Effectiveness of International Financial Reporting Standard Enforcement in Nigeria

- Innocent Okwuosa

- Oluwole Dotun Peter

- 798-843

- Apr 23, 2024

- Finance

Effectiveness of International Financial Reporting Standard Enforcement in Nigeria

Innocent Okwuosa, Oluwole Dotun Peter

Department of Accounting, Caleb University

DOI: https://doi.org/10.51244/IJRSI.2024.1103055

Received: 06 February 2024; Revised: 13 March 2024; Accepted: 18 March 2024; Published: 23 April 2024

INTRODUCTION

Background to the Study

The general belief in accounting literature is that the adoption and application of IFRS in developing countries will enhance the quality of financial statement information including its reliability and comparability (Ballas, Skoutela and Tzovas, 2010). However, it is also argued that no matter how high the quality of the accounting standards adopted, comparable and high-quality accounting information will not be achieved without strict enforcement of these standards (White house, 2012). IFRS is “a set of accounting rules, principles and procedures that aim to create a common financial reporting platform with the objective of bringing transparency, accountability, efficiency to financial markets, harmonization of accounting practices and enforcement.

Even though some countries claimed they have officially adopted IFRS and mandated companies to prepare financial statements accordingly, some companies may selectively implement IFRS recognition and disclosure requirements. Even with increasing IFRS adoption around the world, notable differences in financial reporting systems will remain due to regulatory, political, and institutional differences across countries, leading to variation in IFRS compliance between different jurisdictions (Soder storm and Sun, 2007). Such variation hinders the main goal of developing a global set of accounting standards which is comparability of accounting information across countries.

Chen and Zhang (2010) provided empirical corroboration from the Chinese market that mere adoption of IFRS does not necessarily lead to the perceived high-quality and comparable financial accounting information because of enforcement challenges and lack of full compliance.

Statement of the Problem

The worry about compliance with IFRS requirements is essentially emphasized with regard to its application in developing countries that might have deficient financial reporting environment and inadequate monitoring and enforcement mechanisms. The adoption of IFRS in developing countries always has its own shortcomings such as application difficulties, and enforcement issues (Alp and Ustundag, 2009) that might cast doubts on the expected benefits of global harmonization of accounting standards.

There are cases involving FRCN and some companies in Nigeria concerning enforcement of IFRS in Nigeria. Notable ones are cases involving FRCN and Stanbic IBTC. FRCN and Eko Hotels, FRCN and Audit Committee chairman. The judgement passed on these cases shows the challenges of FRCN in enforcing IFRS in Nigeria. Given these challenges, this research work examined issues affecting proper enforcement activities of Financial Reporting Council of Nigeria.

Although, there have been several literatures regarding adoption of IFRS in Nigeria, but none has really delved into effectiveness of IFRS enforcement in Nigeria. This research work therefore examines the effectiveness of IFRS enforcement in Nigeria using the functions of FRCN such as review, monitoring, sanctions, culture, Legal law setting up FRCN and education as proxy to measure the effectiveness of financial reporting enforcement in Nigeria.

Objective of the Study

The main aim of this study is to examine the effectiveness of IFRS enforcement in Nigeria. In order to accomplish the aim of the study, three research objectives were developed and stated below.

- To examine the challenges faced by FRCN in the enforcement of IFRS in Nigeria.

- To examine the perception of accountants and auditors about the effectiveness of IFRS enforcement in Nigeria.

- To examine the difference in perception between accountants and auditors concerning effectiveness of IFRS enforcement in Nigeria

Research Questions

- What are the challenges faced by FRCN in the enforcement of IFRS in Nigeria?

- What is the perception of the effectiveness of FRCN’s IFRS enforcement by accountants and auditors?

- What is the difference in perception of the effectiveness of IFRS enforcement in Nigeria between the auditors and accountants?

Research Hypotheses

H01: There is no significant challenges faced by FRCN in the enforcement of IFRS in Nigeria.

H02: There is no perception of effectiveness of FRCN’s IFRS enforcement by accountants and auditors.

H03: There is no significant difference in the perception of effectiveness of IFRS enforcement in Nigeria between auditors and accountants.

Scope of the Study

The study examines the current state of effectiveness of IFRS enforcement in Nigeria by FRCN using the views of accountants and auditors and FRCN staffs.

Significance of the Study

This study would provides a guide that will assist investors to assess the enforcement mechanism put in place by Nigerian Government to make meaningful decision as regards their investment. Similarly, this study would enable auditors and accountants to realize the extent to which enforcement mechanisms put in place by FRCN assist in ensuring compliance with International Financial Reporting Standards.

Definition of Terms

- Accounting Quality: Relevance and reliability of accounting measures used to inform stakeholders regarding the financial situation and position of the company.

- International Financial Reporting Standards (IFRS): IFRS is the international accounting framework within which to properly organize and report financial information.

- Financial Reporting Council of Nigeria (FRCN): This is the Federal Government Agency in Nigeria charged with the responsibility of setting accounting standards, enforcing the standards, and monitoring compliance.

- Enforcement Mechanisms: In relation to IFRS enforcement, enforcement mechanisms are procedures put in place by FRCN to ensure companies in Nigeria abide by provisions of accounting standards.

- Accounting Harmonization: This is the process of increasing the level of agreement in accounting standards and practices between countries

- Accounting Comparability: Comparability is the level of standardization of accounting information that allows the financial statements of multiple organizations to be compared to each other. This is a fundamental requirement of financial reporting that is needed by the users of financial statements.

REFERENCES

- Ballas, A., D. Skoutela, and C. Tzovas, (2010). The relevance of IFRS to an emerging market: evidence from Greece Managerial Finance, 36(11): 931-948

- Benston, G. J., Bromwich, M., Litan, R. E., & Wagenhofer, A. (2006). Worldwide Financial Reporting: The Development and Future of Accounting Standards. New York: Oxford University Press.

- Chen, J., and H. Zhang, (2010). The Impact of Regulatory Enforcement and Audit upon IFRS Compliance -Evidence from China. European Accounting Review, 19(4):665-692

- Collins, S. H. (1989). The Move to Globalization: Is a Common International Accounting Language Feasible? Journal of Accountancy, 167, 82-85.

- Roussey, R. S. (1992). Developing International Accounting and Auditing Standards for World Markets. Journal of International Accounting, Auditing and Taxation, 1 (1), 1-11.

- Samuels, J. M., & Piper, A. G. (1985). International Accounting: A Survey. New York: St. Martin’s Press

- Securities and Exchange Commission, (2012). Work Plan for the Consideration of Incorporating International Financial Reporting Standards into the Financial Reporting System for U.S. Issuers, Final Staff Report, July 2012.

- Soderstrom, N., and K. Sun, (2007). IFRS Adoption and Accounting Quality: A Review. European Accounting Review, 16(4):675-702.

- Whitehouse, T., (2012). SEC Delays IFRS Plans, Companies Grow Impatient. Complianceweek.com, February: 22-58.

- Wyatt, A. R., & Yospe, J. F. (1993, July). Wake-up Call to American Business: International Accounting Standards are on the Way. Journal of Accountancy, 80-85.

LITERATURE REVIEW

Theoretical Review

Institutional Theory

Institutions are the foundation of social life and are generally defined as “rules, norms and beliefs that describe reality for the organization, explaining what is and what is not, what can be acted upon and what cannot” (Hoffman, 1999). These understandings, taken-for-granted and culturally absorbed, specify, and justify social arrangements and formal and informal behaviors (Garud et al., 2007). Thus, institutional influences are exerted on organizations through rules and regulations, normative prescriptions, and social expectations (Pache and Santos, 2010). A country’s social, political, economic, and accounting environment cannot be ignored in the process of international accounting convergence (Uzma, 2016). The neo-institutional theory has been applied to better understand how accounting influences and is influenced by the institutional context at the organizational and societal levels (Dillard et al., 2004).

Historically, the institutional perspective has been mainly used as a theoretical framework to explain the perceived homogeneity within organizational fields (DiMaggio and Powell 1983; Greenwood et al., 2017). Neo-institutional theorists tend to focus on how organizations obtain legitimacy by describing processes of isomorphism and compliance within a particular organizational field (Deephouse et al., 2017). In these fields, cultural, social, and political issues explain the change. In this regard, Hannan and Carroll (1995) argue socio-political legitimacy cannot be ignored since organizations do not function in isolation from professions, the State, and broader societal influences.

Financial reporting council of Nigeria was set up as an agency of Government to monitor the activities of public and private entities in Nigeria as regards their financial reporting activities. From the findings, most entities see IFRS compliance in Nigeria as a mere regulatory requirement and therefore a tick box approach. This goes a long way to explain that without a proper institution in place to monitor the financial reporting activities of these companies, they would have decided not to adopt and comply with IFRS provisions. From another perspective, findings also revealed that most entities agreed that IFRS enforcement in Nigeria is effective because someone is acting as a watchdog, checking, and reviewing the financial statements of these entities if they are in line with requirements of the IFRS framework. One of the functions of FRCN is to enhance the credibility of financial reporting, improve the quality of accountancy and audit services, actuarial, valuation and corporate governance standards. With this, an institution is in place to carry out review activities of financial reporting activities of corporate entities in Nigeria.

Therefore, institutions are like pillars that ensure a structure stand firm. In this regard, Financial Reporting Council of Nigeria play a pivotal role in ensuring that corporate entities in Nigeria prepare financial statements that conforms in all material respects with the provision of IFRS.

Agency Theory

Agency theory is a principle that is used to explain and resolve issues in the relationship between business principals and their agents. Most commonly, that relationship is the one between shareholders, as principals, and company executives, as agents.

Agency theory proposed by Jensen and Meckling (2019) is a theory which suggests that the separation between owners and managers of a company can cause agency problems. The agency problem in question, among others, is the occurrence of asymmetric information (not the same) between those owned by the owner and manager. With the unequal ownership of information, the management (agent) of the company tends to carry out moral hazard and adverse selection. Managers do have an obligation to maximize the welfare of shareholders. But on the other hand, managers also have an interest in maximizing their welfare. The unification of the interests of these parties often creates a problem called the agency problem.

The worsening condition of agency problems is also caused even though managers get compensation from their work, but the change in the wealth of managers is much smaller when compared to changes in the prosperity of shareholders or owners (Midiastuty and Machfoedz 2003). Agency theory provides an important role for accounting, especially in providing information after an event which is referred to as the post-decision role. This role is often associated with the accounting stewardship role, where an agent reports to the principal about past events. This is what gives accounting its feedback value in addition to its predictive value.

According to Eisen hardt (1989) because what is analyzed is the contract that regulates the relationship between the principal and agent, the focus in this theory is on determining the most efficient contract, agency theory is based on three assumptions, namely: assumptions about human nature, assumptions about organizations, assumptions about information. Agency theory that is starting to develop refers to the fulfillment of the main goal of financial management, namely maximizing shareholder wealth. This wealth maximization is carried out by management called agents. The inability or reluctance of managers to increase shareholder wealth creates what is called the agency problem.

With respect to compliance with IFRS in Nigeria, Financial Reporting Council of Nigeria ensure protection of investors and other stakeholder’s interest by ensuring accuracy and reliability of financial reports and corporate disclosures, pursuant to the various laws and regulations currently in existence in Nigeria. This function by FRCN compel companies to disclose relevant information that the shareholders and investors would require to make informed decisions. This information would not have been disclosed if FRCN is not there as a body to ensure such disclosure. This disclosure however discourages information asymmetry that always constitute problem in agency theory. Enforcement of IFRS by FRCN in Nigeria ensure companies disclose full information about what transpired in the companies in the last twelve months. This is supported by respondents’ reaction to one of the questions in the questionnaire. Majority of the respondents agreed that FRCN conduct thorough review of financial statements submitted by companies in line with IFRS.

Public Interest Theory of Regulation

Over the years there have been many arguments and debates over the necessity for regulation. Those who believe in the efficacy of markets argue that regulation is not necessary as market forces will operate to best serve society and optimize the allocation of resources. However, there are many who point out that markets do not always operate in the best interests of societies so some form of intervention in the form of regulation is necessary. This is obvious in many aspects of society. For example, if there were no road rules for drivers’ chaos would result on the roads. If there were no restrictions on some “economic” activities, then there would not be any need of drug smugglers as the market would indicate the need (demand) for drugs which would subsequently be supplied. These are obviously extreme examples, but it is not hard to realize that there are many instances were regulations protect societies from undesirable activities.

In 19th century Britain there was considerable optimism over the benefits brought by the Industrial Revolution, and it was deemed undesirable for governments to “interfere” with the operation of “pure capitalism”. Governments, therefore, pursued a policy of what was known as laissez-faire (from the French “let be”, or leave alone). However, people soon came to realize that this created many social ills and some of these are reflected in the novels of Charles Dickens, such as Oliver Twist, and the writings and work of other artists and social commentators. Working conditions were often dangerous and inhumane, such as making use of child labor and extraordinarily long working hours which led to considerable poverty and misery. Governments soon intervened and imposed the regulations on economic activity that were considered socially desirable. The issue of the regulation of accounting also became an issue, especially after the economic crash of the 1920-30s which, amongst other things, led to the search for accounting principles and theory described. A major objective of accounting is to provide information to interested parties who may not have access to complete (or the necessary) information to make economic decisions – they are at an information disadvantage so there is information asymmetry. This information asymmetry is often used to justify the need for accounting regulation. However, the regulation extends well beyond the information to the preparers of information. That is, the professional competence of those calling themselves accountants or auditors and generally believed to be the most able to provide and/or supervise the provision of financial information.

Levine and Forrence (1990) see public interest theory as achieving certain publicly desired results which, if left to the market, would not be obtained. The regulation is provided in response to the demand from the public for corrections to inefficient and inequitable markets. Thus, regulation is pursued for public, as opposed to private, interest related objectives. This was the dominant view of regulation until the 1960s and still retains many adherents. It is generally felt that determining what is the public interest is a normative question and advocates of positive theorizing would, therefore, object to this approach on the basis that they believe it is not possible to determine objective aims for regulation; there is no basis for objectively identifying the public interest.

In the context of IFRS enforcement in Nigeria, public interest theory of regulation provides an avenue where stakeholders of financial reporting see the laws and regulations of FRCN as guiding principle in ensuring compliance with IFRS in Nigeria. From the findings of this study, Nigerian companies comply with provisions of IFRS because they realize that sanctions and penalties imposed by FRCN are hefty and will affect the financial resources of their organization. Therefore, they ensure no stone is left untouched regarding what to do in ensuring reliable and comparable financial statements are produced.

There are other charges laid at the feet of the public interest approach. These include attention being directed to the regulators themselves. Is it possible for them to act in a disinterested manner? Are they sufficiently competent? As might be expected such critics suggest there may be questions of the reward structure for regulators (being insufficient), their career structure and training may be inadequate. In addition, it is often argued that the public interest approach underestimates the effects of economic and political power influences on regulation.

Conceptual Literature Review

Financial Reporting Council of Nigeria (FRCN)

The Financial Reporting Council (FRC) of Nigeria is a federal government agency established by the Financial Reporting Council of Nigeria Act, No. 6, 2011. It is a federal government Parastatal under the supervision of the Federal Ministry of Industry, Trade, and Investment. The FRC is responsible for, among other things, developing and publishing accounting and financial reporting standards to be observed in the preparation of financial statements of public entities in Nigeria, and for related matters. The Council’s main objectives, as defined in the FRC Act, No. 6, 2011 are to: (i) Protect investors and other stakeholder’s interest, (ii) Ensure good corporate governance practices in the public and private sectors of the Nigerian economy, (iii) Give guidance on issues relating to financial reporting and corporate governance to professional, institutional, and regulatory bodies in Nigeria, (iv) Ensure accuracy and reliability of financial reports and corporate disclosures, pursuant to the various laws and regulations currently in existence in Nigeria, (v) Harmonize activities of relevant professional and regulatory bodies as relating to corporate governance and financial reporting, (vi) Promote the highest standards among auditors and other professionals engaged in the financial reporting process, (vii) Enhance the credibility of financial reporting, and improve the quality of accountancy and audit services, actuarial, valuation and corporate governance standards.

The benefits of high-quality Financial Reporting are numerous; amongst which are: (i) Promoting private sector growth and reducing volatility in the economy by strengthening the country’s financial reporting architecture and reducing the risk of financial market crises together with the associated negative economic impact, (ii) Enhancement of local and foreign Direct and portfolio Investment as investors are better able to evaluate corporate prospects and make informed decisions resulting in access to capital at lower costs, (iii) Facilitating the growth of small-scale enterprises as their compliance with transparent reporting will provide easier access to credit. (iv) Facilitating integration into global financial and capital markets, (v) improvement of public sector fiscal discipline and enhancement of value for money, and (v) Generation of employment opportunities.

Operations of FRCN

High quality financial reporting is a building block of a market-based monitoring of companies, external auditors, and other professionals whose work bear upon financial reporting integrity and corporate governance of entities, no matter how remote. This will allow shareholders and the public at large to assess management performance confidently and objectively, thus influencing their behavior and decisions. High quality financial reporting will also contribute to national public finance by improving the assessment and collection of taxes on corporate profits.

The operating arms of the FRC are: (i) Directorate of Accounting Standards – Private Sector, (ii) Directorate of Accounting Standards – Public Sector, (iii) Directorate of Auditing Practice Standards, (iv) Directorate of Actuarial Standards, (v) Directorate of Valuation Standards, (vi) Directorate of Inspection and Monitoring, and (vii) Directorate of Corporate Governance. (Each Directorate is managed by a team of professionals and experts as applicable).

IFRS Enforcement

The introduction of IFRS in any particular jurisdiction would simply constitute a part in the laws and regulations existing in that jurisdiction relating to how business affairs are being governed. Often times, these laws and regulations try to overlay one another or simply become inconsistent especially when sound enforcement mechanisms are absent or the role of various institutions responsible for the enforcement are not well defined (NASB, 2010). The role of institutional infrastructures in ensuring rigorous and effective application of IFRS cannot be over emphasized. Realizing the benefits attached to these global standards involves strong legal, institutional and professional support (Europeens, 2001). Therefore, absence of stringent and clearly spelt out enforcement and regulatory system as well as quality professional accountants may result in inefficiency and inappropriate application of IFRS. Moreover, for the adoption of IFRS to be effective, there should be an adequate awareness campaign and improvement in the quality of a professional accountant, at the same time, professional accountants are required to give orientation on how IFRS are being applied (James, 2009).

Challenges of IFRS Enforcement

The adoption of new reforms, standards and strategies by organizations is always associated with challenges and problems emanating from internal and external environment of organizations. These internal and external environmental challenges if not properly managed and addressed can hamper the gains associated with the new standards, reforms and strategies introduced. By application and implication, the adoption and enforcement of the International Financial Reporting Standards (IFRS) in Nigeria is likely to be confronted with challenges and problems which demands proper measures in order to enjoy the full benefits of IFRS.

Duplicate Regulation

The tussle for hegemony among ‘gatekeepers’, namely, those with some form of watchdog role in the financial reporting framework, e.g., the Securities and Exchange Commission, the Stock Exchange, accounting profession, standards setters, legislature, and, to some extent, the academia. They must see the commonality of their goals and demonstrate candor by yielding to common purpose of ensuring a robust framework for responsible financial reporting, instead of engaging in internecine bickering over irrelevant leadership posturing.

The Return of Non-audit services

Severance of consulting services that amount to executive management function of clients from the variety of services offered by audit firms was aimed at improving their independence. Since after Sarbanes-Oxley Act in 2002, some accounting firms and their protagonists have launched back intellectual and philosophic arguments against restrictions to audit services despite empirical evidence that in all the egregious cases of financial reporting scandals, weak auditor independence, particularly with low-visibility conflict of interest scenario, contributed immensely, sometimes most profoundly, to auditor compromise and acquiescence that resulted in fraudulent financial reporting (Coffee, 2006).

Degrading Standards in Education

Many commentators and analysts (Financial Research Associates, 2009) have observed that there are “massive institutional pedagogical gaps and dysfunctions in accounting education” that affect the quality of graduates feeing the cycle of accounting manpower in the profession. Due to lowering of standards and inadequate investment in education, especially in SSA countries, students pass through accounting programs reading sketchy lecture notes as their main source of knowledge, then go on to prepare for professional examinations by reading hurriedly-collated study packs that do not cover necessary scope in accounting education. The Big accounting firms, professional bodies and government have so far failed in the moral duty to provide financial and research support to accounting teachers and students. The result is a generation of accountants who, even if they have good intention, lack the superior competence necessary to face the complex challenges of financial reporting in a sophisticated capitalism.

Resistance and Acceptability Challenge

The adoption of new accounting reform measures like the International Financial Reporting Standard (IFRS) in a developing country like Nigeria is usually associated with the problems of integration, resistance and acceptability. Accounting reforms that are geared towards promoting transparency in financial information being reported are bound to be resisted by those who are beneficiaries of the “old system”. Implementing accounting reforms that emphases standards are usually perceived as pertinent mechanisms for making and encouraging transparency in government (Kettl, 2000) and private sector. Stakeholders in public and private organizations might question their “hope and future” in the adoption, implementation and enforcement of IFRS. Where such “hope and future” are not bright enough to motivate support for IFRS, resistance and acceptability challenges might occur. As some studies have demonstrated, top management and executive may sometimes be less interested in accepting and implementing change (Ridder, Bruns and Spier, 2005). The resistance in adopting IFRS and accepting its “tenets and prescriptions” is also connected to the mentality associated with colonization and recolonization of countries by the strong and clever countries. For instance, the International Financial Reporting Standards has not been adopted in the United State of America because IFRS is viewed by the operators of the US economy as an attempt by European countries to colonize and corrupt the US accounting sector with inferior/substandard set of accounting standards (Ocheni, 2015). This debate has been on especially among radical political economists in developed and developing countries.

Although the view has been on, Gelter and Eroglu (2014) have countered it by arguing that it is a myth. According to them, the introduction of IFRS in Europe was strongly supported and backed-up by the United States especially following capital market internationalization in the 1990s. Speaking about the benefit of internationalization in the accounting sector Ball (1995:29) writes that “Internationalization will reduce some or much of diversity in accounting rules and practices across nations, it will not eliminate it. Nor should it”.

Adaptability and leadership Challenges

Similar to the challenge of resistance and acceptance is the problem of adaptability and leadership. Leadership has been a challenge in the implementation of policies and programmes in developing countries. In addition, the adoption of foreign based reforms and prescriptions like those advocated by IFRS is associated with variations and diversity. Ball (2006) shows this challenge and concern when he noted that the adoption of IFRS by countries and organizations will not be uniform and that this will impact on the reporting and perception of IFRS quality by users (Ball, 2006 cited in Odia and Ogiedu, 2013). IFRS poses the challenges of creating the necessary structures and institutions to support its adaptability. The adoption of IFRS by countries as observed by some scholars are sometimes not accompanied with complementary changes in enforcement structures and institutions (Ramanna, 2013). Change in leadership of public and private organizations are known to affect sustainability of new reforms. We see this challenge in the implementing IFRS in Nigeria. Providing the right legal structures, addressing cultural and old traditions to align with the tenets/standards of IFRS are some of the implementation challenges that will affect the adoption of IFRS in Nigeria. In the light of the above, technical challenges, cultural and traditions, legal difficulties and requirements, educational and training needs, and politics are said to affect the implementation process of IFRS in countries of the world (Obazee, 2007, Odia & Ogiedu, 2013).

Frequent Change in Government

Most developing countries are prone to unconstitutional changes in government. When this occurs the policies and programmes of the “displaced” government might be changed by new government. The fear expressed is that IFRS will be negatively affected if implemented in such an uncertain environment that is susceptible to change. This therefore poses the challenge and concern that the adoption of IFRS will be associated with inadequate enforcement for emerging markets economies that are making efforts to harmonize with IFRS (World Bank cited in Ramanna & Sletten 2013). Frequent changes in government may be accompanied with undue political interference in the implementation process of IFRS.

Bureaucratic Bottleneck

Bureaucratic procedures could pose a threat to the implementation of IFRS. Most public and private organizations are established on strong and rigid norms and rules which sometimes constitute a strong opposition to the implementation of reforms.

Till date, the profession is facing many of these challenges and threats. This is the historical context underpinning the enactment of the Financial Reporting Council of Nigeria (FRC) law. The litmus test for the FRC therefore lies in its capacity to overcome the threats and challenges and to usher a sustained regime of better professional accounting practice and improved financial reporting environment. That is the benchmark against which the success or failure of the FRC is to be measured or judged.

Empirical Review

Numerous works has been carried out by scholars on adoption of International Financial Reporting Standards locally and globally while few ones has been carried out on International Financial Reporting Standards enforcement. The purpose is to see the effectiveness of accounting standards in bringing consistency, integrity, and comparability of accounting information, regardless of the company or the country. The empirical review will focus on both developed and developing countries to examine from empirical perspective how effective is enforcement and compliance with IFRS from different jurisdiction across the world.

These research works are grouped into different strands in accordance with the research areas. Nicolae, Albu and Hoffman (2021), Samarasekera, Chang and Tarca (2012), Al-Hussaini, Al-Shammari and Al-Sultan (2008), Silva, Jorge and Rodrigues (2021), Johansson and Giljam (2014), Leonard and Jan (2013) analyzed and examined IFRS enforcement mechanism put in place by countries in ensuring effectiveness of accounting standards in their various jurisdictions.

Nicolae et al. (2021) examined westernization of a financial reporting enforcement system in an emerging economy. The study uses a semi-structured interviews and publicly available information in accounting, auditing and capital market of Romania. The study further investigated the institutional factors within and across the key components of Romanian Financial Reporting Enforcement System (FRES) which include the preparers and auditors of corporate financial reports and public oversight bodies. The study concluded that the operationalization of Financial Reporting Enforcement System in Romania has been more superficial than substantive driven by impression of management desires than pursuit of fundamental and systemic change. However, the study did not come across any explicit case of corruption or consequences of corruption in relation to financial reporting processes.

Silva et al. (2021) examined enforcement and accounting quality in the context of IFRS to assess whether there is a gap in literature. The study used structured literature review by conducting scientometric analysis of papers on the relationship between enforcement and accounting quality construed in a broad sense. The study reviewed papers published between 2006 and 2019 selected from web of science database. The study discovered that there are shortage of studies analyzing IFRS enforcement practices in individual countries and also shows that most studies rely on quantitative analysis using multivariate regression analysis. The study also proposes analysis of the practices of enforcers.

Johansson and Giljam (2014) Investigated enforcement of IFRS in Europe by identifying practical differences between countries. The study used qualitative descriptive study with a primary research approach based on semi-structured interviews using representatives from nine enforcement bodies. The study also analyzed empirical findings by comparing it with previous literature. The study found out that national enforcement bodies differ in several areas. The areas are structures, resource legal authority, examination approach, results of examination, sanctions and European cooperation of enforcement overseen by ESMA (European Security and Market Authority). However, the study calls for further research to conduct quantitative analysis or study examining the availability of information among enforcers as well as a similar study involving the use of implementation of consultation papers from ESMA.

Leonard and Jan (2013) examined IFRS, enforcement, and their role for accounting quality and comparability. The study analyzed twelve-year time period using a data set consisting of 24 countries. The proxy for accounting quality in this study includes value relevance and earnings management. Empirical construct was used to measure accounting comparability and test design to determine the influence of institutional settings on accounting comparability. Regression analysis was used to analyze data while the study found out that accounting quality and comparability decreases following IFRS adoption. Furthermore, findings also indicate that the importance of concurrent enforcement changes seems to be limited to second order capital market effects documented by prior research.

Al-Hussaini et al. (2008) investigated the development of enforcement bodies mechanism following the adoption of International Accounting Standards in Gulf Cooperation Council. Member states namely, Bahrain, Oman, Kuwait, Saudi Arabia, Qatar, and United Arab Emirates were chosen as population. Year 1999 to 2003 were reviewed. It was discovered that activities of the enforcement bodies increased because of International Accounting Standards adoption. This was depicted in majority of audit reports qualified during the period while complaints about financial reports were faced with severe actions by the enforcement bodies on the company’s directors and officers. Despite common accounting standards, legal framework and audit requirements among member countries, enforcement outcomes differ. The study shows the activities of the enforcement bodies and the external auditors but did not provide link between compliance and enforcement activities. The study combines both primary and secondary data collection methods. Personal interviews were conducted with directors of surveillance departments for joint stock companies of the ministries of commerce, stock exchanges and the banking control departments of the central banks in the Gulf member states.

Samarasekeraa et al. (2012) reviewed IFRS and accounting quality and Impact of enforcement. The study aims at investigating the impact of enforcement on accounting quality under IFRS using factors such as earnings smoothing, timely loss recognition and value relevance. The study took sample of 495 listed UK firms from 2000 to 2009 under UK GAAP and IFRS. The sample also include 246 cross listed firms. Firms were drawn from range of industry sectors based on GICS: 138 financial firms, 104 industrial, 93 consumer discretionary, 53 information technology, 37 materials, 26 consumer staples, 19 health care, 13 energy, 7 utilities and five telecommunication services. Data were also collected from DataStream to measure accounting quality. Regression model and spearman rank correlation test were used to analyze the variables (earnings smoothing, value relevance and timely loss recognition). The study concludes that IFRS has the potential to provide more transparent and comparable information which in turn will influence capital market efficiency and economic growth. However, the study fails to address the impact of changes in oversight of auditors and enforcement of financial reporting system by independent enforcement bodies.

In similar work across different countries, Ball, Robin and Wu (2003), Brown, Preiato and Tarca (2014), Preiato, Brown and Tarca (2015), Andre, filip and Paugam (2015), reviewed legal settings, institutional settings, and enforcement of accounting standards as it affects audit and financial reporting while Verdi (2006), Heralth and Albarqi (2017) examined financial reporting quality in the context of IFRS.

Ball et al. (2003) examined the relationship between accounting standards and structure of other financial institutions on the attributes of financial reporting system. Four Asian countries were taken into consideration which include Hongkong, Malaysia, Thailand and Singapore. Findings revealed that the four countries deployed high-quality standards to achieve quality financial accounting reports but faced with institutional structures which provide incentives that affect the outcome of financial reporting. The study argued that beyond quality accounting standards, remunerations of auditors and preparers, enforcement mechanism and ownership structure affect the quality of financial reporting. Regression models were employed to analyze data, but the study did not state the appropriate benchmark for quality financial reporting, the level of conservation needed as regards timely recognition of loss.

Brown et al. (2014) measures country differences in enforcement of accounting standards: An audit and enforcement proxy. This study shows differences between countries in relation to institutional settings for financial reporting, auditing of financial statements and enforcing compliance with each country’s accounting standards. The study conclude that the proxies are less effective because they rarely concentrate on factors that solely influence how accounting standards and compliance are promoted through activities of external audits and independent enforcement bodies. The scope of the study covers 51 countries and secondary data were gathered from international federation of Accountants (IFAC), World Bank and national security regulators concerning public company auditors, working environments and degree of accounting enforcement activities. Despite the reliability of this study due to the underlying data employed, the study does not have direct evidence of relationship included in the index and the quality of audit and enforcement. Though, assumptions were made about the relationship of activities and outcome but detailed evidence that demonstrate the relationship were not known.

Preiato et al. (2015) conducted research on comparison of between country measures of legal settings and enforcement of accounting standards. This study dwells on promotion of high-quality financial reporting and favorable capital market outcomes. The study also examines firms’ information environment, represented by the error in analyst, consensus forecast and extent of disagreement among analysts. A sample of 357,054 firm-month observation on the errors and dispersion of analyst were selected for the financial year 2003-2009 and earnings forecast of 10,764 firms stationed in 39 countries of political and economic importance to the researcher. The study concluded that accounting enforcement can be more important in securing favorable economic outcomes than has been previously realized. Regression model was employed in data analysis but the study basis of selecting the countries were not adequately stated with facts and figures.

Andre et al, (2015) examined the impact of mandatory change to IFRS by European firms on the level of accounting conservatism. It was discovered that accounting conservatism reduced after IFRS adoption by European countries. Also, differences in institutional and legal settings across countries in Europe disappears after IFRS adoption. The level of decrease in conservatism is most significant with European countries that possess the highest differences with the new IFRS standards. The study covers 16 European countries which are Austria, Belgium, Denmark, Germany, Finland, France, Great Britain, Greece, Ireland, Italy, Netherlands, Norway, Portugal, Spain, Sweden, and Switzerland for the period 2003 to 2007. The study uses linear regression model to analyze timely loss recognition of accounting earnings on stock returns, legal incentives, Governance, investor protection and enforcement, prior tax book conformity and prior accounting differences. A sample of 2,477 mandatory IFRS adopters from 16 EU countries were selected. However, the study did not place emphasis on whether conditional conservatism is good or bad.

Verdi (2006) studied the relationship between financial reporting quality and investment efficiency. A sample 38,062 firm year observations in the period between 1980 and 2003 were taken. Multiple regression model was employed to analyze the data gathered. The study revealed that the relationship between financial reporting system and investment efficiency was stronger for firms with low quality information environments. The study also examines the link between financial reporting quality and investment efficiency using under investment, over investment, cost of raising funds, project selection and agency issues. Though financial reporting quality is more associated with over investment for firms with large cash balances and dispersed ownership but, the study did not investigate the determinants of investment efficiency and economic consequence of enhanced financial reporting.

Herath and Albarqi. (2017) examined financial reporting quality. The study reviewed existing literature from some accounting journals, official accounting information and published papers from 2009 to 2015. The study revealed that financial reporting quality depends on some important features which are reliability, comparability, under stand ability, timeliness, and faithful representation. The study further shows that financial reporting quality is influenced by several factors such as earnings management, corporate governance practices, capital markets, internal control, internal reporting system, accounting Standards, Information technologies and accounting, information Systems, auditing, accounting Conservatism, financial restatements, company reputation, culture, business ethics, chief executive Officers (CEO) age, CEO inside debt holdings, the entity size, age, and the board size. The study did not get enough samples to draw reasonable conclusions. Also, the study did not dwell much on corporate governance as a factor that can influence financial reporting quality.

Also, the streams of work below from scholars abroad and Nigeria examined mandatory adoption of IFRS, IFRS compliance and audit quality, and effects of IFRS adoption on factors such as performance, earnings management, investment efficiency and financial statement quality.

Rouhou et al. (2015) examined the effect of mandatory adoption of IFRS and enforcement factors on analyst earnings forecasts accuracy. The study took a sample from the population of French non-financial groups listed in French stock exchange during the period before mandatory adoption of IFRS between 2003-2004 and the period post mandatory adoption of IFRS 2006 to 2007. A sample of 98 companies were selected and were analyzed using regression model. The study concluded that mandatory adoption of IFRS by French companies has improved the disclosure quality particularly the accuracy of earnings forecasts. Also, the independence and international competency, quality of external audit, the board size and the frequency of meeting are important factors for the implementation of IFRS in France. The study however did not place emphasis on financial reporting quality attributes such as reliability, comparability, and timeliness as well as other enforcement factors like culture, foreign financial markets and institutional factors.

Ebrahim (2014) conducted a thorough review of IFRS compliance and audit quality of financial statements using income tax accounting in Egypt. This study sample 118 Egyptian companies listed in Egyptian stock exchange and their financial statements for the year 2007 which happen to be the year IAS 12 was implemented in Egypt. The 118 companies selected were divided into 14 different industry sectors. The study also tested the effect of independent audit quality on both recognition of deferred tax and disclosures in the financial statements. Regression analysis was employed to analyze the effect of audit quality on compliance. The study found out that companies audited by independent auditors with international affiliation are more likely to obey the recognition and disclosure requirements of the adopted international accounting standards. The result for the first year shows a low level of compliance with provisions of income tax accounting in the year 2007 which was the first year of adoption. This study, however, did not examine the effect of corporate governance.

Gao and Sidhu (2018) investigated the impact of mandatory international financial reporting standards adoption on investment efficiency: Standards, enforcement, and reporting incentives. With a sample consists of 20,396 firm-year observations, from 5,438 unique mandatory adoption firms, and a benchmark sample of 62,328 firm-year observations from 13,328 non-adoption firms. The study revealed that the probability of under-investment in capital expenditure declines for firms from 23 countries requiring mandatory adoption of IFRS relative to firms from countries that do not have such requirements; meanwhile the probability of over-investment remains unchanged. The real effect becomes smaller when we control for concurrent changes to the enforcement of financial reporting along with the introduction of IFRS in some countries, suggesting that the switch in standards is only one of the drivers for the observed benefits. The study also revealed that after mandatory IFRS adopt ion, capital investment becomes more value-relevant, less sensitive to the availability of free cash flows, and more responsive to growth opportunities.

Atoyebi and Simon (2018) analyzed the impact of International Financial Reporting Standards (IFRSs) adoption on financial reporting practice in the Nigerian banking sector. Secondary data were employed in this study and data were gleaned from the annual reports of fourteen Nigerian listed banks. One hypothesis was developed and tested at five (5) per cent level of significance. Findings revealed that the quantitative differences in the financial reports prepared under NGAAP and IAS/IFRS are statistically significant. The study therefore concludes that IFRS have impacted on financial reporting in the Nigerian Banking sector.

Elosiuba and Okoye (2018) examined the effects of international financial reporting standards on corporate performance of selected banks listed on Nigeria Stock Exchange. Eight (8) out of the fourteen (14) quoted banks were selected for the study. The four indices of performance employed in the study are profitability using the return on equity, liquidity using total deposit to total loan, loan grants and then market value measured by price earnings ratio for the period (2011 and 2012). 2011 represented GAAP era while 2012 stands for IFRS adoption. A comparability index for the banks was computed using the Excel spread sheet for each of the banks on each variable. Then the One Sample Test was employed for the analyses. The mean was used to answer the research question while the t-statistics tested the hypotheses. The results showed that mean values for profitability, liquidity and market value are greater in the GAAP era (2011) than in the IFRS period (2012), while loan grant was higher for the IFRS period (2012). The t-test indicated the fact that none of the variables had significant effect. Thus, the study concluded that IFRS adopted does not have significant effect on bank performance reported in 2011 and 2012. The use of IFRS for all firms, as well as incorporation of IFRS guideline in professional training are recommended by this study.

Odoemelam et al. (2019) investigated the effect of international financial reporting standards (IFRS) adoption on the financial reporting quality of listed manufacturing firms in Nigeria. The study adopted a descriptive survey design, while the population of the study comprises all listed manufacturing firms in Nigeria. A sample size of 250 respondents consisting of 5 accountants selected from each firm of 50 firms in Port Harcourt. The sample size was selected using stratified random sampling techniques, with the respective firm as the strata. From each stratum, 5 accountants were sampled using a systematic random sampling technique. The sample size represents 5% of the target population for the study. Data obtained from the study were analyzed using descriptive mean and standard deviation, while the hypothesis was tested using regression analysis. The result revealed that there is a positive and significant effect of the adoption of international financial reporting standards (IFRS) on the financial reporting quality of listed manufacturing firms in Nigeria. This is because all the indicators of international financial reporting standards (IFRS) and Financial Reporting Quality (FRQ) revealed a high extent of considerable impact both when they are considered as single (univariate) and bivariate variables

Onipe et al. (2015) examined the effects of the adoption of the International Financial Reporting Standards on the financial statement’s quality of banks. A regression model was employed using pooled data and fitted with dependent variables. The results show that international financial reporting standards (IFRS) adoption has positively impacted some variables in the financial statement of banks, for example, profitability and growth potential. The study therefore concludes that the banks experienced a quality financial statement under the period of adoption of international financial reporting standard than any other period. Financial statement of banks was qualitative than ever.

Saidu and Dauda (2014) reviewed the assessment of compliance with IFRS framework at first time adoption by quoted banks in Nigeria. The study used ex-post facto and survey research design that involve sourcing data from structured questionnaire and audited financial statements of sampled banks. Multiple regression and chi square test were used in measuring the effects of factors responsible for compliance and difficulties associated with it. The study concluded that Nigerian banking industry complied semi-strongly with the requirements of IFRS framework but faced with challenges of proper understanding and in-depth knowledge of IFRS framework particularly from the preparers of financial statements sighting globalization and response to users’ needs as factors discouraging compliance with IFRS framework. However, the study focusses more on IFRS 1 which deals with first time adoption of IFRS at the expense of other standards.

In Ghana, Boateng et al. (2014) employed the survey research method to assess eighteen (18) professional Accountants in order to measure the benefits and challenges of IFRS to Ghana. The study revealed that IFRS improved the access of local companies to international markets. It was also observed that the local firms in Ghana gained more credibility, transparency, acceptance and consolidation following IFRS adoption. Adopting the survey research design, Acquaye (2015) investigated 145 personnel of 29 public companies in Ghana towards ascertaining the compliance attitude of Ghana public listed companies to IFRS disclosure requirements. Results of the regression and correlation analyses carried out showed that a high level of compliance by Ghanaian listed companies with IFRS exists. Appiah et al. (2015) employed the unweight disclosure index to conduct an empirical study on 31 public listed companies in Ghana for the years 2008–2012. Result of their regression analysis showed that variations in the level of the firms ‘compliance with IFRS in Ghana exist. Zakari (2017) investigated into whether the adoption of IFRS in the Nigerian Oil and Gas sector; leads to significant financial reporting improvement in terms of value addition and quality. Using the T-test (paired) statistical tool, outcome of ratio analysis conducted on extracts from the pre and post IFRS Financial Statements of four (4) public companies in the Oil and Gas sector for years 2007 – 2016 showed that IFRS was more attractive and promising to long term lenders than the defunct Nigerian GAAP

Abedana et al. (2016) just like Agyei-Mensah (2013) adopted the disclosure index approach that is based on IAS 12 to examine the financial reports of twenty-two (22) companies listed in Ghana Stock Exchange for the years 2006 – 2008 to ascertain the disclosure quality levels of their financial reports before and after the adoption of IFRS. Relevant analyses were carried out using Pearson‘s correlation and it was observed that the disclosure quality level of annual reports and accounts of listed firms in Ghana seem to be high and has improved, portraying a significant positive correlation between the disclosure quality (based on the qualitative characteristics of relevance, understand ability, comparability and faithful presentation) of listed firms following the adoption of IFRS.

Wulandari and Rahaman (2004) assert that having accounting standards in place, does not guarantee effective regulation mechanism; institutional infrastructures for the application and enforcement of these standards are also vital in providing the standards with the aptitude to make financial information relevant for all capital markets. Strong institutional infrastructures and sound enforcement apparatus will enable investors to develop confidence that financial reports reveal a true and fair view of the firm’s fundamentals. In addition, enforcement mechanisms are necessary ingredients in the application of IFRS, unless consistently and rigorously enforced, so that perceived benefits of the new set of standards can be reaped (NASB, 2010).

Paglietti (2009) reveals that countries with sound enforcement changes during IFRS introduction, tended to benefit more from increased liquidity than countries with no changes in enforcement mechanisms. The study confirms that countries that made changes in the enforcement mechanism without even moving to IFRS also experienced increased liquidity benefits than countries that did not make changes in the enforcement mechanism during the IFRS adoption. Therefore, changes in enforcement mechanism play a vital role in attaining liquidity benefits before and after IFRS introduction. Hence, achievement of IFRS targeted objectives can be concurrently accomplished with proper and sound enforcement mechanism in place.

Pawsey (2008) explored how effective is enforcement mechanism in realising the benefit of IFRS, using firm-month observations of 391,462 firms from 51 countries in Europe and Australia that mandatorily apply IFRS, with US and Canadian firms used as control sample between recent financial year. The study reveals lesser error and low dispersion for users of IFRS as well as firms in jurisdictions with strong enforcement mechanism. In this vein, robust institutional infrastructures and strong monitoring mechanism were found to be an important factor in improving reporting quality and reducing income smoothing for both domestic and cross border listed firms in the UK after the adoption of IFRS (Jermakowicz, & Tomaszewski, 2006). Having Accounting Standards in place do not guarantee effective regulation mechanism; institutional infrastructures for enforcement and monitoring the application of these standards are also vital in providing the standards with the ability to make financial information relevant for all capital markets (Wulandari & Rahaman, 2004). Paglietti (2009) equally reveals that, countries with sound enforcement changes concurrent with IFRS introduction seemed to benefit more from increased liquidity than countries with no changes in enforcement mechanisms.

Summary of Literature Review

From the empirical review of international scholars, Nicolae, Albu and Hoffman (2021) concluded that the operationalization of Financial Reporting Enforcement System in Romania has been more superficial than substantive driven by impression management desires than pursuit of fundamental and systemic change. In the same vein, Johansson and Giljam (2014) found out that national enforcement bodies differ in several areas ranging from structures, resources, legal authority, examination approach, results of examination, and sanctions. Leonard and Jan (2013) indicated that comparability decreases following IFRS adoption and stressed that concurrent enforcement changes seem to be limited to second order capital market effects documented by prior research. Silva, Jorge and Rodrigues (2021) propose analysis of the practices of the enforcers whereas Samarasekara, Chang and Tarca (2012) concluded that IFRS has the potential to provide more transparent and comparable information which in turn will influence capital market efficiency and economic growth.

From the perspective of institutional settings, legal settings and IFRS adoption, Brown, Preiato and Tarca (2014) concluded that the proxies are less effective because they rarely concentrate on factors that solely influence how accounting standards and compliance are promoted through activities of external audits and independent enforcement bodies. In the same context, Preiato, Brown and Tarca (2015) indicated that accounting enforcement can be more important in securing favorable economic outcomes than has been previously realized. Also, Ball, Robin and Wu (2003) argued that beyond quality accounting standards, remunerations of auditors and preparers, enforcement mechanism and ownership structure affect the quality of financial reporting whereas Andre, Filip and Paugam (2015) discovered that differences in institutional and legal settings across countries in Europe disappears after IFRS adoption. Verdi (2006) revealed that the relationship between financial reporting system and investment efficiency was stronger for firms with low quality information environments while Herath and Albarqi (2017) suggested that financial reporting quality depends on some important features which are reliability, comparability, understandability, timeliness, and faithful representation. Ebrahim (2014) study found out that companies audited by independent auditors with international affiliation are more likely to obey the recognition and disclosure requirements of the adopted international accounting standards. Also, Rohou, Douagi and Hussainey (2015) concluded that mandatory adoption of IFRS by French companies has improved the disclosure quality particularly the accuracy of earnings forecasts.

Gap in Knowledge

The overview of literature reflects that there are shortage of studies analyzing enforcement practices in Nigeria. However, most empirical findings in Nigeria discusses IFRS adoption, accounting quality and performance. In Nigeria and Ghana, most of the empirical findings revealed that IFRS will enhance the performance of firm’s organization towards consistency and integrity to accounting standards and practices. On the adoption of IFRS, most of the study concludes that there is need for strong institution that will stand as backbone for proper enforcement of the accounting rules and regulations. However, the empirical findings from Nigeria and Ghana dwelled more on the impact of IFRS adoption on accounting quality, comparability, and company’s performance but less attention were placed on the enforcement of IFRS to promote adequate compliance. Therefore, this study seeks to close the gap by examining the effectiveness of IFRS enforcement in Nigeria.

REFERENCES

- Abedana, V., Omane-Antwi, K., & Oppong, M. (2016). Adoption of IFRS/IAS in Ghana: Impact on the quality of corporate financial reporting and related corporate tax burden. Abedana, VN, Omane-Antwi, KB and Oppong M. (2016), Adoption of IFRS/IAS in Ghana: Impact on the Quality of Corporate Financial Reporting and Related Corporate Tax Burden, Research Journal of Finance and Accounting, 7(8), 10-25

- Acquaye, S. (2015). The Adoption of International Financial Reporting Standard (IFRS) by Ghanaian companies the level of compliance with reference to the preparation of financial statement. Kwame Nkrumah University of Science and Technology.

- Agyei-Mensah, B. K. (2013). Adoption of international financial reporting standards (IFRS) in Ghana and the quality of financial statement disclosures. Macro think Institute, International Journal of Accounting and Financial Reporting, ISSN, 2162-3082

- Al-Hussaini, A., Al-Shammari, B., & Al-Sultan, W. (2008). Development of Enforcement Mechanisms Following Adoption of International Accounting Standards in the Gulf Co-Operation Council Member States. Journal of International Business Strategy, 8(3)

- Appiah, K. O., Awunyo-Vitor, D., Mireku, K., & Ahiagbah, C. (2016). Compliance with international financial reporting standards: the case of listed firms in Ghana. Journal of Financial Reporting and Accounting.

- André, P., Filip, A. and Paugam, L. (2015), “The effect of mandatory IFRS adoption on conditional conservatism in Europe”, Journal of Business Finance and Accounting, Vol. 42 No. 3-4, pp. 482-514

- Atoyebi, T. A., & Simon, A. J. (2018). The impact of International Financial Reporting Standards (IFRSs) adoption on financial reporting practice in the Nigerian banking sector.

- Ball, R. (2006). International Financial Reporting Standards (IFRS): Pros and cons for investors. Accounting and business research, 36(sup1), 5-27

- Ball, R., Robin, A. and Wu, J. 2003, ‘Incentives versus standards: properties of accounting income in four East Asian countries.’ Journal of Accounting and Economics, vol. 36, no. 1-3, pp. 235-270

- Boateng, A. A., Arhin, A. B., & Afful, V. (2014). International Financial Reporting Standard’s (IFRS) adoption in Ghana: Rationale, benefits and challenges. Journal of Advocacy, Research and Education, 1(1), 26-32

- Brown, P., Preiato, J., & Tarca, A. (2014). Measuring country differences in enforcement of accounting standards: An audit and enforcement proxy. Journal of Business Finance & Accounting, 41(1-2), 1-52

- Coffee Jr, J. C. (2006). Reforming the securities class action: An essay on deterrence and its implementation. Colum. L. Rev., 106, 1534

- Deephouse, D. L., Bundy, J., Tost, L. P., & Suchman, M. C. (2017). Organizational legitimacy: Six key questions. The SAGE handbook of organizational institutionalism, 4(2), 27-54

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American sociological review, 147-160

- Dillard, J. F., Rigsby, J. T., & Goodman, C. (2004). The making and remaking of organization context: duality and the institutionalization process. Accounting, Auditing & Accountability Journal.

- Ebrahim, A. (2014). IFRS compliance and audit quality in developing countries: The case of income tax accounting in Egypt. Journal of International Business Research, 13(2), 19.

- Eisenhardt, K. M. (1989). Agency theory: An assessment and review. Academy of Management Review, 14(1), 57–74

- Erin, O. A., & Oduwole, F. (2018). An investigative analysis into the impact of International Financial Reporting Standards (IFRS) on the profitability ratios of Nigerian banks. Euro Economica, 38(1)

- Elosiuba, J. N., & Okoye, E. I. (2018). Effects of International Financial Reporting Standards on Corporate Performance of Selected Banks Listed on Nigeria Stock Exchange.

- Gao, R., & Sidhu, B. K. (2018). The impact of mandatory international financial reporting standards adoption on investment efficiency: Standards, enforcement, and reporting incentives. Abacus, 54(3), 277-318

- Garud, R., Hardy, C., & Maguire, S. (2007). Institutional entrepreneurship as embedded agency: An introduction to the special issue. Organization studies, 28(7), 957-969

- Gelter, M., & Eroglu, Z. G. K. (2014). Whose Trojan Horse-The Dynamics of Resistance against IFRS. U. Pa. J. Int’l L., 36, 89

- Greenwood, R., Oliver, C., Lawrence, T. B., & Meyer, R. E. (Eds.). (2017). The Sage handbook of organizational institutionalism. Sage.

- Hannan, M. T., & Carroll, G. R. (1995). Theory building and cheap talk about legitimation: Reply to Baum and Powell. American Sociological Review, 60(4), 539-544.

- Herath, S. K., & Albarqi, N. (2017). Financial reporting quality: A literature review. International Journal of Business Management and Commerce, 2(2), 1-14

- Hoffman, A. J. (1999). Institutional evolution and change: Environmentalism and the US chemical industry. Academy of management journal, 42(4), 351-371

- Holthausen, R. W. (2003). Testing the relative power of accounting standards versus incentives and other institutional features to influence the outcome of financial reporting in an international setting. Journal of Accounting and Economics, 36(1-3), 271-283

- Jensen, M. C., & Meckling, W. H. (2019). Theory of the firm: Managerial behavior, agency costs and ownership structure. In Corporate Governance (pp. 77-132). Gower

- Jermakowicz, E. K., & Gornik-Tomaszewski, S. (2006). Implementing IFRS from the perspective of EU publicly traded companies. Journal of International Accounting, Auditing and Taxation, 15(2), 170-196

- Johansson, F., & Giljam, P. (2014). Enforcement of IFRS in Europe-A study identifying practical differences between countries.

- Kettl, D. F. (2000). The transformation of governance: Globalization, devolution, and the role of government. Public administration review, 60(6), 488-497

- Kurauone, O., Kong, Y., Sun, H., Muzamhindo, S., Famba, T., & Taghizadeh-Hesary, F. (2021). The effects of International Financial Reporting Standards, auditing and legal enforcement on tax evasion: Evidence from 37 African countries. Global Finance Journal, 49, 100561

- Leonard, L., & Jan, S. (2012). IFRS enforcement and their role for accounting quality and comparability (Doctoral dissertation, MS thesis, Stockholm School of Economics).

- Levine, M. E., & Forrence, J. L. (1990). Regulatory capture, public interest, and the public agenda: Toward a synthesis. JL Econ & Org., 6, 167

- Midiastuty, P. P. (2003). Mas’ ud Machfoedz. 2003. Analisis Hubungan Mekanisme Corporate Governance dan Indikasi Manajemen Laba, 176-199.

- Nicolae Albu, C., Albu, N., & Hoffmann, S. (2021). The Westernisation of a financial reporting enforcement system in an emerging economy. Accounting and Business Research, 51(3), 271-297

- Ocheni, S. I. (2015). Perceived challenges of international financial reporting standards (IFRS) adoption in Nigeria. Indian Journal of Commerce and Management Studies, 6(1), 7-11.

- Odoemelam, N., Okafor, R. G., & Ofoegbu, N. G. (2019). Effect of international financial reporting standard (IFRS) adoption on earnings value relevance of quoted Nigerian firms. Cogent Business & Management, 6(1), 1643520

- Onipe, A.Y., Musa, J.Y. and Isah, S.D. (2015). International Financial Reporting Standards’ adoption and financial statement effects: evidence from listed deposits money banks in Nigeria. Research Journal of Finance and Accounting, 6(12), 107-123

- Owolabi, A., & Iyoha, F. O. (2012). Adopting international financial reporting standards (IFRS) in Africa: Benefits, prospects and challenges. African Journal of Accounting, Auditing and Finance, 1(1), 77-86

- Obazee J. O. 2007, Current Convergence Efforts in Accounting Standard Setting and Financial Reporting: Lagos, Nigerian Accounting Standing Board. January 31.

- Ogiedu,K.O. 2011 , International Financial Reporting Standards Adoption: A Challenge of Definition and Implementation, A Seminar paper presented in the PhD Accounting ,Department of Accounting ,University of Benin.

- Odia, J.O., & Ogiedu, K.O (2013). IFRS Adoption, Issues, challenges and lessons for Nigeria and other Adopters. Mediterranean Journal of Social Sciences, 4(3), 389-399.

- Pache, A. C., & Santos, F. (2010). When worlds collide: The internal dynamics of organizational responses to conflicting institutional demands. Academy of management review, 35(3), 455-476

- Paglietti, P. (2009). Investigating the Effects of the EU Mandatory Adoption of IFRS on Accounting Quality: Evidence from Italy International Journal of Business and Management, 4(12), P3

- Pawsey, N. L. (2008). Australian preparer perceptions towards the quality and complexity of IFRS. La Trobe University.

- Preiato, J., Brown, P., & Tarca, A. (2015). A comparison of between‐country measures of legal setting and enforcement of accounting standards. Journal of Business Finance & Accounting, 42(1-2), 1-50

- Ramanna, K. (2013). Network Effects in Countries’ Adoption of IFRS/Karthik Ramanna, Ewa Sletten. Harvard Business School. –2013.–48 pp

- Ridder, H. G., Bruns, H. J., & Spier, F. (2005). Analysis of public management change processes: the case of local government accounting reforms in Germany. Public administration, 83(2), 443-471

- Rouhou, N. C., Douagi, W. B. M., & Hussainey, K. (2015). The effect of IFRS enforcement factors on analysts’ earnings forecasts accuracy. Corporate Ownership and Control, 13(1), 266-282

- Saidu, S., & Dauda, U. (2014). An assessment of compliance with IFRS framework at first-time adoption by the quoted banks in Nigeria. Journal of Finance and Accounting, 2(3), 64-73

- Samarasekera, N., Chang, M., & Tarca, A. (2012). IFRS and accounting quality: The impact of enforcement. Available at SSRN 2183061

- Silva, A., Jorge, S., & Rodrigues, L. L. (2021). Enforcement and accounting quality in the context of IFRS: is there a gap in the literature? International Journal of Accounting & Information Management, 29(3), 345-367

- Uzma, S. H. (2016). Cost-benefit analysis of IFRS adoption: developed and emerging countries. Journal of Financial Reporting and Accounting.

- Verdi, R. S. (2006). Financial reporting quality and investment efficiency. Available at SSRN 930922

- Wulandari, E. R., & Rahman, A. R. (2004). A cross-country study on the quality, acceptability, and enforceability of accounting standards and the value relevance of accounting earnings. Unpublished Working Paper. Nanyang Technological University, Singapore.

- Zakari, M. (2017), ―International Financial Reporting Standard (IFRS) Adoption and Its Impact on Financial Reporting: Evidence from Listed Nigeria Oil and Gas Companies, Asian Journal of Finance & Accounting, Vol. 9 No. 1, pp. 464 – 474

METHODOLOGY

Research Design

Research design entails overall strategy used to integrate different component of the study in a logical and coherent way so that the study will effectively address the research problem which include examining the issues affecting FRCN enforcement activities and examining the effectiveness of IFRS enforcement in Nigeria. This study used a combination of descriptive research design and correlational research design to describe and analyze the challenges of FRCN enforcement activities in Nigeria as well as perception of accountants and auditors regarding effectiveness of IFRS enforcement. Online survey method was used to gather data through questionnaires.

Population of the Study

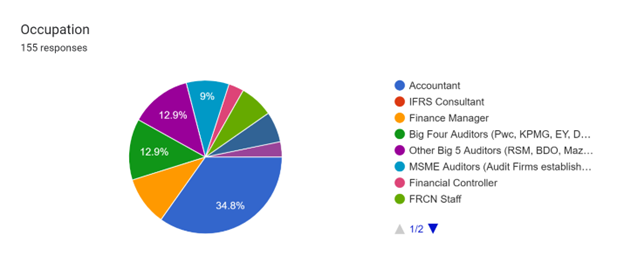

The population of the study were made up of 155 stakeholders within the financial reporting space in Nigeria. These includes, accountants, auditors, IFRS consultants, FRCN staffs, and Investors within the financial reporting chain in Nigeria.

Sample Size and Sampling Technique.

Snowball sampling technique was used in this study. Snowball sampling or chain-referral sampling is a non-probability sampling technique in which the samples have traits that are rare to find. This is a sampling technique, in which existing subjects provide referrals to recruit samples required for a research study. This sampling technique was used because the research requires respondents that have knowledge and expertise of financial reporting and IFRS enforcement so that their responses will provide information useful for the research study. Questionnaires were administered to respondents based on referrals obtained until reasonable responses were gotten that form the representative of the population. 155 responses were gotten from the referrals provided and this represent the sample size used.

Sources of Data

Data for this study were predominantly primary data. These were obtained through questionnaires. Questions were developed by the researcher on challenges of IFRS in Nigeria, perception of accountants and auditors as regards IFRS enforcement in Nigeria and differences in perception between accountants and auditors concerning enforcement of IFRS in Nigeria. Semi-structured interview was also conducted for three FRCN staff and three stakeholders namely accountants, auditors, and investors to obtain information on challenges of IFRS enforcement in Nigeria.

Data Collection Instruments

Questionnaires was used to collect data from respondents. This consist of questions that were designed using Likert scale to obtain responses from respondents. 5-point rating scale was employed to capture respondents’ responses. This consist of Strongly Agree, Agree, Neutral, Disagree, and Strongly Disagree.

Validity and Reliability of the Instrument

Concurrent validity is a type of evidence that can be gathered to defend the use of a test for predicting other outcomes (Taherdoost, 2016). It refers to the extent to which the results of a particular test, or measurement, correspond to those of a previously established measurement for the same construct. In brief, concurrent validity assesses the operationalization’s ability to distinguish between groups that it should theoretically be able to distinguish between. This study uses concurrent criterion validity to determine relationship between perception of accountants and auditors as well as differences in perception.

Reliability deals with the extent to which a measurement of a phenomenon provides stable and consistent result (Carmines and Zeller, 1979). Reliability is also concerned with repeatability. For example, a scale or test is said to be reliable if repeat measurement made by it under constant conditions will give the same result (Moser and Kalton, 1989). For this study, Cronbach Alpha Coefficient measure was used as it is the most appropriate technique when using Likert scales.

Method of Data Analysis

The study combined both descriptive and inferential statistics to analyze data. T-test analysis technique, mean, median, standard deviation, frequency and percentages were employed to analyze the challenges, perception, and the difference in perception between auditors and accountants about effectiveness of IFRS enforcement in Nigeria. Also, qualitative analysis technique was employed to examine challenges of IFRS enforcement in Nigeria through the semi-structured interview conducted.

REFERENCES

- Carmines, E. G. & Zeller, R. A. 1979. Reliability and Validity Assessment, Newbury Park, CA, SAGE

- Hudelson PM. Qualitative Research for Public Health Programmes. WHO/MNH/PSF/94.3. Geneva 1994. http://libdoc.who.int/hq/1994/WHO MNH PSF 94.3.pdf

- Mays N, Pope C. Assessing quality in qualitative research. BMJ. 2000 Jan 1;320(7226):50-2.