Investigating The Role of Internal Audtior’s Attributes in Preventing and Detecting Fraud in Business Organisations. A Case Study of Smes in Mutare Showground.

- Liberty D Mudzengerere

- Shelter Machingura

- Kudakwashe Munyepwa

- Memory Matsikure Cheure

- Allen mutumwa

- Denny Chakauya

- Tafadzwa Mudadi

- Tinashe Mudzengerere

- 727-770

- Mar 17, 2025

- Education

Investigating the Role of Internal Auditor’s Attributes in Preventing and Detecting Fraud in Business Organisations. A Case Study of Smes in Mutare Showground.

Liberty D Mudzengerere, Shelter Machingura, Kudakwashe Munyepwa , Memory Matsikure Cheure, Allen mutumwa, Denny Chakauya, Tafadzwa Mudadi, Tinashe Mudzengerere

Manicaland State University, Mutare, Manicaland, Zimbabwe

DOI: https://doi.org/10.51244/IJRSI.2025.12020061

Received: 10 February 2025; Accepted: 14 February 2025; Published: 17 March 2025

ABSTRACT

This research investigated the role of internal auditor’s attributes in preventing and detecting fraud in business organizations. The focus was on the influence of internal auditor’s attributes in the prevention and detection of fraud. A case study of 54 respondents in SMEs in Mutare Showground was carried out using both qualitative and quantitative research approaches. Stratified random sampling was used when distributing questionnaires and a convenient sampling method when carrying out interviews. Data analysis was done using tables, charts, graphs, descriptive tables, chi-square test and multiple linear regression model with IBM SPSS version 21 and Amos V18 to produce output tables. The results show that auditor experience has a positive and significant effect on fraud prevention and detection, auditor ethics has a positive and significant effect on fraud prevention and detection, professional scepticism has a positive and significant effect on fraud prevention and detection and auditor’s competency has a positive and significant effect on fraud prevention and detection. However, internal auditors in SMEs in Mutare Showground does not have the ability to prevent and detect fraud effectively as they do not have sufficient resources to employ qualified internal auditors, limited scope, pressure to maintain profitability in a competitive environment and nature as a small organisation. The findings of this study are supported by agency theory, fraud triangle theory and red flag theory. The study concluded that there is a positive correlation between auditor’s attributes and their ability to prevent and detect fraud.

INTRODUCTION

The informal and small to medium entities plays a crucial role in the global economy, serving as the backbone of economic activities and facilitating transactions worth trillions of dollars. However, this vital sector is not immune to the threat of financial crimes such as fraud, which have far-reaching consequences, including reputational damage, financial losses, and destabilisation of the financial system. In this context, to mitigate these risks, organizations rely on internal auditors to play a crucial role in preventing and detecting fraud.

Internal auditors act as independent third parties responsible for examining and evaluating the financial records and processes of organizations to assure their accuracy and compliance with relevant laws and regulations. Internal auditors’ role in detecting and preventing fraud is paramount, as it is tasked with identifying red flags, inconsistencies, and suspicious activities that may indicate financial crimes.

This research delved into the specific attributes of internal auditors that contribute to their effectiveness in safeguarding organizational assets and maintaining financial integrity. There was an examination of the impact of internal auditors’ attributes in the prevention and detection of fraud in business organizations.

Background

According to Zimstats Fraud Crime Report (2022), Zimbabwe has been plagued by numerous financial scandals and cases of fraud. This has been seen in all forms of fraud including check forgery, inventory and cash theft, expense fraud, procurement fraud, payment fraud, vendor fraud, bribery, accounting fraud and payroll fraud. These incidents have had severe repercussions on the country’s economy and its reputation in the global business community.

According to Anto et al (2020), internal auditors are pillars that serve as supervisors as well as guards in the implementation of internal controls required to prevent and detect the potential fraud that would occur in a business organization. One of the internal auditors’ roles is to discover weaknesses within the business organization to prevent fraudulent acts in advance. Auditors must make it challenging for criminals to take advantage of the vulnerabilities (Bologna, 2019).

According to the Annual Corruption Report (2021) and World History Fraud Cases (2020), the statistics of Fraudulent Cases in Parastatals and Private Companies show that companies have lost billions of funds. This shows that the financial sector has a crucial role in the global economy, serving as the backbone of economic activities and facilitating transactions worth trillions of dollars and the auditors act as immune to the threat of financial crimes which can have far-reaching consequences, including reputational damage, financial losses, and destabilization of the financial system. In this context, internal attributes are essential in executing their responsibilities of giving assurance, prevention and detection of fraud in business organizations.

In the USA, a study was conducted by Siahaan et al (2024), Wirecard Scandal in 2020 were $2.1 billion was lost by missing from its accounts leading to insolvency and a massive scandal. Due to this Siahaan et al (2024), investigated the roles of internal auditors in preventing and detecting fraud stating that auditors should be competent enough with the experience to prevent and detect fraud. He also stated that internal auditors should have a questioning mindset on certain financial transactions and information being provided by the management. This has been supported by International standards such as the International Standards on Auditing (ISA), and International Auditing and Assurance Board (IAAB) providing guidelines for auditors to effectively follow to detect and prevent fraud in organizations such as ISA 240 ( The Auditor’s Responsibility Relating to Fraud in Audit of Financial Statement) stating that auditors should maintain professional scepticism throughout the audit and IAS 315( Identification and Assessment of Risks of Material Misstatement Through Understanding the Entity and its Environment) stating that auditors should focus on understanding the entity’s business including its risk of fraud and red flags which can give auditors hits to fraud.

In South Africa, a retail holding company Steinhoff Retail Africa, is one of the largest companies in Africa. In 2017, accounting irregularities involving misstating revenue and profits over several years led to the resignation of the CEO. As a result of this, research has been conducted by Mkhize (2020), a student from Cape Town University on the prevention and detection of fraud and concluded that there was a lack of expertise, independence and objectivity in auditors’ ability to prevent and detect fraud. This is in line with professional bodies like the Association of Accountancy Bodies in West Africa (ABWA) and the Pan African Federation of Accountants (PAFA) which guide auditors on fraud detection techniques and best practices. The Association of Certified Fraud Examiners (ACFE) South Africa Chapter also work closely with auditors to provide training and resources on fraud detection techniques.

Many fraud scandals happened in Zimbabwe according to Auditors’ General Report2023. National Railways of Zimbabwe (NRZ) looted and price inflation scandals involving top management leading to significant financial losses and operational disruptions. In Zimbabwe United Passenger Company (ZUPCO), there was bribery and corruption in procurement processes. In Zimbabwe Mining Development Corporation (ZMDC), there were diamond mining revenue losses and corruption causing significant revenue loss to the government and damage to the country’s reputation. There was also Corruption, theft of electricity, and financial mismanagement in the Zimbabwe Electricity Supply Authority (ZESA) which has leads power shortages, increased load shedding, and financial losses. This has been also supported by Mtombeni et al (2023) on malpractices in government companies.

Due to this, it shows that internal auditors have a role to play in the stability of an economy. The Institute of Chartered Accountants of Zimbabwe (ICAZ) regulates the accounting profession and sets standards for auditors to follow from ISA, IAASB and money laundering regulations imposed by the Reserve Bank of Zimbabwe (RBZ) and the Financial Intelligence Unit (FIU). According to Lu Y & Ma D (2024), auditors must be vigilant in detecting financial irregularities, conducting thorough risk assessments, and reporting suspicions of fraud to relevant authorities. The above researchers looked into fraud side of events and this research is going to investigate the role of internal audtior’s attributes in preventing and detecting fraud in business organisations.

Statement of the problem

Fraud remains a pervasive challenge in Zimbabwe, undermining corporate governance, public trust and economic development, despite auditors in both the public and private sectors. High-profile scandals reveal alarming levels of financial misconduct, as highlighted by the 2023 Auditor-General’s report, which noted over USD 100 million in unaccounted-for funds across various government entities. The collapse of the National Social Security Authority (NSSA) exemplifies failures in fraud detection, where auditors overlooked significant fraudulent activities. While internal auditors implement controls to combat fraud, challenges persist, suggesting that factors such as professional skepticism, competence, experience, and independence may influence auditors’ effectiveness. However, there is limited empirical evidence on how these attributes affect fraud mitigation in Zimbabwe, particularly within small and medium-sized enterprises (SMEs). This study aimed to investigate the impact of auditor attributes on their fraud detection and prevention capabilities in this context.

Research Gap

Despite the extensive literature on the roles of auditors in preventing and detecting fraud in business organizations, there is a noticeable gap in the specific examination of the practices of internal auditors’ attributes in effectively addressing issues of fraud. According to Yusoff et al (2023), the studies have highlighted the importance of auditors in fraud detection and prevention. Kourtesis (2019), focused on the research determinants of the ability to prevent and detect fraud in the business formal sector. However, there is limited research focusing on the roles of internal auditors’ attributes in preventing and detecting fraud in SMEs. Understanding the specific challenges, strategies, and best practices employed by SMEs, the researcher went to investigate on the role of internal auditor’s attributes in preventing and detecting fraud in SMEs in Mutare Showground.

Purpose

This research investigated the role of internal auditors’ attributes in preventing and detecting fraud. In examining the specific qualities and competencies possessed by effective internal auditors, this study aimed to identify the key factors that contribute to their success in safeguarding organizational assets and maintaining financial integrity. This research contributed to a deeper understanding of the essential characteristics that organizations should seek in internal auditors to strengthen their fraud prevention and detection capabilities. It provided valuable insights for organizations to enhance their internal audit functions and mitigate the risks of fraudulent activities.

Research Objectives

- To determine how auditors’ experience influences the auditor’s ability to prevent and detect fraud.

- To determine the extent to which auditors’ ethics influence the auditor’s ability to prevent and detect fraud.

- To establish the effect of professional scepticism on the auditor’s ability to prevent and detect fraud.

- To determine the extent to which auditors’ competency influences the auditor’s ability to prevent and detect fraud

Research Questions

- How does auditors’ experience influence the auditor’s ability to prevent and detect fraud?

- What is the influence of auditors’ ethics on the auditor’s ability to detect and prevent fraud?

- What is the effect of professional scepticism on auditors’ ability to detect and prevent fraud?

- To what extent does the auditors’ competency affect the auditor’s ability to detect and prevent fraud?

Hypothesis

H1: Auditors with more years of experience have a higher ability to detect and prevent fraud compared to less experienced auditors

H2: Higher levels of ethical standards in auditors positively influence their ability to detect and prevent fraud.

H3: Increased levels of professional scepticism significantly enhance auditors’ ability to detect and prevent fraud.

H4: Auditors with higher competency, as measured by qualifications and specialized training, demonstrate greater effectiveness in detecting and preventing fraud.

Definition of key terms

- Internal Auditor: A professional who provides independent assurance and consulting services to enhance an organization’s operations and risk management (Turetken, 2020). An internal auditor is a skilled professional who plays a crucial role within an organization by providing an independent and objective assessment of the organization’s operations, financial reporting, and internal controls, analyzing processes, identifying weaknesses, and recommending improvements, internal auditors help to mitigate risks, enhance efficiency, and ensure compliance with relevant regulations (Christ, 2021).

- Fraud: Intentional deception for personal gain, often involving misrepresentation, concealment, or breach of trust. Fraud is a deliberate act of deception intended to gain an unfair advantage or illicit benefit (Karpoff, 2021). It involves dishonest and unethical behavior, such as misrepresentation, concealment, or breach of trust and fraud can take many forms, including financial fraud, cybercrime, and employee fraud (Rashid, 2022). The consequences of fraud can be severe, leading to financial losses, reputational damage, and legal repercussions.

- Prevention of Fraud: Proactive measures taken to deter and discourage fraudulent activities, such as implementing strong internal controls, conducting regular risk assessments, and fostering a culture of integrity (Rashid, 2022).

- Detection of Fraud: Identifying and uncovering fraudulent activities through various methods, including data analysis, surveillance, investigations, and whistleblowing (Hilal, 2022).

- Auditor’s Attributes: The personal qualities, skills, and knowledge that enable an auditor to effectively perform their duties, including professional scepticism, independence, objectivity, and technical competence (Lamboglia, 2021).

- Professional Scepticism: A questioning mind and critical attitude that is essential for effective auditing and involves a healthy dose of doubt and a willingness to challenge assumptions (Brazel, 2022). A professional auditor must possess a questioning mind and a critical attitude and involves a healthy dose of doubt and a willingness to challenge assumptions, even when faced with seemingly credible information (Agustina, 2021). In maintaining a sceptical mindset, auditors can identify potential risks and uncover hidden issues that may not be apparent at first glance.

- Independence: The freedom from influence or bias that allows an auditor to make objective judgments (Kapla, 2020). Auditors must be free from any influence or bias that could compromise their judgment and this includes avoiding conflicts of interest, maintaining objectivity, and adhering to professional standards. Independence allows auditors to provide unbiased assessments and recommendations (Jefferson, 2019).

- Objectivity: Impartiality and fairness in carrying out audit work (Galison, 2021). Objectivity requires auditors to be impartial and fair in their work and auditors must avoid personal biases and consider all relevant information when forming opinions and making decisions

- Technical Competence: skills and knowledge to perform audit tasks effectively, including understanding accounting principles, auditing standards, and relevant regulations (Kourtesis, 2019)

- Experience: In auditing refers to the practical knowledge and skills gained through direct involvement in auditing engagements over time (Ghanbari-Homaie, 2021). It’s a valuable asset for auditors through practical experience in auditing engagements, auditors develop the skills and knowledge needed to assess risks, evaluate internal controls, and provide insightful recommendations.

LITERATURE REVIEW

Introduction

Internal audit has existed for a long time but it was not given much importance in the past. It has now become more forefront because of an increase in financial scandals like Enron and WorldCom. Internal audit investigative skills must prevent and detect financial crimes. An internal audit is a health check to ensure that the company is on track to achieve its goals by identifying risks and inefficiencies that could hinder the organization from achieving its objectives. This chapter focuses on the documentation of an exhaustive literature review of published and unpublished work in line with the researcher’s areas of interest. The chapter’s structure is guided by the research objectives and it explores some concepts, developments and findings by various authors, specialists and researchers on internal auditing. This review encompassed literature specific to Zimbabwe while incorporating relevant research from developed, and developing countries and the rest of the world. This chapter also covers the theoretical framework, conceptual framework and empirical evidence, critically evaluating it to establish knowledge gaps which the research was aimed at discovering.

Literature Review

According to the Association of Certified Fraud Examiners (ACFE) (2018), fraud is defined as any intentional deception or misrepresentation that an individual or entity makes, knowing it to be false and that it could result in some unauthorized benefit to the perpetrator. This has also been supported by the Financial Action Task Force (FATF) (2021), as dishonest and illegal activities undertaken by individuals or entities intending to deceive for financial gain or other benefits. It involves intentional acts that are deceptive, designed to mislead others for personal or financial gain, and may include financial statement fraud, misappropriation of assets, or corruption schemes (American Institute of Certified Public Accountants (AICPA), 2019). According to the International Federation of Accountants (IFAC) (2021), fraud involves an intentional act by one or more individuals among management, those charged with governance, employees, or third parties, involving the use of deception to obtain an unjust or illegal advantage. Securities and Exchange Commission (SEC) (2022), also stated that fraud encompasses a wide range of illegal actions characterized by intentional deception or misrepresentation for financial gain, often involving securities trading or investment schemes and this has been supported by Doig et al (2021); Kaur et al (2023) & Karpoff (2021).

Internal auditors play a crucial role in preventing and detecting fraud within organizations by providing independent and objective assessments of internal controls, risk management processes, and compliance with regulations (Ratmono et al, 2022). Internal auditors are responsible for assessing the effectiveness of internal controls and identifying weaknesses that could be exploited by fraudsters. According to Albrecht et al (2020), internal auditors should have a deep understanding of the organization’s operations, processes, and risks to effectively evaluate the adequacy of controls. In conducting risk assessments and testing controls, internal auditors can help identify vulnerabilities that may increase the likelihood of fraud occurring.

Chang et al (2019), defined internal auditor’s attributes as qualities, skills, and knowledge that enable internal auditors to effectively carry out their responsibilities. This has been supported by Khan (2020), internal auditors’ attributes are the essential qualities and skills that enable them to effectively assess and improve an organization’s governance, risk management, and internal control processes. According to Botha et al (2020), some examples of internal auditors’ attributes include experience, professional scepticism, competency, communication skills, resilience and ethics. This has been supported by Boskou (2019), some examples of internal auditors’ attributes include ethics, competency and professional scepticism. All these attributes work together to empower internal auditors to provide unbiased evaluations, identify risks, ensure compliance, and enhance overall organizational integrity.

Experience

According to Heymann (2020), experience has been defined as practical knowledge and skills gained through working in a specific field. Indah et al (2022), defined it as knowledge, skills, and understanding gained through practical involvement in a particular field or activity. Experience has been considered to help internal auditors in preventing and detecting fraud as it leads to practical knowledge, exposure to various scenarios, problem-solving skills, industry familiarity and relationship building (Ainscow, 2020). According to Indah (2022), seasoned auditors have encountered various scenarios and challenges, equipping them with insights into common fraud schemes and red flags and their practical knowledge allows them to navigate complex situations, make informed judgments, and implement effective fraud prevention strategies based on experiences.

Ethics

Ethics has been defined by Dewey et al (2020) as a branch of philosophy that explores moral principles and values and it delves into questions of right and wrong, good and bad, and seeks to understand what constitutes moral behaviour as it guides individuals and societies in making decisions that are just, fair, and beneficial. In auditing, ethics is a critical aspect of the profession as involves adhering to a code of conduct that ensures the integrity, objectivity and independence of the audit process (Morley, 2020). Jobin et al (2019) stated that auditors must be honest, truthful, unbiased and confidential in their role of preventing and detecting fraud. Ethical behaviour in auditing is crucial as it leads to quality work, creates trust and creditability, deterrence of fraud, transparent, long-term relationships and professional reputation. This has been supported by Asaro (2020) stating that ethical behaviour as an auditor leads to public trust, unbiased judgement, accurate reporting, detection of fraud and professional reputation.

Professional Scepticism

Internal auditors must have a questioning mind, a critical assessment of evidence, and a willingness to challenge assumptions and assertions made by management and others and that is called professional scepticism according to Brazel (2022). Professional scepticism has also been defined by Agustina (2021) as an attitude that includes a questioning mind, being alert to conditions that may indicate possible misstatement due to error or fraud, and a critical assessment of the evidence. Professional scepticism allows fraud detection, audit quality, objectivity, risk assessment and continuous improvement (Stevens. 2019). This has been supported by Hardies et al (2021), professional scepticism helps in detecting fraud and errors, maintaining public trust, preventing material misstates and adapting to evolving risks. According to Brazel (2022), professional scepticism supports informed decision-making by providing reliable and accurate findings, which is essential for stakeholders and builds trust and credibility in the audit process, ensuring that financial reporting remains transparent and reliable.

Competency

According to Wong et al (2020), competency it’s refers to the combination of knowledge, skills, abilities, and behaviors that enable an individual to perform their job effectively. Long et al (2020), defined competency as the ability to apply knowledge and skills effectively to complete a task or achieve a goal. In the auditing context, it has been defined by Karsenti et al (2020), as the ability of an auditor to apply relevant knowledge, skills, and judgment to effectively carry out their duties. It also has been called the essential knowledge, skills, and abilities that auditors must possess to perform their duties effectively and deliver high-quality audit services. Competency in auditing allows for accurate reporting, effective risk assessment, and efficient and effective audits (Boudet al. 2023). This is also in line with Redman et al (2021), competency in auditing allows quality assurance, regulatory compliance, professional credibility and continuous improvement.

Auditors ability to prevent fraud

Auditors’ ability to prevent and detect fraud is called internal auditors’ capacity to identify potentially fraudulent activities before they occur and to uncover them if they have taken place (Hashim; 2019). Kassem (2021), defined auditors’ ability to prevent and detect fraud as the ability to possess the skills, knowledge, and ethical standards to identify and mitigate risks that could lead to fraudulent activities. This ability is backed up by internal auditors’ attributes such as experience, ethics, professional scepticism, and competency. This has been supported by Bauer (2020), ability of internal auditors to prevent and detect fraud is significantly enhanced by their key attributes.

As this research is using internal auditors’ attributes of auditors in SMEs in Mutare Showground, there are high chance that their ability to prevent and detect fraud is low or poor. This is normally because internal auditors in small and medium-sized enterprises (SMEs) ability to prevent and detect fraud is often hindered by several challenges. Many SMEs lack the resources to employ qualified or experienced internal auditors, resulting in a workforce that may not possess the necessary ethical behaviour and a sceptical mindset or training to identify complex fraudulent activities (Sule, 2019). Coffee (2019), also said that the limited scope of internal audits in SMEs can lead to insufficient evaluation of internal controls, leaving vulnerabilities unaddressed. According to Khaksar (2022), the often-informal nature of processes in smaller organizations may also contribute to a lack of documented procedures, making it difficult for auditors to establish effective controls. The pressure to maintain profitability in a competitive environment can also lead to a culture that prioritizes short-term gains over robust risk management practices (Hashim, 2019). Internal auditors in SMEs may struggle to effectively prevent and detect fraud, exposing the organization to greater risk.

Despite the perceived limitations, research has demonstrated that internal auditors in SMEs can effectively prevent and detect fraud when proper structures are implemented. Contrary to common assumptions by Mwangi (2021), found that smaller audit teams in SMEs often develop deeper institutional knowledge and closer relationships with operations, enabling them to spot irregularities more quickly than their counterparts in larger organizations. The focused scope of SME operations can be advantageous, as internal auditors can dedicate more attention to high-risk areas and develop specialized expertise in industry-specific fraud schemes (Kumar & Patel, 2022). Williams (2020), revealed that SME internal auditors frequently demonstrate higher levels of professional scepticism due to their direct exposure to daily operations and closer working relationships with management. Additionally, Zhao et al (2023), found that the informal nature of SME processes can enhance fraud detection, as auditors can more easily identify deviations from established patterns without being constrained by rigid corporate structures. Implementing cost-effective technology solutions has also significantly improved SME auditors’ capabilities, with Ahmed (2022), reporting that automation tools have enabled smaller audit teams to achieve detection rates comparable to those of larger enterprises. Rodriguez (2023), discovered that SMEs internal auditors often receive more direct support from management, leading to stronger ethical cultures and more effective fraud prevention programs.

Theoretical Framework

Agency Theory

Agency theory was first developed by Stephen Ross and Barry Mitnick in 1976, focusing on the relationship between two parties, the agent and the principal. The agency must act on behalf of the principal, with the expectation that the agents will make decisions in the principal’s best interest achieving the shareholder’s objective of wealth maximization (Raimo et al, 2021). Its main aim was to explain globally the relationship between managers, directors and the shareholders of the company (Zogning, 2022). A conflict of interest exists when directors and managers want to focus on short-term objectives to boost their bonuses. In order to mitigate the conflict of interest between directors, managers and shareholders, internal auditors need to put in place internal controls to prevent and detect the misdoing of the directors and managers of the company to achieve company objectives. According to Huong et al (2022), internal auditors act as the check on managers and directors to reduce agency problems. This has been supported by the latest Cardiberry Report UK, (2023); King Code IV SA (2016) and Zimcode (2015) that auditors should solve the agency problem and work in the best interest of the owners of the company. Internal auditors review processes, identify risks and ensure that controls are in place. Internal auditors must act independently, honestly and faithfully when curbing the agency problem without the influence of managers and directors of the company (Ma’Ayan et al, 2016). This theory has been used by many researchers in various departments such as accounting, finance, economics and law. This theory has been supported by Anie et al (2021), saying that the participation of female directors reduces agency costs as they provide better monitoring roles. Panda et al (2017), also said that the conflict of interest and agency cost rise due to the separation of ownership from control, different risk preferences, information asymmetry and moral hazards.

For internal auditors to work effectively and efficiently for shareholders to solve the conflict of interest between the shareholders, and managers and directors, internal auditors’ attributes such as experience, ethics, professional scepticism, and competency are crucial in solving the problem. This has been supported by Agustina (2021), stating that experienced auditors can effectively assess the risks and controls in place, identifying potential areas of weakness to ensure that shareholders’ objectives are met whilst ethics ensures that auditors act with integrity and objectivity, holding management accountable for their actions. According to Surya et al (2021), a sceptical approach helps auditors uncover hidden information and challenge misleading representations to the shareholders by managers and directors of the company whilst competency helps internal auditors analyze complex financial information and identify inconsistencies or red flags.

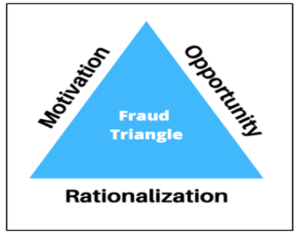

Fraud Triangle Theory

The diagram shows three conditions which increase the chances of committing fraud which are pressure, opportunity and rationalization.

According to Awang et al (2020), the fraud triangle theory was developed by Donald Cressy in the 1970s to understand the reasons behind the committing of fraud by people. Donald Cressy stated that three conditions can increase the chances of committing fraud which are pressure, opportunity and rationalization.

Pressure

According to Kotter et al (2020), pressure is a force being applied over an area while Hanson (2020), defined pressure as a feeling of stress or urgency and Donald Cressey said that pressure is the root cause for people to commit fraud (Awang et al, 2020). According to Knisley et al (2022), different types of pressure include personal stress, employment stress, and external pressure. Setiawan (2019), further examines personal and corporate forces as causes of fraud commitment. For example, pressure can be greed, living beyond one’s means, large expenses or personal debt, family financial problems or health, drug addiction and gambling. Several studies (Hollow 2014; Azam2018; Anindya et al2019 and Gill et al (2016), pinpoint pressure as the major reasons for committing fraud. They also stated that many sources of pressure include financial strain, personal issues, company culture and career advancement.

The fraud triangle theory helps internal auditors identify the root cause of committing fraud which could be prevented at early stages rather than being detected at a later stage as prevention is better than cure (Chelation, 2023). According to Kagias et al (2022), fraud theory can help to identify red flags especially when employees are living beyond their salary capabilities could cause them to commit fraud. However internal controls will be tailored towards specific pressure (Sanchez-Aguayo, 2021). In order to understand the pressure and be able to identify red flags (Kagias et al, 2022), internal auditors should have experience, competency and professional scepticism in the field (Adikaram, 2024).

However, according to Schunter (2016), some argue that pressure cannot be the only reason for committing fraud, some people commit fraud because of a lack of ethical standards or maybe because someone has an opportunity to commit fraud regardless of being under pressure or not.

Opportunity

The other element that contributes to committing fraud is opportunity according to the Fraud Triangle Theory in 1970 (Awang et al, 2020). Tunley (2011), defined an opportunity as circumstances that allow fraudulent activities to take place. According to Wang (2021), people are more likely to commit fraud if they see a chance of getting away with it. The lower the risk of getting caught, the higher the chances of committing fraud (Kagias et al, 2022).

Usually, the chances of committing fraud increase when there are weaknesses in the company system. This mostly happens when the company does not take necessary action when employees break the rules (Sujeewa, 2018). According to Kagias et al (2022), weak controls make it possible for employees to temper with them to commit fraud. There is support from Lokanan (2015), that even if someone is pressured to commit fraud, they cannot do it unless there is an opening door.

Through experience internal auditors can identify red flags and patterns associated with fraudulent activities, reducing opportunities for fraud to go unnoticed and an ethical framework discourages fraudulent behaviour by promoting a culture of honesty and accountability within the organization (Kim et al, 2022). Professional scepticism encourages auditors to critically assess information and challenge management assertions, which can uncover opportunities for fraud being backed up by competency (Braze 2022). All this shows that internal auditors’ attributes are crucial in achieving organizational goals.

Rationalization

According to Schunter (2016), rationalization is coming up with good reasons for our unethical behaviour. It can be described as justification and an excuse for the wrongdoing (Cheliatsidou, 2023). For example, someone can commit fraud because he has no money to feed the family so they are left with no other option except stealing. Knisley et al (2022), state that justification it’s a way to run away from crime which is not valid in the eyes of the law as it’s a lack of ethical behaviour. According to Mansor et al (2015), rationalization is an indirect indicator of committing fraud, internal auditors cannot assess a person’s thoughts. This means that professional scepticism is a required tool by internal auditors when preventing and detecting fraud (Brazel et al, 2021).

Red Flag Theory

Red Flag Theory has been developed by many authors in different dimensions which are Karen Horney in 1937, John Bowlby in 1951, Aaron Beck in 1967, Dorothy in 1979, Hendrik Van Brenen in 1983 and Amir Levine in 2006. In all of their findings, a conclusion was made that red flags are warning signs of a potential problem. Izebige et al (2020), defined red flags as a systematic way of detecting the symptoms or any signs of fraudulent activities within the organizational settings. According to Oktaroza (2022), red flags are indicators or warning signs that may represent fraud or irregularities. He also stated that fraud detection does not always get a bright spot as fraudsters use many ways to commit fraud and this gives the need to understand and recognize red flags within a business organization. Professional scepticism is a requirement to spot these red flags.

According to Moyes et al (2019), they are several examples of red flags within an organization which auditors must take note which include excessive personal debt, material lifestyle with low income, gambling, alcohol and drugs addiction, greediness, lack of job rotation, lack of supervision, lack of training, lack of auditing firms, lack of personal ethics and morality, too much power and resistance to stress. According to Perlo-Freeman (2029), red flags are mainly divided into pressure and opportunities linked with triangle fraud theory. All these red flags cannot be detected or prevented if internal auditors are not competent enough to identify them. This has been supported by Wong (2020), stating that competent auditors are knowledgeable about common fraud schemes, enabling them to identify patterns or behaviours that may indicate fraudulent activity.

According to Finucane et al (2020), red flags are important to internal auditors as they are indicators of fraudulent activities. This means that auditors must assess the risk associated with each red flag to put effective control measures in place. For internal auditors to identify red flags, audit experience, competency and scepticism are requirements (Faradina 2021).

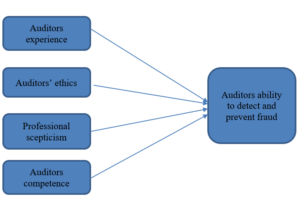

Conceptual framework

This study examines the impact of internal auditor’s experience, ethics, professional scepticism, and competence on their ability to detect and prevent fraud. The conceptual framework of this research can be seen in Figure 1 as follows.

Independent variables Dependent variable

Fig 1:- The diagram illustrates the relationship between the independent and dependent variables.

The effect of auditor experience on fraud detection and prevention

According to Faradina (2021), audit experience is an experience gained from the number of tasks that have been handled by the auditor. Auditors with a lot of experience can detect fraud as soon as it occurs in the company and can provide a better explanation than auditors with little experience. The more auditors perform their roles, the higher the level of experience owned by the auditors. Auditors without experience may not necessarily be able to find fraud in the company.

Experience is a powerful tool in the hands of an internal auditor. According to Wahidahwati et al (2020), experienced auditors can recognize patterns of fraudulent behaviour, identify red flags, and assess the effectiveness of internal controls. Daoust (2019), stated that experienced auditors have a keen eye for anomalies and inconsistencies, allowing them to uncover hidden risks and potential fraud schemes. In drawing on their experiences, internal auditors can anticipate emerging threats and develop strategies to mitigate them (Kim et al, 2020). Additionally, experienced auditors can effectively communicate with management and other stakeholders, building trust and fostering a culture of integrity and accountability through their knowledge and insights, experienced auditors play a crucial role in preventing and detecting fraud, safeguarding the organization’s assets, and protecting its reputation.

Due to this, Kartikarini et al (2021), stated that internal auditors’ experience improves fraud detection. These results indicate that the auditors must have good audit experience when conducting an audit. Auditors with a lot of experience can find out various audit problems in more depth, besides those auditors will find it easier to follow increasingly complex developments.

H1: Auditor experience has a positive effect on preventing and detecting Fraud

The effects of auditor ethics on fraud detection and prevention

Ethics is related to morals that become the guide for a person or a group of nature to regulate their behaviour and benchmarks in assessing the goodness or badness of an action (Morley, 2020). An auditor must comply with ethical rules in carrying out their duties to facilitate in detection of fraud (Susanto et al, 2021). According to Helmiati & Helmiati (2021), auditor ethics improves fraud detection and prevention. This shows that if an auditor follows the regulated professional ethics, it will guarantee the quality and increase the ability to detect and prevent fraud owned by the auditor. According to Agustia et al (2020), the application of ethical rules owned by an auditor affects quality audit results. The quality of the work audited by an auditor is influenced by the ethical application of an auditor. Detection and prevention of fraud in the audit of the company’s financial statements requires the auditor to have ethics because ethical auditors have integrity and objectivity in carrying out their work. According to Arief et al (2020), the application of ethical rules is defined as principles, rules, and moral values applied to regulate the behaviour of an auditor in carrying out his duties. Three values must be applied by auditors which are independence, integrity and professionalism The ethics of auditors when auditing reports can affect audit results to be of higher quality (Khadilah et al, 2020). This means that the quality of the audited financial statements can be influenced by the ethics of the auditors.

However, ethical rules can be effective in fostering a culture of integrity and discouraging fraudulent behavior but they are not a foolproof solution. Jaganjac (2024), argue that sole reliance on ethical rules can be insufficient in preventing and detecting fraud as individuals may still circumvent ethical guidelines, particularly in environments with weak internal controls or a lack of oversight. According to Trevino (2021), ethical rules can be subjective and open to interpretation, which may lead to inconsistent application and enforcement and fraudsters often employ sophisticated techniques to conceal their activities, making it difficult to detect them solely through adherence to ethical principles.

H2: The application of ethical rules has a positive effect on preventing and detecting Fraud.

The effect of professional scepticism on fraud detection and prevention

According to Adikaram (2024), professional scepticism is a crucial mindset for anyone in a field where critical thinking and questioning assumptions are important. This means that auditors can question where it seems suspicious and deepen their investigation. This shows that the higher the professional scepticism of an auditor, the higher they will prevent and detect fraud. Audit professional requires auditors to exercise professional scepticism which includes an attitude of questioning mind and objectively evaluating the adequacy, competence, and relevance of evidence according to the International Standard on Auditing 200 (ISA200).

The International Auditing and Assurance Standard Board (IAASB), explain that professional scepticism is an attitude that always questions the validity of data and evaluates audit evidence critically. According to Umri (2022), the higher the attitude of scepticism owned by the auditor, the greater the fraud that will be detected and prevented. According to Kartikarini et al (2021), the attitude of professional scepticism improves the ability of an auditor to detect fraud. The higher the attitude of professional scepticism that the auditor has, the more signs of fraud around him will be prevented and detected. According to Fullerton and Durtschi (2020), auditors with high scepticism will increase their ability to detect and prevent fraud by developing additional information searches when faced with signs of fraud.

Auditors must have an attitude of professional scepticism in carrying out their audit duties, especially for fraud prevention and detection and auditors with a sceptical attitude will not immediately believe the assertions given by management (Brasel, 2019). Auditors will always look for additional information and evidence that can support management’s assertions. Auditors with an attitude of professional scepticism in making decisions and providing opinions will be more careful, the auditor will also seek additional information and evidence to ensure that the audited financial statements are free from all forms of misstatement (Wells 2019).

According to Martinov‐Bennie et al (2022), professional scepticism is a vital attribute for internal auditors in preventing and detecting fraud as they work with a questioning mind, challenging assumptions, identifying inconsistencies, and uncovering hidden issues. A sceptical mindset allows auditors to critically evaluate evidence, seek additional information, and avoid taking things at face value (Agustina et al, 2021). This helps to identify red flags, such as unusual transactions, unexplained variances, or inconsistencies in documentation. In maintaining a sceptical attitude, internal auditors can play a crucial role in safeguarding the organization’s assets and reputation, reducing the risk of fraud, and ensuring the accuracy and reliability of financial information (Hoos, 2019).

According to Helmiati et al (2021), professional scepticism improves an auditor’s ability to detect fraud, because the higher the scepticism of an auditor, the higher the level of the auditor’s ability to detect fraud.

However, according to Rinard (2022), a sceptical mindset can sometimes lead to over-cautiousness or excessive doubt, potentially resulting in missed opportunities to identify legitimate financial practices. Hoos (2019), also stated that auditors may become insensitive to scepticism over time, leading to a perfunctory approach that fails to engage deeply with the nuances of each audit. According to Hardies (2021), the increasing complexity of financial transactions and fraud schemes can overwhelm even the most sceptical auditor, making it difficult to discern between genuine anomalies and normal variations in data and an auditor’s scepticism may be undermined by organizational pressures or relationships with clients, which can compromise their objectivity and lead to complacency in scrutinizing suspicious activities.

H3: Professional Scepticism Has a Positive Effect on Fraud Prevention and Detection

The effect of auditors’ competency on fraud detection and prevention

According to Hariyani et al (2024), audit competency refers to the knowledge, skills and behaviour an auditor needs to effectively perform their duties. It’s a combination of technical expertise, professional judgement and personal qualities that allow auditors to conduct high-quality audits and deliver valuable insights (Gunawan et al, 2021). According to Noch et al (2022), auditors’ competence improves the ability of auditors to prevent and detect fraud. The higher the audit competence in the field the higher the quality of audit in preventing and detecting fraud (Handoko et al, 2022). This means that the auditor must have expertise in auditing and sufficient knowledge of the field being audited.

All this has been supported by the fact that competent auditors possess knowledge, skills, and judgment to identify and assess risks, evaluate controls, and uncover fraudulent activities and their technical expertise allows them to analyze complex financial data, understand accounting principles, and apply relevant auditing standards (Marwa, 2019). According to Maresch (2020), strong analytical and problem-solving skills enable internal auditors to identify anomalies, inconsistencies, and red flags that may indicate fraudulent behaviour and by staying updated on industry trends, regulatory changes, and emerging fraud schemes, competent auditors can proactively address potential risks and safeguard the organization’s assets.

However, highly skilled auditors can be limited by the inherent complexity and sophistication of modern fraud schemes, which can outstrip their training and experience (Mandal, 2024). According to Maulid (2021), auditors may face time constraints and workload pressures that hinder their ability to conduct thorough investigations, regardless of their competence and competent auditors might still rely heavily on management representations and insufficiently challenge assumptions, leading to potential oversight of fraudulent activities. The effectiveness of competent auditors can be compromised by a lack of organizational support or a culture that discourages questioning and scepticism (Rashid, 2022).

H4: Auditors’ Competency Has a Positive Effect on Fraud Detection

Empirical Evidence

A research project by Anto La Ode (2020), on ”The Auditor’s Ability to Detect Fraud through the Use of Independence, experience, Professional Scepticism and Workload”, states that to gather information, a survey to collect data used by distributing questionnaires to a wide range of accountants and auditors. He gathered that audit experience and professional scepticism positively influence the auditor’s ability to prevent and detect fraud.

In contrast to Anto La Ode, Kurniadi (2019), focused on fraud detection using the red flag theory. They developed a model to assess the likelihood of fraud using the red flag approach. The study involved 370 auditors from major accounting firms. They found out that an auditor’s evaluation of internal controls is crucial when estimating fraud risk.

Another study from Zimbabwe by Mabika (2015) researched “Fraud and fraud prevention strategies in Zimbabwe Local Authorities” and his main focus was on the causes of fraud, using the fraud triangle theory. He concluded that to reduce the level of fraud, management must get involved, create systems, teach about the systems and monitor local authorities. He also concluded that local authorities must employ the correct people with the required skills and knowledge in their jobs as well as pay salaries and allowances on time.

Summary

The chapter compiled a variety of academic works on the role of internal auditors in preventing and detecting fraud. The researcher explained the effectiveness of internal auditor’s attributes in preventing and detecting fraud supporting theories from different scholars. The next chapter looked at the research methodology.

METHODOLOGY

Introduction

A plan is a blueprint for action giving direction on how the outcome will be achieved and the same applies to methodology. Methodology is a system of methods and principles on how a certain task will be completed. It can also be procedures, applications and rules on how research is to be carried out. This chapter focuses on the research methodology that the researcher is going use for the study. The focus is mainly on research design, research approach, population, sampling strategies and data collection methods that will be used by the researcher when carrying out the project. This chapter will also look at measures to be used such as formulas and scales.

Research design

Research design has been defined as a structure of research that is a glue that holds all the elements of the research project together (Islamia, 2016). The research design is a plan for the research (Bloomfied, 2019). According to Abbott et al (2012), research design is a plan for gathering and analysing information that directly addresses research questions whilst being efficient and organized.

As research design outlines the research process from formulating the questions to the conclusion, it is important because it acts as a bridge between the question one is trying to answer and the data collected. The design clarifies how your questions relate to the information you gather and what methods are best suited to analyze it and find the answer (Dannels, 2018). According to Mayers et al (2013), three main types of research design are exploratory, descriptive and explanatory. These designs represent different approaches to gathering and analyzing data to answer research questions. This research chooses a descriptive approach.

The research will involve collecting data using interviews and questionnaires distributed to a sample of internal auditors in SMEs in Mutare Showground. The research will include questions that assess the auditors’ current experience, competency, professional scepticism and ethics in preventing and detecting fraud in business organizations. The research will utilize both closed-ended and open-ended questions to gather quantitative and qualitative data. The closed-ended questions will provide structured responses for quantitative analysis, while the open-ended questions will allow auditors to elaborate on their experiences and provide detailed insights (Freites et al, 2023).

The sample will be selected using stratified sampling where the population is divided into homogeneous subgroups or strata on certain variables and random samples are taken from each stratum mostly using a simple random sampling method (Singh et al, 2014). Here, the population will be divided into five groups which are food and beverage sellers, manufacturers, service providers, sports bodies and farmers. After this, random samples are taken from these five groups using simple random sampling and then the samples from each group are combined to form the overall sample. According to Tipton (2013), stratified sampling is more accurate as it ensures that each subgroup or stratum is represented in the sample and it also allows a more diverse representation of the population.

Research Approach

Three types of research approaches can be used in the research project process which are quantitative approach, qualitative approach and mixed approach (Leavy et al.2022). According to Pandey et al (2021), quantitative research involves gathering numerical data and analysing it using statistical techniques and its main objective is to measure variables, test hypotheses, and determine the cause-and-after connections whilst qualitative approach centres on gathering non-numerical data such as texts, images and audio recordings to comprehend the meaning of experiences, delving into phenomena, and gaining insights into people’s perspectives. For this approach, a mixed approach will be used which integrates quantitative and qualitative methods to offer a comprehensive understanding of research questions (Dawadi et al, 2021). In combining the strength of both approaches, researchers can address complex issues using a more diverse and extensive data set, leading to a deeper understanding of the topic.

Geographical Area

Geographical area refers to an area of boundary (Gallotta et al, 2022) and the research will be using Mutare Showground when conducting the research. Mutare Showground is a multi-purpose event venue in the eastern highlands of Zimbabwe, within the Manicaland province. Mutare is a vibrant economic hub with various types of businesses and it is mainly focused on mining, agriculture and manufacturing. However, this research focuses on Small and Medium Enterprises (SMEs) within Mutare Showground because SMEs are highly vulnerable to fraud due to less robust internal controls and lack of sufficient resources to prevent and detect fraud. The decision to study SMEs in this specific area is motivated by limited internal audit practices and data accessibility. However, to some extent using SMEs could have limitations such as data confidentiality as SMEs may be hesitant to share sensitive information about internal controls or potential fraud incidents due to confidentiality concerns and lack of established function as SMEs might not have a dedicated internal audit function, making data collection on existing practices difficult.

Target Population

According to Zhao et al (2013), a target population is a specific group of individuals or items that a researcher or marketer is interested in studying or researching. Tang et al (2018), defined a target as a subset of the larger population that shares characteristics relevant to the research or marketing goal. This project mostly focusing with in internal auditors in SMEs in Mutare Showground such as food and beverages sellers, manufacturers, service providers, sports bodies and farmers. The population is indicated in Table 1.0 below according to Mutare Showground Management Records in 2023.

Table 3. 1 Target Population

| Organization | Population |

| Food and beverage sellers | 26 |

| Manufacturers | 23 |

| Service providers | 26 |

| Sports bodies | 11 |

| Farmers | 23 |

| Total | 103 |

Sampling

According to Mujere (2016), sampling is a research technique where a small group is selected from the larger population for analysis. Instead of using the entire population researchers use sampling to gather data more efficiently and make conclusions about the large population based on the sample’s characteristics. Lohr (2021), stated that two types of sampling are probability sampling and non-probability sampling. Here, the researcher is using probability sampling which is a method of sampling where each element has an equal chance of being selected (Alvi, 2016). Probability sampling better represents the population and reduces bias in population representation. According to Mujere (2016), different types of probability sampling are simple random sampling, stratified sampling and systematic sampling. In this project, the researcher will use stratified sampling.

According to Singh et al (2014), stratified sampling is where the population is divided into homogeneous subgroups or strata on certain variables and random samples are taken from each stratum mostly using a simple random sampling method. Here, the sample will be selected using stratified sampling where the population is divided into homogeneous subgroups or strata on certain variables and random samples are taken from each stratum mostly using a simple random sampling method (Singh et al 2014). Here, the population will be divided into five groups which are food and beverage sellers, manufacturers, service providers, sports bodies and farmers. After this, random samples are taken from these five groups using simple random sampling and then the samples from each group are combined to form the overall sample. According to Tipton (2013), stratified sampling is more accurate as it ensures that each subgroup or stratum is represented in the sample and it also allows a more diverse representation of the population.

Sample size

Yamane’s (1967) model will be used to calculate sample size. According to Louangrath et al (2017), the Yamane model is a statistical tool used in research to determine the sample size for a study. It helps the researcher to figure out how many people are needed to get accurate results that can be applied to the entire group. The resultant sample size will represent the target population. The study used this sample size method due to its simplicity.

Formulae

n=N/1+(e)2 Where N is the population size, e is the level of precision, n is the sampling size

Given N= 103, n= 0.05 (95% confidence level)

n=103/1+103(0.05)2

n=65

Hence sample size is 65

Table 3. 2 Sample selection

| Respondents | Population | Sample size selected |

| Food and beverage sellers | 26 | 16 |

| Manufacturers | 23 | 15 |

| Service providers | 20 | 12 |

| Sports bodies | 11 | 7 |

| Farmers | 23 | 15 |

| Total | 103 | 65 |

The table above 3.2 shows that the sample size shows the sample size according to the Yamane model.

Data Collection Methods

Various types of data collection methods can be used when conducting research. Paradis et al (2016), defined data collection methods as techniques and processes used to gather data for research, analysis or decision-making process which include surveys, interviews, questionnaires, observation, experiments and focus groups. In this research, the researcher will be using questionnaires and interviews as data collection methods.

Interviews

An interview has been defined as a formal conversation between two or more people, typically with one person the interviewer. The interviewer will be asking questions to obtain information from participants who provide answers (Sunkersing et al, 2024). It allows for a more in-depth exploration of the topic and can provide qualitative insights into the experiences and perspectives of auditors. This means that structured interviews will be conducted with auditors in SMEs in Mutare Showground and these interviews will be done face-to-face.

Questionnaires

According to Kronsick (2018), questionnaires are a valuable tool for gathering information from people. They are essential questions used to collect data in a wide range of contexts such as market research, social sciences, education and healthcare. There are two main types of questionnaires namely structured questionnaires and unstructured questionnaires with open-ended questions to allow for more detailed responses (Pattern 2016). Therefore, the researcher is using structured questionnaires as they are inexpensive and quick to administer, efficiently collecting standardized data, and allowing for anonymity which can encourage more honest responses.

Data Collection Procedure

The first step of data collection for the researcher will be to seek approvals from the organizations concerned. 65 questionnaires will be distributed physically to the organizations. Completed questionnaires will be collected later on.

Reliability and Validity

Carroll and Goodfriend (2022) describe reliability as a concept describing how replicable a study is. If a study can be repeated and the same results are found, the study is considered reliable. Studies can be reliable across time and reliable across samples. Validity of research is an evaluation of how accurate the study is (Price et al, 2015). It describes the extent to which the study measures what it intends to measure. Both internal and external validity will be used by the researcher. Internal validity will be restricted to what is supposed to be measured and external validity of research findings refers to the data’s ability to be generalized across persons, settings and times (He et al2021). The method to be used by the researcher to improve reliability and validity is through pilot testing.

In order to guarantee the accuracy and dependability of the data, a pilot study was conducted beforehand, as suggested by Lowe (2019). 12 questionnaires were distributed randomly to internal auditors in Mutare Showground to test the instrument, aligning with Eldridge et al (2016), recommendation to avoid using the target population for pilot studies. This pilot phase helped refine ambiguous questions and verify the effectiveness of the data collection methods.

It proactively identified potential challenges, allowing for the implementation of mitigating strategies before the main study commenced. The pilot study also provided valuable insights into the required time and resources, aiding in effective planning, as noted by Bitzenbauer (2023).

To further assess the reliability of the research methods, Cronbach’s alpha was calculated using SPSS software. The instrument achieved a reliability score of 0.845 (85%), falling within the acceptable range of 0.80 to 0.90 as suggested by Vaske et al (2017).

Measurements

According to Dabiri et al (2019), measurements refer to formulae and scales which can quantify variables of interest. These measurements provide a standard and a numerical representation of the data collected. In this research, the researcher is using the Likert scale.

Likert Scale

According to Yin (2013), the Likert scale is a tool used by researchers to gauge participants’ attitudes, reactions, opinions, and perceptions regarding a certain subject. He proposed that to maximize the effectiveness and efficiency of the study, more information is needed in the response when utilizing the Likert scale to get a person to the goal level of agreement with the proclaimed assertion. For respondents to grasp the questions, Huettner (2015) underlined the significance of accuracy while framing the questions. It was used by respondents to indicate agreement or disagreement with statements. The participants will be asked to rate their level of agreement on the scale, typically ranging from strongly agree to strongly disagree.

Table 3.3: Likert scale

| Strongly Agree | Agree | Neutral | Disagree | Strongly Disagree |

| 5 | 4 | 3 | 2 | 1 |

The table above shows a table of Likert scale

Data presentation and analysis

For simple interpretation, the researcher will gather both qualitative and quantitative data, which will be evaluated using bar graphs, pie charts, and tables. The researcher chose graphs, tables and pie charts because they are simple to understand and display the trends leading to a more accurate conclusion. Tables will be employed to summarize the data since they make it simple to compare variables. These graphs, charts and tables will be generated using SPSS v21 and Excel.

Ethical Consideration

Confidentiality: According to Corley (2022), confidentiality it’s the principle of protecting sensitive information from unauthorized access, disclosure and use, keeping it a secret. This means that all information obtained during the research is treated with confidentiality and is not disclosed to unauthorized individuals, protecting the integrity and privacy of the data.

Informed Consent: Information should be obtained with consent from participants, the purpose of the study should be outlined on the voluntary nature of participation, and how their data will be used, ensuring that they understand and agree to participate.

Avoiding Bias: According to Smith et al (2014), bias is a tendency of favouritism often unfairly. Brighton et al (2015), defined it as preconceived opinions or judgments that can influence how things should be done. Therefore, any biases that could impact the results which result in a lack of credibility and reliability should be avoided.

Respect for Participants: When carrying out research, respect should be considered. According to Engelman et al (2019), respect it’s a fundamental human value that involves recognizing, appreciating and valuing others treating them with dignity, kindness and consideration. This means that when carrying out the research will be considering the rights and dignity of participants throughout the research process, considering their well-being and ensuring that they are not harmed or exploited.

Transparency: Kosack (2014), defined transparency as the quality of being open, clear and honest in revealing information hiding nothing or being secretive. This involves disclosing any conflicts of interest, sources of funding, or affiliations that could impact the research outcomes, maintaining transparency and honesty in the study.

Compliance with Regulations: This involves all relevant laws, regulations, and ethical guidelines governing, ensuring that research is conducted ethically and by established standards from all the SMEs to be involved when carrying out the research.

Environmental considerations

According to Rupert et al (2016), ethical considerations are the factors related to the natural world that must be considered when making decisions or undertaking actions. This means that there shall be compliance with environmental rules and regulations by the Environmental Management Agency (EMA). This research will be conducted in a manner that is environmentally friendly ensuring zero pollution of any form. Research materials will be disposed of at designated areas.

Gender Considerations

Anyone interested and qualified shall participate in the research process regardless of being a woman or a man.

Chapter Summary

The main elements of the study’s research technique are outlined in this chapter. Data sources and research methodologies have been identified, and the research methodology for the study has been explained. Discussions were held regarding the target population, data collection techniques, data presentation, and analysis. The following chapter will provide and examine the main research findings.

DATA PRESENTATION AND ANALYSIS

Introduction

With the SMEs in Mutare Showground as a case study, this chapter presents data and analyses research findings to conclude the effect of internal auditor’s attributes in preventing and detecting fraud in business organisations. Several data analysis techniques are used in analysing the findings such as tables, graphs and pie charts. Transcripts and analysed information from interviews are also used in conducting this study, the searcher used IBM SPSS version 21 and Amos V18 to produce output tables. These output tables were descriptive statistics tables, demographics analysis tables, hypothesis test summary figures, bar graphs and pie chart this chapter interpreted. Research findings are in-depth analyzed, and connected to research goals and research questions.

Response rate analysis

Table 4.1 below shows the overall response rate for the study.

| Sample | Questionnaires distributed | Questionnaires returned | Response rate |

| 65 | 65 | 54 | 54/65 x 100 = 83. 08% |

Source: Researcher’s Compilation, (2024)

As shown in the table above, the researcher issued the questionnaire to a target population, using a calculated sample size of 65 participants. Out of the 65 questionnaires distributed, 54 participants responded and returned the questionnaire. This gave the study an overall response rate of 83.08 % in total which is above the threshold of 75%. This means about 16.92 % of the target market did not respond, probably because they were too reluctant to share their opinions with the researcher or the questionnaires were sent out during their busy and tight schedule as finance is considered the second busiest profession (Hearns2021).

Demographics analysis

The questionnaires included a section that asked participants about their background such as their gender, age, work experience and level of education. This information is crucial for this study as it helps to find the relationship between these factors and emotional intelligence and understand the characteristics of the sample representing the target population.

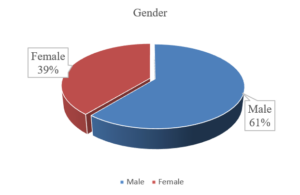

Gender

The pie chart below shows the male and female representation in this research.

Source: Primary Data, (2024)

Figure 4.1 Gender of Respondents.

After collecting and analysing data, the results indicate that the response rate for men is higher than that of women, with men having a response rate of 61.1% compared to 38.9 for women. These findings align with demographic analysis by Benjamin (2021) which concluded that men are more prevalent in the management of SMEs. This observation was further supported by Zimstats (2022), who reported that women’s overall labour rate participation in Zimbabwe is 16.6% lower than that of men. This disparity may stem from the limited educational opportunities available to women compared to men, according to Zimstats (2022).

In order to prevent bias in the study’s findings, gender equality must be considered when doing research, according to Wiknman (2015).

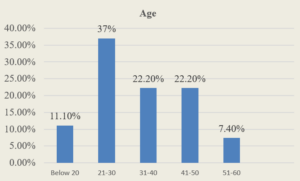

Age range of respondents

The bar graph below shows the age range of respondents in this research.

Source: Primary Data, (2024)

Figure 4.2 Age Range of Respondents.

The bar graph above indicates that individuals aged 21-30 years comprise the largest segment of SMEs in Mutare Showground at 37%, followed by those aged 31-40 and 41-50 years at 22.2%, then below 20 years with 11.1 % and lastly its 51-60 with 7.4%. Analysing the information above, clearly shows that SMEs are highly dominated by people aged 21-30 this may be due to the high unemployment rate in Zimbabwe where the soon graduated from colleges and universities cannot get jobs and they open their small businesses and work as an accountant (internal auditors). According to Oywe (2023), UNICEF Zimbabwe (2021), and Pswaya (2023), over 60% of the country’s population is under the age of 30 and youth continue to face obstacles to realise their economic potential. On the other hand, many formal companies require an internal auditor with 3 to 5 years of work experience and as a result, most people aged 21-30 will work in SMEs until they get the experience required in big companies and some even reach 30 years or enter 31-50 years in the informal sector because employers of big companies require someone with experience from a reputation organisation (Halkiv, 2023). These findings also explain the declaration by Zimstats, (2023), that people that are 15-19 years old participated less in the labour force whilst those aged 35-39 years were the most dominant participants. However, when put together, it can clearly show that SMEs in Mutare Showground are dominated by the youth.

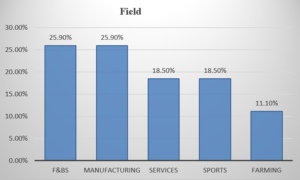

Field

The bar graph below in Fig 4.3 shows the fields or segments which the researcher carried on the research

A bar graph of the fields of research

Source: Primary Data, (2024)

Fig 4.3 Fields or segments

The bar graph above shows the segments in which the research was carried in. The bar graph shows that F&BS and manufacturing companies participated the most in this research with 25.9% followed by services and sports with 18.5% then lastly farming with 11.1%. Mostly the participation is according to the frequency. F&BS and manufacturing are more in Mutare Showground as compared to others so is their participation according to Mutare City Council (2023).

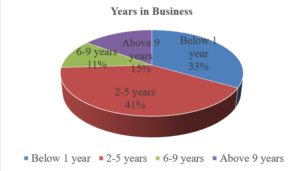

Years in Business

The pie chart below shows the number of years individuals have been in the work industry.

A pie chart 4.4 of years in business

Source: Primary Data, (2024)

Fig 4.4 Years in Business

The data presented above in the pie chart reveals that individuals with 2-5 years in business constitute the largest group at 40.7%. This is followed by less than 1 year with 33.3% whilst those between 6-9 years are 11.1% and those above 9 years are 14.8%. This is mostly in line with the age of those who are 21-30 who soon graduated. On the other hand, also employers in big companies require work experience, (Halkiv,2023) which is why those 2-5 are dominated in SMEs.

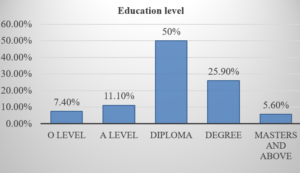

Education level

The bar graph below shows the level of education of people working in SMEs in the Mutare showground. Table 4.5 of the level of education

Source: Primary Data, (2024)

Fig 4.5 level of education

The research results indicated that individuals with diplomas comprised the largest segment of SMEs in Mutare Showground with 50% followed by those with degrees who has 25.9%. Those with masters and above comprise 5.6 then lastly those with O’ level and A’ level with 7.4% and 11.1% respectively. The findings suggest that those with diplomas and degrees dominated the market which is linked to the fact that the soon graduates are not getting jobs easily. It shows also that there are few highly educated people as they are just 5.6% who could be the owners of the businesses. On the other hand, there are also a few with O level and A level which has been supported by Zimstats (2022), there are few employees in the field below the age of 20 years.

Results relating to the objectives of the study

Auditors ability to prevent and detect fraud

This section measures the dependent variable of the study. Table 4.6 below shows descriptive statistics for auditors’ ability to prevent and detect fraud.

The scale used was: 1 – Strongly Disagree, 2 – Disagree, 3 – Neutral, 4 – Agree and 5 – Strongly Agree.

Table 4.2 Descriptive statistics: Auditor’s ability to prevent and detect fraud.

| N | Minimum | Maximum | Mean | Std. Deviation | |

| AA1: The rate of fraud has decreased significantly for the past 2 years | 54 | 1.00 | 5.00 | 3.0741 | 1.21083 |

| AA2: We have detected financial malpractices for the past 2 years | 54 | 1.00 | 5.00 | 2.5556 | 1.31273 |

| AA3: Our internal auditors’ efforts to combat fraud are bearing fruits | 54 | 2.00 | 5.00 | 4.0370 | .91038 |

| AA4: Our employees have been at the forefront of detecting fraud | 54 | 1.00 | 5.00 | 2.4259 | 1.12605 |

| Valid N (listwise) | 54 |

Source: Primary Data, (2024)

In order to find out the level of internal auditors’ ability to prevent and detect fraud in SMEs in Mutare Showground, descriptive statistics table was utilized. The table above shows the descriptive statistics on auditors’ ability to prevent and detect fraud as compiled by IBM SPSS Statistical version 21. As shown in the table, the mean for the rate of fraud decreasing for the past 2 years is 3.07 so moderately auditors have reduced fraud for the past 2 years. A mean of 2.56 shows that the auditors have detected financial moderately well but there is room for improvement. A mean of 4.04 shows that internal auditors are putting great effort into combating fraud areas bearing fruits. There is also a mean of 2.43 shows that employees are less involved in detecting fraud which also means that there is a need for improvement.