Macroeconomic Instability in Nigeria; Examining the Roles of External Debts

- Adedokun Adebayo

- Okorie Ukafor Ukafor

- 1098-1116

- Jun 23, 2024

- Economic Development

Macroeconomic Instability in Nigeria; Examining the Roles of External Debts

Adedokun Adebayo & Okorie Ukafor Ukafor

Department of Economics

Obafemi Awolowo University, Nigeria

DOI: https://doi.org/10.51244/IJRSI.2024.1105074

Received: 24 May 2024; Accepted: 07 June 2024; Published: 23 June 2024

ABSTRACT

This study investigates the effects of external debts on the index of macroeconomic instability, which incorporate multiple macroeconomic indicators in a single index, so as to present a more robust findings as against the studies in the literature which investigates the effects of debts on each of the macroeconomic variables on individual bases. After generating the single index of instability, the study employed the Autoregressive Distributed Lag (ARDL) for the analysing under four different models which interchange four different measures of external debts. The results show that external debt stock to GDP ratio exerts negative effects on macroeconomic instability in the short and long run. Debt-to-export ratio is not significant on macroeconomic instability both in the short and long run. It is also established that debt-to-revenue has negative and significant impact on macroeconomic instability in the short run, but not in the long-run. In contrast, the results show that debt service-to-revenue exerts a positive and significant effects on macroeconomic instability both in the short and long-run. This implies that increase in the proportion of revenues that are expended on debt servicing worsen macroeconomic instability in Nigeria both in the short and long run.

Keywords: External debt, macroeconomic instability, Nigeria Economy

INTRODUCTION

Macroeconomic stability is a major goal of every country irrespective of time and place. To achieve it, there is no limit to how far the government could go to ensure a formidable environment that supports its achievement. Indeed, resources are pulled from different sources for investment into whatever activities that could spurt macroeconomic performances. In most cases, the challenges of macroeconomic instability are more pronounced among the developing countries, because they are often faced with inadequate economic and financial resources to develop at required pace, more so, with limitation of mobilizing sufficient savings to finance investment (Spilbergs et al, 2023, Senadza, Fiagbe & Quartey, 2017). In these cases, many give in to exogeneous source of big push. Among the limited options for the existing financial gaps, borrowing is a readily available way of stimulating or stabilizing macroeconomic activities in the developing countries, Sahu & Mahalik (2024) .

In some other clime, some of these economies suffer Dutch disease, in which case, despite the existence of huge natural resources, there is huge gaps in financial needs to spur development, (Bresser-Pereira, 2024). Nigeria is one of the countries in the latter category. Considering the Nigerian economic structure, being an oil-dependent economy, in which case, the country’s survival is heavily reliant on money from oil rent. Oil and gas revenue accounts for around 50% of government revenue and more than 90% of earnings from exports (Budget Office of the Federation, 2020). In many situations, any shock to global oil prices will impact revenue of the government and thus exhibits multiplier effects on every other sector of the economy.

Over the years, falling oil prices have continually increased borrowing to fund government projects and programmes. Prior to the global oil price crash, in 2014, Nigeria’s external debt growth rate persisted at single digit between 2006 and 2010. Recalling that in 2005, Nigeria debt was rescheduled and paid off. However, years after, debt began to increase at increasing rate, moving from single digit in 2010 and increased to an average of 10 per cent between 2011 and 2013. However, subsequent drastic drop in oil price in 2014 brought about profound decline in government revenue in the face of ever-growing budgetary needs. Remarkably, the government did not reduce expenditures during the negative oil shocks and rather contracted more debt to fill the budget shortfalls. Consequently, external debt consistently rose from 8.82 USD billion in 2013 to a whopping $22.07 billion as at 2018 and further increased tremendously to $27.68 billion in 2019. Nigeria’s external debt stock increased by 43.2% in one year and 213% in seven years, rising from $10.72 billion in 2015 to $15.35 billion in 2016 alone (CBN, 2020).

In essence, the country’s debt is gradually budging to where it was in 2005-2006 before the debt relief. More especially, the rapid surge in recent years have raised serious concerns about its implications on macroeconomic stability. In addition to the drop in global crude oil prices, the upsurge in foreign debt may as well be due to weak economic structure, which stimulate macroeconomic instability. For instance, Nigeria economic growth contracted from 6.2 percent in 2014 to 1.6 percent in 2016. The economy slipped into recession in second quarter of 2016 and upheld a negative growth rate in all the subsequent quarters of the year (CBN, 2020). Also, the economy suffered another recession within 5 years. Specifically, in third quarter of 2020, occasioned by the impact of COVID-19 and oil price shocks induced by the pandemic (CBN, 2020). Following those periods, the economy experienced unprecedented instability in the form of foreign exchange uncertainty, apathy of private sector investors, high inflation, low aggregate demand and high fiscal deficit. In the state of confusions within the economic landscape, and in attempt at instigating a swift rebound and stabilise the economy, in the face of dwindling government revenue, government borrowing becomes inevitable. In this vicious circle of borrowing which keeps aggravating the debt profile of the country, without foreseeable economic rebound and stability. In this situation therefore, it is necessary to examine the role that the accumulated debt is playing in the economic stability or otherwise of Nigeria, the basis for this study.

LITERATURE REVIEW

Theoretically, foreign debt is not a problem, if the debt generates higher return to the economy, more than the cost of contracting it. In this case, the debt would improve capacity as well as minimise macroeconomic volatility, making it productive and justifiable (Dey &Tareque, 2018). Besides, public debt is expected to rise during a recession due to its capacity to serve as automatic stabilisers and a key source of financing government deficit, in order to stimulate demand and stabilise the economy (Rafique, Nisar & Shah, 2024). Given this perspective, momentarily rising public borrowing assists in lessening the impact of shocks on macroeconomic variables. Nevertheless, there seem to be limits to the capability of debt to stabilise the economy, when public borrowing is high and has no inbuilt mechanism to play the stabilisation roles (Otovwe, 2023; Egert, 2013). Scholars have shown that government financial obligations and output fluctuation have correlation (Khan, Raza & Vo, 2024). Specifically, the stabilising role of government borrowing may turn out to be weaker when the level of debt in an economy is not commensurate to its returns. This echoes negative perception to economic agents such as investors that debt dynamics may threaten their investment returns and thus makes the economic system to be unpredictable. In this case, the expectations of the private investors would be that public borrowing will ultimately give rise to increase in taxes and lessen the fiscal policy effectiveness in smoothening fluctuation in the economy (Ultremare, 2023). Also, when the debt level is high, fiscal policy may even turn out to be pro-cyclical (Gootjes & de Haan, 2022).

These possibilities of positive and negative effects of debt are in line with different schools of thought in economics. Keynesian postulates that a rise in debt stimulates an economy and is essential to redirect the path of an economy during recession. An aspect of the prevailing studies corroborates this stand on the subject, which states that foreign borrowing portends a desirable influence on an economy (Joshua et al., 2020). On the other hand, neoclassical theory envisions an adverse effect of debt on macroeconomic performance as debt engenders crowding out private capital, resulting in a loss of long-run output. This position is supported by some extant studies which suggests that external debt undesirably shapes economic performance (Ring et al., 2021; Edo, Nneka, & Isuwa, 2020; Dey and Tareque 2020). Despite the fact that there is numerous research on external debt in the literature, greater numbers of the studies focussed on the influence of external debt on economic growth.

In the face of diverse perspectives in the literature, it is imperative to examine the government’s debt position in Nigeria alongside the effects it has exercised in the current instability the country faces, particularly in line with some key macroeconomic variables. Even though the country’s debt-to- Gross Domestic Product ratio in 2020 which was 35 percent still is below the 40 percent benchmark for developing countries as suggested by (IMF, 2010), The expenditure on debt servicing accounts for two-thirds of retained government revenue, thereby tightening the fiscal flexibility of the government to invest in crucial infrastructure to back private investment and macroeconomic stability (Abdulkarim & Saidatulakmal, 2021). The rising cost of government debt extends to a new landmark in 2020 with the country’s debt payment as a percentage of income increasing to 83%. This implies approximately 83 percent of government revenue was used for settling debt servicing obligations in 2020, raising question about the macroeconomic stability of the country.

(Abdulkarim and Saidatulakmal, 2021), analyzed impact of public borrowing on the economic growth of Nigeria over 1980 to 2018. The study shows that foreign borrowing is harmful to the economy in the long run, whereas the effect was desirable at the short run. In other words, the study assert that debt has desirable impact on the economy in long run but the impact was damaging in the short- term. (Kolawole, 2024) also established that foreign debt has no positive effect on the economic growth. However, while the focus of several studies in Nigeria have been on the relationship between debt and economic growth, the issue of economic stability is beyond a single macroeconomic variable. Consequently, this study extends the investigation to capture various macroeconomic variables by generating index to capture the aggregated instabilities inherent in the variables of interest. The outcome of the analysis could assist in a better way to reaching conclusion on how external debt exerts stability or instability on the Nigerian economy.

METHODOLOGY

Model Specification

This study adapts the models specified in (Dey & Tareque, 2020) as shown in eq. 1

Y_t=δ+ρEXD_t+τK_t+κX_t+e_t (1)

Where macroeconomic stability (y) is regressed with external debt (measured as external debt stock to GDP ratio), physical capital (K) and X_t (which is a set of control variables which includes trade openness and credit to private sector). t is the time index and e represent the error term.

To model the effect of external debt on macroeconomic stability in Nigeria, this study used Autoregressive Distributed Lag (ARDL) model as proposed by Pesaran et al., (2001). This approach is most appropriate for few reasons. First, it gives both the short- and long run unbiased estimate in a dynamic form. For instance, the effect could be noticed in the short and long run; higher external debt could spur macroeconomic stability in the short run, whereas it might crowd out private investment in the long run, resulting in instability of the macroeconomic indicators. Secondly, it is robust to the order of integration i.e. both I(0) and I(1)variables. As a result of this, there is no need for pre-unit-root testing as long as none of the variables is above I (1). More so, ARDL provides the chance to substantiate the presence of long-run equilibrium among the variables via bounds testing cointegration, which utilises F-statistic. In this case, to ascertain the existence of long-run association, F-test values is measured up against two critical values of upper and lower bound (Pesaran et al., 2001). Accordingly, long run cointegration is present if F-statistic outdo the upper critical bound value for which the null hypothesis of no cointegration is abandoned. If F-statistic is not as much as the lower bound value, the null hypothesis of no cointegration would be upheld.

Taking all the relevant variables into consideration and expanding equation 1, the ARDL model is specified as;

![]()

Here, Y represents macroeconomic instability, K signifies physical capital, TOP designates trade openness and CPS is the credit to private sector. Further, stand for the first difference operator, δ represent the drift element, ςj (j = 1, 2…,5) represents the long-run component of the model, ω,ρ,β,κ and φ stand for the short run subsect of the model. a, b, c, d and e, express the maximum lags which will be selected automatically using the Akaike Information Criterion, and et is the white noise.

Measuring Instability of Macroeconomic Indicators

A number of procedures have been adopted to measure macroeconomic instability. Ismihan, Metin-Ozcan and Tansel, (2005) calculated a macroeconomic instability index using four macroeconomic indicators which include exchange rate, inflation rate, external debt to GDP ratio and fiscal deficit to GDP. Also, Haghighi, Sameti and Isfahani (2012) built on Ismihan, Metin-Ozcan and Tansel, (2005) to compute a macroeconomic instability index using macroeconomic variables which include inflation rate, exchange rate, budget deficit and terms of trade.

This study however, considering the specificity of the Nigeria economy, follows Haghighi, Sameti and Isfahani (2012), by using inflation rate, exchange rate, fiscal deficit and terms of trade as indicators of macroeconomic instability for the Nigerian economy. The factors will be individually computed, by means of the formula stated thus;

![]()

Here, Y represents macroeconomic instability index with values that ranges between 0 and 1. The value 0 means total stability while there is total macroeconomic instability when the value is 1. Furthermore, weights are allotted to each of the indicators. The weights assigned to the variables will be constructed using standard deviation of individual indicators. The macroeconomic instability index will then be computed by summing the weighted sub-indices.

![]()

Where inf stands for inflation rate, fd represents fiscal deficit, er signifies exchange rate while tot denotes the term of trade. The link among the coefficients and Y is established, such that their summation will be equal to 1, explicitly δ + θ + α + ϕ = 1. Vector normalisation and the coefficients’ significance will be established by means of maximum likelihood ratio.

Definition and Operational Measurement of Variables

- Inflation rate: This is the consumer price index. The data is extracted from Central Bank of Nigeria (CBN) Statistical Bulletin.

- Exchange Rate: Rate of Naira to US dollar. The data is extracted from Central Bank of Nigeria (CBN) Statistical Bulletin.

- Fiscal deficit: Fiscal deficit/Surplus is the difference between revenue and expenditure scaled by GDP. The data is extracted from Central Bank of Nigeria (CBN) Statistical Bulletin

- Term of Trade: this is the ratio of a country’s export prices to her import prices. It shows the quantity of import goods that the country can purchase per unit of export goods. The data is extracted from CBN Statistical bulletin

- Trade Openness (TOP): This is gross exports and imports value as a proportion of GDP. It is therefore projected that it should reduce instability. However, in a country like Nigeria which depend hugely on imported items, an increase in trade openness may propagate macroeconomic instability. The data is extracted from CBN Statistical bulletin

- Physical Capital as percentage of GDP (K): this is measured by the gross domestic investment. It is expected to decrease instability in the macroeconomic indicators. The data is extracted from CBN Statistical bulletin

- Credit to Private Sector as percentage of GDP (CPS): it denotes the financial capitals offered by financial institutions to the private sector in a country and it is thus projected to reduce macroeconomic instability. The data is extracted from CBN Statistical bulletin

- Total External Debt Stock as percentage of GDP: This is the portion of the total public debt from foreign sources scaled by GDP.

- Debt to revenue ratio: This is the percentage of the total revenues to debt and determines the borrowing risk.

- Debt service to export ratio: This is the ratio of debt service payments (principal + interest) to export earnings.

- Debt service to revenue ratio: This is the percentage of debt-service to revenues which measures a country’s ability to meet its minimum principal and interest payments from its revenue.

Theoretically, external debt stock is expected to reduce macroeconomic instability if the loans are channelled to productive use. The data on debt are extracted from Debt Management Office (DMO) and CBN Statistical Bulletin.

DATA ANALYSIS & FINDINGS

Descriptive Statistic

The nature of the variables is first investigated using descriptive statistics before looking at the econometric relationship between foreign debt and macroeconomic instability. In Table 1, the results of the descriptive statistics are presented. It shows that all the series exhibit consistency because their mean and median values are within the range of these series’ maximum and minimum values. The Macroeconomic Instability Index (Y) has a mean value of 0.37, which is lower than the median value of 0.40. This suggests a left-skewed distribution for the Macroeconomic Instability Index (Y) data. The largest value (0.99) was recorded in the year 1993, while the lowest value (0.57) was recorded in 1996. Nigeria external debt average value stands at 20.1 percentage point, the highest level (60.4) was recorded in 1992 and the lowest level (1.2) in the year 2010. This shows that as external debt to GDP ratio increases, GDP figure has also been on the increase in the recent years. As observed in the Table 1, the credit to the private sector (CPS) in Nigeria averaged 9.28 points from 1981 to 2019, attaining an all-time high of 19.63 points in 2009 and recorded lowest of 4.96 points in 1990. This shows that there has been inconsistency in the amount of credit that was provided to the private sector during the study.

As observed in the Table 1, the mean of capital stock (K) is 36.143. The standard deviation which measures the dispersion of the data shows that external debt to GDP ratio (ED_GDP) is highly dispersed variable, this implies that there has been inconsistency in the Nigeria debt profile in Nigeria over the years. With respect to skewness, credit to the private sector (CPS), external debt to GDP ratio (ED_GDP) and capital stock (K) are positively skewed while Macroeconomic Instability Index (Y) and trade openness (TP) are skewed to the left. It is however observed that the mean and median of all the variables are very close, which denotes a nearly symmetric distribution and the existence of low variability. This also suggests that the series displays a high level of consistency.

Table 4.1: Descriptive Statistics

| Y | Debt (%GDP) | TP | K | CPS | Debt-to-revenue | Debt service-to-revenue | Debt service-to-export | |

| Mean | 0.377 | 20.059 | 32.128 | 36.143 | 9.283 | 147.67 | 22.14 | 10.36 |

| Median | 0.401 | 10.433 | 33.872 | 32.518 | 8.202 | 114.95 | 10.77 | 8.37 |

| Maximum | 0.566 | 60.369 | 53.278 | 89.381 | 19.626 | 485.40 | 96 | 30.99 |

| Minimum | 0.048 | 1.244 | 9.136 | 14.904 | 4.958 | 6.65 | 2.95 | 0.25 |

| Std. Dev. | 0.107 | 20.094 | 12.293 | 18.871 | 3.540 | 135.92 | 24.45 | 9.27 |

| Skewness | -0.801 | 0.745 | -0.331 | 1.095 | 1.131 | 0.87 | 1.63 | 0.61 |

| Kurtosis | 4.059 | 2.082 | 2.255 | 3.930 | 3.879 | 2.69 | 4.89 | 2.28 |

| Observations | 39 | 39 | 39 | 39 | 39 | 39 | 39 | 39 |

Source: Author’s computation, 2023. Note: TP, K, CPS denote trade openness, physical capital, and credit to private sector

Unit Root Test

The times series properties of the variables are investigated. This is done in order to ensure that correct methodology and estimation technique are utilised, thereby, circumventing erroneous inference. Consequently, two (2) unit root testing procedures; Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) are adopted to generate robust and dependable results. For ADF and PP, the study set aside the null hypothesis of nonstationary on condition that the test statistics were superior when compare to the critical value. Tables 2A and 2B present the results of the unit root tests.

As shown in the tables, all variables, aside the Macroeconomic Instability Index (Y) and credit to the private sector (CPS), are integrated after the first difference, or I(1). Results of the unit root test using only constants show that the external debt to GDP ratio (ED_GDP), trade openness (TP), capital stock (K), debt to revenue ratio, debt service to revenue ratio, and debt service to export ratio are stationary after the first difference, indicating that they are I(1) variables, while the Macroeconomic Instability Index (Y) is stationary at level. The results of ADF and PP are identical.

In summary, the findings indicate that, at the 5% level of significance, the variables’ order of integration does not exceed one. This justifies the usage of ARDL bound testing method. It is recalled that when the variables are jumbled in terms of the order of integration, the ARDL testing method is appropriate.

TABLE 2A. Unit root test for stationarity (Augmented Dickey–Fuller)

| variable | intercept | intercept & trend | intercept | intercept/ trend | stationarity |

| ED_GDP | -1.460 | -4.428 | -3.956*** | -5.608*** | I(1) |

| Y

TP K CPS |

-3.350***

-1.944 -2.215 -0.993 |

-3.44**

-7.373*** -4.973*** -5.805*** |

-7.041***

-1.874 -0.579 -4.156*** |

-6.966***

-3.852** -5.486*** – |

I(0)

I(1} I(1) I(0) |

| DEBT-TO-REV | -1.66 | -2.856 | -5.350*** | -5.308*** | I(1) |

| DEBT SER-TO-EXP | -1.403 | -4.24*** | -8.050*** | -8.124*** | I(1) |

| DEBT SER-TO-REV | -2.182 | -1.950 | -3.350*** | -2.636 | I(1) |

Source: Author’s computation. *, ** ,*** denote 10, 5 and 1 percent levels of significance, respectively . The automatic maximum lag utilised is based on Schwarz information criterion,

TABLE 2B: Unit root test for stationarity (Phillips-Perron)

| variable | intercept | intercept & trend | intercept | intercept/ trend | stationarity | |

| ED_GDP | -1.840 | -4.442 | -5.296*** | -6.082*** | I(1) | |

| Y

TP K CPS |

-3.15***

-1.856 -2.163 -1.491 |

-3.354***

-7.360*** -4.961*** -10.199*** |

-7.27***-1.874

-0.694 -2.548 |

-7.19***-8.015***

-5.476*** -9.895*** |

I(0)

I(1) I(1) I(1) |

|

| DEBT-TO-REV | -1.83 | -2.80 | -5.33*** | -5.29*** | I(1) | |

| DEBT SER-TO-EXP | -1.90 | -4.35* | -8.24*** | -8.37*** | I(1) | |

| DEBT SER-TO-REV | -2.241 | -2.708 | -3.70** | -3.75*** | I(1) |

(a) Source: Author’s computation. *, ** ,*** denote 10, 5 and 1 percent levels of significance, respectively. automatic lag length selection is based on Newey-West Bandwidth.

ARDL Bound Test of External Debt Measure on Macroeconomic Instability in Nigeria

This study makes use of the ARDL bounds test to examine how external debt affects macroeconomic instability in Nigeria. In Tables 3A, 3B, 4.63C and 3D, the outcomes of the cointegration tests are presented. The models are estimated using various measures of external debt which include; external debt stock, debt service to export ratio, debt service to revenue ratio, and debt stock to revenue ratio, in separate models. The results show long-term association between the macroeconomic instability and various measures of external debt. That is, there are evidences of cointegration, which implies that the variables converge to a stable equilibrium over time.

Table 3A: ARDL bound testing of co-integration on External debt

(H0: No cointegration exists)

| F-Bounds Test Model 1 | ||

| Test Statistic | Value | |

| F-statistic | 8.093815 | |

| K | 5 | |

| Critical bounds | ||

| I(0) | I(1) | |

| 10% | 2.26 | 3.35 |

| 5% | 2.62 | 3.79 |

| 2.5% | 2.96 | 4.18 |

| 1% | 3.41 | 4.68 |

Source: Author’s Computation, 2024

Table 3B. ARDL Bounds Tests for the Debt service -Export ratio

Model 2 ARDL bounds test

| Test statistic | Value | k |

| F statistic | 7.38 | 4 |

| Significance | Lower bound | Upper bound |

| I(0) | I(1) | |

| 10% | 2.45 | 3.52 |

| 5% | 2.86 | 4.01 |

| 1% | 3.74 | 5.06 |

k represents the number of exogenous variables

Table 3C. ARDL Bounds Tests for the Debt Serv.-Revenue ratio

Model 3 ARDL bounds test

| Test statistic | Value | k |

| F statistic | 9.26 | 4 |

| Significance | Lower bound | Upper bound |

| I(0) | I(1) | |

| 10% | 2.45 | 3.52 |

| 5% | 2.86 | 4.01 |

| 1% | 3.25 | 4.49 |

k represents the number of exogenous variables

Table 3D. ARDL Bounds Tests for the Debt-Revenue ratio

Model 4 ARDL bounds test

| Test statistic | Value | k |

| F statistic | 4.74 | 4 |

| Significance | Lower bound | Upper bound |

| I(0) | I(1) | |

| 10% | 2.45 | 3.52 |

| 5% | 2.86 | 4.01 |

| 1% | 3.74 | 5.06 |

k represents the number of exogenous variables

The F-statistics in each model surpasses both the lower and the upper bounds critical values. This implies that the variables if drift apart in the short run would converge to steady equilibrium in the long-run.

Effects of Macroeconomic Variables on Instability in Nigeria

Sequel to the validation of long run relationship among the variables by means of ARDL Bound Test, the study proceeds to estimating the effects of each of the external debt measures on macroeconomic instability.

Model 1: External Debt to GDP

The results of ARDL are presented in Table 4. The outcomes show that external debt to GDP ratio (ED_GDP) exerts a negative and statistically significant effects on Macroeconomic Instability (Y) in the short run as well as in the long run. This implies that an increase in external debt stock reduces macroeconomic instability in the short run and long run. This supports the findings of (Saheed, Sani & Idakwoji, 2015) which conclude that external debt as capital inflow increases countries resources base and foreign exchange inflows with favourable outcomes for internal savings and investment which help to stimulate stability of macroeconomic indicators. This is also in tandem with studies of (Muhammad & Zaman, 2014) that found external debt as a boost in Nigeria economic productivity, hence lessens macroeconomic instability. (Mensah, Bokpin, & Boachie-Yiadom, 2018) argued that external debt invested correctly in profitable projects increase standard of living, reduce poverty and boost productivity. Furthermore, the finding support Keynesian theory that increase in government spending through borrowing stimulate demand and economic productivity. In which case, the resulting deficits would be repaid by an expanded economy that followed the borrowing. Therefore, external debt diminishes macroeconomic instability.

Considering other variables in the model, trade openness exerts a positive insignificant influence on macroeconomic instability (Y) in the short and long run. This suggests that trade openness has no effect on macroeconomic instability in Nigeria within the study period. the effect of capital stock (K), show negative and statistical insignificant effects macroeconomic instability (Y) in the short run and long run in our model. This shows that physical capital as ratio of GDP is not an important driver of macroeconomic instability in Nigeria in both the short and long run. Lastly, like other control variables, credit to private sector (CPS) as ratio of GDP is statistically insignificant. This suggests that credit to private sector has no effect on macroeconomic instability in Nigeria within the framework of model 1.

Table 4: ARDL long run and short run estimates

| Model 1: (Dependent Variable: Y) | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| short run | ||||

| C | 0.064781 | 0.561655 | 0.115340 | 0.9090 |

| ED_GDP | -0.019113*** | 0.004686 | -4.078831 | 0.0003 |

| CPS(-1) | -0.015372 | 0.031865 | -0.482391 | 0.6331 |

| K | -0.013160** | 0.006496 | -2.025980 | 0.0521 |

| TOP(-1) | 4.29E-05 | 0.006405 | 0.006704 | 0.9947 |

| D(K) | 0.032426 | 0.034564 | 0.938155 | 0.3559 |

| D(TOP) | 0.015771 | 0.007896 | 1.997243 | 0.0553 |

| DUMMY | -0.517555 | 0.259501 | -1.994422 | 0.0556 |

| CointEq(-1)* | -1.071158 | 0.141958 | -7.545582 | 0.0000 |

| long run | ||||

| ED_GDP | -0.017843*** | 0.003872 | -4.607875 | 0.0001 |

| CPS | -0.014350 | 0.029736 | -0.482584 | 0.6330 |

| K | -0.012286 | 0.006194 | -1.983634 | 0.0568 |

| TOP | 4.01E-05 | 0.005978 | 0.006705 | 0.9947 |

| DUMMY | -0.483173 | 0.245224 | -1.970335 | 0.0584 |

| Diagnostic test | ||||

| Serial Correlation LM Test | 0.7338 | (0.4894) | ||

| Heteroscedasticity test | 0.8508 | (0.5672) | ||

| Ramsey reset test | 1.1681 | (0.2890) | ||

Note: *** = 1%, and ** = 5% levels of significance in that order

Source: Author’s Computation

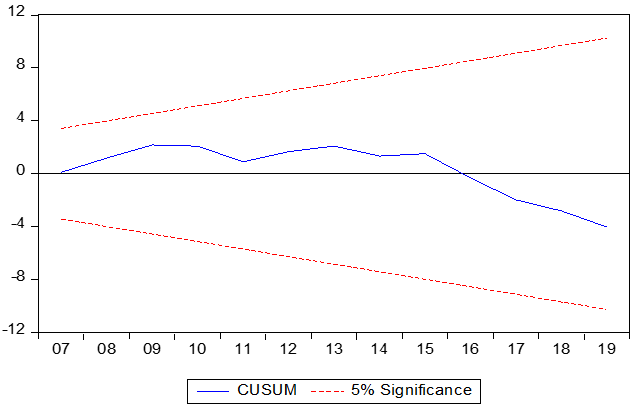

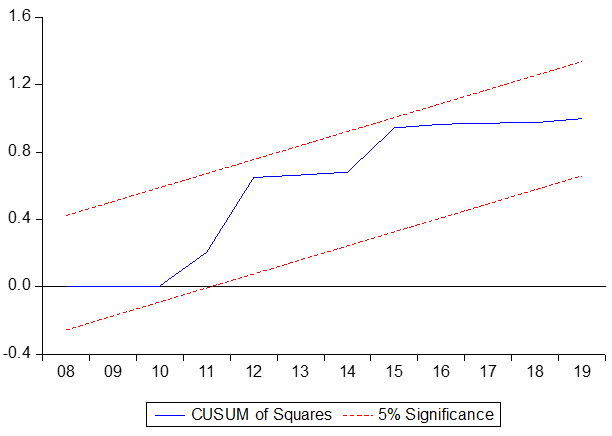

Figure 1. Stability test for model 1

Source: Author’s Computation

In the model, the error correction term [(ECT(–1)] coefficients which portray the quickness with which dynamic equilibrium will be re-established per time period after deviation on account of shocks, are negative and statistically significant. This reaffirms the presence of long run link amongst the variables. It also suggests that the models returned to steady state equilibrium after a shock.

More so, the diagnostic test results in table 4 indicate that the models are free from serial correlation in the residual. This is affirmed by the result of LM Test. In the same way, Ramsey reset test reveals that the models do not suffer from specification error. Finally, Heteroscedasticity test results depict that heteroscedasticity cause no problem to the credibility of the estimated models. This suggests that the ARDL model estimates are consistent and appropriate.

Also, the stability of the parameters estimated is assessed by the means of cumulative sum (CUSUM) and cumulative sum of squares (CUSUMSQ) to the recursive residuals estimated of the ARDL model. The cumulative sum (CUSUM) and cumulative sum of squares (CUSUMSQ) affirms the stability of the assessed parameters, given that the lines fall with the 5 percent boundaries as displayed in figure 1.

Model 2: External Debt to Export

Following the evidence of cointegration in bound test results in table 3B, the results of the short and long-run estimates of the ARDL is presented in Tables 5. The results show that debt-to-export has no statistical significance on macroeconomic instability, both in the short and long run. It implies that export cannot account for instability within the framework of debt and macroeconomic instability.

Table 5: Short and long-run estimates of ARDL (3, 4, 3, 3, 4)

Model 2: (Dependent Variable: Y)

| Variable

Y |

Coefficient | Std. Error | t-Statistic | Prob. |

| Panel A

Long run estimates |

||||

| C | 0.4204 | 0.2786 | 1.5809 | 0.1552 |

| Debt-to-export | -0.0040 | 0.0046 | -0.8753 | 0.3972 |

| CPS | -0.0020 | 0.0130 | -0.1609 | 0.8746 |

| TOP | 0.0021 | 0.0020 | 1.0800 | 0.2998 |

| GCF | -0.0035 | 0.0047 | -0.7511 | 0.4660 |

| Panel B

Short run estimates |

||||

| D(instability(-1)) | 0.161 | 0.1733 | 0.9293 | 0.3697 |

| D(instability(-2)) | 0.585*** | 0.158 | 3.699 | 0.0027 |

| D(debt-export) | -0.002 | 0.003 | -0.757 | 0.4623 |

| D(debt-export(-2)) | -0.0115** | 0.002 | -3.882 | 0.0019 |

| D(CPS) | 0.0257*** | 0.008 | 2.899 | 00124 |

| D(TOP) | 0.009*** | 0.017 | 5.387 | 0.0001 |

| D(GCF) | -0.010** | 0.0049 | 2.113 | 0.054 |

| ect(-1)* | -1.002*** | 0.176 | -5.664 | 0.0001 |

| Breusch–Godfrey serial correlation LM test | 3.3405 | (0.0735) |

| Ramsey RESET test | 1.2965 | (0.1972) |

| Heteroskedasticity test: Breusch–Pagan–Godfrey | 1.4628 | (0.1692) |

Source: Author’s Computations.

* p-value incompatible with t-Bounds distribution.

** Variable interpreted as Z = Z(-1) + D(Z).

***, ** and * represent 1%, 5% and 10% levels of significance respectively for the coefficients.

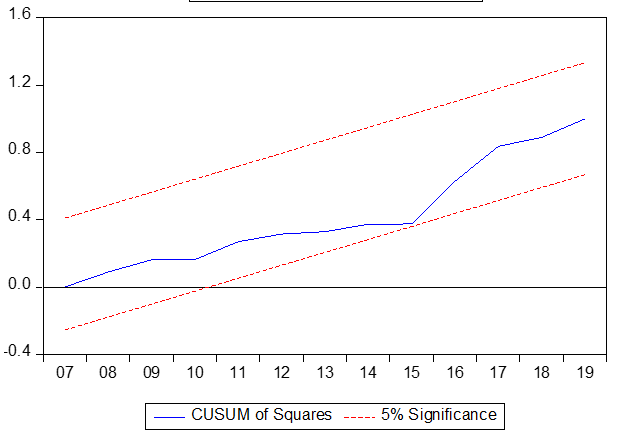

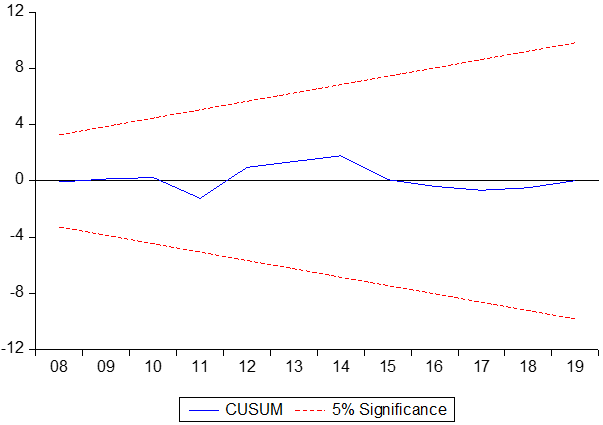

Figure 2. Stability test: Cusum and CumsumSq for debt-to-export ratio.

Source: Author’s Computation

Model 3: Debt Service to Revenue

In contrast to the findings in Model 2, the results presented in table 6 show that debt service-to-revenue ratio exerts a positive and statistically significant effects on macroeconomic instability in Nigeria. This is an indication that the larger the percentage of revenues spent on debt servicing, the more the instability within the Nigeria economy. This is supporting historical behaviours of debt servicing. For instance, in 2019, Nigeria spent 96 percent of total revenues on debt servicing (Efuntade et al, 2023). This invariably limit the fiscal space for government intervention on economic activities which would engender macroeconomic stability. High debt service-to-revenue ratio implies government have to cut spending on productive sectors such as agriculture, manufacturing, trade, and technology, thus, making the economy less productive and competitive, and also reduces the income and wealth of the nation.

A main economic implication of this finding is that external debt is too heavy on the economy to achieve stability; hence government must reduce public debt and/or increase revenues. For example, government could diversify the economy away from crude oil so as to have reliable and less volatile streams of revenue to improve macroeconomic stability in the country.

Table 6: Short and long-run estimates of ARDL (2, 2, 2, 2, 1)

Model 3: (Dependent Variable: Y)

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| Panel A

Long run estimates |

||||

| D_SER__REV_ | 0.009866 | 0.002967 | 3.325248 | 0.0061 |

| CPS | -0.020537 | 0.008508 | -2.413955 | 0.0327 |

| TOP | -0.007902 | 0.003222 | -2.452763 | 0.0304 |

| GCF | -0.014438 | 0.003811 | -3.788385 | 0.0026 |

| C | 1.450139 | 0.298805 | 4.853131 | 0.0004 |

| Panel B

Short run estimates |

||||

| D(Y(-1)) | 0.165342 | 0.141048 | 1.172239 | 0.2638 |

| D(D_SER__REV_) | 0.005567 | 0.003286 | 1.694261 | 0.1160 |

| D(D_SER__REV_(-1)) | 0.012622 | 0.005060 | 2.494490 | 0.0282 |

| D(CPS) | -0.004661 | 0.006783 | -0.687187 | 0.5050 |

| D(CPS(-1)) | 0.012255 | 0.008498 | 1.442098 | 0.1749 |

| D(TOP) | 0.000703 | 0.001723 | 0.407872 | 0.6906 |

| D(TOP(-1)) | 0.004100 | 0.002077 | 1.973792 | 0.0719 |

| D(GCF) | -0.003580 | 0.005392 | -0.663991 | 0.5193 |

| ECT*(-1) | -0.986452 | 0.165050 | -5.976673 | 0.0001 |

| Breusch–Godfrey serial correlation LM test | 0.0113 | (0.9887) |

| Ramsey RESET test | 1.6461 | (0.1280) |

| Heteroskedasticity test: Breusch–Pagan–Godfrey | 0.3268 | (0.9720) |

Source: Author’s Computations.

* p-value incompatible with t-Bounds distribution.

** Variable interpreted as Z = Z(-1) + D(Z).

***, ** and * represent 1%, 5% and 10% levels of significance respectively for the coefficients.

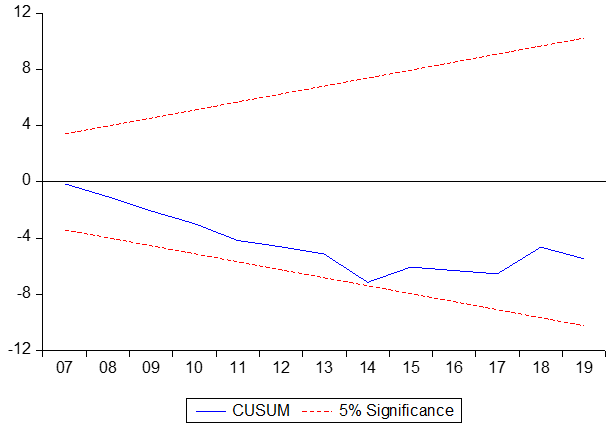

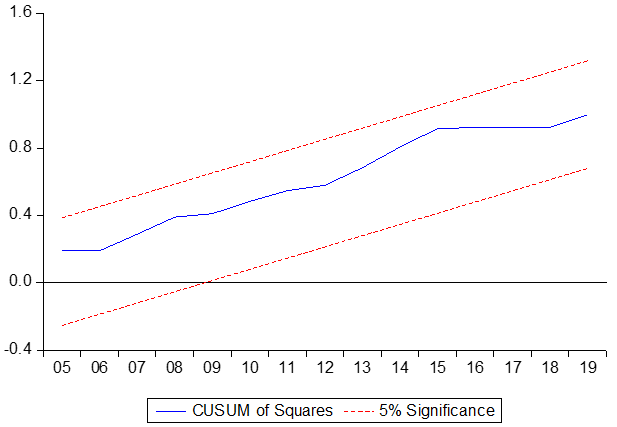

Figure 3: Stability test: Cusum and CumsumSq for the model of debt service -to-revenue ratio.

Source: Author’s Computation

Model 4: External Debt to Revenues

The results, as presented in table 7, also show that debt-to-revenue has a negative and statistically significant impact on macroeconomic instability in the short run. This implies that the stock of external debt, regardless of ratio it measures, does reduce macroeconomic instability in Nigeria, especially, in the short run. However, the result does not show any significant impact in the long run. This further shows that the effect of revenues weign on the ratio of debt stock in the long run, as such it weaking the possibility of impact on the economy in whatever form.

Table 7. Short and long-run estimates of ARDL (3, 4, 1, 3, 4)

Model 4: (Dependent Variable: Y)

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| Panel A

Long run estimates |

||||

| DEBT__TO_REVENUE | -0.00041 | 0.000326 | -1.24446 | 0.2324 |

| CPS | -5.1E-05 | 0.006886 | -0.00734 | 0.9942 |

| TOP | 0.004101 | 0.002005 | 2.045593 | 0.0587 |

| GCF | 0.000103 | 0.004163 | 0.024683 | 0.9806 |

| C | 0.28142 | 0.16796 | 1.675516 | 0.1145 |

| Panel B

Short run estimates |

||||

| D(Y(-1)) | 0.468231 | 0.252499 | 1.854384 | 0.0834 |

| D(Y(-2)) | 0.390122 | 0.203860 | 1.913671 | 0.0749 |

| D(DEBT__TO_REVENUE) | -0.000687 | 0.000252 | -2.721114 | 0.0158 |

| D(DEBT__TO_REVENUE(-1)) | 0.001194 | 0.000483 | 2.473554 | 0.0258 |

| D(DEBT__TO_REVENUE(-2)) | -0.000754 | 0.000479 | -1.575171 | 0.1361 |

| D(DEBT__TO_REVENUE(-3)) | 0.000481 | 0.000258 | 1.868428 | 0.0814 |

| D(CPS) | 0.011506 | 0.006447 | 1.784787 | 0.0945 |

| D(TOP) | 0.002495 | 0.001942 | 1.285121 | 0.2182 |

| D(TOP(-1)) | 0.004364 | 0.001997 | 2.184922 | 0.0452 |

| D(TOP(-2)) | -0.005070 | 0.001822 | -2.781902 | 0.0140 |

| D(GCF) | 0.001385 | 0.005486 | 0.252369 | 0.8042 |

| D(GCF(-1)) | -0.007964 | 0.004966 | -1.603649 | 0.1296 |

| D(GCF(-2)) | 0.014169 | 0.005641 | 2.511715 | 0.0239 |

| D(GCF(-3)) | -0.009423 | 0.003286 | -2.867191 | 0.0118 |

| ect*(-1) | -0.883331 | 0.235259 | -3.754721 | 0.0019 |

| Breusch–Godfrey serial correlation LM test | 0.5633 | (0.5826) |

| Ramsey RESET test | 1.3827 | (0.1884) |

| Heteroskedasticity test: Breusch–Pagan–Godfrey | 2.0319 | (0.0841) |

Source: Author’s Computations.

* p-value incompatible with t-Bounds distribution.

** Variable interpreted as Z = Z(-1) + D(Z).

***, ** and * represent 1%, 5% and 10% levels of significance respectively for the coefficients.

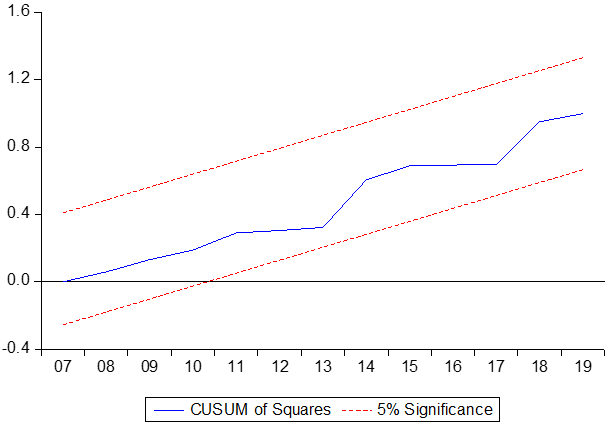

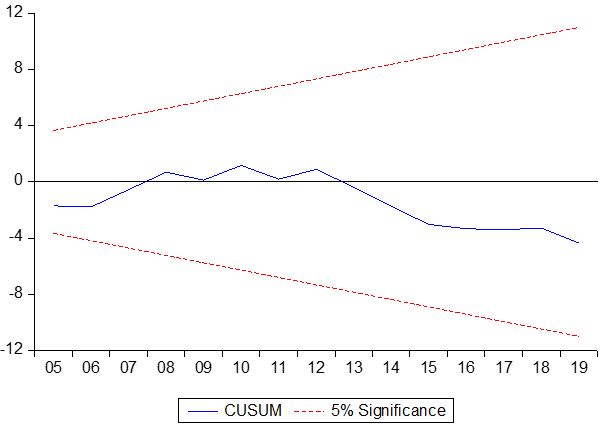

Figure 4. Stability test: Cusum and CumsumSq for debt-to-revenue Ratio on the Economic Instability Model.

Source: Author’s Computation

Diagnostic Tests

To test the reliability and robustness of the ARDL model, a battery of diagnostic tests is performed and the results are presented in the lower part of the tables 4, 5, 6 and 7. The results of the serial correlation tests suggest the estimated models do not suffer from serial correlation in the error term. Similarly, the results of Ramsay Reset test also show that the null hypothesis of inappropriate functional form was rejected, indicating that the nonlinear estimates do not suffer from specification error. The Breusch-Pagan’s test for heteroskedasticity shows that the model is devoid of heteroskedasticity’s problem. Similarly, the Breusch-Godfrey (BG) LM test suggests that the study fails to reject the null of no-auto correlation at 5% level of significance. These results indicate that the models are correctly specified and the estimates are reliable.

The study also performs further analyses to confirm the stability of parameters of the ARDL. The Cumulative sum (CUSUM) test and cumulative sum of squares (CUSUMSQ) test are performed. The results of the two tests as presented in Figures 1, 2, 3 and 4 point to the stability of both short and long-run estimates as the parameters’ stability lines are well situated within the critical boundaries.

DISCUSSION OF RESULTS AND RECOMMENDATIONS

The outcomes show that external debt stock to GDP ratio exerts a negative effect on Macroeconomic Instability (Y). This shows that an increase in external debt reduces macroeconomic instability in Nigeria both in the short and long run. Debt-to-export is not significant on macroeconomic instability both in the short and long run. It is also established that debt-to-revenue has negative and statistically significant impact on macroeconomic instability in the short run. This implies that debt-to-revenue reduces macroeconomic instability in the short run only, but the effect fades over time. In contrast; the results show that debt service-to-revenue rate exerts a positive and significant effects on macroeconomic instability in Nigeria. This implies that an increase in debt service-to-revenue worsen instability in Nigeria both in the short run and in the long run.

The findings implies that a reasonable level of borrowing from external sources helps to reduces macroeconomic instability, especially in the short-run. This implies that excessive external debts exert crowd-out effects on investment, which limits the ability of government investment in productive economic activities and limit the ability to borrow more to smooth economic cycles, thus, undermine macroeconomic stability. Therefore, as earlier stated, government should seek effective means to reduce public debt and/or increase revenue to normalise debt service payments. In this case, government might consider diversification of the economy away from crude oil driven economy to a more predictable and less volatile streams of revenue.

It is also recommended that deliberate policies be put in place to ensure that the accumulation of external debt in Nigeria is consistent with the country’s macroeconomic objectives. In this case, it is important to ensure that the borrowed funds are expended on productive activities so as to boost the capability to service the debts without defaulting and consequently achieve macroeconomic stability. More so, the projects to be financed with borrowing should be properly appraised and ensure that their technical feasibility, financial viability and economic desirability are ascertained before the funds are committed. This would help to restore financial discipline and curtail misappropriation and inefficiency that may mar the future revenue to use in servicing such debts. In doing this, government should ensure that borrowings are done on terms that are consistent with sustainability profile that would make its servicing easier for the economy. This is necessary if the country is to outgrow its debt servicing problems, restore creditworthiness and achieve macroeconomic stability.

REFERENCE

- Abdulkarim, Y. & Saidatulakmal, M. (2021). The impact of government debt on economic growth in Nigeria. Cogent Economics and Finance, 9(1), 1 – 19.

- Bresser-Pereira, L. C. (2024). The Dutch Disease and its neutralization. In New Developmentalism (pp. 139-148). Edward Elgar Publishing.

- Budget Office of the Federation, (2020). Addendum of the 2020-2022 Medium Term Expenditure Framework & Fiscal Strategy Paper. Budget Office of the Federation and Federal Ministry of Finance Budget and National Planning, Abuja.

- Central Bank of Nigeria (2020), Statistical Bulletin, Publication of Central bank of Nigeria

- Dey, S. R., & Tareque, M. (2020). External debt and growth: role of stable macroeconomic policies. Journal of Economics, Finance and Administrative Science, 25(50), 185-204.

- Dey, S. R., & Tareque, M. (2020). External debt and growth: role of stable macroeconomic policies. Journal of Economics, Finance and Administrative Science, 25(50), 185-204.

- Edo, S., Nneka E. O., and Isuwa, F. D. (2020). Growing external debt and declining export: The concurrent impediments in economic growth of sub-Saharan African countries. International Economics 161, 173–87.

- Efuntade, O. O., Efuntade, A. O., & FCIB, A. (2023) Debt Servicing To Revenue Ratio (DSR) in the Context of Fiscal Space, Barro-Ricardian Equivalence and Debt Sustainability in Nigeria (General Outlook and Trend).

- Egert, B. (2013). The 90% Public Debt Threshold: The Rise and Fall of a Stylised Fact, CESifo Working Paper 4242. Munich: CESifo Group.

- Gootjes, B., & de Haan, J. (2022). Procyclicality of fiscal policy in European Union countries. Journal of International Money and Finance, 120, 102276.

- Gootjes, B., & de Haan, J. (2022). Procyclicality of fiscal policy in European Union countries. Journal of International Money and Finance, 120, 102276.

- Haghighi, H.K., Sameti, M. & Isfahani, R.D. (2012). The Effect of Macroeconomic Instability on Economic Growth in Iran. Research in Applied Economics, 4(3), 39-63.

- IMF (2010). From Stimulus to Consolidation: Revenue and Expenditure Policies in Advanced

and Emerging Economies. Washington, DC: International Monetary Fund. - Ismihan, M., Metin-Ozcan, K., & Tansel, A. (2005). The Role of Macroeconomic Instability in Public and Private Capital Accumulation and Growth: The Case of Turkey 1963–1999. Applied Economics, 37(2), 239-251.

- Joshua, Udi, Festus F. Adedoyin, & Samuel A. Sarkodie. (2020). Examining the external-factors-led growth hypothesis for the South African economy. Heliyon 6, 1–8.

- Khan, M., Raza, S., & Vo, X. V. (2024). Government spending and economic growth relationship: can a better institutional quality fix the outcomes?. The Singapore Economic Review, 69(01), 227-249.

- Kolawole, B. O. (2024). External Debt and Economic Growth Relationship in Nigeria: A Reconsideration. Theory, Methodology, Practice-Review of Business and Management, 20(01), 21-32.

- Mensah, L. Bokpin, G. & Boachie-Yiadom, E. (2018). External Debts, Institutions and Growth in SSA. Jounal African Business, 19, 475–490.

- Muhammad, A. & Zaman, R. (2014). The Role of External Debt on Economic Growth: Evidence from Pakistan Economy, Journal of Economics and Sustainable Development, 5(4), 140- 147.

- Otovwe, E. (2023). The implication of public debt and financial instability on economic growth: A case study of selected West African countries (Doctoral dissertation, Anglia Ruskin Research Online (ARRO)).

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of applied econometrics, 16(3), 289-326.

- Rafique, R., Nisar, A., & Shah, S. S. A. (2024). Testing the effects of fiscal policy shocks on output growth in recession and expansion: empirical evidence from developing countries. Economic Change and Restructuring, 57(3), 129.

- Ring, T. S., Abdullah, M. A., Osman, S. M., Hamdan, R., Hwang, J. Y. T., Mohamad, A. A., Hassan, M. K. H., & Khalid, F. D. (2021). Impact of External Debt on Economic Growth: The Role of Institutional Quality. International Journal of Research in Economics and Management Science, 10(3), 223 – 236.

- Saheed S. S., Sani I. E. & Idakwoji, B. O. (2015). Impact of Public External Debt on Exchange Rate in Nigeria. International Finance and Banking, 2(1), 15 – 26.

- Sahu, A. K., & Mahalik, M. K. (2024). What drives more for macroeconomic instability-carbon inequality or income inequality? Panel evidence from emerging economies. Environment, Development and Sustainability, 1-24.

- Senadza, B., Fiagbe, A. & Quartey P. (2018). The effect of external debt on economic growth in sub-Saharan Africa. International Journ-al of Business and Economic Sciences Applied Research 11, 61–69.

- Spilbergs, A., Norena-Chavez, D., Thalassinos, E., Noja, G. G., & Cristea, M. (2023). Challenges to Credit Risk Management in the Context of Growing Macroeconomic Instability in the Baltic States Caused by COVID-19. In Digital Transformation, Strategic Resilience, Cyber Security and Risk Management (pp. 83-104). Emerald Publishing Limited.

- Ultremare, F. (2023). Debt–public. Elgar Encyclopedia of Post-Keynesian Economics, 45(1), 101.