Impact of Financial Innovation on the Competitiveness of Deposit Money Banks in Nigeria

- AYODELE, Oluwafemi Godwin

- AFOLABI, Taofeek Sola

- 23-36

- Oct 27, 2023

- Accounting

Impact of Financial Innovation on the Competitiveness of Deposit Money Banks in Nigeria

AYODELE, Oluwafemi Godwin; AFOLABI, Taofeek Sola

Department of Finance, Redeemer’s University, Ede, Nigeria

DOI: https://doi.org/10.51244/IJRSI.2023.101004

Received: 12 August 2023; Accepted: 27 September 2023; Published: 27 October 2023

ABSTRACT

The world has changed dramatically, since the industrial revolution and innovation is now at the forefront of every industry. Scholars have identified innovation as a critical factor that aids economic expansion, accelerates financial development and facilitates investment diversification. However, despite the undeniable importance of financial innovation in fostering growth, questions remain on whether such innovation boosts competitiveness among banks in Nigeria. Therefore, this study investigated the impact of financial innovation on the competitiveness of Deposit Money Banks (DMBs) in Nigeria. Ninety-six bank officers were randomly selected from the twenty-four DMBs in Nigeria, to provide responses to a structured questionnaire, developed in line with the objectives of the study. A Structural Equation Model (SEM) was used to specify the relationship between the dimensions of financial innovation (mobile banking, internet banking, ATM banking & CBN digital currency) and banks’ competitiveness. The model assessment was done using the standard factor loading, composite reliability, construct and the discriminant validity tests. The Partial Least Squares (PLS) technique was further used to estimate the model parameters and test the research hypotheses, via the Smart-PLS 3 statistical software. The results revealed that both internet banking and CBN digital currency directly and significantly affect banks’ competitiveness. The study concludes that internet banking and CBN digital currency are key financial innovation tools influencing competitiveness among DMBs in Nigeria. Therefore, it is recommended that management and stakeholders in Nigerian DMBs should encourage frequent usage of their internet banking platforms by making it more customer-friendly and enhancing its safety features. Furthermore, the government should by way of policy encourage businesses and individuals to embrace the E-naira for carrying out financial transactions.

Keywords: Mobile Banking; Internet Banking; ATM; Digital Currency; Banks’ competitiveness.

INTRODUCTION

Since the industrial revolution, the world has changed dramatically, and innovation is now at the forefront of every industry. When businesses innovate, they might replace an outdated method with one that is both innovative and more effective. According to Lawrence (2010), innovation is a significant advancement made by businesses by introducing new goods or adopting novel manufacturing procedures. Organizational innovation is characterized by creating novel ideas, products, or processes that produce fresh, high-quality, and user-friendly goods and services (Kumar et al., 2011). The financial sector is one area where there has been an uptick in interest in adopting innovations designed to keep up with the dynamic nature of the market place. New and improved technology, financial instruments, institutions, and markets that facilitate communication, commerce, and the transfer of funds are considered innovations in the financial services sector (Sloan, 2003). Nofie (2011) defines innovation in the financial industry as introducing a new or improved product or procedure that reduces the cost of generating current financial services or transactions. Financial innovation refers to the process through which new financial instruments, technology, institutions, and markets are developed and adopted by the financial sector (Satya Sekhar, 2018).

Qamruzzaman and Jianguo (2019) note the significance of a developed financial sector in promoting growth stability, technological innovation, access to affordable financial information, and just investment decisions. Accelerating financial development by facilitating risk mitigation and investment diversification, financial innovation is a critical factor in economic expansion (Desai & Low, 1987). Schumpeter (1928) argues that financial innovation is vital to economic progress, but researchers have paid too little attention to its effect on the economy. However, in recent time financial innovation and its potential influence has gained tremendous attention among scholars and stimulated more exploration by taking into account the many facets of the economy, such as economic development (Bara & Mudzingiri, 2016; Bara et al., 2016), on company competitiveness (Valverde et al., 2016; and Muthinja & Chimwemwe, 2018); on banking sector expansion (Kamau & Oluoch, 2016; and Chipeta & Moses, 2018); and on many other topics.

As Batiz-Lazo and Woldesenbet (2006) pointed out, financial innovations are now vital for banks to boost efficiency and enhance their market competitiveness. Evidently, financial innovation not only aids the bank in cutting expenses but also provides a wide variety of new options and prospects that will aid the bank in enhancing its competitiveness in several ways (Sujud & Hashem, 2017). According to Aduda and Kingoo (2012), Deposit Money Banks (DMBs) may improve their competitiveness and sustain their market success by using financial innovation to help them compete in financial markets. These suggest that studying how innovations in the financial sector have affected the overall success of deposit money banks is crucial.

DMBs in Nigeria have been notoriously lenient in encouraging the introduction of novel financial technologies (Mengistu, 2018). To begin, the return on investment (ROI) may take too long and be unacceptably slow for management and shareholders. Second, it might be because digital financial services lack the ‘analogue complements’ of regulation, expertise, and established institutions. Thirdly, no guarantee implementing these innovations would improve a bank’s profitability or efficiency. It stands to reason that banks’ evaluation of the effectiveness of this new creative technology-based banking will determine whether or not they gain advantages and collect profits. Therefore, it is imperative to investigate impacts of financial innovation on the efficiency of deposit money banks in Nigeria.

Nigeria’s financial industry cannot remain an exception in growing the usage of the system even if it lags far behind the rest of the globe in implementing financial innovations (Gardachew, 2010). Any commercial bank in Nigeria would do well to provide itself with the knowledge and tools essential to thrive in today’s dynamic business environment (Solomon, 2016; Iriobe, et al. 2021). The relevance of the CBN’s financial inclusion strategy, which has increased the usage of electronic money and innovative financial products, was also highlighted in the organization’s most recent annual report (CBN, 2022). The banking industry has been at the forefront of the mobile banking revolution, offering a wide variety of digital banking products with a variety of user interfaces (cardless ATM services, weather derivatives, central bank digital currency, QR code payment, hedge funds, and exchange-traded funds), support for numerous languages, and access to multilingual customer care representatives. ATMs, mobile banking, online banking, card banking, agency banking, free advising services, and other innovations have all contributed to the growth of Nigeria’s banking and financial sector in recent years. In light of this, issues about whether or not the advent of such new financial channels marked a beneficial shift and are hurting the financial and operational competitiveness of the banks will become more pressing.

This research aims to determine how DMBs in Nigeria react to financial innovations. Specifically, the study examined the impact of mobile banking, internet banking, ATM banking and CBN digital currency on the competitiveness of DMBs in Nigeria. To achieve this the following hypotheses were tested; Mobile banking has no significant influence on the competitiveness of DMBs in Nigeria; Internet banking has no significant influence on the competitiveness of DMBs in Nigeria; ATM banking has no significant influence on the competitiveness of DMBs in Nigeria; CBN digital currency has no significant influence on the competitiveness of DMBs in Nigeria.

LITERATURE REVIEW

Conceptual Review

Financial innovation is the creation and spread of new financial instruments, technology, institutions, and markets (Lemo, 2005). Unlike industrial innovations, which often include entirely new items, financial innovations typically build on preexisting financial tools or structures (Victor, 2015). Product, process, and institutional innovations are the three main categories of financial innovations identified by Frame and White (2002). According to Ignazio (2007) mobile, Internet, and ATM banking are the most extensively embraced forms of financial innovation in the Nigerian environment. Mobile banking has emerged as a feasible alternative for financial services due to the widespread use of mobile phones and the quick development of internet technology. Also known as banking on the go, it is the practice of handling financial matters using a mobile device, most commonly a smart phone (Anyasi & Otubu, 2009). It improves productivity and facilitates business growth by providing a secure, low-cost, and convenient money service support system that reduces reliance on physical currency transaction, as well as the dangers involved (Anyasi & Otuba, 2009).

According to Sathye (2009), value-added banking services are those provided to financial institution clients through the internet and other communications networks. Internet banking allows clients to access their bank accounts online using a computer with internet access. The fast global expansion of internet banking attests to its widespread recognition as a superior means of delivering financial services in terms of cost and efficiency (Zarei et al., 2008). Another financial innovation tool that is widely recognized for providing electronic access for banks’ clients is the Automated Teller Machine (ATM). This device has allowed financial institutions banks to expand their services outside their physical locations by connecting them with retail banking customers for various routine banking transactions (Dossantos & Peffers, 1993). Literature suggests that customers favour ATM banking, making it the second most popular channel after branch banking to access banking goods and services (Charles, 2016).

Financial and market competitiveness, customer-focused competitiveness, human resource competitiveness, and product/service competitiveness are the four facets of competitiveness identified by Alam et al. (2011). Organizational goals serve as the foundation for the competitiveness metrics used by various businesses. Both monetary and non-monetary metrics may be used to evaluate this competitiveness indicator (Bergin-Seers & Jago, 2007). However, most businesses choose to utilize financial indicators instead (Beccalli, 2007). When it comes to providing the bank with investment possibilities, Omondi and Muturi (2013) define financial competitiveness as “the use of financial indicators to measure the extent to which objectives have been accomplished.” It determines how well a firm can capitalize on its principal business model to create profits (Heremans, 2007). However, financial metrics are not the sole yardstick for a company’s success. It must be combined with nonfinancial measurement to adapt to shifting internal and external conditions. Most prior research exclusively used financial indicators to gauge business success; however, this is insufficient and there are calls to include nonfinancial indicators through an integrated approach (Hansen & Wernerfelt, 1989).

Theoretical Framework

Rogers’ diffusion of innovation theory, Silber’s hypothesis of constraint-induced financial innovation and Hicks and Niehans’ theory of transaction cost innovation provided the theoretical framework for this study. Silber (1983) theory opines that since the banking industry is heavily regulated Deposit Money Banks (DMBs) will constantly use new forms of financial innovation to stave off competition. According to Rogers (1995) theory, innovations are more likely to be widely embraced if they provide demonstrable improvements over the status quo of a firm. 2004). Hicks and Niehans (1983) theory held that a firm’s primary motivation for adopting financial innovation is the decrease of transaction cost resulting from technological innovations, such as mobile/internet banking and other cardless services. Furthermore, profit maximization is the primary motivation for financial innovation in financial organizations. These theories are the basis for the model developed for the hypothesized relationships.

Empirical Review

The effect of financial innovation on bank competitiveness has been the subject of several empirical studies in both developed and developing economies. According to Roberts and Amit (2003), who sought to identify the link between innovation and the creation of unique competitive positions in Australian retail banking, financial inventive activities have a substantial influence on the present financial competitiveness of banks. Rahman (2007) conducted research to ascertain the effect of cutting-edge technology on the bottom lines of Bangladeshi financial institutions and discovered that the competitiveness of those institutions that embraced such technology increased with age. Furthermore, Hernando and Nieto (2007) conducted a study to determine the relationship between internet banking channels and the competitiveness of Spain retail banking. Their finding showed that internet-based digital banking channel has a significant effect on the sample bank’s competitiveness. Francesca and Claeys (2010) did similar research, this time looking at what factors influence banking conglomerates’ strategic decisions when it comes to the distribution of online services. Their research included analyzing panel data from the sixty major banking firms in the European Union during the years 1995 and 2005. They concluded that financial innovations in internet banking do not boost banks’ financial competitiveness because online banks fail to develop synergies with other banking operations.

Malhotra and Singh (2010) analyzed the impact of financial innovations, particularly online banking, on the competitiveness of India’s Deposit Money Banks (DMBs). The researcher utilized panel data from eight-two scheduled DMBs covering the periods 1998-2007 and discovered no significant correlation between banks’ use of online banking and their financial outcomes. Similarly, Al-Smadi and Al Wabel (2011) investigated the impact of online banking on the performance of financial institutions in the Jordanian banking sector. Using panel data from fifteen different banks, spanning 2000 to 2010, they discovered that electronic banking had no significant effect on banks’ bottom lines. Onay and Ozsoz (2013) used panel data from 1990 to 2008 gotten from eighteen Turkish retail banks to assess the impact of electronic banking on bank competitiveness. Their results showed that internet banking adoption is positively associated with the level of profits, deposits, and loans per branch. However, the research further indicated that after two years of use, online banking services had no significant influence on bank’s profitability. Similarly, Sadr (2013) used a cross-national sample to analyze data from four banks in various Asian nations for his own research. Using modified OLS, the researcher showed that online banking positively affects return on equity after a lag of three years, but has a negative effect after just one year. The impact of electronic banking on the efficiency of Pakistani DMBs was also investigated by Rauf and Qiang (2014). The researchers discovered that the interest margin, return on assets, and return on equity of more recent adopters of electronic banking are all significantly positively impacted by the switch, whereas the ROA and interest margin are significantly positively impacted for early adopters. Karimzadeh et al. (2014) looked into the effects of expanding electronic banking on the profitability of an Iranian commercial bank and found that doing so was positively correlated with the bank’s return on assets.

Studies in African economies have also revealed contrasting findings on the effect of financial innovation on bank’s bottom line. Kimingi (2010) conducted a study to determine the impact of technological innovations on Kenyan Deposit Money Banks, and he concluded that such banks’ bottom lines benefited from the innovations in the form of higher profits, higher sales, and higher returns on equity after adopting the innovations. Financial innovation has a favourable and considerable effect on the profitability of Kenyan deposit money banks, as was also observed by Okiro and Ndungu (2013). Furthermore, Paul et al. (2015) set out to analyze yearly financial data from 2009 through 2013 to determine how the introduction of new financial innovations affected the profitability of Fidelity Bank in Ghana. They arrived on the conclusion that a Ghanaian bank’s profits would rise as the country became more receptive to financial innovations. Similarly, Mensah (2016) used annual financial data from twenty selected rural banks in Ghana between 2011 and 2014 to determine the effects of Information Communication Technology (ICT) on the competitiveness of these institutions and found that ICT has a significant impact on the competitiveness of the rural banks.

In Nigeria, Oyerinde (2011) conducted a research on the impact of electronic banking on the competitiveness of bank. His finding showed that electronic banking significantly improves return on assets and net interest margin. Abaenewe et al. (2013) set out to investigate how the rise of electronic banking in Nigeria has affected the financial success of the country’s banks. Findings revealed a positive and significant correlation between Nigerian banks’ use of electronic banking and their return on equity, with no effect on return on assets. Furthermore, Jegede (2014) used a questionnaire sent to 125 workers at the five selected banks in Lagos State to investigate the impact of ATMs on the efficiency of Nigerian banks. The research found that, on average, Nigerian banks’ productivity increased after using ATMs. Nkem and Akujinma, (2017) conducted a study to determine the effect of financial innovation on the productivity of Nigerian DMBs. The researchers discovered that the value of transactions made via ATMs and other points of service was inversely proportional to the efficiency of the banks. When the efficiency of banks was compared to the use of mobile and online banking, a positive correlation was found between the two. A study by Gbalam et al. (2017) aimed to analyze how electronic banking affects the bottom lines of Nigerian DMBs. Using data from 2006 to 2014, result showed that profit before tax regressed due to the rise in use of four electronic banking channels: ATM, mobile banking, internet banking transactions, and point-of-sale services. Overall, the data showed that electronic banking had a significant effect on DMBs’ bottom lines, despite the effects of different channels being mixed.

Still in Nigeria, Girma (2016) investigated the effect of Information and Communication Technology (ICT) on the efficiency of the Nigerian banking sector, using secondary data from 2010 to 2014. Statistical analysis indicated that increasing spending on ICT infrastructure like ATMs and POS terminals had no influence on return on assets of DMBs in Nigeria. Similarly, Solomon (2016) used panel data from nine DMBs in Nigeria from 2013 to 2015 to analyze the impact of electronic banking on financial competitiveness. The researcher found that DMBs’ financial health improved when their ATM, POS, and market share metrics all rose. However, the rise in debit card use hurt the bank’s bottom lines. This is also similar to the findings of Tilahun (2016) who investigated the effect of electronic banking on the financial performance of DMBs in Nigeria. Furthermore, Rukiya (2018) used secondary data from nine DMBs in Nigeria between 2015 and 2017 to investigate how financial innovation affected their competitiveness. The research found that DMBs financial competitiveness improved due to lower transaction costs and greater deposit mobilization as the number of mobile banking users and new saving accounts rose. However, DMBs financial competitiveness suffers significantly owing to the costly initial investment of ATM machines in comparison to the revenue they earn. Also, in the work of Ighomereho, Afolabi and Oluwakoya (2022), internet banking quality and ease of usage were noted to drive customers’ satisfaction, which affects bank’s bottom line.

The empirical reviews have shown contrasting results on the effect of financial innovation on the competitiveness of DMBs in Nigeria. Most of the earlier investigations employed secondary data in analyzing the relationship between the study variables. In addition, the effect of digital technology has not been properly investigated. The current study therefore utilized a survey approach to determine how mobile banking, internet banking, ATM banking and CBN digital currency affect competitiveness amongst Nigerian DMBs.

MATERIAL AND METHODS

This study adopted the descriptive survey design which involved the collection of data from respondents across the twenty-four Deposit Money Banks (DMBs) in Nigeria. Four senior managers/officers in each of the corporate head offices of the banks were randomly selected to participate in the survey. Ninety-six (96) copies of a structured questionnaire were filled by the respondents and these provided the data for the analysis. The questionnaire contained indicator items on the construct variables, which are dimensions for financial innovations and bank’s competitiveness. Responses were captured on a 5-point likert scale, ranging from strongly agree (5) to strongly disagree (1).

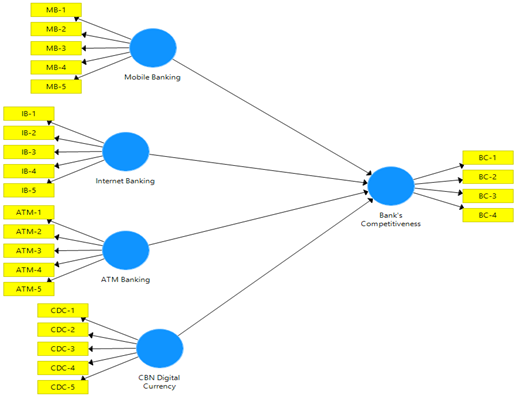

A Structural Equation Model (SEM) was used to transform the indicators in the research questionnaire into latent variables in order to study the relationship among them. The functional model for the linear relationship is adapted from Sibler and Hicks (1983). The SEM framework is presented as:

Figure 1 – SEM Framework

Source: Smart-PLS 3 (2023)

The econometric model representing the relationship in the SEM is specified thus;

BC = β0 + β1MB +β2IB +β3ATM +β4CDC + ui………………………….. (1)

Where, BC is Bank’s Competitiveness; MB is Mobile Banking; IB is Internet Banking; ATM is ATM Banking; CDC is CBN Digital Currency; β0 is regression constant; β0, β1, β2, β3 are regression coefficients and ui is the error term. The Partial Least Squares (PLS) estimation technique was used for econometric analysis, via the Smart-PLS 3 statistical software. The standard-factor loading, composite reliability test, construct validity test and the discriminant validity test were used for the assessment of the structural model, while the PLS-SEM bootstrap was used to test the hypotheses.

RESULTS

The demographic analysis results in Table 1 show that majority of respondents are male (53.1%) and within the age bracket 41-50years (38.5%). Furthermore, most of the respondents have at least a first degree (65.5%), spent more than 10years in the banking industry (69.8%) and belong to the middle management cadre (50%). The spread of these results suggests that the respondents have the ability and are well experienced to adequately provide responses on the subject of study.

Table 1: Demographic Characteristics

| Characteristics | Categories | Frequency | Percentage |

| Gender | Male | 51 | 53.1 |

| Female | 45 | 46.9 | |

| Age | 30years and below | 5 | 5.2 |

| 31-40years | 24 | 25.0 | |

| 41-50years | 37 | 38.5 | |

| 51-60years | 21 | 21.9 | |

| 61years and above | 9 | 9.4 | |

| Qualification | BSc/HND | 63 | 65.6 |

| Masters | 28 | 29.2 | |

| PhD | 2 | 2.1 | |

| Others | 3 | 3.1 | |

| Experience in Banking | Below 5years | 5 | 5.2 |

| 5 – 10years | 24 | 25.0 | |

| 11 – 15years | 37 | 38.5 | |

| Above 15years | 30 | 31.3 | |

| Position | Bank Officers | 15 | 15.6 |

| Middle Management | 48 | 50.0 | |

| Top Management | 33 | 34.4 | |

| Counts (N) | 96 | 100.0 |

Source: Field Work (2023)

Table 2 reveals the assessment of the measuring items in the questionnaire. The results show that the factor loadings for the retained items are above the minimum acceptable threshold of 0.6, indicating that they are valid in measuring their respective constructs. Similarly, the composite reliability statistics of the construct variables are above the minimum required threshold of 0.7, implying that the items are reliable in jointly measuring their individual constructs. Furthermore, the Average Variance Extracted (AVE) results show that all the constructs have values above the minimum acceptable value of 0.5, which establishes their convergent validity.

Table 2 – Assessment of Measuring Items

| Constructs | Items | Loadings | Composite Reliability | AVE |

| Mobile Banking | MB-1 | 0.89 | 0.92 | 0.75 |

| MB-2 | 0.87 | |||

| MB-3 | 0.86 | |||

| MB-5 | 0.84 | |||

| Internet Banking | IB-1 | 0.80 | 0.84 | 0.64 |

| IB-2 | 0.82 | |||

| IB-3 | 0.78 | |||

| ATM Banking | ATM-1 | 0.93 | 0.91 | 0.83 |

| ATM-2 | 0.90 | |||

| CBN Digital Currency | CDC-1 | 0.83 | 0.83 | 0.55 |

| CDC-2 | 0.75 | |||

| CDC-4 | 0.72 | |||

| CDC-5 | 0.65 | |||

| Bank’s Competitiveness | BC-1 | 0.75 | 0.87 | 0.53 |

| BC-3 | 0.74 | |||

| BC-4 | 0.67 | |||

| BC-5 | 0.80 | |||

| BC-6 | 0.70 | |||

| BC-8 | 0.70 |

Source: Smart-PLS 3 (2023)

The Fornell-Larcker and Heterotrait-Monotrait (HTMT) criteria were used to test the discriminant validity of the constructs and the results are presented in Tables 3 and 4. The Fornell-Larcker criterion requires that the square root of the AVEs (located in the diagonal column of Table 3) must be greater than any of the inter-construct correlations (located elsewhere). The results show that this condition has been met and hence satisfying the discriminant validity condition.

Table 3 – Fornell-Larcker Condition

| MB | IB | ATM | CDC | BC | |

| MB | 0.87 | ||||

| IB | 0.31 | 0.80 | |||

| ATM | 0.62 | 0.34 | 0.91 | ||

| CDC | 0.36 | 0.51 | 0.44 | 0.74 | |

| BC | 0.23 | 0.52 | 0.22 | 0.55 | 0.73 |

Source: Smart-PLS 3 (2023)

In addition, discriminant validity is also satisfied if the HTMT ratios do not exceed the 0.9 maximum threshold and results from Table 4 indicate that this condition is satisfied. Therefore, it can be concluded that there is no discriminant validity problem among the construct variables.

Table 4 – HTMT

| MB | IB | ATM | CDC | BC | |

| MB | |||||

| IB | 0.38 | ||||

| ATM | 0.74 | 0.44 | |||

| CDC | 0.42 | 0.67 | 0.56 | ||

| BC | 0.24 | 0.66 | 0.27 | 0.69 |

Source: Smart-PLS 3 (2023)

The model fit results in Table 5 shows the Standardized Root Mean Residual (SRMR) for the SEM is 0.01 which is below the maximum acceptable benchmark of 0.08. Similarly, the overall model fit indices (d_ULS & d_G) are both below the acceptable benchmark (HI95.=1.74 & 1.27 respectively). In addition, the R-squared value of 0.382 indicates that the independent constructs jointly explain 38.2percent of the total variation in the exploratory variable. The summary of the structural model implies a good model fit.

Table 5 – Model Fit

| Criteria | Value | Benchmark |

| SRMR | 0.07 | < 0.08 |

| d_ULS | 1.672 | <HI95=1.74 |

| d_G | 0.988 | <HI95=1.27 |

| Chi-Square | 2232.064 | |

| R-squared | 0.382 | |

| R Square Adjusted | 0.376 |

Source: Smart-PLS 3 (2023)

Test of Hypotheses

Table 6 shows the path coefficients for the four research hypotheses that have been put forward for testing. The regression results of the path relationships in the SEM are also specified. The path coefficient from the mobile banking construct to bank’s competitiveness is positive (β=0.03), implying a direct relationship. However, the t-statistic (t=0.56) of this path is not significant at the 5% level (p=0.58). Therefore, the null hypothesis is supported and it is concluded that mobile banking has no significant effect on the competitiveness of Deposit Money Banks in Nigeria. In addition, the path coefficient from the internet banking construct to bank’s competitiveness is positive (β=0.34), indicating a direct relationship. The t-statistic (t=5.89) of this path is also significant at the 5% level (p=0.00). Hence, the null hypothesis is rejected and it is concluded that internet banking has a significant effect on the competitiveness of Deposit Money Banks in Nigeria.

Table 6 – Path Coefficients

| Paths | Beta | T-Statistics | P-Values | Decision on H0 |

| Mobile Banking -> Bank’s Competitiveness | 0.03 | 0.56 | 0.58 | Supported |

| Internet Banking -> Bank’s Competitiveness | 0.34 | 5.89 | 0.00 | Rejected |

| ATM Banking -> Bank’s Competitiveness | -0.08 | 1.54 | 0.13 | Supported |

| CBN Digital Currency -> Bank’s Competitiveness | 0.40 | 8.94 | 0.00 | Rejected |

Source: Smart-PLS 3 (2023)

Further results from Table 6, reveal that the path coefficient from the ATM banking construct to bank’s competitiveness is negative (β=-0.08), implying an inverse relationship. However, the t-statistic (t=1.54) of this path is not significant at the 5% level (p=0.13). Therefore, the null hypothesis is supported and it is concluded that ATM banking has no significant effect on the competitiveness of Deposit Money Banks in Nigeria. Lastly, the path coefficient from the CBN digital currency construct to bank’s competitiveness is positive (β=0.40), suggesting a direct relationship. The t-statistic (t=8.94) of this path is also significant at the 5% level (p=0.00). Hence, the null hypothesis is rejected and it is concluded that CBN digital currency has a significant effect on the competitiveness of Deposit Money Banks in Nigeria.

Implication of Findings

The empirical result from the path analysis has shown that mobile banking innovation has a direct but non-significant effect on the competitiveness of DMBs in Nigeria. This implies that innovations coming from mobile banking usage or platform have little or no impact on the quest of the banks to remain competitive and thus suggesting there may be other factors. This finding agrees with those of Al-Smadi and Al Wabel (2011) who established that mobile banking does not influence bank’s competitiveness. However, the finding disagrees with Rauf and Qiang (2014); Gbalam et al. (2017), Nkem and Akujinma (2017); and Rukiya (2018), who have argued otherwise.

Furthermore, internet banking innovation has been shown to have a direct and significant effect on the competitiveness of DMBs in Nigeria. The implication of this is that stakeholders in the banking industry must continuously maintain a user-friendly internet banking platforms in order to boast customer usage. The government must also do more to facilitate cheap and affordable internet connection for the citizens. The finding here is in tandem with those of Hernando and Nieto (2007); Sadr (2013); Karimzadeh et al. (2014); and Gbalam et al. (2017), but not consistent with those of Malhotra and Singh (2010); and Frascesca and Claeys (2010).

In addition, findings have revealed that ATM banking innovation has an inverse but non-significant effect on the competitiveness of DMBs in Nigeria. This underscores the relevance of any innovative efforts through the bank’s ATM outlets, as customers could afford to use any, based on proximity and convenience. The findings here is consistent with those of Girma (2016); Nkem and Akujinma (2017); and Rukiya (2018) who postulate that ATM banking does not significantly influence the efficiency and competitiveness of banks. However, it disagrees with those of Jegede (2014); Solomon (2016); and Gbalam et al. (2017).

Lastly, the empirical findings have shown that the CBN digital currency directly and significantly affects the competitiveness of DMBs in Nigeria. This implies that the CBN innovative effort through the introduction of digital currency (e.g the E-Naira) is perceived as a major driver of competitive amongst DMBs. This finding is in agreement with those of Rahman (2007); Okiro and Ndungu (2013); Paul et al. (2015); and Mensah (2016). However, it disagrees with that of Girma (2016).

CONCLUSION AND POLICY RECOMMENDATIONS

This research investigated the influence of the dimensions of financial innovations (mobile banking, internet banking, ATM banking & CBN digital currency) on the competitiveness of Deposit Money Banks (DMBs) in Nigeria. Findings from the research have shown that internet banking and digital currency significantly influence banks’ competitiveness. However, such significant influence does not hold for mobile banking and ATM banking. This establishes internet banking and CBN digital currency as key financial innovations influencing competitiveness. It is therefore concluded that DMBs in Nigeria can enhance their performance and retain their relevance in the banking sector if they channel their innovative efforts through these platforms.

The study recommends that stakeholders in the Nigerian banking industry should ensure customers have constant and uninterrupted access to their internet banking platforms. Safety features on the platform should also be enhanced in order to encourage frequent usage. Furthermore, the government through the apex bank needs to create more awareness on the relative usefulness of the digital currency and encourage the use of the E-naira for individual and businesses’ transactions. In addition, the government should by way of policy facilitate access to cheap and affordable internet connection in the country. The internet service providers should be made to reduce the charges on their services and avoid unnecessary ones. Collaborations can also be encouraged among the service providers to expand courage across the country and increase internet bandwidth.

REFERENCES

- Abaenewe, Z., Ogbulu, O. M., & Ndugbu, M. (2013). Electronic Banking and Bank Competitiveness in Nigeria. West African Industrial Academic Res 6: 171-187.

- Aduda, J. & Kingoo, N. (2012). The Relationship between Electronic Banking and Financial Competitiveness among Deposit money banks in Kenya. Journal of Accounting and Taxation 9(19), 231 -256.

- Alam, H., Raza, A., & Akram, M. (2011). Financial Competitiveness of Leasing Sector. The Case of China. Interdisciplinary Journal of Contemporary Research in Business, 2(12), 339-345.

- Al-Smadi, M., & Al-Wabel, S. (2011). The Impact of E-banking on the Competitiveness of Jordanian Banks. Journal of Internet Banking and Commerce 16(2), 1–10.

- Anyasi, F., & Otubu, P. (2009). Mobile Phone Technology in Banking System: Its Economic Effect, Empirical Lessons from Selected Sub-Saharan Africa Countries. International Journal of Development Societies, 1(2), 2012, 70-81.

- Bara, A. & Mudzingiri, C. (2016). Financial innovation and economic growth: Evidence from Zimbabwe. Investment Management and Financial Innovations 13, 65–75.

- Bara, A., Gift, M., & Pierre, L. (2016). Financial Innovation and Economic Growth in the Economic Research Southern Africa 1, 1–23.

- Beccalli, E. (2007). Does IT Investment Improve Bank Competitiveness? Evidence from Europe. International Journal of Banking Finance 31: 2205-2230.

- Bergin-Seers, S. & Jago, L. (2007). Competitiveness Measurement in micro finance institution in Australia. International Journal of Financial Research, (7)2, 144-155.

- Charles, M. (2016). Impact of ATM Banking Competitiveness on Customer Satisfaction with the Bank in Malawi. International Journal of Business and Economics Research. 5(1), 1-9. 10.11648/j.ijber.20160501.11

- Chipeta, C. & Moses, M. (2018). Financial innovations and bank competitiveness in Kenya: Evidence from branchless banking models. South African Journal of Economic and Management Sciences 21: 1–11.

- Cronbach, L. J. (1995). Coefficient Alpha and the Internal Structure of Tests. Sychometrical, 22(3), 297-334.

- Desai, M. & Low, W., (1987). Financial innovation: measuring the opportunity for product innovation. New Delhi, India: New age International Publishers.

- Dossantos, B. & Peffers, K. (1993). The Effects of Early Adoption of Information Technology: An Empirical Study. Journal of Information Technology Management. 5(1) 1-13.

- Frame, W., Scott, W., & Lawrence, J. (2002): Empirical Studies of Financial Innovation: (Working Paper 2002-12). Atlanta, GA, USA: FRB of Atlanta.

- Frame, W. & White, L. (2009). Technological Change, Financial Innovation, and Diffusion in Banking, Financial Innovation and Diffusion in Banking. India, New Delhi; Aseda Publishing.

- Francesca, A., & Claeys, P. (2010). Innovation and Competitiveness of European Banks Adopting Internet. University of Milan and Cass Business School, City University London and University of Barcelona Centre for Banking Research, Cass Business School, City University London Working Paper Series,WP 04/10.

- Gardachew, W. (2010). Electronic-Banking in Nigeria: Practices, Opportunities and Challenges, Journal of Internet Banking and Commerce, 15(2).

- Gbalam, L., Ezeoha, A. & Iwayemi, A. (2017). The Impact of Electronic Banking on Profitability of Deposit Money Banks in Nigeria. African Journal of Business Management, (5)11, 2323- 2343.

- Girma, A. (2016). The Impact of Information and Communication Technology on Competitiveness of Deposit Money Banks in Nigeria. Unpublished MBA project, Addis Ababa University.

- Greenhalgh, T., Robert, G., Macfarlane, F., Bate, P., & Kyriakidou, O. (2004). Diffusion of innovations in service organizations: systematic review and recommendations. International Journal of Information and Communications Technology, 3(8): 405-31.

- Hansen, S., & Wernerfelt, B. (1989). Determinants of firm competitiveness: The relative importance of economic and organizational factors. Strategic Management Journal, (10)5, 399-411.

- Heremans, D. (2007). Corporate Governance Issues for Banks: a Financial Stability Perspective, Working paper, No. 2. pg. 34.

- Hernando, I. & Nieto, M. (2007). Is the Internet delivery channel changing banks’competitiveness? The case of Spanish banks. Journal of Banking & Finance 31(4), 1083 -1099.

- Hicks, D. &Niehans J. (1998). Financial Innovation, multinational banking and Monetary Policy. Journal of banking and Finance, 537-551.

- Ighomereho, O. S., Afolabi, T. S. & Oluwakoya, A. O. (2022). Impact of E-Service Quality on Customer’s Satisfaction: A Study of Internet Banking for General and Maritime Services in Nigeria. Journal of Financial Services Marketing, 28, 488-501, org/10.1057/s41264-022-00164-x

- Ignazio, V. (2007). Financial Deepening and Monetary Policy Transmission Mechanism, BIS Review 124/2007

- Iriobe, G. O., Williams, H. T., Ayodele, T. D. & Afolabi, T. S. (2021). Financial Technologies’ Evolution and Traditional Banking: A Study of Retail Payments in Nigeria. Global Journal of Business, Economics & Management, 11(3), 163-177, doi.org/10.18844/gjbem.v11i3.5369

- Jegede, C. (2014). The effects of ATM on the Competitiveness of Nigerian Banks. American Journal of Applied Mathematics and Statistics, 2(1), 40-46.

- Kamau, M., & Oluoch, J. (2016). Relationship between Financial Innovation and Commercial Bank Competitiveness in Kenya. International Journal of Social Sciences and Information Technology, 2(4), 34-47.

- Karimzadeh, D., Emadzadeh, D., & Shateri, J. (2014). The effects of electronic banking expansion on profitability of a commercial bank (Sepah bank of Iran). Indian Journal of Scientific Research 4(6): 305–312.

- Kimingi, N. (2010). The effects of technological innovations on the financial competitiveness of the deposit money banks in Kenya. Unpublished MBA project, University of Nairobi.

- Kombo, D. & Tromp, D. (2009). Proposal and Thesis Writing; An Introduction. Nairobi, Kenya: Don Bosco Printing Press.

- Kumar, V., Batista, L., & Maull, R. (2011). The Impact of Operations Competitiveness on Customer Loyalty. Service Science, 3 (2), 158–171.

- Lavrakas, P. (2008). Encyclopedia of Survey Research Methods. United States of America, Los Angeles; Sage Publications.

- Lawrence, J. (2010). Technological Change Financial innovation and Financial Regulation in the The Challenges for Public policy. Retrieved From citeseerx.ist.psu.edu/viewdoc/ download?doi=10.1.1.155.1655

- Lemo, T. (2005). Regulatory oversight and stakeholder protection. A Paper Presented at the BGC Mergers and Acquisitions Interactive Seminar, held at Eko Hotels and Suite, 24th Victoria Island, Nigeria.

- Malhotra, P. & Singh, B. (2010). Experience in internet banking and competitiveness of banks. International Journal of Electronic Finance, 4(1), 64-83.

- Mengistu, B. (2018). Financial inclusion in Nigeria: Ten takeaways from the latest Findex Report. Accessed from: Https://blogs.worldbank.org/africacan/financial-inclusion-in -Nigeria-10-takeaways-from-findex-2017.

- Mensah, H. (2016). The effect of ICT on the competitiveness of twenty selected rural banks in Ghana. African Journal of Business Management, 8(12), 543-567.

- Mugenda, O. & Mugenda, A. (2003). Research Methods. Quantitative and Qualitative Approaches. Kenya, Nairobi; Acts Press.

- Muthinja, M. (2016). Financial Innovations and Bank Competitiveness in Kenya: Evidence from Branchless Banking Models. Ph.D. thesis, University of the Witwatersrand, Johannesburg, South Africa.

- Muthinja, M., & Chimwemwe, C. (2018). Financial innovation, firm competitiveness and the speeds of adjustment: New evidence from Kenya’s banking sector. Journal of Economic and Financial Sciences 11: 1–11.

- Nkem, I. & Akujinma A. (2017). Financial Innovation and Efficiency on the Banking Sub Sector: The Case of Deposit Money Banks and Selected Instruments of Electronic Banking. Asian Journal of Economics, Business and Accounting. 2(1), 1-12.

- Nofie, I. (2011). The Diffusion of Electronic Banking in Indonesia, Asian Journal of Accounting Auditing and Finance Research 3(7), 334 -354.

- Omondi, O. & Muturi, W. (2013).Factors Affecting the Financial Competitiveness of Listed Companies at the Nairobi Securities Exchange in Kenya. Journal of Finance and Accounting, 4 (15), 99 –104.

- Onay, C., & Ozsoz, E. (2013) The Impact of Internet Banking on Bank Profitability: The Case of Oxford Business Economics Conference Program.

- Oyerinde, D. (2011). Value and relevance of Accounting Information in Emerging Stock Market in Nigeria. Kampala: International Academic of African Business and Development (IAABD). Uganda.

- Paul H., Hamire, K. & Lombre, F. (2015). The effect of financial innovations on the profitability of banks in Ghana. African Journal of Business Management, 7(6), 326-346.

- Qamruzzaman, M. & Jianguo, W. (2019). Financial Innovation and Financial Inclusion Nexus in South Asian Countries: Evidence from Symmetric and Asymmetric Panel Investigation. Int. J. Financial Studies, 7(4), 61.

- Rahman, M. (2007). Innovative technology and bank profitability: the Bangladesh experience, Working Paper No.0803. Bangladesh Bank.

- Rauf, S. & Qiang, F. (2014). The integrated model to measure the impact of E-banking on commercial bank profitability: evidence from Pakistan. Asian Journal of Research in Banking and Finance 4 (1): 25–45

- Roberts, P. & Amit, R. (2003). The dynamics of innovative activity and competitive advantage: The case of Australian retail banking, 1981 to 1995. Indian Journal of Scientific Research, 14(2), 107-122.

- Rogers, E. (1995). Diffusion of Innovations, 4th ed. USA, New York; The Free Press.

- Rukiya, T. (2018). The effect of financial innovation on financial competitiveness of deposit money banks in Nigeria. Unpublished MBA project, Addis Ababa University.

- Sadr, L. (2013). The impact of internet banking on financial competitiveness of selected Asian Asian Journal of Accounting Auditing and Finance Research 13(14), 125-157.

- Sathye, M. (2009). Adoption of Internet banking by Australian consumers: an empirical International Journal of bank marketing, 27(17), 324-334.

- Satya Sekhar, G. (2018). Financial Innovation: Theories, Models and Regulation, Vernon Press Titles in Economics, Vernon Art and Science Inc, edition 1, number 373, December.

- Schumpeter, J. (1928). The instability of capitalism. The Economic Journal, 38 (151), 361-386.

- Silber, W. (1983). The Process of financial Innovation. American Economic Review Papers and proceeding, 89 -91.

- Solomon, W. (2016). Role of Electronic Banking on financial competitiveness of deposit money banks in Nigeria. Unpublished MBA project, Addis Ababa University.

- Sujud, H. & Hashem, B. (2017). Effect of Bank Innovations on Profitability and Return on Assets (ROA) of Deposit money banks in Lebanon. International Journal of Economics and Finance, 21(6), 35-50.

- Tilahun, D. (2016). Effects of Electronic Banking on the Financial Competitiveness of Deposit money banks in Nigeria. Unpublished MBA project, Addis Ababa University.

- Valverde, C. Santiago, R., López, P. and Francisco, R. (2016). Financial innovation in Banking: Impact on Regional Growth. Journal of Development Economics 10: 1–40.

- Victor, E. (2015). Measuring and Reporting Financial Innovation Competitiveness and its Indian Journal of Scientific Research 9(3), 405–432.

- Zarei, S. (2008). Risk management of internet banking. International Journal of Humanities and Social Science. 9(30), 422-439.