Fiscal Deficit Inflation Nexus in Nigeria

- Nkemjika Nwosu

- Uduakobong Sammy Inam

- Paul Atanda Orebiyi

- 3274-3287

- Aug 23, 2024

- Economics

Fiscal Deficit Inflation Nexus in Nigeria

Nkemjika Nwosu, Uduakobong Sammy Inam, Paul Atanda Orebiyi

Department of Economics, University of Uyo, Ikpa Road, PMB 1017, Akwa Ibom State, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.807249

Received: 15 June 2024; Accepted: 15 July 2024; Published: 23 August 2024

ABSTRACT

This study analyses the relationship between fiscal deficit and inflation in Nigeria using annual data covering the period 1980 to 2023. Specifically, the study seeks to: investigate the long and short-run effects of fiscal deficit and inflation in Nigeria; and also ascertain the causal relations between fiscal deficit and inflation in Nigeria. The study employs the Auto-Regressive Distributed Lag (ARDL) technique and the Granger Causality test to address the specific objectives. The study reveals that fiscal deficit has a direct and significant impact on inflation in the long run and an inverse insignificant relationship in the short run in Nigeria and there is no causal relation between fiscal deficit and inflation in Nigeria. The study recommends that the government should closely monitor fiscal deficit given its crowding out effect. To achieve this, there is need for the government to be cautious in reducing government spending (borrowing) which can help to free up funds for private investment. However, there should be caution, as this can negatively hurt economic growth. Furthermore, the government should closely monitor and support agricultural and real sectors because developing the agricultural sector has great potential to increase the supply of farm products and other necessities of life. The increased supply will reduce prices and increase employment generation. Also, establishing job-creating industries, will help to reduce the level of unemployment in the country, increase output, reduce prices of goods and services, and thus, reduce the level of inflation in the economy.

Keywords: Fiscal Deficit, Inflation, Auto- Regressive Distributed Lag (ARDL), Nigeria.

JEL Classification: E31, E62, E63, H62, P24,

INTRODUCTION

In recent decades, the relationship between fiscal deficit and inflation has been a topic of substantial interest and debate among economists, policymakers, and researchers worldwide. In light of Africa’s developing economy, such as Nigeria, understanding this intricate relationship is imperative for ensuring sustainable economic growth and stability. Nigeria, as one of the largest economies in Africa, has experienced significant fluctuations in its fiscal deficit and inflation rates, making it an ideal case study to explore the nexus between these two critical economic variables.

Fiscal deficit, the difference between government expenditures and revenues, has long been recognized as a fundamental component of economic policy. Simultaneously, inflation, the persistent increase in the general price level of goods and services, poses challenges to economic stability and purchasing power. The interaction between these phenomena, often referred to as the fiscal deficit-inflation nexus, has far-reaching implications for a nation’s economy.

Understanding the dynamics of this relationship is pivotal for crafting effective fiscal and monetary policies that can mitigate inflationary pressures without compromising essential public spending. The growth and persistence of fiscal deficits in both industrialized and developing countries have led to a critical reassessment of their impact on economic activities. In the Nigerian context, this phenomenon can be traced back to the economic crisis of the 1980s, marked by issues such as over- indebtedness and the debt crisis, high inflation rates, and poor investment performance as highlighted by Onwioduokit (1999).

These challenges underscore the urgency of investigating the intricate relationship between fiscal deficits and economic stability in Nigeria. Over several decades, Nigeria has witnessed a consistent rise in expenditures, surpassing its revenue generation. Government interventions in economic development, implemented through policy measures, have been constant in the country. However, the scale, magnitude, and method of financing these interventions have the potential to trigger macroeconomic repercussions, including inflation, distortions in external economies, and the crowding-out effect on private sector investments.

Addressing these challenges is paramount for ensuring a stable and sustainable economic environment in Nigeria. The nexus between fiscal deficit and inflation is one of the fiercely contested themes in economics. The effect of fiscal deficit on inflation has been immensely debated for a while now. Achieving sustainable economic growth and macroeconomic stability is the oneirism of several developed, developing, and underdeveloped economies. Governments in the global economy deploy diverse policies, plans and programmes to achieve macroeconomic stability in their respective countries. Fiscal Policy is one of the main drivers for the attainment of this commendable objective.

Fiscal deficit is the difference between government revenue and expenditure (including government expenditure and investment). According to theory, when expenditure increases without aligning revenue for a year, deficit occurs. Moreover, fiscal theory of price level posits that a persistent fiscal deficit in an economy can lead to inflation. This occurs because governments, in their attempts to bridge the deficit, resort to creating more money, which subsequently drives up commodity prices, as suggested by Juvenalis (2020).

In the Nigerian context, the escalating inflation rates can be directly linked to a high fiscal deficit, serving as a contemporary manifestation of the consequences stemming from the continuous rise in price levels. This situation underscores the urgency of examining the fiscal deficit-inflation nexus in Nigeria comprehensively. Furthermore, the relationship between higher fiscal deficits and elevated inflation can be elucidated through several mechanisms. One such mechanism involves the government’s increased borrowing requirements, which augment net credit demands within the economy. This surge in demand exerts upward pressure on interest rates, ultimately crowding out private sector investment.

Consequently, the economy experiences a reduced growth rate, leading to a decrease in the availability of goods for a given level of cash balances. This scarcity results in an increase in the overall price level as demand outstrips supply. Additionally, higher deficits can contribute to inflation even in scenarios where central banks do not directly monetize the debt. In these cases, the private sector steps in to monetize deficits when the government’s borrowing induces high interest rates. Financial institutions respond by creating new interest-bearing assets that possess liquidity almost equivalent to money and are considered risk-free.

According to Kaur (2018) privatized monetization of government debt effectively fuels inflationary pressures, as articulated by Kaur (2018). These intricate mechanisms underline the multifaceted ways in which fiscal deficits can instigate inflationary trends, emphasizing the need for a nuanced understanding of these dynamics in Nigeria. When a government runs a deficit, borrowing becomes a necessity, leading to the accumulation of debt. In Nigeria’s case, this has been evident through the growth in domestic debt, pushing the country’s total public debt from 41.60 trillion to 42.84 trillion, as reported by the Debt Management Office in 2022. Moreover, the government’s accumulation of over 11 trillion to finance the budget in 2023 has coincided with a continuous rise in inflation rates.

This scenario underscores the significant challenge that fiscal deficit poses to the monetary management, specifically inflation control, within the Nigerian economy. In Nigeria, fiscal expenditure is enabled by historically high oil sales revenues, which are typically punctuated by periods of oil glut that result in sharp drops in government revenues. The custom of fiscal deficits in Nigeria is that it is skewed heavily in favour of recurrent expenditure which does not necessarily drive economic development.

Since one of the critical instruments of fiscal policy is fiscal deficits, hence, stabilization of prices, growth of per capita income, and employment requires that fiscal deficit itself must grow or expand at a low constant rate. The rate at which the fiscal deficit has been increasing is concurringly inconsistent. Nevertheless, the pandemic crisis in 2020, affected all sectors of the economy, as till date we have been experiencing its aftermath. Furthermore, some of the reasons Nigeria has been experiencing poor performance as a result of ineffective formulation and implementation of policies is the volatility in fiscal deficit and inflation.

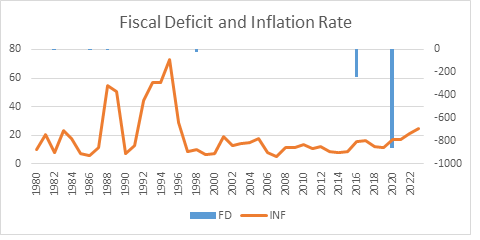

Figure 1: Fiscal Deficit and Inflation Rate

Source: Author’s computation

Changes in fiscal deficit influences inflation as government tries to raise revenue to finance fiscal deficit, they create more money which raises inflation because of increased demand of commodities (Carto and Torrens 2005). Moreover, in 1981 due to the oil glut, it resulted into balance of payment deficit leading to foreign exchange crisis that necessitated various measures of import restrictions. The lack of goods and services resulting from this for local consumption drove up inflation to 17.8% in 1984. The government embarked on price control measures, which saw inflation rates falling to 5.7% in 1986.

With the adoption of Structural Adjustment Programme (SAP) in 1986, there was a temporal reduction in fiscal deficit as government removed subsidies and reduced her investment in the economy. From 1993 to 1995 inflation rate rose drastically due to increased lending rate, the policy of guided deregulation and lagged impact of fiscal indiscipline. Between 1988 and 1989 due to fiscal expansion which was financed by credit from the CBN, inflation rate increased. Thereafter, in 1990, due to improved level in agricultural output, inflation rate reduced to 7.3%.

However, from 1996 to 1999 inflation rate remains relatively stable. Furthermore, inflationary pressure was curtailed in 2006 and 2007 as it reduced to a single digit resulting from the implementation of sound macroeconomic policies. In 2014 and 2015, the country experienced a single digit. But due the pandemic in 2020, the rate increased till date. Furthermore, the global supply chain was disrupted in 2022 by the Russia-Ukraine war leading to the rise in energy prices and non- exportation of wheats, which is a staple used in most food products; hence a continuity of inflation in the economy. Furthermore, the fiscal deficit has been increasing from 21.2 per cent in 1984 to 38.3 % in 1993 except for 1987 when the rate stood at 8.3%. The growth in fiscal deficit was substantial during the SAP (Structural Adjustment Programme) years except in 1987 when it decreased by 31%.

However, from the graph, Nigeria recorded high deficit rate in 1995 to 2000, 2010 with high volatility from 2010 to 2014. Thereafter, in 2016 Nigeria approved a budget of N6.08 trillion with projected revenue of N3.86trillion and an outlay of N4.49 trillion; implying a deficit of N2.22trillion or 2.16 per cent of GDP. The deficit was to be financed by a combination of domestic borrowing of N984 billion and foreign borrowing of N900 billion totaling N1.884 trillion (FGN, 2015).

Hence, volatility of fiscal deficit has continued till date.

Also, the fiscal deficit narrowed to 4.9% of GDP in 2022 from 5.2% in 2021 and was financed by borrowing, bringing public debt to $103.1 billion (about 22% of GDP) from $92.6 billion in 2021. Despite the fact that the modest increase in oil exports created a 0.1% GDP surplus in 2022, correcting a three-year deficit. Notwithstanding the austerity measures introduced by the Obasanjo regime, government deficit spending even after the introduction of SAP in 1986, has continued to be on the increase with a fluctuating trend as shown on the trend above.

Governments in Nigeria had financed their fiscal deficits largely through monetary expansion although not significant to surmount the inflationary pressure. In addition, fiscal deficit has become a challenge to the monetary and fiscal management of the Nigerian economy and therefore poses some concerns to citizens in general.

What really is the relationship between fiscal deficit and inflation in Nigeria? Does fiscal deficit has long and short run effects on inflation in Nigeria? What is the nature and direction of causality between fiscal deficit and inflation in Nigeria? Therefore, the major objective of this study is to analyze the relationship between fiscal deficit and inflation in Nigeria using annual data covering the period 1980 to 2022.

Specifically, the study seeks to: investigate the long and short run effects of fiscal deficit and inflation in Nigeria; and also ascertain the causal relations between fiscal deficit and inflation in Nigeria. The study is relevant as it will bridge the gap in the literature and serve as a guide for recommendation. Apart from this section which is the introduction; Section 2 reviews Theoretical and Related Empirical Literature while Section 3 contains the Research Methodology. The results are presented in Section 4 while Section 5 embodies the Summary, Conclusions and Recommendations.

LITERATURE REVIEW

Theoretical Framework.

Three major schools of thought are considered by economists while looking at the effects of fiscal deficits. The neoclassical school advances the crowding-out hypothesis (Barro, 1974; Blanchard, 1985), while the Keynesians postulates that an increase in government spending stimulates the domestic activity and crowds-in private investment (Friedman, 1978). The Ricardian Equivalence, however, argues that increase in the deficit financed by fiscal spending will be matched with a future increase in taxes, and therefore interest rates and private investment will remain unchanged (Bernheim, 1987; Barro, 1989; Bahmani-Oskooee, 1999)

Keynesian Theory

The Keynesian hypothesis states that fiscal imbalances can influence social welfare and help the economy grow. According to Keynes, government expenditure will increase output and employment by a factor of two. Spending more will boost the economy’s overall demand, which will encourage advanced investment and increase the profitability of domestic investments. Government spending is an important component of Aggregate Demand (AD) in the economy. Whenever AD falls short (through recessions), the government can raise spending, which in turn will increase the AD, and in turn, inspire the economy (Hussain and Haque 2017).

Keynesian further argument is that government deficits expands domestic production, and grantees private investors to be more optimistic about the future course of the economy which results to increase in investment. This is called the “crowding-in” effect. But looking at the multiplier effect side, Keynesians note that the total impact of government spending can overweigh any loss of investment due to the higher interest rates. Hence government spending can increase total output.

Government borrowings is typically associated with an expansionary short –term economic impact. When the government borrows money to pay for ongoing expenses, it increases aggregate demand, which raises output in situations where the supply is elastic and the prices and / or wages are sticky. The short-term effect is this.

However, in the long run, the effect could be contrary according to the neoclassical view point.

This is due to the fact that rising real interest rates are eventually necessary to balance the securities market and as a consequence, investment gets crowded out and capital and output eventually fall. This is the long run effect. According to this theory, fiscal deficits increase overall lifetime consumption by shifting taxes to subsequent generations which may lead to reduction in investment. therefore, when consumption rises there is the likelihood of a fall in savings . by inference, a fall in savings raises interest rates and hence a reduction in investment which is the crowding out effect. When the government is facing a deficit, it may borrow money from the loanable funds market, which affects interest rates and demand. It also implies that government borrowing crowds out private business by increasing interest rates. Nonetheless, the neoclassical perspective is against government deficit spending since it holds that investments and savings will equalize if the loanable funds market is allowed to operate independently.

The Ricardian Equivalence Theory

Ricardo equivalence proposition, advocates that government fiscal deficits do not distress the overall level of demand in an economy (Eigbiremolen 2013). From a Ricardian perspective, a decline in administrative savings resulting from the fiscal deficit is offset by an increase in private savings, leaving national savings and, therefore, investment unchanged. In this instance, there is no shift in the true interest, and those who hold this opinion are confident that a budget deficit is a sign of future trade taxes for current taxes. In other words, the government should tax more than it spends tomorrow if it spends more than it collects today. Once people understand this correlation, they will spend and save accordingly. We assume that the increases in the deficit have two major outcomes. First, the tax reduction increases disposable income. Second, if the deficit is increased, there is an increase in net private sector financial assets (Tharaka and Ichihashi (2012).

This follows the equilibrium condition.

I +G = S + T (Equation 1)

This can be written as

G − T = S – I (Equation 2)

Where I is investment, G is government spending, S is national saving and T is the tax revenue,

G − T is the government deficit.

The effect of the tax cut and deficit increase is represented by an upward shift of the IS curve. The expansionary effect of the shift in IS curve will depend on whether the LM curve shifts or not. The movement of the LM curve will depend on how the deficit is financed. If additional reserves provided to the commercial banks are created, the money supply increases and the LM shifts to right, adding to the expansionary effect of the deficit. This ultimately affects the monetary policy decisions and general price level, each government has its budget constraint; it has to pay its bills just like individual’s households do. It raises revenue by levying taxes or going into debt by issuing government bonds.

Fiscal Theory of Price Level

It states that when the government faces a persistent fiscal deficit the general price level tends to increase. The increase in inflation is assumed to be a monetary phenomenon because when an economy faces sustained fiscal deficit government looks for a way of financing them. In so doing, they create money leading to increased levels of income and this increases total demand for commodities and hence inflation rises.

Empirical Literature

Several studies have empirically investigated the relationship between fiscal deficit and inflation in most countries of the world. Some studies revealed a positive relationship between fiscal deficit and inflation. For instance, Ezeabasili, Mojekwu and Herbert (2012), Ozurumba (2012), Mehmood (2013), Nguyen (2015), Anofofum, Yahaya and Suleman (2015), Nwakobi, Echekoba and Ananwude (2018), Kaur (2018), Okoro and Oksakei (2020), Eche, James Alexander and Abdullahi (2022).

On the contrary, some studies reveal a negative relationship between fiscal deficit and inflation. For instance, see Onwioduokit (1999), Anayochukwu (2012). Also, some studies found no causal relationship between fiscal deficit and inflation. For instance, Oladipo and Akinbobola (2011), Kaur (2018). On the contrary, some studies reveal unidirectional causal relation between fiscal deficit and inflation. For instance, see Ozurumba (2012), Orji, Onyeze and Edeh (2014).

RESEARCH METHODOLOGY

Nature and Sources of Data

Data used for this study are secondary in nature. They are annual time series data obtained from sources such as: the Central Bank of Nigeria Statistical Bulletin (various issues) and the National Bureau of Statistics publication of various issues. The data employed spanned the period 1980-2022.

Model Specification

INF = F (FD, GDP, MS, LIR, OPN, UMP) (Equation 3)

FD> 0, GDP >0 or< 0, MS>0, LIR>0, OPN>0, UMP<0

Where,

INF=Inflation Rate (%)

MS=Money supply (M2) Growth Rate (%)

FD=Fiscal deficit/GDP (%)

GDP=Gross Domestic Product (%) Growth Rate

LIR=Lending Interest Rate (%)

OPN= Trade Openness

UMP= Unemployment Rate (%)

Analytical Technique

The analytical techniques employed for the purpose of this study is based on the specific objectives of the study.

Objective One: To examine the long and short- run relationships between fiscal deficits on inflation in Nigeria, the Auto Regressive Distributed Lag (ARDL) model was employed.

The Auto Regressive Distributed Lag (ARDL)

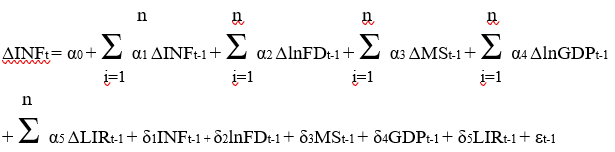

The Auto Regressive Distributed Lag (ARDL) Model which uses a bound test approach based On the Unrestricted Error Correction Model (UECM) was employed here to measure the connection between fiscal deficit and inflation and to test for a long –run relationship among the relevant variables. This model was developed by Pesaran and Pesaran (1997) and used by Pesaran, et al (2001). The main advantage of this approach lies in the fact that it can be applied irrespective of whether the variables are I (0) or I (1).

This approach also allows for the model to take a sufficient number of lags to capture the data-generating process in a general-to-specific modeling framework. Also, it provides very efficient and consistent test results in small and large sample sizes (Pesaran et al., 2001). Following Shrestha and Chowdhury (2007), to illustrate the ARDL modeling approach, the Unrestricted Error Correction Model of the three equations is stated below:

(Equation 4)

(Equation 4)

Having done this, there is also the need to perform a series of diagnostic tests on the stochastic properties established model. This is because the existence of a long –run relationship does not necessarily imply that the estimated coefficients are stable (Bahmani- Oskooee and Brooks, 1999). This, therefore, involves testing of the residuals (that is homoscedasticity,non-serial correlation, etc), as well as normality tests to ensure that the estimated model is statistically robust.

It is also pertinent to note here that one of the arguments against the ARDL is that the estimators will be inefficient and biased (or even inconsistent) in the presence of autocorrelation of the disturbances. However, Pesaran and Shin (1999) show that appropriately modifying the orders of the ARDL model is adequate to simultaneously correct for residual serial correlation and the problem of endogenous regressors, thus giving ARDL an advantage over other approaches to Cointegration.

In addition, Pesaran and Shin (1999), argue that endogeneity problems are addressed in this technique by modeling the ARDL with the appropriate lags, thus correcting for both serial correlation and endogeneity problems. Jalil et al (2008) in their study also show that endogeneity is less of a problem if the estimated ARDL model is free of serial correlation. In this approach, Khan et al (2005) equally argue that where all the variables are assumed to be endogenous, the long –run and short –run parameters of the model can be estimated simultaneously.

Objective Two: To examine the causal relationship between fiscal deficits on inflation in Nigeria the Granger causality test was employed.

The Granger Causality Test

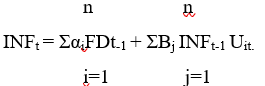

The Granger causality test states that the cause-and-effect relationship is that the past value should affect the present value. The Granger causality equations for this study are specified thus:

(Equation 5)

(Equation 5)

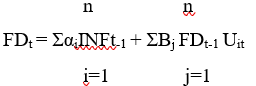

(Equation 6)

(Equation 6)

The INFt is affected by the past values of FD and INF. FD is affected by past values of INF and FD. The test is conducted by regressing the current INF on all lagged value of INF but not FD because it is being tested for causation. By this, we will obtain the RSSr. Afterwards, we regress the current INF on its past value and the lagged values of FD, to obtain the unrestricted residual sum of squares.

The decision rule is that if αi = 0, then FDt-1 does not granger cause changes in INFt. if δj=0 then INFt-1 does not granger cause changes in FDt. Thereafter, the F-test is being applied. (RSSr – RSSur)/m * N – K/RSSur. Where M represents the number of lagged terms. If Fcomp > Ftab at a chosen significant level, then the lagged values of the FDt causes changes in INFt. To determine m, we use the AIC or SIC = nk/nEu2/n = nk/n RSS/n.

ANALYSIS OF RESULTS

We began our empirical assessment with some preliminary checks beginning with the descriptive statistics and then the unit roots tests. The outcomes are reported in Tables 4A and 4B respectively

Table 1 A: Descriptive Statistics

| Inflation Rate | Fiscal Deficit | GDP Growth Rate | Trade Openness | Exchange Rate | Broad Money Supply | Lending Interest Rate | |

| Mean | 17.01 | 1297.76 | 3.01 | 31.65 | 116.24 | 22.96 | 17.27 |

| Median | 13.30 | 198.80 | 3.30 | 33.35 | 115.20 | 19.10 | 16.90 |

| Maximum | 75.40 | 6404.70 | 15.30 | 53.20 | 448.80 | 87.70 | 31.60 |

| Minimum | 0.60 | -861.40 | -13.10 | 9.10 | 0.60 | -0.70 | 8.90 |

| Std. Dev. | 14.04 | 1914.38 | 5.29 | 12.13 | 120.68 | 17.60 | 4.81 |

| Skewness | 2.12 | 1.32 | -0.82 | -0.24 | 1.07 | 1.50 | 0.36 |

| Kurtosis | 8.69 | 3.57 | 4.74 | 2.22 | 3.40 | 5.97 | 3.60 |

| Jarque-Bera | 88.26 | 12.84 | 10.14 | 1.47 | 8.32 | 31.38 | 1.54 |

| Probability | 0.00 | 0.00 | 0.00 | 0.47 | 0.01 | 0.00 | 0.46 |

| Sum | 714.59 | 54506.00 | 126.70 | 1329.50 | 4882.40 | 964.59 | 725.50 |

| SumSq. Dev. | 8092.12 | 1.50 | 1150.91 | 6036.82 | 597157.1 | 12704.72 | 950.92 |

| Observations | 42 | 42 | 42 | 42 | 42 | 42 | 42 |

Source: Author’s computation using E-views

As seen in Table 1A, the descriptive statistics showed a mean of 17.01 and median of 13.30 for the inflation rate. Moreover, the statistic also showed that the data for the inflation rate was a leptokurtic distribution because the kurtosis value is greater than three indicating a positive kurtosis, though positively and significantly skewed, showing a good fit. Furthermore, the total variability within the data for inflation is 714.59. Though all other variables have reflected diverse values.

Table 1 B: Augmented Dickey-Fuller (ADF) and Philip-Perron (PP) Unit Root Analysis

| ADF | Philip Perron | ||||||||||

| Levels | First | Difference | Levels | First | Difference | Order of | |||||

| Variables | T-Statistic | P-Value | T-Statistic | P-Value | T-Statistic | P-Value | T-Statistic | P-Value | Integration | ||

| Inflation Rate | -6.075 | 0.0000 | -6.0759 | 0.0000 | I (I) | ||||||

| Gross Domestic product | -5.215 | 0.0001 | -3.786 | 0.0000 | I (0) | ||||||

| Uemp

Fiscal Deficit |

-3.881

-6.151 |

0.0177

0.0000 |

-6.652 | 0.0000 | -3.8610 | 0.0165 | 1(0)

I (I) |

||||

| Lending Interest Rate | -5.512 | 0.0000 | -7.093 | 0.0000 | I (I) | ||||||

| Exchange Rate | -3.830 | 0.0054 | -3.750 | 0.0068 | I (I) | ||||||

| Trade Openness | -8.162 | 0.0000 | -9.315 | 0.0000 | I (I) | ||||||

| Broad Money Supply | -4.019 | 0.0033 | -4.018 | 0.0032 | I (0) | ||||||

Source: Author’s computation using E-views

The outcomes of the unit root test validated the use of Auto regressive Distributed Lag (ARDL) technique in analysing the data used for this study. The level of stability showed by the statistical significance further enhanced the level of certainty in the prediction that ARDL technique will yield reliable results from the analyses of the data used for this study.

Table 2: Bounds Test

| Dependent variable: INF | F- statistics = 5.3778

K= 4 |

|

| Critical Values | Lower Bound 1(0) | Upper Bound 1(1) |

| 10% | 2.45 | 3.52 |

| 5% | 2.86 | 4.01 |

| 2.5% | 3.25 | 4.49 |

| 1% | 3.74 | 5.06 |

Source: Author’s computation using E-views

It can be observed that the f- statistic of 5.3778 was both greater than the upper bound value of 3.52 with a degree of freedom, K=4. This implies that, in this model, there exist long- run relationships between the dependent and independent variables. Based on this, the long- run and short -run error correction models can be estimated.

Table 3: long run estimates on the nexus between fiscal deficit and inflation in Nigeria

| Dependent Variable: Inflation | ||

| Regressors | Positives Estimates | Negative Estimates |

| Constant Term | 64.113 (0.4337) | |

| Uemp Fiscal deficit | 0.003(0.0450) | -2.113(0.5121) |

| Exchange rate | 3.420(0.0535) | |

| GDP (Growth Rate) | -0.245(0.2623) | |

| Lir | -0.263(0.3321) | |

| Money Supply | 0.5295 (0.1461) | – |

| Trade Openness | 0.017 (0.9816) | |

Source: Author’s computation using E-views.

The coefficient of fiscal deficit (FD) is 0.003, implying that in the long run, there is a positive link between fiscal deficit and inflation. This means that a 1% increase in fiscal deficit will result in a 0.003% increase in inflation rate. However, in line with fiscal theory of price level. This also implies that in the long run, the revenue-to- expenditure disparity may expand to the point where inflationary pressures are exerted on the economy. When an economy has a large deficit, it portrays its poor revenue base structure and as much will be forced to borrow. Hence, borrowing becomes onerous in the long term since the borrowed money are majorly spent on ineffective initiatives. In accordance to the classical view, repaying the loans in the long term will fall to the population, disturb the private sector equilibrium and limit investment capital hence, leading to inflation due to low production.

Also, the result shows a crowding-out effect, as when the government borrows heavily from the market, it can lead to an increase in the money supply. This increase in the money supply can ultimately lead to inflation.

As shown in Table 3, the result showed that exchange rate would transmit fiscal deficit-inflation nexus to the tune of about 3.42 percent, though statistically significant. The implication is that more than 3 percent of exchange rate can distort inflation rate. The implication of this result is is that more than 3 percent of the exchange rate can distort the inflation rate. This result implies that, the continuous loss in the value of the Naira makes exports cheaper and imports more expensive. Nigeria being a net importer of both capital and consumer products, affects the price of imported items and, as a result, the overall price level. The significance of the coefficient, further supports the applicability of this connection to Nigeria.

Also, the coefficient of Gross Domestic Product (GDP) is -0.245, implying that in the long run, there is a negative link between GDP and inflation. This means that a 1% increase in inflation will result in a 0.245% decrease in GDP. This implies that an increase in inflation leads to a decline in the purchasing power of money, which reduces consumption and therefore decreases GDP. An increase in inflation makes investment less desirable, since it creates uncertainty for the future and also affects the balance of payment because exports become more expensive. As a result, GDP decreases further. However, the statistical insignificance may be due to distortions associated with time series data in Nigeria amongst other factors.

Furthermore, the result affirms the fact that interest rate harms inflation in the Nigerian economy. With a coefficient of -0.263, though statistically insignificant, the result indicated that there would be about a 0.263 percent drop in inflation. This implies that a higher interest rate leads to lower inflation. The rationale is that higher interest rate increases the cost of borrowing and dampen demand across the economy, resulting in excess supply leading to a reduction in inflation.

The coefficient of money supply is 0.529, implying that in the long run, there is a positive link between money supply and inflation. This means that a 1% increase in interest rate will result in a 0.529% increase in inflation rate. Nevertheless, its probability level is insignificant; the statistical insignificance may be due to distortions associated with time series data in Nigeria amongst other factors. However, in line with the quantity theory of money. this result implies that if the government prints more money, then there will be an increase in cash in the economy. Households would have more money and so their demand for goods and services would rise. With more cash, they intend to buy more goods. However, if the amount of goods for sale, remained the same, then firms would see a big rise in demand for this limited supply and so would respond to the higher demand by increasing prices.

The positive relationship between trade openness and inflation is a deviation from theory. Trade openness reduces inflation by encouraging competition in domestic markets, production efficiency, better allocation of resources, better use of capacities and increasing foreign investment. Also, due to stronger competition in the market, monetary policy is expected to be more prudent and lower inflation. This does not to the Nigerian economy due to over-reliance on imports and negligence of the domestic market (infant industries).

The coefficient of unemployment rate (UEMP) is -2.113. There is a negative relationship between the unemployment rate and inflation. This means that a 1% increase in the unemployment rate will result in a 2.113% increase in the inflation rate. This implies that there is a trade-off relationship between the variables. Also in line with the Philip curve theory, hence proving the existence of the Philip curve in Nigeria. Therefore, there should be caution when implementing policies that will reduce unemployment; because a decrease in the unemployment rate could make inflation rise.

Table 4: Short run estimates on the nexus between fiscal deficit and inflation in Nigeria

| Dependent Variable: Inflation | ||

| Regressors | Positives Estimates | Negative Estimates |

| Uemp Fiscal deficit | -0.026758(0.9072)

-0.001237 (0.7167) |

|

| Exchange rate | -0.010711 (0.2153) | |

| GDP (Growth Rate) | -1.372493 (0.0072) | |

| Lir | -2.132000 (0.0059) | |

| Money Supply | 0.031272(0.1072) | – |

| Trade Openness | -0.216273 (0.5501) | |

| ECM (-1) | -3.67162 (0.5260) | |

| Adjusted R2 | 0.880320 | D-W stat.: 1.43 |

Source: Author’s computation using E-views

It was also pertinent to investigate the short-run relationship between inflation and other macroeconomic variables considered in the study. On the other hand, the short-run effect did not

reflect much difference from the foregoing results analyzed. As seen in Table 4, the coefficient estimates of fiscal deficit (-0.0012) in the short run showed that, ceteris paribus, a rise in the level of fiscal deficit will truncate the possibility for inflation at about 0.0012 percent rate.

Furthermore, the exchange rate showed a negative relationship with inflation. This result implies that when inflation is high, it makes a currency weaker, suppressing investment and thus negatively impacting the exchange rate. A negative interest rate as equally seen in the result reduces the profit margins of lending institutions and commercial banks. Hence, may encourage banks to cease or decrease lending as profitability decreases. Also, foreign investors earn lower returns on their investment, which leads to lower demand for the domestic currency- devaluing the currency and reducing the exchange rate as seen in the table above -0.010711 (0.2153) as this is the case in Nigeria today.

The positive relationship between money supply and inflation implies that printing money by increasing the money supply causes inflationary pressure. This can be seen on the coefficient of 0.031272(0.1072) although insignificant. However, this can be due to distortions associated with time series data in Nigeria amongst other factors.

Furthermore, there is an inverse relationship between trade openness and inflation. between trade openness and inflation. however, this is in line with the new growth theory. Hence an increase in trade openness can promote competition and create a favourable allocation of resources, thereby reducing inflation.

Also, the ECM represents the percentage of correction to any deviation in the long –run equilibrium in a single period and also respects how fast the deviations in the long –run equilibrium is corrected. The ECM (-1) showed -3.46 but insignificant. This implies that whenever there is any disturbance in the system in the long run, in every short-run period, a 36% correction to disequilibrium will take place.

Table 5: Causality result

| Null Hypothesis: | Obs | F-Statistic | Prob. |

| FD does not Granger Cause INF | 40 | 1.40914 | 0.2579 |

| INF does not Granger Cause FD | 0.10081 | 0.9044 | |

The result showed that there is no causality between fiscal deficit and inflation at 5% level of significance. This implies that the traditional relationship of no causal relations between fiscal deficit and inflation may not always hold. If fiscal deficit does not cause inflation, government may need to reconsider their fiscal policies. Instead of focusing solely on reducing fiscal deficits to control inflation, they may need to consider other factors, such as monetary policy and supply-side factors, to achieve their inflation control goals.

SUMMARY, CONCLUSION AND POLICY RECOMMENDATIONS

The major objective of this study was to analyze fiscal deficit- inflation nexus in Nigeria: A time series analysis. Specifically, it sought to: investigate the long and short-run effects of fiscal deficit and inflation in Nigeria; and also ascertain the causal relations between fiscal deficit and inflation in Nigeria. The study employed the Auto Regressive Distributed Lag (ARDL) and the Granger Causality test to address the specific objectives. The (ARDL) Uses a bounds test to test for a long-run relationship among the relevant variables. Since there was an existence of a long run then the Error Correction Model was done. The study has revealed that fiscal deficit has a direct and significant impact on inflation in the long run and an indirect insignificant relationship and in the short run in Nigeria and there are no causal relations between fiscal deficit and inflation in Nigeria.

Conclusion

This study has revealed the nexus between fiscal deficit and inflation. Thus, the Nigerian government could display a high sense of transparency in the fiscal operations to bring about a realistic fiscal surplus. Fiscal surplus, when recorded should be channeled to productive investments like road construction, electricity provision, and so on, that would serve as incentives to productivity through the attraction of Foreign Direct Investment, in other to reduce the incidence of inflation in Nigeria. In addition, what should be of utmost concern to policy makers as regards the fiscal deficit-inflation nexus should not necessarily be the level of fiscal deficits but the channels through which the deficits are financed and the ability of the productive base of the economy to absorb the impact of such financing. However, a fiscal management process that does not encourage increased revenue and reduce fiscal deficits in Nigeria would further worsen the level of inflation in the country.

Recommendation

- Government should closely monitor fiscal deficit given its crowding out effect. To achieve this government should consider its expenditure (reducing borrowing) which can help to free up funds for private investment. However, there should be caution, as this can hurt economic growth.

- The government should closely monitor and support agricultural and real sectors. This is because developing the agricultural sector has great potential to increase the supply of farm products and other necessities of life. The increased supply will reduce prices and increase in employment generation. Also, establishing job-creating industries, will help to reduce the level of unemployment in the country, increase output, reduce prices of goods and services, and thus, reduce the level of inflation in the economy.

- The government should encourage trade openness to reduce inflation over time and also boost the country’s productivity.

REFERENCES

- Anayochukwu, O. B. (2012). The relationship between fiscal deficits and inflation: The causality approach, International Journal of Scientific and Technology Research 1(8), 6

- Anfofum,A.A, Yahaya, A.O and Suleman, T (2015). Empirical investigation of fiscal deficit and inflation in Nigeria. European journal of business and management 4(2): 24-34

- Bahmani-Oskooee, M. (1999). Do federal budget deficits crowd out or crowd in private investment? Journal of Policy Modeling, 21(1), 633-640

- Barro, R. J. (1989). The Richardian approach to budget deficits, Journal of Economic Perspectives 3, 37 – 54

- Barro, B. (1974). The determination of public debt, Journal of Political Economy. 87(5), 940-971.

- Bernheim, B.D (1987). Ricardian Equivalence: An Evaluation of Theory and Evidence, NBER Chapters, in: NBER Macroeconomics Annual 1987, 2: 263-316. National Bureau of Economic Research.

- Blanchard, O; (1985). Debt, Deficits and Finite Horizons. Journal of political economy 93: 223-47.

- Bleaney M, and Francisco M (2016), Inflation and Fiscal deficit in sub-Saharan Africa. Journal of African Economies 25(4), 529-547

- Catao, L. V. and Terrones, M. E. “Fiscal deficits and inflation”, Journal of Monetary Economics, 52, 529-554, March 2005

- Debt Management Office (2022). Published 19th September 2022.

- Ekanayake, H.K, J (2012). The link between fiscal deficit and inflation: Do public sector wages matter? The Australian National University Australian South Asia Research Centre.

- Ezeabasili, V. N., Mojekwu, J. N., and Herbert, W. E. (2012), An empirical analysis of fiscal deficits and inflation in Nigeria, International Journal of Business and Management, 4(1) 105-120

- Eigbiremolen, G.O (2013). Causality and Dynamics of Foreign Direct Investment and Economics Growth in Nigeria: An impulse Response Function Analysis, journal of Economics and sustainable development 4, (19): 44-51.

- Eche, N.Austine; James, P.B; Alexander, I.A and Abdullahi, H.P (2022). Effect of Fiscal Deficit on Inflation and Selected Macroeconomic Fundamentals of Nigeria: 1981-2020. Journal of Contemporary Issues in Accounting (JOCIA) . 3 (1) : 176-197.

- Fischer, S., Sahay, R., Végh, C.A., (2002). Modern hyper- and high inflations. Journal of Economic Literature, 40 (3), 837–880.

- FGN (2015), The Budget of Change, 2016 Budget Speech delivered by His Excellency, Muhammadu Buhari, President, Federal Republic of Nigeria to A Joint Session of the National Assembly, December 22, 2015.

- Friedman, M. (1978). The role of monetary policy, American Economic Review, 58, 1-17

- Hussain, M and Haque, M (2017). Fiscal deficit and its impact on Economic Growth: Evidence from Bangladesh, Economies, 5(4),37.

- Jalil, A., Tariq, R., and Bibi, N. (2008). Fiscal deficit and inflation: New evidences from Pakistan using a bounds testing approach. Economic Modelling, 37, 120–126

- Juvenalis M.S (2020). The nexus between inflation and fiscal deficit in Kenya. A research paper submitted to the school of economies university of Nairobi, in partial fulfilment of the requirement for award of masters of Arts Degree in economies.

- Kaur, G. (2018). The relationship between fiscal deficit and inflation in India: A cointegration analysis. Journal of Business Thought, 8, 24-41

- Khana, R.E.A and Gill A.R (2005). Determinant of inflation: a case of Pakistan. Journal of economies 1(1): 45-51

- Lin, H.Y., Chu, H.P., (2013). Are fiscal deficits inflationary? Journal of International Money Finance, 3(1), 214–233.

- Mehmood. S (2013). The relationship between fiscal deficit and inflation in Zimbabwe. International journal of economies 16: 0-33

- Nwakaobi P.C, Echekobia F.N and Ananwude A.C (2018). Fiscal deficit in an oil dependent revenue country and selected macroeconomics variables a time series analysis. European journal of economic and financial research 3(1), 126-167.

- Nguyen, V. B. (2015). Effects of fiscal deficit and money M2 supply on inflation: Evidence from selected economies of Asia. Journal of Economics, Finance and Administrative Science.

- Oladipo, S. O. and T. O. Akinbobola (2011). Budget deficit and inflation in Nigeria: A causal relationship, Journal of Emerging Trends in Economics and Management Sciences (JETEMS) 2(1), 1-8

- Okoro, A. S and Y.P Oksakei (2020). Impact of fiscal deficits on macroeconomic variables in Nigeria. International Journal of Accounting Research (I JAR) 6 (1),1-13.

- Onwioduokit, E.A. (1999). Fiscal Deficits and Inflation Dynamics in Nigeria: An Empirical Investigation of Causal Relationships. Central Bank of Nigeria Economic and Financial Review, 37(2), 1-16.

- Orji, M.A, Onyeze, S.R and Edeh, O.U (2014). The causal relationship between inflation and fiscal deficit in Nigeria. Journal of Research in National Development 10 (3): 34-41

- Ozurumba, B.A. (2012). Fiscal deficit and inflation in Nigeria: The causal approach. International Journal of Science and Technology Research. 3(5), 6-12.

- Persaran, M. H and Persaran, B (1997). Working with microfit 4,0: Interactive Econometric Analysis, Oxford, Oxford University Press.

- Persaran, M. H., Shin Y. and Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships, Journal of Applied Econometrics, 16, 289-326.

- Shrestha, M and Chowdhury, K (2007) Testing financial liberalization hypothesis with ARDL modelling approach. Applied financial economics 17(18): 1529-1540.

- Tharaka, N. D. and Ichihashi, M. (2012). How does the budget deficit affect inflation in Sri Lanka, IDEC Discussion Paper, Hiroshima University, Japan, 739-8529?

- Tiwari A.K (2011). Fiscal deficit and inflation: An empirical analysis for India. The Romanian Economies journal XIV (42): 131-158