Affective Factors on Firm Value

- Putu Riska Wulandari

- Kadek Apriada

- M. Rudi Irwansyah

- 485-495

- Feb 4, 2023

- corporate governance

Affective Factors on Firm Value

Putu Riska Wulandari1, Kadek Apriada2, M. Rudi Irwansyah3

1Faculty of Dharma Duta, State Hindu University I Gusti Bagus Sugriwa Denpasar

2Faculty of Economic and Business, Mahasaraswati University, Indonesia

3Fakultas Ekonomi, Universitas Pendidikan Ganesha, Indonesia

Abstract

The performance of the company determines the stock price, which is determined by supply and demand on the capital market and represents how the general public perceives the performance of the company. The issue with firm value, namely the volatility of share prices, which is a reflection of the unstable value of the business. The purpose of this study is to examine the impact of the investment opportunity set, excellent corporate governance, corporate social responsibility, and sustainability report on the stock value of manufacturing businesses listed on the Indonesia Stock Exchange from 2017 to 2019. Manufacturing businesses registered on the Indonesia Stock Exchange from 2017 to 2019 make up the research population. Based on the purposive selection method, the study’s sample of 46 companies was selected. This study employed multiple linear regression analysis as its analysis method. The outcomes demonstrated that the collection of investment opportunities had a favorable impact on business value. The value of a company is unaffected by good corporate governance, CSR, or sustainability reports.

Keywords— Investment opportunity set, good corporate governance, corporate social responsibility, sustainability report, and firm value

Introduction

The company is a production organization that employs and coordinates financial resources to meet needs in a successful manner (Swastha, 2002). By maximizing the company’s or firm’s worth, every business aims to boost the wealth of its owners. The company’s performance is represented in the share price, which is determined by supply and demand on the capital market and represents how society views the performance of the company (Harmono, 2009). The issue with a company’s value is its unstable value, which is reflected in its fluctuating stock price. Capital searchers and investors congregate on the capital market. The stock exchange is a type of capital market where adequate analysis of financial data must be done in order to determine precisely how the company’s state is. In the field, conditions often occur that are not in accordance with reality, with the enactment of the agency problem (theory), agency theory, according to Anthony and Govindarajan (2011), is the connection or interaction between the principle and the agent. The principal hires the agent to carry out activities for the principal’s benefit, including giving the agent permission to make decisions. Meiser et al. (2006) assert that this agency link leads to the following two issues. The fisrt is the occurrence of information asymmetry, when management typically has more knowledge than the owner about the actual financial situation and position of the organization. Second, the occurrence of conflicts of interest (conflict of interest) brought on by opposing goals, in which case management does not always act in the owner’s best interests to be presented in the financial statements. Financial statement or reports, according to Fahmi (2011), are information that reflect a company’s financial state and that can also be used to describe the company’s financial performance. Financial reports can also be utilized as a source of information to forecast future business performance.

The set of investment opportunities is one of the elements that might impact firm value (IOS). IOS is a range of potential future investment possibilities that may have an impact on the development of corporate assets or initiatives with a positive net present value. IOS therefore plays a crucial function for the company because it is an investment choice that affects the value of a company by combining current assets with potential future investments. In other words, good corporate governance is a system that regulates and controls businesses. It consists of a set of rules governing the relationship between shareholders, company managers, creditors, the government, employees, and other internal and external interest holders regarding rights and obligations (Sutedi, 2006). GCG is one of the variables that affects firm value, hence updating business performance is essential. Corporate social responsibility (CSR) is another element that affects how valuable a company is. CSR is a type of corporate responsibility that shows care for society and the environment. According to ISO 26000 (in Rusdianto, 2013) CSR is defined as an organization’s duty to consider how its actions and decisions will affect society and the environment through openness and morality that is consistent with social welfare and sustainable development, taking stakeholder interests into account, and that is integrated into all organizational activities, including both activities and the production of goods and services.

Through the use of sustainable management, which is reported by all relevant parties, the company can draw in investors by demonstrating to them how its strategy and operations are sustainable in a number of different ways. Companies must produce sustainability reports that serve as a means of reporting to stakeholders regarding their corporate responsibility. A corporation or organization’s sustainability report examines the effects of its operations on the economy, society, and the environment (GRI, 2013). A nonprofit organization that supports economic sustainability is the Global Reporting Initiative (GRI). Environmental Social Governance (ESG) Reporting, Triple Bottom-Line (TBL) Reporting, and Corporate Social Responsibilities (CSR) Reporting are just a few of the sustainability reporting standards produced by GRI that are frequently utilized by businesses throughout the world. The G4 Guidelines were formally announced in May 2013 by the Global Reporting Initiative (GRI). According to Melewar (2008), signaling theory demonstrates that businesses will send signals through their actions and communications. Companies use these signals to disclose to stakeholders hidden characteristics. In essence, signal theory also explains how financial reports are utilized to send their owners either good or negative signals.

Whether the investment opportunity set, excellent corporate governance, corporate social responsibility, and sustainability report affect the business value listed on the Indonesia Stock Exchange in 2017–2019 is the issue that will be examined in this research. The performance of the company determines the share price, which is determined by supply and demand on the capital market and represents how the public views the company’s success (Harmono, 2009). High stock prices raise a company’s value and boost investor confidence in the company’s future prospects. Ratios referred to as valuation ratios, such as Price Book Value and Tobin’s Q, can be used to calculate a company’s value. This study aims to evaluate the impact of investment opportunity set, excellent corporate governance, corporate social responsibility, and sustainability reports on firm values listed on the Indonesia Stock Exchange in 2017–2019. This research was re-conducted based on the components that affect company value because there are discrepancies in the research gap issue or different research findings from prior studies. Differences in parameters that showed to have an impact on one study but not necessarily on other studies were the reason of the inconsistent findings of earlier studies. It is anticipated that the study’s findings will add to the body of knowledge regarding the variables that affect business value.

Hypothesis of research

Investment Opportunity Set’s (IOS) impact on firm value

The term “Investment Opportunity Set” (IOS) refers to a description of the variety of investment options or business chances (Hartono, 2003). IOS is a business that uses its net profit differently. The Market to Books Value of Assets (MBVA) ratio, which measures investments in the form of assets used by businesses, is employed in this study to calculate IOS. In order to increase the value of the company in the eyes of investors and the company, investments in the form of assets increase investors’ interest in investing their capital. According to studies by Astriani (2014), Hidayah (2015), Darmayanti (2016), and Dewi (2019), the set of investment opportunities has a favorable impact on the value of the company. This implies that the business value will be better and higher the better or higher the investment opportunity set. The following is how the hypothesis is put forward in light of the aforesaid theoretical foundation and justification:

H1: Investment opportunity set (IOS) has an impact on firm value.

Good corporate governance’s (GCG) impact on firm value

In other words, good corporate governance is a system that regulates and controls businesses. It is a set of laws that govern the interaction between shareholders, firm management, government creditors, employees, and other internal and external stakeholders in terms of rights and obligations (Sutedi, 2006). Investors can identify companies that effectively apply GCG when the company’s control system can be trusted and the company is transparent, increasing investor confidence in the company and its worth. According to studies by Retno (2012), Randy (2013), Syafitri (2018), and Dewi (2019), effective corporate governance increases the value of a company. This implies that the business value will be better and higher the better or higher the value of strong corporate governance. The following is how the hypothesis is put forward in light of the aforesaid theoretical foundation and justification:

H2: good corporate governance (GCG) has an impact on firm value.

Corporate Social Responsibility’s (CSR) Impact on Firm Value

Corporate social responsibility (CSR) is the responsibility of an organization for the impact of its decisions and actions on society and the environment through transparent and ethical behavior that is consistent with sustainable development and community welfare, taking into account the interests of stakeholders, in compliance with applicable law and consistent with international norms, integrated in all organizational activi (Rusdianto, 2013). When making decisions within the firm, numerous social and environmental concerns must be taken into account in order to maximize long-term financial performance, which may later boost the company’s worth. The higher the quality and quantity of a company’s social disclosure concepts, the more valuable the company will be. CSR has a beneficial impact on company value, according to studies by Retno (2012), Herwiyanti (2015), Monica (2018), and Dewi (2019). This implies that the business value will be better and higher the better or higher the value of corporate social responsibility. The following is how the hypothesis is put forward in light of the aforesaid theoretical foundation and justification:

H3: The value of a firm is positively impacted by corporate social responsibility (CSR).

A Sustainability Report’s (SR) impact on a company’s value

A sustainability report is described as a public report by a corporation to give internal and external stakeholders an overview of the company’s position and operations on economic, environmental, and social aspects by Heemskerk, Pistorio, and Scicluna (2002:7). A corporation’s obligation to its stakeholders is demonstrated by the publication of a sustainability report, and investors will be more confident in a company with a sustainable mission that can enhance firm value. The purpose of the company’s sustainability report is to entice investors to purchase company stock. The company seeks to improve firm value by raising the number of outstanding shares and the stock price. The sustainability report has a favorable impact on firm value, according to studies by Sujati (2014), Fatchan (2016), Latifah (2017), Maskat (2018), and Siregar (2019). This implies that the firm value will be greater and higher the better or higher the value of the Sustainability Report.

The following is how the hypothesis is put forward in light of the aforesaid theoretical foundation and justification:

H4: A sustainability report enhances the value of the firm.

Method

In an effort to support the research premise, this study was designed using a quantitative methodology. The population in this study consisted of all 182 manufacturing businesses that were listed and listed (go public) on the Indonesia Stock Exchange (IDX) between 2017 and 2019. Purposive sampling, or sampling with specific criteria, was used to carry out the sampling. The following list of sample criteria is used in this study:

- Between 2017 and 2019, every manufacturing company listed on the Indonesia Stock Exchange

- Businesses in the manufacturing sector whose 2017–2019 financial reports are accessible

- Manufacturing firms with comprehensive data for the factors examined from 2017 to 2019.

In accordance with the aforementioned sampling criteria, 46 of the 182 companies examined between 2017 and 2019 presented full financial disclosures on the Indonesia Stock Exchange. 138 corporate data observations were made in total.

This study employed a documentation study to gather secondary data from the financial reports of manufacturing companies listed on the Indonesia Stock Exchange for the years 2017 through 2019; these reports may be accessible on the website www.idx.co.id. The acquired data was then examined using the Regression Linier Analysis following analytical techniques in an effort to address the study question.

The relationship between the independent (independent) variables and the dependent (dependent) variable is explained using multiple linear regression analysis Ghazali (2018:95). Based on the developed hypothesis, the regression equation has the following form:

NP = a + B1 IOS + B2 GCG + B3 CSR + B4 SR + E …. (1)

Description formula

NP : Firm Value

a: contstant

B1-B4: coefficient of regression

IOS: Investment Opportunity Set

GCG: Good Corporate Governance

CSR : Corporate Social Responsibility

SR: Sustainability Report

E: Error

Result and Discussion

The study’s findings indicate that each variable’s standard deviation value is less than the mean, indicating that the data are good. This is because the standard deviation is a reflection of a very high deviation, ensuring that the distribution of the data displays normal results and does not introduce bias, as shown in Figure 1.

Table 1 Data Description

The results of data collection were carried out by prerequisite regression tests including normality tests, multicollinearity tests, heteroscedasticity tests and autocorrelation tests. The test results can be seen in table 2, table 3, table 4 and table 5 respectively.

Table 2 Result of Normality test

The Asymp. Sig (2-tailed) is 0.084 > 0.05, which indicates that the residual data is normally distributed or that the assumption of normality is satisfied, according to the results of the normality test in Table 2 using the Kolmogorov-Smirnov Test technique.

Table 3 Result of Multicollinearity test

Based on the results in table 3, the tolerance coefficient is greater than 0.10 and VIF is less than 10. This means that the variable investment opportunity set, good corporate governance, corporate social responsibility, and sustainability report on the firm value used does not occur multicollinearity and the model regression is feasible to use.

Table 4 Result of Autocorelation test

The test results reveal that the dw value is 1.894, where the du value is derived from the Durbin Watson statistical table with 138 observations (n) and the number of independent variables (k) being 4, and the autocorrelation test results are obtained using the criterion du dw (4-du) is 1.7819 1.902 2.2181. These findings demonstrate the absence of autocorrelation in the constructed regression model.

Table 5 Result of Heterocedasticity test

The significant value of each independent variable is more than 0.05, which may be explained by the heteroscedasticity test results in Table 5 above. This result indicates that there is either no heteroscedasticity or the variance in the regression model is the same from one test to the next.

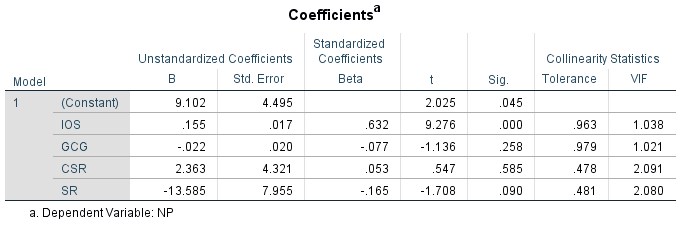

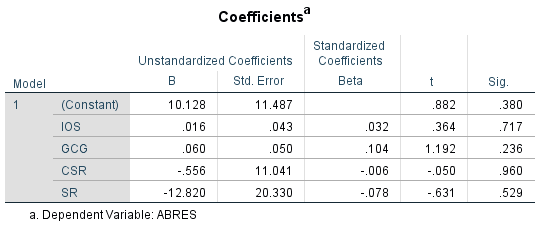

According to Table 3, the constant value () is 9.102, the regression coefficients (r1), (r2), (r3), and (r4) are each 0.0155, -0.022, 2.363, and 13.585 respectively. The equations for the multiple linear regression model can be constructed using the values of the constants and regression coefficients as follows:

NP = 9,102 + 0,0155 IOS – 0,022 GCG + 2,363 CSR – 13,585 SR

Description formula

NP: Firm Value

a: contstant

B1-B4: coefficient of regression

IOS: Investment Opportunity Set

GCG: Good Corporate Governance

CSR : Corporate Social Responsibility

SR: Sustainability Report

E: Error

As can be seen from the results of the multiple linear regression equation, a constant value () of 9.102 indicates that the firm value will be 9.102 percent if the independent variables, which are the investment opportunity set (IOS), good corporate governance (GCG), corporate social responsibility (CSR), and sustainability report (SR), are equal to zero. With a regression coefficient value of 0.155 and a significance level of 0.000 less than 0.05, the investment opportunity set variable (IOS) has a positive impact on company value. Accordingly, the firm value will increase by 0.155 percent if the IOS variable grows by one percent and the other variables remain unchanged. With a regression coefficient of -0.022 and a significance level of 0.258 higher than 0.05, the good corporate governance (GCG) variable had no impact on business value. Corporate social responsibility (CSR) has no effect on business value, as evidenced by the variable’s regression coefficient value of 2.363 and significance level of 0.585 greater than 0.05. As CSR has no impact on company value, the variable sustainability report (SR) has a regression coefficient value of -13.585 and a significance level of 0.090 greater than 0.05.

The analysis’ findings demonstrate that the investment opportunity set has a favorable impact on business value, supporting H1’s acceptance. IOS is a business that uses its net profit differently. The ratio of market value to books of assets (MBVA), which measures investment in the form of assets used by businesses, is employed in this study to measure IOS. Investment in the form of assets increases investors’ desire in making capital investments, raising the business’s value in their eyes and the company’s perceived quality, both of which help to raise firm value. According to studies from Astriani (2014), Hidayah (2015), Darmayanti (2016), and Dewi (2019), the investment opportunity set has a favorable impact on business value.

Variable good corporate governance has no effect on firm value, so H2 is rejected. This can be taken to suggest that the company’s GCG index score has no bearing on its ability to increase firm value, and that there is no additional economic benefit to be gained from being named “The Indonesia Most Trusted Company – based on CGPI.” The components of the CGPI calculation do not require a third party, such as a public accounting firm, such that external oversight determines if the company’s performance is excellent or bad, hence GCG has no impact on firm value. Investors will be less interested in viewing it from a GCG viewpoint as a result. The findings of this study conflict with those of Retno (2012), Randy (2013), and Syafitri (2018), whose studies found that strong corporate governance enhances business values. The findings of this study, however, are consistent with those of studies by Herwiyanti (2015) and Fatchan (2016), which found no relationship between excellent corporate governance and business value.

H3 is disproved by the findings of the analysis of the CSR variable, which demonstrate that corporate social responsibility has no impact on business value. According to the Limited Liability Corporation Law No. 40 of 2007, a company must engage in CSR and report it because failing to do so could result in legal repercussions. As a result, firm value is unaffected by CSR disclosure. This study’s findings contradict those of studies by Retno (2012), Herwiyanti (2015), and Dewi (2017), which found that corporate social responsibility enhances firm values. The findings of this study, however, are consistent with those of a study by Ardimas (2015) that found no connection between corporate social responsibility and firm values.

H4 is rejected since it is clear from the criterion that the sustainability report has no impact on the firm value. The disclosure of sustainability reports by businesses is not an investor’s evaluation because sustainability reports have no impact on company value and investors typically are not aware of or understand them. The findings of this study conflict with those of Sejati (2014), Fatchan (2016), and Latifah (2017), whose studies found that sustainability reports increase firm value. The findings of this study, however, concur with those of a study by Habibi (2018) that found no connection between sustainability reports and business value.

Conclusion

This study looks at the impact of sustainability report, excellent corporate governance, corporate social responsibility, and investment opportunity set on business value. Investing opportunity sets have a positive impact on firm value, whereas good corporate governance, corporate social responsibility, and sustainability reports have no impact on firm value, according to research findings obtained through statistical testing and discussion as described in the previous chapter.

The three-year observation duration and utilization of a manufacturing business are the study’s limitations and recommendations (2017-2019). To widen the scope of the research findings, future researchers will likely lengthen the observation period and use more samples. It is anticipated that future study would expand and diversify the independent variables considered, such as environmental performance, firm size, and solvency.

References

- Agoes, Sukrisno 2011. Etika Bisnis Dan Profesi: Tantangan Membangun Manusia Seutuhnya, Jakarta: Salemba Empat

- Agraheni Niken Susanti, Rahmawati, Y. Anni Aryani. 2010. Analisis Pengaruh Corporate Governance Dengan Kualitas Laba Sebagai Variabel Intervening Pada Perusahaan Manufaktur Yang Terdaftar di Bursa Efek Indonesia Periode 2004-2007. Simposium Nasional Keuangan I Tahun 2010

- Andreas, Lako. 2014. Dekonstruksi CSR dan Reformasi Paradigma Bisnis dan Akuntansi. Jakarta: Erlangga.

- Ardimas, W., dan Wardoyo, W. (2015). Pengaruh Kinerja Keuangan Dan Corporate Social Responsibility Terhadap Nilai Perusahaan Pada Bank Go Public Yang Terdaftar Di BEI. Benefit: Jurnal Manajemen dan Bisnis, 18(1), 57-66.

- Arthur J. Keown, 2008, Manajemen Keuangan, Edisi 10, Jakarta: PT macanan Jaya Cemerlang

- Astriani, E. F. (2014). Pengaruh kepemilikan manajerial, leverage, profitabilitas, ukuran perusahaan dan investment opportunity set terhadap nilai perusahaan. Jurnal Akuntansi, 2(1).

- Brigham, Eugene F, dan Joel F. Houston. 2014. Dasar-Dasar Manajemen Keuangan. Buku 1. Edisi 11. Jakarta : Salemba Empat.

- “Corporate Governance” dan “Good Corporate Governance”. IICG. 16 November 2009. www.iicg.or.id.

- Dewi, K. R. C., dan Sanica, I. G. (2017). Pengaruh kepemilikan institusional, kepemilikan manajerial, dan pengungkapan corporate social responsibility terhadap nilai perusahaan pada perusahaan manufaktur yang terdaftar di bursa efek indonesia. Jurnal Ilmiah Akuntansi dan Bisnis, 2(1), 231-246.

- Dewi, N. L. Gd. Rustina. (2019). Pengaruh Corporate Social Responsibility, Good Corporate Governance, Investment Opportunity Set dan Profitabilitas Terhadap Nilai Perusahaan Pada Perusahaan Manufaktur Yang Terdaftar Di BEI. Skripsi. Universitas Mahasaraswati: Denpasar

- Fahmi, Irham, 2011, Analisis Laporan Keuangan, Bandung: Alfabeta.

- Fatchan, I. N., dan Trisnawati, R. (2018). Pengaruh Good Corporate Governance Pada Hubungan Antara Sustainability Report dan Nilai Perusahaan (Studi Empiris Perusahaan Go Public di Indonesia Periode 2014-2015). Riset Akuntansi Dan Keuangan Indonesia, 1(1), 25-34.

- Fatimah, F., Mardani, R. M., dan Wahono, B. (2019). PENGARUH GOOD CORPORATE GOVERNANCE TERHADAP NILAI PERUSAHAAN DENGAN KINERJA KEUANGAN SEBAGAI VARIABEL INTERVENING (Studi Kasus Pada Perusahaan Manufaktur Sektor Barang. Jurnal Ilmiah Riset Manajemen, 8(15).

- Fitri, Riana dan Eliada, Herwiyanti. 2015. Pengaruh Good Corporate Governace dan Corporate Social Responsibility Terhadap Nilai Perusahaan. Jurusan Akuntansi FEB Universitas Jendral Soedirman.

- Global Reporting Initiative (GRI). 2013. G4 Sustainability Reporting Guidelines-Reporting Principles and Standard Disclosures. Amsterdam.

- Ghozali, Imam. 2018. Aplikasi Analisis Multivariate dengan Program IBM SPSS 25. Badan Penerbit Universitas Diponegoro: Semarang

- Gitman, Lawrence J, 2006. Principles of Managerial Finance. USA, Pearson.

- Hadi, Nor. 2011. Corporate Social Responsibility. Cet.Pertama. Yogyakarta: Graha Ilmu.

- Harmono,2009, Manajemen Keuangan : Berbasis Blanced Scorecard, Jakarta : Bumi Aksara.

- Heemskerk, B., Pistorio, P. dan Scicluna, M. (2002, December). Sustainable Development Reporting Striking the Balance. World Business Council for Sustainable Development, 1-61.

- Hermuningsih,Sri.2013. “ Pengaruh Profitabilitas,Growth Opportunity,Struktur Modal terhadap Nilai Perusahaan pada Perusahaan Publik Indonesia”. Buletin Ekonomi Moneter dan Perbankan,Edisi Oktober 2013.

- Hidayah, N. (2015). Pengaruh Investment Opportunity Set (Ios) Dan Kepemilikan Manajerial Terhadap Nilai Perusahaan Pada Perusahaan Property Dan Real Estat Di Bursa Efek Indonesia. Jurnal Akuntansi, 19(3), 420-432.

- Ikatan Akuntansi Indonesia, 2009, Standar Akuntansi Keuangan, PSAK No.1: Penyajian Laporan Keuangan, Jakarta: Salemba Empat.

- Ikatan Akuntan Indonesia. 2015. Pernyataan Standar Akuntansi Keuangan. Jakarta : Ikatan Akuntan Indonesia.

- I Made Sudana. 2011. Manajemen Keuangan Perusahaan Teori dan Praktik. Jakarta: Erlangga

- Imam Sjahputra Tunggal dan Amin Widjaja Tunggal. 2012. Membangun Good Corporate Governance. Jakarta: Harvarindo.

- Jogiyanto Hartono. 2003. Teori Portofolio dan Analisis Investasi. Yogyakarta: BPFE

- Kasmir, 2014. Analisis Laporan Keuangan, Edisi Pertama, Cetakan Ketujuh. Jakarta: PT. Rajagrafindo Persada.

- Keputusan Direksi PT Semen Baturaja (Persero) Tbk Nomor : PH. 01. 04/ 180/ 2013 Tentang Perubahan atas Surat Keputusan Direksi PT Semen Baturaja (Persero) Nomor : PH. 01. 04/ 034 /2012 Tentang Buku Pedoman Good Coroporate Governance (GCG) PT Semen Baturaja (Persero)

- Latifah, S. W., dan Luhur, M. B. (2017). Pengaruh Pengungkapan Sustainability Report terhadap nilai perusahaan dengan profitabilitas sebagai pemoderasi. Jurnal Akuntansi dan Bisnis, 17(1), 13-18.

- Mahendra, K. Oky. T. (2018). Faktor-faktor yang mempengaruhi nilai perusahaan pada perusahaan pertambangan yang terdaftar di bursa efek inonesia tahun 2013-2017. Skripsi. Universitas Mahasaraswati:Denpasar.

- Mardiyanto, H. (2008). Intisari Manajemen Keuangan: Teori, Soal, dan Jawaban. Jakarta: Grafika.

- Maskat, A. (2018). Pengaruh Sustainability Report Terhadap Kinerja dan Nilai Perusahaan (Studi Empiris pada Perusahaan Sektor Pertambangan (mining) yang Terdaftar di Bursa Efek Indonesia tahun 2011-2016).

- Monica dan N. N. Aprilia. K. (2018). Pengaruh corporate social responsibility dan intellectual capital pada nilai perusahaan (Studi Empiris Pada Perusahaan Manufaktur Yang Terdaftar di BEI Tahun 2015-2017) Skripsi. Universitas Mahasaraswati:Denpasar.

- Muliaman. D. Hadad dan Istiana Muftuchah. 2015. Sustainable Financing. Jakarta: PT Elex Media Komputindo

- Randy, V. (2013). Pengaruh Penerapan Good Corporate Governance terhadap Nilai Perusahaan 2007-2011. Business Accounting Review, 1(2), 306-318.

- Retno, R. D., dan Priantinah, D. (2012). Pengaruh good corporate governance dan pengungkapan corporate social responsibility terhadap nilai perusahaan (studi empiris pada perusahaan yang terdaftar di Bursa Efek Indonesia periode 2007-2010). Nominal: Barometer Riset Akuntansi dan Manajemen, 1(2), 99-103.

- Rifqiah, A., Mahsuni, A. W., dan Hariri, H. (2020). PENGARUH KINERJA KEUANGAN DAN GOOD CORPORATE GOVERNANCE TERHADAP NILAI PERUSAHAAN (Studi Empiris Pada Perusahaan Food and Beverage Yang Terdaftar di Bursa Efek Indonesia Periode 2016-2018). Jurnal Ilmiah Riset Akuntansi, 9(01).

- Rusdianto, Ujang (2013). CSR Communication A Framework for PR Practitioners. Yogyakarta: Graha Ilmu.

- Sari, N. A., Artinah, B., dan Safriansyah, H. (2017). Sustainability Report Dan Nilai Perusahaan Di Bursa Efek Indonesia. JURNAL ILMIAH BISNIS dan KEUANGAN, 7(1), 21-30.

- Sejati, B. P., dan Prastiwi, A. (2015). Pengaruh pengungkapan sustainability report terhadap kinerja dan nilai perusahaan. Diponegoro Journal of Accounting, 195-206.

- Siregar, N. Y., dan Safitri, T. A. (2019). PENGARUH PENGUNGKAPAN ENTERPRISE RISK MANAGEMENT, INTELLECTUAL CAPITAL, CORPORATE SOCIAL RESPONSIBILITY, DAN SUSTAINABILITY REPORT TERHADAP NILAI PERUSAHAAN. Jurnal Bisnis Darmajaya, 5(2), 53-79.

- Sudiani, N. K. A., dan Darmayanti, N. P. A. (2016). Pengaruh profitabilitas, likuiditas, pertumbuhan, dan investment opportunity set terhadap nilai perusahaan. E-Jurnal Manajemen Universitas Udayana, 5(7).

- Sugiyono. (2018). Metode Penelitian Kuantitatif. Bandung: Alfabeta.

- Surat Keputusan Menteri BUMN Nomor Kep-117/M-MBU/2002 Tanggal 1 Agustus 2002 Tentang penerapan GCG, Jakarta.

- Swastha, Basu, dan Ibnu Sukotjo W, 2002, Pengantar Bisnis Modern, Edisi Ketiga, Liberty. Yogyakarta

- Syafitri, T., Nuzula, N. F., dan Nurlaily, F. (2018). Pengaruh Good Corporate Governance Terhadap Nilai Perusahaan (Studi pada perusahaan industri sub sektor logam dan Sejenisnya yang terdaftar di bei periode 2012-2016). Jurnal Administrasi Bisnis, 56(1), 110-117.

- Syifa. 2015. Pengaruh Investment Opportunity Set (IOS), Kepemilikan Institusional, Komisaris Indepenen, Dan Return On Investment (Roi) Terhadap Nilai Perusahaan Pada Perusahaan Manufaktur Yang Terdaftar Di Bursa Efek Indonesia. Skripsi. Universitas Negeri Yogyakarta

- Widhi, N. M. Astari. D (2018). Pengaruh corporate governance dan kinerja keuangan terhadap nilai perusahaan (Studi Empiris Pada Perusahaan Yang Terdaftar di Bursa Efek Inonesia Tahun 2013-2017). Skripsi. Universitas Mahasaraswati:Denpasar