Assessment of CBN Cashless Policy (Electronic Payment System) on Economic Growth in Nigeria

- OBAINOKE, Eromosele Felix

- OKOYE Uche Patrick, Ph. D

- NWAKA-NWANDU, Okwukwe Chihurumnanya

- UGEGE, Joseph Eromosele

- 506-521

- Apr 10, 2024

- Economic Development

Assessment of CBN Cashless Policy (Electronic Payment System) on Economic Growth in Nigeria

OBAINOKE, Eromosele Felix1, OKOYE Uche Patrick, Ph. D2 , NWAKA-NWANDU, Okwukwe Chihurumnanya2, UGEGE, Joseph Eromosele2

1Department of Banking and Finance, National Institute of Construction Technology and Management, Uromi, Edo State, Nigeria

2Department of Public Administration, School of Business and Management Technology, National Institute of Construction Technology and Management (NICTM), Uromi, Edo State.

DOI: https://doi.org/10.51244/IJRSI.2024.1103036

Received: 05 March 2024; Accepted: 11 March 2024; Published: 10 April 2024

ABSTRACT

Purpose: The objective of this study was to examined the effect of electronic payment systems on economic growth in Nigeria from 2012-2022, the relationship between real GDP and electronic payment systems and its impact on business growth in rural areas.

Theoretical framework: The conventional wisdom in the field of growth economics is that the only path to long-term, sustainable development is an increase in productivity achieved via technical advancement. Previous literatures provide a linkage between e-payment and growth (Ravikumar, 2019). However, there is still much to investigate and learn about nexus between electronic payment and economic growth in Nigeria in recent development.

Design/methodology/ approach: The data analysis method uses the Autoregressive Distributed Lagged Regression (ARDL) Method Covering the Period of 2012–2022. The data collection technique is carried out through a questionnaire administered to respondents across the six geopolitical zone. The data for the e-payment statistics was obtained from the quarterly and annual report of Central Bank of Nigeria statistics (2022) and the data for the real gross domestic product was obtained from the Central Bank of Nigeria Statistical Bulletin (2022).

Findings: The results of ADRL indicate positive and direct relationship between real GDP and electronic payment systems with a significant impact on business growth in rural areas. The short-run analysis using the vector error correction model showed the short-run relationship and convergence of the variables real GDP, the value of POS transactions, the value of ATM transactions, the value of mobile transactions, and the value of internet transactions to the long-run equilibrium position.

Research, Practical & Social implications: the result of this study showed that e-payment systems have a positive and direct relationship with economic growth, but it does not significantly contribute to economic growth in Nigeria.

Originality/value: E-payment systems and security investment have a good association with economic growth, which means that if the government prioritize technology and internet infrastructure to make e-payment channels easier and cheaper for the public, it will amount to economic growth vis-à-vis development in Nigeria.

Keywords: Electronic Payment systems, ADRL, Gross domestic product, Monetary Policy and Economic growth

INTRODUCTION

Ever since the beginning of civilization, people have had to pay for goods and services. Over time, there have been more and more ways to pay. As technology got better, electronic alternatives to money were used more and more. This made it possible to do financial transactions at any time and in any place. No one knows when the first electronic payment was made, but in 1870, Western Union was the first company to use a new way to send money electronically. It is thought to be when the first electronic system was made. In 1918, the American Federal Reserve Bank sent money by telegraph (Nino 2018). A few years ago, many people bought goods and services with cash or checks. Cash was used for smaller transactions, while checks were used for larger ones. Even though cash is still the most common way to pay in many parts of the world, it is used less and less because general-purpose payment cards have made it easier for people and businesses to buy and sell. Consumers can now use credit, debit, and prepaid cards, as well as devices like watches and cell phones, to make electronic payments. Using cards more around the world raises a number of concerns, (Akanni, 2022).

A cashless and paperless way to do business and pay for goods and services refers to electronic payment system. With this system, you can pay for goods and services over a computer network, mobile phone instead of with cash or checks. It’s also called an electronic payment system or an online payment system in some places. Over the past few decades, the electronic payment system has grown because more and more people bank and shop online. As the world as a whole move forward on the path of technological progress, many electronic payment systems and payment processing devices have been made to expand, improve, and make more secure e-payment transactions while reducing the number of transactions done with checks and cash. Afaha (2019), posit that e-payment economy is not one in which cash transactions are completely eradicated from the economic environment; rather, it is an economy in which the number of cash-based transactions is reduced to the absolute bare minimum. In recent years, the proliferation of e-payment systems has resulted in the creation of a channel via which money may be sent quickly and easily.

According to Onyeagba (2015), the use of cashless systems of payments and instruments makes a major contribution to the overall efficiency and stability of the financial system. For instance, in Ghana, Cameroon, Benin Republic, Egypt, Morocco, and Asia countries have been implemented electronic payment systems, and they have been embraced by hundreds of thousands of people in across the world. The development of these platforms has made it possible for families living on a low income to conduct financial transactions at a reduced cost.

This has resulted in these users and low-income families no longer having to pay the costs of travelling to the bank or using its services (Akintaro, 2012). In January 2012, the central government of Nigeria implemented a strategy that prioritised the elimination of cash transactions. One of the primary motivations behind the adoption of this policy was the need to expand and update the country’s existing methods of monetary exchange. This was in accordance with the National Payment Systems Vision 2020 (PSV 2020), whose primary objective was to establish a mechanism that was secure, efficient, and effective in order to facilitate the making and receiving of all types of payments from any location at any time through a variety of electronic channels. The strategy, by making more advanced use of information technology, makes it easier to transfer funds, which in turn reduces the amount of time that is lost in banks. The use of electronic payment systems has laid the foundation for Nigeria’s transformation to a contemporary market economy. According to the Central Bank of the Netherlands (2011), a financially stable, effectively operating e-payment system has a significant impact on monetary policy and the level of economic activity as a whole. The growth of e-payments lowers costs and speeds up the flow of goods. It also boosts customer confidence and makes it easier for them to get credit. It is a safe and efficient alternative to cash, and it gets people involved in their finances. Computerized payments are more open and less likely to be done without being registered (Slozko, & Pelo, 2014). As a result, it brings in more tax money and cuts down on the shadow economy.

Based on the facts above, the development of electronic payment systems has led to a positive cycle of economic growth: consumption goes up, goods go down, and demand goes up as a result. Because of this, employment is going up, productivity is going up, and wealth is going up (Zandi, 2016). The usage of various payment methods in Nigeria has significantly increased over the course of the years, but the effects of this trend have not been fully transferred to the country’s economy. One of the primary causes of this is the unwillingness and ignorance of Nigerians to conduct financial transactions over the internet, owing to the fear of becoming victims of online fraud.

The high level of technological sophistication required to use some payment methods makes it more difficult to attract the majority of people. Another significant obstacle that stands in the way of the potential of payment systems is the inability of the banking and finance industries to attract the participation of the majority of the public on these platforms. It is possible that the facilities that will be used for efficient financial transactions by the available deposit money banks in Nigeria will not be able to carry the load of the electronic system. ATMs, point-of-sale systems, mobile banking, and other mediums need to experience a dramatic expansion in order to touch at least 80% of the entire country before any efficient financial intermediation can be achieved (Ravikuma, 2019). In addition to problems with ATMs, customers have reported problems with the network. This suggests that both the network and the ATM machines need to undergo significant improvements in order to ensure the seamless functioning of financial transactions.

Acha et al. (2017) highlighted some of the challenges that are affecting the actualization of the cashless policy and the shift towards electronic systems of payment. Some of these challenges include the lack of availability of point-of-sale terminals at purchase centres, poor internet access, a lack of knowledge on how to use payment systems, difficulties with transactions, a limited number of ATM machines, ATM robberies, and a lack of access to funds. A significant portion of the country’s population is illiterate, making it hard to accurately count everyone in the country. According to Joseph & Richard (2015), in order for citizens to get the most out of e-payment systems, they need to not only be able to read and write but also have a fundamental understanding of information and communication technology (ICT). According to Ajisegiri & Oyebisi (2014), the use of mobile money and internet/web services or platforms may be related to the internet connection and the cost of bandwidth. Ajisegiri & Oyebisi (2014) identified a lack of internet connectivity and a high cost of band width as the primary factors impacting the use of mobile money and internet/web services in Nigeria. The variables used in the study are real GDP, the value of POS transactions, the value of ATM transactions, the value of mobile transactions, the value of internet transactions, the volume of POS transactions, volume of ATM transactions, volume of mobile transactions and the volume of internet transactions. The study aims to examined the impact of electronic payment systems on economic growth in Nigeria from 2012-2022 with reference to relationship between real GDP and electronic payment systems and its impact on business growth in rural areas. The justification for study is hunched on the desire to find out why usage of various e-payment methods in Nigeria has significantly increased over the course of the years, but the impact of this trend have not been fully transferred to the country’s economy.

This study’s findings have policy implications because they provide empirical evidence of the positive effects of e-payment systems on the Nigerian economy, as measured by their performance ratio. Additionally, the study’s findings suggest that encouraging the use of electronic money could lead to increased government spending on internet security, reducing the prevalence of fraudulent activities in the country. The importance of this study also lies in the fact that it promotes an understanding of the electronic payment system as the most expedient and risk-free means of conducting financial transactions. The relevance of this study lies in the fact that, due to its originality, its findings may have an effect not just in Nigeria but also elsewhere around the world. The research work is sectionalized into five sections. Section one dwells on background to the research work, section two deals with the review of related literatures on the debate on the role of transaction settlement in economic growth. Section three focused on research methodology that forms the basis of analysis, while section four presents results and discussion of findings and section presents policy implication, conclusion, recommendations and appendixes that demonstrates result of analysis.

Conceptual Review

To critically understand the subject matter under review, it imperative we conceptualize the following key terms:

Economic Growth: When comparing one time period to another, economic growth can be defined as an increase in an economy’s overall capacity to produce goods and services. It is possible to evaluate it using either nominal or real (that is, inflation-adjusted) terms. It is also possible to view it as an overall increase in an economy’s capacity to produce the things it needs to survive.

Cashless Policy: The ability to conduct transactions without the use of banknotes is referred to as a cashless policy. It is a policy implemented by the Central (Apex) Banks to reduce the amount of physical cash in circulation, thereby encouraging the use of electronic platforms for goods and services settlement or payment.

Gross Domestic Product (GDP): The amount of money that can be spent on all finished goods and services made in a country in a certain amount of time (usually one year). Most of the time, the gross domestic product (GDP) is used to measure how the economy is doing. It shows how much all goods and services produced during a certain time period were worth in dollars.

Electronic Payment (e-payment): This is a way to buy things or pay for services without using cash or checks.

Monetary Policy: This is what the government or the central bank does to change how much money and credit is available, how much they cost, and how they are used.

E -Payment Systems and the Nigerian Economy

The effectiveness of monetary policy is significantly impacted by the use of electronic payment systems. The two are interwoven, and the growth of e-payment systems in Nigeria plays a crucial role in the efficacy of monetary policy in Nigeria. Both of these things are intertwined. It is possible for the influence of monetary policy in a country to be impacted by the widespread adoption of electronic payment systems since these systems play a crucial role in determining how quickly money circulates.

In order to have an effect on the amount of money available in the country, monetary policy makes use of a variety of tools. Without well-developed payment systems, financial institutions will be forced to keep a larger reserve of money from the central bank in order to maintain and manage their liquidity, which will put a damper on their ability to spend and lend money. This, in turn, causes monetary policy impulses to be weaker than intended since the purpose of controlling money supply and flow in the economy is not as effective as it was supposed to be. Once payment systems in a nation have been established and reached a particular level, their influence on monetary policy is determined not only by efficiency alone but also with reference to the velocity of money. This is the case when payment systems in the nation have reached the given threshold. Improvements in the effectiveness of electronic payment systems lead to improvements in the velocity of money in circulation. The velocity of money in circulation refers to the average frequency with which money is spent within a specified time period and relative to a given money supply. In Nigeria, the most common form of electronic payment is the use of a payment card. It gives customers access to the money that is stored in their respective bank accounts. The use of debit cards contributed $983 billion more to the economy, according to the findings of a study that was carried out by Mark (2016) on the effect that card payments have had on the economy. The research covered 56 nations throughout the period of time from 2008 to 2013, and it was completed during this time period.

Numerous scholarly debates have been proposed to analyze the significant of ARDL co-integration to determine long/short term relationship that exist between variables and difficulty of quantifying intent in cutting-edge technological contexts. Pesaran et al. (2001) created the ARDL limits testing strategy as a co-integration method for determining whether or not a long-run relationship exists between variables. There are many benefits to using this process, which is relatively new compared to the traditional co-integration testing. First, it doesn’t matter if the series are I(0) or I(1); the method can still be applied to them. Second, a linear adjustment of the ARDL bounds testing can yield the unrestricted error correction model (UECM). The dynamics of this model occur both in the short and long term. Third, the empirical results prove that the method is effective and reliable, even for low-sample sizes. The ARDL model has been frequently used in studies on the long- and short-term relationship between variables particularly as it concerns economic growth.

For instance, Hasan, Tania, & Heiko (2012) used data from 27 different European markets between 1995 and 2009 to look into the link between retail payments and economic growth. Their study looked at the years 1995–2009. The switch from paper to electronic retail payments drives overall economic growth and is good for the real economy, the study’s results show. They are in favour of policies that will help people switch quickly to electronic payment tools that are both efficient and standardised.

Manwa (2015) examined the effect of trade liberalization on the economic growth of the five Southern African Customs Union (SACU) countries of Botswana, Namibia, South Africa, Swaziland and Lesotho through the ARDL Bounds testing method to co-integration for the period of 1980 to 2011. The study utilized fixed–effects panel data estimations as well for testing the strength of empirical findings among the five countries. The results revealed that in the case of Lesotho, Botswana, Swaziland and Namibia, liberalization of trade measured through trade ratios, tariffs, the real effective exchange rate and adjusted trade ratios exerted an insignificant impact on economic growth.

Similarly, and utilizing the ARDL methodology on time series data from 1971 to 2013, Qazi (2015) examined the effect of financial and trade liberalization on economic growth in Pakistan. Based on the findings of the ARDL model, the long-run association was present in all models. The findings revealed that capital stock, financial liberalization index (banking and stock market) and labour force representing skills were positively linked to economic growth. The results further revealed that de facto financial openness index and trade openness had negative impacts on growth. In another similar study,

Dabel (2016) used the Autoregressive Distributed Lag (ARDL) method to co-integration and data from 1986 to 2015 to investigate the relationship between trade openness and economic growth in Ghana. Based on Composite Trade Index (CTI), a new trade openness measure developed by the author, openness to trade had a positive and significant impact on economic growth. Furthermore, the results revealed that real effective exchange rate, labour force, foreign direct investment (FDI) and the capital stock had positive and significant effects on economic growth. However, inflation exerted a negative and significant impact on economic growth. The result of the Granger causality test between trade openness and economic growth showed a unidirectional causality from trade openness to economic growth.

Yusuf (2016) looked into how Nigeria’s cashless policy and the country’s growing economy from 2008 to 2015 are related. In this study, the Ordinary Least Square (OLS) method was used, and the results showed that point-of-sale (POS), mobile, and web payments all have a positive and significant effect on the rate of economic growth in Nigeria. According to the study’s results, when customers use non-cash payment methods, the inflation rate will go down, foreign direct investment will go up, government revenue will go up, and unemployment will go down. All of these things contribute to Nigeria’s growth.

In another related study, Moyo, Nwabisa, & Hlalefang (2017) investigated the long run nexus between trade openness and economic growth in Ghana and Nigeria using the ARDL model from 1980 to 2016. The results revealed the presence of a long-run relationship among the variables for both nations. Furthermore, the findings showed that trade openness exerted a positive and significant effect on economic growth in Ghana. However, openness to trade had a negative and insignificant impact on economic growth in Nigeria. On the same subject, Moyo and Khobai (2018) investigated the nexus between of trade openness and economic growth for 11 Southern African Development Cooperation (SADC) countries of Botswana, Madagascar, Mauritius, Namibia, Swaziland, Zambia, Lesotho, Malawi, Mozambique, South Africa and Tanzania over the period of 1990 to 2016 using the ARDL Bounds test method and Pooled Mean Group (PMG) model. The findings showed that trade openness exerted a negative impact on economic growth in the long-run.

Likewise, Keho (2017) used the ARDL Bounds test to co-integration and the Granger causality test of Toda and Yamamoto to investigate the impact of trade openness on economic growth in Cote d’Ivoire for the period of 1965 to 2014. The results showed that trade openness exerted positive impacts on economic growth in both the short-run and the long-run.

Saidi did research in 2018 on how e-payment technology has changed how well banks in developing economies do their jobs. The research was done using an ex post facto design, and the random panel regression model was used as the main way to analyze the data. Since it was found that bank performance doesn’t match up with autoregressive and random walk processes, investors shouldn’t worry about how banks have done in the past. Instead, they should worry about the resources that banks are offering now.

Researchers Iluno, Farouk, & Saheed (2018) looked into how electronic banking products and services affect how happy customers are with their bank. A frequency distribution table and multiple regression analysis were used to figure out what was going on. The results of the study showed that both electronic banking services (EBS) and electronic banking products (EBP) have a big and positive effect on customer satisfaction (CS) in the Nigerian state of Kaduna. So, it was suggested that the Central Bank of Nigeria (CBN) come up with a policy framework that will improve the way e-banking works by making policies that focus on customer satisfaction. Based on what was found, this was the best thing to do. Also, information technology providers and financial institutions should work together to make service delivery technology that is easy to use, safe, not too complicated, and efficient. This will increase customer satisfaction.

Ravikumar (2019) looked at the effects of digital payment methods on the growth of the Indian economy between 2011 and 2019. In the study, the ordinary least squares (OLS) regression method and the auto-regressive distributed lag (ARDL) co-integration method were used. According to the results, the use of digital payment methods has a big effect on the rate of economic growth in the short term, but it has no effect on the rate of economic growth in the long term. The Bank for International Settlements recently updated their survey, which included data from 95 countries all over the world. This led to the release of another in-depth survey about the growth of electronic money, mobile payments, and payments made over the internet. This survey was mostly about how innovations affect markets and less about how they can be used for technical purposes. People in each country who took the survey were asked for their information and data, which were then used to make comparison tables about how innovative products and systems could be used. (International Bank for Settlements, 2004) The survey’s data were collected at the end of 2002 or in 2003. It looked at plans that were being thought about, tested, or put into place.

Afaha (2019) looked into the link between electronic payment systems and economic growth by looking at monthly data from 2012 to 2017, which covers the years in question. The autoregressive distributed lag regression (ADLR) method was used to do the analysis. The results show that there is a strong link between the use of electronic payment systems and the growth of the real gross domestic product (GDP).

Moawad, (2019) investigated financial development and economic growth using ARDL Model. This article compares and contrasts the financial sector growth and overall economic development in France and Malaysia to test for the existence of such a correlation and to establish the direction in which it runs. In this analysis, we employ the auto-regressive distributed lags (ARDL) model as our econometric framework. Finding a long-term correlation between financial sector growth and economic expansion in the two countries under examination is the study’s primary finding.

Menegaki (2019) interrogates ARDL Method in the Energy-Growth Nexus Field; Best Implementation Strategies as well as those in other “X-variable-growth nexus” studies like the tourism-growth nexus, the environment-growth nexus, and the food-growth nexus, have relied heavily on the autoregressive distributed lag model (ARDL) bounds test approach to determine whether or not two variables are co-integrated. As a result, other researchers are often left scratching their heads over the proper order of events in an ARDL technique and the most effective paradigms for putting them into practice. This paper provides a thorough overview of the ARDL technique and makes recommendations for what should be done before and after the operation in terms of investigating causation and conducting a robust analysis.

Flowing from the above, Alotaibi & Al-Rabee (2023) argued that the only metric that calculates the rise in “real” national income over a prolonged time period is the “Gross National Product”. This is because Gross National Product (GNP) per capita metric evaluates the long-term growth of individual incomes. The degree to which individuals receive material items and social benefits may be thought of as a measurement of their level of well-being. Indicators of social well-being that takes an individual’s fundamental needs into consideration such as point-of-sale (POS), mobile, and web payments impact positively on national economic growth.

Consequently, the significance of e-payment system during covid-19 pandemic was interrogated by Purwanto, Sjarief, Dawan, Kurniawan, Pertiwi, & Zahra, (2023), they argued that digital payments system such as Electronic money, Internet banking, SMS banking, and mobile banking played vital role during pandemic crisis and rise in the use of this trend is expected to continue because it contributed significantly to the economy. The authors claimed that mobile devices, such as smartphones, have revolutionized payment methods, including digital payments, has spread to more than 60% of developing nations. However, not to completely change the traditional (cash payment) system.

By adopting the ARDL model, the hypotheses is formulated as follows:

H01: Electronic payment system has no significant impact on gross domestic product in Nigeria

H01: Electronic payment system has no significant impact on business growth in rural areas in Nigeria

H01: There is no causality relationship between e-payment systems and economic growth in Nigeria.

METHODOLOGY

For the purposes of this investigation, one state was chosen to represent each of Nigeria’s six different geopolitical zones (for a detailed map analysis, see figures 1–6 in appendix). The quantitative method was utilized, and structured questionnaires were used to solicit information from the respondents. Quarterly and Annual data for the e-payment statistics was obtained from the Central Bank of Nigeria statistics (2022), and the data for the real gross domestic product was obtained from the Central Bank of Nigeria Statistical Bulletin (2022). Using three phase multistage random sampling, a total of 600 respondents were selected as study participants from across all six geopolitical zones (for a map analysis, see figures 1–6. To test the reliability of the instrument, a test-retest method was adopted. Thirty (30) copies of the questionnaire were distributed to target population outside the scope (State sampled) of study. After some days, the instruments were collected and re administered the second time. The questionnaire distributed were completed and returned. Cronbach Alpha was used to test the reliability of the instrument. At 0.74 and above, the instrument was considered as having internal consistencies.

In this study, statistical figures are provided regarding the connection between electronic payment (e-payment) systems and the expansion of the country’s economy in Nigeria. Annual Data for Nigeria on the Values of Various Payment Systems were Analysed Using the Autoregressive Distributed Lagged Regression (ARDL) Method Covering the Period of 2012–2022, the Study Made Use of Map Analysis for Areas of Sampling for Interviews, Both Augmented Dickey Fuller (ADF) and Philips Perron (PP) Units Root Test In order to validate the data that were utilized, a results test was performed as a pre-test, and a co-integration test was performed as a post-estimation test. The value of transactions carried out with automated teller machines (ATM), mobile payments (MOP), point-of-sale terminals (POS), and web payments (WEP) were considered independent variables, whereas real gross domestic product (RGDP) served as the dependent variable in this study.

The Wald test, known as the F statistic, served as the foundation for the ARDL-bound test. Under the assumption that there is no co-integration between the variables, the asymptotic distribution of the Wald test will not follow the standard form. Pesaran et al. (2001) provide the co-integration test with two important variables to use in its interpretation. The lower critical bound makes the assumption that all of the variables have the value I (0), which indicates that there is no co-integration relationship between the variables that are being looked at. The upper bound is based on the assumption that all of the variables are I (1), which indicates that there is co-integration between the variables. If the computed F-statistic is higher than the upper bound critical value, then the null hypothesis H0 is rejected, and it is determined that the variables are co-integrated.

If the F-statistic is less than the lower bound critical value, then it is impossible to reject the null hypothesis that H0 holds true (there is no co-integration between the variables). When the computed F-statistics lie between the lower and upper bounds, then the results cannot be definitively said to be either positive or negative. When compared to other methods of co-integration, the limits test method of co-integration offers a number of econometric benefits, some of which are as follows: It is assumed that every variable in the model is an endogenous variable. The bounds test method for co-integration is being applied regardless of the sequence in which the variable was integrated. There could be an integrated first order of I (1) or (0). Either one is possible.

The coefficients of the model in both the short run and the long run are computed at the same time.

In order to determine whether or not there is a causal relationship between the two variables, a Granger causality test was performed. In other words, it is used to determine whether the independent variable is responsible for the cause of the dependent variable or whether the dependent variable is responsible for the cause of the independent variable. In other words, it is used to test which of these two scenarios is true. As a result, this relationship might either be one that is un-directional or one that is directed. In this particular scenario, we want to determine whether or not there is a causal connection between the level of GDP and each of the explanatory variables. Because of this, every instance of this causality involves two separate causes and effects. If we look at it from a mathematical perspective, GDP = f (ELP).

Model Specification

The functional relationship is stated as:

𝑅𝐺𝐷𝑃 = ∫(𝐴𝑇𝑀, 𝑀𝑂𝑃, 𝑃𝑂𝑆, 𝑊𝐸𝑃)

This can be econometrically written as

RGDPt = β0 + β1ATMt + β2MOPt + β3POSt + β4WEPt + µt ………… (1)

Where RGDP – Real Gross Domestic Product

ATM – value of transactions using automated teller machine

MOP – value of transactions using Mobile Payment

POS – value of transactions using Point of Sale

WEP – value of transactions using Web Payments

b0, b1 … b4 are parameters

β0 = intercept

µ = Error term

However, an ARDL representation of equation (1) above is formulated as follows:

Where X is a vector of all the right-hand side variables in equation (1); i = 1, 2, 3…P; j = 1, 2, 3 …h; and θ= 0, 1, 2, …, q.

RGDPt = β0 + RGDPt-1 + ∆ATMt-1 + ∆MOPt-1 + ∆POSt-1 + ∆WEPt-1 + µ ……………………..(2)

Equation 2 above can be simplified as follows.

RGDPt = β0 + β1RGDPt-1 + β2ATMt-1 + β3MOPt-1 + β4POSt-1+β5WEPt-1 + µt …………………………..(3)

To know the value of this impact (impact of electronic payment Systems on Nigeria’s economic growth) in percentages the values in the model was logged. Analysis based on the reports from the five hundred and seventy-six (576) questionnaires retrieved.

RESULTS AND DISCUSSION

The ADRL results analysis starts with the respondents’ sociodemographic variables. Following the presentation of demographic information, the research moves on to the measurement of the ADRL model. The emphasis at this stage is on testing the hypotheses developed throughout the investigation. The ADRL model evaluation entails investigating the interactions between constructs and determining the degree and importance of these associations. This approach enables the evaluation of hypothesised paths as well as the determination of the impact of each component on the dependent variable.

Age, gender, educational status, and occupation are among the socioeconomic characteristics of the respondents studied. According to the table, 13.4% of all respondents are under the age of 20, 31.3% are between the ages of 21 and 25, 22% are between the ages of 26 and 30, 18.8% are between the ages of 31 and 35, and 14.6% are over the age of 35. This indicates that the respondents are adults, and so should have knowledge of the influence of electronic payment systems on Nigerian economic growth, as well as an understanding of the impact of their contribution on the subject of inquiry. The gender socio-demographic characteristics results show that the bulk of the respondents questioned were males (70.1%), but a good number of the respondents were females (29.9%), implying that the research is not gender biased and that both genders were represented in the analysis. Education is a critical factor of any research since it impacts the dependability of results generated from a primary source; this research has taken appropriate efforts in obtaining respondents to ensure that the respondents are educated enough to answer the questions posed by this research. According to the findings, just 16.8% of the total respondents had no formal education, while the remaining respondents all have an educational certificate (see table 1-3 in appendix).

Test of Hypotheses

Hypothesis 1

Pre-Test

Unit Root

The dependent variable (RGDP) was also stationary at first order one (I(1)) when the unit root test results using Phillips Perron (PP) were analyzed. The results of the unit root test indicated that all of the independent variables (ATM, POS, Mobile, and WEP) are stationary at order one (constant) (I(I)). As a consequence of this, the order of integration does not proceed past the first differential; hence, ARDL was determined to be an effective modeling technique.

Source: Author Computation 2023

ARDL Bound Test

The outcome of the ARDL model can be found in the table that can be found below. The findings make it abundantly clear that the adoption of electronic payment systems in Nigeria has a sizeable effect on the country’s GDP. According to the findings, the adoption of electronic payment systems does not have an immediate impact on the expansion of the national economy. In other words, such an impact will not be seen in the near term, but its effect will be seen in the long run. The findings make it abundantly clear that the value of the F-statistics, which comes in at 12.09, is higher than the upper bound critical values – I(1) at each and every level of statistical significance. This finding substantiates the existence of a significant significance in the link between the dependent and independent variables, as well as a positive long-run association inside the model.

Short-Run Post-estimation

Table 4 further presents the findings of this investigation. The fact that the coefficient of the ARDL short run adjustment mechanism (CointEq (-1)) in the table stood at -7.721, which indicates that 7.72% of the model’s disequilibrium is adjusted monthly, can be seen by looking at the table. This indicates that for every loss in the investment on electronic payment system, there exists a rate of return on investment on a short run (lag one) annually of 7.72%, and this is also relevant to the growth of RGDP in a short run.

Hypothesis II

To achieve this objective, Chi-square statistical techniques was adopted to evaluate the questions pose by the research in the cause of this study and thereby draw inferences on the results generated. Chi-square rule stated that if the calculated chi-square is greater than the chi-square table value (X2cal> X2Tab) rejects the null hypothesis and accept the alternative hypothesis but if the calculated chi-square is less than the chi-square table value (X2cal < X2Tab) rejects the alternative hypothesis and accept the null hypothesis. For this analysis Statistical Package for Social Sciences (SPSS) version 23 was adopted for accuracy and efficiency means of calculation.

Chi-Square Descriptive Table

Source: Authors Computation 2023, using SPSS 23.

The results reveal a chi-square value of 339.781 with a significant value of 0.000, indicating that electronic payment systems have a considerable impact on business growth in rural Nigeria (0.000 < 0.05). We reject the null hypothesis and find that “Electronic payment system have considerable impact on company growth in rural areas in Nigeria”. The interview question also demonstrates that while few marketers have used electronic payment systems, most bulk purchasers prefer them over cash.

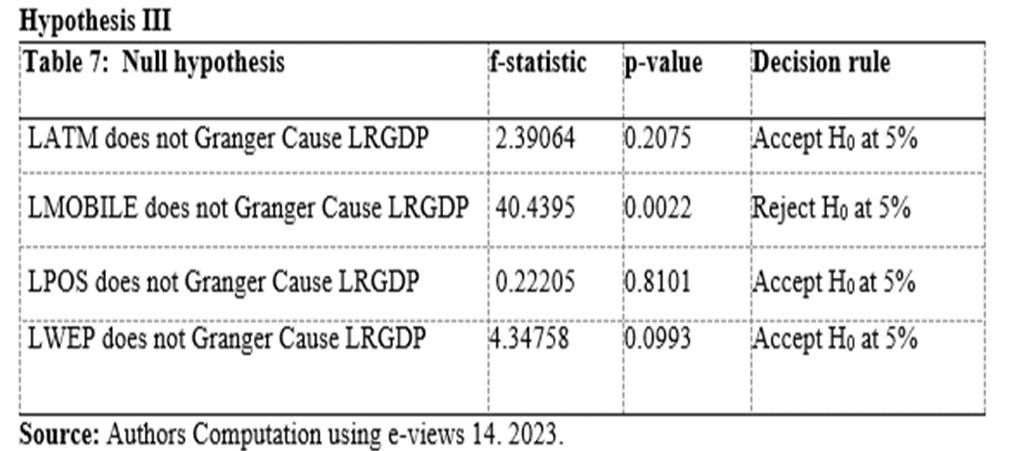

The Granger causality test findings for Hypothesis 3 are presented in the table above. The Granger causality test results show that we accept the null hypothesis that the volume of POS transactions does not granger cause real GDP because the probability is greater than 0.05, and we reject the null hypothesis that real GDP granger causes the volume of POS transactions because the probability is greater than 0.05 and the F statistics is also greater than 3. As a result, there is a bidirectional causal relationship between POS transaction values and real GDP. This study shows that changes in the values of POS transactions will have little impact on economic development. The findings also accept the null hypothesis that the value of internet transactions (WEP) does not granger cause real GDP and do not reject the null hypothesis that real GDP granger causes the volume of internet transactions. The value of internet transactions (WEP) and real GDP have a bidirectional causal relationship. This result means that changes in the value of internet transactions will have little impact on economic development and vice versa. The results reject the null hypothesis that the number of mobile transactions does not granger cause real GDP because the probability is 0.05, but we fail to reject the null hypothesis that the amount of mobile transactions granger causes real GDP. The volume of mobile transactions and real GDP have a unidirectional causal relationship, which means that changes in the volume of mobile transactions cause major changes in economic growth but not vice versa. Because the likelihood > 0.05, the results failed to reject the null hypothesis that the amount of ATM transactions granger causes real GDP. The findings suggest that changes in ATM transaction volume do not correlate to economic growth in Nigeria, and vice versa.

The Autoregressive Distributed Lagged Regression (ARDL) for Hypothesis I shows a positive and direct link between real GDP and the electronic payment system (the value of ATM transactions, POS transactions, mobile transactions, and internet (WEB) transactions). In the same way, the results for Hypothesis II show that electronic payment systems have a big effect on business growth in rural Nigeria. These results agree with what Zandi (2016) found, which was that e-payment was good for economic growth. However, they disagree with what Afaha (2019) found, which was that e-payment systems had a strong negative effect on economic growth in Nigeria. The Johansen co-integration test for Hypothesis 1 shows that real GDP, ATM transaction value, mobile transaction value, and internet (WEB) transaction value are all linked in the long run. The result fits with what Mamudu and Udo, (2019), postulation. Using the vector error correction model, a short-term analysis of Hypothesis 1 shows that the variables real GDP, POS transaction value, ATM transaction value, mobile transaction value, and internet transaction value all move toward a long-term equilibrium point. Using the vector error correction model, the short-run analysis shows how real GDP, the number of POS transactions, the number of ATM transactions, the number of mobile transactions, and the number of internet transactions all move toward the long-run equilibrium position.

This finding is in consonance with the finding of Mamudu & Udo, (2019) who found that POS, ATM, mobile, and Internet transactions in Nigeria have a strong short-term equilibrium relationship with real GDP. These results are similar to what they found. Ravikumar et al. (2019), who found a strong link between epayments and economic growth in the short term, came to the same conclusions. The chi-square analysis shows that electronic payment systems have a big effect on the growth of businesses in Nigerian rural areas. The results show that, even though many merchants haven’t switched to electronic payment systems, it’s impossible to overstate how important they are. Even though there is a positive and direct link between e-payment systems and economic growth, the data show that it doesn’t really help Nigeria’s economy grow. This could be because people in rural areas are afraid to use new technology because of online fraud. The granger causality test for Hypothesis III shows that the value of POS, ATM, and internet (WEB) transactions is linked to real GDP in both directions. The results show that the value of POS, ATM, and mobile transactions does not affect real GDP at the 5% level. This means that there are two ways in which each variable affects GDP and vice versa. Still, there is a one-way causal link between the number of mobile transactions and real GDP. This means that changes in the number of e-payment system transactions will cause a big change in economic growth, not the other way around.

Implication

The implication of findings is that electronic payment contributes significantly to Nigeria economic growth due to the usage of various e-payments system. However, most of the rural settings that host 70% population have no access to internet and are not exposed to e-payment system which of which if the government fails to invest heavily in its internet in the rural areas and embark on intensive campaigns to increase awareness and incentives to the use of non-cash methods such as e-payment systems, it will experience a fatal blow to its economic growth this is because findings reveals that there is a unidirectional causal relationship between the volume of mobile transactions and real GDP.

Limitation of the Study

The research work focuses on the nexus between e-payment and economic growth in Nigeria between 2012-2022 with emphasis on the value of transactions carried out with automated teller machines (ATM), mobile payments (MOP), point-of-sale terminals (POS), and web payments (WEP), other contributory factors to Nigeria economic growth such the role of the banking system and availability of networks for transactions. However, crude oil export, transportation, education/health sector, telecommunication and agricultural products amongst other were not covered in the research. Further studies might be carried out for a long- and short-term impact of the aforementioned on Nigeria Economy. This notwithstanding does not affect the findings of this study.

CONCLUSION

The findings show that that rural business benefits from electronic payment systems. The causality results show a unidirectional causal relationship between mobile transaction volume and real GDP, indicating that changes in mobile transaction volume would significantly affect economic growth. The study concludes that e-payment systems have significant impact on economic growth. The report also links e-payment systems to Nigeria’s economic growth. So, the government should implement policies and programs to expand e-payment adoption, which will raise the number of e-transaction, bring more people into the formal sector, and boost trade and company efficiency and efficacy, promoting economic growth. E-payment systems have a good association with economic growth; thus, the government should prioritize technology and internet infrastructure to make e-payment channels easier and cheaper for the public. Decades of poor security investment and spending in Nigeria have hindered e-payment system adoption. So, Nigeria must aggressively invest in internet security to create a firewall against fraud and instill confidence in the populace to use new payment systems, which would increase aggregate consumption and economic growth. The limited penetration of e-payment systems in Nigeria explains their bidirectional effects on economic growth. Hence, campaigns to educate and encourage non-cash means like e-payment systems will assist the system and economy thrive.

ACKNOWLEDGEMENT

The authors are very grateful to the polytechnic for Tetfund sponsorship and thank the entire respondent who participated in this research work and the CBN for publishing the necessary information used for this work.

REFERENCES

- Acha, I. A. (2017). Cashless Policy in Nigeria: The Mechanics, Benefits and Problems. Innovative Journal of Economics and Financial Studies, Vol. 1 (1), 28-37.

- Afaha, J. S. (2019). Electronic payment systems (e-payments) and Nigeria economic growth, European Business & Management, 5 (6), 77-87.

- Akanni, Bola (2022), Impact of Electronic Payment Systems on Nigerian Economic Development Bingham University Journal of Accounting and Business (BUJAB) Pp 206 – 213.

- Akintaro, S. (2012). Going Cashless. IT & Telecom digest, online Magazine

- Alotaibi, M. N., Al-Rabee, A. A. (2023) The Role of Najran University in Achieving Economic Development in the Region from the Point of View of Faculty Members. Intern. Journal of Profess. Bus. Review. V.8, n. 7. Doi: https://doi.org/10.26668/businessreview/2023.v8i7.2709

- Bank for International Settlements (2004), Survey of developments in electronic money and internet and mobile payments (March 2004)

- Central Bank of Nigeria Statistical Bulletin (2022). Annual Statistical Bulletin 2021 https://www.cbn.gov.ng/documents/statbulletin.asp. Published 5/23/2022 retrieved on 1st March, 2023.

- Central Bank of Nigeria Statistical Bulletin (2023). Annual Statistical Bulletin 2022 https://www.cbn.gov.ng/rates/RealGDP.asp retrieved on 1st March, 2023.

- Central Bank of Nigeria Statistics (2023). E-Payment Statistics https://www.cbn.gov.ng/Paymentsystem/ePaymentStatistics.asp retrieved on 1st March, 2023.

- Dabel, I. (2016). Trade openness and economic growth: Evidence from Ghana. An Unpublished Master of Philosophy Degree in Economics of the University of Cape Coast.

- Iluno, B., Frank, S. & Saheed, W. (2018). Impact of accounting information system on the financial performance of selected FMCG companies, Asian Journal of Applied Science and Technology, 2(3), 8-17.

- Keho, Y. (2017). The impact of trade openness on economic growth: The case of Cote d’Ivoire. Cogent Economics & Finance, 5(1), 1-14. Available at: http://dx.doi.org/10.1080/23322039.2017.1332820

- Mamudu, Z. & Udo, G. G. (2019). Cashless policy and its impact on the Nigerian economy, International Journal of Education and Research, 7 (3), 111-132.

- Manwa, F. (2015). Impact of trade liberalisation on economic growth: The case of the Southern African Customs Union (SACU) countries. PhD Thesis, Southern Cross University, Lismore NSW.

- Menegaki, A. (2019) The ARDL Method in the Energy-Growth Nexus Field; Best Implementation Strategies. Economies 2019, 7(4), 105; https://doi.org/10.3390/economies7040105

- Moawad, R.R (2019) Financial Development and Economic Growth: ARDL Model. International Multilingual Journal of Science and Technology (IMJST) ISSN: 2528-9810 Vol. 4 Issue 7, www.imjst.org IMJSTP

- Nigerian Population Commission (NPC) (2022) https://nationalpopulation.gov.ng/

- Nino M. (2018) Development of electronic payments in Georgia. Business Academy of Georgia, Georgia Republic. Economics And Culture 15(2), 2018 DOI: 10.2478/jec-2018-0021

- Onyeagba, J. B. (2015). Impact of Cashless Banking System of Payment on Entrepreneurial Activities in Anambra State. Vol. 1 (2).

- Opeyemi Quadri (2022) 6 Geopolitical Zones in Nigeria and Their States Last updated on December 16th, 2022, at 05:50 pm retrieved on 28th February, 2023

- Oyewole, A., El-Maude, E. A., Abba, I. & Onuh, J. (2013). The Impact of Internet Banking on Performance and Risk Profile: Evidence from Australian Credit Unions, The journal of international banking regulation, 6(20), 23 – 45

- Purwanto, E., Sjarief, R., Dawan, A., Kurniawan, S., Pertiwi, N., Zahra, N. (2023) The Acceptance of Electronic Payment Among Urban People: An Empirical Study of the C-Utaut-Irt Model. Intern. Journal of Profess. Bus. Review. V.8, n. 7. Doi: https://doi.org/10.26668/businessreview/2023.v8i7.2909

- Qazi, M. A. H. (2015). Impact of economic liberalization on economic growth in the case of Pakistan. An Unpublished Doctor of Philosophy Degree of the Faculty of Economics & Administration, University of Malaya, Kuala Lumpur,

- Ravikumar T, S. B. (2019). Impact of Digital Payments on Economic Growth: Evidence from India, International Journal of Innovative Technology and Exploring Engineering, 8 (12), 70 – 75.

- Saidi, W. (2018). Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure, Journal of Financial Economics, 3 (9), 305-360.

- Schumpeter, J.A. (1911/1934) The Theory of Economic Development. Cambridge, MA: Harvard University Press

- Schumpeter, J.A. (1942) Capitalism, Socialism and Democracy. New York: Harper & Row

- Schumpeter, J. A. (2002). New Translations from Theorie der wirtschaftlichen Entwicklung. American Journal of Economics and Sociology 61: 405–37

- Slozko, O. & Pelo, A. (2014), The Electronic Payments as a Major Factor for Further Economic Development, Economics and Sociology, Vol. 7, No 3, pp. 130- 140. DOI: 10.14254/2071-789X.2014/7-3/13