The Role of Deposit Growth in The Productivity of Deposit Money Banks in Nigeria: Case Study of Union and Wema Banks in Lagos State.

- Aliu Oguntade Fatai

- Raymond Osi Alenoghena

- 234-246

- Jan 8, 2024

- Finance

The Role of Deposit Growth in The Productivity of Deposit Money Banks in Nigeria: Case Study of Union and Wema Banks in Lagos State.

Aliu Oguntade Fatai1, Raymond Osi Alenoghena2

1Department of Management Sciences, Trinity University, Yaba, Lagos

2Department of Economics, Trinity University, Yaba, Lagos

DOI: https://doi.org/10.51244/IJRSI.2023.1012019

Received: 07 December 2023; Accepted: 12 December 2023; Published: 07 January 2024

ABSTRACT

The ability of deposit money banks (DMBS) to achieve steady growth on their deposit base is a significant performance indicator to assess the efficiency and effectiveness of these banks. There has been a steady decline in banks’ deposit base, signalling performance deterioration, attributed to poor service rendering, high non-performing loans, increasing cost of operations and high staff attritions. This study examined the importance of deposit-based growth of two DMBs in Lagos State and their efforts to mobilise cheap deposits to increase their interest revenues and ultimately enhance their profitability. An aggressive deposit mobilisation drive is one policy option for these DMBs to motivate their staff to deliver superior performances. A survey research design was employed, and five hundred copies of research instruments were administered to the staff of the two banks. SPSS was adopted to process the The data weressed using SPSS, and the results showed that deposit growth positively and significantly affects overall organisational productivity. The multiple regression analysis results showed that fixed deposits (B = 0.099, p = 0.013) and recurring deposits (B = 0.159, p = 0.000) have a positive and significant effect on productivity at the selected deposit money banks. The study concluded that giving attractive incentives to the organisation’s staff of all categories will improve productivity. The study emphasised that extra efforts should be placed on rendering excellent service, which would significantly improve and sustain deposit mobilisation and organisational productivity. Also, the study recommends that attractive remunerations should be implemented for staff in line with the changing dynamics of the environment to their performance in meeting the bank’s deposit target responsibilities.

Keywords: Deposit growth, deposit money banks, deposit mobilisation, quality service, organisational productivity, staff remuneration.

INTRODUCTION

Deposit growth is a critical factor for the productivity and overall health of deposit money banks (DMBs), also known as commercial banks. DMBs play a pivotal role in the economy by facilitating financial intermediation, mobilising savings, and funding various economic activities in a nation. The Nigerian Banking system has been bedevilled by the systematic drop in the volume of liquidity, which has prompted the Central Bank of Nigeria to recapitalise the banks on several occasions (Obi-Nwosu et al., 2017). The deposit base of banks is essential to the primary role of financial intermediation, which requires banks to absorb the surplus funds in the form of savings (from the surplus sector) and make it available for investment in the needed sector of the economy. The intermediation role of banks is critical for the growth and development of the economy. The volume of investment activities entails the outflow of funds from the banking system, which requires careful supervisory management to ensure the timely recovery of funds and the maintenance of a balance in the bank’s liquidity position to ensure the continuous delivery of the intermediation function (Broby, 2021). The ability of the deposit money banks to maintain a healthy liquidity position makes it possible for them to discharge their regular function, improve their profitability, minimise operational risks and discharge their developmental role to the nation. Hence, deposit banks’ liquidity management is regarded as of utmost relevance and receives the attention of the monetary authority, practitioners, policymakers and researchers alike since liquidity shortages could lead to the failure of banks and trigger a contagion of systemic instability and collapse.

The growth of deposits has proved pivotal to the success and productivity of commercial banks on several other grounds. For instance, a growing customer deposit base allows banks to expand their range of services and products as a way of increasing revenue streams and mitigating the risks associated with market fluctuations and economic downturns (Ozili, 2018). With the growth of bank deposits, banks can engage in more investment opportunities and enjoy improvements in capital adequacy in meeting the regulatory requirements to improve business opportunities.

On the other hand, several problems are often associated with deposit generation in commercial banks. For instance, bank depositors face alternative investment opportunities in several other platforms like fintech-based, robo-investment and other very competitive non-traditional financial product investment avenues with higher returns than traditional banking products (Hornuf et al., 2021). Also, banks need more investment environments, which constrain them to offer low returns on their traditional deposit products. The younger generation of consumers tends to prefer digital banking, convenient payment apps, and peer-to-peer payment platforms, which might only sometimes involve keeping significant amounts of money in traditional bank accounts (Windasari et al., 2022). Traditional banks compete with digital-only (neobanks) that offer innovative and user-friendly interfaces and provide higher interest rates and convenient services. In developing countries like Nigeria, traditional banks face the problem of literacy and a large pool of unbanked businesses in the informal sector. Poverty and low income are rampant in developing countries and often leave a large segment of the population with little or nothing to bank on as they live hand to mouth by the day.

The rapidly changing environment, economic uncertainties, technological disruptions and several other factors which characterise the operations of deposit money banks in recent times have brought about a series of challenges that negatively affect the ability of these banks to meet their deposit targets (Alenoghena et al., 2020). Thus, these factors have been responsible for the banks’ inability to render smooth and uninterrupted services to their customers. The adverse effects of these challenges threaten the long-time survival of most traditional deposit money banks in recent times.

LITERATURE REVIEW

One of the major problems faced by deposit money banks in Lagos State, Nigeria, is their increasing inability to mobilise adequate and cheap deposits to enable them to advance loans to interested customers and earn more interest incomes on these deposits. The challenges are critical to the extent that it has negatively affected their growth and threatened their long-term survival (Alenoghena et al., 2023). As a follow-up, different banks have adopted varying strategies to mobilise deposit funds. One of these strategies includes placing every staff member on deposit targets (Amer & Mohammed, 2017). Hence, the staff that meet their target thresholds are rewarded, and those that persistently fail to measure up to the required standards are given varying punishments, including denial of bonus payment and in extreme cases, such staff may suffer delayed promotion. Bank also engages in extensive radio, television, and billboard advertisements.

Moreover, with the advancement of technologies, primarily through internet outlets, deposit money banks engage in extensive advertisement on social media platforms like Twitter, Facebook and Instagram. Dedicated units or departments of the bank are usually assigned to monitor achievements through online platforms. In addition, deposit money banks often sponsor events using the opportunities to canvass for more liquidity mobilisation (Akaninyene et al., 2018).

2.1 Types of Bank Deposits

There are two main types of deposits, which are demand and time deposits. Demand deposits are funds held in conventional banks. Withdrawals can be made on the account at any time. Time deposits are those with a fixed time and usually pay fixed interest rates. These interest-earning accounts offer higher rates than the savings accounts. Deposit money banks take the issue of deposit mobilisation seriously because the volume of deposits at these banks largely determines and also influences their ability to lend money to generate interest income. Ikechukwu & Ifeanyi (2015) explained that the different types of deposits, like savings, demand and call deposits, have peculiar characteristics, and it is more beneficial to the banks to mobilise cheap deposit funds for lending to their customers. A primary strategy to get the staff of the deposit money banks to mobilise cheap deposits is the award of bonus schemes that entail rewarding staff based on a specified percentage of the volume of deposits they can mobilise, the tenor of the deposits (the longer, the better) as well as the applicable rates (, the lower, the better).

A savings account is a demand deposit account that earns interest over time. When a customer makes a deposit, the bank pays them a set percentage of interest in exchange for holding their money for a specified period. The savings account is a type of account mainly suitable for people who have a definite source of income and are looking to save money for future usage or during emergencies. According to Duncan (2012) and Sylvester (2010), a savings account can be opened with a minimum initial deposit that varies from bank to bank, and deposits can be made anytime. Withdrawals on the account can be made either by signing withdrawal forms or by use of technology through online transactions of internet banking and automated teller machines. Most banks always put restrictions on the number of withdrawals periodically, which may be monthly or quarterly. If the threshold is exceeded, then part or whole of the interest due to be paid on the account may be forfeited. Also, the applicable interest rate on savings accounts varies from bank to bank, and the account holder must maintain a minimum credit balance on the account as the bank prescribes.

A fixed deposit account is when an account holder deposits money in his account for a specified period at a specified interest rate. Within the period, withdrawals may not be allowed. If there are any, there are accompanying penalties in the form of forfeiture of part or whole of interest already accrued before the withdrawal date. At the end of the specified period, the deposit may be withdrawn, terminated or renewed for a further period at negotiated covenants. Ahmad et al. (2016) stated that one of the advantages of deposits to banking institutions is that it ensures that the mobilised funds are transformed into productive capital resources, which are made available to individuals and corporate entities to engage in economic and financial activities. The multiplier effect will have positive growth in the economy. Akaninyene et al. (2018) pointed out that deposits are used as fixed investments, which attract guaranteed interest accruals for the agreed period.

The current checking account is a standard demand deposit account that allows customers to deposit cash or cheques. Some customers may use direct deposit to have an employer automatically deposit their salaries or other transfers into the account. A checking account has unique features that enable easy cash accessibility by allowing direct cash withdrawals, usage of automated teller machines, and writing cheques. The checking account allows withdrawals anytime from the account without penalty for the increased frequency of several withdrawals. Versatility and freedom are some of the significant benefits of a checking account. The operation of checking accounts allows the account holder to withdraw amounts over their balance on the account. This facility is known as an overdraft facility, which allows the account holders to exceed their book balance subject to them meeting the terms and conditions specified by the bank.

2.2 Liquidity Management in Banks

Bank liquidity refers to the bank’s ability to ensure the availability of funds to meet maturing obligations and operational commitments at a realistic price at all times. Hence, bank liquidity means a bank having money when they need it, mainly to satisfy the withdrawal needs of the customers. The survival of commercial banks depends significantly on how liquid they are since illiquidity, a sign of imminent distress, can quickly erode the public’s confidence in the banking sector and result in deposits. The liquidity management procedure is the compulsory requirement imposed on banks by the Central Bank to ensure that the banks do not become easily insolvent. Therefore, monitoring bank’s liquidity minimises the chances of raising loans under undesirable loan agreements and high interest-bearing costs. Liquidity management in DMBs also minimises the incidence of insolvency and liquidation, which are simply the result of illiquidity, and thereby helps to protect customers’ deposits. The Central Bank thus developed a framework to guide banks’ liquidity management in line with international standards and best practices. Liquidity management therefore, entails the control and planning required to ensure that the organisation keep enough liquid assets to meet customer withdrawal obligations which is incidental to the survival of the business (Aliu & Alenoghena, 2023). A commercial bank must plan to effectively manage its liquidity position and comply with the statutory regulatory authority and legal requirements. Liquidity management skills comes into play for a bank to avoid excesses or recklessness with the required primary reserves.

The Central Banks the world over manage the liquidity of DMBs using various techniques like Balances held with Other Banks in the Country, Inter-Bank Placement, Balances Held with CBN, Treasury Bills, Negotiable Certificates of Deposit, Commercial Papers, Investment in Federal Government Development Stocks and Bankers’ Acceptances.

Several researchers have questioned the need for excess liquidity by banks; according to Krool (2013), it may be financially unviable and unwise to maintain extra idle cash in the vault. Osborne et al. (2012) also raised questions about banks’ maintaining excess liquidity and further stated that it could adversely affect a bank’s profitability.

2.3 Theoretical Framework

The four theories discussed in this section include the shift-ability theory, the diffusion of innovation theory, the bank-led theory and the trade-off theory.

Shift-Ability Theory

This theory constitutes an approach of Deposit Money Banks to maintain liquidity by shifting assets to meet rising obligations. When a bank has liquidity problems, it can sell some of its assets to a more financially solid and liquid bank (Al-Zaidanin & Zaidanin, 2021). This approach cushions banks with liquidity problems and allows the system of banks to operate more efficiently, holding fewer reserves with less investment in long-term assets. Under the shift-ability approach, the financial system tries to avoid liquidity problems by enabling banks to always sell or repurchase liquid assets at reasonable prices.

The Diffusion of Innovations Theory

Diffusion of innovations is a theory that explains why, how and at what rate new technologies and innovations spread through different countries. Rogers (2003) posits that diffusion is the process by which a successful innovation is transmitted through specific channels to participants in a social system over time. The origin of the theory is varied and spans across multiple disciplines. The four vital diffusion elements are time, innovation, social system and communication channels. Diffusion is a version of communication concerning the messages on new ideas. The message must concern new ideas. The process involves a set of choices and actions through which an organisation or individual assesses a new idea to decide whether or not to invest in the new idea. The process entails dealing with uncertainty involving deploying a new production option. It is novel perspective of innovation and the uncertainty associated with it that makes it a distinctive aspect of innovation decision-making (Rogers, 2003). Deposit mobilisation is a new version of the diffusion theory in terms of approaching savers through marketing techniques and financial inclusion and adopting new techniques that have yet to be used before now. It is perceived and communicated through channels, and the social system facilitates adoption. In mobilising deposits, an innovation has to be applied to convince the savers to make deposits.

Bank led theory

The bank-led model provides a different option to the conventional branch banking approach, such that bank customers can conduct financial transactions at the shops of a range of retail agents instead of the bank branches (Dzombo et al., 2017). Even with the spread of services, the bank remains the ultimate provider of customer financial services, and it is the institution where all the bank customers’ accounts are domiciled. The retail agents have regular contact and face-to-face interaction with the bank customers. The retail agents also perform most of the cash-in/cash-out functions, performing the role of a branch-based teller that accepts deposits and processes withdrawals. Generally, the outlet that handles cash and performs other customer transactions would serve as a retail agent. With the established contract, each retail agent is electronically equipped to communicate with the bank for which he serves as an agent. The link equipment could be a point-of-sale (POS) machine or a mobile phone installed with a code.

The Trade-Off Theory

This study adopts the Trade-Off theory, which states that central banks’ liquidity management imposition is directed at banks to have higher liquidity in their possession to manage the financial demands of the customers. Some authors have argued that in enforcing the Trade-Off Theory, the central bank forces deposit banks to hold liquidity often above their private optimal level. Hence, banks are forced to hold liquidity balances above their internal optimal level (Robatto, 2019). Also, excess liquidity may result in a sizeable voluntary buffer in competitive markets since higher liquidity constitutes a more effective guarantee of the bank’s solvency. Such excess liquidity could also tempt banks to offer more surplus to borrowers. Some authors have opined that if banks are thriving in attaining their optimal liquidity level, there may be no short-run relationship since the standard first-order conditions imply that any change in liquidity has no impact on profitability (Akinwumi et al., 2017). This is corroborated by Osborne et al. (2012), who opined that a bank’s optimal liquidity level rises during periods of banking sector distress. Since, in such conditions, the fear and expected cost of bankruptcy rises. As a follow-up, the estimated average relationship between profitability and profitability across banks is cyclical. Osborne et al. (2012) argue further that in periods of distress, banks tend to maintain liquidity below their optimal levels.

On the other hand, during normal conditions, banks often meet their optimal capital level such that the liquidity levels will enhance their profitability. However, the performance, efficiency and survival of banks are generally more reflected in the possession of high liquidity by banks. The focus of the theory is to increase the bank’s optimal liquidity level and the performance of the banks in the long run.

2.4 Empirical Literature

The discussion on empirical literature is centred on the results of existing empirical studies conducted on the effect of deposit liability and the performance of banks.

Lartey et al. (2013) sought to establish the nature of the relationship between liquidity and the profitability of Ghanaian banks listed on the Stock Exchange for the period 2005 to 2010. The results showed that indicated a declining position of both the liquidity and profitability of the listed banks. Also, the study observed that a fragile positive relationship existed between the liquidity and profitability of the listed banks in Ghana. About the same period, Ogege & Boloupremo (2014) investigated the relationship between deposit money banks and Nigeria’s economic growth using time series data over the period 1973 to 2011. Adopting the cointegrating regression approach, they found that credit allocation to the productive sector of the Nigerian economy significantly promoted the level of industrial output and economic growth in Nigeria.

Tuyishime et al. (2015) used the Equity Bank Rwanda Limited as a case study in a target population for the study of bank managers that were involved in deposit mobilisation, drawing a sample of 27 staff. The main source of data was primary and secondary data. The findings indicated that most respondents (85%) confirmed that the brand name of Equity Bank assisted the marketing staff on deposit mobilisation. Also, the positive changes in deposit volume and rates charged positively impacted the bank performance measures like the net profit, return on assets (ROA) and returns on equity (ROE).

Edem (2017) investigated the effect of liquidity management on the performance of deposit money banks in Nigeria from 1986 to 2011. Deploying secondary data and inferential statistics, they found a significant positive correlation between liquidity management and the performance of Deposit Money Banks in Nigeria.

Onyekwelu et al. (2018) examined the effect of liquidity on the financial performance of deposit money banks in Nigeria from 2007 to 2016. Adopting multiple regression approach in their analysis, they found that the volume of liquidity in banks has a positive and significant effect on banks’ profitability. In the same year and in another related study on the impact of liquidity on the performance of commercial banks in Ghana, Charmler et al. (2018) examined a sample of 21 banks over a ten-year period covering 2007 to 2016. For analysis, the authors employed descriptive statistics, correlation and regression analysis. The study findings reveal that liquidity is positively associated with return on assets using both bank liquidity measures. Regarding return on equity (ROE), there is a weak positive relationship between liquidity ratios and total assets (LIDQ1). On the other hand, an insignificant negative relationship was observed between return on equity (ROE) and liquid assets to total interest-bearing liabilities (LIQD2).

In a similar study conducted in Bangladesh, Parvin et al. (2019) examined the effect of commercial banks’ liquidity and bank size on their profitability from 2011 to 2015. The study took a sample of seven banks and utilised descriptive statistics and correlation analysis to evaluate data. The study findings reveal that loan-to-asset ratio and bank size had a positive relationship with return on asset (ROA), which was the indicator of profitability. Also, the findings showed that the deposit-to-asset ratio negatively impacted on the selected bank’s return on assets (ROA). Although there were relationships among profitability, bank size and liquidity; bank size and liquidity did not have a significant iimpact on the profitability of the banks.

Chinweoda et al. (2020) examined the effect of liquidity management on the performance of banks in Nigeria over the period 2011 to 2017. The research study sample comprised of 18 banks listed on the exchange over a 5-year period. The findings reveal that while there is a significant positive effect of asset quality on the banks’ performance indicators, the liquidity ratio is positively and significantly related to the banks’ performance indicators. This result showed that banks with efficient liquidity management will improve their profitability over time.

Sathyamoorthi et al. (2020) examined liquidity management and financial performance with evidence from commercial banks in Botswana using secondary data on nine commercial banks. They utilised descriptive statistics, correlation and regression analyses to analyse data. The results from the analysis showed significant positive relationships between the loans to total assets ratio and the Liquid assets to total assets ratio with return on assets and return on equity. Also, the results on the Loans to deposits ratio and Liquid assets to deposits ratio had statistically significant negative relationships with return on assets and return on equity.

In another related study on the effects of deposit funds on the Performance and Growth of Financial Institutions, Newman et al. (2021) investigated BancABC Bank in a case study. The study adopted primary data based on a sample of 28 bank employees using the stratified sampling technique. The study results show a positive and significant relationship between the deposits and the performance of the banks. The findings also showed that deposit interest rate affects the bank deposit volume and, later on, the profitability of the bank.

On examining the role of institutional quality in bank deposit growth in European transition economies, Nguyen (2022) utilised GMM on WDI data covering the period 2000 to 2017. The study found that institutional quality strengthens the positive effect of deposit mobilisation on bank deposit growth and, hence, bank performance. Specifically, the rule of law has a positive correlation with bank deposits. Macroeconomic factors, including broad money supply and economic growth, are also significant factors in bank deposit growth.

Research gap

This study focuses on deposit mobilisation and the financial performance of deposit-taking banks in Nigeria. The existing related research in this area should have considered the deposit mobilisation factors and their role in the performance of commercial banks. The existing studies should have also examined how improving bank deposits can improve the financial performance of banks in Nigeria. This study takes account of the existing lacuna. It examines the effects of deposit mobilisation on the financial performance of deposit-taking banks in Nigeria with a specific focus on Union Bank and Wema Bank based in the Lagos State of Nigeria.

METHODOLOGY

The study adopted a survey research design. A survey design was adopted in this study because it enables the researcher to collect data for further analysis (Trochim et al., 2015). The target population for this study comprised 429 staff of the two deposit money banks in Lagos State. The banks were Union and Wema. The staff sampled consisted of 429 top- and middle-level management of the banks using the total enumeration technique. The data for this study was gathered using a quantitative approach through a structured questionnaire. The justification for using the quantitative research approach was that it facilitates the collection of large amounts of data that can be analysed to obtain patterns and trends (Bruner, 2019).

An adapted questionnaire was used to collect data from the participants. The questionnaire was divided into three sections as follows: Part A dealt with demographic variables, in which the study’s participants were asked to provide some specific personal and business information. Part B contained questions on deposit growth (DG) as an independent variable, while Part C measured organisational productivity (OP) as the dependent variable. The response rate of the questionnaire ranged from 6 being the highest to 1 being the lowest on a 6-point Likert-type scale. The response pattern includes VH = Very High, H = High, MH = Moderately High, ML = Moderately Low, L = Low, and VL = Very Low. The justification for using a 6-point Likert scale is that a six-point scale enables the participants to read the questions and make a decisive choice carefully. In addition, a six-point scale helps account for this reality.

Moreover, an even number of items on the response scale produces groupings that are easier to understand and discuss. The questionnaire was validated using content and construct validity through experts’ assessments and statistical tools. The reliability of the research instrument was established using the internal consistency method through Cronbach’s alpha since the study used multiple-item measures.

A pilot study was conducted at two deposit money banks in Lagos State. A total of 42 copies of the questionnaire were distributed in the process, out of which 33 copies were retrieved and analysed. The results of the reliability test confirmed that the instrument was reliable (deposit growth = 0.839, organisational productivity = 0.862, Cronbach’s α > 0.70) and valid for the study. The decision was based on Nunnally’s (1978) recommendation value of 0.70 and above. The inferential statistical technique was used to analyse data collected using Statistical Package for Social Sciences (SPSS version 28.0). A multiple linear regression analysis was adopted to predict the effect of deposit growth dimensions on organisational productivity. The reason for using multiple linear regression was that regression helps the researcher predict and obtain causal inference for a given variable (Allen, 2004; Jolliffe, 1988; Sykes, 1993).

The regression model specified for the study was represented by:

![]()

Where:

Yi = Organisational productivity

β0 = Constant term

β1 – β4 = Coefficient of deposit growth dimensions respectively

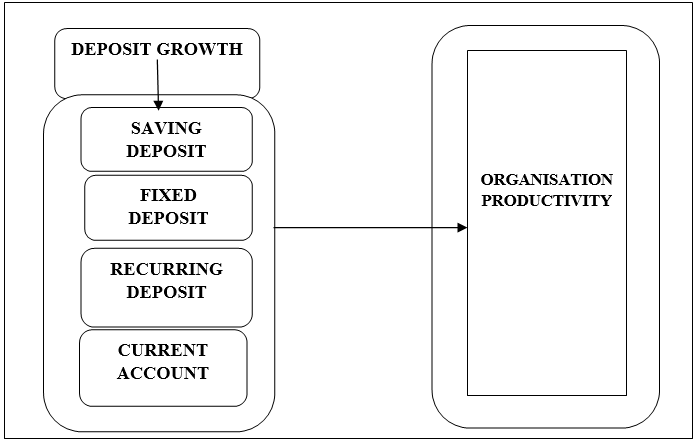

X1 = Savings Account

X2 = Fixed Deposit

X3 = Recurring Deposit

X4 = Current Account

εi = Error term

RESULTS AND DISCUSSION

The researcher administered 429 copies of the questionnaire to the respondents, of which three hundred ninety-eight (398) copies were filled correctly and returned to the respondents. Meanwhile, 31 copies were either not returned or found not usable. The overall successful response rate was 92.77%. The recorded high response rate was attributed to the data collection procedures adopted by the researcher.

Table 4.1: Response Rate

| Category | Frequency | Percentage% |

| Completed usable copies of questionnaire | 398 | 92.7 |

| Unreturned/Incomplete copies of questionnaire | 31 | 7.3 |

| Total | 429 | 100 |

Source: Field survey result, 2023

As stated earlier, multiple linear regression analysis was employed to predict the effect of deposit growth dimensions on organisational productivity. The deposit growth dimensions (savings account, fixed deposit, recurring deposit, and current account) were independent sub-variables, while the dependent variable was organisational productivity. In the analysis, data for deposit growth dimensions were created by adding together responses of all the items under each dimension to create an independent score for each dimension. Similarly, data for organisational productivity was created by adding responses of all items under the variable to create an organisational productivity index. The results of the linear regression analysis and the parameter estimated are presented in Table 4.2.

Table 4.2: Summary of Results of Multiple Linear Regression Analysis to Predict Effect of Deposit Growth on Organisational Productivity

| Coefficients | |||||||||

| N | Variables | B | β | T | Sig | R2 | Adj. R2 | F(4, 393) | F Sig2 |

| 393 | Constant | 15.380 | 7.713 | 0.000 | 0.116 | 0.107 | 12.777 | 0.000 | |

| Savings Account | 0.126 | 0.094 | 1.841 | 0.066 | |||||

| Fixed Deposit | 0.099 | 0.137 | 2.504 | 0.013 | |||||

| Recurring Deposit | 0.159 | 0.202 | 3.692 | 0.000 | |||||

| Current Account | 0.066 | 0.054 | 1.023 | 0.307 | |||||

- Dependent Variable: Organisational Productivity

- Predictors: (Constant): Savings Account, Fixed Deposit, Recurring Deposit and Current Account

Table 4.2 presents the results of a multiple linear regression analysis predicting the effect of deposit growth dimensions (savings account, fixed deposit, recurring deposit, and current account) on organisational productivity at selected deposit money banks in Lagos State, Nigeria. The results showed that fixed deposits (β= 0.099, p<0.05) and recurring deposits (β= 0.159, p<0.05) significantly predicted organisational productivity, helping banks mobilise cheap and profitable long-tenor deposits, resulting in higher incomes and profitability. On the other hand, savings deposits (β= 0.126, p > 0.05) and current accounts (β= 0.066, p > 0.05) had a positive but insignificant effect on productivity.

The possible reasons for the insignificance of the current account dimension could be the existence of some challenges in the implementation of robust current account programmes, which serve as disincentives to employees from being fully committed to the organisation’s deposit mobilisation efforts and strategies. The adjusted coefficient of determination (Adjusted R2) was 0.107, indicating that all deposit growth components accounted for 10.7% of the variance in organisational productivity at the selected banks. The p-value of 0.000 indicates statistical significance at the 95% level. The remaining unexplained 89.3% variance could be attributed to poor employee remuneration packages, which could cause disenchantment at the organisation. The combination of deposit growth sub-variables was statistically significant in explaining the improvement in banks’ productivity. The regression model that was established to predict the effect of deposit growth sub-variables on organisational productivity at the deposit money banks is summarised as follows:

OP = 15.380 + 0.099FD + 0.159RD+ 0.066CA …………… (4.1a) Predictive Model

OP = 15.380 + 0.099FD + 0.159RD …………………………(4.1b) Prescriptive Model

Where:

OP = Organisational Productivity

FD = Fixed Deposit

RD = Recurring Deposit

SA = Saving Account

CA = Current Account

The regression equation shows that holding all factors constant at zero results in 15.380 productivity at deposit money banks. An improvement in fixed deposits leads to a 0.099-times improvement in productivity. A 10% change in recurring deposits will stimulate a 1.59% positive change in organizational productivity. The impact of recurring deposits on productivity is positive such that, with generous staff benefits having the greatest influence. Recurring deposits are the largest predictor of organizational productivity, followed by fixed deposits. The overall model significance is 12.777 with p = 0.000 (p < 0.05), supporting the effectiveness of recurring and fixed deposits in predicting organizational productivity. The growth of selected banks deposits through fixed deposits and recurring deposits significantly predicts organizational productivity at these banks in Lagos State. Therefore, banks should design internal policies that attract fixed and recurring deposits to enhance organizational growth and overall performance.

FIG. 1 Conceptual Model of Deposit Growth and Productivity

DISCUSSIONS

The findings of this study revealed that deposit growth had a significant effect on the organisational productivity of selected deposit money banks in Lagos State. The finding further showed that recurring deposits had the most significant impact in boosting the productivity of selected deposit money banks. In contrast, savings and current accounts deposits had no significant influence on the deposit’s growth with p-values greater than 0.05. The findings of this study support the research of Bernardin (2017), who found that organisations that focus on maintaining and improving employee quality of life and providing financial security for their family members are more likely to achieve higher productivity. Benefit programs aim to attract, retain, and motivate qualified staff to drive deposit mobilisation within the institution. However, attractive benefits and packages can create psychological golden handcuffs that make employees more reticent to move to other employers.

In some older-generation banks in Nigeria, these benefits, particularly medical programs, may make some staff unwilling to leave despite their low salaries and packages. Tafirei et al. (2014) confirmed that deposit growth and organisational productivity are positively related. Deposit money banks monitor their deposit balances closely and devise strategies to grow them continuously, as large and healthy balances strengthen their capacity to lend. Staff play a unique role in the mobilisation, utilisation, and management of deposits, ensuring that they do not take “hot deposits” and that interest income should be greater than interest expense. Organisation management must also ensure that their assets are appropriately matched, avoiding short-term deposits to finance longer-term loan obligations. Deposits form part of a bank’s working capital, which determines the volume of business undertaken. Financial intermediation activities enable the creation of money and its spread throughout the economy, and bank deposits are primary tools for investment. The efficiency wages theory further supports the finding. Menezes & Raposo’s (2014) study explains that efficiency wages theory suggests higher organisational productivity, leading to higher wages for workers. This theory suggests that employees should be paid higher than the market wage for their contributions to productivity.

Deposit money banks often award competitive bonuses to motivate performance, particularly in deposit mobilisation. These bonuses are paid outside of an employee’s base pay and are typically given to reward specific behaviour or purpose. Bonus schemes provide incentives and motivation for employees within the organisation. Regular and different types of bonus payments can incentivise employees to work hard and be rewarded. Organisations that give out bonuses at specific periods of the year, such as quarterly, half-yearly, or annually, provide employees with something to work towards and encourage them to excel. Appreciation is another advantage of bonus payment, as employees feel more appreciated and motivated to excel.

CONCLUSION AND RECOMMENDATIONS

From the findings of this study, deposit mobilisation positively affects the productivity of deposit money banks in Lagos State, Nigeria. The findings concluded that different banks use different strategies and processes to mobilise cheap deposits since deposits play a vital role in overall organisational productivity. The findings enumerated the key variables that were instrumental to mobilising cheap deposits, which included the volume of deposit, intended tenor and the applicable rates. The introduction of technology has positively impacted the quantum of funds mobilised at relatively lower costs. The study used survey research and multiple regression analysis, which revealed that deposit growth components of savings deposits, fixed deposits, current accounts and recurring deposits significantly affect the ability of deposit money banks to be profitable. Deposit mobilisation and management of the funds mobilised requires delicate balancing to achieve a healthy or positive deposit loan to loan rations. The result of the study further revealed that the steady growth of deposits indicates that deposit money banks can be trusted with depositors’ funds without any impairment. The outcome of this study established that banks use different policies and strategies to mobilise cheap funds to meet and surpass organisational targets. The findings also concluded that deposit growth broadly supports increased demand for loans and advances in most Nigerian banks, as many fixed deposit customers tend to use their fixed deposit accounts as cash-backed securities for their credit facilities because they always attract lower interest charges.

The study recommends that deposit money banks should constantly review the quality of their deposits. The study also recommends that deposit money banks award attractive incentives to their staff to motivate higher productivity and promote the spirit of healthy competitiveness within the organisation strata. Such incentives should include both financial and non-financial packages to have broader appeal to a large segment of the workforce. It is recommended that deposit money banks should create new credit products and review the existing ones in order to support more business growth. Further, they should also engage in creative product diversification in order to meet the increasing credit demands of expanding business operations, especially that of small-scale enterprises, since the operating banks mainly lend from pooled funds to sustain their credit activities.

REFERENCES

- Ahmad, R., Eric, H. Y. K., & Shahrin, S. S. (2016). Determinants of bank profitability: A comparative study of East Asia and Latin America. International Journal of Banking, Accounting and Finance, 7, 34–51.

- Akaninyene, B. O., Innocent, O. O., & Aniekpeno, E. (2018). Inflation and deposit mobilisation in deposit money banks. The Nigerian perspective. International Journal of Public Administration and Management Research, 4(4), 109-121.

- Akinwumi, I. A., Essien, J. M., & Adegboyega, R. (2017). Liquidity management and banks performance in Nigeria. Business Management and Economics, 5(6), 88-98.

- Al Zaidanin, J. S., & Al Zaidanin, O. J. (2021). The impact of credit risk management on the financial performance of United Arab Emirates commercial banks. International Journal of Research in Business and Social Science (2147-4478), 10(3), 303-319.

- Alenoghena, R. O., Saibu, O. M., & Adeoye, B. W. (2020). Financial development and economic growth in Nigeria: Asymmetric cointegration and threshold analysis. In Forum Scientiae Oeconomia (Vol. 8, No. 4, pp. 43-63).

- Alenoghena, R. O., Samuel, D. A., & Charles, A. O. (2023). Fiscal Policy and Macroeconomic Variables in Africa: A Bayesian VAR Approach. International Journal of Research and Innovation in Social Science (IJRISS). 6(12), 731-741 URL: https://www.rsisinternational.org/journals/ijriss/Digital-Library/volume-6-issue-12/731-741.pdf

- Aliu, O. F., & Alenoghena, R. O. (2023). Employee Training and Organisational Performance of Selected Deposit Money Banks in Lagos State, Nigeria, International Journal of Research and Innovation in Social Science (IJRISS). 7(2), 129-140

- Allen, M. P. (2004). Understanding regression analysis. Springer Science & Business Media.

- Amer, S. J., & Mohammed, S. M. (2017). The factors that affect deposits mobilisation in Palestinian Islamic banks. Asian Journal of Finance and Accounting, 9(1).

- Bernardin, H. J. (2017). Human Resource Management. An Experiential Approach. Tata McGraw Hill. London.

- Broby, D. (2021). Financial technology and the future of banking. Financial Innovation, 7(1), 1-19.

- Bruner, K. M., Wang, Z., Simonetti, F. R., Bender, A. M., Kwon, K. J., Sengupta, S., & Siliciano, R. F. (2019). A quantitative approach for measuring the reservoir of latent HIV-1 proviruses. Nature, 566(7742), 120-125.

- CBN, (2017). Saving in a financial institution: What you need to know. CBN Publications, Abuja.

- CBN, (2018). Statistical bulletin. CBN Publications, Abuja

- Chinweoda, U. O., Onuora, U. R., Ikechukwu, E. M., Ikechukwu, A. C., & Ngozika, O. A. (2020). Effect of liquidity management on the performance of deposit money banks in Nigeria. The Journal of Social Sciences Research, 6(3), 300-308.

- Dzombo, G. K., Kilika, J. M., & Maingi, J. (2017). The effect of branchless banking strategy on the financial performance of commercial banks in Kenya. International Journal of Financial Research, 8(4), 167-183.

- Edem, D. B. (2017). Liquidity management and performance of deposit money banks in Nigeria (1986–2011): An investigation. International Journal of Economics, Finance and Management Sciences, 5(3), 146-161.

- Hornuf, L., Klus, M. F., Lohwasser, T. S., & Schwienbacher, A. (2021). How do banks interact with fintech startups?. Small Business Economics, 57, 1505-1526.

- Ikechukwu, S. N., & Ifeanyi, S. M. (2015). Bank deposits and demand for credits in Nigeria: What lessons are available? Journal of Accounting and Financial Management, 1(8), 11-21.

- Jolliffe, I. T. (1986). Principal components in regression analysis. In Principal component Analysis. 129-155. Springer, New York, NY

- Lartey, V. C., Antwi, S., & Boadi, E. K. (2013). The Relationship between Liquidity and Profitability of Listed Banks in Ghana. International Journal of Business and Social Science, 4(3), 1-9.

- Menezes, A. T., & Raposo, I. (2014). Wage differentials by firm size: The efficiency wage test in a developing country. Estudos Econômicos (São Paulo) 44, 1.

- Newman, W., Nkhambala, F. A., & Tshwane, S. M. (2021). Effects of Depositors Funds on the Performance and Growth of Financial Institution: A Case Study of BancABC, Academy of Strategic Management Journal, 20(3)

- Nguyen, T. A. N. (2022). The role of institutional quality in bank deposit growth in European Transition Economies. Finance Research Letters, 47, 102630.

- Obi-Nwosu, V., Okaro, C. S. O., Ogbonna, K., & Atsanan, A. (2017). Effect of liquidity on performance of deposit money banks. International Journal of Advanced Engineering and Management Research, 2(4).

- Ogege, S., & Boloupremo, T. (2014). Deposit money banks and economic growth in Nigeria. Financial Assets and Investing, 5(1), 41-50.

- Onyekwelu, U. L., Chukwuani, V. N., & Onyeka, V. N. (2018). Effect of liquidity on financial performance of deposit money banks in Nigeria. Journal of Economics and Sustainable Development, 9(4), 19-28.

- Osborn, M., Fuertes, A. & Milner, A. (2012). Capital and Profitability in Banking: Evidence from US Banks: Business journal, 4(9). 203-214.

- Ozili, P. K. (2018). Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review, 18(4), 329-340. doi.org/10.1016/j.bir.2017.12.003

- Parvin, S., Chowdhury, A. M. H., Siddiqua, A., & Ferdous, J. (2019). Effect of liquidity and bank size on the profitability of commercial banks in Bangladesh. Asian Business Review, 9(1), 7-10.

- Robatto, R. (2019). Systemic banking panics, liquidity risk, and monetary policy. Review of Economic Dynamics, 34, 20-42.

- Rogers, E.M. (2003). Diffusion of innovations (5th ed.). New York: Free Press.

- Sathyamoorthi, C. R., Mapharing, M., & Dzimiri, M. (2020). Liquidity management and financial performance: Evidence from commercial banks in Botswana. International Journal of Financial Research, 11(5), 399-413.

- Sykes, A. O. (1993). An introduction to regression analysis. Chicago.

- Sylvester, O. (2010). Mobilizing Deposits; The role of commercial banks, Ghana

- Tafirei, M., Rabson, M., Linda, C., & Gumbo, L. C. (2014). Analysing the relationship between banks’ deposit interest rate and deposit mobilisation: Empirical evidence from Zimbabwean commercial banks (1980-2006). Journal of business and management (IOSR-JBM), 16, 64-75.

- Trochim, W., Donnelly, J. P., & Arora, K. (2015) Research Methods: The Essential Knowledge Base. Nelson Education, Cengage Learning, Boston

- Tuyishime, R., Memba, F., & Mbera, Z. (2015). The effects of deposits mobilization on financial performance in commercial banks in Rwanda. A case of equity bank Rwanda limited. International Journal of small business and entrepreneurship research, 3(6), 44-71.

- Windasari, N. A., Kusumawati, N., Larasati, N., & Amelia, R. P. (2022). Digital-only banking experience: Insights from gen Y and gen Z. Journal of Innovation & Knowledge, 7(2), 100170.