Remittances and Domestic Investment in Sub-Saharan Africa: The Role of Exchange Rate

- Agbafor, Michael Ogbonna.

- Edeh, Chukwudi Emmanuel.

- Nwaobi, Obinna Victor

- 801-813

- Aug 12, 2024

- Economic Development

Remittances and Domestic Investment in Sub-Saharan Africa: The Role of Exchange Rate

1Agbafor, Michael Ogbonna., 2Edeh, Chukwudi Emmanuel., 2Nwaobi, Obinna Victor

1Department of Economics, Ebonyi State University, Abakaliki

2Department of Economics, Enugu State University of Science and Technology Enugu

DOI: https://doi.org/10.51244/IJRSI.2024.1107063

Received: 17 May 2024; Accepted: 31 May 2024; Published: 12 August 2024

ABSTRACT

This study examines the impact of remittances on domestic investment and the interplay between remittances and exchange rates in Sub-Saharan African countries from 1998 to 2022. The results of the Levin, Lin & Chu t* (2002) panel unit root test indicate that all the time series variables are stationary at levels, while the Johansen-Fisher panel cointegration test shows evidence of a long-run relationship among the variables in the model. Panel FMOLS regression techniques are employed to assess this relationship. Findings indicate that remittance inflows significantly bolster private domestic investment in the region, but the interaction of remittances and exchange rates negatively and significantly decreases domestic investment in the region. The causality relationship analysis shows that remittances unilaterally influence private domestic investment, underscoring their importance in regional economic dynamics. The study recommends that policymakers prioritize policies that enhance remittance inflows by reducing transaction costs, improving remittance channels, and promoting financial literacy among recipients. Stabilizing exchange rates is critical to mitigate depreciation’s adverse effects on remittances and subsequent domestic investment. Central banks in the region are advised to manage foreign exchange reserves and implement appropriate monetary policies for stability.

Keywords: Remittances, Exchange rates and domestic investment

INTRODUCTION

Sub-Saharan Africa, a region comprising 49 countries located south of the Sahara Desert, boasts a rich tapestry of cultural diversity and ecological landscapes. From dense rainforests to arid deserts, its geographical span encompasses a range of ecosystems. This diversity extends to its people, with myriad ethnic groups, languages, and traditions shaping its cultural landscape. The legacy of colonialism still influences the region, impacting political, economic, and social structures.

Despite abundant natural resources, Sub-Saharan Africa grapples with economic challenges such as poverty, unequal wealth distribution, and infrastructure deficits. However, sectors like agriculture, mining, and services offer avenues for growth. With a youthful population, the region faces both challenges and opportunities in education, employment, and societal development.

Political instability and varying governance structures mark the region’s history, alongside health challenges like malaria, HIV/AIDS, and recent events such as the COVID-19 pandemic. Migration, historically tied to the Trans-Saharan trade, has shaped the region, with significant emigration to Europe and North America during the mid-20th century (Allen, 2021).

Remittances, crucial financial transfers from migrants to their home countries, play a significant role in Sub-Saharan Africa’s economy, often exceeding Foreign Direct Investment (FDI) and official development assistance (ODA). Nigeria, in particular, ranks among the top recipients globally. However, effective government policies to engage diaspora communities in economic development remain lacking, unlike successful models seen in countries like Israel, India, and Chile (Allen, 2021).

Investment stands as a key driver of economic growth in Sub-Saharan Africa. Domestic private investment, involving spending on assets like machinery, infrastructure, and research, fuels job creation, technological advancement, and economic diversification. The private sector’s role in resource allocation and utilization is pivotal, recognized by international organizations for its potential to drive inclusive and sustainable growth.

Unique factors influence the impact of remittances on domestic investment in Sub-Saharan Africa, including economic structure, financial inclusion challenges, and reliance on agriculture. Proactive policies that encourage the productive use of remittances for investment can amplify their positive effects, necessitating context-specific strategies tailored to the region’s diverse economic, social, and political landscapes

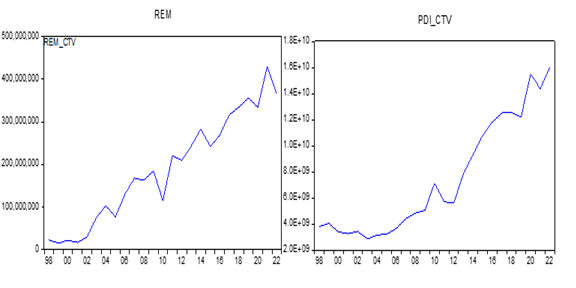

Examining international remittance inflows, evidence of the trend of remittance inflows and private domestic investment on some countries in Sub-Sahara Africa can be evaluated. Ivory Coast boasts a substantial diaspora, with Ivorian communities residing in diverse countries globally. Remittances frequently emanate from these diasporic communities. The graphical representation in Figure 1 depicts the trend of remittance inflows and private investment in Côte d’Ivoire from 1998 to 2022.

Figure 1: Graphical trend of remittance inflows and private domestic investment in Ivory Coast

Source: Researcher’s graphical output

In 2016, remittance inflows into Côte d’Ivoire (CDI) accounted for approximately 1% of the gross domestic product (GDP), according to the World Bank (2016). CDI stands out as a net sender of remittances, with outflows being nearly three times higher than inflows, underscoring its significance as a destination for migrants. Over the past two decades, both remittance inflows and outflows have witnessed an upward trend, as illustrated in Figure 1. Following a slight decline in inflows post-2014, estimates for 2017 suggest a recovery to 2014 levels. Outflows peaked in 2014 at USD 746 million, decreasing to USD 650 million in 2015 (Centre for Financial Regulation & Inclusion, 2018).

Recent data from the World Bank (2024) reveals a decline in remittance inflows since 2021. Concurrently, the trend of private domestic investment has exhibited fluctuations, with an overall appreciation observed between 2021 and 2022.

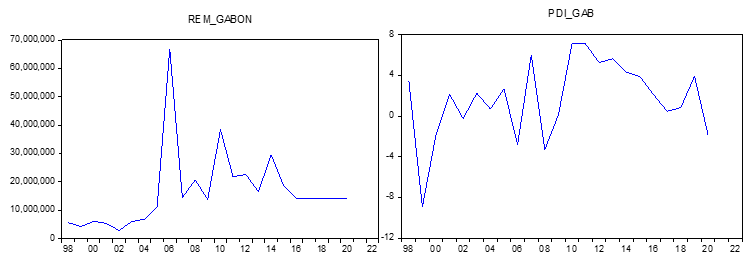

Gabon has a diverse population, and remittances may come from Gabonese nationals living abroad, particularly in Europe and other African (World Bank, 2023). Remittances play a role in Gabon’s economy, contributing to foreign exchange reserves and potentially supporting household income (World Bank, 2023).

Figure 2: Graphical trend of remittance inflows and private domestic investment in Gabon

Source: Researcher’s graphical output

Remittance inflows to GDP (%) in Gabon was reported at 0.11579 % in 2020 (WDI, 2021). The trend has remained steady over the past ten years. Remittance inflows in Gabon dropped from 29.47 million dollars in 2014 to 18.46 million dollars. In 2022, the personal remittances received in Gabon did not change in comparison to the previous year. The personal remittances received remained at 18.46 million U.S. dollars (Statista, 2024).

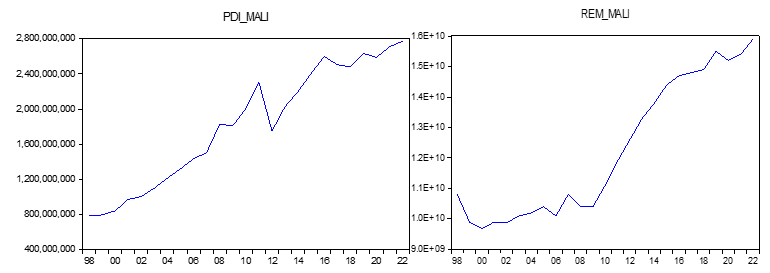

Remittances are an essential component of Mali’s economy, contributing to foreign exchange reserves and supporting household income (World Bank Development indicators, 2018). Mali has a significant diaspora, with many Malians residing in other countries, particularly in Europe and neighboring West African nations (World Bank Development indicators, 2018).

Figure 3: Graphical trend of remittance inflows and private domestic investment in Mali

Source: Researcher’s graphical output

While the private domestic investment has generally been on an upward trajectory throughout the study period, experiencing a dip around 2019, it has consistently shown an upward trend since 2020. In contrast, personal remittances received in Mali exhibited minimal variation in 2022 compared to the preceding year, 2021, maintaining a level of approximately 1131 million U.S. dollars. The decline of 0.5 million U.S. dollars (-0.04 percent), as reported by Statista in 2024, indicates no significant change from the figures observed in 2021.

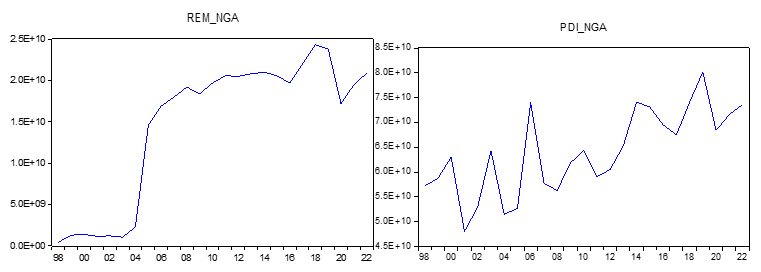

Remittances play a significant role in Nigeria’s economy, contributing to foreign exchange reserves and supporting household income. Nigeria has a large diaspora, and many Nigerians living abroad send remittances back to their families. The Central Bank of Nigeria (CBN) and other financial institutions typically monitor and report on remittance inflows. (Englama, 2007). The majority of remittances to Nigeria come from countries with significant Nigerian diaspora populations, including the United States, the United Kingdom, Canada, and other European countries (Taiwo, 2007). The Central Bank of Nigeria has implemented various measures to enhance the tracking and inflow of remittances. In 2020, the CBN introduced the “Naira 4 Dollar Scheme,” which provided an incentive for recipients of remittances by offering them additional Naira for every dollar received (CBN, 2021).

Figure 4: Graphical trend of remittance inflows and private domestic investment in Nigeria

Source: Researcher’s graphical output

While private domestic investment has shown volatility and a declining trend, remittance inflows in Nigeria have demonstrated a consistent upward trajectory since the 1990 s. Notably, there was a sharp decline between 2019 and 2020, which can be attributed to the impact of the COVID-19 pandemic. However, a recovery has been evident since 2021. In 2022, personal remittances received in Nigeria experienced an increase of 0.7 billion U.S. dollars (+3.59 percent) compared to 2021. The total personal remittances received amounted to 20.13 billion U.S. dollars in 2022 (Statista, 2024).

The interaction between exchange rates and remittances can have significant implications for domestic investment in an economy. Exchange rate movements can directly affect the value of remittances. When the local currency strengthens against the currencies of the countries where migrants are earning, the value of remittances in the local currency increases. Conversely, a weaker local currency may result in lower remittance values. In economies where remittances form a substantial portion of household income, the exchange rate’s impact on remittances can influence overall consumer spending and saving patterns. Higher remittance values can contribute to increased disposable income, potentially stimulating consumption and investment.

Exchange rate movements can influence inflation and interest rates. A depreciating currency may contribute to higher inflation, affecting the purchasing power of remittances. Central banks may respond with changes in interest rates to manage inflation, which, in turn, can impact the cost of borrowing for domestic investment. In addition, Migrants sending remittances may be influenced by currency risk. Exchange rate fluctuations can affect the amount of money their families receive in the home country. This uncertainty may influence migrants’ decisions on the timing and amount of remittances sent. Against these backdrops, the present study argues that studying the interplay between exchange rates and remittance inflows on domestic investment is essential for policymakers, businesses, and researchers to make informed decisions, formulate effective policies, and contribute to the overall economic well-being of a nation.

Countries in Sub-Sahara Africa have been grappling with persistent challenges in stabilizing and achieving sustainable economic growth and development. These challenges encompass low rates of savings, investments, per capita income, productivity, foreign exchange earnings, high poverty rates, inflation, and low aggregate demand. Additionally, issues such as balance of payments deficits, continuous depreciation in the exchange rate, and overdependence on imports further compound the economic difficulties. These challenges have resulted in developmental setbacks for the nation, leading to its classification as an underdeveloped nation despite its abundant resource endowments.

The classical and neoclassical economic theories have tended to overemphasize the role of capital accumulation, while Keynesian economics asserts that investment spending is a pivotal component of aggregate expenditures. Private domestic investment, involving investments by individuals within a specific nation or residence country, includes initiatives like starting small and medium-scale enterprises. The persistently low investment rates in Sub-Sahara African countries seem to be linked to insufficient incomes and savings necessary to fund various private investment opportunities in the country. In the realm of development and international finance, migrant remittances are globally acknowledged as a contemporary and significant source of financing private investment, particularly in developing countries.

Various perspectives exist on the remittance-investment relationship. Some scholars posit that it is the low level of investment that prompts migrants to remit a portion of their earnings to their country of origin, seeking to capitalize on the advantages of start-up firms where multinational enterprises are lacking. In many less developed countries, the primary motivation for remitting money is to exploit untapped investment opportunities in the home country. Consequently, proponents of this view argue that the low level of investment in the country of origin attracts remittance inflows. Conversely, others believe that the continuous influx of remittances is the driving force behind the increased rate of investment. Therefore, this research aims to reconcile these conflicting perspectives among researchers using cross-country analysis.

To gain a comprehensive understanding, it is essential to supplement expert opinions by delving into what propels the impact of remittance flows on domestic investment. The argument in the present study examines the exchange rate- remittance inflows interplay and how both variables impact private domestic investment in Sub-Saharan Africa region. Remittance inflows can also affect exchange rates. Large remittance inflows may lead to an appreciation of the domestic currency if they result in increased demand for the local currency. However, the impact can be nuanced and depends on various factors, including the overall economic situation and policies. Government policies, such as those related to foreign exchange regulations and incentives for domestic investment, can influence the dynamics between remittances, exchange rates, and investment.

This study addresses the potential role of remittances in stabilizing exchange rates and promoting private sector investment. While previous studies (Ranjan 2020; Ibrahim 2018; Ezike & Ogboi, 2017; Edoun & Ezeanyika, 2015; Jushi 2021; Edeh, Ijemba & Njeze 2023) have neglected this area, the present research asserts the need to investigate the interaction between remittance inflows and exchange rates on private domestic investment in Sub-Saharan African countries. Employing a Panel Fully Modified Ordinary Least Squares regression technique within an amended Accelerator investment model, this study aims to fill the gap in empirical research by examining this relationship for the first time.

The work is organized in five sections. The introduction serves as the first part of the study, while the literature review served as the second part. Methodology forms the third section of the study. Results and discussions formed the fourth part of the study. The final part of the is the conclusion and recommendations.

LITERATURE REVIEW

Private domestic investment encompasses the procurement and advancement of productive assets like machinery, equipment, buildings, and technology to generate income and bolster economic activity. It fosters capital formation within a nation, accumulating both physical and financial capital to produce goods and services, foster employment, and propel economic advancement (Ofosu-Mensah, Aboagye, Barnor, & Agyei, 2022).

Remittances can potentially contribute to exchange rate stability in a recipient economy. When individuals send remittances back to their home country, it increases the supply of foreign currency in the recipient country. This influx of foreign currency can help stabilize the exchange rate by offsetting currency depreciation pressures. Additionally, remittances can enhance overall economic stability, which indirectly contributes to exchange rate stability. However, the impact of remittances on exchange rate stability can vary depending on various factors such as the volume of remittances, the economic policies in place, and external market conditions (Singer, 2010).

Theoretically, the accelerator theory, pioneered by Clark (1923) posits that investment spending rises with increases in demand or income. It suggests firms adjust investment to match demand levels, termed the Capital Stock Adjustment model. Developed further by Koyck’s (1954), Flexible Accelerator Theory addressed the lag in capital stock adjustment, allowing firms to adjust investment over time. This model assumes firms aim to close the gap between desired and actual capital stock gradually, leading to a net investment equation: I = ΔK = kΔYt, where I represents net investment, ΔK is the change in capital stock, and ΔYt is the change in current output, with k as the capital/output ratio.

Edeh, Ijemba, and Njeze (2023) assessed remittances’ influence on domestic investment in Nigeria (1981–2020). Employing accelerator theory, they constructed a model incorporating remittances, GDP, interest rate, and private sector credit. Unit root tests confirmed stationarity, and bound tests indicated cointegration. Auto regressive Distributed Lagged model results revealed a positive yet insignificant impact of remittances on investment, both short and long term. Similarly, Ojapinwa and Odekunle (2018) examined remittances’ impact on investment levels in Nigeria (1977–2010). Results suggest remittances enhance physical investment stock, particularly in developed financial systems, complementing investment financing.Top of Form

Ranjan (2020) explored remittances’ impact on domestic investment across Six South Asian Countries using panel data from 1991 to 2017. Employing advanced panel estimation methods, the study finds remittances positively affect domestic investment both short and long term, indicating their use for capital development. Panel causality analysis suggests a unidirectional causality from remittances to domestic investment. In the same vein, Ibrahim (2018) explored remittances’ impact on domestic investment in five Sub-Saharan African countries. Using panel fixed effects with data from 1984 to 2014, remittances positively affect investment. Interaction effects reveal political institutions and financial development magnify remittances’ impact. Results suggest remittances can bolster domestic investment, influenced by local institutions and financial sector development.

Similarly, Mensah (2018) studied remittances and infrastructure’s impact on investment in Nigeria (1986–2017). Long-term effects showed positivity in remittances and human capital, while GDP investment and interest rate negatively affected economic growth. Short-term effects exhibited positivity in remittances, human capital, GDP investment, and inflation, with negative influence from interest rates.

Okeke, Chinanuife, and Muogbo (2021) examined how international remittances affect private domestic investments in Nigeria, investigating their causal relationship. Using annual data from 1981 to 2014, Philips-Perron and Toda-Yamamoto tests were conducted. Results indicate both remittances and private domestic investment are integrated of order one, with a unidirectional causal relationship from remittances to private investment.

Ezike and Ogboi (2017) studied household inward remittances’ impact on productive investment in Nigeria using GMM estimator on WDI 2015 data. Findings suggest remittances discourage productive investment and increase consumption of imported goods. Ebenezer and Gbenga (2020) investigated remittance income’s effect on food importation in Nigeria (1977–2019), concluding that remittances negatively influence food importation, suggesting they are not pivotal in augmenting it.

Edoun and Ezeanyika (2015) explored if foreign remittances promote investment in rural non-farm sectors among Igbo in Southeast Nigeria. Regression analysis on remittance-receiving households revealed a negative correlation between remittance amounts and rural non-farm investment ratio, yet a positive correlation with expenditure, indicating allocation to profit-oriented activities in this sector.

Ilu, (2019) explored how remittances from Nigerians in Diaspora influence exchange rate stability from 1990 to 2018. Using annual time series data, the study examined remittance inflow as a percentage of GDP, FDI, and oil prices. Employing the ARDL model, both short and long-run analyses indicate remittances positively and significantly affect the exchange rate, leading to Naira depreciation, while FDI and oil prices appreciate the Naira’s value.

Keho (2024) examined the link between remittances, financial development, and domestic investment in ten Sub-Saharan African countries from 1975 to 2019. Using the panel Pooled Mean Group estimator, the study showed positive effects of both remittances and financial development on investment. Their interaction was also positive, emphasizing their complementary role. These findings stress the financial sector’s importance in amplifying remittances’ positive impact on investment in West African countries, highlighting a threshold effect of financial development in this dynamic. Likewise, Kudaisi, Ojeyinka, & Osinubi, (2021) explored the nexus between financial liberalization, remittances, and economic growth in Nigeria (1990–2018). They employed the financial liberalization index by Chinn and Ito (2006) and found a positive and significant impact of financial liberalization and remittances on economic growth, both short and long term.

The literature review reveals a lack of empirical research on the combined impact of exchange rates and remittance inflows on domestic investment in the West African sub-region. To address this gap, this study employs the interaction regression approach.

METHODOLOGY

The study adopted Ex Post Facto research design. Countries in sub-Saharan Africa involved in this study for the period 1998-2022 include: Nigeria, Cote d’Ivoire, South Africa, Sierra Leone, Niger, Mali, Senegal, and Gabon. The data for remittances inflows, domestic investment, nominal exchange rate, domestic credit to the private sector, and interest rate were sourced from the World Bank indicator. For consistency, the complete dataset was sourced from the World Bank Database’s World Development Indicators.

This study adopts the accelerator model of investment as the theoretical framework. The model posits that changes in investment is as a result of changes in national output. This is the process of induced investment, which depends on the rate of change of output or of sales. Remittance inflow is included as an independent variable influencing private domestic investment in Sub-Saharan African countries. The model specification for this study is as follows:

Ip = f(ΔY), (3.1)

where Ip is induced private investment which depends on (i.e., is a function of) change(s) in national income (ΔY). where Ip is induced private investment which depends on (i.e., is a function of) change(s) in national income (ΔY). An amended accelerator model to suit the present study is shown below:

𝑃𝐷𝐼 = (RGDP, REM, EXR, EXR*REM, CPS,) (3.2)

Where, 𝑃𝐷𝐼 is Private Domestic Investment, while RGDP is Real National output, 𝑅EM is International Migrant Remittances, EXR is Exchange Rate, EXR*REM is interactive effect of remittances inflows and exchange rate, while CPS is Credit to Private Sector. To enhance parameter interpretation and minimize noise, the entire dataset was logged before estimation.

![]() (3.3)

(3.3)

Where:

LPDI = Private domestic investment (dependent variable: proxied by gross fixed capital formation). Explanatory variables are: LRGDP = Real National Output; LREM = Remittance inflows; LEXR = Exchange rate of domestic currencies to the dollar; LCPS = Credit to the private sector by the banking system of various countries; β0– β5 = Parameter estimates; t = time series (annual); i = country; α = unknown intercept for each entity, and; ε = error term

A priori Expectations:

![]()

The model is estimated using Fully-Modified Ordinary Least Squares (FMOLS) regression analysis introduced by Phillips and Hansen (1990). FMOLS employs a semi-parametric approach for estimating long-run parameters, ensuring consistency even with small sample sizes. It addresses issues like endogeneity, omitted variable bias, and allows for heterogeneity in long-run parameters. FMOLS estimates a single cointegrating relationship among I (1) variables. Following Priyankar (2018), the FMOLS estimator is obtained accordingly:

![]() (3.4)

(3.4)

Equation (3.5) includes terms Yt+ and ʎ12+ to address endogeneity and serial correlation. As per Adom et al. (2015), the FMOLS estimator technique is asymptotically unbiased. It exhibits a fully efficient mixture-normal asymptotic distribution, enabling standard Wald tests through asymptotic chi-square statistical inference.

Dumitrescu and Hurlin (2012) proposed a non-causality test for heterogeneous panels that takes into account individual unit fixed effects. The test is based on the estimation of the following regression:

i, N t, =1,…,T, 3.5

i, N t, =1,…,T, 3.5

i, N t, =1,…,T, 3.6

i, N t, =1,…,T, 3.6

In Equation (3.5), individual effects αi are fixed, and D represents first differences. The autoregressive parameters γi (k) and regression coefficient slopes βi (k) differ across series. Likewise, in Equation (3.6), autoregressive parameters βi (k) and regression coefficients slopes γi (k) vary. To assess Granger causality from remittances to PDI, the null hypothesis is tested.

H0: βi = 0 for all i = 1, …, N is tested against the alternative:

Ha: βi ≠ 0 for some i є {1, …, N}

β ≡ [Bi (1), …, βi(k)]′ represents the ‘homogeneous non-causality’ hypothesis, distinguishing it from the alternative hypothesis, which permits causality from remittances to investment for some individuals. Similarly, to investigate Granger causality from domestic investment to remittances, the null hypothesis is tested.

H0: γi = 0 for all i = 1, …, N is tested against the alternative:

Ha: γi ≠ 0 for some i є {1, …, N}

RESULTS AND DISCUSSIONS

This section presents and discusses the estimated models. It initiates with the presentation and discussion of stationarity test and cointegration test results. Subsequently, the estimated models, diagnostic checks, and tests for model stability are presented and discussed.

The series in the panel data are tested for stationarity. The result is shown in Table 1 below

Table 1: Result of Levin, Lin & Chu t* (2002) Unit Root Test of the Variables

| Variable | Level Form | First Difference | Order of integration | ||

| Levin, Lin & Chu test statistic | Probability | Levin, Lin & Chu test statistic | Probability | ||

| CPS | 0.81058 | 0.7912 | -5.12028 | 0.0000 | I (1) |

| EXR | 5.38187 | 1.0000 | -4.11021 | 0.0000 | I (1) |

| GDP | 3.24758 | 0.9994 | -2.17772 | 0.0147 | I (1) |

| PDI | 2.64746 | 0.9959 | -6.53699 | 0.0000 | I (1) |

| REM | 1.27388 | 0.8986 | -3.24434 | 0.0006 | I (1) |

Source: Author’s computation from E Views 9

The result of the Levin, Lin & Chu t* (2002) Unit root test is presented in Table 1 above. Using the probability values of the Levin, Lin & Chu (2002) t-statistic, which were all below 0.05 at first difference, the result shows that all the time series variables are stationary at first difference, I (1); The next step is to test for the existence of long run relationship among these variables. The essence of cointegration test is to check if the above non-stationary variables have a long run relationship. The result was presented in the Table 2 below.

Table 2 Result of Johansen Fisher Panel Cointegration Test

| Johansen Fisher Panel Cointegration Test | ||||

| Series: REM PDI EXR GDP CPS | ||||

| Unrestricted Cointegration Rank Test (Trace and Maximum Eigenvalue) | ||||

| Hypothesized | Fisher Stat.* | Fisher Stat.* | ||

| No. of CE(s) | (from trace test) | Prob. | (from max-eigen test) | Prob. |

| None | 181.7 | 0.0000 | 118.4 | 0.0000 |

| At most 1 | 87.75 | 0.0000 | 60.74 | 0.0000 |

| At most 2 | 42.82 | 0.0003 | 33.42 | 0.0065 |

| At most 3 | 24.45 | 0.0802 | 22.10 | 0.1399 |

| At most 4 | 17.30 | 0.3667 | 17.30 | 0.3667 |

| * Probabilities are computed using asymptotic Chi-square distribution. | ||||

Source: Author’s computation from E views 9

Table 2 displays the outcomes of the Johansen Fisher Panel Cointegration analysis. The Trace test and maximum eigenvalue revealed that the Fisher Stat* values (from Trace test) surpass those of the Fisher Stat* (from max-eigen test) until the fourth null hypothesis. This suggests four cointegrating equations. All probability values of the null hypotheses were below 0.05 until the fourth null hypothesis, supporting the presence of cointegration. Hence, we infer a long-term relationship among all variables in the model.

Due to the stationarity of the result above and the cointegration methodology used, the Fully Modified OLS is deemed appropriate for the estimation of the parameters of the model in this study. The result of the regression result is presented in Table 3 below.

Table 3: Result of the Panel Fully Modified OLS

| Dependent Variable: LPDI | ||||

| Method: Panel Fully Modified Least Squares (FMOLS) | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| LREM | 0.369815 | 0.112545 | 3.285944 | 0.0012 |

| LEXR | 1.102721 | 0.316313 | 3.486174 | 0.0006 |

| LREM*LEXR | -0.066111 | 0.019618 | -3.369844 | 0.0009 |

| LGDP | 0.997449 | 0.200033 | 4.986420 | 0.0000 |

| LCPS | 0.286333 | 0.148661 | 1.926074 | 0.0557 |

| R-squared | 0.995316 | Mean dependent var | 19.60606 | |

| Adjusted R-squared | 0.995002 | S.D. dependent var | 7.350177 | |

| S.E. of regression | 0.519645 | Sum squared resid | 48.33547 | |

| Long-run variance | 0.304743 | |||

Source: Author’s computation from E Views 9

Table 3 illustrates FMOLS estimates of the private domestic investment-remittances relationship, revealing a positive association. Higher remittance inflows correlate with increased private domestic investment. A one percent rise in remittance leads to a 40 percent uptick in private domestic investment, statistically significant at the 5 percent level (p = 0.0012). This underscores remittances’ potential to stimulate private investment in a stable economy. Hence, policymakers should prioritize strategies to enhance remittance inflows, as they could serve as a vital tool for bolstering private domestic investment with focused policy attention and direction.

The interacting variables (remittances and exchange rate) have a negative relationship with private domestic investment in the table above. The result indicates that the combined effect of exchange rate depreciation and remittances is inversely related to private domestic investment. A one percent increase in the combined effect of exchange rate depreciation and remittances leads to a 6.6 percent decline in private domestic investment. This result is considered statistically significant at the 5 percent level, with a probability value of 0.0009.

The GDP-private domestic investment relationship is positive, aligning with the accelerator theory. A one percent GDP increase corresponds to a 99.7 percent private investment increase, statistically significant at 5% (p = 0.0000). Credit to the private sector shows a positive but insignificant association with a 28.6 percent increase in investment (p = 0.055). Exchange rate positively correlates with investment, where a one percent depreciation leads to a 110 percent investment increase (p = 0.0006).

As an OLS-based model, the coefficient of determination is 0.995, indicating that 99.5 percent of variations in domestic investment are explained by the explanatory variables. This highlights the model’s high explanatory power.

The result of the estimation of the causality relationship between private domestic investment and remittance inflows is presented in Table 4 below. Optimal lag length is selected based on the AIC.

Table 4: Pairwise Dumitrescu Hurlin Panel Causality Tests

| Pairwise Dumitrescu Hurlin Panel Causality Tests | |||

| Null Hypothesis: | W-Stat. | Zbar-Stat. | Prob. |

| REM does not homogeneously cause PDI | 6.88587 | 5.13951 | 3.E-07 |

| PDI does not homogeneously cause REM | 3.00387 | 0.83577 | 0.4033 |

Source: Author’s computation from E Views 9

Table 4 displays the findings of the Dumitrescu Hurlin Panel causality analysis. The probabilities of the W-statistics and Zbar-statistic were considered for interpretation. For the initial pair of null hypotheses, the probability values (P (W-stat, and Zbar-stat)) were 3.E-07 and 0.4033, respectively. This indicates a uni-directional causality relationship from remittances to private domestic investment. These results align with the FMOLS findings presented in Table 4. This present finding is supported by the result of the study by Ranjan (2020) which shows that their panel causality results suggest the presence of uni-directional causality running from remittances to domestic investment in South Asia countries for the period 1991–2017. Also, the Yamamoto causality test carried out by Okeke, et al. 2021 reveals that there is a unidirectional causal relationship between remittances and private investment in Nigeria

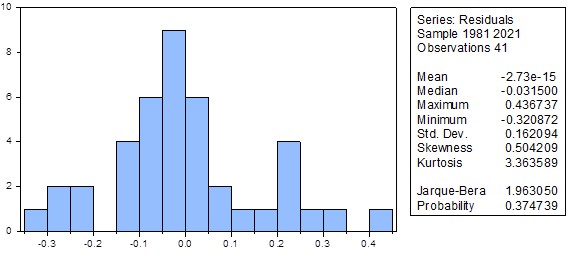

Test for Normal Distribution of Residual

Normality test is essential to ascertain the distribution of the data set in the model. The null hypothesis for this test is that the residuals are normally distributed. This is to be rejected if the probability of Jarque-Bera is less than 0.05.

To test this, we use the Jarque-Bera (JB) test. In this case, the p-value of the JB test is 0.374734. Since this p-value is greater than the common significance level of 0.05, we fail to reject the null hypothesis. Therefore, we conclude that the residuals are normally distributed.

CONCLUSION AND RECOMMENDATIONS

Theoretical studies propose that remittance inflows can influence domestic investment by bolstering savings, consumption, promoting financial development, improving the balance of payment deficit through exchange rate effects, easing credit constraints, and enhancing human and physical capital in migrant-receiving countries. This study explores the role of remittances in bolstering domestic investment and investigates the interaction between remittances and exchange rates in shaping domestic investment across a panel of sub-Saharan African countries from 1998 to 2022. Given the significance of this research question, panel data analysis and FMOLS regression are employed to assess this impact.

Result of data analysis has shown that Remittance inflows significantly bolster private domestic investment in sub-Saharan Africa when prioritized by policymakers. Conversely, exchange rate depreciation adversely affects remittances, leading to decreased domestic investment. Additionally, remittances unilaterally influence private domestic investment, demonstrating their pivotal role in shaping economic dynamics across the region.

It is recommended that policymakers in sub-Saharan African countries prioritize policies to enhance remittance inflows. This includes reducing transaction costs, improving remittance channels, and boosting financial literacy among recipients. Efforts to stabilize exchange rates are crucial to mitigate depreciation’s adverse effects on remittances and subsequent domestic investment. Central banks should manage foreign exchange reserves and implement suitable monetary policies for stability. Coordination among government agencies, central banks, and stakeholders is essential to formulate and implement supportive policies. Regional collaboration can facilitate sharing best practices to maximize remittance benefits. These strategies can foster economic growth and development in sub-Saharan Africa.

REFERENCES

- Adom, P. K., Amakye, K., Barnor, C. & Quartey, G. (2015). The long-run impact of idiosyncratic and common shocks on industry output in Ghana, OPEC Energy Review 39(1):17-52.

- Allen, C. (2021, February 24). Remittances in Sub-Saharan Africa: An Update. International Monetary Fund African Department. Special Series on COVID-19. Retrieved from https://www.imf.org/ /media/Files/Publications/covid19-special-notes/en-special-series-on-covid-19-remittances-in-sub-saharan-africa-an-update.ashx2853–2862.

- CBN. (2021). Naira 4 Dollar Scheme. Trade and Exchange Department. Retrieved from https://www.cbn.gov.ng/out/2021/ccd/naira4dollar.pdf

- Centre for Financial Regulation & Inclusion. (2018). Exploring barriers to remittances in sub-Saharan Africa series: Remittances in Côte d’Ivoire, Cenfri, 5, 1-18.

- Chinn, M.D. and Ito, H. (2006) What Matters for Financial Development? Capital Controls, Institutions, and Interactions. Journal of Development Economics, 81, 163-192.

http://dx.doi.org/10.1016/j.jdeveco.2005.05.010 - Clark, J. M., (1923). Business acceleration and the law of demand: a technical factor in economic cycles, Journal of Political Economy, 25(1),217-235.

- Dumitrescu, E.-I., & Hurlin, C. (2012). Testing for granger non-causality in heterogeneous panels. Economic Modelling, 29(4), 1450–1460.

- Edeh, C. N., Ijemba, O. N., & Njeze, A. V. (2023). Remittance-Domestic Investment Nexus in Nigeria. International Journal of Economics and Financial Management (IJEFM), 8(2), 92-103. Retrieved from iiardjournals.org

- Edoun, E. I., Ezeanyika, S., & Mbohwa, C. (2015). Foreign remittance and investment in rural non-farm economy: Evidence from Igbo of South East Nigeria. Journal of Business Economic Finance, 3(4), 251-260.

- Englama, A. (2007). The Impact of Remittance on economic development, The Bullion, Central Bank of Nigeria, 34(4), 5-16.

- Ezike, J. E., & Ogboi, C. (2017). Household Inward Remittances and Productive Investment in Nigeria: A Multidimensional Analysis. Advances in Social Sciences Research Journal, 4(16) 62-76.

- Ibrahim, I. (2018). The impact of remittance on domestic investment: the role of financial and institutional development in five countries in Sub-Saharan Africa. Forum of International Development Studies, 2(1), 48-9.

- Ilu, A. I. (2019). Impact of remittances from Nigerians in diaspora on exchange rate stability. Retrieved from https://mpra.ub.uni-muenchen.de/97555/ (MPRA Paper No. 97555).

- Jushi E. (2021). Remittances and Foreign Direct Investment: Evidences from Balkan Countries. Journal of Financial Management, 14(3), 117; EISSN 1911-8074, Published by Multidisciplinary Digital Publishing Institute (MPDI).

- Keho, Y. (2024). Impact of remittances on domestic investment in West African countries: The mediating role of financial development. SN Business & Economics, 4, 20. https://doi.org/10.1007/s43546-023-00621-2

- Koyck, L. M. (1954). Distributed lags and investment analysis. 3rded) North-Holland Publishing Co., Amsterdam. Ministry of Foreign Affairs.

- Kudaisi, B. V., Ojeyinka, T. A., & Osinubi, T. T. (2021). Financial liberalization, remittances and economic growth in Nigeria (1990–2018). Journal of Economic and Administrative Sciences, 38(4), 562-580.

- Levin, A., Lin, C.-F., & Chu, C.-S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1-24.

- Mensah, S. (2018). Effects of remittances and infrastructure on private investment: Evidence from Ghana [Master’s thesis, University of Cape Coast]. Department of Economic Studies, School of Economics, College of Humanities and Legal Studies.Top of Form

- Ofosu-Mensah Ababio, J., Aboagye, A. Q. Q., Barnor, C., & Agyei, S. K. (2022). Foreign and domestic private investment in developing and emerging economies: A review of literature. Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2132646

- Ojapinwa, T. V., & Odekunle, L. A. (2013). Workers’ Remittance and Their Effect on the Level of Investment in Nigeria: An Empirical Analysis. International Journal of Economics and Finance, 5(4), 89-99.

- Okeke, I. C., Chinanuife, E., & Muogbo, K. (2021). International Remittances and Private Domestic Investment inNigeria: A Toda and Yamamoto Causality Approach. International Journal of Humanities Social Sciences and Education (IJHSSE), 8(7), 67-76. https://doi.org/10.20431/2349-0381.0807008

- Phillips, P. C. B. & Hansen, B. E. (1990): Statistical inference in instrumental regression with I (1) Processes. The Review of Economic Studies, 57(1),99-125.

- Priyankar, E. A. C. (2018). The long run effect of services exports on total factor productivity growth in Sri Lanka based on ARDL, FMOLS, CCR and DOLS approaches. International journal of Academic Research, Business and Social Sciences, 8(6),

- Ranjan K. D. (2020) Impact of Remittances on Domestic Investment: A Panel Study of Six South Asian Countries. South Asia Economic Journal, 21(1), 7–30Taiwo, 2007

- Singer, D. A. (2010). Migrant Remittances and Exchange Rate Regimes in the Developing World. The American Political Science Review, 104(2), 307-323.

- Taiwo, S. H. (2007). Remittances inflow: a potential source of economic development for Nigeria, The Bullion, Central Bank of Nigeria 34(4), 17-35

- World Development Indicator, (2021). Personal remittances, received (% of GDP) – Gabon https://data.worldbank.org/indicator/BX.TRF.PWKR.DT.GD.ZS?locations=GA.

- World Bank Development indicators, (2018). The World bank in Mali. https://databank.worldbank.org/reports.aspx?source=2&country=MLI

- World Bank, (2023). The World Bank in Gabon, https://www.worldbank.org/en/country/gabon/overview.

- World Bank (2023). Migration and Development Brief 39: Leveraging Diaspora Finances for Private Capital Mobilization December. World Bank, Washington, DC.

- World Bank, (2024). Remittance Inflows to GDP for Cote d’Ivoire [DDOI11CIA156NWDB], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DDOI11CIA156NWDB, February 3,