An Evaluation of Factors that Influence the Adoption of Mobile Money Services by Zambain Univsersity Students. A Case of ZCAS University

- Jackson sishumba

- John Mapalo Mulenga

- Loti Saidi

- 2616-2639

- May 22, 2024

- Education

An Evaluation of Factors that Influence the Adoption of Mobile Money Services by Zambain Univsersity Students. A Case of ZCAS University

Jackson sishumba1, John Mapalo Mulenga2, Loti Saidi3

ZCAS University

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804252

Received: 26 March 2024; Revised: 07 April 2024; Accepted: 12 April 2024; Published: 22 May 2024

ABSTRACT

Mobile money services in Zambia, like in many other African countries, have been experiencing a significant growth in their user base. According to Bank of Zambia records, the value of mobile money transactions in 2023 skyrocketed by an astonishing 52.8%, reaching a staggering K452.0 billion. This remarkable statistic serves as evidence of acceptability and adoption of digital financial services among Zambian consumers. The mobile money services were deemed to be financial services for the poor and unformalized business communities, surprisingly, with the passage of time mobile services have gained so much popularity even among the elite communities. This study evaluates the factors that influence the adoption of mobile money by Zambian university students using ZCAS-University as a case study.

The research adopted a mixed method approach and used questionnaires and semi-structure interviews to collect data from a sample size of 150 students. The quantitative data was then analyzed using statistical package for social sciences while the qualitative data was analyzed using thematic technique.

The findings were that students adopted mobile money mainly due to accessibility and ease of use. The study showed that they were areas where banks were better than mobile money in terms of security and professionalism, therefore, students did not adopt mobile money because it was highly better than banks but because it was more accessible. Other factors such as ease of use, perceived usefulness and affordability played a role in the adoption of mobile money in varying degrees.

Keywords: mobile money, ZCASU, Zambia

INTRODUCTION & BACKGROUND

The term mobile money attributes to the use of mobile phones for financial transactions. Mobile money began to emerge in Africa in the early 2000, with pioneering efforts such as smart money in the Philippine and M-pesa in Kenya. M-pesa, launched by Safaricom around 2007 is widely regarded as the genesis example of mobile money success on the continent Initially designed as a way to facilitate microfinance loan repayments, M-Pesa quickly evolved into a full-fledged mobile money transfer service, allowing users to send and receive money via simple text messages. According to Phiri (2019), from the launch, the number of subscribers increased to over 7 million in merely over 2 years. According to MNS Consulting the invention of M-pesa mobile money by Safaricom was inspired by the challenges the unbanked community had in accessing financial services. Since then, these services have grown globally. Empirical evidence shows that Africa is taking a lead globally in mobile money service delivery. Every business comes to meet a need on the ground, therefore, for Africa to be the global leader of this innovation, it entails that it is equally a leader of a certain problem or problems that this innovation is solving. According to Banda (2019), Africa has 100 million active mobile money accounts. This record is significantly much higher than South Asia which has the second biggest market share with only about 40 million active accounts. This alone is an indicator that there is a great problem that was prevalent in Africa that mobile money operators came to solve while banks were laid back. As of December, 2020, mobile money accounts increased to 159 million active accounts in sub-Saharan African regions alone. The transactions recorded to have been drive by mobile money services amounted to 548 billion USD (1090 et al.2022). This shows how tremendous the growth of mobile money has been.

Expanding upon the success of M-Pesa, mobile money services experienced rapid growth throughout Africa. Telecom operators, financial institutions, and technology firms acknowledged the vast potential of mobile money in reaching unbanked and underserved populations. Consequently, initiatives like Airtel Money, Tigo Cash, and Orange Money were introduced across various African nations, offering similar mobile money transfer and payment solutions.

Recognizing the pivotal role of mobile money in fostering financial inclusion and economic progress, governments and regulators in numerous African countries implemented supportive regulatory frameworks. These measures aimed to cultivate the expansion of mobile money services while ensuring consumer safeguarding and financial sector stability. Such regulatory backing spurred additional investment and innovation in mobile money infrastructure and technology.

Over time, mobile money offerings in Africa transcended basic peer-to-peer transactions to encompass a diverse array of financial services. These encompassed mobile banking, savings accounts, microloans, insurance, bill payments, merchant transactions, and remittances. Consequently, mobile money platforms evolved into comprehensive financial ecosystems, offering users seamless access to formal financial services via their mobile devices.

The impact of mobile money on the African continent has been profound, driving significant advancements in financial inclusion. Millions of individuals, especially those residing in rural and remote areas, gained access to formal financial services for the first time. Moreover, mobile money catalyzed economic activity, bolstered livelihoods, heightened resilience to economic shocks, and spurred entrepreneurship and innovation across Africa.

Zambia was one of the early adopters of mobile money services. The first services were introduced in 2009 (BoZ, 2016). The country has since then seen a number of players come on board the digital financial services platform. These include MTN mobile money, Airtel money, and Zoona.

The adoption of mobile money in Zambia ballooned in 2021, where the sector saw subscriptions increased from 9.8 million in 2021 to 11.2 million subscribers in 2022, representing a growth rate of 13.98%.

In this period, the value of mobile money transactions increased significantly from ZMW 169.4 billion recorded at the end of 2021 to ZMW 295.8 billion at the end of 2022, reflecting an increase of 74.63%. Detailing the performance of the Zambian ICT sector, ZICTA says the country witnessed increased utilization of ICT services in the country over the period January to December of 2022. To support this, ZICTA notes, by the end of December 2022, there were a total of 84 valid licenses in the ICT sector compared to 73 valid licenses that had been issued by the regulator at the end of December 2021

Similarly, ZICTA notes, the volume of mobile money transactions increased from 834 million transactions at the end of 2021 to 1 581 million transactions at the end of 2022, reflecting an improvement of 89.60%.

“This performance represents extensive adoption of digital financial services and presents important opportunities for increased financial inclusion in the country,” says the regulator.

n the postal sector, there were a total of 71 valid licenses at the end of December, 2022, compared to 49 valid licenses that had been issued at the end of December 2021, reflecting a growth rate of 45%.

Looking ahead, the regulator forecasts a positive outlook in the general uptake and use of ICT services in the subsequent review period.

“The number of active mobile network subscriptions is expected to increase from 19.8 million reported at the end of 2022 to 20.4 million subscriptions at the end of 2023, and, subsequently, 21.3 million in 2024. In addition, the volume of domestic outgoing mobile voice call minutes is forecasted to increase from 28.5 billion minutes estimated at the end of 2022 to 32.1 billion projected for the year 2023 and could reach 34.5 billion minutes in 2024,” says ZICTA.

These anticipated improvements in uptake and usage of ICT services are on the backdrop of increased investments by operators in the capacity and coverage of their networks, competitive pricing outcomes on the market as well as general improvement in demand for ICT services among other attributes

STATEMENT OF THE PROBLEM

Mobile money services in Zambia can be traced to as far as 2001 when Celpay was introduced which facilitated a payment system connecting post offices in the country (Phiri, 2019). Thereafter, in 2009 ZOONA was introduced which allowed the unbanked in distant places (mostly rural) to receive and send money. Phiri (2019), further states that in 2011 AIRTEL launched AIRTEL money followed by a launch by MTN in 2012 January.

However, the growth of mobile money services has been continuously overwhelming. In 2021 the market recorded a 15% increase in the number of subscribers from 2020. The number of subscribers in 2021 moved to 9.9 million from 8.6 million in 2020 (Bank of Zambia, 2021). The mobile money sector has not just grown big, but has covered more people than the traditional banks have. In 2014 Bank of Zambia announced that the number of accounts by mobile money networks was higher than the accounts held by banks (Phiri, 2019). Thus, the factors that have influenced many people to adopt mobile money services with others abandoning traditional banking services has been a national conundrum.

The bank of Zambia reported that as of 2022, over 50 % of the transactions in the Zambian payment system were through mobile money (FY22 payment stats reveal Zambia’s financial transformation as Momo exceeds 1BN transactions, 2023). This is an indication of great growth in mobile money services beyond traditional banks.

What is appalling is the fact that banks are more secure than mobile money networks and offer all banking solutions in one place. Banks have a one-stop-shop type of module in their service delivery making it very convenient for clients, however, people have continued to adopt mobile money services. Wilkinson (2021) stated that bank use by Zambians decreased by 4% from 24% in 2015 to 20% in 2020. Nevertheless, during the same period the use of digital financial services (which includes mobile money services) experienced growth from 14% to 59%.

When mobile money services were first introduced, they were deemed to be for the unbanked who couldn’t afford banking services (Mwansa 2020), however, we have continued to witness the unprecedent growth of adoption of mobile money services by not only the unbanked poor communities but also by the elite. It is against this the background that the researcher embarked has on a research journey to evaluate the factors influencing the adoption of mobile money services by ZCAS university students.

Purpose Of The Study

The purpose of this study was to evaluate factors influencing the adoption of mobile money services by University students in Zambia with Zcas University as a case study. Specifically, the study examines.

Specific Objectives

- To assess factors influencing the adoption of mobile money services by ZCAS University students.

- To assess the impact of technological advancement on mobile money services

- To evaluate the relationship between easy accessibility and the adoption of mobile money services

- To assess the relationship between the associated cost of use and the adoption of mobile money services.

Theoretical Framework & Conceptual Framework

The New Competition Faced by Banks.

Banda (2019) wrote a dissertation under an UNZA master’s program where she addressed the issue of mobile money services taking bank customers. In her dissertation she sampled out ZANACO customers. She stated that the growth of Mobile Money Operators (MMOs) as providers of financial services has affected the way banks conduct their transactions in Zambia. This is true because banks have since then rapidly embraced mobile banking services and focused on them as a medium of service delivery. The problem with that is, prior to the advent of mobile money services by telecommunication companies (telecoms), banks had their own ambitions and business plans. However, that was compromised as they had to put their energy to fixing a new problem in the market. It is true that as small as telecoms may seem, they posed a serious threat on the banks’ market share.

Competition with Zanaco was rated very high especially that the Banks are registered financial institutions but the MMOs have captured house maids, house servants, casual workers, rural areas, and where banks have failed to deliver. The Zanaco officials interviewed, indicated that with the MMOs on the market the competition was uneven. Zanaco was supposed to compete with fellow large banks but was then being subjected to compete with the MMOs. They acknowledged that the competition was significant but that Zanaco was the first bank to provide mobile banking services through booths and express agents (Banda, 2019).

Just as Banda stated, banks thought that their only focus of competition was their fellow banks, most especially the big banks, but something unanticipated happened when MMOs started taking customers that belonged to banks. Apparently, many students happen to be among those customers.

2.2 Levels of Financial Literacy by Students

Financial literacy is an essential skill that enables individuals to make informed decisions about managing their financial resources. In Zambia, financial literacy among students is a critical issue, given the country’s economic challenges and the need for sustainable development.

The lack of financial literacy among students in Zambia has been highlighted in various studies. According to Chilala and Chanda (2017), most students lack knowledge of financial management, which leads to poor financial decisions. The study found that 62% of the students surveyed did not have any knowledge of budgeting, while 72% were unaware of the importance of saving. The study also revealed that students were more likely to rely on friends and family for financial advice than seeking professional advice.

Similarly, a study by Chanda and Mupeta (2019) found that most students lacked knowledge of financial planning, investing, and managing debt. The study revealed that only 25% of the students surveyed had a basic understanding of financial planning, while 80% were not aware of the different investment options available to them. The study also found that 90% of the students surveyed did not have any knowledge of managing debt.

Furthermore, the study by Moyo(2018) revealed that most students in Zambia lacked financial knowledge, skills, and confidence. The study found that 64% of the students surveyed had never received any financial education, while only 7% had received financial education in school. The study also found that students who had received financial education were more likely to save, invest, and manage debt than those who had not.

In contrast, a study by Manda and Kamau (2019) found that financial literacy among students in Zambia was moderate. The study revealed that 52% of the students surveyed had basic financial knowledge, while 32% had moderate financial knowledge.

Statistics and observations have shown that quite a number of students have adopted mobile money services. One would conclude that it’s because their financial literacy levels are high, however, the different literatures cited above have shown different results on literacy levels among students.

A study by Siwale and Banda (2021) argues that high literacy influences the adoption of mobile money services as it was found that students with a high level of financial literacy were more likely to adopt mobile money services than those with a low level of financial literacy. The study also found that financial literacy positively influenced the intention to use mobile money services among students.

However, according to Thapa and Nepal (2020), a survey was conducted on how much financial literacy students have. The findings where that students have quite some knowledge on banking but relatively little knowledge on credit. And one of the benefits of being part of the banking business is access to credit. Every person at one point or another will need some sort of credit, as a matter of fact, businesses operate on credit. This means that the fact that students have no full knowledge on what credit is, then there is a problem to be solved because possibilities are that such ignorance is one of the things making them avert banking migrate to mobile money services. However, Manda and Kamau (2019), found that only 16% of the students had advanced financial knowledge. This justifies why some students would completely abandon traditional banking because it takes high levels of financial literacy to appreciate traditional banking. On the other hand, basic financial literacy is enough to make one adopt mobile money services. This implies that a majority of Zambian students lack deep financial knowledge and this postulation is consistent with Chilala and Chanda (2017) and Chanda and Mupetat (2019).

2.3 Factors Influencing the Adoption of Mobile Money Services

Mobile money services have become increasingly popular in Zambia, but the factors influencing their adoption are complex and multifaceted. Factors such as perceived usefulness, perceived ease of use, awareness and knowledge of mobile money services, social influence and trust in mobile money providers were significant predictors of mobile money adoption in Zambia (Ngwenya & Tapela, 2019; Chansa & Mwitwa, 2019).

Mudenda & Nkonde (2019), found that factors such as ease of use, affordability, and perceived usefulness were significant predictors of mobile money adoption in Lusaka Province. The study also highlighted the importance of education and awareness-raising initiatives in promoting mobile money adoption.

Factors such as perceived usefulness, perceived ease of use, trust in mobile money providers, and compatibility with existing financial systems as key determinants of mobile money adoption in Zambia (Banda, F. M., & Mutale, G. J. (2020).

Overall, these studies suggest that factors such as perceived usefulness, perceived ease of use, trust in mobile money providers, and awareness and knowledge of mobile money services are important determinants of mobile money adoption in Zambia. Education and awareness-raising initiatives may also play a critical role in promoting adoption.

2.4 Other Reasons for Adopting Mobile Money Services

As for the logistic regression analysis, the results reveal on the one hand that the offer of mobile money services is low cost and on the other hand that the intention of use and convenience are the real factors explaining adoption of mobile money services. Also, the monetary and regulatory authorities should speed up the implementation of the interoperability project. This would facilitate the execution of financial transactions between customers belonging to different banks and mobile operators (Sossou & Gaye, 2022).

Sossou stated reasons as to why people (in this case students) have adopted the use of MMOs. The factors he mentioned are independent such that if well maintained and satisfied, banks wouldn’t experience the loss in customers as has been the case. However, Banda (2019) used the rational choice theory to explain why people have adopted the services offered by MMOs. The rational choice theory states that people will do something that brings out their best satisfaction according to their specific needs and beliefs. An example is, one can smoke because it gives them relief while another will avoid smoking because they believe it’s bad for their health. This somehow implies that banks can only do so much to retain their customers because at the end of the day customers must make a choice according to what they feel best meets their needs. However, the theory of Sossou seems to be outstanding here. This is because when MMOs surfaced on the market, huge numbers adopted their services. What Banda stated in her dissertation was how MMOs focused on providing services to the unbanked. However, what we are seeing today among friends and the people we know is that the banked too have adopted mobile money service, the students who had bank accounts abandoned them focusing on MMOs. This sort of means that there are services banks were not providing that the MMOs started providing and attracted the unbanked and at the same time provided the services banks provide, but in a better and refined manner thereby, attracting the banked as well. One of the refinery attributes MMOs introduced was minimal requirements and limitations in using their services. Banks, despite the recent improvement, have too many restrictions which in essence pushed people to the banks’ rival.

However, Eleanor (2022) stated that Africa is at the forefront of the mobile banking revolution, spearheaded by the mobile phone technological platform for financial services. She further alluded to the number of mobile Internet subscribers rising in Africa. In her article she highlighted how Africa seems to become the worldwide leader in mobile money services and that is because Africans have the willingness and ability to absorb innovations in the area of mobile money services.

According to Eleanor, Africa is a leading mobile banking revolutionist. This could be because most Africans are unbanked. Gutierrez (2014), suggests that the African mobile money services provided by telecoms are based on a non-bank-model. She further states that this is typical for low income developing countries. This could imply that the reason students left the banking industry and adopted MMOs is because their income levels are low and hence, they felt unaccommodated by most banking products. For instance, many bank accounts require a minimum maintenance balance in the account. However, mobile money services offer accounts where one does not need maintenance fees for the account. That may have specifically being designed for the unbanked but the researcher was tempted to think it was strategically designed to also pool the banked such as students and employees with relatively low salaries. The other reason why telecoms seem to be leading in Africa, is because in Africa technology really moves slowly and therefore banks were reluctant in adopting new technologies while as in other places like Korea internet banking was introduced as early as 2005 and later on mobile banking. However, for Africa particularly Zambia, mobile money operators were the first ones to vigorously introduce a model that used mobile phones for financial transactions (Phiri, 2019). While some banks had this facility, they were still laid back on vigorously creating awareness on mobile banking among customers.

2.5 Theoretical Framework

2.5.1 The Technology Acceptance Model

The Technology Acceptance Model (TAM) was developed by Davis in 1989 to explain how users adopt and use new technologies. TAM posits that perceived usefulness (PU) and perceived ease of use (PEOU) are the two key determinants of users’ intention to use a technology, which in turn predicts actual usage behavior. The model has been widely used to study technology adoption in various contexts, including mobile money services (Venkatesh & Davis, 2000).

In the context of mobile money adoption in Zambia, perceived usefulness refers to the extent to which users perceive mobile money services as beneficial for their financial transactions, while perceived ease of use refers to the extent to which users perceive mobile money services as easy and convenient to use.

Another factor that may influence the adoption of mobile money services is trust. Trust has been identified as an important factor in the adoption of e-commerce and mobile payment systems (Rao & Troshani, 2008; Yang, Kim, & Kim, 2018). In the context of mobile money services, trust refers to the degree to which individuals believe that their transactions are secure and that their personal information is protected.

2.5.2 Theory of Reasoned Action

Social influence may also play a role in the adoption of mobile money services. According to the theory of reasoned action, individuals’ behavior is influenced by the subjective norms of significant others (Ajzen & Fishbein, 1980). In the context of mobile money services, subjective norms refer to the degree to which individuals perceive that their friends, family, and colleagues approve or disapprove of using mobile money services.

2.5.3 The Diffusion Innovation Theory

Finally, access to mobile phones and mobile network coverage may also influence the adoption of mobile money services. According to the diffusion of innovations theory, the rate of adoption of a new technology is influenced by its relative advantage, compatibility, complexity, trialability, and observability (Rogers, 2003). In the context of mobile money services, access to mobile phones and mobile network coverage may determine the relative advantage and compatibility of the technology.

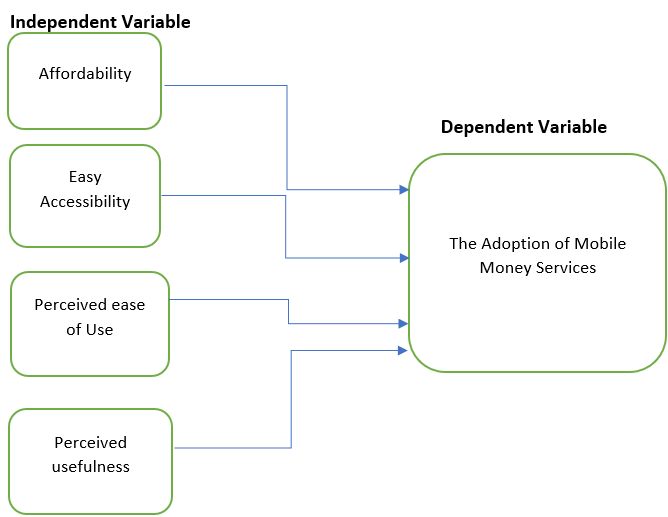

Conceptual Framework

The diagrammatic presentation below illustrates the relationship between the independent variables and dependent variables.

The independent variables were measured through surveys and the literature review. The dependent variable was measured by how many students have affective bank accounts and how many have mobile money accounts in place of bank accounts. However, those with both bank and mobile money accounts, I will determine via questionnaires which account they us more frequently.

GAPS IN LITERATURE REVIEW

This research focused on an area that other literatures haven’t focused on. Many have talked about mobile money services and their adoption but none of them has talked about the adoption of mobile money by ZCAS University students with a perceived-up history of students coming to from well to do families.

Banda & Mutale (2020) wrote about the factors affecting the adoption of mobile money services in Zambia, and their focus was the whole Zambia. Chansa & Mwitwa (2019), discussed on the factors influencing the adoption of mobile money in Zambia. Similarly, their focus was the entire Zambia which made this research different as its focus was on the ZCAS university students. Other researchers such as Rao & Troshani (2008) wrote about mobile banking adoption which is a different focus from this research. Banda (2019) wrote a about the impact of mobile of money and her focus was on the customers of ZANACO bank. None of the papers put ZCAS University in focus as regards the adoption of mobile money. Even those that talked about the factors affecting the adoption of mobile in Zambia such as the article by Kawimbe (2022), didn’t bring out the fact that despite banks offering a one-man-stop shop module in their service delivery students have quickly adopted mobile money services in place of banking services. In summary, this theoretical framework was based on the Technology Acceptance Model (TAM), the theory of reasoned action (TRA) and the diffusion innovation theory and proposed that perceived usefulness, perceived ease of use, trust in mobile money providers, compatibility with existing financial systems, and social influence are the key factors influencing mobile money adoption in Zambia. Further research was conducted to understand how these factors interact and promote the adoption of mobile money services in Zambia.

RESEARCH METHODOLOGY

The rapid growth of mobile money services has transformed financial transactions, particularly in emerging economies. Understanding the factors influencing the adoption of mobile money services is crucial for stakeholders aiming to enhance service uptake and financial inclusion. This research aims to evaluate these factors through a comprehensive methodology.

Research Design.

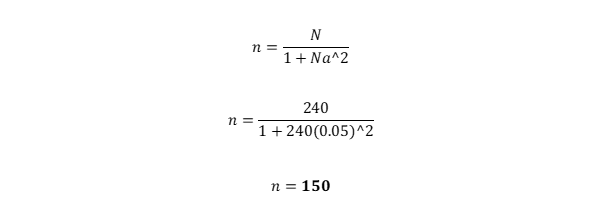

The study adopted a mix method approach and utilized questionnaires, semi-structured interviews and observations. From a student population of 3,500 on all three modes of study (Fulltime, Part-Time and Distance) Questionnaires were administered to a sample of 240 students who were in boarding only for easy of reach using the Slovin formula.

n= sample size required

N= size of population

a= accuracy degree in proportion (0.05)

Quantitative data was analyzed using Microsoft Excel. The software extracted bar graphs and pie charts that were used to present the data analyzed. Thematic analysis was used to analyze qualitative data. According to Braun and Carke (212), thematic analysis is a technique a researcher can use to evaluate and report repeated data patterns in the collected qualitative data

DATA ANALYSIS AND FINDINGS

Response Rate

From the population of 240 boarders the sample size calculated of 150 was arrived at using Slovin’s formula. However, from the 150 students 108 responded to the questionnaire and 30 responded to the interview, making a total of 138 respondents, a response rate of 92%. According to scholars such as Hardigan et. al (2016), a response rate of 60% and above should be considered outstanding, therefore, the 92% response rate in this case is an outstanding and excellent rate and good enough to be considered reliable in terms of data validation.

4.2 Profiles of Respondents

To easily get data, the researcher targeted ZCAS boarders only due to their availability, however, the researcher collected the data from boarders of the institution. Data was collected from both males and females on different academic levels. The profiles included whether the respondents had bank and mobile money accounts, and what mobile money service provider those with mobile money accounts preferred.

4.2.1 Gender

The researcher investigated the gender of the participants and found that (as illustrated by the tables and pie chart below) 52.8% were males while 47.2% were females.

| Statistics | ||

| Gender | ||

| N | Valid | 108 |

| Missing | 0 | |

| Gender | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Male | 57 | 52.8 | 52.8 | 52.8 |

| Female | 51 | 47.2 | 47.2 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.2.2 Academic Year

Further, the researcher sought to identify the academic years or levels of the respondents and found that the participants only ranged from second year to fourth year students. This was probably owing to the fact that the researcher had little interaction with freshmen students.

| Statistics | ||

| Academic year | ||

| N | Valid | 108 |

| Missing | 0 | |

| Academic Year | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Second year | 27 | 25.0 | 25.0 | 25.0 |

| Third year | 30 | 27.8 | 27.8 | 52.8 | |

| Fourth year | 51 | 47.2 | 47.2 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.2.2 The Preferred Mobile Money Service Provider by Per Respondent

In addition, the researcher attempted to find out the service provider that each respondent preferred. The findings suggested that AIRTEL Money ranked first with 52.8%, seconded by MTN Money with 36.1% and lastly ZAMTEL Money 5.6% and those who did not use mobile money were also 5.6% of the total respondents.

| The Preferred Mobile Money Operator | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Airtel | 57 | 52.8 | 52.8 | 52.8 |

| MTN | 39 | 36.1 | 36.1 | 88.9 | |

| Zamtel | 6 | 5.6 | 5.6 | 94.4 | |

| none | 6 | 5.6 | 5.6 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.2.3 Respondents with Bank Accounts

The researcher also sought to find out how many respondents have bank accounts and compared with those that have mobile money accounts. The findings were that 77.8% had bank accounts while only 22.2% are the ones who didn’t have. However, 94.4% of respondents had mobile money accounts which is 16.6% more than the number of respondents with bank accounts. The findings also suggested that only 5.6% of respondents didn’t have mobile money accounts which is way lower than the 22.2% of respondents without banks accounts.

| Statistics | ||

| Do you have bank account? | ||

| N | Valid | 108 |

| Missing | 0 | |

| Do you have bank account? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Yes | 84 | 77.8 | 77.8 | 77.8 |

| No | 24 | 22.2 | 22.2 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3 The Assessment of Findings and Analysis of Each Instrument

The researcher assessed the findings of questionnaire and interviews. The assessment and analysis of the two was done independently. The researcher used Statistical Package for Social Sciences (SPSS 20th Version) to analyze each question from the questionnaire. Thereafter, qualitative data from the semi-structured interviews was analyzed using the thematic technique.

4.3.1 Respondents Responses

The researcher provided possible answers to questions in the questionnaires and asked the respondents to mark the answers they felt were correct according to their experiences. The researcher further incorporated a 5 linkert scale in the questionnaires which allowed the respondent to state the degree to which they agreed or disagreed with a particular statement. Some questions demanded the researcher providing a rating for various items.

4.3.1.1 Reasons for preferring a particular Mobile Money Network

| Statistics | ||

| Reasons for using MMO | ||

| N | Valid | 108 |

| Missing | 0 | |

| What makes prefer your current mobile money service provider? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Cheaper | 18 | 16.7 | 16.7 | 16.7 |

| Accessible | 51 | 47.2 | 47.2 | 63.9 | |

| Ease of use | 33 | 30.6 | 30.6 | 94.4 | |

| not applicable | 6 | 5.6 | 5.6 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.2 General Reasons for Using Mobile Money

| Statistics | ||

| In general, what makes you use mobile money? | ||

| N | Valid | 108 |

| Missing | 0 | |

| In general, what makes you use mobile money? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Affordability | 12 | 11.1 | 11.1 | 11.1 |

| Usefulness | 33 | 30.6 | 30.6 | 41.7 | |

| Ease of use | 21 | 19.4 | 19.4 | 61.1 | |

| Accessibility | 36 | 33.3 | 33.3 | 94.4 | |

| Not applicable | 6 | 5.6 | 5.6 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.3 Challenges with Banks

| Statistics | ||

| If you have a bank account, what challenges do you have with banks? | ||

| N | Valid | 108 |

| Missing | 0 | |

If you have a bank account, what challenges do you have with banks?

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Expensive | 21 | 19.4 | 19.4 | 19.4 |

| Many requirements | 36 | 33.3 | 33.3 | 52.8 | |

| Unreliable | 27 | 25.0 | 25.0 | 77.8 | |

| N/A | 24 | 22.2 | 22.2 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.4 Reasons for Not Owning a Bank Account

| Statistics | ||

| Reasons for not having a bank account | ||

| N | Valid | 108 |

| Missing | 0 | |

| If you don’t have a bank account, what are your reasons for not owning a bank account? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | no perceived usefulness | 15 | 13.9 | 13.9 | 13.9 |

| no ease of use | 3 | 2.8 | 2.8 | 16.7 | |

| not easy to open acc | 3 | 2.8 | 2.8 | 19.4 | |

| expensive | 3 | 2.8 | 2.8 | 22.2 | |

| N/A | 84 | 77.8 | 77.8 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.5 Frequency of use for Mobile Money

| Statistics | ||

| Frequency MMOs | ||

| N | Valid | 108 |

| Missing | 0 | |

| How frequently do you use mobile money? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | very rarely | 6 | 5.6 | 5.6 | 5.6 |

| rarely | 3 | 2.8 | 2.8 | 8.3 | |

| average | 3 | 2.8 | 2.8 | 11.1 | |

| frequenlty | 21 | 19.4 | 19.4 | 30.6 | |

| very frequently | 75 | 69.4 | 69.4 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.6 Ratings for Mobile Money

| Statistics | ||

| Rating Mobile Money | ||

| N | Valid | 108 |

| Missing | 0 | |

| From a scale of 1-5 rate your experience with mobile money (1 is very bad, 5 is very good). | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | very bad | 3 | 2.8 | 2.8 | 2.8 |

| bad | 6 | 5.6 | 5.6 | 8.3 | |

| average | 18 | 16.7 | 16.7 | 25.0 | |

| good | 45 | 41.7 | 41.7 | 66.7 | |

| very good | 36 | 33.3 | 33.3 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.7 Ratings for Banks

| Statistics | ||

| Rating Banks | ||

| N | Valid | 108 |

| Missing | 0 | |

| Rate your experience with banks. | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | very bad | 3 | 2.8 | 2.8 | 2.8 |

| bad | 24 | 22.2 | 22.2 | 25.0 | |

| average | 33 | 30.6 | 30.6 | 55.6 | |

| good | 42 | 38.9 | 38.9 | 94.4 | |

| very good | 6 | 5.6 | 5.6 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.8 Banks and Mobile Money

| Statistics | ||

| Is MMO better than banks? | ||

| N | Valid | 108 |

| Missing | 0 | |

| Is Mobile Money better than banks? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Highly agree | 30 | 27.8 | 27.8 | 27.8 |

| Agree | 51 | 47.2 | 47.2 | 75.0 | |

| Neutral | 12 | 11.1 | 11.1 | 86.1 | |

| Disagree | 9 | 8.3 | 8.3 | 94.4 | |

| Highly disagree | 6 | 5.6 | 5.6 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.9 Factors

| Statistics | ||

| Factors for using MMOs | ||

| N | Valid | 108 |

| Missing | 0 | |

| What factors do you consider when choosing a mobile money provider? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Ease of use | 21 | 19.4 | 19.4 | 19.4 |

| Accessibility | 48 | 44.4 | 44.4 | 63.9 | |

| Affordability | 15 | 13.9 | 13.9 | 77.8 | |

| Usefulness | 18 | 16.7 | 16.7 | 94.4 | |

| Not applicable | 6 | 5.6 | 5.6 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.3.1.10 Technological Preferences

| Statistics | |||||||

| What would you prefer to use to withdraw Cash? | |||||||

| N | Valid | 108 | |||||

| Missing | 0 | ||||||

| What would you prefer to use to withdraw cash? | |||||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||||

| Valid | Phone | 84 | 77.8 | 77.8 | 77.8 | ||

| ATM | 24 | 22.2 | 22.2 | 100.0 | |||

| Total | 108 | 100.0 | 100.0 | ||||

4.3.1.11 Technological Impact

| Statistics | ||

| Using a phone for cash withdraws makes you adopt mobile money. | ||

| N | Valid | 108 |

| Missing | 0 | |

| Does using a phone for cash withdraws make you adopt mobile money? | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | highly agree | 33 | 30.6 | 30.6 | 30.6 |

| Agree | 54 | 50.0 | 50.0 | 80.6 | |

| Neutral | 9 | 8.3 | 8.3 | 88.9 | |

| Disagree | 3 | 2.8 | 2.8 | 91.7 | |

| highly disagree | 9 | 8.3 | 8.3 | 100.0 | |

| Total | 108 | 100.0 | 100.0 | ||

4.6 Presentation and Analysis of Interview Findings

4.6.1 What would you prefer to use to withdraw your money, a phone or an Automated Teller Machine?

The researcher interviewed 30 different respondents and asked them the above question. 75% of them stated that they preferred to withdraw their money using a phone as opposed to an ATM. They claimed that a phone is much more convenient and safer than an ATM. They stated that an ATM gets to have cases where money or the debit card is swallowed by the machine creating inconveniences for the account holder. Further claims where that ATMs are associated with huge sums of money and therefore, they tend to attract a lot of theft and attacks on people from withdrawing money. However, the remaining 25% insisted that banks are more secure than mobile money and as such, it is better to withdraw money from an ATM. They stated that ATMs have more accuracy than mere human beings found at mobile money booths. They further stated that Automated Teller Machines are well guarded by police officers or security guards making them a safer option.

4.6.2 What would you prefer to use to withdraw your money, a phone or a debit card?

As this question was asked, 88% of the respondents suggested that if banks had an option of withdrawing money from an ATM using a phone, they would prefer that to a debit card. They further stated that services that banks are gradually adopting these services such as e-wallet and other wireless cash withdraw services are deemed more convenient than the traditional way of using a debit card.

The respondents claimed that the use of phones in place of debit cards is better because people are always with their phones making it easy to transact at any time and protect their account log in details unlike debit cards which sometimes don’t require a PIN (personal information number) or password due to the tapping options available. However, even after someone steals one’s mobile phone the owner still has a chance to report the theft to their respective service providers and secure their accounts, however, the tapping option on debit cards afford no one time to notice and report the theft, by the time one is noticing the theft the account would have already been emptied.

However, as indicated by the respondents even payments on the point of sale would be much better if phones were used in place of debit cards. Therefore, the technological advancements on mobile phones have increased the proclivity of people for wanting to use mobile phones to perform financial transactions.

4.6.3 What are some of the challenges you face with banks?

On this question, respondents claimed that banks sometimes have limited withdrawals. Each account has a prescribed number and size of withdraws it can perform per day. The respondents compared this to mobile money services where one can withdraw as much money and as many times as they can. They also added to how ATMs don’t always have cash making them unreliable. They further compared this to mobile money and talked of how unavailability of cash on mobile money booths is offset by the great number of booths available as options. In contrast, ATMs don’t only have limited cash, they are also located in highly selective places.

4.6.4 What are some of the challenges you face with mobile money services?

Despite mobile money services seeming to be a savior, 67% of respondents complained of the unreliability of MMOs to offer financial transaction reversals. Many respondents complained of how it is difficult and sometimes impossible to finalize transaction reversals. Further, mobile money services are unreliable in terms of performing a mobile money to bank transactions as well as an inter-network transaction.

4.6.4 What are some of your determining factors for adopting mobile money services?

All the 30 respondents to the interview indicated that accessibility was their major determining factor. This was followed by ease of use and perceived usefulness. A majority of the respondents claimed that affordability was their last determining factor because it depends on the amount in question. Those transacting huge amounts will find banks to be cheaper and safer while those transacting small amounts will find mobile money to be cheaper. They also complained of how banks charge over every little service while mobile money has a number of free services or at a lower cost.

CONCLUSION & RECOMMENDATION

Research Objective 1: To assess factors influencing the adoption of mobile money services by ZCAS University students.

The researcher assessed the factors influencing the adoption of mobile money services by Zambian University students as the first objective. In accordance with the responses to the questionnaire, it was indicated that accessibility, affordability, ease of use and perceived usefulness are the factors that influenced the adoption of mobile money and ranked respectively. 44% of the respondents suggested that they adopted mobile money because of its accessibility, 19% imputed the adoption on affordability, 16.7% on ease of use, 13.9% on perceived usefulness and 6% were not users of mobile money. Therefore, the above-mentioned factors are the determinants of the adoption behavior of mobile money by Zambian students.

5.1.2 Research Objective 2: To evaluate the relationship between easy accessibility and the adoption of mobile money services.

As the second objective, the researcher aimed to evaluate the relationship that exists between easy accessibility and the adoption of mobile money. The findings indicate that among the four factors identified in the first objective, easy accessibility ranked first at 44.4%. Almost half of respondents suggested that easy accessibility was the factor influencing their adoption behavior. To further assess the relationship, respondents were asked what made them prefer one mobile money service provider to the other. It was found that the majority being 47% preferred the most accessible service provider in their particular area while 30.6% and 16.7% preferred one service provider to the other due to ease of use and affordability respectively. This shows that easy accessibility has an impact on the adoption of mobile money services. This further suggests that it may not necessarily be that students are adopting mobile money because its offered services are significantly better than banks but because it’s easy to access them. Therefore, it is safe to conclude that there is a positive relationship between easy accessibility and the adoption of mobile money services.

5.1.3 Research Objective 3: To assess the impact of technological advancement on the adoption of mobile money services.

In this day and age technology is drastically advancing and apparently, almost everything is becoming linked to our mobile phones, therefore, the researcher embarked on a journey to find out if the technological advancements are impacting the adoption of mobile money. The researcher aimed to find out if the adoption of mobile money services is due to the fact that mobile money is directly linked to mobile phones. Therefore, the respondents were asked if the option of withdrawing money through a mobile phone has influenced their adoption of the mobile money. The findings were that 54% agreed while 33% highly agreed. This proved that a majority of students have adopted these services because of the advancement in technology allowing one to own a mobile account by virtue of owning a mobile phone and to withdraw money by simply dialing few digits on their phone.

5.1.4 Research Objective 4: To assess the relationship between the associated cost of use and the adoption of mobile money services.

Under this objective, the researcher aimed to investigate the relationship prevalent between the associated cost of use and adoption of mobile money. Therefore, the respondents were asked what factors they considered when choosing a mobile money service provider and only 16.7% considered the associated cost of use. This factor ranked last with accessibility and ease of use being the first and second respectively. The respondents were further asked what general factors they considered when adopting mobile money and once again affordability ranked last with 11.1% of respondents having considered affordability. This indicated that the associated cost had an influence on the adoption behavior but not as much as the other factors such as accessibility, usefulness and ease of use. therefore, the cost of use is not a major reason as to why people students have adopted mobile money. To further affirm this claim, the findings show that on the 24 students without bank accounts, only 3 (12.5%) didn’t have one due to the associated cost. However, the respondents to the interviews claimed that banks become more expensive than mobile money when it comes to small amounts of money. This is because banks have fixed withdraw and transaction fees which are expensive when transacting small amounts but friendly when transacting huge amounts. However, mobile money fees vary depending on the amount involved.

Therefore, the findings suggested that cost has an influence on mobile money adoption where small amounts are involved but not much influence on the adoption where huge amounts are involved.

5.5 Recommendations

5.5.1 Policy Makers Must Regulate Mobile Money

According to the finding, 24 students claimed to have no bank accounts and of the 24, 13% stated that they had no bank account owing to the fact that banks have many requirements. The researcher also asked respondents to rate their experience with banks and with mobile money.

5.6% rated banks to very good while 38.9% rated them to be good. 33.3% rated mobile money to be very good and 41.7% rated them to be good. The difference on the “very good” rating between banks and mobile money was recorded to be significant, therefore, it could be concluded that students found mobile money to be significantly better because it has less regulations. Therefore, the policy makers must adequately regulate mobile money. This is because the financial industry telecommunication companies have diversified into is supposed to be heavily regulated according to the Bank of Zambia Act. This venture has posed great competition on banks (Banda 2019) and therefore, the regulation must be even in order to even the competition.

5.5.2 Banks Must Increase their Reach

Apart from focusing on those with definite sources of income, banks should also begin to offer services to the unbanked and those without definite sources of income such as students. The respondents to the questionnaire that didn’t have bank accounts were asked why they didn’t and 78% indicate that it was because of no perceived usefulness for banks. This is because they believed that a bank account was only ideal for one with definite inflows of income. However, some banks have gone ahead by offering student products such as FNB offering student accounts and ZANACO offering XAPIT accounts. However, banks need to advertise such products more to increase awareness among students. Nevertheless, those that don’t have this initiative in their service provision should quickly do so. This is should also extend to the general unbanked community. Banks can incorporate a booth module like mobile money in order to increase their reach. Many respondents talked of how bank services are not easy to access, this calls for increasing the number of ATMs in urban areas and booths in rural areas.

5.5.3 Banks Should Adopt and Encourage Mobile Phone Oriented Products

Some banks have already incorporated wireless services on their ATMs, however, the fact that most people have not been acquainted with such services means that banks have not done a good job at making those wireless services, known, affordable, accessible and easy to use. One of the factors students mainly considered when adopting mobile money services was ease of use. many bank products are associated with complexities. This is because banks have tried to make their services so secure to a point of compromising their user friendliness. To curb this, banks should for example, make their wireless withdraw services so simple that one will just withdraw on their phone and only provide a few details to the ATM or booth operator. Banks must also increase the number of ATMs to make these services accessible. The goal must be for people to understand how linked their bank account is to their mobile phones.

In addition, banks must slightly lower the transaction costs for small amounts to make them more affordable and attract sales.

5.6 Limitation of the Study

Time constraint was the number one challenge for the researcher, the research was done in three months due to the time allocation of the semester. This hindered much depth and collection of data. The researcher also faced challenges with data collection, this is because the research was based on students and at the time of data collection many students were busy with exams and carrying out their own research. ZCAS University is a private and expensive institution, therefore, the other limitation the researcher faced was in getting views from people of similar economic classes. Lastly, the fact this research was confined to ZCAS University was a limitation too.

5.7 Direction for Further Research

For the purpose of further similar research, the researchers must focus on at least two different institutions with people from different economic classes. ZCAS University being a private and quite costly institution most likely creates the bias of only carrying out research on people from the similar economic classes, therefore, further research must touch many economic classes to avoid bias. Furthermore, researchers embarking on a similar journey of research must also focus on other demographic groups other than students.

5.8 Conclusion

The researcher collected data from respondents at ZCAS University from both questionnaires and interviews to evaluate the factors influencing the adoption of mobile money services. From the collected data, it can be concluded that the factors influencing the adoption of mobile money services can be ranked as easy accessibility, ease of use, perceived usefulness and affordability. Therefore, it is quite important for both the police makers and banks to work hand in hand in addressing these factors. The truth is that mobile money has come and addressed some angles of these factors and as long as banks remain rigid, they’ll continue to face unmatched competition from the telecommunication companies that have diversified into the financial sector.

REFERENCES AND & BIBLIOGRAPHY

- Aron, J. (2018). Mobile money and the Economy: A Review of the evidence. The World Bank Research Observer, 33(2), 135–188. https://doi.org/10.1093/wbro/lky001

- Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behavior. Prentice- Hall.

- Banda, F. M., & Mutale, G. J. (2020). Factors affecting the adoption of mobile money services in Zambia. International Journal of Scientific and Research Publications, 10(9), 369-378. doi: 10.29322/ijsrp.10.09. 2020. p10523

- Banda, G. (2019). the development of mobile money operators: implications for ZANACO mobile banking customers in Lusaka (Postgraduate). University of Zambia.

- Bhandari, P. (2022, October 10). Population vs. Sample | Definitions, Differences & Examples. Scribbr. https://www.scribbr.com/methodology/population-vs-sample/

- Bouma, G. and Atkinson, G. (1995) A Handbook of Social Science Research: A Comprehensive and Practical Guide for Students (2nd edn). Oxford: Oxford University Press.

- Brierley, J. A. (2017). The role of a pragmatist paradigm when adopting mixed methods in behavioural accounting research. International Journal of Behavioural Accounting and Finance, 6(2), 140. https://doi.org/10.1504/ijbaf.2017.10007499

- Chanda, E. M., & Mupeta, S. (2019). Financial literacy levels among university students in Zambia. Journal of Financial Economic Policy, 11(4), 612-626. doi: 10.1108/JFEP-05-2019-0079

- Chansa, C., & Mwitwa, C. (2019). Factors influencing the adoption of mobile money in Zambia: A case of Lusaka Province. International Journal of Business and Social Science Research, 8(4), 1-10. doi: 10.18533/ijbsr. v8i4.1274

- Cherry. (2022, September 4). How Do Cross-Sectional Studies Work? Verywell Mind. Retrieved November 16, 2022, from https://www.verywellmind.com/what-is-a-cross-sectional-study-2794978

- Chilala, M. M., & Chanda, M. (2017). Financial literacy and its impact on the financial management behavior of university students in Zambia. Journal of Economics and Behavioral Studies, 9(6), 70-78.

- Cohen, L., Manion. L., & Morrison, K. (2011). Research methods in education. London: Routledge.

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319-340.

- Easterby- Smith, M., Thorpe, R. Jackson, P. and Lowe, A. (2008) Management Research (3rd edn). Sage: London.

- Eleanor, N. (2022). A review of strategies banks have adopted to gain market share of the unbanked community dominated by mobile network operators: a case of Zanaco bank. (Postgraduate). The University of Zambia.

- GSMA (2013) State of the industry 2013. Mobile financial services for the unbanked, GSMA, 2013

- Gutierrez, E. & Choi, T. (2014). Mobile Money Services Development; The Cases of the Republic of Korea and Uganda. Available from https://www.researchgate.net/publication/263809182 Mobile Money Services Development The Cases of the Republic of Korea and Uganda [Accessed 6 October 2022]

- Hammersley, M. (2013). What is Qualitative Research? London and New York: Bloomsburry. Morris, C. (2003) Quantitative Approaches in Business Studies (6th edn). Harlow: FT Prentice Hall.

- Morris, C. (2003) Quantitative Approaches in Business Studies (6th edn). Harlow: FT Prentice Hall.

- Hölldobler, S., & Schneeberger, J. (1990). A new deductive approach to planning. New Generation Computing, 8(3), 225–244. https://doi.org/10.1007/bf03037518

- FY22 payment stats reveal Zambia’s financial transformation as Momo exceeds 1BN transactions. The Business Telegraph. (2023, February 5). Retrieved March 15, 2023, from https://thebusinesstelegraph.com/2023/02/05/fy22-payment-stats-reveal-zambias-financial-transformation-as-momo-exceeds-1bn-transactions/#:~:text=The%20report%20reveals%20that%20retail,in%20third%20place%20at%20K111.

- Ideas, D. (2022, February 3). The rise of Mobile Money in sub-saharan africa: Has the digital technology lived up to its promise? African Arguments. Retrieved April 3, 2023, from https://africanarguments.org/2022/02/the-rise-of-mobile-money-in-sub-saharan-africa-has-the-digital-technology-lived-up-to-its-promise/

- Kabala, E. (2023). Dynamics of Mobile Money Entrepreneurship and employment in Kitwe, Zambia. Global Labour in Distress, Volume I, 1, 387–391. https://doi.org/10.1007/978-3-030-89258-6 19

- Kawimbe, S., Sishumba, J., & Loti, S. (2022). Factors affecting the adoption of mobile money services in Zambia: Case of Central Bank of Zambia. International Journal of Current Science Research and Review, 05(10). https://doi.org/10.47191/ijcsrr/v5-i10-13

- Manda, D. K., & Kamau, M. W. (2019). Determinants of financial literacy among university students in Zambia. Journal of Economics and Sustainable Development, 10(9), 84-90.

- Moyo, M., Chikwati, E., & Ngwenya, M. (2018). The impact of financial education on the financial literacy of university students in Zambia. Journal of Economics and Behavioral Studies, 10(3), 168-179.

- Mudenda, D. M., & Nkonde, G. (2019). Factors influencing the adoption of mobile money services in Zambia: A case of Lusaka Province. International Journal of Social Sciences and Humanities Research, 7(1), 34-45. doi: 10.11648/j.ss.2019.07103.13

- Musonda, F. (2019). The impact of stress among bankers: a case of FNB head office branch (Undergraduate). ZCAS University.

- Mwansa, R. (2020). Investigating consumer preference and usage of mobile money services in Zambia: a case study on mobile network operators (airtel, mtn & Zamtel) in lusaka (undergraduate). Cavendish University.

- Ngwenya, S., & Tapela, B. (2019). An empirical assessment of mobile money adoption in Zambia. Journal of African Business, 20(3), 303-324. doi: 10.1080/15228916.2019.1614236

- Phiri, M. N. (2019). International journal of advanced studies in computer science and engineering. Investigating Mobile Money Usage Patterns in Zambia: A Case of Mobile Network Operator Systems, 1.

- Rao, S., & Troshani, I. (2008). Mobile banking adoption: A literature review. Telematics and Informatics, 25(2), 97-116.

- Rogers, E. M. (2003). Diffusion of innovations. Free Press.

- Saunders, M., Lewuis, P. & Thornhill, A. (2009). Research methods for business students (5th ed.). England. Pearson education.

- Teddlie, C. and Tashakkori, A. (2009) Foundations of Mixed Methods Research: Integrating Quantitative and Qualitative Approaches in the Social and Behavioral Sciences, Sage, Thousand Oaks, CA.

- Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the Technology Acceptance Model: Four longitudinal field studies. Management Science, 46(2), 186-204. doi: 10.1287/mnsc.46.2.186.11926

- Yang, K., Kim, J., & Kim, H. (2018). Factors influencing the adoption of mobile payment services by generation Y in South Korea. Journal of Computer Information Systems, 58(1), 33-42.What is Quantitative Data? (n.d.). Careerfoundry. Retrieved November 18, 2022, from https://careerfoundry.com/en/blog/data-analytics/what-is-quantitative-data/