Effect of Board Gender Diversity on Financial Performance of Quoted Deposit Money Banks in Nigeria

- John Abuh Oyidih

- 442-456

- Dec 18, 2023

- Finance

Effect of Board Gender Diversity on Financial Performance of Quoted Deposit Money Banks in Nigeria

John Abuh Oyidih

Nasarawa State University Keffi Nigeria

DOI: https://doi.org/10.51244/IJRSI.2023.1011037

Received: 31 October 2023; Revised: 08 November 2023; Accepted: 15 November 2023; Published: 18 December 2023

ABSTRACT

The monitoring role of the board of directors is a critical corporate governance and control mechanism, especially in countries like Nigeria where external control mechanisms are less well developed. This study examines the effect of gender diversity on financial performance of listed deposit money banks in Nigeria. The population comprises of all the deposit money banks in Nigeria while thirteen (13) listed deposit money banks were sampled, based on their being listed on the Nigerian Exchange Limited from the period 2010 to 2021. The data was analysed using Shapiro-Wilk Normality, Pearson correlation, Heteroskedasticity Breusch-Pagan Test, Hausman specification test and Breusch-Pagan Lagrangian Multiplier Test while hypotheses were tested using robust random effect regression model. The results show that gender diversity (GD) has a significant positive effect on financial performance of listed deposit money banks in Nigeria for the period under review. The study recommends that the owners and regulators of deposit money banks in Nigeria should increase the numberof women gender on their boards to about 45% to enhance their financial performance.

Keywords: Gender Diversity, Return on Assets, Listed Deposit Money Banks, Financial Performance

INTRODUCTION

Board diversity as a mechanism of corporate governance is an age-old term and refers to the demographic characteristics of a board of directors. Diversity may be viewed in various ways but this study focuses on diversity from the angle of the gender proportion on the board of directors. Corporate governance, to which board diversity is one of the mechanisms, is as old as the history of modern corporations. Corporate governance can be defined as that responsibility and accountability that companies owe their diverse stakeholders. It is the system by which companies are directed and controlled (Cadbury Committee, 1992). According to Jenkinson and Mayer (1992), corporate governance refers to the processes and structures by which the business and affairs of institutions are directed and managed, in order to improve long term shareholders’ value by enhancing corporate performance and accountability, while taking into account the interest of other stakeholders. The pride of place that corporate governance currently enjoy stem from the recent failures and scandals of some world class corporations like Enron, WorldCom, Lehman Brothers, Polaroid, Swiss Air and Woolworths just to mention a few.

There have been several studies on corporate governance and financial performance most of which use mechanisms like board size, number of board meetings, independence of the board, among others but only a few used board diversity. Some of such prior studies that used other mechanisms aside from board diversity are Kajola, (2008), Uwuigbe, (2011) Akpan and Riman, (2012), Joshua, et al (2013), Obetan, et al (2014), Adekunle and Aghedo, (2014) and Ogege and Boloupremo, (2014). This paper uses board diversity demographics with particular emphasis on gender and return on assets as financial performance proxy. The results of past research work in this area are as diverse as the number of studies carried out thereby creating a need for more study.

The key issue addressed by this current study is whether gender diversity of the board of listed deposit money banks in Nigeria affect their financial performance. For board composition, the recommended best practice is to have a fair representation of the female gender on the board (Nnabuife, et al, 2015). According to Nnabuife, et al (2015), two approaches are used to have a fair representation of women on the board which are legislative action (Spain, Norway, Iceland, Italy, etc) and voluntary measures (Australia, Malaysia, U.K., Hong Kong. Does this said recommended best practice on fair representation affect financial performance? This is part of what the paper attempts to answer.

The null hypotheses formulated for testing in this study is that the proportion of female directors on the board of listed deposit money banks in Nigeria has no significant effect on their financial performance.

LITERATURE REVIEW

Conceptual Literature

In this section of the paper, we define and review the concepts of board diversity and financial performance. Before the conceptual discussion on board diversity however, there is a need for an appreciation of the concept of corporate governance, the ambit of which, board of directors and consequently board (gender) diversity falls. The term corporate governance is a relatively new one both in the public and academic debates although the issues it addresses have been around for much longer dating as far back as Adam Smith’s (Wealth of Nations) time of 1776 (Bocean& Barbu, 2007). Corporate governance is the rules, processes or laws by which businesses are operated, regulated and controlled. A well-defined and enforced corporate governance provides a structure that, at least in theory, works for the benefit of everyone concerned by ensuring that the enterprise adheres to accepted ethical standards and best practices as well as to formal laws. According to Council (2007), corporate governance is defined as “the framework of rules, relationships, systems and processes within and by which authority is exercised and controlled in corporations”. It went further to state that “corporate governance encompasses the mechanisms by which companies, and those in control”, are held to account. It concluded that corporate governance influences how the objectives of the company are set and achieved, how risk is monitored and assessed and how performance is optimized,

Another definition of corporate governance was that provided by Imhanze (2015) in an article in the September 2015 edition of the Nigeria Bar,wherein he defined corporate governance as “the framework of rules and practices by which a board of directors ensures accountability, fairness and transparency in a company’s relationship with its all stakeholders (financiers, customers, management, employees, government and the community)”. Additionally, he stated that the corporate governance framework consists of (1) explicit and implicit contracts between the company and the stakeholders for distribution of responsibilities, rights and rewards, (2) procedures for reconciling the sometimesconflicting interest of stakeholders in accordance with their duties, privileges and roles and (3) procedures for proper supervision, control and information flows to serve as a system of checks and balances. Corporate governance can therefore be seen as acting responsibly, fairly and transparently to all stakeholders of a company.

There are several corporate governance characteristics that includes board size, board composition, independence of directors, audit committees, number of board meetings, chief executive officer duality and board diversity, among others. An importanttopic in recent academic literature is that a diversified board engender sound corporate governance observance. Examples include Conger and Lawler (2001). Both the Higgs Review of 2003 and Walker Review of 2009 stressed the importance of board diversity. Board diversity, as a corporate governance mechanism, does not have a uniform definition though matters like gender, race, age, experience, education background, professional qualification, personal attributes, etc are considered as critical features that determine diversity. Board diversity means having people of different attributes on the board of directors. The attribute selected for this study is gender diversity. Gender diversity means the male-female proportion of the board. Gender diversity is the independent variable of this study.

Corporate financial performance could be viewed as the financial returns associated with investments in a given entity. Financial performance and profitability are loosely and interchangeably used to mean one and the same thing. Financial performance is usually a measure of the health and wellbeing of a company. According to Barney (2002) in Gentry and Shen (2010), financial performance is the fulfilment of the economic goals of the firm. In this study, an accounting financial performance measure of return on assets (ROA) is used as proxy for financial performance. Return on assets is the earnings after taxation expressed as a proportion of assets used to generate the profit.

Empirical Review

Findings from prior studies are almost as varied as the number of works thus there are mixed results. In a study by Miller and Triana (2009) that focused on demographic diversity in the boardroom; mediators of the board diversity-firm performance relationship, they found that both board gender and racial diversity are positively related to innovation (in the form of R&D expenditures). Ujunwa, et al (2012) on the other hand found that gender diversity was negatively linked with firm performance while board nationality and board ethnicity were positive in predicting firm performance. One of the peculiarities of that study which this paper seek to address is that it was done in the manufacturing sector while this present work is in the banking sector.

Nganga (2017) found that there exists a statistically significant relationship between board diversity and financial performance of commercial banks in Kenya. All components of board diversity in that study, including gender diversity were all important in enhancing financial performance of commercial banks. With findings similar to the above, in another study by Abubakar, et al (2014) found that gender diversity and board composition have significant and positive influence on firm performance. Gender diversity – as measured by percentage of women on the board and by the Blau and Shannon indices – has a positive effect on firm value and that the opposite causal relationship is not significant (Campbell & Minguez-Vera, 2017). Thus, they concluded that balanced representation between women and men as against the number of female genders on the board should be the main focus. They further stated that greater gender diversity may generate economic growth.

In another study, Erhardt, et al (2003) found that board diversity is positively associated with return on assets and return on investment as financial indicators of firm performance. Their study drew sample from large United States of America corporations. Closely related to the present study is that by Dutta and Bose (2007) in which they found to exist what they called a paradoxical relationship between gender diversity in the boardroom and financial performance of commercial banks in Bangladesh. That study used a small sample size and covered a period of just four years as a result of unavailability of data. This paper covers all the thirteen (13) banks listed on the Nigerian Exchange Limited during the study period which is a longer period of twelve years. Furthermore, though both studies are in emerging markets with some similarities, the former covered banks in Bangladesh while this one is on banks in Nigeria with the individual countries’ peculiarities.

In a research work on commercial banks in Kenya, Ekadah, and Mboya (2009) found that board diversity has no effect on performance of banks in Kenya. While the present work and the above share some similarities, a major shortcoming of Ekadah and Mboya (2009) work which the authors identified and which this work sets out to address is that majority of banks in Kenya have no female directors on their boards. This, they opined may have affected the findings of their study. On the contrary most banks in Nigeria, and for that matter those selected for this study, have female directors on their boards. However, Rose (2007) did not find any significant link between financial performance and female board representation. Similarly, Darmadi (2011) found that accounting and market performance have negative association with gender diversity. Also, Abdullah and Ismail (2017) found that gender diversity is negatively associated with Tobin’s Q and return on assets (ROA).

From these reviews, it is apparent that the findings from previous researchers ranges from negative relationship between gender diversity and financial performance through neutral relationship to positive ones. This present work therefore becomes important because of these varied findings.

Theoretical Framework

There are several theories on corporate governance. The theories include agency, stakeholder, resource dependence and stewardship theories. While this work is underpinned by resource dependence theory, below is a brief explanation of the theories generally. Agency theory is one of the oldest theories in corporate governance studies. It is premised on modern corporations’ model in which ownership is divorced from management where the managers acting as agents of owners are perceived to be self-interested and pursue objectives different from those of the owners. The self-interested motive of Managements lead to under performance. According to Shapiro (2005) some incentives like commissions, bonuses, piece rates, equity ownership, stock options, profit sharing, share cropping, deductibles, etc are used as options to align the agent’s interests with the principal’s objectives.

Resource dependence however look at directors, as corporate governance tool, from the perspective of contributions that directors can offer an organization. The theory opposed the agency theory’s view of the suspicion by the shareholders that the managers will act opportunistically and selfishly. The key contribution of the resource dependence theory, as developed by Pfeiffer and Salancik (1978), is the observation that the board, and in particular its constitution of the non-executive element, can provide the firm with a vital set of resources. Seeing the board as a source of resources presents a good dimension to the board’s role of creating high performance. The stakeholder theory expands on the limitations of agency theory by emphasizing the entire stakeholders as against a narrow focus on owners-managers (principal-agent) relationship. As a typical firm is fundamentally a nexus of stakeholder relationships who hold the tangible and intangible resources needed for the firm’s maintenance, focus should be on these entire stakeholders. Freeman, et al (2004) believed that stakeholder theory begins with the assumption that values are necessarily and explicitly a part of doing business.

Stewardship theory, which is related to the resource dependence theory, postulate motive of executive different from that put forward by the agency theorists. Here, as against the self-interested and self-serving motives of executives under agency theory, stewardship theory emphasizes the pro-organization motives. The theory affirms that the problem of governance may lie not in the self-interest of the executive but rather in the assumptions that distant others (investors and regulators) make as to their self-interested motives. Donaldson and Davis (1991) argue that in agency theory, shareholder interests require protection of incumbency of roles of board chair and CEO while stewardship theory argues that shareholder interests are maximized by shared incumbency of these roles. This study is however underpinned by the resource dependence theory as directors are viewed from their resource supply context.

METHODOLOGY

This study used a longitudinal research design to address the research objective. The design is used to examine the statistical relationship between two or more variables. The population of the study consists of all the listed deposit money banks in Nigeria on the Nigerian Exchange Limited for the period 2010 to 2021 financial years. The sample size of this study comprises thirteen (13) listed deposit money banks in Nigeria. The study employed panel data mainly from secondary sources which are quantitative in nature. The data were obtained from the annual reports and accounts of the quoted banks submitted to the Nigerian Exchange Limited. The technique of data analysis employed by this study is panel multiple regression analysis. The study adopted this technique and ascertained the effect of gender diversity on financial performance of listed deposit money banks in Nigeria. The data was an alysed using STATA 15 and the outcome were used to test the research formulated hypothesis. Various robustness tests were carried out to test the validity of the research result. This included Hausman test to test for the existence of unobservable heteroscedasticity between the explanatory variables.

Financial performance is proxied by return on assets (ROA) which is measured by profit after tax over total assets and as a function of gender diversity. Board gender is measured as a proportion of the number of female board members as a function of the total number of persons on the board. To determine the nature of relationship between female board membership and financial performance, the study used ROA for financial performance and proportion of female board membership for gender diversity. Therefore;

ROA = ƒ(GD)

Econometrically, the above equation is rewritten into a model as follows:

ROAit = β0 + β1GDit+ μit………………………(1)

Where:

β1: parameter to be estimated with a-priori expectation.

β1> 0

ROA = Return on Assets

GD = Gender Diversity

βo = Constant

μ = Error term

i = Firms

t = Periods

Table 1 Variable Measurement

| Variable | Acronym | Type of variable | Measurement | Justification |

| Return on Assets | ROA | Dependent | Profit after tax/Total assets. | Semra et al. (2016), Siti and Hassan (2015) |

| Gender Diversity | GD | Independent | This is the percentage of women on the board of directors. | Enakirerhi and Chijuka (2016), Semra et al. (2016), Siti and Hassan (2015). |

Source: Researcher’s compilation, 2022.

RESULTS AND DISCUSSION

The data of thirteen (13) deposit money banks regarding return on assets (ROA) and gender diversity (GD) were used. The data were analysed with the aid of Stata 15 software using Descriptive Statistics, Shapiro-Wilk Test, Pearson Correlation, Heteroscedasticity test, Hausman Specification Test and robust random effect regression model.

Descriptive Statistics

Table 2 Descriptive Statistics

| Variable | Obs | Mean | Std. Dev. | Min. | Max. |

| ROA | 156 | 0.024 | 0.045 | -0.099 | 0.266 |

| GD | 156 | 20.831 | 10.850 | 0 | 45.450 |

Source: Researcher’s Computation using STATA 15 software

Table 2 shows that return on assets (ROA) has a minimum value of -0.099, a maximum value of 0.266 and a mean value of 0.024 that is within the minimum and maximum indicating a good spread within the period studied. The table also reveals that ROA has a standard deviation of 0.045 that is more than the mean which may signify a high variability in values of data.

Table 2also shows that the gender diversity (GD) has a minimum value of 0, a maximum value of 45.450 and a mean value of 20.831 that is within the minimum and maximum values indicating a good spread within the period studied. The Table also reveals that GD has a standard deviation of 10.850 that is less than the mean which may signify a low variability in data values.

Shapiro-Wilk Test for Normality

Table 3 Normality Test

| Variable | OBS | W | V | z | Prob. Chi2 |

| Residual | 156 | 0.97837 | 2.603 | 2.173 | 0.01488 |

Source: Researcher’s Computation using STATA 15 software

Table 3 above shows the probability value of residual of 0.01 which isnot normally distributed around the mean value. This indicates that one of the basic assumptions of linear regression technique is violated, which according to Gujarati (2003) is corrected using robust regression technique.

Heteroscedasticity test

Table 4: Heteroscedasticity Test

| Type of test | Chi2 | P-Value |

| Heteroscedasticity Test | 43.29 | 0.00 |

Source: Researcher’s Computation Using STATA 15 software

To establish that the data for this study was robust for the model, heteroscedasticity test was carried out. However, the study revealed that data is heteroskedastic; as such the basic linear regression model would not be reliable. This can be confirmed from the heteroskedasticity result in Table 4above which revealed the chi2 value of 43.29 with a p-value of 0.00. In order to correct for this anomaly, the robust linear regression technique was used as suggested by (Hoechle, 2007).

Hausman Specification Test

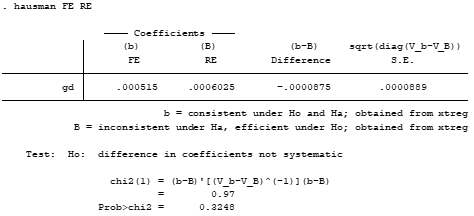

The data for this study is panel and panel data can lead to an error that is clustered and possibly correlated over time. This is due to the fact that each financial firm may have its own entity specific characteristic that can determine its information (i.e. unobserved heterogeneity). This may affect the outcome variable or even the explanatory variables. Hausman specification test was run and the result shows that the random effect model is more appropriate. This can be confirmed from the Chi2 value of 0.97 with a p-value of 0.0.3248 in Table 5 which is not significant at all levels of significance as suggested by (Hoechle, 2007).

Table 5 Hausman Specification Test

| Chi2 | 0.97 |

| Prob. Chi2 | 0.3248 |

Source: Researcher’s Computation using STATA 15 software

Breusch-Pagan Lagrangian Multiplier Test

Table 6 Breusch-Pagan Lagrangian Multiplier Test

| Variable | Chibar2 | P-Value | |

| FL | 138.69 | 0.00 |

Source: Researcher’s Computation using STATA 15 software

Based on the result of Hausman test that supported Random Effect Model (REM) regression, the Breusch-Pagan Lagrangian Multiplier test was conducted to give an insight into an actual test to be carried out between Random Effect Model and Pooled Ordinary Least Square Regression. From the Breusch-Pagan Lagrangian Multiplier test, the chibar2 value of (138.69) and the probability of (0.00) in Table 6 above, therefore, suggests that REM is more appropriate instead of Pooled Ordinary Least Square.

Gender Diversity and Financial Performance using Robust Random Effect Model (REM)

Table 7 below is the robust random effect regression model conducted for the estimation of this model.

| Variable | Coefficients | z-value | Prob. |

| Cons. | 19.936 | 10.27 | 0.00 |

| GD | 37.741 | 2.72 | 0.006 |

| R-sq overall | 0.6409 | ||

| Wald chi2 | 7.42 | ||

| Prob. >F | 0.006 |

Source: Researcher’s Computation using STATA 15 software

Table 7 above indicated that approximately 64% variation of return on assets is predicted by the effect of gender diversity with (Overall R-sq of 0.6409). This indicates that the independent variables are properly combined and used. The wald chi2 value of 7.42 with a P-value of 0.006 signified that the model is fit for the study.

To examine the effect of gender diversity on financial performance of listed deposit money banks in Nigeria, the formulated hypothesis was tested using a robust random effect regression model.

The result also reveals that the z-value of 2.72 and the corresponding p-value of 0.006 shows that gender diversity (GD) has a significant positive effect on return on assets (ROA) of listed deposit money banks in Nigeria for the period under review. Based on this, the null hypothesis which says that gender diversity (GD) has no significant effect on return on assets (ROA) of listed deposit money banks in Nigeria is rejected.

DISCUSSION OF FINDINGS

Gender Diversity and Firm Financial Performance (ROA)

The study reveals that gender diversity (GD) has a significant positive effect on financial performance of listed deposit money banks in Nigeria for the period under review. This implies that a percentage increase in gender diversity increases the performance of quoted deposit money banks in Nigeria. This finding is in line with the a-priori expectation and also in line with the Resource Dependence Theory which underpinned this study. This finding is equally in consonance with the finding of Sener andKaraye, (2014) and Nganga, (2017). Along the same line, just like the findings in this study, Abubakar, et al (2014) found that gender diversity has a significant and positive influence on firm’s financial performance. However, the finding of this present study does not support the findings in Darmadi (2011) who found a negative relationship and Campbell and Minguez -Vera (2007) as well as Rose (2007) which both found no effect of gender diversity on financial performance. Also, Abdullah and Ismail (2017) found that gender diversity is negatively associated with Tobin’s Q and ROA which is at variance with the finding of this study.

CONCLUSION AND RECOMMENDATIONS

An increase in the number of females on the boards of deposit money banks in Nigeria will increase the level of their financial performance. This paper concludes that increasing the proportion of female board members will enhance the financial performance of listed deposit money banks in Nigeria. It is also the opinion of this paper that a significant variability in return on assets (ROA) is predicted by changes in the number of women on the board. According to Campbell and Minguez-Vera (2017) women are known to be diligent and committed in their dealings. Having more women on the board of directors may therefore enhance the financial performance of deposit money banks in Nigeria. Therefore, the number of women on the board must be increased to enhance the financial performance of deposit money banks in Nigeria. On the basis of the finding, this paper recommends that owners and regulators of deposit money banks in Nigeria should substantially increase the threshold for women gender representation on their boards to enhance the banks’ financial performance.

REFERENCES

- Abdullah, S. N., & Ku Ismail, K. N. I. (2017). Gender, ethnic and age diversity of the boards of large Malaysian firms and performance. Journal Pengurusan, 38, 27-40.

- Abubakar, B. A., Garba, T., Sokoto, A. A., &Maishanu, M. M. (2014). Corporate board gender diversity and performance: Evidence from Nigerian stock exchange. An Unpublished PhD Thesis, Department of Economics, Usmanu Danfodiyo University, Sokoto.

- Adekunle, S. A., & Aghedo, E. M. (2014). Corporate governance and financial performance of selected quoted companies in Nigeria. European Journal of Business and Management, 6(9).

- Akpan, E. S., & Riman, H.B. (2012). Does corporate governance affect bank profitability? Evidence from Nigeria. American International Journal of Contemporary Research, 2(7).

- Ali, M., Ng, Y. L., & Kulik, C. T. (2014). Board age and gender diversity: A test of competing linear and curvilinear predictions. Journal of Business Ethics, 125(3), 497-512.

- Barney, J. B. (2002). Strategic management: From informed conversation to academic discipline. Academy of Management Perspectives, 16(2), 53-57.

- Bocean, C. G., & Barbu, C.M. (2007). Corporate governance and firm performance. Management and Marketing 5(1), 125-131.

- Cadbury, A. (1992). The financial aspects of corporate governance – A report of the committee on corporate governance. Gee and Co., Landon.

- Campbell, K., & Mínguez-Vera, A. (2008). Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics, 83(3), 435-451.

- Conger, J. A., & Lawler, E. I. (2001). Building a high-performing board: How to choose the right members. Business Strategy Review, 12(3), 11-11.

- Council, A. C. G. (2007). Corporate governance principles and recommendations with 2010 amendments. Accessed online www. asx. com. au. Viewed June, 10, 2014.

- Darmadi, S. (2011). Board diversity and firm performance: The Indonesian evidence. Corporate Ownership and Control Journal, 8 (1).

- Darmadi, S. (2013). Do women in top management affect firm performance? Evidence from Indonesia. Corporate Governance: The international journal of business in society 13(3), 288-304

- Donaldson, L., & Davis, J.H. (1991). Stewardship theory oragency theory: CEO governance and shareholder returns. Australian Journal of Management, 16(1), 49-64.

- Dutta, P., & Bose, S. (2007). Gender diversity in the boardroom and financial performance of commercial banks: Evidence from Bangladesh.The Cost and Management. 34(8), 70 – 74

- Ekadah, J. W., &Mboya, J. K. (2009). Effect of board gender diversity on the performance of commercial banks in Kenya.European Scientific Journal, 8(7), 128 – 148

- Erhardt, N. L., Werbel, J. D., & Shrader, C. B. (2003). Board of director diversity and firm financial performance. Corporate governance: An international review, 11(2), 102-111.

- Freeman, R.E., Wicks, A.C., & Parma, B. L. (2004). Stakeholder theory and “The corporate objective revisited”. Organization science, 15(3), 364-369.

- Gentry, R.J., & Shen, W. (2010). The relationship between accounting and market measures of firm performance: How strong is it? Journal of Management Issues, 22(4), 514-550.

- Higgs, D. (2003), Review of the role and effectiveness of non-executive directors, London: DTI.

- Imhanze, I. (2015). Assessing corporate governance through judicial decisions. The Nigeria Bar, 17/09/2015.

- Jenkinson, T., & Mayer, C. (1992). The assessment: corporate governance and corporate control. Oxford Review of Economic Policy, Autumn.

- Jepkemboi, J. (2017). Relationship between board diversity and financial performance of insurance firms in Kenya (Doctoral dissertation, University of Nairobi).

- Joshua, O., Joshua, S. G., Tauhid, S. (2013). Corporate governance principles application and the financial performance of deposit money banks in Nigeria: An impact assessment. Research Journal of Finance and Accounting, 4(2), 53-64.

- Kajola, S. O. (2008). Corporate governance and firm performance. The case of Nigerian listed firms. European Journal of Economics, Finance and Administrative Sciences, 14(14), 16-28.

- Miller, T. & Triana, M. C. (2009). Demographic diversity in the boardroom: Mediators of the board diversity–firm performance relationship. Journal of Management Studies, 46(5), 755-786.

- Nganga, B. (2017). Influence of corporate governance on financial performance of commercial banks in Kenya.

- Nnabuife, E., Okaro, S. C., & Okafor, G. O. (2015). Gender diversity on corporate boards: Evidence from the Nigerian capital market. The International Journal of Business & Management, 3(1), 228.

- Obetan, O. I., Ocheni, S., & John, S. (2014). The effects of corporate governance on the performance of commercial banks in Nigeria. International Journal of Public Administration and Management Research, 2.

- Ogege, S., & Boloupremo, T. (2014). Corporate governance and financial performance of banks: Evidence from Nigeria. Acta Universitatis Danubius. O Economica, 2(2), 216-230.

- Rose, C. (2007). Does female board representation influence firm performance? The Danish evidence. Corporate Governance: An International Review, 15(2), 404-413.

- Schwizer, P., Soana, M. G., & Cucinelli, D. (2012). The relationship between board diversity and firm performance: The Italian evidence. Retrieved September, 10, 2013.

- Şener, İ., &Karaye, A. B. (2014). Board composition and gender diversity: comparison of Turkish and Nigerian listed companies. Procedia-Social and Behavioral Sciences, 150, 1002-1011.

- Shapiro, S. P. (2005). Agency theory. Annual Review of Sociology, 263-284.

- Ujunwa, A., Okoyeuzu, C., &Nwakoby, I. (2012). Corporate board diversity and firm performance: Evidence from Nigeria. Revista de Management Comparat International, 13(4), 605.

- Uwuigbe, O. R. (2011). Corporate governance and financial performance of banks: A study of listed banks in Nigeria. Theses.covenantuniversity.edu.ng.

- Walker, D. (2009). A review of corporate governance in UK banks and other financial industry entities, 1 – 175

- Wang, Y., & Clift, B. (2009). Is there a “business case” for board diversity?. Pacific Accounting, 21(2), 88-103

APPENDICES

Appendix A

Sampled Quoted Deposit Money Banks in Nigeria Covering 2010 to 2021

| Bank | Year | Id | GD | ROA |

| Access Bank | 2010 | 1 | 6.67 | 0.0178 |

| Access Bank | 2011 | 1 | 14.29 | 0.0144 |

| Access Bank | 2012 | 1 | 13.33 | 0.0208 |

| Access Bank | 2013 | 1 | 25.00 | 0.0182 |

| Access Bank | 2014 | 1 | 31.25 | 0.0215 |

| Access Bank | 2015 | 1 | 33.33 | 0.0254 |

| Access Bank | 2016 | 1 | 33.33 | 0.0248 |

| Access Bank | 2017 | 1 | 33.33 | 0.0187 |

| Access Bank | 2018 | 1 | 37.50 | 0.0172 |

| Access Bank | 2019 | 1 | 25.00 | 0.0127 |

| Access Bank | 2020 | 1 | 33.33 | 0.0182 |

| Access Bank | 2021 | 1 | 31.25 | 0.0044 |

| ETI | 2010 | 2 | 42.86 | 0.0036 |

| ETI | 2011 | 2 | 25.00 | 0.0178 |

| ETI | 2012 | 2 | 20.00 | 0.0059 |

| ETI | 2013 | 2 | 20.00 | 0.0080 |

| ETI | 2014 | 2 | 20.00 | 0.0168 |

| ETI | 2015 | 2 | 25.00 | 0.0063 |

| ETI | 2016 | 2 | 41.67 | 0.0032 |

| ETI | 2017 | 2 | 27.27 | 0.0110 |

| ETI | 2018 | 2 | 25.00 | -0.0009 |

| ETI | 2019 | 2 | 30.77 | 0.0063 |

| ETI | 2020 | 2 | 30.77 | 0.0031 |

| ETI | 2021 | 2 | 23.08 | 0.0125 |

| FBN | 2010 | 3 | 20.00 | 0.0135 |

| FBN | 2011 | 3 | 25.00 | 0.0071 |

| FBN | 2012 | 3 | 21.05 | 0.0238 |

| FBN | 2013 | 3 | 7.69 | 0.0182 |

| FBN | 2014 | 3 | 10.00 | 0.0191 |

| FBN | 2015 | 3 | 7.69 | 0.0036 |

| FBN | 2016 | 3 | 25.00 | 0.0026 |

| FBN | 2017 | 3 | 27.27 | 0.0076 |

| FBN | 2018 | 3 | 27.27 | 0.0107 |

| FBN | 2019 | 3 | 27.27 | 0.0119 |

| FBN | 2020 | 3 | 28.57 | 0.0117 |

| FBN | 2021 | 3 | 8.33 | 0.0169 |

| FCMB | 2010 | 4 | 0.00 | 0.0138 |

| FCMB | 2011 | 4 | 0.00 | -0.0195 |

| FCMB | 2012 | 4 | 0.00 | 0.0135 |

| FCMB | 2013 | 4 | 0.00 | 0.0458 |

| FCMB | 2014 | 4 | 0.00 | 0.0410 |

| FCMB | 2015 | 4 | 0.00 | 0.0195 |

| FCMB | 2016 | 4 | 0.00 | 0.0284 |

| FCMB | 2017 | 4 | 8.33 | 0.0116 |

| FCMB | 2018 | 4 | 9.09 | 0.0267 |

| FCMB | 2019 | 4 | 11.11 | 0.0269 |

| FCMB | 2020 | 4 | 18.18 | 0.0227 |

| FCMB | 2021 | 4 | 18.18 | 0.0357 |

| Fidelity | 2010 | 5 | 13.33 | 0.0122 |

| Fidelity | 2011 | 5 | 13.33 | 0.0081 |

| Fidelity | 2012 | 5 | 16.67 | 0.0215 |

| Fidelity | 2013 | 5 | 20.00 | 0.0075 |

| Fidelity | 2014 | 5 | 28.57 | 0.0116 |

| Fidelity | 2015 | 5 | 23.53 | 0.0127 |

| Fidelity | 2016 | 5 | 20.00 | 0.0050 |

| Fidelity | 2017 | 5 | 30.77 | 0.0159 |

| Fidelity | 2018 | 5 | 23.08 | 0.0120 |

| Fidelity | 2019 | 5 | 25.00 | 0.0202 |

| Fidelity | 2020 | 5 | 20.00 | 0.0164 |

| Fidelity | 2021 | 5 | 15.38 | 0.0093 |

| GTB | 2010 | 6 | 21.43 | 0.0342 |

| GTB | 2011 | 6 | 21.43 | 0.0315 |

| GTB | 2012 | 6 | 21.43 | 0.0528 |

| GTB | 2013 | 6 | 28.57 | 0.0458 |

| GTB | 2014 | 6 | 21.43 | 0.0110 |

| GTB | 2015 | 6 | 28.57 | 0.0098 |

| GTB | 2016 | 6 | 25.00 | 0.0485 |

| GTB | 2017 | 6 | 23.08 | 0.0571 |

| GTB | 2018 | 6 | 33.33 | 0.0615 |

| GTB | 2019 | 6 | 28.57 | 0.0565 |

| GTB | 2020 | 6 | 28.57 | 0.0439 |

| GTB | 2021 | 6 | 33.33 | 0.0576 |

| Stanbic IBTC | 2010 | 7 | 23.08 | 0.0210 |

| Stanbic IBTC | 2011 | 7 | 25.00 | 0.0075 |

| Stanbic IBTC | 2012 | 7 | 25.00 | 0.0145 |

| Stanbic IBTC | 2013 | 7 | 27.27 | 0.1105 |

| Stanbic IBTC | 2014 | 7 | 27.27 | 0.1736 |

| Stanbic IBTC | 2015 | 7 | 40.00 | 0.1300 |

| Stanbic IBTC | 2016 | 7 | 33.33 | 0.0066 |

| Stanbic IBTC | 2017 | 7 | 30.00 | 0.2584 |

| Stanbic IBTC | 2018 | 7 | 37.50 | 0.1436 |

| Stanbic IBTC | 2019 | 7 | 36.36 | 0.2658 |

| Stanbic IBTC | 2020 | 7 | 45.45 | 0.1795 |

| Stanbic IBTC | 2021 | 7 | 45.45 | 0.2068 |

| Sterling | 2010 | 8 | 0.00 | 0.0161 |

| Sterling | 2011 | 8 | 8.33 | 0.0092 |

| Sterling | 2012 | 8 | 10.00 | 0.0120 |

| Sterling | 2013 | 8 | 10.00 | 0.0117 |

| Sterling | 2014 | 8 | 20.00 | 0.0109 |

| Sterling | 2015 | 8 | 33.33 | 0.0129 |

| Sterling | 2016 | 8 | 28.57 | 0.0062 |

| Sterling | 2017 | 8 | 26.67 | 0.0079 |

| Sterling | 2018 | 8 | 26.67 | 0.0087 |

| Sterling | 2019 | 8 | 21.43 | 0.0087 |

| Sterling | 2020 | 8 | 21.43 | 0.0087 |

| Sterling | 2021 | 8 | 21.43 | 0.0083 |

| UBA | 2010 | 9 | 21.05 | 0.0015 |

| UBA | 2011 | 9 | 15.00 | -0.0099 |

| UBA | 2012 | 9 | 20.00 | 0.0245 |

| UBA | 2013 | 9 | 27.78 | 0.0210 |

| UBA | 2014 | 9 | 23.53 | 0.0171 |

| UBA | 2015 | 9 | 25.00 | 0.0215 |

| UBA | 2016 | 9 | 15.79 | 0.0187 |

| UBA | 2017 | 9 | 15.79 | 0.0145 |

| UBA | 2018 | 9 | 21.05 | 0.0114 |

| UBA | 2019 | 9 | 21.05 | 0.0152 |

| UBA | 2020 | 9 | 25.00 | 0.0109 |

| UBA | 2021 | 9 | 33.33 | 0.0105 |

| UBN | 2010 | 10 | 14.29 | 0.1396 |

| UBN | 2011 | 10 | 14.29 | -0.0987 |

| UBN | 2012 | 10 | 15.38 | 0.0036 |

| UBN | 2013 | 10 | 12.50 | 0.0058 |

| UBN | 2014 | 10 | 11.76 | 0.0223 |

| UBN | 2015 | 10 | 21.05 | 0.0178 |

| UBN | 2016 | 10 | 23.53 | 0.0141 |

| UBN | 2017 | 10 | 33.33 | 0.0096 |

| UBN | 2018 | 10 | 26.67 | 0.0139 |

| UBN | 2019 | 10 | 25.00 | 0.0142 |

| UBN | 2020 | 10 | 21.43 | 0.0119 |

| UBN | 2021 | 10 | 26.67 | 0.0075 |

| Unity Bank | 2010 | 11 | 6.67 | 0.0407 |

| Unity Bank | 2011 | 11 | 6.25 | 0.0065 |

| Unity Bank | 2012 | 11 | 6.25 | 0.0156 |

| Unity Bank | 2013 | 11 | 11.11 | -0.0559 |

| Unity Bank | 2014 | 11 | 25.00 | 0.0259 |

| Unity Bank | 2015 | 11 | 33.33 | 0.0106 |

| Unity Bank | 2016 | 11 | 33.33 | 0.0044 |

| Unity Bank | 2017 | 11 | 13.33 | -0.0953 |

| Unity Bank | 2018 | 11 | 22.22 | -0.0365 |

| Unity Bank | 2019 | 11 | 30.00 | 0.0115 |

| Unity Bank | 2020 | 11 | 30.00 | 0.0042 |

| Unity Bank | 2021 | 11 | 30.00 | 0.0059 |

| Wema | 2010 | 12 | 0.00 | 0.0799 |

| Wema | 2011 | 12 | 0.00 | -0.0344 |

| Wema | 2012 | 12 | 8.33 | -0.0205 |

| Wema | 2013 | 12 | 16.67 | 0.0048 |

| Wema | 2014 | 12 | 15.38 | 0.0062 |

| Wema | 2015 | 12 | 33.33 | 0.0059 |

| Wema | 2016 | 12 | 33.33 | 0.0062 |

| Wema | 2017 | 12 | 33.33 | 0.0060 |

| Wema | 2018 | 12 | 27.27 | 0.0070 |

| Wema | 2019 | 12 | 36.36 | 0.0081 |

| Wema | 2020 | 12 | 33.33 | 0.0047 |

| Wema | 2021 | 12 | 26.67 | 0.0077 |

| Zenith | 2010 | 13 | 0.00 | 0.0186 |

| Zenith | 2011 | 13 | 0.00 | 0.0172 |

| Zenith | 2012 | 13 | 0.00 | 0.0393 |

| Zenith | 2013 | 13 | 16.67 | 0.0290 |

| Zenith | 2014 | 13 | 16.67 | 0.0270 |

| Zenith | 2015 | 13 | 10.00 | 0.0263 |

| Zenith | 2016 | 13 | 0.00 | 0.0278 |

| Zenith | 2017 | 13 | 9.09 | 0.0325 |

| Zenith | 2018 | 13 | 7.69 | 0.0334 |

| Zenith | 2019 | 13 | 7.69 | 0.0328 |

| Zenith | 2020 | 13 | 7.69 | 0.0278 |

| Zenith | 2021 | 13 | 15.38 | 0.0296 |

Appendix B

xtregroagd, re vce(robust)

Random-effects GLS regression Number of obs = 156

Group variable: id Number of groups = 13

R-sq: within = 0.0165 Obs per group: min= 12

between = 0.6010 avg = 12.0

overall = 0.6409 max = 12

Wald chi2(1) = 7.42

corr(u_i, X) = 0 (assumed) Prob > chi2 = 0.0065