The Influence of Financial Risk Hedging Practices on the Performance and Resilience of Companies Listed on the Zimbabwean Stock Exchange (ZSE).

- Brian Basvi

- 761-774

- Jun 13, 2024

- Finance

The Influence of Financial Risk Hedging Practices on the Performance and Resilience of Companies Listed on the Zimbabwean Stock Exchange (ZSE).

Brian Basvi

University of Zimbabwe

DOI: https://doi.org/10.51244/IJRSI.2024.1105048

Received: 15 May 2024; Accepted: 27 May 2024; Published: 13 June 2024

ABSTRACT

Businesses are more vulnerable to a range of hazards in the dynamic and demanding business environment, particularly due to unfavourable changes in the macroeconomic landscape and heightened competition. Businesses that operate in such an unstable environment are primarily susceptible to financial risk. Many businesses in Zimbabwe are currently losing money as a result of improper hedging and expensive procedures used to reduce these risks. Massive companies in Zimbabwe recorded losses of 25.7 billion USD and 262.3 million USD respectively in 2023. These losses were attributed to improper hedging methods. Therefore, the purpose of this study was to look into how financial risk hedging strategies affected ZSE firms’ performance. The research had four main goals: to determine how foreign exchange hedging practices affect listed firms’ performance at the ZSE; to investigate the impact of commodity price hedging practices; to assess the impact of interest rate hedging practices; and to investigate the impact of equity risk hedging practices. The quantitative data that was gathered for the study was analysed using both descriptive and inferential statistics. The average distribution and variance were measured in the descriptive analysis by the study using the mean and standard deviation respectively. A multiple regression model was used in the inferential statistics. Using a regression model, the researcher was able to examine how different performance was depending on whether foreign exchange, interest rate, and commodity price risks were hedged using futures, forwards, options, or swaps. For the last five years, from 2019 to 2023, information on the return on invested capital (ROIC) and return on assets (ROA) was gathered from the company’s financial statements. A slightly high degree of influence was indicated by the mean score of the study variables which included equity hedging practices (mean=3.9369), central bank controls (mean=3.9922), commodity pricing risk hedging practices (mean=3.8693), interest rate risk hedging practices (mean=3.6406), and foreign exchange hedging practices (mean=3.6311). The study found a favourable correlation between listed firms’ performance, the moderator (central bank controls), and their hedging activities. When the moderator variable (central bank controls) was included in the model regress, the study’s R2 increased from 0.391 to 0.617.

Key Words: Financial Risk Hedging, foreign exchange, interest rates, commodity price risk, futures, swaps, forward contracts and Firm’s Performance.

INTRODUCTION

Both diversifiable and non-diversifiable risk are referred to as total financial risk. Non-diversifiable risk cannot be eradicated, whereas diversifiable risk can be spread out and removed. Insurance, credit risk, compliance, liquidity risk, operational risk, and market risk are a few examples of prevalent financial risk types. The four components that determine market risk are equities risk, interest rate risk, currency risk, and commodity risk. Market risk is the risk that results from fluctuation in market prices and was the subject of this study (Sharpe, 2018). In essence, equity risk is the financial risk associated with owning equity in a specific investment; interest rate risk is the risk that bond traders face due to interest rate volatility; commodity risk is the risk associated with commodity pricing volatility; and currency risk/foreign exchange risk is the risk associated with currency rate volatility (Wachowicz 2020).In order to lessen the impact of these risks on company expansion, a growing number of companies are implementing and formalizing financial risk management techniques. As a result, one of the most crucial business tactics for companies nowadays is financial risk management. When compared to companies that implement financial risk management strategies, those that do not are likely to see poor growth trends. A variety of financial risk management techniques, such as portfolio diversification for diversifiable risks and hedging measures for non-diversifiable risks, are available to help lower financial risks (Sharpe and others, 2019).

Hedging is a popular risk-reduction tactic employed by businesses. Hedging lessens the chance of future price fluctuations, which, if poorly managed, could have a negative impact on a company (Horne, 2020). A company or individual uses hedging to guard against a change in pricing that might otherwise have a detrimental impact on profitability (Brigham, 2019). It offers highly liquid and reasonably priced positions that are comparable to those attained through diversified stock portfolios (Bailey 2013). A company can accomplish its hedging objectives by using a variety of financial instruments, such as forward agreements, futures contracts, options, or swaps. among a survey of non-financial companies across countries, Bartram et al. (2011) discovered that the usage of these instruments decreased overall company risk and was more common among companies with higher exposure to interest rate, currency rate, and commodity price risks. According to Bodnaretal (2008), 83% of hedging companies in the US utilize forward agreements, futures contracts, options, or swaps to manage foreign exchange risk, 76% use them to manage interest rate risk, and 56% manage commodity price risk. Thus, it follows that hedging interest rate, foreign exchange, and commodity price risks frequently involves the use of forward agreements, futures contracts, options, and swaps.

However, the use of derivatives as a tool for risk mitigation is uncommon in developing nations; Zimbabwe, South Africa and India, for example, only use derivatives on short-term contracts like futures, forwards, and swaps (Sakar, 2022). An example of hedging in the mining sector in Zimbabwe is when firms in the sector that would have otherwise experienced a downturn are stabilized through the use of interest rate swaps and fixed forward exchange rates as hedging mechanisms. These firms face risk due to unsuccessful exploration, input price volatility, and production costs (Minnit, 2017). Blaaw (2019) provided evidence to support this claim by pointing to the robust capital market structures of third-world economies, such as Zimbabwe, and the use of derivatives to reduce risk, which was absent from Nigeria’s capital market, as the reasons for these economies’ resilience during the 2008 global financial crisis. The researcher went on to say that inadequate risk management might cause enormous losses and almost bring down entire institutions. Although sufficient mechanisms have been established in Zimbabwe to support interest rate risk hedging, particularly among commercial banks, there are no data available to show the level of hedging done by Zimbabwean businesses (Kothari, 2017).

The main cause of financial risk in Zimbabwe is the inflation problem. One of the greatest periods of inflation Zimbabwe has had since independence has recently occurred (CBK, 2010). During this time, many projects came to a standstill and commodity prices, like oil, saw an increase. At the height of the global financial crisis, which occurred between 2007 and 2009, economic cycles were notably impacted by macroeconomic conditions. Additional obstacles might be linked to this event. Business cycles frequently have an impact on the cash flows of different economic units and the performance of loan portfolios (Yiping, 2018). Many hedging strategies are employed by Zimbabwean businesses to lessen the impact of these risks. For instance, Wanja (2021) discovered that Zimbabwean businesses employ forward contracts, swaps, futures, and options as hedging strategies against interest rate risk. However, market trading platform technology and institutional restrictions hinder Zimbabwean businesses (Otsyula, 2022). It’s unclear how hedging affects a company’s success in Zimbabwe.

It would be wise to include both financial and non-financial companies from every area of Zimbabwe’s economy in order to fully comprehend the impact of hedging on the performance of Zimbabwean businesses. This is due to the fact that, among other things, the industry and firm size affect how well hedging affects a firm’s performance (Bodnaretal., 2018). Businesses from both financial and non-financial sectors are comprehensively presented by companies registered on the Zimbabwe Stock Exchange (ZSE). The businesses come from several economic sectors as well. There are 63 companies listed on the Zimbabwe Stock Exchange. The businesses are divided into ten groups: banking, insurance, investment, agriculture, commercial and services, telecommunication and technology, automobiles and accessories, manufacturing and related businesses, construction and related businesses, and energy. The companies are divided into the following ten groups: banking, insurance, investment, agriculture, commercial and services, telecommunication and technology, automobiles and accessories, manufacturing and allied, construction and allied, and energy and petroleum (Zimbabwe Stock Exchange, 2023).

According to the aforementioned research, third-world economies prefer to use insurance to reduce risk rather than heavily utilizing futures, forwards, and swaps as a tool for risk reduction, in contrast to affluent nations that frequently use derivative markets for this purpose (Murungi, et al., 2020). As the only nation in Africa to employ derivatives to hedge its gold production, South Africa exclusively uses them for short-term contracts. According to Borse Group (2014), the usage of derivatives allowed for the elimination of uncertainty and the reduction of market risk, which may account for the developed economies’ apparent resilience in terms of the composition of their capital markets. Zimbabwe’s financial markets, like those of other developing nations, are underdeveloped and shallow. The political climate, participant attitudes, managerial scepticism, financial infrastructure and international competition all impede Zimbabwe’s use of hedging mechanisms like derivatives (Wanjau, 2019). Zimbabwean businesses thus have difficulty using hedging tools against the required market microstructure. Pricing and valuing hedging instruments is another challenge faced by businesses.

Businesses must carefully weigh the expenses of hedging against the consequences of not hedging because hedging has a cost. Only in situations where precise risk assessment and forecasting are feasible can this occur. Hedging will out to be an inefficient business strategy if the anticipated risk does not materialize (Giddy, 2021). Depending on the strategies they employ to protect themselves from risk, Zimbabwean businesses have had varying degrees of success in recent years. Centum Zimbabwe has announced a 900 thousand USD profit, which it attributes to appropriate investment from its subsidiaries and an increase in the value of its properties. Zimbabwe Airways, which has lost a Significant amount due to swings in fuel prices, is also in danger of failing. Due to excessive operating costs and bad management choices, the OK chain of supermarkets reported a 262.3 million ZWL loss during the same period last year, down from a profit of 106.9 million ZWL. Research on the hedging strategies used by Zimbabwean companies, such as Njuguna et al. (2018), revealed that hedging using options and forwards had a favourable impact on the expansion of the microfinance industry. According to Mugenda et al. (2019), there are no financial derivatives used in risk hedging operations, and management believed that risk management in Zimbabwean businesses could be addressed by other tools, such as insurance. Based on this, the study set out to determine the effect that financial risk hedging practices had on the ZSE-listed companies’ performance. Businesses are nevertheless susceptible to a variety of hazards in the ever-changing and demanding business environment, particularly due to unfavourable changes in the macroeconomic climate and heightened competition. Businesses that operate in such an unstable environment are primarily susceptible to financial risk. The study’s precise goals were to look into how financial hedging activities affected the performance of companies listed on the ZSE. To assess the effect of foreign exchange hedging practices on the performance of firms listed in the ZSE. To examine the influence of commodity price hedging practices on the performance of firms listed in the ZSE. To evaluate the effect interest rate hedging practices on the performance of firms listed in the ZSE. Lastly to examine the effect of equity hedging practices on the performance of firms listed in the ZSE.

LITERATURE REVIEW

The Concept of Financial Hedging and Firm Performance

Interest rate parity theory is predicated on the idea that the volatility of the nominal interest rate is explained by differences in interest rates between a nation and its trading partners. The difference in interest rates between foreign and local countries is known as interest rate parity. When there is no financial activity of buying and selling currency in the financial market, the parity condition states that interest rate differentials in two different currencies will be reflected in the premium or discount for the forward exchange rate on the foreign currency (Dash, 2017). According to the liquidity preference theory, economic units prefer liquidity to investing. By using this hypothesis, the premium provided by forward rates over anticipated future spot rates was explained. In exchange for the usage of limited liquid resources, this premium is paid. The demand for liquidity can be explained by the necessity for economic units to maintain specific levels of liquid assets in order to make purchases of goods and services, as well as the unpredictability of these near-term future expenses.

The value of options in the market is determined by option pricing theory. The Black-Scholes model and the Binomial model make up the theory. Because Black-Scholes is intended to value options that can only be exercised at maturity and underlying assets that do, it is the most often used option pricing theory for European options.

Due to its ability to value options that may only be exercised at maturity and underlying assets that do not generate dividends, Black-Scholes is the most widely used option pricing theory for European options. But in the seZSE that it is meant to value options that can be exercised at any moment, independent of the amount of time before the underlying asset’s maturity, the binomial model is a popular option pricing theory for American options. The real interest rate plus the inflation rate added together equals the nominal rate, according to Fisher’s impact theory of interest rates. Fishers’ interest rate theory offers a justification for monetary policy that centres on controlling inflation in order to maintain interest rate levels and safeguard wealth’s buying power (Tymoigne, 2016). According to the study a nation’s economic inflation rate affects the interest rates that are charged on investments. While stabilization may lower the danger of default and allow for the achievement of return on investment, volatile conditions may result in losses.

Hedging offers the hedging firm a number of advantages, according to Judge (2021). Hedging, according to the author, lowers the likelihood that a company will experience financial distress, which in turn lowers the expected costs of financial distress; it lessens the risk placed on the company’s managers, employees, suppliers, and customers; it can control the conflict of interest between bondholders and shareholders, which lowers the agency costs of debt; and it makes it easier to finance investment projects with internal funds rather than relying on expensive external financing.

The effect of using exchange rate hedging on business value has been examined in a number of research. According to Allayannis (2021), there is a strong and positive correlation between the usage of currency derivatives and the effect of using exchange rate hedging on business value has been examined in a number of research. For a sample of American businesses, Weston (2021) verified the presence of a positive and substantial relationship between the use of currency derivatives and company value. The authors discovered a hedging premium of over 4.87%. The impact of commodity price hedging by American airline firms was examined in a study by Carter et al. (2006). The results indicated that hedging in the airline industry with regard to oil prices is positively correlated with firm value, and the hedging premium can exceed 5%. Because there is a strong correlation between the fuel price and investment prospects, the authors provided evidence that the biggest advantage of hedging in this industry would be the decrease in underinvestment costs within the sector. Additionally, the study demonstrated that businesses can thrive by implementing suitable hedging strategies in which the “intensity” of hedging is positively correlated with the value of the business. Otsyula (2014) looked into the difficulties commercial banks in Zimbabwe faced while using financial derivatives to hedge interest rate risk. According to the Central Bank of Zimbabwe’s definition of commercial banks, the study looked into five commercial banks: two large, one medium, and two tiny banks.

The financial institution policy and market trading platform technology are the primary obstacles to Zimbabwean commercial banks’ attempts to use derivatives as a hedging strategy against interest rate risk. Even though the Central Bank of Zimbabwe has the necessary tools at its disposal to use derivatives among other things to manage interest rate risk. The Central Bank of Zimbabwe has the necessary tools at its disposal to use financial derivatives to hedge interest rate risk among Zimbabwe’s commercial banks, but the banks’ trading platforms and financial institution norms have made this process more difficult.

According to Brodsky (2020), stock market players used options and futures in relation to their portfolio strategies. However, the researcher discovered that, in contrast to other financial derivatives like interest rates, stock index futures and options contributed to the positive expansion and liquidity of the underlying stock market. Despite concentrating on just two financial derivatives, the study does demonstrate a connection between corporate performance and stock hedging practices. Despite concentrating on just two financial derivatives, the study does demonstrate a connection between corporate performance and stock hedging practices. According to Pwc’s (2021) poll, managers saw equity prices as one of the most significant components of market risk. According to Gutierrez’s (2018) research, a country’s autonomy that is, its independence from both the political and economic spheres allows the central bank to intervene in the economy of that nation. The study notes that the central bank’s political independence allows it to withstand pressure from the government that might otherwise exacerbate fiscal repercussions like the “burden of debt” or even trigger an economic slowdown due to decreased tax revenues. Because of its economic independence, central banks are able to predict when a country’s money supply and demand will improve, compelling the government to balance the budget without creating new money a move that might have an endogenous impact on the nation’s economy. Goselin (2017) discovered no statistical evidence of a connection between the level of financial market development and central bank performance.

However, since the soundness and financial strength of private banks are both negatively correlated with inflation deviations, there is a similarity with Krause and Rioja’s (2016) finding that the strength of the private banking sector was positively correlated with meeting targets more consistently. Additionally, a mixed relationship between hedging and company performance has been found in reviewed studies. For example, research by Carter et al. (2006) demonstrates the beneficial impact of hedging on a firm’s performance. Conversely, studies by Naranjo (2010) demonstrate that hedging’s relationship to performance is dependent on the nation, industry, and corporate governance of the business.

STUDY DESIGN AND METHODOLOGY

The blueprint for data collection, measurement, and analysis is known as the research design (Kothari, 2020). The design establishes a link between the collected data and the research questions or objectives. In this study, survey research designs for causation and description were integrated. Survey descriptive research is employed when the goal of the study is to depict the features of a social phenomena and ascertain its frequency of occurrence, according to Dehdashti (2021). Because the proposed study sought to highlight the hedging strategies employed by ZSE-listed companies and their respective performance, the design was therefore perfect for the research. The 63 companies listed on the ZSE were the study’s target population. At the head offices, the chief financial managers were the respondents from each firm were the chief financial managers of the head offices. The research gathered data from primary and secondary sources. The financial managers were asked to self-administer a questionnaire that included both closed- and open-ended questions in order to gather primary data. When gathering a large quantity of data in a short period of time, a questionnaire was appropriate (Orodho, 2020). The firms’ performance was the main focus of the secondary data. The company’s financial statements were used to gather information on the return on assets and return on capital invested for the last five years, from 2019 to 2023, information on the return on assets and return on capital invested was gathered from the company’s financial statements. The requirement for listed organizations to produce official financial statements that reflect their performance and overall business health guided the choice of financial statements as a means of gathering secondary data.

Direct Relationship Model

Y =β0 + β1X1 + β2X2 +β3X3 +β4X4 +εi

Where Y presents performance offirms, the dependent variable

Β0 is a constant term

X1 = Foreign exchange hedging practices

X2 = Commodity price hedging practices

X3 = Interest rate hedging practices

X4 = Equity hedging practices

Β 1, β2, β3 andβ4= regression coefficients to be estimated

εi= regression error term.

Moderated Relationship Model

Y =β0 + β5X5 + β6X6 +β7X7 +β8X8+ β9X9 +εi

Where Y presents performance offirms, the dependent variable,

Β0 is a constant term

β5, β6, β7,β8 and β9= moderated regression coefficients to be estimated

X5 = moderated Foreign exchange hedging practices

X6 = moderated Commodity price hedging practices

X7 = moderated Interest rate hedging practices

X8 =moderated Equity hedging practices

X9=Moderating variable (central bank controls)

εi= regression error term.

To display the performance trend over the last five years, the firms’ performance was quantitatively examined. ROIC and ROA were used to gauge performance. ROIC is calculated as earnings before finance charges and taxes divided by the average of total capital for the previous and current years, plus the current component of long-term debt and short-term debt. The book value of capital invested in current assets was considered in this calculation, and it was assumed that the invested capital was accurately measured by the book values of debt and equity. Earnings before financing charges and taxes were divided by the entire asset book value to get ROA.

FINDINGS AND DISCUSSIONS

The internal consistency technique of reliability testing was used to measure the study’s reliability, as shown in table 4.1 below. With 20 items utilized in the study to measure the independent and mediating factors, the Cronbach Alpha co-efficient was calculated to be 90.3%.

Table 4.1 Reliability Analysis

| Variable | Items | α | Comment |

| Foreign exchange risk hedging practices | 5 | 0.820 | Reliable |

| Commodity pricing risk hedging practices | 4 | 0.868 | Reliable |

| Interest rate risk hedging practices | 4 | 0.808 | Reliable |

| Equity risk hedging practices | 4 | 0.855 | Reliable |

| Central bank controls | 3 | 0.828 | Reliable |

| Score | 20 | 90.3 | Reliable |

Source: survey data (2024)

70.31% of respondents to the study completed it. Forty-five of the 64 questionnaires that were distributed were satisfactorily completed and used for analysis. Regarding foreign exchange practices, the majority of respondents (26.7%) agreed that their companies utilized forward contracts for foreign exchange as a tool for risk hedging, while 2.2% thought their company used swaps and options as a tool for risk mitigation. Regarding interest rate risk hedging strategies, the majority of respondents (26.7%) concurred that their companies employed interest rate forwards as a tool to reduce risk, while a smaller percentage (2.2%) said their companies utilized a combination of futures, options, and swaps. Regarding procedures for commodity pricing risk hedging, the majority of respondents (44.4%) thought that their companies employed commodity futures as instruments for risk hedging. 2.2% of respondents, on the other hand, said that their companies did not employ any of the risk reduction methods. The majority of respondents (40%) concurred that equity futures were a technique utilized by their companies to reduce risk.2.2% of respondents said their company utilized none of the risk-mitigating instruments, while 2.2% said their company used all of the tools. These are the minority views.

The descriptive results on foreign exchange practices are shown in the table below. The descriptive results on foreign exchange practices are shown in the table below. Likert scale with five points: 1 for not at all, 2 for mild extent, and 3 for significant extent 4=high degree 5=extremely high extent was applied to the foreign exchange practices statements.

Table 4.2 Foreign exchange hedging practices

| N | Min. | Max. | Mean | Std. Deviation | |

| Currency fluctuations | 45 | 1.00 | 5.00 | 3.8222 | 1.07215 |

| Firm sensibility | 45 | 1.00 | 5.00 | 3.5333 | 1.03573 |

| Firm remuneration | 45 | 1.00 | 5.00 | 3.6889 | 1.45886 |

| Tax advantage | 45 | 1.00 | 5.00 | 3.4222 | 1.03328 |

| Financial market condition | 45 | 1.00 | 5.00 | 3.6889 | 1.06221 |

| Aggregate score | 45 | 3.6311 | 1.13245 |

Source: survey data (2024)

According to table 4.2 above, respondents’ answers to the statements fell between 1 and 5. The majority of respondents concurred that the following factors somewhat to a great extent influenced foreign exchange hedging practices: currency fluctuations (mean=3.8222), firm sensitivity (mean=3.5333), firm remuneration (mean=3.6889), and financial market conditions (mean= 3.6889). According to respondents, tax advantage (mean = 3.4222) had a moderate impact on foreign exchange hedging strategies. The respondents generally believed that the statements had a slightly high influence on foreign currency rate hedging activities, as indicated by the average mean score of 3.611. The responses showed a normal fluctuation, as indicated by the aggregate standard deviation of 1.13245. The descriptive results on commodity pricing risk hedging strategies are shown in the table below. Likert scale with five points: 1 for not at all, 2 for a slight extent, and so on. 3 = moderate degree 4=high degree For the four statements on commodity pricing risk hedging strategies, 5=very high extent was employed.

Table 4.3 Commodity pricing risk hedging practices

| N | Min. | Max. | Mean | Std. Deviation | |

| Cash flow risk | 44 | 1.00 | 5.00 | 3.9545 | 1.32866 |

| Underinvestment costs | 44 | 1.00 | 5.00 | 3.7955 | 1.21195 |

| Agency costs | 44 | 1.00 | 5.00 | 4.1364 | 1.06947 |

| Financial market condition | 44 | 1.00 | 5.00 | 3.5909 | .99576 |

| Aggregate score | 44 | 3.8693 | 1.15146 |

Source: survey data (2024)

The responses from the respondents ranged from 1 to 5, as shown in table 4.3 above. The majority of respondents concur that financial market situation favorability (mean=3.5909), underinvestment costs (mean=3.7955), agency costs (mean=4.1364), and cash flow risk (mean=3.9545) all had a significant impact on commodities price risk hedging strategies. The respondents generally believed that the remarks influenced commodity pricing risk hedging strategies to a slightly high amount, as indicated by the aggregate mean score of 3.8693. The respondents’ responses showed a normal deviation, as indicated by the aggregate mean score of 1.15146. Studies like Carter et al. (2018), which discovered underinvestment and the use of agencies as some of the techniques taken into consideration in reduction of commodity price risk hedging practices, support these findings. The descriptive results about interest rate risk hedging strategies are shown in the table below. Likert scale with five points: 1 for not at all, 2 for a slight extent, and so on. 4=high extent, 3=moderate extent For the four comments on interest rate risk hedging strategies, the term “5=very high extent” was used.

Table 4.4 Interest rate risk hedging practices

| N | Min. | Max. | Mean | Std. Deviation | |

| Level of interest payment | 44 | 1.00 | 5.00 | 3.4318 | 1.08687 |

| Market trading platform | 44 | 1.00 | 5.00 | 3.7727 | 1.05354 |

| Credit arrangement | 44 | 1.00 | 5.00 | 3.6136 | 1.22410 |

| Financial market condition | 43 | 1.00 | 5.00 | 3.7442 | .87541 |

| Aggregate score | 43 | 3.6406 | 1.05998 |

Source: survey data (2024)

The responses from the respondents ranged from 1 to 5, as shown in table 4.4 above. The majority of respondents concurred that interest rate risk hedging methods were somewhat influenced by the market trading platform (mean = 3.7727), credit arrangement (mean = 3.6136), and financial market condition favorability (mean = 3.7442). Nonetheless, respondents believed that interest payment level had a moderate impact on interest rate risk hedging strategies. The respondents generally believed that the remarks influenced interest rate risk hedging practices to a slightly high amount, as indicated by the aggregate mean score of 3.64056. The responses of the respondents varied normally, as indicated by the aggregate standard deviation of 1.05998.

The descriptive results of equity riskhedging strategies are shown in the table below. On a Likert scale of 1 to 5, 1 represents not at all and 2 denotes a slight extent 4=high extent, 3=moderate extent For the four statements on equity risk hedging strategies, the scale of 5=very high extent was applied.

Table 4.5 Equity risk hedging practices

| N | Min. | Max. | Mean | Std. Deviation | |

| Price volatility | 44 | 1.00 | 5.00 | 3.7500 | 1.10232 |

| Investment portfolio | 45 | 1.00 | 5.00 | 4.1111 | 1.07073 |

| Equity prices | 44 | 2.00 | 5.00 | 4.1136 | 1.01651 |

| Financial market condition | 44 | 2.00 | 5.00 | 3.7727 | .77350 |

| Aggregate score | 43 | 3.9369 | 0.990765 |

Source: survey data (2024)

Table 4.5 above shows that the respondents’ answers on investment portfolio and price volatility fell between 1 and 5, while their answers on equity prices and the state of the financial markets fell between 2 and 5. The majority of respondents concurred that financial market situation favorability (mean=3.7727) and price volatility (mean=3.7500) had a slightly high influence on stock hedging practices. Additionally, respondents revealed that a considerable degree of effect was exerted by investment portfolio (mean=4.1111) and equity prices (mean=4.1136) on equity risk hedging techniques. The overall mean score was 3.9369, which showed that most respondents believed the remarks had a moderately significant impact on equity hedging strategies Milanova (2013) discovered in their research that equity prices and investment portfolios have an effect on the practice of hedging equity risk.The descriptive findings on central bank controls are shown in the table below. On a Likert scale of 1 to 5, 1 represents strongly disagreement and 2 represents agreement. 3= unsure 4=in agreement For the three assertions on central bank controls, the rating of 5=strongly agree was applied.

Table 4.6 Central bank controls

| N | Min. | Max. | Mean | Std. Deviation | |

| Economic independence | 43 | 1.00 | 5.00 | 3.9302 | .96103 |

| Central bank regulations | 43 | 2.00 | 5.00 | 4.1163 | .90526 |

| Inflationary controls | 43 | 1.00 | 5.00 | 3.9302 | 1.00937 |

| Valid N (listwise) | 43 | 3.9922 | 0.95855 |

Source: survey data (2024)

The questions on economic independence and inflationary controls ranged from 1 to 5, according to table 4.6 above, whereas the questions on central bank rules ranged from 2 to 5. The majority of respondents concurred that the central bank controls were heavily impacted by economic independence (mean=3.9302), central bank rules (mean=4.1163), and inflationary controls (mean=3.9302). The overall mean score of 3.9922 showed that most respondents believed the remarks had a significant impact on central bank controls. The total standard deviation was 0.95855, which suggests that the respondents’ replies varied normally. The total standard deviation was 0.95855, which suggests that the respondents’ replies varied normally. The descriptive findings of this study are supported by studies by Guttierez (2003), in which the researchers identify inflationary controls, central bank regulations, and economic independence as some of the metrics of central bank controls.

Based on the descriptive results, the study draws the conclusion that risk hedging strategies, particularly those related to foreign exchange, interest rate, commodity price, and equity risk, have an impact on a company’s performance. There are other mediating factors that also affect the relationship between risk hedging strategies and listed corporations’ financial performance, such as central bank restrictions. The ANOVA table indicates the model’s significance, the coefficients table gives the beta coefficients and the importance of each variable to the investigation, and the model summary table computes the R squared to show the strength of the association.

Table 4.7 Inferential analysis of direct relationship

Model Summaryb

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin-Watson |

| 1 | .625a | .391 | .328 | .62295 | 1.015 |

ANOVAa

| Model | Sum of Squares | df | Mean Square | F | Sig. |

| Regression

1 Residual Total |

9.712 | 4 | 2.428 | 6.256 | .001b |

| 15.135 | 39 | .388 | |||

| 24.847 | 43 |

Coefficientsa

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | .956 | .621 | 1.539 | .052 | |

| foreign exchange | .533 | .246 | .455 | 2.170 | .036 | |

| Commodity pricing | .116 | .182 | .135 | .641 | .125 | |

| Interest rate | .119 | .188 | .154 | .635 | .129 | |

| equity risk | .278 | .217 | .309 | 1.281 | .048 | |

Source: survey data (2024)

Based on the model summary presented in Table 4.7 above, R2=0.391 suggests that hedging practices, such as those related to foreign exchange risk, commodity pricing risk, interest rate risk, and equity risk, account for 39.1% of the variation in the financial performance of companies listed on the ZSE. Still, other factors not covered in the study account for 60.9% of the difference. The ANOVA table shows that the model utilized is significant at F=6.256; P<0.05, indicating that the findings are adequate for drawing conclusions about the study. The determined regression equation was as follows, with reference to the coefficients table:

Y= 0.956 + 0.455 X1+ 0.135 X2+ 0.154 X3 + 0.309 X4+ e

A unit increase in hedging practices (foreign exchange risk, interest rate risk, commodity pricing risk, and equity risk) is associated with a 0.956 increase in the financial performance of firms listed on the ZSE, according to the regression equation, which also reveals a positive relationship between the independent and independent variables with a constant of 0.956. The results of Weston (2021) corroborate this beneficial association between hedging activities and business financial success.

The first objective evaluated the impact of foreign exchange hedging strategies on the ZSE-listed companies’ performance. The results of the analysis showed a significant positive correlation (β=0.455; p<0.05) between the performance of companies listed on the ZSE and their strategies for hedging foreign exchange risk. The results of the analysis showed a significant positive correlation (β=0.455; p<0.05) between the performance of companies listed on the ZSE and their strategies for hedging foreign exchange risk. The second objective looked at how the performance of companies listed on the ZSE was affected by risk hedging strategies related to commodity pricing. The study found a weakly negative correlation (p>0.05) between the performance of companies listed on the ZSE and their strategies for hedging commodity pricing risk (0.135). The third objective assessed the impact of interest rate risk hedging strategies on the ZSE-listed companies’ performance. The research found a somewhat positive correlation at β= 0.154; p>0.05 between the performance of companies listed on the ZSE and their interest rate risk hedging strategies. The fourth objective looked at how the performance of companies listed on the ZSE was affected by equity risk hedging strategies. The results of the analysis showed a significant positive correlation (β= 0.309; p<0.05) between the performance of companies listed on the ZSE and their equity risk hedging strategies.

Table 4.8 Inferential analysis on moderated relationship

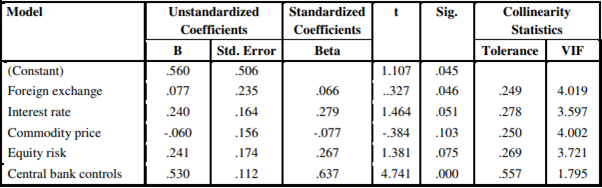

Model Summaryb

![]()

ANOVAa

Coefficients

Source: survey data (2024)

Based on the model summary presented in Table 4.8 above, R2=0.617 indicates that central bank controls on hedging practices, such as those related to foreign exchange risk, commodity pricing risk, interest rate risk, and equity risk, account for 61.7% of the variation in the financial performance of companies listed on the ZSE. Still, other factors not covered in the study account for 38.3% of the difference. The ANOVA table shows that the model was significant at F=12.255; P<0.05, showing that the study’s conclusions were valid based on the findings.

The fifth objective of the study aimed to examine how central bank controls affect the correlation between risk hedging strategies and the performance of ZSE-listed companies. When moderated, the established regression equation was, according to the coefficients table:

Y= 0.560 + 0.066 X5-0.279 X6 + 0.077 X7 + 0.267 X8+ 0.637 X9 e

An increase of one unit in hedging practices (foreign exchange risk, interest rate risk, commodity pricing risk, and equity risk) results in a 0.56 increase in the financial performance of firms listed on the ZSE, according to the regression equation, which also demonstrates a positive relationship between the independent and independent variables with a constant of 0.560. The results of Judge (2002) and Weston (2001) corroborate this beneficial association between hedging activities and business financial success. The results of the study, which show that the mediation of central bank controls increased the strength of the relationship between the study variables (i.e., R2 from 39% to 61.7%), suggest that an intervention by a county’s central bank controls has a positive impact on the effect of risk hedging practices on a firm’s financial performance. Gutiérrez (2003) identified central bank controls as an intervening variable.

CONCLUSIONS AND RECOMMENDATIONS

The study’s main goal was to find out how financial hedging strategies affected the ZSE-listed companies’ performance. The financial performance of companies listed on the ZSE was found to be positively impacted by financial risk hedging methods. The first objective evaluated the impact of foreign exchange hedging strategies on the ZSE-listed companies’ performance. The results of the analysis showed a significant positive correlation (β=0.455; p<0.05) between the performance of companies listed on the ZSE and their strategies for hedging foreign exchange risk. The responses showed a normal fluctuation, as indicated by the aggregate standard deviation of 1.13245.

The second objective looked at how the performance of companies listed on the ZSE was affected by risk hedging strategies related to commodity pricing. The study found a weakly negative correlation (p>0.05) between the performance of companies listed on the ZSE and their strategies for hedging commodities pricing risk hedging (0.135). The respondents generally believed that the remarks influenced commodity pricing risk hedging strategies to a slightly high amount, as indicated by the aggregate mean score of 3.8693. The respondents’ responses showed a normal deviation, as indicated by the aggregate mean score of 1.15146. The research found a somewhat positive correlation (β= 0.154; p>0.05) between the performance of companies listed on the ZSE and their interest rate risk hedging strategies. The respondents generally believed that the remarks influenced interest rate risk hedging practices to a slightly high amount, as indicated by the aggregate mean score of 3.64056. The responses of the respondents varied normally, as indicated by the aggregate standard deviation of 1.05998.

The fourth objective looked at how the performance of companies listed on the ZSE was affected by equity risk hedging strategies. The results of the analysis showed a significant positive correlation (β=0.309; p<0.05) between the performance of companies listed on the ZSE and their equity risk hedging strategies. The total mean score was 3.9369, which showed that most respondents believed the statements had a moderately high impact on stock hedging strategies. The responses of the respondents varied normally, as indicated by the aggregate standard deviation of 0.99077. The fifth objective aimed to examine the impact of central bank regulations on the correlation between risk hedging strategies and the performance of companies that are listed on the ZSE. The study discovered that the association between risk hedging strategies and business financial performance was positively enhanced by central bank controls, as seen by the large rise in the R2 from 39. % to 61.7%. The total standard deviation was 0.95855, which suggests that the respondents’ answers varied normally.

The results clearly show that financial risk hedging techniques improve listed companies’ financial performance. The association gets stronger with tighter central bank regulations, suggesting that a nation’s central bank plays a big part in reducing risk and maintaining the financial stability of its securities exchange market. The research suggests that companies in the stock exchange should use alternative risk mitigation tools including exchange-traded funds, insurance, collateralized debt obligations, and credit default swaps because commodities price risk and equity risk, in particular, continue to be weakly significant. Only four risk mitigation tools swaps, options, futures, and forward contracts were included in the study. Subsequent studies ought to contemplate reproducing the findings through an amalgamation of alternative instruments to facilitate cross-referencing.

REFERENCES

- Adam, T., and S. Fernando. (2006) “Hedging, Speculation and Shareholder Value.” Journal of Financial Economics, 81 (2), 283-309.

- Ahmed H., Azevedo A. and Guney, Y. (2010) The Effect of Hedging on Firm Value and Performance: Evidence from the Nonfinancial UK Firms Journal of Corporate Finance, 18 (12), 221-237

- Allayannis, G., Ihrig, J., & Weston, J. (2005).Financial vs. operational strategies, American Economic Review Papers and Proceedings, 91, 391-395.

- Barney, J. (2001). Firm resources and sustained competitive advantage. Journal of Management, Vol. 17, pp. 99-120.

- Bhole, L., & Dash, P. (2002). Industrial Recession in India: Is Interest Rate the cause? Productivity, 43(2), 268-277.

- Bilson, J. F. & Hsieh, D. A. (2008). The profitability of currency speculation. International Journal of Forecasting, 3(1), 115-130. 53

- Blaaw, A. (2008). Market risk management in Nigeria. United Bank of Africa.

- Bodnar, G.; Tang, C.; Weintrop, E. J. (2011). Both Sides of Corporate Diversification: the Value Impact of Geographical and Industrial Development. NBER Working Paper 6224.

- Boehm, T. P., &Schlottmann, A. (2007). Mortgage pricing differentials across Hispanic, African-American, and White households: Evidence from the American housing survey. Cityscape, 93–136.

- Brigham, F. E. &Ehrhardt C. M. (2002).Financial Management, Theory & Practice, India, 158, 932.

- Brodsky, W. (2010). The Globalization of Stock Index Futures: A Summary of the Market and Regulatory

- Developments in Stock Index Futures and the Regulatory hurdles which exist for Foreign Stock Index Futures in the United States. Northwestern Journal of International Law and Business, 15(2).

- Carter, D. ; Rogers, D.; Simkins, B. (2006). Does hedging affect firm value? Evidence from the US airline industry. Financial Management, Spring 2006: 53-86.

- Carter, D., Rodgers, D. A., & Simkins, B. (2003). Does fuel Hedging make Economic seZSE? The case of US airline Industry. Journal of Financial Website, December.

- Craig, F. (2003). The Treynor Capital Asse Pricing Model. Journal of Investment Management, 1(2).

- Cumby, R.E. & M. Obstfeld (2009). A note on Exchange Rate Expectations- and Nominal Interest Differentials: A Test of the Fisher Hypothesis. Journal of Finance, 5, 697 703 Dhanani, A.; S. Fifield; C. Helliar; and L. Stevenson.(2007),“Why UK Companies Hedge Interest Rate Risk.” Studies in Economics and Finance, 24 72-90.

- Deutsche Borse Group. (2014). The Global derivatives market: An Introduction. Retrieved 2015, from http://www.math.nyu.edu/faculty/avellane

- Elahi and Dehdashti (2011),Classification of Researches and Evolving a Consolidation Typology of Management Studies. London. The Center for Innovations in Business and Management Practice

- Fauver, L., and A. Naranjo. (2010). “Derivative Usage and Firm Value: The Influence of Agency Costs and Monitoring Problems.” Journal of Corporate Finance, 16 , 719-735.

- Giddy, I.H. (2010). Exchange Risk Whose view? Financial Management,8, 23-33.

- Goselin, M. A. (2007). Central bank performance under inflation taregeting.

- Gutierrez, E. (2003). Infaltion performance and constitutional Central Bank Independence: Evidence from LatinAmerica and the Carribean. IMF.

- Krause, S., & Rioja, F. (2006). Financial Development and Monetary Policy Efficiency. Retrieved September 2015, from http://www.bankofcanada.ca/wp-content/uploads/2010/06/gosselin.pdf

- Hagelin, N.; Holmen, M.; Knopf, J. and Pramborg, B. (2004). Managerial stock option and the hedging premium, unpublished paper.

- Haushalter, G. D. (2007). “Financing Policy, Basis Risk, and Corporate Hedging: Evidence from Oil and Gas Producers.” Journal of Finance, 55 (20) 107-152.

- Hofer, C. (2003). Know-how and asset accumulation and dynamic capabilities accumulation: The case of R&D. Strategic Management Journal 18:339–360.

- Horne Van C. James &Wachowicz M. John Jr, (2012). Fundamentals of Financial Management, 9th edition, New Jersey, USA, 209-10.

- Judge, A. (2003). ‘Why do firms hedge? A review of the evidence’, unpublished mimeo.