An Integrated Implementation System on SME

- Ali Farhan

- 405-413

- Feb 22, 2024

- Accounting

An Integrated Implementation System on SME

Ali Farhan

STIE Mahardhika

DOI: https://doi.org/10.51244/IJRSI.2024.1101031

Received: 09 January 2024; Revised: 20 January 2024; Accepted: 24 January 2024; Published: 22 February 2024

ABSTRACT

This case study-based research with an action research approach aims to explain the implementation process of the online-based information system, Accurate Online for SMEs, Karnevor.id. The results of this research show that the motivation for the desire to implement the program is; the need for valid financial reports, the need for integrated business information, and easy reporting flexibility. Retention encountered in the implementation process; user awareness about the benefits of the system, user understanding of the system mechanism.

Keywords: information system, accounting, implementation, Technology Acceptance

INTRODUCTION

Several previous studies stated that management/company performance is supported by an effective management information system, because the existence of an effective management information system will encourage appropriate strategic decision making, then the impact will be an increase in material performance. Soobaroyen and Poorundersing (2008) found that Management Accounting Systems have a positive impact on managerial performance and could support decentralized activities in management, apart from that, information systems can also increase information sharing between departments (Argyropoulou, 2013). The growing needs of organizations demand that management accounting systems must improve, researchers such as Johnson and Kaplan, 1987; Bromwich, 1990; IFAC, 1998[1]; Abdel-Kader and Luther, 2004; Sulaiman et al., 2004 argue that the traditional characteristics of information produced through traditional methods such as; historicity, internally oriented, provided periodically, and based on general knowledge/general regulations are becoming increasingly inadequate for effective decision making. In many cases, especially in SMEs, information integration and database preparation are actually the main problems that must be resolved, the absence of an adequate database causes business decision making in SMEs to be based only on intuition.

Business and economic advances such as modern manufacturing technology, competition in the market, the evolution of looser management models, deregulation of economic sectors, privatization of state-owned enterprises, and changes in consumer behavior have not only made the use of accounting information more important but also driven increased demand for systems. “quality” management accounting. (Lucas, 1997; Granlund and Lukka, 1998; Mia and Clarke, 1999). However, the process of integrating systems into a business is not without challenges. TAM (Technology Acceptance Model) (Masrom, 2007) suggests that the ease of the implementation and integration process of a new technology is determined by the belief that using the technology will improve work performance and the perception of ease of use.

The research above is the basic argument for this research to conduct a study of the implementing a new program process at Karnevor.id, a company operating in the F&B sector with online services. The ability of SMEs to manage information in their business is very important to be able to create competitive advantages for SMEs, as well as create new added value for consumers. The program that will be implemented into Karnevor.id is the Accurate Online ecosystem which facilitates the distribution of financial transactions and information as well as an integrated sales system on the same server, so that all activities and transactions are integrated in one database which can be used as a source of information for adequate decision making. This next article will explain the mechanism for implementing the accurate online program, its impacts and the challenges it faces.

Accurate Online

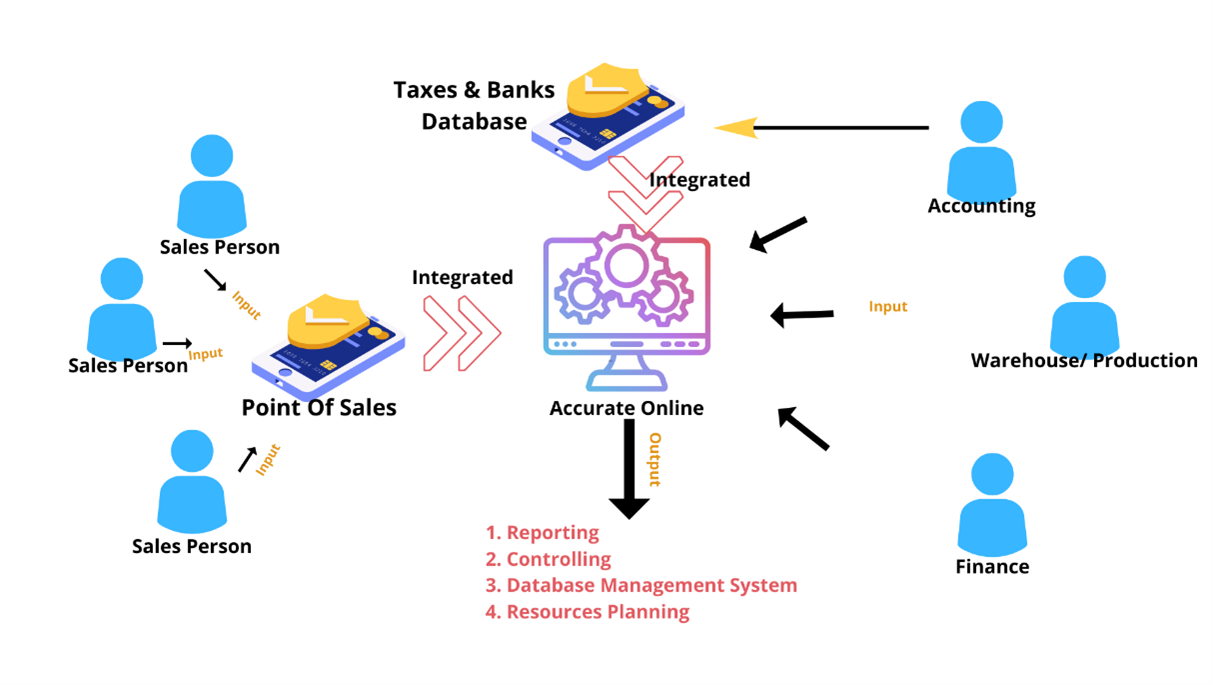

Accurate online is a cloud-based accounting software that integrates accounting records from many activities; Warehouse, finance, accounting and simple production departments. Apart from that, Accurate Online is also an integrated ecosystem between sales people, tax reporting, banking and companies. The following is a chart of the accurate online ecosystem

Image 1. Accurate Online Ecosystem

It is the program ecosystem above that will be implemented in the company, and then all implementation activities will be discussed and analyzed with adequate approaches and theories related to this context.

RESEARCH METHODOLOGY

Action research has been categorized into a newer research methodology category. Action research is defined as the realization of the human need to be autonomous in various things; loving relationships, productivity; encouragement towards freedom, creativity and self-recreation. Because of the complexity of the construction of the reality that is trying to be analyzed, then. Traditional research methods in similar contexts become less relevant. The appropriate form of theory for such inquiry already exists in one’s mind, where each person is able to say, ‘I understand what I am doing and why I am doing it.’ This theory is realized within oneself and produced through practice. (Whitehead, 2000). Examining our practices and the assumptions that underlie them allows us to develop a creative understanding of ourselves and our own processes of learning and growth. When we do action research, we make our thinking different. ‘After discovering something, I will never see the world again like before. My eyes became different; I have made myself into a person who sees and thinks differently. I have crossed the gap, the heuristic gap that lies between problem and discovery’ (Polanyi, 1958: 143). Here I want to talk about the evolution of knowledge, and how it can lead to the evolution of practice. What do we need to know to realize the potential of action research at personal and collective levels, and how do we translate that knowledge into purposeful collective action? It is also important to recognize the existence of powerful forces that may try to suppress personal and collective reform, and why they do so, and to demonstrate the need to develop the power and political will to circumvent these forces and develop a vision of reform. in a practical way.

To develop this approach, certain conditions apply. People need to increase their awareness of the importance of what they do as a form of social change, and have confidence in the legitimacy and importance of it. They also need to be aware of the politically constructed nature of the context in which they work. This means that they must be aware of how powerful institutional voices have the capacity to close off means of self-expression and avenues for further development of their work and to support their efforts.

A practical guide to action research is available in the You and Your Action Research Project (McNiff et al., 1996). Therefore I do not intend to explain in detail here how to conduct action research. In this book I want to present some of the main ideas, as well as examples, to show how people approach the investigation of their actions, and how they develop different insights in the process. The basic process of action research can be described as:

- We review our current practices,

- Identify the aspects we want to improve,

- Imagine the way forward,

- Implementation of work programs.

- We change our plans based on what we find and proceed with ‘action’

- Evaluation of modified actions,

DISCUSSION

Karnevor.id is a brand from an F&B business that sells its products online. Karnevor has 13 employees divided into 3 departments; sales, production and finance. This company has 40 partners spread across 40 cities in Java, Bali and Nusa Tenggara. In running its business, the Company needs a recording system that integrates activities in the production, sales and finance departments.

“I need a program that can help with the recording process so that there is no need for manual recording and reporting activities from employees. With programmed recording, the data should be more valid and easier to manage.” Management said

As long as the business is running, the recording that occurs in the company is on many working papers that are not integrated, so that management finds it difficult to get updated data related to the business.

“If I want to know retail and partner sales, I still have to look at different data. I’m having a hard time with that.” Management said

The first thing to do in this implementation process is to identify and plan the business activities required by the Company. Each department needs to identify its activities so that they can be integrated into the programming process in the accurate online ecosystem.

Current Practices Planning & Identification

The plans prepared by researchers to implement the program and the evaluation process are as follows;

- Identify activities and difficulties encountered

- Identify management needs

- Identify user needs so that their activities can be relevant to management needs

- Inventory of the entity’s assets and liabilities

- Develop work procedures, transaction documentation, separation of responsibilities and reporting processes

- Program implementation

- Evaluation

Sales Department

In the sales department, the main difficulty faced is tabulating data and reporting on sales transactions. Therefore, it is necessary to design patterns that form sales activities, so that the data received can be managed and processed as a source of management information. Sales admins have difficulty managing data, because data documentation is messy and still in the form of manual data.

Finance & Accounting Department

The Finance & Accounting Department has obstacles evaluating the value and quantity of inventory, as well as reporting on the company’s business performance because the data for each partnership has not been integrated. Finance & Accounting also finds it difficult to identify which recorded debts/receivables belong to which customer/vendor. This will certainly be a problem for companies to carry out cash flow management and control. Production Department

The production and warehouse departments have obetacles in carrying out production planning and goods management procedures, due to the lack of adequate records/methods to assist the administrative process of their work.

Management Needs

Management has a need for information and control in its business, so that business activities become efficient and have an impact on positive business growth. Management has several things that must be fulfilled by each department;

- Sales reports per item, city and customer used to develop promotional programs and performance assessments

- Profit and Loss and Cash Flow Statements

- Segment Performance Report.

- Integration of sales reporting, business segments and profit and loss reports

Table 1. Challanges & Needs

| Sales | Data tabulation and analysis for sales reporting | 1. Knowlegde to manage data and analysis |

| 2. Controlling transaction data validation | ||

| Finance & Accounting | Evaluate stock value | 1. Controlling the stock transaction |

| 2. Data management system for stocks | ||

| Reporting Business Performance | 1. Knowlegde to manage data dan analysis | |

| 2. Controlling transaction data validation | ||

| Account receivable & payables identification | 1. Database for consumer and vendor | |

| 2. System to maintain the transaction for each vendor and costumers | ||

| Production & Warehouse | Production planning and warehouse management system | 1. Data management system for stocks |

| 2. Knowlegde to manage data dan analysis | ||

| 3. Controlling transaction data validation |

Improving Programs

There are several fundamental aspects regarding technical work and support systems that need to be improved so that the business/organization can meet management needs. From the tabulation above we can find several basic things needed by entities in general;

- Database of stock, vendors, customers

- Data analysis knowledge/skills

- Systemized work procedures

- Work aids/programs that help with documentation/transaction recording needs.

The four things mentioned above are fundamental needs that must be improved by management, so that management performance becomes more effective. To make changes, what must be done is as follows;

Create a database of vendors, stock and customers

Creating a vendor, inventory and customer database can be done by arranging categories for each designated item.

Table 2. Design Inventory Item and Category

| List of Database | Category | Indicators |

| Stocks | Meat | Product made form meat |

| Chicken | Product made form chicken | |

| Veggie | Product made form vegetables | |

| Sauce | Sauce Product | |

| Production Material | Inventory that been used for raw material | |

| Packaging | Inventory that been used for raw packaging | |

| Vendor | Scheduled Vendor | Vendor that facilitating term of payment |

| Cash Vendor | Vendor that did not facilitating term of payment | |

| Customer | Meating Point | Dine in customers |

| Reseller | Retail by Product Customers | |

| Stockist | Agent that manage some resellers |

Skills dan data analysis

There are couples skills that need to improve regarding to data processing and the job description among employees. Those skill are; data tabulation, product knowledge, business process knowledge, mirosoft excel, data verification and reporting. All skills that need to improve were described and been transferred to the employee by practicing the skilss and giving the feed back.

Table 3. Skills and Learning Method

| Departement | Needs | Skills to be Updated | Learning Method |

| Sales | 1. Knowlegde to manage data and analysis | 1. Data tabulation | 1. Trial and error practicing |

| 2. Data input | |||

| 2. Controlling transaction data validation | 3. Data validation | ||

| 4. Excel | |||

| Finance & Accounting | 1. Controlling the stock transaction | 1. Stock Opname | 1. Learning by Based practice |

| 2. Data management system for stocks | 2. Verification Transaction | ||

| 3. Knowlegde to manage data dan analysis | 3. Reconcile transaction | 2. Dummy transaction learning | |

| 4. Controlling transaction data validation | 4. Reporting analysis | ||

| 5. Database for consumer and vendor | 6. Business Process Analysis | ||

| 6. System to maintain the transaction for each vendor and costumers | |||

| Production & Warehouse | 1. Data management system for stocks | 1. Stock Opname | 1. Learning by Based practice |

| 2. Knowlegde to manage data dan analysis | 2. Verification Transaction | ||

| 3. Controlling transaction data validation |

Working Procedures

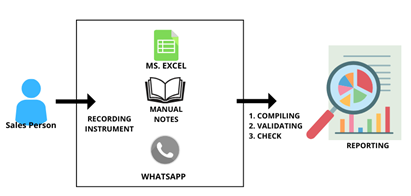

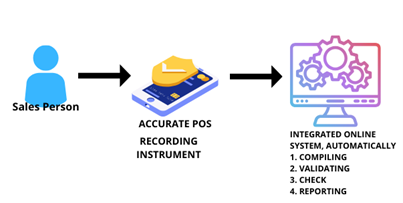

If previously the sales admins only used Microsoft Excel, WhatsApp chat and written notes in books to document sales, then compiled, tabulated and analyzed the data again, then this method must be changed, the sales admins took notes in the Accurate POS (Point of Sales) program ) and Accurate Online to record sales (invoices) and cash receipts.

Previously :

Image 2. Previously Working Procedure

In general, this happens in every department related to recording and documenting transactions, including sales, production admin, and finance & accounting. Changes in procedures for recording on the Accurate POS and Accurate Online instruments reduce repetitive work for compiling data, the following are changes to work procedures that occur.

Image 3. Improved Working Procedure

Implementation of Work Program and Inventory of Assets & Liabilities

After carrying out an inventory of assets, liabilities and all work procedures and their challenges, the results of this work are then implemented into the work process and Accurate Online application ecosystem. From the results of this implementation, researchers received several feedback from respondents.

“Often the available inventory data doesn’t show how much is in the warehouse, so I’m confused.” Sales Admin

“Sometimes there are menu items that are not yet available in the program, so invoices cannot be updated immediately.” Sales Admin.

“I often can’t input into the program because I can’t do multiple job descriptions, because I have to serve customer chats. Can input be postponed to a different time?” Sales Admin

“My product input is now more updated than before, so I can follow and manage the production schedule better. This program is very helpful.” Production Admin

“The procedure for recording the invoice and payment is quite long, there are quite a lot of inputs that have to be filled in. Sometimes we are still confused about where these inputs lead to the transaction?” Finance & Accounting.

Table 4. User’s Obstacle During Implementation

| Departement | Problems |

| Sales | 1. Uncompleted menu listed on the programs |

| 2. The information did not represent the actual | |

| 3. Did non understand the program mechanism | |

| 4. Multiple jobdesc while input the data | |

| Finance & Accounting | 1. Missinterpretation transaction |

| 2. Did non understand the program mechanism | |

| Production & Warehouse | 1. Did non understand the program mechanism |

From this implementation process it was also found that the findings from this research confirmed the TAM (Technology Acceptance Model) which states that the ease of the implementation and integration process of a new technology is determined by the belief that the use of technology will improve work performance and the perception of ease of use (Masrom, 2007). This can be seen during the evaluation stage, that the difficulties faced by users when inputting and using the program are caused by not knowing the function, benefits, objectives and mechanisms of the program. If the user has discovered the benefits, goals and mechanisms, it will be easier to understand and run the program.

Evaluation

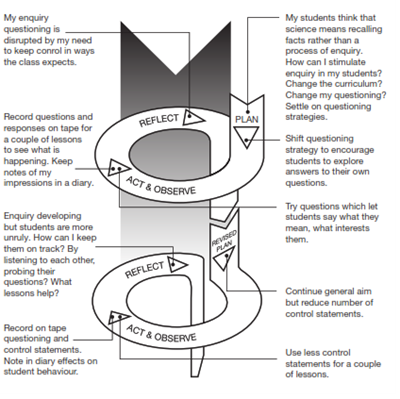

In general, the obstacles faced in implementing new programs/new technology in this research arise due to the planning process and identification of risks and obstacles that have not been completed. This will certainly be difficult to resolve ideally without sufficient experience from the implementer and the users involved. In the evaluation and improvement stages it is important for the users involved to know the benefits and ultimate goals of technological changes, this will create an integration and improvement process within program changes will become easier. Naturally, in each stage of this research, the action research procedure is carried out in a spiral, where dialectics, analysis, observation, implementation and evaluation move in a ‘conical’ form. In Kemmis and McTaggart’s research (1998), the design is as follows;

The impact resulting from changes in work procedures and integrated program implementation in the Company, the Company has a strong database, its validity is tested, reporting is faster and updated, and it is easy to coordinate between departments because of the same data and data access in the program.

CONCLUSION

Based on the results of program implementation using this action research approach, it has been confirmed that the Technology Acceptance Model in implementing new technology has proven its validity in this research. This research also shows that the difficulties faced in the implementation process arise due to incomplete planning and identification of risks and activities. Therefore, future implementers/researchers need to carry out comprehensive studies in planning, risks and activity design to be able to carry out the implementation process efficiently.

REFERENCE

- Abdel-Kader, M. G., & Luther, R. (2004). An empirical investigation of the evolution of management accounting practices. Department of Accounting, Finance and Management.

- Argyropoulou, Maria. (2013). Information systems’ effectiveness and organisational performance. Thesis. Brunel Business School. Brunei University.

- Bromwich, Michael. “The case for strategic management accounting: the role of accounting information for strategy in competitive markets.” Accounting, organizations and society 15, no. 1-2 (1990): 27-46.

- Granlund, M., & Lukka, K. (1998). It’s a Small World of Management Accounting Practices. Journal of management accounting research, 10.

- Johnson, H.T. and Kaplan, R.S. (1987) Relevance lost: The rise and fall of management accounting, Boston: Harvard Business School Press.

- Kemmis, S. and McTaggart, R. (1988) The Action Research Planner (third edition). Geelong, Deakin University Press.

- Masrom, M. (2007). Technology acceptance model and e-learning. Technology, 21(24), 81.

- McNiff, J., McNamara, G. and Leonard, D. (eds) (2000) Action Research in Ireland. Dorset, September Books.

- Mia, L., & Clarke, B. (1999). Market competition, management accounting systems and business unit performance. Management Accounting Research, 10(2), 137-158.

- Polanyi, M. (1967) The Tacit Dimension. New York, Doubleday.

- Soobaroyen, T., & Poorundersing, B. (2008). The effectiveness of management accounting systems: Evidence from functional managers in a developing country. Managerial Auditing Journal, 23(2), 187-219.

- Sulaiman, M. B., Nazli Nik Ahmad, N., & Alwi, N. (2004). Management accounting practices in selected Asian countries: a review of the literature. Managerial Auditing Journal, 19(4), 493-508.

- Whitehead, J. (2000) ‘How do I improve my practice? Creating and legitimating an epistemology of practice’, Reflective Practice 1(1): 91–104.