The Impact of Working Capital Management on the Profitability of Listed Banks: The Ghanaian Economy Experience

- Edward Domina Attafuah, (Ph.D.)

- 235-252

- Feb 5, 2024

- Economic Development

The Impact of Working Capital Management on the Profitability of Listed Banks: The Ghanaian Economy Experience

Edward Domina Attafuah, (Ph.D.)

Accountant, University Health Service,

University for Development Studies

DOI: https://doi.org/10.51244/IJRSI.2024.1101019

Received: 15 December 2023; Revised: 30 December 2023; Accepted: 03 January 2024; Published: 05 February 2024

ABSTRACT

The study examined the impact of working capital management practices on the profitability of banks listed on the Ghana Stock Exchange from 2012 to 2022. The study had three specific objectives to determine the relationship between cash conversion cycle and profitability; to determine the relationship between acid ratio and profitability of banks, and to determine the relationship between loan to deposit ratio and profitability of banks. The study was quantitative in nature and used secondary data (audited financial records of banks listed on the Ghana Stock Exchange from 2012 to 2022) of five banks. The data were retrieved purposively. Stata (StataCorp, Texas, USA) was used to analyze the data. The linear regression model was used to analyze the data after Pearson correlation was done. The study found a negative significant association between cash conversion cycle and return on capital employed after controlling for bank size, leverage and debt. This was consistent with study’s hypothesis. This implies that effective cash management is key to commercial banks performance. Also, acid ratio was positive and significantly associated with profitability of banks. Again, the profitability of commercial banks is accounted for by loan to deposit ratio. The study concludes that the profitability of banks is significantly associated with working capital management. That is, when working capital is well managed, commercial banks are better able to meet their short-term commitments as and when they fall due. This enables the commercial banks to operate efficiently without any interruptions. It is recommended that finance managers of commercial banks list on the Ghana Stock Exchange pay external attention to the cash position of their banks at all times.

Keywords: Working capital, Cash Conversion Cycle, Acid ratio, Loan to debt ratio, Return on Capital Employed

BACKGROUND OF THE STUDY

Monitoring of short-term capital decisions remains pertinent as well as an imperative constituent of corporate fiscal supervision for the reason that it unswervingly disturbs the earnings and organization’s ability to pay its debt irrespective of the institution’s capacity. The key word Working capital management inherent in this treatise cannot be overemphasized. It can be simply be explicated as the supervision of present resources and present obligations (Devi, 2022). It provides accurate policies for handling short-term assets and obligations (Joshi 2022).

A lot of intellectuals are versed into the comparison of current assets over current liabilities in divers’ means nonetheless an accord is given that managing your current asset over your current liabilities has a substantial influence on earnings, profitability and firm value (Gonçalves, & Robles, 2018). Hence, efficient and effective working capital management is regarded to have numerous advantageous impacts which will also yield to a great rippling effect on the Ghanaian banking sector:

Efficient working capital management will expedite the disbursement of interim assurances happening in organizations (El-Maude & Shuaib, 2016), it will also simplify and concise owner financing as well as diminish working capital as a basis for failure amid minor firms (Agyei, 2020). It guarantees a comprehensive inflow for assurance of durable fiscal development as well as accomplishment of revenue-making progression. It guarantees adequate association among mechanisms of organizations waged for a competent and effective blend that ensures wealth sufficiency (Agyei & Yeboah 2020). Narrowing working capital management practices from other sectors or institutions of the economy to the banking sector in Ghana which this study is centred on, the banking institutions in Ghana also contribute immensely to financial development through the adoption of monetary alternatives to ease the creation in supplementary businesses

(Yeboah, & Yeboah, (2014). However, the banking scheme in Ghana from time to time makes it challenging to sponsor its activities. These sponsoring repercussions correspondingly go a long way to distress the running of the monetary adequacy of the distinct banking institutions that aim to distress their level of profitability Lartey, Antwi, , & Boadi, (2018).

Statement of the Problem

Existent literature on working capital management and profitability appears to be predominant in the context of non-financial institutions (Ahmed & Mwangi, 2022; Abdulnafea, Almasria, & Alawaqleh, 2022; Soda, Hassan Makhlouf, Oroud, & Al Omari, 2022). From this context, although scholars have also approached the consequences of WCM on enterprises’ financial performance in various ways, there seem to be an identified agreement that effective WCM has a significant bearing on profitability (Abdulnafea et al., 2022; Soda et al., 2022; Basyith, Djazuli, & Fauzi, 2021). However, Agyei and Yeboah (2021) argues that, due to the varied running of working capital practices of various operations of enterprises, the implications of it on enterprises’ profitability varies in literature. Consequently, Agegnew (2019) recorded that the WCM negatively contributes to the performance of enterprises. Thus, organizations can improve profitability by minimizing the cash conversion cycle (CCC) while managing it to the desirable levels. In the same vein, Akgun and Karatas (2020) documented a contrary link between gross working capital and enterprises profitability. Contrastingly, Amponsah and Asiamah (2020) provide scholarly evidence that indicates there is a positive nexus between working capital and the profitability of manufacturing enterprises. This suggests that longer CCCs are more profitable to some enterprises. Likewise, No banee (2019) argued a positive link between CCC and enterprise’s performance. However, these exemplified studies that have been cited focused on the non-financial sector, which Agyei and Yeboah (2021) contends that though managing the 14 finances of banks and non-financial institutions are identical, significant differences are prevalent in the financial regulation and practices of banks. In the Ghanaian context, although there has been the proliferation of such studies on non-financial institutions, with various findings, there is also a fair share of studies investigating the WCM and financial performance of banks in Ghana. Yet, these studies have conflicting results. For instance, Nkrumah (2018), using 5 commercial banks, found that there is a negative consequence of WCM on the profitability of universal banks in Ghana while using the simple ordinary least squares (OLS) estimator. On the other hand, without applying the Hausman test, Yeboah and Yeboah (2014) found an insignificant nexus between WCM and commercial banks’ profitability when using a simple OLS; whereas a negative effect was revealed when the authors used a fixed effect estimator from a sample of 9 commercial banks. Nonetheless, Owusu (2019), using a sample of 6 commercial banks, found an insignificant bearing of WCM on the financial performance of the banks while also using a simple OLS estimator. Consequently, these disparities in the results from the commercial banks could be attributed to the few commercial banks used for the study, especially that there have been over 10 commercial banks operating in Ghana for over two decades. Consequently, despite the conduct of these studies (Owusu, 2019; Nkrumah, 2018; Yeboah & Yeboah, 2014), the link between WCM and profitability in the commercial banking sector in relation to whether such relationship differ among Ghanaian and foreign commercial banks has not been explored in Ghana. Although other empirical works (such as Agyei & Yeboah 2021; Afrifa & Padachi, 2014; Deari, Kukeli, Misu, & Virlanuta, 2022) assessed the nexus between WCM and enterprises’ profitability, Afriyie and Aidoo (2022) draws attention to firm-based and fundamental characteristics which distinguishes the operations of foreign from local commercial banks. Thus, this study contributes by further exploring this research area which comprises foreign and local commercial banks in Ghana. Insights from this empirical enquiry will enable commercial banks endeavor to achieve the optimum working capital conditions needed to spur profitability.

LITERATURE REVIEW

Conceptual Definition of Variables

Definition of Working Capital

As given by Firer, Jordan, Ross, and Field (2018) explain “Working capital as a company’s ability to meet its short-term capital decision over its current liability”. Von and John (2020) claim that it is the quantity of short-term resources that cannot be met by short-term creditors” Soni, and Trivedi (2016) provide a concise explanation for working capital. As given away by him, “working capital basically discusses the variation with short term capital decision”. The meaning of working capital given by Soni and Trivedi (2016) was in line with the explanation given by (Atrill 2019). He explains working capital as the excess of current assets over current liabilities. Arnold (2018) provides a comprehensive description of working capital. As given away by him, “working capital comprises current assets as well as the arithmetical accuracy of short-term obligation such as various creditors as denoted by unsettled workshop expenditures”.

Fareed (2019) also hastened to give a detailed explanation of working capital management as the difference between current assets and current liabilities. Orbunde, Arumona and Adeyeye (2021) pooled a comparable view on the description of working capital. As given by Orbunde, Arumona and Adeyeye (2021), “working capital talk about time lag with the expenses made in the acquisitions of raw materials and assembly made from the proceed of finished goods.

Concept of Working Capital

Short term capital decision satisfies a business initiative’s immediate financial needs (Gitman, 2015). Working capital is used as a standard for managing everyday financial operations as a result. It is a consequence of the lag time between the cost of acquiring the inflow from turnovers or provided services (Gitman, 2015). Most financial firms’ liquidity and profitability issues are solved by their working capital needs. This work has a significant impact on the finance and investment choices of most banking industries.

Managing Working Capital

As given away by Appuhami (2018), short-term capital decision comprises the administration of up-to-date resources over short-term obligations. Frimpong (2018) provided his own opinion on what short term capital decision signifies. He said that, short term capital decision involves the financing, investing, and administration of a company’s net current assets in accordance with its policy directives. It emphasis on decision making on the development of companies’ existing assets and the management of these assets. “A key purpose of the administration of short term capital decision is the preservation of a prime stability within short term capital decision periphery. Krueger and Filbeck (2018) suggests “the accomplishment of firms is centered on commercial directors’ capacity to be able to evaluate present resources as well as present obligations”. Pass and Pike (2020) pointed out two objectives of short term capital decision. As given away by them, the objectives comprise of improving the lucrativeness of a firm and safeguarding sufficient financial resources to pay short-term obligations.

Cash Conversion Cycle

As given away by Watson and Head (2020), “suggest that the prerequisite quantity of short term capital decision is reliant on the budget deals as well as cash cycle of most financial institutions, nonetheless, there is a likelihood of an adjustment amid the projected as well as actual. Numerous empirical investigations imply a negative relationship between the inflows of the cash conversion cycle of organizations as well as its effectiveness. This corroborates studies shepherded by Sarbapriya (2022) and (Orbunde, et al 2021).

Profitability

Profitability, often interchangeable with performance, refers to organizations’ ability to utilize investment and operational decisions to sustain the organization and attain success and stability in finances (Amponsah & Asiamah, 2020). In a practical manner, Pendey (2020) describes financial performance as the degree at which a firm performs over a stipulated period of time which is quantified in terms of profits or losses. An organization’s financial performance encompasses various performance indicators. In effect, accounting and finance literature gathers various performance indicators in assessing organizations’ profitability which includes profitability, debt, and liquidity indicators (Mabandla, 2018). There is a general consensus in the academic literature and profession that the sole purpose for most firms operating is maximizing their profit. Thus, profitability indicators are usually considered as performance indicators relative to the other indicators. According to Nyabuti and Alala (2014), the financial performance indicators of a firm provide general metrics for the overall financial health of a company over a span of time which is referenced against industry standards, similar companies or from reference point in time. Generally, firms are to lay down their business objectives and goals in order to assess chalked progress and success using relevant and crucial financial performance indicators. Essentially, profitability ratios assess enterprises’ financial success, reflecting the capacity of management to use the assets of the firm to generate sales and profit. Shareholders, creditors and managers find profitability ratios among the useful indicators to assess the performance of a firm (Parrino et al., 2012).

The profitability of a firm is based on the movements in income and expenses. Firms that do not constantly make positive net income face the challenge of performance and lack credit worthiness. Therefore, to ensure a firm’s survival, management has the onerous task to be driven by reaping profits for the shareholders. Although the various ratios present constructive evidence of the operational results of a firm, the profitability ratios provide a metric that reflects the latent effects of operational outcomes (Agha & Mphil, 2014). For the purposes of this empirical investigation, the ROA and ROE are utilised due to their vast use in literature and suitability for this research.

Return on Assets (ROA)

Return on assets is the proportion of net profit before tax to the total assets of a firm (Amponsah & Asiamah, 2020; Agegenew, 2019). It is the ratio that measures the link between profit and the total assets employed by the firm. It represents how well the total assets of the firm have been used to generate profit. ROA exhibits as a crucial metric for the assessment of enterprises’ performance in the body of knowledge, it shows the performance metric of a firm as gained per unit of total assets. The ratio is provided by:

𝑅𝑂𝐴 = 𝑁𝑒𝑡 𝑃𝑟𝑜𝑓𝑖𝑡 𝑏𝑒𝑓𝑜𝑟𝑒 𝑇𝑎𝑥/𝑇𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠

Relatively, a higher ROA metric indicates the efficiency and productivity of management in managing its balance sheet to make profit whereas a lower metric demonstrates to management that there is the need for improvement in affairs. Thus, higher metrics provide the indication that the firm is able to earn more from a small sum of investment. Further, it reflects on management’s capacity to convert the finances invested into net income.

Return on Equity

Return on equity (ROE), as a metric, measures the equity invested in the firm. The ROE provides a metric of the degree to which the profit of an enterprise is generated from the finances provided specifically by shareholders (Dietrich & Wanzenried, 2021). This ratio provides a reference for shareholders to compare the returns that could have been gotten from investing elsewhere in determining the fair value of their return. Investors are eligible to receive the excesses of the net income of a firm (Ajao & Small, 2012). The ROE is given by;

𝑅𝑂𝐸 = 𝑃𝑟𝑜𝑓𝑖𝑡 𝑎𝑓𝑡𝑒𝑟 𝑡𝑎𝑥 /𝑆ℎ𝑎𝑟𝑒ℎ𝑜𝑙𝑑𝑒𝑟𝑠’ 𝑒𝑞𝑢𝑖𝑡𝑦

The ROE is considered a two-way part ratio by linking the income statement and balance sheet of the firm; thus, net income compared to shareholders’ equity. Relating the ROE to industry benchmark shows the competitive advantage of the firm in the industry. The ratio demonstrates the effectiveness of management in growing the firm sustainably through equity financing. The higher the ROE metric, the better it provides insight on how well a firm increases shareholder value as it operates efficiently and prudently reinvesting its earnings to boost productivity and profits.

Theoretical Literature

Here are numerous models and concepts that describe how current over current liability can be conducted proficiently so as to profit the mostly the banking industry as a whole. Some of these models or theories consist of:

- Liquidity Preference Theory

- Operating Cycle Theory

- Working Capital and Profitability Theory

Liquidity Preference Theory

This model or concept explains the basis behind a company’s having resources that can effortlessly be transformed into cash. These motives can be ascribed to the three reasons for the request of its ability to pay its debt. These reasons include transitionary, speculative and precautionary. Cash relating to theory is viewed as cash flows. If the request for inflows by organization is mostly recurrent, it maintain its resources to be smoothly changed into cash. This will permit most banking institutions to make up its regular demand for liquidity in the running of its commercials. This will enhance the banking institution to make up its short-term obligations.

Operating Cycle Theory

The concept positions that the more suitable approach to see the cash flow movement of the banking institution is the involvement of short-term capital constituents. Debtor income involves the periods taken for financial institutions to transform their receivables into cash. In circumstances where a banking institution gives its clients longer credit duration for compensation the less liquid its trade receivables. Furtherance to this, in a condition where the banking institution gives its clients longer credit terms for settlement more easily convertible trade receivables. As given by Weston (2021), recommends that when financial institutions have an extreme current ratio, it implies that the institution has ineffective current assets for instance inventory, and hence do not produce revenue. Operational periods for organizations are fundamentally grounded on receivables and inventory income.

Working Capital and Profitability Theory

Business ventures in the short term have an impact on the company’s performance. Financial administration norm demands a significant investment in short-term capital decision components that will result in growth in the organization’s earnings as in the case of liquidity as well as viability. In contrast, when working capital investment is low, the firm’s performance suffers. Previous studies showed that the profitability of a firm should be absolutely correlated negatively with low levels of short-term capital correlated at greater echelons (Ponsian, Chrispina, Tago, & Mkiibi, 2014).

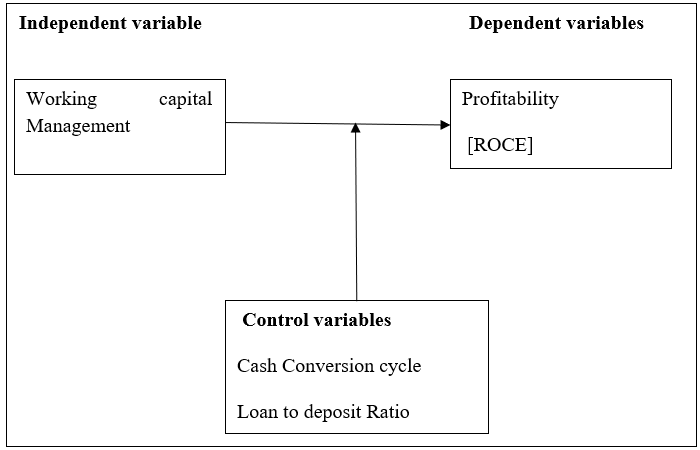

Conceptual Framework

The important elements: constructs or variables of a social research and the presumptive relationships among them are explained in a conceptual framework, either graphically or narratively (Tamene 2016).

Frameworks can be simple or complex, theory-driven or simply a description of an event or its causes. A conceptual framework outlines what and who will be investigated or not. A conceptual framework, according to Ravitich and Riggan (2022), is a defense of the relevance and necessity of the research methods being proposed as well as the issue being studied. Another analytical tool that reflects multiple viewpoints on problems in specific circumstances is a conceptual framework. One may need a conceptual framework to describe how the concepts relate to one another in order to distinguish between concerns relating to ideas and how to organize them. Effective conceptual framework frequently depicts actual situations and presents them in a way that makes them simple to recall and put into practice (Ravitch and Riggan 2022). The goals of a research study may be tied to abstract representations called conceptual frameworks that guide data revisions and analysis. According to Shields and Rangarajan (2014), conceptual framework is the method used to organize ideas in order to accomplish a research project’s aim. Therefore, a conceptual framework helps the researcher stay on task and avoid being side-tracked.

Presentation of the conceptual framework in diagrams

The conceptual framework for the investigation is shown in Figure 2.1 and described. Framework showing working capital management techniques’ effects on the Ghanaian banking sector.

METHODOLOGY

Research Design

The exploratory design was used for this investigation. It aims to determine whether working capital management strategies have any effects on how well Ghana’s banking industry performs. In order to achieve this, the study creates a multiple regression model and conducts the analysis using Stata. To determine whether the data is reliable, Variance Inflation Factor and Pearson Correlation Analysis are utilized.

Data

This study uses secondary data to acquire the necessary information. The important details required for the investigation was gathered using the chosen banks’ financial statements. The following banks’ financial statements were used to gather the pertinent data: Prudential Bank, GCB Bank, Access Bank, Guaranty Trust Bank, and Zenith Bank. The study used data mostly for secondary purposes. This was because the public financial accounts of the selected institutions had all the relevant and required data. Therefore, there was no need to gather original data. The researcher did not conduct interviews with the stakeholders of the selected institutions or issue questionnaires to them in order to collect information. The data gathered from the financial accounts of the selected organizations was examined using the analytical tool STATA Statistical Software version 16.0. Regression analysis was used by the researcher, to determine how closely the dependent and independent variables were correlated.

Methods

The financial statements of five banks were used as the primary source of the basic data for this study, which covered the ten-year period from 2012 to 2021. This information came from the Bank of Ghana. The World Bank Data on Ghana were used to obtain information on the loan loss ratio and exchange rate.

Descriptive Statistics

The collected ratios were used to construct the descriptive statistics for the study’s findings, which included information on the number of observations, mean, standard deviation, minimum and maximum values. The Mean for the study’s descriptive statistics is represented by the following formula: Mean= (𝑥) The descriptive statistics for the study’s standard deviation are represented by the following formula: SD= √(𝑥−𝑥𝑖) 𝑛

Model Specification

Raheman and Nasr’s (2007) recommended regression model in the study as follows: 𝑅𝑂𝐶𝐸𝑖𝑡 = 𝛽0 + 𝛴𝑖=1𝑛 𝛽1 𝑋𝑖𝑡 + ε ………… (1)

𝑅𝑂𝐶𝐸𝑖𝑡 = Return on Capital Employed by Bank (i) at time (t); i = 1, 2… n

𝛽0= the intercept of equation

𝛽1= coefficient of 𝑋𝑖𝑡 variables

𝑋𝑖𝑡= the different independent variables for working capital management of firm i at time t

T = number of years from 1, 2 …. N

ε= error term

The study intended to establish a relationship between the elements of working capital management and profitability using some liquidity and other pertinent ratios because liquidity is a key factor in determining how effective a firm’s working capital management procedures are. The following ratios were employed by the researcher to represent the independent variables:

- Acid Ratio (AR): This ratio is used to measure a company’s ability to meet its financial obligations as they fall due.

AR= Current Assets – Inventory Current Liabilities

- Loan to Deposit Ratio (LDR): This ratio measures the proportion of customer deposits given out as loans to customers.

LDR = Total Loans

Total Deposit

- Cash Conversion Cycle (CCC): This ratio measures the “period of time between Debtors Collection Period and Creditors Payment Period”.

CCC = Debtors collection period – Creditors payment period

The dependent variable which was the profitability of the banks was represented by the Return on Capital Employed (ROCE). Return on Capital Employed (ROCE) measures the overall profitability made from the total capital employed by the bank.

ROCE= Profit before Interest and Tax

Capital Employed

The model above, according to Nuamah-Owusu (2015), could be transformed into the model below to represent our given variables:

𝑅𝑂𝐶𝐸𝑖𝑡=𝛽0+𝛽1𝐴𝑅+𝛽2𝐿𝐷𝑅+𝛽3𝐶𝐶𝐶+ε…… (2)

𝑅𝑂𝐶𝐸𝑖𝑡 = Return on Capital Employed by Bank (i) at time (t); i = 1, 2… n

𝛽0= Intercept of Equation

𝛽1= Coefficient of Acid Ratio (AR)

𝛽2= Coefficient of Loan to Deposit ratio (LDR)

𝛽3= Coefficient of Cash Conversion Cycle (CCC)

ε= Error term

Diagnostic Testing

A few model diagnostic tests were run to see whether any of the panel regression model’s assumptions were broken before arriving at the best empirical model for testing the hypotheses. The multi collinearity test and the correlation test were two of the assessments made. The descriptions of the various model diagnostic tests undertaken are provided below.

Correlation Test

The Pearson correlation matrix was used in the study to demonstrate the presence of multi collinearity among the independent variables. A test for normality was carried out to check that the data had a normal distribution and to lessen the impact of outliers. The Skewness and Kurtosis test was used in this investigation to determine the data’s normalcy. As a general rule, normal data are thought to have values for skewness and kurtosis close to 0. Therefore, the data cannot be claimed to be normally distributed if the values are not close to zero. According to Field (2009), for instance, if skewness (asymmetry) and kurtosis are to be used to determine the normalcy of data, they should both be zero or very close to zero. He contends that after the data is not normally distributed once the values for skewness and kurtosis are larger than 1.96 and 3.29, respectively.

Multi collinearity Test

When the correlation between the two variables is more than 0.7, it is considered that there is a multi-collinearity issue. Ho and Wong (2002). To determine whether the independent variables have a multi collinearity issue, the variables’ Variance Inflation Factor (VIF) was employed. VIF refers to the degree to which one independent variable inside the model explains another independent variable. According to Field (2009), multicollinearity is generally caused by independent variables with correlation coefficients more than 0.7 or VIFs greater than 10.

Table 3.1. Variable Description and Measurements

| Variables | Measurement/ Description | Notation |

| Acid Ratio | This variable is use to measure a company’s ability to meet its financial obligation as they fall due, | AR |

| Loan to Deposit Ratio | This ratio measures the proportion of customer deposit given out as loans to customers | LDR |

| Cash Conversion Cycle | This ratio measures the period of time between debtors’ collection period and creditors payment period | CCC |

| Return on Capital Employed | This ratio measures the overall profitability made from the capital employed by the bank. | ROCE |

RESULTS

Introduction

This chapter presents the findings from the data extracted from the audited financial records of the selected banks. The findings are discussed and inferences are made in relation to empirical literature. The chapter is presented in three main sections as descriptive statistics, correlation and multicollinearity test (variance inflation factor) and logistic regression analysis.

Descriptive Statistics

Details of the summary of descriptions of the independent variables’ descriptive statistics (currency conversion cycle [CCC], acid ratio and loan to deposit ratio [LDR]) and dependent variable (return on capital employed [ROCE]) are presented in Table 4.1. The mean score of 0.747 and standard deviation of 0.517 for ROCE is an indication that the selected banks made positive returns on their capital. This corroborates that the selected banks were able to improve their working capital, which is the strongest indicator of the selected banks reducing their cash conversion cycle to increase profit margins (Narasimhan & Murty, 2021). The positive ROCE implies that the banks reduction in stock turnover and debtors’ collection is functioning efficiently and their operations and debt reduction deployment have improved, hence, investors of the selected can continuously invest with the selected banks.

Acid ratio sought to measure to a banks’ ability to meet its financial obligations as they fall due. The mean score of 1.859 and standard deviation of 1.927 proves that the selected banks are liquid enough to meet its financial obligations, especially in situations where the macroeconomic stability is questionable. This suggests that the selected banks is capable of meeting its own obligations when they become due, repay deposits and make payments based on the orders of customers (Lartey et al. 2013).

The mean score of 4.061 and standard deviation of 1.933 for loan to deposit ratio (LDR) suggests that the profitability of the selected banks could dwindle because of the high proportion of customer deposit given out as loans to customers. The positive mean score is an indication that the selected banks are alert and have the ability to keep a good balance between customers’ deposits and loans given out to customers (Saeed, 2014).

The mean cash conversion cycle [CCC] is 2.76 days with 1.82 days of standard deviation. This suggests that when the CCC is shorter, it makes the collection of receivables quicker and payment to suppliers are delayed hence improve the effectiveness of the selected banks in the use of working capital which is linked to profitability. This corroborates the fact that the selected banks can increase their profit margins by reducing the number of days accounts receivables as well as inventories, thus, a shorter CCC is related to better financial performance (Wang, 2012).

The bank size of the selected banks is 8.704 and standard deviation of 1.845. Large banks have large customers, hence, has large borrowers economies of scale and diversification. This resonates with Anbar and Alper (2011) who found that bank size have significant positive effects on financial performance of banks. Similarly, the finding is in agreement with a study by Masood and Ashraf (2012) who argued that large bank size increase, its effectiveness increases. Another school of thought suggests that bank size leads to high marketing and asymmetric information which increases financial performance of banks (Tan, 2016). By inference, large bank size improves surveillance, confidence, prevents conflicts in order to increase financial performance.

Furthermore, the mean score of 0.45 and standard deviation of 0.317 for debt is an indication that the selected banks had high financial leverage because of the low percentage of their non-performing loans. This pattern, on one hand, is favorable since reduced debt increases the image of the banks, thus, increasing trust among stakeholders, and thereby increasing the financial viability of banks (Ajorsu, Hongli & Musah, 2020). On another hand, financial difficulties have been a major problem impeding the company’s profitability in developing nations like Ghana. As a result, depending on the operations of the company, the decision regarding debt capital can either increase the bank’s profit margin or have a negative impact on profitability due to the nonpayment of borrowed money.. By inference, higher equity capital declines the level of financial leverage and risk which adversely affect the general profitability of the selected banks.

Leverage recorded a mean score of 6.914 and standard deviation of 1.73. This is an indication that the high leverage score has positive impact on the profitability of the selected banks because it reduces the funding cost, increases the selected banks creditworthiness and lowers the need for external funding, thereby increasing depositors’ funds (Paolucci, 2016; Tan, 2017; Sufin &Kamrudin, 2012). This implies that the selected banks are highly leveraged and employ about 91.4% debt to finance the bank’s total assets.

Table 4.1: Summary of Descriptive Statistics

| Variable | Obs | Mean | Std. Dev. | Min | Max |

| ROCE | 50 | .747 | .517 | .01 | 1.613 |

| Bank Size | 50 | 8.704 | 1.845 | 3.552 | 10.189 |

| Debt | 50 | .45 | .317 | .028 | .999 |

| Leverage | 50 | 6.914 | 1.73 | 3.472 | 11.947 |

| Acid Ratio | 50 | 1.859 | 1.927 | .073 | 7.685 |

| LDR | 50 | 4.061 | 1.933 | 1.033 | 9.984 |

| CCC | 50 | 2.769 | 1.82 | .081 | 8.542 |

ROCE: Return on capital employed; LDR: Loan to deposit ratio; CCC: Cash conversion cycle

Normality Tests

The correlation analysis showing the association among the dependent variable independent factors (acid ratio, loan to deposit ratio, and cash conversion cycle) and the dependent variable (return on capital employed). is presented in Table 4.2.

A correlation was conducted at 95% confidence interval in order to describe the association between the dependent and independent variables. One can determine whether or not there is multi collinearity based on the magnitude. Wooldridge (2020) asserts that multi collinearity should be taken into account when explanatory variables have correlations greater than 0.8. A variable is considered to be close to perfect or highly linked if its coefficient is equal to or higher than 0.8. None of the independent variables have a strong link with one another, according to the correlation matrix. As a result, the model contained all of the independent variables.

Pairwise correlations

| Variables | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

| (1) ROCE | 1.0 | ||||||

| (2) Bank Size | -0.548** | 1.0 | |||||

| (3) Debt | -0.300** | -0.047 | 1.0 | ||||

| (4) leverage | 0.106 | 0.320** | -0.176 | 1.0 | |||

| (5) Acid Ratio | 0.238* | 0.158 | -0.712** | 0.132 | 1.0 | ||

| (6) LDR | -0.086 | -0.052 | 0.470** | -0.067 | -0.278 | 1.0 | |

| (7) CCC | 0.025 | -0.084 | 0.325** | 0.003 | -0.226 | 0.736** | 1.0 |

| ROCE: Return on capital employed; LDR: Loan to deposit ratio; CCC: Cash conversion cycle

** p>0.05 *p>0.01 |

|||||||

Variance Inflation Factor

Table 4.3 presents the measurement of the study’s construct using collinearity. A collinearity diagnostic was conducted in order to reduce multicollinearity and describe the association between the variables. From the collinearity diagnostic matrix, none of the variables was highly correlated with another. The mean VIF of 1.957 obtained for this study shows that there is no problem of multicollinearity. The implication of the VIF results is that the variables are independent of each other and can be included in the model.

Table 4.3: Variance inflation factor

| VIF | 1/VIF | |

| Loan to Deposit Ratio | 2.547 | .393 |

| Debt | 2.514 | .398 |

| Cash Conversion Cycle | 2.227 | .449 |

| Acid Ratio | 2.126 | .47 |

| Bank Size | 1.166 | .858 |

| Leverage | 1.162 | .86 |

| Mean VIF | 1.957 | . |

Relationship between Cash Conversion Cycle and Profitability of Banks

There was a negative significant association between cash conversion cycle and return on capital employed [ROCE] (β=-0.179, p<0.001), holding all other variables constant. The model predicts that for everyone unit increase in cash conversion cycle, there is about 0.179 decrease in profitability of the selected banks. The regression coefficient (β) value of -0.179 indicates that about 18% of the variance between cash conversion cycle and profitability is a function of other factors other than the choice between cash conversion cycle and ROCE only. Thus, the null hypothesis is rejected in favor of the alternate hypothesis that there is a relationship between cash conversion cycle and ROCE.

Table 4.4 Linear Regression between CCC and ROCE

| ROCE | Coef. | St.Err. | t-value | p-value | [95% Conf | Interval] | Sig | |||

| CCC | -.179 | .025 | -7.26 | 0.001 | -.229 | -.129 | *** | |||

| Bank Size | .02 | .028 | 0.73 | .469 | -.035 | .076 | ||||

| Debt | -.503 | .181 | -2.78 | .008 | -.867 | -.139 | *** | |||

| Leverage | .077 | .03 | 2.59 | .013 | .017 | .136 | ** | |||

| Constant | 1.946 | .334 | 5.82 | 0.001 | 1.273 | 2.619 | *** | |||

| Mean dependent var | 0.747 | SD dependent var | 0.517 | |||||||

| R-squared | 0.471 | Number of obs | 50 | |||||||

| F-test | 14.997 | Prob > F | 0.000 | |||||||

| *** p<.01, ** p<.05, * p<.1 | ||||||||||

Relationship between Acid Ratio and Profitability of Banks

The regression model measured with acid ratio (independent variable), debt, leverage and bank size (control variables) against the constant (ROCE) was significant statistically (Adj. R square=0.471). The correlation of the determination value of 0.471 meant 47.1% of the total variability between acid ratio and ROCE was affected by debt, leverage and bank size. The F-statistics show the overall model is significant at 5%. Thus, the null hypothesis is rejected in favor of the alternate hypothesis that there is a relationship between acid ratio and ROCE.

Table 4.5: Linear Regression between Acid Ratio and ROCE

| ROCE | Coef. | St.Err. | t-value | p-value | [95% Conf | Interval] | Sig | |||

| Acid Ratio | .081 | .031 | 2.61 | .012 | .019 | .143 | ** | |||

| Bank Size | -.189 | .024 | -7.98 | 0.001 | -.237 | -.141 | *** | |||

| Debt | -.211 | .302 | -0.70 | .488 | -.818 | .396 | ||||

| Leverage | .058 | .048 | 1.21 | .233 | -.039 | .156 | ||||

| Constant | 1.821 | .378 | 4.82 | 0.001 | 1.06 | 2.582 | *** | |||

| Mean dependent var | 0.747 | SD dependent var | 0.517 | |||||||

| R-squared | 0.489 | Number of obs | 50 | |||||||

| F-test | 16.767 | Prob > F | 0.000 | |||||||

| *** p<.01, ** p<.05, * p<.1 | ||||||||||

Relationship between Bank Profitability and Loan to Deposit Ratio

According to the model’s R-squared of 0.468, the loan to deposit ratio and the model’s control variables (bank size, leverage, and debt) account for 47% of changes in ROCE. The F-statistics’ main purpose was to evaluate how well the regression model fit the data. The model fits well, as shown by the F-statistic value of 14.869 at a 5% significance level (prob>F=0.000). This means that the F-statistics was used to determine if the regression equation considerably increased the amount of the effect on the loan to deposit ratio that influenced financial performance as assessed by ROCE that was not due to chance. Consequently, the null hypothesis is disproved in Table 4.6: Linear Regression between Loan to Deposit Ratio and ROCE

| ROCE | Coef. | St.Err. | t-value | p-value | [95% Conf | Interval] | Sig | |||

| LDR | .078 | .03 | 2.61 | .012 | .018 | .139 | ** | |||

| BankSize | -.18 | .024 | -7.39 | 0.001 | -.23 | -.131 | *** | |||

| Debt | -.495 | .196 | -2.53 | .015 | -.89 | -.101 | ** | |||

| Leverage | .011 | .028 | 0.39 | .701 | -.046 | .068 | ||||

| Constant | 1.956 | .338 | 5.79 | 0.001 | 1.276 | 2.636 | *** | |||

| Mean dependent var | 0.747 | SD dependent var | 0.517 | |||||||

| R-squared | 0.468 | Number of obs | 50 | |||||||

| F-test | 14.869 | Prob > F | 0.000 | |||||||

| *** p<.01, ** p<.05, * p<.1 | ||||||||||

DISCUSSION OF THE FINDINGS

The study assessed the impact of working capital management practices on the profitability banks in Ghana:

Relationship between Cash Conversion Cycle and Profitability of Banks

According to a number of empirical research, there is a negative association between a company’s cash conversion cycle and performance level (Sarbapriya 2022; Orbunde, Arumona & Adeyeye 2021). This is consistent with study findings that showed a negative, statistically significant relationship between the cash conversion cycle, in contrast to Watson and Head’s (2020) findings, which showed a positive relationship between working capital investments and the cash conversion cycle. Thus, the Cash Conversion Cycle establishes the connection between the firm’s cash intake and the peripherals of working capital. Although there is some evidence to the contrary, the finding shows that the quantity of working capital required is influenced by the firm’s cash cycle and sales budget.

Additionally, The result is in line with a study by Meryem (2021) who discovered a negative correlation between business profitability and the various working capital components. The results of this study also line up with those of a study that determined working capital management effectiveness and gross operating profitability for Finnish and Swedish public companies using cash conversion cycle as a determinant, and which came to the conclusion that there was a negative correlation between lengthy cash conversion cycles and a firm’s profitability (Erik 2012). The results suggest that shorter cash conversion cycles result in higher profitability. Therefore, in order to boost profitability, it is crucial for financial organizations to shorten their cash conversion cycle by lowering the number of days of receivables.

Furthermore, the finding suggests that cash conversion cycle directly affects the liquidity and the profitability of any financial institution. This is confirmed by Genesan (2017) who argued that the optimization of the working capital (WC) requirements reduces the demand for the working capital and also generate maximum revenue from it via the efficient management of CCC. Furthermore while managing the working capital efficiently the firm growth increases and also generates good revenue for the stakeholders. The firm who works at the optimal level can manage its cash flow efficiently and the firm’s value also increases (Afza & Nazir, 2017).

The importance of working capital management cannot be overlooked because it directly affects the firms risk and profitability (Appuhami; Rehman & Nasir; Deloof; Christopher & Kamalavalli; Dash & Ravipati, 2019). The importance of working capital management stem from the fact that paying the short terms debts is compulsory to receive cash from the customers within time. Therefore, financial companies should avoid too much investment in their current assets because if their investment is shorter the firms may be unable to meets its short terms debts and obligations, on the other hand efficient management of the working capital involves the planning to control the current assets and the current liabilities to minimize the risk for the firms (Eljely, 2019).

Managers must be involved in working capital choices to address the issue of day-to-day operations (Rehman & Nasir, 2017). The fundamental idea is that current assets are investments with limited lifespans that are continuously transformed into other asset classes. Profitability may rise or fall with a longer cash conversion cycle. Longer cash conversion cycles will result in high profitability, which will enhance sales. When the costs of investing in working capital outweigh the benefits of doing so, profitability may suffer. (Stewart 2015).

Relationship between Acid Ratio and Profitability of Banks

Findings from the present study showed a positive relationship between acid ratio and profitability. This is in line with a study by Ajanthan (2013) who found significant relationship between quick ratio and profitability in commercial companies listed at the stock market in Sri Lanka. Also, the findings from this study agrees with that of Zygmunt (2013) who argued the important role of quick ratios in the company’s performance, have pointed to the existence of a significant effect of the liquidity ratios on profitability in the Polish companies listed in information technology. However, a weak significant relationship was found between current ratio, quick ratio, cash ratio, loan to debt ratio and gross profit margin, and those ratios together impact significantly on the growth of profit of industrial companies in sector food and drink (Khaldun, 2014).

Relationship between Loan to Deposit Ratio and Profitability of Banks

There is a link between commercial banks’ profitability and their lending-to-deposit ratio. This suggests that a conservative working capital policy has greater current assets to current liability. This is to ensure moderate liquidity risk through lower financing cost which also leads to moderate profitability Rahman, Afza, Qayyum, & Bodla, 2020; Afza & Nazir, 2017). By concentrating on a few key areas for cost reduction to increase working capital efficiency, Narasimhan and Murty (2021) emphasized the need for many sectors to enhance their return on capital employed (ROCE). Most academics agree that decreasing the cash conversion cycle increases business profitability, and that effective working capital management has a direct impact on firm profitability. In other words, while decreasing stock turnover and the time it takes for debts to be collected enhances firm profitability, decreasing the time it takes for creditors to pay is seen to hurt businesses’ performance.

In a related study, Wang (2012) stressed that decreasing the number of days that accounts receivable are past due and decreasing inventories can both boost profitability. Therefore, improved performance of the firms is associated with shorter Cash Conversion Cycles (CCC) and net trade cycles. Furthermore, it’s crucial to manage working capital effectively if you want to increase shareholder value. For companies listed on the Athens Stock Exchange, Lazaridis and Tryfonidis (2016) looked into the connection between corporate profitability and working capital management. According to their findings, there is a statistically significant correlation between the Cash Conversion Cycle and profitability as evaluated by gross operating profit. Additionally, managers can make money by managing the various working capital components to the best of their abilities. Similar findings with relatively few differences are displayed in’.

Short term decision and profitability had a negative relationship. Sharma and Kumar (2021), on the other hand, give data that dramatically diverge from the results of numerous international research carried out in various markets and show that working capital management and profitability are positively connected in Indian enterprises. The study also shows that the quantity of inventory and the quantity of accounts payable are adversely connected with a company’s profitability, while the quantity of accounts receivable and the cash conversion time show a positive correlation with corporate profitability. Furthermore, research by Shah and Sana (2016), Howorth and Westhead (2013), Padachi (2016), Garcia-Teruel and Martinez-Solano (2017), and others shows that the value of sound working capital management strategies cuts across industries and business sizes. Other researchers, like Al-Haschimi (2017) and Gelos (2016), conducted a study that also calculated bank interest while there was a lot of focus on working capital management techniques. In 10 SSA nations, Al-Haschimi (2017) investigates the factors affecting bank net interest rate margins. He discovers that operating inefficiencies and credit risk, which indicate market dominance, account for the majority of regional variation in net interest margins. In the study, the impact of macroeconomic risk on net interest margins is rather small. Gelos (2016) uses bank and nation data to examine the factors that affect bank interest margins in Latin America.

In contrast, Vijayakumar (2021) found a positive correlation between the length of the accounts payable period and profitability in a subset of Indian automakers.

SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATIONS

Introduction

A summary of the research results from the chapter is provided analysis. It also presents the conclusions based on the objectives and recommendations informed by conclusions and objectives.

Summary of Findings

The findings are summarized based on the objectives of the study as follows.

Relationship between Cash Conversion Cycle and Profitability of Banks

There was a negative significant association between the cash conversion cycle and return on capital employed after controlling for bank size, leverage and debt. This was consistent with the study’s hypothesis. This implies that effective cash management is key to commercial banks’ performance.

Relationship between Acid Ratio and Profitability of Banks

After controlling for bank size, leverage and debt, the acid ratio was positive and significantly associated with the profitability of banks which is in line with the study’s hypothesis. Thus, commercial banks’ ability to manage liquidity through the issuance of short investments leads to profitability.

Relationship between Loan to Deposit Ratio and Profitability of Banks

The profitability of commercial banks are accounted for loan to deposit ratio and the control variables (bank size, leverage, and debt).This suggests that the profitability of commercial banks are linked with their ability to manage their loans. Thus, the study’s hypothesis is consistent with the findings.

Conclusion

The project work looked at how working capital management techniques affected bank profitability from 2012 to 2022 when they were listed on the Ghana Stock Exchange. Determine the relationship between the cash conversion cycle and profitability, the acid ratio and bank profitability, and the relationship between the loan to deposit ratio and profitability were the three particular goals of the study.

Profitability of banks. The study was quantitative in nature and used secondary data (audited financial records of banks listed on the Ghana Stock Exchange from 2012 to 2022) of five banks. The data were retrieved purposively. Stata (StataCorp, Texas, USA) was used to analyze the data. The linear regression model was used to analyze the data after Pearson correlation was done. Based on the findings, it is concluded that the profitability of banks is significantly associated with working capital management.

Recommendations

Based on the conclusion of the study, the following are recommended.

It is recommended that finance managers of commercial banks list on the Ghana Stock Exchange pay external attention to the cash position of their banks at all times. This is important because establishing and/or ensuring a stable cash position is central to meeting the current liabilities of commercial banks in Ghana.

Additionally, the implementation of an efficient cash management program is imperative to the profitability of commercial banks in Ghana. That is, it is imperative for finance managers of commercial banks to prepare cash budget and cash in order to efficiently plan and control cash.

Commercial banks are suppose implement a thorough training program in finance for their staff, regardless of each individual’s unique educational background and level. Through this, employees will be exposed to financial trends, which will improve their comprehension of cash management systems and the necessity of maintaining liquidity.

Suggestions for Further Studies

Further research can be done to assess how short capital decision impact term on corporate the effectiveness of listed banks in Ghana. Additionally, further research can use financial records to assess how business cycle impacts the cash management and corporate performance relationship of banking firms registered on the Ghana Stock Exchange as well as those not listed on the Ghana Stock Exchange in order to generalize the findings.

REFERENCES

- Abor, J. (2015). The effect of capital structure on profitability: an empirical analysis of listed firms in Ghana. The journal of risk finance, 6(5), 438-445.

- Abdel Jawid, Mat Nor, Ibrahim and Abdul Rahim. (2013). The relationship between working capital management and financial performance of private hospitals in Kenya. A Thesis submitted to the Department of Accounting and Finance, in partial fulfillment of the requirements for the degree of Master of Business Administration, University of Nairobi.

- Adeyeye, and Mukaila Adebisi Ijaiya. “Effect of Social Capital on the Growth of SMALL AND MEDIUM ENTERPRISES IN NIGER STATE.” (2021).

- Afza and Nazir. (2017). Working capital determinants for the UK pharmaceutical companies listed on FTSE 350 index. International Journal of Academic Research in Accounting, Finance and Management Sciences, 7(1), 11-17.

- Agyei M., (2021). Working capital management of commercial banks in Nepal (Doctoral dissertation, Master’s Thesis).

- Agyei, S.K. and Yeboah, B., 2022. Working capital management and profitability of banks in Ghana. British Journal of Economics, 2(2).

- Adjei-Boateng, E. S. (2022). A Literature Review on Management Practices among Small and Medium-Sized Enterprises. Journal of Engineering Applied Science and Humanities, 8(1), 1-23.

- Ahmad, A. and Bano, S., 2015. Working capital management matters profitability of textile sector: With GLS model. International Journal of Economics and Empirical Research, 3(11), pp.543-549.

- Arnold, G. (2008). Corporate Financial Management, 4th Edition. New York: Pearson Education Limited

- Appuhami, B. A. R. (2018). The Impact of Firms’ Capital Expenditure on Working Capital Management: An Empirical Study across industries in Thailand. International Management Review, 4 (1), 8-21.

- Atrill, P. (2019). Financial management for decision makers. Harlow: Financial Times Prentice Hall. Bank of Ghana. Banking Sector Report, Retrieved November, 2018.

- Bank of Ghana. (2014). Working capital management: The effect of market valuation and profitability in Malaysia. International journal of Business and Management, 5(11), 140.

- Boya (2019), “Liquidity-Profitability Tradeoff: An Empirical Investigation in an Emerging Market”, International Journal of Commerce and Management, Vol. 14, No. 2, pp. 48-61.

- Chen, C., & Kieschnick, R. (2021). Bank credit and corporate working capital management. Journal of Corporate Finance, 48, 579-596.

- Delis, M. D. (2022). Bank competition, financial reform, and institutions: The importance of being developed. Journal of Development Economics, 97(2), 450-465.

- Deloof, M. (2020). Does working capital management affects profitability of Belgian firms? Journal of Business Finance & Accounting, 30(3), 573 – 587.

- Devi, N., 2022. Impact of Working Capital Management on Profitability and Liquidity of Public Sector Banks in India. Contemporary Issues in Banking, Insurance and Financial Services, p.16.

- El-Maude, J.G. and Shuaib, A.I., 2016. EMPIRICAL EXAMINATION OF THE ASSOCIATION OF WORKING CAPITAL MANAGEMENT AND FIRMS’ PROFITABILITY OF THE LISTED FOOD AND BEVERAGES FIRMS IN NIGERIA. Researchers World, 7(1), p.12.

- Erik, R., 2022. Effects of Working Capital Management and Company Profitability: An Industry-wise study of Finish and Swedish Public Companies (Doctoral dissertation, a Thesis Submitted to the Department of Accounting, Hankin School of Economics, Helsinki).

- Falope, O. I. and Ajilore, O. T. (2019). Working capital management and corporate profitability: evidence from panel data analysis of selected quoted companies in Nigeria. Research Journal of Business Management, 3, 73-84.

- Fareed S. (2019). An overview of working capital with Financial Management. Vol 113 pp. 1

- Filbeck, G., & Krueger, T. M. (2018). An analysis of working capital management results across industries. American journal of business, 20(2), 11-20.

- Firer C., Jordan B. D., Ross S. A. & Westerfield R.W. (2018) Fundamentals of Corporate Finance 4th South African Edition. McGraw Hill.

- Frimpong, S. (2018). Working capital policies and value creation of listed non-financial firms in Ghana: a panel FMOLS analysis. Business and Economic Horizons, 14(4), 725-742.

- Gamlath, G. R. M., & Rathiranee, Y. (2014). The Impact of Capital Intensity, Size of Firm and Firm’s Performance on Debt Financing in Plantation Industry of Sri Lanka. SSRN.

- Gelos., (2016). The effect of working capital management of Ghana banks on profitability: Panel approach. International Journal of Business and Social Science, 5(10).

- Gitman, L. A. (2005), Principles of Managerial Finance, 11th Edition, Addison Wesley Publishers, New York.

- Gonçalves, T., Gaio, C. and Robles, F., 2018. The impact of Working Capital Management on firm profitability in different economic cycles: Evidence from the United Kingdom. Economics and Business Letters, 7(2), pp.70-75.

- Uyar, A. (2009). The Relationship of Cash Conversion Cycle with Firm Size and Profitability: An Empirical

- Empirical evidence from Vietnam. Journal of Asian Finance, Economics and Business, 7(3), pp.115-125.

- Lazaridis, I. and Tryfonidis, D. (2006). Relationship between working capital management and profitability of listed companies in the Athens stock exchange. Journal of Financial Management and Analysis, 19(1), 26-35.

- Lartey, V. C., Antwi, S., & Boadi, E. K. (2018). The relationship between liquidity and profitability of listed banks in Ghana. International journal of business and social science, 4(3), 48-56.

- Loutskina, E., 2021. The role of securitization in bank liquidity and funding management. Journal of Financial Economics, 100(3), pp.663-684.

- Maryem. (2021). Determinants of working capital management for emerging markets firms: evidence from the MENA region. Journal of Economic and Administrative Sciences.