Accounting Conservatism and Corporate Governance: An Examination of the Influence on Financial Reporting Quality and Stakeholder Trust

- Guanwei Liu

- 2158-2175

- Apr 17, 2024

- corporate governance

Accounting Conservatism and Corporate Governance: An Examination of the Influence on Financial Reporting Quality and Stakeholder Trust

Guanwei Liu

Macau University of Science and Technology

DOI: https://dx.doi.org/10.47772/IJRISS.2024.803151

Received: 25 February 2024; Revised: 11 March 2024; Accepted: 16 March 2024; Published: 17 April 2024

ABSTRACT

This study explores the effects of accounting conservatism and strong corporate governance in Chinese private enterprises based in Foshan City, Guangdong, China. The mixed-methods approach particularly the quantitative part of the survey found strong evidence of conservative accounting practices and high levels of corporate governance. These practices were perceived by companies to significantly affect financial reporting quality and enhance stakeholder trust. Likewise, thematic analysis of the qualitative part of the survey revealed both the complexities of implementing accounting conservatism and strong corporate governance, alongside the substantial benefits perceived by companies that embrace these practices. With these findings, the study recommends promoting awareness, best practices, resource investment, and knowledge sharing to strengthen accounting conservatism, corporate governance, and overall financial reporting integrity.

Keywords: accounting conservatism, corporate governance, financial reporting quality, stakeholder trust, Chinese private enterprises

INTRODUCTION

Accounting conservatism has become a crucial aspect of financial reporting procedures in the ever-changing world of global commerce. It is said to have a significant impact on corporate governance structures and helps to build confidence among stakeholders. Particularly in areas with distinct business landscapes like China, the interaction between conservative accounting practices and corporate governance is becoming more important as firms maneuver through intricate economic situations.

As frequently reported in Forbes, China is a prominent global economy. It has seen rapid economic expansion and globalization, leading to a significant increase in the number of publicly traded enterprises. This highlights the critical need for trustworthy financial reporting methods and strong company governance processes. Accounting conservatism, a measure of confidence in the accuracy of accounting information, necessitates the capacity to independently verify a company’s earnings and losses (Shen & Ruan, 2022). Thus, it involves a careful approach to recognizing profits and a proactive strategy for disclosing losses, which may influence the quality of financial reporting and the rise of stakeholders’ trust.

This study’s aim is to investigate the complex correlation between accounting conservatism, corporate governance, financial reporting quality, and stakeholder trust within the Chinese environment particularly in private small or medium enterprises within Foshan City, province of Guangdong. The main objective is to examine the extent of practice and challenges and opportunities in accounting conservatism and corporate governance in select private enterprises in Foshan City and how these practices contribute to the level of stakeholder trust and financial reporting quality.

The study’s relevance in China is emphasized by the country’s rapid economic expansion and changing socio-political environment. Given China’s ongoing integration into the global economy, it is crucial to have strong corporate governance and dependable financial reporting processes. Because of this, it is very important to understand how accounting conservatism affects the quality of financial reporting and the trust of stakeholders in a society that is unique in its mix of historical traditions, political ideology, and social and cultural dynamics. Furthermore, this study focuses on the current obstacles and possibilities encountered by firms functioning in China’s unique socio-cultural and political environment, as the country aims to enhance openness and credibility in its financial markets.

Relatively, this work makes a substantial contribution to the theoretical comprehension of the correlation between accounting conservatism, corporate governance, and the quality of financial reporting. By examining private firms in the Chinese environment particularly those based in Foshan City, this study provides insights into how cultural and institutional issues might impact the implementation and efficacy of accounting conservatism. The study fills gaps in the current body of literature, enhancing accounting and corporate governance theories by including context-specific details. This theoretical innovation is of utmost importance for both academics and practitioners since it offers a framework for improving financial reporting methods and governance structures in fast-changing countries such as China.

REVIEW OF RELATED LITERATURE

The literature discussed in this section covers the following topics: (1) the convergence of accounting conservatism and corporate governance; (2) the historical evolution of accounting and corporate governance in China; (3) the impact of financial reporting quality on stakeholder trust; and (4) the challenges and opportunities associated with implementing accounting conservatism in China.

Accounting Conservatism vis-à-vis Corporate Governance

The intersection of accounting conservatism and corporate governance fundamentally supports transparency, dependability, and integrity in financial reporting across various organizational settings worldwide. A fundamental aspect of reliable financial reporting is accounting conservatism, which is defined as being thorough when acknowledging profits and proactive when declaring losses (Hajawiyah et al., 2020). The presentation of financial information should represent a realistic and careful assessment of an organization’s financial status, in line with the concept of prudence (Christensen, 2023). Relatively, accounting conservatism emphasizes that the identification of losses should occur more promptly than the recognition of profits due to the asymmetry in the costs and rewards associated with providing verified information by managers and/or companies (Guay & Verrecchia, 2006, as cited in Pasko et al., 2021). Thus, accounting conservatism, when included in corporate governance frameworks, promotes the disclosure of possible risks and uncertainties, which in turn enhances the quality and reliability of financial information, supports accountability, and encourages trust among stakeholders.

Correspondingly, frameworks exist to direct and supervise enterprises in a way that satisfies the needs and expectations of their stakeholders. In the book of Larcker and Tayan (2020), corporate governance is defined as a system of checks and balances that the organization implements as some kind of monitoring or control system to reduce agency expenses. It is a set of control measures used by an organization to discourage management from participating in actions that might harm the interests of its stakeholders (Larcker & Tayan, 2020). These explanations highlight that in today’s society, it is crucial to adopt a more comprehensive and stakeholder-focused approach to corporate governance (Solomon, 2020).

Although there are no widely accepted criteria for what constitutes effective governance (Larcker & Tayan, 2020), a company’s capacity to maintain accountability and ethical behavior depends on its corporate governance processes, which should include strong board supervision, independent audit committees, and open disclosure policies. Financial misstatements or manipulations may be prevented, opportunistic conduct can be discouraged, and agency conflicts can be reduced by integrating conservative accounting standards into corporate governance structures (Hajawiyah et al., 2020). Through this connection, the legitimacy of financial reporting is consequently bolstered, investor trust will increase, and long-term sustainability is promoted in the organization. Hence, as maintained in El-Habashy (2019), the implementation of efficient corporate governance practices and a rigorous adherence to accounting conservatism would enhance the overall quality of the company’s financial reporting.

Accounting conservatism and corporate governance may operate together globally (Aguilera, Desender, & López-Puertas Lamy, 2021) to establish financial honesty and openness in all firms. Conservative accounting standards must be incorporated into corporate governance frameworks to provide transparency, reduce risks, and build stakeholder confidence (Pasko et al., 2021). This applies to mature economies with stringent regulations and developing markets with changing governance frameworks. By following prudence, openness, and accountability, organizations may traverse complicated business situations, mitigate risks, and promote sustainable growth, stabilizing global financial markets.

Accounting and Corporate Governance in China

The evolution of accounting and corporate governance in China mirrors the transition from a centrally planned economy to a market-oriented one, characterized by substantial changes and modernization efforts (Lennox & Wu, 2022; Jiang & Kim, 2020). Traditionally, Chinese accounting processes were mostly informal and centered on maintaining records for taxes and administrative objectives, rather than providing financial reports for external stakeholders. Nevertheless, when economic reforms were implemented in the late 1970s and the transition to a market-based economy occurred (Chen & Zha, 2023), it became clear that there was a need for more advanced accounting systems. China responded by assimilating aspects of Western accounting methodologies, resulting in the establishment of more structured accounting norms and rules (Guo & Krever, 2022).

Likewise, the development of corporate governance in China has been shaped by wider economic and political changes with the goal of modernizing the nation’s business climate and enticing international investment (Jiang & Kim, 2020). During the first phases of economic reform, state-owned companies (SOEs) had a prominent position in the corporate sector, with governance structures mostly under the supervision of government agencies (Chen & Zha, 2023). Nevertheless, during China’s shift towards a more market-oriented economy, significant measures were taken to enhance corporate governance standards. These measures included the creation of regulatory entities like the China Securities Regulatory Commission (CSRC) and the implementation of corporate governance guidelines for publicly traded companies (Lennox & Wu, 2022).

China has made significant progress in aligning its accounting and corporate governance systems with global standards despite cultural and institutional challenges (Shen & Ruan, 2022). In 2007, China adopted International Financial Reporting Standards (IFRS), which improved financial reporting quality and comparability (Guo & Krever, 2022). Legislation has also been passed to strengthen corporate governance, including board autonomy, transparency and disclosure, and corporate fraud and misconduct. Despite these advances, concerns remain concerning enforcement, state-owned enterprises, and corporate governance transparency and accountability. In conclusion, China’s accounting and corporate governance development shows its ongoing attempts to build an open, accountable, and investor-friendly business environment that promotes sustainable economic growth (Chen & Zha, 2023).

The Impact of Financial Reporting Quality on Stakeholder Trust

As it changes stakeholders’ opinions, decisions, and interactions within and outside firms, financial reporting quality affects their trust in the company (Velte, 2023). Quality financial reporting gives investors, creditors, regulators, and employees accurate, relevant, and reliable information about an organization’s financial performance and position. Clear and dependable financial records help stakeholders make educated investment, financing, and strategic partnership decisions, boosting corporate confidence and sentiment (Zhang, 2023). Low-quality financial reporting, distinguished by mistakes, omissions, or purposeful lies, weakens stakeholder trust, causing uncertainty, ambiguity, and reputation damage. False or misleading financial data undermines stakeholders’ faith in the organization’s management, honesty, and ability to fulfill obligations, compromising long-term relationships and viability (Zhang, 2023).

Furthermore, the confidence of stakeholders is not only dependent on the accuracy and dependability of financial reporting, but also on the perceived ethical standards, governance procedures, and openness shown by the business (Velte, 2023). Strong financial reporting is often a sign of strong internal controls, effective governance processes, and a dedication to ethical behavior, all of which enhance stakeholder confidence. Organizations that give high importance to openness, accountability, and integrity in their financial reporting procedures not only increase stakeholder trust but also create better relationships based on mutual respect and shared principles. Organizations may successfully manage risks, attract investment, and maintain long-term success in a competitive and dynamic business environment by promoting confidence via the use of high-quality financial reporting (Powell, 2023).

Challenges and Opportunities in Implementing Accounting Conservatism in China

Implementing accounting conservatism in China is influenced by the country’s distinctive economic, cultural, and regulatory environment, which poses both difficulties and prospects. A notable obstacle is the harmonization of traditional accounting concepts with the dominant corporate culture and practices in China (Du et al., 2022), which have traditionally emphasized rapid development and expansion. Resistance may be encountered when attempting to promote the use of conservative accounting techniques in an environment where market players emphasize short-term profits and aggressive financial reporting (Shen & Ruan, 2022). Moreover, the prevalence of state-owned companies (SOEs) in crucial areas of the economy and the impact of government policies may provide additional challenges in implementing conservatism. This is because strategic considerations and political objectives may deviate from conservative accounting procedures (Zhao, Hou, & Chen, 2020).

Nevertheless, accounting conservatism in China may promote long-term sustainability and fortitude in the face of economic volatility and market unpredictability. Conservative accounting approaches may better reflect an organization’s financial health, decreasing risks and financial instability (Li, 2020). In China’s quest of a more sustainable and balanced economic model, conservative accounting rules may promote attention, transparency, and accountability. This supports corporate governance and regulatory oversight measures (Jiang & Kim, 2020). As China becomes more connected to global markets and faces greater scrutiny from international investors and regulators, the importance of implementing globally recognized accounting standards (Guo & Krever, 2022), such as conservatism, to improve Chinese financial markets’ credibility and trustworthiness is growing.

Moreover, the changing regulatory environment in China (Lennox & Wu, 2022) offers prospects for promoting the use of accounting conservatism. The Chinese government has shown a dedication to improving financial transparency and corporate governance by implementing legislative changes and measures that try to harmonize local accounting standards with international norms (Gao, 2023). Regulators may promote firms to emphasize long-term wealth creation and risk management above short-term benefits by offering explicit instructions and incentives for adopting conservative accounting practices. Furthermore, as Chinese corporations extend their presence worldwide and strive to gain entry into international capital markets, there is a growing need to embrace cautious accounting methodologies in order to satisfy the demands of foreign investors and adhere to global reporting requirements (Lennox & Wu, 2022). Adopting accounting conservatism in China may help to building confidence, improving market stability, and encouraging long-term sustainable economic development.

Study Framework

The framework of the study is drawn from several established theories within the disciplines of accounting, finance, and corporate governance. The Agency Theory, the Positive Accounting Theory, the Institutional Theory, and the Stakeholder Theory served as the philosophical underpinnings for this research study.

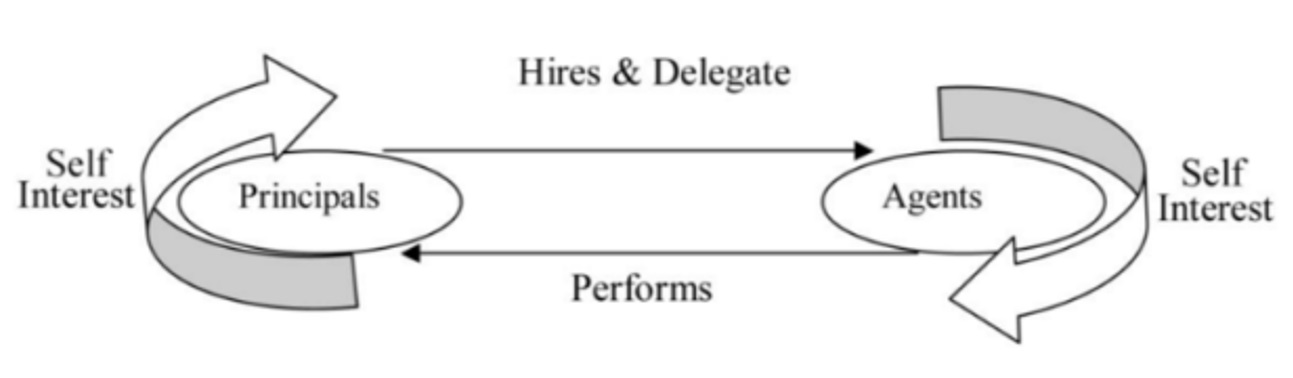

The Agency Theory, as explained in Murthy and Mutyala (2021), was first introduced by Alchian and Demsetz (1972) and further expanded upon by Jensen and Meckling (1976). It refers to the dynamics between principals, such as shareholders, and agents, such as firm executives and managers. This theory espouses that shareholders, who are the individuals or entities that own or have control over the firm, employ agents to carry out the tasks. Principals entrust the management of the firm to the directors or managers, who act as representatives of the shareholders (Clarke, 2004, as cited in Murthy & Mutyala, 2021). Using Agency Theory as a framework, this study looks at how conservative accounting practices may help bring together management and shareholders, leading to more reliable financial reporting and more confidence and trust from stakeholders.

Fig. 1 The Agency Theory (Adapted from Corporate Governance: Theory and Practice by Murthy & Mutyala, 2021)

The Positive Accounting Theory (PAT) is a theoretical framework that seeks to clarify the rationale behind accounting decisions and practices employed by accountants and managers, as well as the consequences of these actions on resource distribution and individuals. Developed by Watts & Zimmerman (1978, as cited in Mardessi & Fourati, 2021), the aim of this theory is to understand the accounting decisions made by managers during the preparation of financial statements, with a particular focus on choices related to profits. In this study, the Positive Accounting Theory was used as the basis for the analysis of accounting practices in the subject organizations of this research.

The Institutional Theory, introduced through the works of Meyer and Rowan (1977) and DiMaggio and Powell (1983), is widely recognized as the prevailing theory in the field of organizations, specifically focusing on the relationship between organizations and their external environment (Aksom & Tymchenko, 2020). The fundamental concept behind the Institutional Theory is that institutions emerge as a consequence of individuals’ construction of their social reality. When individuals engage in social interactions, several behavioral patterns emerge. In studies on sustainability reporting and reporting, Institutional Theory is often used in an effort to better understand how and why accounting and reporting have evolved into what they are or are not (Rimmel & Jonäll, 2020). In the context of this research study, Institutional Theory will serve as the basis for examining the impact of organizational elements on the implementation of conservative accounting procedures and corporate governance systems in Chinese companies.

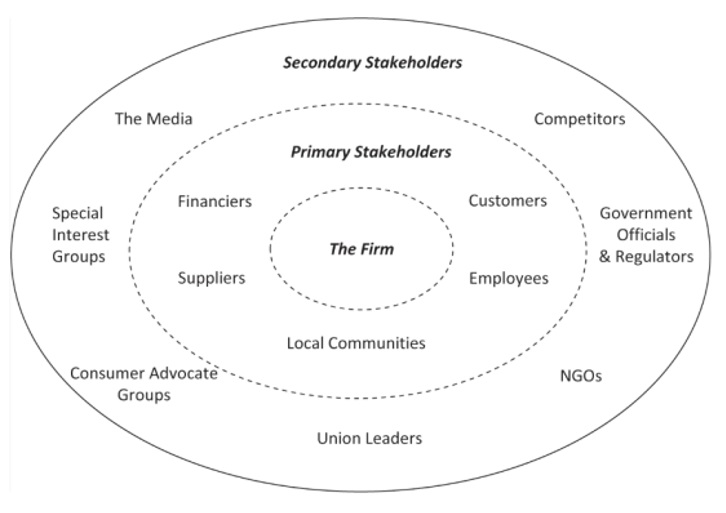

The Stakeholder Theory is based on a theoretical framework that asserts that businesses possess several stakeholders (Donaldson & Preston, 1995, as cited in Rimmel & Jonäll, 2020). Freeman (1984) defines a stakeholder as a group or individual who is affected by the organization’s actions or may influence them. Workers, customers, suppliers, shareholders, banks, environmental activists, and government officials are stakeholders. Each stakeholder may affect a corporation favorably or negatively (Rimmel & Jonäll, 2020). According to stakeholder theory, firms should prioritize protecting stakeholder interests and organize their company to optimize these interests for long-term performance (Şeker & Şengür, 2021). This study employed Stakeholder Theory to examine how accounting conservatism affects transparency, accountability, and responsiveness to stakeholders other than its shareholders.

Fig. 2 The Stakeholder Theory (Adapted from Cambridge University Press Published Online, 2018)

Conceptual Framework

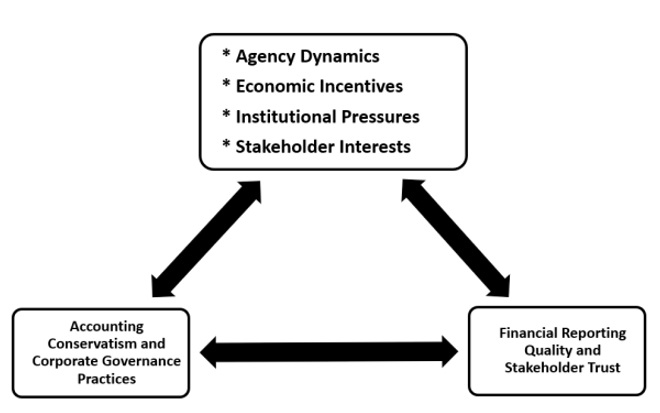

The research’s conceptual paradigm is focused on analyzing the impact of accounting conservatism and corporate governance on the quality of financial reporting and stakeholder trust in Chinese companies in Foshan City. Figure 3 illustrates how agency dynamics, economic incentives, institutional constraints, and stakeholder interests affect accounting conservatism and corporate governance practices, which have an impact on the quality of financial reporting and the level of confidence from stakeholders. This conceptual framework highlights the interaction between the different theoretical viewpoints mentioned in the section on the study framework and their consequences in the context of the Chinese business environment.

The research distinguishes accounting conservatism and corporate governance as separate factors while considering financial reporting quality and stakeholder trust as outcomes influenced by these factors. Guided by theories on positive accounting, stakeholder interests, intitutions, and agencies, this study aims to investigate the processes by which accounting conservatism and corporate governance impact financial reporting quality and stakeholder trust. Specifically, based on the perceptions of its respondents, the study sought to gain a thorough understanding of the following: (1) What is the extent of the practice of accounting conservatism and good corporate governance in Chinese businesses? (2) What is the perceived level of financial reporting quality and stakeholder trust in Chinese private enterprises? (3) What is the impact of accounting conservatism and good corporate governance on financial reporting quality and stakeholder trust in the Chinese business context? (4) What are the challenges and opportunities of adopting accounting conservatism and good corporate governance in the Chinese business context?

The research study covered select private enterprises in the manufacturing industry that are based in Foshan City, Guangdong, China. Through the insights provided by the participants of the study, it intends to achieve its primary goal, which is to determine how effective corporate governance and conservative accounting practices can work together to improve the quality of financial reporting and eventually increase stakeholder confidence in Chinese companies, particularly in Foshan City.

The research study in question is significant because it has the ability to clarify the critical interaction between effective corporate governance and accounting conservatism in forming stakeholder confidence in Chinese enterprises. Through an examination of the interplay and impact of these two principles, this study not only provides a valuable understanding of the mechanisms that drive financial reporting quality and stakeholder trust but also offers practical suggestions for organizations aiming to fortify their governance structures and improve transparency and accountability. Moreover, given China’s dynamic regulatory environment and growing focus on corporate governance reforms, the study’s conclusions can assist regulators, policymakers, and business professionals in advancing sustainable business practices and building industry confidence.

Fig. 3 The Conceptual Framework of the Study on the Influence of Accounting Conservatism and Corporate Governance on Financial Reporting Quality and Stakeholder Trust

METHODOLOGY

Research Design

The study used a mixed-methods research strategy, which combines quantitative and qualitative methodologies, to examine the correlation between accounting conservatism, corporate governance, financial reporting quality, and stakeholder confidence in Chinese companies. In Mertens (2023), mixed methods were referred to as the incorporation of both quantitative and qualitative methodologies within a single research project or a series of investigations. It combines closed-ended (quantitative) and open-ended (qualitative) data and utilizes the collective strengths of these data to comprehend research problems and form interpretations (Creswell, 2015, as cited in Watkins, 2022). Likewise, it also employs descriptive research with the objective of attaining a thorough comprehension of the topic being investigated (Watkins, 2022). In this study the quantitative part involves a survey of the perception of the subject companies regarding the extent of practice of accounting conservatism and strong corporate governance, the level of financial reporting quality and stakeholder trust, and the subsequent impact of accounting conservatism and strong corporate governance in financial reporting quality and stakeholder trust. The qualitative part of the study deals with identifying challenges and opportunities of adopting accounting conservatism and good corporate governance in the Chinese business context.

Population and Sampling

Foshan City is home to several private enterprises. Focusing on the manufacturing industry, particularly food, technology, and industrial sector, the study was able to purposely select the research subjects. There were 20 private (non-state-owned) small and medium enterprises that participated in the study through their nominated representatives, who are members of the top management and are knowledgeable in financial operations. Because the profiles of these companies are not the ones being studied, these 20 firms were anonymized in this research and are named in this study as Company 1 to Company 20.

Research Instrument

To facilitate the gathering of relevant data, the researcher constructed a survey questionnaire that includes narrative statements regarding the practice of accounting conservatism, the exercise of good corporate governance, and the impact of accounting conservatism and corporate governance on financial reporting quality and stakeholder trust. It utilized a 4-point Likert scale to determine the perceptions of the respondents regarding the extent of practice and adoption of accounting conservatism and corporate governance, as well as their impact on financial reporting quality and stakeholder trust. This approach was utilized because as explained by McLeod (2023), Likert scales treat perception data as a continuous line, with options like ‘strongly agree’ and ‘strongly disagree’ representing the extremes and suggests the idea that attitudes can be captured along this spectrum. For determining practices of accounting conservatism and corporate governance, the study made use of extent of practice to interpret the resulting scores. Likewise, for identifying the level, scores were interpreted from “very low” to “very high” level, such as in the case of stakeholder trust and financial reporting quality. This constitutes the quantitative part of the research study.

Moreover, functioning as the qualitative part of the study, the survey also included an open-ended question on the challenges and opportunities of adopting accounting conservatism and employing good corporate governance mechanisms. Themes that emerged from the qualitative responses were analyzed to determine the insights of the participants regarding challenges and opportunities of the subject matter being studied.

Data Gathering Procedure

Upon the consent of the top management of the enterprise respondents, the researcher requested the nomination of representatives, as these individuals are the ones who will answer the survey questionnaire. As soon as the company representative was identified, the survey questionnaire was handed to the respondent, including the provision of orientation regarding the objectives of the study and what the research intends to achieve.

Data Analysis

The collected data from the survey questionnaire was analyzed statistically (quantitative data) and thematically (qualitative data). Descriptive statistics and hypothesis testing were applied to the quantitative data to determine the collective responses of the participants particularly the research questions on extent of practice and level of stakeholder trust and financial reporting quality. On the other hand, thematic analysis was employed to identify the answers to the challenges and opportunities in employing accounting conservatism and employing good corporate governance mechanisms.

RESULTS AND DISCUSSIONS

Quantitative Analysis

In the analysis of quantitative data, the study employed descriptive statistics for determining the extent of accounting conservatism and corporate governance practices and level of financial reporting quality and stakeholder trust. Mean ranges were interpreted as follows: 1.00 – 1.75 (Very Low Extent/Level), 1.76 – 2.50 (Low Extent/Level, 2.51 – 3.25 (High Extent/Level), and 3.26 – 4.00 (Very High Extent/Level). Inferential statistics, such as hypothesis testing was used to ascertain the effect or impact of accounting conservatism and corporate governance to stakeholder trust and financial reporting quality.

Table I: Extent Of Accounting Conservatism Practices

| Factors | Mean | SD | Verbal Interpretation |

| Prudent income recognition. | 3.25 | 0.44 | High Extent |

| Cautious asset valuation. | 3.30 | 0.47 | Very High Extent |

| Disclosure of potential obligations. | 3.30 | 0.47 | Very High Extent |

| Provision for uncollectible debts. | 2.85 | 0.37 | High Extent |

| Financial adjustments to economic changes. | 2.85 | 0.49 | High Extent |

| Adoption of conservative accounting policies. | 3.35 | 0.49 | Very High |

| Composite Scores | 3.15 | 0.45 | High Extent |

The survey findings suggest that the firms investigated demonstrate a significant degree of adherence to accounting conservatism in several areas, with a composite score of 3.15±0.45 interpreted as “high extent.” Specifically, there is a significant focus on careful assessment of the value of assets (3.30±0.47), transparent reporting of possible liabilities (3.30±0.47), and the implementation of prudent accounting practices (3.25±0.44). Nevertheless, there is a degree of variability in the level of support for uncollectible debts (2.85±0.37) and financial modifications in response to economic fluctuations (2.85±0.49), suggesting that organizations may need to enhance their conservative policies (3.35±0.49) in these specific areas. All things considered, the results point to a generally favorable adherence of the surveyed companies to conservative accounting rules.

The study’s conclusions on accounting conservatism in the examined firms match prior researches. According to Shen and Ruan (2022), accounting conservatism functions as both an internal company governance system and an outward information transmission mechanism. Firms have less financial constraints when accounting conservatism grows. Thus, CEOs’ self-serving behavior and information asymmetry decrease. The research also found that accounting conservatism reduces wasteful expenditure allocation and leader self-interest, improving innovation efficiency. In another research, organizations were advised to improve system architecture, accounting information disclosure, and external audit supervision to increase accounting conservatism (Wang, Li, & Liu, 2021). They also believed that a robust accounting information disclosure system and good corporate governance may help the capital market thrive properly. Accounting conservatism may reduce unsustainable investments, especially in unique situations like China (Ma & Jeong, 2022).

TABLE II: Extent Of Corporate Governance Practices

| Factors | Mean | SD | Verbal Interpretation |

| Independent board with diverse expertise. | 3.25 | 0.44 | High Extent |

| Robust audit committee ensures financial credibility. | 2.85 | 0.49 | High Extent |

| Stakeholder accountability through communication. | 3.25 | 0.44 | High Extent |

| Strong internal control systems implemented. | 2.80 | 0.41 | High Extent |

| Ethical culture upheld with defined processes. | 3.25 | 0.44 | High Extent |

| Composite Scores | 3.08 | 0.45 | High Extent |

The survey findings show that the businesses examined exhibit a high level of adherence to corporate governance practices in many areas. The focus is primarily on autonomous boards of individuals with varied experience (3.25±0.44), ensuring responsibility to stakeholders via effective communication (3.25±0.44), and maintaining an ethical environment with well-defined procedures (3.25±0.44). While the audit committee’s credibility (2.85±0.49) is perceived slightly lower, it still reflects a high extent of implementation. Furthermore, it is stated that robust internal control mechanisms have been established to a significant degree (3.80±0.41). In general, the composite score (3.08±0.45) indicates a consistently high level of corporate governance processes in the companies that underwent assessment.

Zhou, Li, and Chen (2021) found a comparable relationship between corporate governance quality and financial leverage levels. The results also show the practice of Chinese corporate governance. According to Tricker and Li (2019), China’s corporate governance culture, economic ethics, and business-government ties are constantly changing. Chinese companies understood early on that corporate governance was essential for economic success and national prosperity (Tricker & Li, 2019).

TABLE III: Level Of Stakeholder Trust

| Indicators | Mean | SD | Verbal Interpretation |

| Investor Confidence | 3.15 | 0.37 | High Level |

| Stable Shareholder Base | 3.20 | 0.41 | High Level |

| Positive Market Reputation | 3.20 | 0.41 | High Level |

| Stakeholder Engagement | 3.30 | 0.47 | Very High Level |

| Ethical Conduct | 3.30 | 0.47 | High Level |

| Consistent Performance | 3.20 | 0.41 | Very Level |

| Composite Scores | 3.23 | 0.42 | High Level |

Table 3 shows the results of the survey on the level of stakeholder trust in the company based on the perception of the representative-respondents. Using indicators of investor confidence (3.15±0.37), stable shareholder base (3.20±0.41), positive market reputation (3.20±0.41), stakeholder engagement (3.30±0.47), ethical conduct (3.30±0.47), and consistent performance (3.20±0.41), the survey was able to determine whether stakeholders were more likely to trust the company or otherwise. Aside from the high level rating, two indicators, stakeholder engagement and ethical conduct scored “very high level,” with a composite mean score of 3.23±0.42 suggesting this is a “high level” of stakeholder trust. Overall, the study’s findings suggest a positive relationship between the company’s actions and stakeholder trust.

The positive scores across all indicators suggest that these private firms in Foshan City fosters a high level of stakeholder trust. Consistent with the Stakeholder Theory, its core principle is reinforced as these firms consider the interests of various stakeholders and acting responsibly, consequently building strong and trusting relationships that can ultimately benefit all parties involved.

TABLE IV: LEVEL OF FINANCIAL REPORTING QUALITY

| Indicators | Mean | SD | Verbal Interpretation |

| Accuracy | 3.40 | 0.50 | Very High Level |

| Consistency | 3.45 | 0.51 | Very High Level |

| Comparability | 3.50 | 0.51 | Very High Level |

| Minimal Errors and Restatements | 3.30 | 0.47 | Very High Level |

| Absence of Fraud | 3.55 | 0.51 | Very High Level |

| Disclosure Quality | 3.45 | 0.51 | Very High Level |

| Composite Scores | 3.44 | 0.50 | Very High Level |

Table 4 shows that the level of financial reporting quality of the company is very high, with a composite mean score of 3.44±0.50. This is because all the indicators which contribute to financial reporting quality have scores in the “very high level” range. These indicators include accuracy (3.40±0.50), consistency (3.45±0.51), comparability (3.50±0.51), minimal errors and restatements (3.30±0.47), absence of fraud (3.55±0.51), and disclosure quality (3.45±0.51). In general, the very high level of financial reporting quality suggests that stakeholders, such as investors, can have greater confidence in the accuracy and information provided by the company’s financial statements, thus, allowing them to make more informed investment decisions.

These findings all suggest that subject companies in Foshan City are strategically managing their financial disclosures to reduce information asymmetry. This transparency by minimizing errors, ensuring consistency, and providing high-quality disclosures allows stakeholders, particularly investors, to make more informed decisions. Thus, consistent with the Positive Accounting Theory, having high-quality financial reports can more likely to attract and retain investors due to the increased confidence in the information presented. This can translate to a lower cost of capital for the company, ultimately benefiting its financial performance.

TABLE V: Effect Of Accounting Conservatism and Corporate Governance to Stakeholder Trust and Financial Reporting Quality Based on Participants’ Perspectives

| Variables | X̄ | σ2 | t/F | p-value | VI |

| Accounting Conservatism

Corporate Governance |

3.15

3.08 |

0.06

0.08 |

1.77 | 0.046 | Significant Effect |

| Accounting Conservatism

Stakeholder Trust |

3.15

3.23 |

0.06

0.04 |

-1.34 | 0.098 | No Significant Effect |

| Accounting Conservatism

Financial Reporting Quality |

3.15

3.44 |

0.06

0.05 |

-3.52 | 0.001 | Significant Effect |

| Corporate Governance

Stakeholder Trust |

3.08

3.23 |

0.08

0.04 |

-2.06 | 0.026 | Significant Effect |

| Corporate Governance

Financial Reporting Quality |

3.08

3.44 |

0.08

0.05 |

-4.08 | 0.0003 | Significant Effect |

Using t-test, the results on the extent of practice of accounting conservatism and corporate governance, and the level of stakeholder trust and financial reporting quality have undergone inferential analysis. Table 5 identifies whether there is statistical significant effect of the variables of the study to one another. For accounting conservatism and corporate governance, the p-value (0.046) is significant, suggesting a positive effect of accounting conservatism on corporate governance. This entails that companies with more conservative accounting practices tend to have better corporate governance. In terms of accounting conservatism and stakeholder trust, the resulting p-value of 0.098 indicates that there is not enough evidence to conclude a clear effect of accounting conservatism on stakeholder trust based on this data. As for accounting conservatism and financial reporting quality, the p-value (0.001) is very significant, indicating a strong positive effect. companies with more conservative accounting likely produce higher quality financial reports. In the context of corporate Governance and Stakeholder Trust, the resulting p-value of 0.026 indicates that there is a significant positive effect. This means that companies with better corporate governance seem to have higher stakeholder trust. Finally, in terms of corporate governance and financial reporting quality, the p-value (0.0003) is highly significant, indicating a strong positive effect. This shows that better corporate governance is likely associated with higher quality financial reporting.

Overall, the results suggest that accounting conservatism, corporate governance, and financial reporting quality are interrelated and can positively influence each other. The results are very much aligned with Stakeholder Theory, as the findings highlights the interconnectedness of financial practices and stakeholder trust. While accounting conservatism does not directly impact stakeholder trust itself, it does contribute to higher quality financial reporting. This transparency, along with strong corporate governance, fosters trust among stakeholders by ensuring the accuracy of information used for decision-making process. Ultimately, this can be further reinforced by private enterprises in Foshan City and prioritize these practices to create a foundation for strong relationships with stakeholders, a key tenet of stakeholder theory.

Thematic Analysis

The second part of the survey questionnaire distributed to company representatives involve open-ended questions regarding challenges and opportunities in adopting accounting conservatism and practices good corporate governance. The responses of the participants have undergone thematic analysis and produced several relevant themes regarding the accounting conservatism and corporate governance practices.

TABLE VI: Challenges In Adopting Accounting Conservatism And Practicing Good Corporate Governance

| Theme | Description | Significant Statement | Inform-ant |

| Stakeholder Perception and Support | This theme underscores the challenges related to stakeholders’ concerns, and highlights the need for companies to engage with stakeholders effectively, educate them about the benefits of conservative practices and governance reforms, and build trust and confidence in the organization’s financial reporting and management practices. | Some reservation from shareholders regarding conservative practices | A |

| Lack of understanding of accounting conservatism’s benefits | B | ||

| Skepticism from investors regarding conservatism’s impact | K | ||

| Little support from stakeholders for governance initiatives | N | ||

| Operational Challenges | This theme is about the range of obstacles and difficulties that organizations face in adopting accounting conservatism and practicing good corporate governance. | Difficulty in balancing accounting conservatism with growth goals | C |

| Pressure to meet short-term financial targets | D | ||

| Limited resources for implementing governance frameworks | E | ||

| Complexity in identifying conservative accounting methods | G | ||

| Reluctance to change existing accounting practices | I | ||

| Inadequate training on conservative accounting principles | J | ||

| Challenges in aligning conservatism with industry norms | L | ||

| Balancing conservatism with maintaining competitiveness | M | ||

| Limited access to reliable financial data for conservatism | Q | ||

| Inconsistencies in applying conservatism across subsidiaries | R | ||

| Difficulty in measuring the effectiveness of governance practices | S | ||

| Regulatory and Compliance Issues | This theme is about the difficulties the surveyed companies encountered concerning adherence to regulatory standards and evolving requirements. | Compliance burden with evolving regulatory requirements | H |

| Organizational Culture and Govern-ance Structures | This theme highlights the need for organizations to address cultural barriers, manage conflicts of interest, promote transparency and disclosure, and foster a strong commitment to ethical standards and integrity to effectively navigate challenges in adopting conservatism and governance practices. | Cultural barriers to transparency and accountability | F |

| Conflicts of interest within board and management structures | O | ||

| Some reluctance to increased disclosure and transparency | P | ||

| Insufficient commitment to ethical standards and integrity | T |

Several important insights were revealed by the analysis of themes that were taken from the responses of the survey participants as regards the difficulties encountered while implementing excellent corporate governance and adopting accounting conservatism. First, it emphasizes the significance of stakeholder perception and support in effectively carrying out a task. The presence of reservations among investors and limited support from stakeholders highlights the need to use strong communication and engagement tactics to get approval for conservative policies and governance efforts. Furthermore, the operational issues that have been recognized, such as the struggle to maintain a balance between caution and the desire for expansion, the need to achieve immediate objectives, and the constraints of limited resources, highlight the practical obstacles encountered by companies. These problems highlight the need to find a middle ground between traditional procedures and long-term goals while investing sufficient resources to assure successful implementation. Moreover, the emergence of regulatory and compliance concerns poses substantial hurdles, especially the onerous task of staying abreast of ever-changing regulatory standards. This emphasizes the need to keep up-to-date with regulatory changes and adopt strong monitoring and enforcement systems to reduce risks related to non-compliance. Lastly, the corporate culture and governance structures are crucial in influencing the adoption of conservatism and corporate governance practices. The presence of cultural obstacles, conflicting interests, and a challenge to being open and honest highlight the need to further cultivate a culture that promotes accountability, openness, and ethical behavior within businesses.

In summary, the survey was able to highlight the complex and varied challenges encountered when adopting accounting conservatism and establishing effective corporate governance. To tackle these difficulties, it is necessary to adopt a comprehensive strategy that includes all relevant parties, aligning operations, complying with regulations, and promoting a supportive corporate culture. Organizations may improve their financial reporting quality, stakeholder trust, and long-term sustainability by properly handling these challenges.

TABLE VII: Perceived Opportunities In Adopting Accounting Conservatism And Practicing Good Corporate Governance

| Category | Description | Significant Statement | Inform-ant |

| Financial Stability and Risk Management | The theme encapsulates the potential benefits of adopting accounting conservatism and practicing good corporate governance in promoting financial stability, resilience, risk management, regulatory compliance, and integrity within organizations. | Enhanced financial stability and resilience. | A |

| Strengthened risk management practices. | D | ||

| Reduced exposure to regulatory scrutiny. | K | ||

| Better management of financial risks. | P | ||

| Better protection against financial misconduct. | H | ||

| Greater resilience to economic downturns. | M | ||

| Trust and Reputation | The theme emphasized possible opportunities in enhancing trust, transparency, credibility, and reputation within organizations, thereby fostering positive relationships with stakeholders and contributing to long-term sustainability and success. | Improved investor confidence and trust. | B |

| Increased transparency and accountability. | E | ||

| Enhanced credibility with stakeholders. | F | ||

| Improved relationships with lenders and creditors. | O | ||

| Enhanced reputation and brand value. | R | ||

| Business Growth and Competitive-ness | The theme is about promoting alignment with long-term goals, improving access to capital, attracting talent, enhancing competitiveness, driving stock performance, and fostering sustainable business growth. | Better alignment with long-term business goals. | C |

| Potential for improved access to capital. | G | ||

| Opportunity to attract quality talent. | I | ||

| Enhanced competitiveness in the marketplace. | J | ||

| Potential for improved stock performance. | L | ||

| Opportunity for sustainable business growth. | Q | ||

| Decision-Making and Adaptability | This theme undescores informed decision-making that ensures compliance with legal and regulatory requirements and enhancing organizational adaptability to changing market conditions. | Enhanced decision-making based on reliable data. | N |

| Improved compliance with legal and regulatory requirements. | S | ||

| Better ability to adapt to changing market conditions. | T |

The thematic analysis employed from the responses on perceived opportunities in taking on accounting conservatism and executing effective corporate governance discloses many significant observations. First, it highlights the need to maintain financial stability and manage risks as the main reasons for employing conservative accounting procedures and good corporate governance systems. The respondent firms acknowledge the opportunity to strengthen their ability to withstand economic downturns, reduce financial risks, and safeguard themselves from regulatory scrutiny by implementing strong governance systems and practicing cautious financial reporting. Furthermore, the prioritization of trust and reputation underscores the importance of stakeholder confidence in fostering business success. Organizations strive to bolster their image and brand value by adopting effective corporate governance processes and using conservative accounting standards. This is done to promote openness, accountability, and trust with shareholders and other stakeholders. Additionally, the acknowledgment of prospects for company expansion and competitiveness suggests that firms see the adoption of accounting conservatism and good corporate governance as catalysts for sustained success. Organizations may improve their competitive position in the marketplace and achieve sustainable development by aligning with strategic objectives, recruiting people, and accessing finance more efficiently. Lastly, the emphasis on decision-making and adaptability underscores the need for dependable data and adherence to regulatory mandates to promote efficient decision-making and enable organizational flexibility. Organizations may enhance their decision-making and effectively manage the dynamic business environment by following conservative accounting principles and good corporate governance norms.

Overall, the survey results highlight the many advantages that companies see when they embrace accounting conservatism and establish effective corporate governance mechanisms. Organizations may achieve greater financial stability, trustworthiness, competitiveness, and flexibility by properly addressing these possibilities. This, in turn, will lead to long-term value creation and success.

CONCLUSION

This study aims to investigate the practice, perceived effect, challenges, and opportunities of implementing accounting conservatism and strong corporate governance in Chinese enterprises, particularly those based in Foshan City. The subsequent conclusions were derived from the results of this study.

Chinese private enterprises have a general adherence to conservative accounting practices, coupled with consistent strong corporate governance processes. Chinese firm operations depend on accounting conservatism and corporate governance to improve suggesting commitment to financial transparency and responsible management.

Surveyed Chinese private enterprises in Foshan City reported a high level of stakeholder trust and a very high level of financial reporting quality, demonstrating accurate and informative financial statements that further foster stakeholder trust.

Chinese financial reporting in private enterprises is influenced by accounting conservatism and good company governance. Accounting conservatism and corporate governance promote high-quality financial reporting in Chinese private enterprises. Relatively, good corporate governance significantly affect stakeholder trust thereby helping private firms develop confidence and improve stakeholder relations.

The problems and prospects of as experienced by subject-companies in Foshan City on accounting conservatism and good corporate governance were recognized. Financial stability, risk management and decision-making processes, stakeholder confidence, and long-term competitiveness can be improved despite challenges in stakeholder perception and support, operational issues, regulation and compliance, and organizational culture and governance structures. Study results emphasize the need to solve challenges and seize opportunities to promote conservative accounting as well as sound corporate governance in Chinese private businesses.

Based on the findings and conclusions presented, the following recommendations may be considered:

Enhancing awareness and education. To increase financial reporting integrity and stakeholder trust, organizations can emphasize accounting conservatism and good corporate governance through awareness and education initiatives. This entails holding seminars and training programs to inform stakeholders regarding conservative accounting and effective governance.

Promoting the adoption of best practices. Organizations should further reinforce the adoption of accounting conservatism and corporate governance best practices. This involves strengthening internal control mechanisms, increasing transparency and accountability, and adapting governance structures to international standards to increase compliance and decrease regulatory risks.

Investing in resources and expertise. Companies should invest in specialized resources and abilities to address limited resources and expertise. This may include hiring conservative accounting and corporate governance specialists and employing technology to streamline processes.

Collaboration and knowledge sharing. Companies may evaluate and improve their accounting and governance procedures. Audits, assessments, and appraisals help identify areas for improvement and implement corrective actions. A culture of continuous improvement may boost resilience, competitiveness, and stakeholder trust in changing organizational environments.

REFERENCES

- Aguilera, R. V., Desender, K., & López-Puertas Lamy, M. (2021). Bridging accounting and corporate governance: New avenues of research. The International Journal of Accounting, 56(01), 2180001.

- Aksom, H., & Tymchenko, I. (2020). How institutional theories explain and fail to explain organizations. Journal of Organizational Change Management, 33(7), 1223-1252.

- Charles, A. (2023). The Effect of IFRS Adoption on Financial Reporting Quality; The Moderating Role of Corporate Governance. Kwame Nkrumah University of Science And Technology.

- Chen, K., & Zha, T. (2023). China’s Macroeconomic Development: The Role of Gradualist Reforms. MA: National Bureau of Economic Research.

- Christensen, D. S. (2023). The Seeds of Accounting Conservatism. European Journal of Business and Management Research, 8(2), 181-185.

- Du, X., Xie, Y., Lai, S., & Zeng, Q. (2022). Confucian culture and accounting conservatism: evidence from China. China Journal of Accounting Studies, 10(4), 549-589.

- El-habashy, H. A. (2019). The effect of corporate governance attributes on accounting conservatism in Egypt. Academy of Accounting and Financial Studies Journal, 23(3), 1-18.

- Gao, X. (2023). Digital transformation in finance and its role in promoting financial transparency. Global Finance Journal, 58, 100903.

- Guo, Y. M., & Krever, R. (2022). The Evolution of Accounting Standards in Modern China as a Reflection of the Country’s Challenging Shift to a Market Economy. Accounting Historians Journal, 49(1), 39-51.

- Hajawiyah, A., Wahyudin, A., Kiswanto, Sakinah, & Pahala, I. (2020). The effect of good corporate governance mechanisms on accounting conservatism with leverage as a moderating variable. Cogent Business & Management, 7(1), 1779479.

- Jiang, F., & Kim, K. A. (2020). Corporate governance in China: A survey. Review of Finance, 24(4), 733-772.

- Larcker, D., & Tayan, B. (2020). Corporate Governance Matters. FT Press.

- Lennox, C., & Wu, J. S. (2022). A review of China-related accounting research in the past 25 years. Journal of Accounting and Economics, 101539.

- Li, H. (2020). Business strategy, accounting conservatism and performance. Accounting and Finance Research, 9(2), 1-23.

- Ma, H., & Jeong, K. (2022). The effects of accounting conservatism on investment decision: Evidence from listed companies in China. Cogent Business & Management, 9(1), 2093484.

- Mardessi, S. M., & Fourati, Y. M. M. (2021). The Audit Committee as Component of Corporate Governance: The Case of the Netherlands. In Corporate Governance and Its Implications on Accounting and Finance (pp. 188-215). IGI Global.

- McLeod, S. (2023, July). Likert Scale Questionnaire: Examples & Analysis. Simply Psychology. https://www.simplypsychology.org/likert-scale.html.

- Mertens, D. M. (2023). Mixed Methods Research: Research Methods. United Kingdom: Bloomsbury Publishing.

- Murthy, K.S. & Mutyala, S. (2021). Corporate Governance: Theory and Practice. United Kingdom: KY Publications.

- Pasko, O., Chen, F., Birchenko, N., & Ryzhikova, N. (2021). Corporate governance attributes and accounting conservatism: Evidence from China. Studies in Business and Economics, 16(3), 173-189.

- Powell, G. (2023, August). The Crucial Role of Regular Accurate Financial Reporting for Business Success. LinkedIn. https://www.linkedin.com/pulse/crucial-role-regular-accurate-financial-reporting-business-powell.

- Rimmel, G., & Jonäll, K. (2020). Theories of accounting for sustainability. In Accounting for Sustainability (pp. 16-29). Routledge.

- Şeker, Y., & Şengür, E. D. (2021). The impact of environmental, social, and governance (esg) performance on financial reporting quality: International evidence. Ekonomika, 100(2), 190-212.

- Shen, Y., & Ruan, Q. (2022). Accounting Conservatism, R&D Manipulation, and Corporate Innovation: Evidence from China. Sustainability, 14(15), 9048.

- Solomon, J. (2020). Corporate Governance and Accountability. John Wiley & Sons.

- Velte, P. (2023). The link between corporate governance and corporate financial misconduct. A review of archival studies and implications for future research. Management Review Quarterly, 73(1), 353-411.

- Wang, Q., Li, X., & Liu, Q. (2021). Empirical research of accounting conservatism, corporate governance and stock price collapse risk based on panel data model. Connection Science, 33(4), 995-1010.

- Watkins, D. C. (2022). Secondary Data in Mixed Methods Research. United States: SAGE Publications.

- Zhang, H. (2023). Quality issues of corporate financial reports and their governance countermeasures [Chinese]. Journal of Project Management, 4(8), 133-135.

- Zhao, Y., Hou, R., & Chen, Y.(2020). Can accounting conservatism be contagious? ——Network centrality perspective [Chinese]. Foreign Economics and Management, 42(8).

- Zhou, M., Li, K., & Chen, Z. (2021). Corporate governance quality and financial leverage: Evidence from China. International Review of Financial Analysis, 73, 101652.