The effect of entrepreneurial orientation on SMEs business performance in Indonesia. Journal of Entrepreneurship Education

- Hesniati, H., Margaretha, F., & Kristaung, R. (2019). Intellectual capital, knowledge management, and firm performance in Indonesia.

- Hussain, I., Mujtaba, G., Shaheen, I., Akram, S., & Arshad, A. (2022). An empirical investigation of knowledge management, organizational innovation, organizational learning, and organizational culture: Examining a moderated mediation model of social media technologies.

- Iliyasu, R., Etikan, I. (2021). Comparison of quota sampling and stratified random sampling. Biometrics & Biostatistics International Journal.

- International Finance Corporation. https://www.ifc.org > publications_ext_content>ar2015

- International Fund for Agricultural Development (IFAD) (2019). https://www.interacion.org.

- Kaur, P. (2014). Outreach and sustainability of microfinance institutions in India in pre and post Andhra Pradesh microfinance crisis in context of South Asia. Global Journal of Finance and Management.

- Kayembe, H., Lin, Y., Munthali, G. N. C., Xuelian, W., Banda, L. O. L., Dzimbiri, M. N. W., & Mbughi, C. (2021). Factors affecting the sustainability of microfinance institutions: a case of Malawi microfinance institutions.

- Kivits, R. A., & Furneaux, C. (2013). BIM: enabling sustainability and asset management through knowledge management. The Scientific World Journal, 2013.

- Kline, R. B. (2023). Principles and practice of structural equation modeling. Guilford publications.

- Lee, J. (2021). Sustainability of Microfinance Institutions: A Systematic Literature Review. Sustainability. https://doi.org/10.3390/su13031511

- Lopatta, K., Tchikov, M., Jaeschke, R., & Lodhia, S. (2017). Sustainable development and microfinance: the effect of outreach and profitability on microfinance institutions’ development mission. Sustainable Development

- Martínez-Peláez, R., Ochoa-Brust, A., Rivera, S., Félix, V. G., Ostos, R., Brito, H., … & Mena, L. J. (2023). Role of digital transformation for achieving sustainability: mediated role of stakeholders, key capabilities, and technology.

- Maes, P. & Reed, D. (2014). Openness, innovation, and entrepreneurship: A literature review. Journal of Technology Management & Innovation.

- Mueller, R. O., & Hancock, G. R. (2018). Structural equation modeling. In The reviewer’s guide to quantitative methods in the social sciences.

- Muhammad, M., Wallerstein, N., Sussman, A. L., Avila, M., Belone, L., & Duran, B. (2015). Reflections on researcher identity and power: The impact of positionality on community based participatory research (CBPR) processes and outcomes. Critical sociology.

- Mujeri, M. K. (2020). Digital Transformation of MFIs: A Post Covid-19 Agenda for Bangladesh

- Mylenko, N., & Iqbal, Z. (2016). Developing islamic finance in the Philippines.

- Nkurunziza, G., Ntayi, J. M., Munene, J. C., & Kaberuka, W. (2018). Knowledge management, adaptability and business process reengineering performance in microfinance institutions.

- Pal, A., Dey, S., Nandy, A., Shahin, S., & Singh, P. K. (2021). Digital Transformation in Microfinance as a Driver for Sustainable Development.

- Panda, D. K. (2018). Entrepreneurial orientation, intermediation services, microfinance, and microenterprises. Managerial and Decision Economics

- RaghuRam, P. K., & Prabhu, T. N. (2014). Impact of Knowledge-based ecosystem for microfinance.

- Serrano-Cinca, C., Gutiérrez-Nieto, B., & Reyes, N. M. (2016). A social and environmental approach to microfinance credit scoring.

- Shea, T., Usman, S. A., Arivalagan, S., & Parayitam, S. (2023). “Knowledge management practices” as moderator in the relationship between organizational culture and performance in information technology companies in India. VINE Journal of Information and Knowledge Management Systems.

- Simatele, M., & Dlamini, P. (2020). Finance and the social mission: a quest for sustainability and inclusion. Qualitative Research in Financial Markets.

- Torres, G.C.L., Guzman, G.M., Kumar, V., Lona, L.R., & Cherrafi, A. (2017). Knowledge management for sustainability in operations. Production Planning & Control https://doi.org/10.1080/09537287.2019.1582091

- WAINAINA, A. W. (2017). Effect of entrepreneurial orientation on the growth of micro finance institutions based in Nairobi, Kenya (Doctoral dissertation, Jomo Kenyatta University of Agriculture).

- World Bank. (2014). Global Financial Development Report 2014: Financial Inclusion. Washington, DC: World Bank. https://doi.org/10.1596/978-0-8213-9998-8

- Zheng, G. W., Siddik, A. B., Masukujjaman, M., & Fatema, N. (2021). Factors affecting the sustainability performance of financial institutions in Bangladesh: the role of green finance.