An Investigation of the Impact of Mobile Money Services on the Profitability of Commercial Banks in Zambia

- Paul Mbunji

- Benjamin Kaira

- 2772-2788

- May 24, 2024

- Banking

An Investigation of the Impact of Mobile Money Services on the Profitability of Commercial Banks in Zambia

Paul Mbunji* and Benjamin Kaira

Graduate School of Business, University of Zambia, Lusaka, Zambia

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804262

Received: 03 April 2024; Revised: 17 April 2024; Accepted: 23 April 2024; Published: 24 May 2024

ABSTRACT

This paper sought to determine the impact of mobile money services on the profitability of commercial banks in Zambia. The study was guided by three objectives; (i) To examine the level of use of mobile money services in Zambia; (ii) to assess the measures of financial performance in the banking industry and (iii) to establish the relationship between the use of mobile money services and financial performance of the banking industry. The study applied both qualitative and quantitative research approaches mainly descriptive correlation design. The target population comprised of workers in all the commercial banks, mobile money operators (MMOs) and regulators and bank experts from Zambia Information and Communications Technology Authority (ZICTA) and Zambia Institute of Bankers (ZIOB) located in Lusaka central business district. A sample of 156 respondents was chosen using purposive sampling techniques to select retail, operations, customer service and finance department employees from banks and MMOs and two experts from ZICTA and ZIOB as key informants. Data were collected using questionnaires administered via Google forms sent to WhatsApp contacts and email addresses of respondents. Data were and analyzed using SPSS statistical packages to generate descriptive statistics (mean and standard deviations) and inferential statistics (regression analysis). The findings of study were presented in form of means, standard deviations, Pearson’s linear correlation coefficient and linear regression analysis. According to the findings of the study, it was indicated that there is generally a high level of use of mobile money services in the banking industry observed from a high level of reliability and accessibility to the services (Means of 3.71 and 4.17 simultaneously). The findings also indicated that there is a high level of financial performance reflected by a high level of profitability (Mean=4.52) in the banking industry, a high level of loan supervision (Mean=3 .85) and relatively high revenue sources (Mean=4. 11) for the banks. It was also indicated that there is an insignificant relationship between mobile money services use and financial performance in terms of profitability of banking industry (Sig. Value=0.2l2). It was also indicated that there is an insignificant relationship between mobile money services use and loan portfolio management of the banking industry (Sig. value=0.605). Finally, it also indicated that there an insignificant relationship between mobile money services use and revenue of banking industry (Sig. Value=0.435). The study thus recommends that commercial banks in Zambia which have not yet collaborated with MMOs should adopt the use of mobile money services on their platforms as it is highly reliable, accessible and reduces congestion in bank premises by customers who come to make transactions. This will help to boost financial performance in the banking industry.

Key words: Banking industry, financial performance, Mobile money, Profitability

INTRODUCTION

The introduction of Mobile Money Services (MMSs) in Zambia by the mobile network operators namely, Airtel, MTN and Zambia Telecommunications Company (ZAMTEL) to their customers has become a way of gaining competitive advantage through diversification, maintaining customer loyalty and increasing the market share in order to grow their profitability and improve their financial position. Zambia has recorded a significant increase in the number of mobile cell phone subscribers from 2.6 million in 2007 to 10.9 million in 2015 (ZICTA, 2016) and 17.2 million in 2019 due to the increased investment in the sub-sector by mobile service providers (Statista, 2020). Thus, a well-developed financial system helps in efficiency and effectiveness of the commercial banks and is an important concept in operation of the banks in a highly competitive environment. The high competition has led firms to embrace the concept of mobile money to develop a competitive edge and stay in the market. The mobile money platform is a financial innovation that could have effects on the commercial banks’ profitability. This is due to the fact that all the people who have mobile cell phones can access the mobile money services. For instance, Zambia has an estimated population of about 19,065,005 million people, according to World Population Review (2021), out of which 17.22 million people are mobile cell phone subscribers according to Statista (2020).

In Zambia, the advent of mobile money services dates back to two decades ago when the now unlicensed (on allegations of fraudulent activities and operational challenges) Celpay launched a mobile payment product in 2002 before being joined by Zoona years later in 2009 (Cooper, et al., 2019). Although Zoona built a strong brand and became a mobile money household name, the entry of Mobile Network Operators (MNOs) in the names of Airtel, MTN and Zamtel in 2011, 2012 and 2017 respectively, massively hurried the pace of adoption mirroring paths of Kenya and Uganda on the continent (Kabala & Seshamani, 2016; GSMA, 2019; Cooper, et al., 2019). At the end of 2019, the number of registered mobile money accounts increased more than 9-fold to over 41 million from 1.4 million in 2012 while the number of active mobile money agent outlets per 1000 square meters jumped to 98 from 2 over the same period. As a result, the volume and value of transactions have grown exponentially over the years. Payments data from the Bank of Zambia (BoZ) indicate a surge in volumes to 750.5 million in 2020 from 17.4 million in 2012 with corresponding value figures rallying over 9000% to ZMW 105.82 billion from ZMW 1.16 billion. Actually, the value of payments made via mobile money surpassed the figure for check settlements in 2018 (ZMW 22.19 billion vs ZMW 12.42 billion).

In addition to the above controversy in empirical findings in countries, published studies on mobile money in Zambia have largely concentrated on drivers behind increasing adoption (Mintz-Roth, 2018; Njele & Phiri, 2021), influence on financial inclusion (Kabala, et al., 2018) and recently impediments on greater adoption (Chipa & Mwanza, 2021). In view of the foregoing, it remains empirically unclear on what the effect of continuously flourishing mobile money services is on profitability of commercial banks in Zambia.

Statement of the Problem

Mobile money was primarily responsible for the nation’s 10.1 percentage point improvement in financial inclusion, which saw it rise from 59.3 percent in 2015 to 69.4 percent (Finscope, 2020). In contrast to the volume of transactions in the first half of 2021, the value of mobile money transactions showed a declining trend in the first half of 2022. In particular, there was a 33.7 percent decrease in the value of transactions from ZMW 76.0 billion in the first half of 2021 to ZMW 50.4 billion in the same period in 2022. In a similar vein, the number of transactions decreased by 22.6 percent, from 358 million in the first half of 2021 to 277 million (Banda, 2022). The primary cause of the decline in mobile money volumes and values was the advent of near alternatives, such as the expanding agency banking network that most commercial banks have implemented. By providing a variety of financial services via their networks, mobile phone service providers have, in this sense, further integrated mobile money services into the financial industry. The successful deployment of mobile money in sub-Saharan Africa coupled with the leading role played by mobile network operators (MNOs) in the delivery of mobile money services (Pelletier et al., 2020; Sy et al., 2019) raises an important policy question about whether mobile money complements existing traditional financial services in relation to firm performance such as bank profitability.

Empirical evidence in this regard is limited as most studies focused on the firm-level implications of either traditional financial services or mobile money (Islam & Muzi, 2020; Islam et al., 2018) without testing for bank profitability. There is evidence showing that mobile money and traditional financial services coexist (Mwange, 2022), but it is not known how the interplay between these two financial services affects banking sector profitability productivity. There are mixed results from the few studies that demonstrate how mobile money affects commercial banks’ profitability in different countries, despite this significant advancement. In addition to the above controversy in empirical findings in countries, published studies on mobile money in Zambia have largely concentrated on drivers behind increasing adoption (Mintz-Roth, 2018; Njele & Phiri, 2021), influence on financial inclusion (Kabala, et al., 2018) and recently impediments on greater adoption (Chipa & Mwanza, 2021). In view of the foregoing, it remains empirically unclear on what the effect of continuously flourishing mobile money services is on profitability of commercial banks in Zambia. This investigation was carried out to fill up this knowledge gap.

Research Objectives

The study was guided by the following specific objectives:

- To examine the level of use of mobile money services in Zambia.

- To assess the measures of financial performance in the banking industry.

- To establish the relationship between mobile money services and financial performance of commercial banks.

EMPIRICAL LITERATURE REVIEW

Mobile banking is defined as “a form of banking transaction carried out via a mobile phone” (Migdadi, 2012). Moreover, it is defined as a “type of execution of financial services in the course of which – within an electronic procedure- the customer uses mobile communication techniques in conjunction with mobile devices”. Mobile banking is classified into three types – App-based banking, SMS banking, and USSD Banking. Mobile banking applications encompass the broadest range of banking services. The technologies generally used for mobile banking are Interactive Voice Response (IVR), Standalone mobile application clients, SMS and WAP. The delivery of a mobile banking service to a consumer involves the participation of four primary players; a bank, mobile network operator (MNO), a mobile banking technology vendor, and the consumer (Popkova & Haabazoka, 2019).

The ability of commercial banks to generate sustained profits is determined by their financial performance (Handema & Haabazoka, 2020). Bank managers place a high value on the identification and efficient management of the variables that affect financial performance levels. In the competitive operating business environment of financial institutions, managers must recognise and implement best practices to achieve outstanding performance, including leveraging innovation like mobile banking.

Heinle and Verrecchia (2016) carried out an on-line survey in Ireland and collected their data using the snowball sampling technique. According to research, consumers’ behavioural intention to use mobile banking in Ireland was significantly influenced by compatibility, perceived utility, and trust. Ireland’s consumers do not shun mobile banking because of inconvenience, security, or perceived risk issues.

Aziz, Badrawy and Hussein (2014) put forth a paradigm with the goal of examining and contrasting the factors and difficulties that affect Egyptian consumers’ intentions to use or adopt alternative self-service banking technologies. The data was analysed using cross tabulations, frequencies, and chi square tests. The three groups diverge greatly in terms of usage, value, risk, tradition, and image barriers. Significant correlations between adoption choices and knowledge of Internet banking, level of education, and type of mobile device ownership were also discovered.

Al-Jabri and Sohail (2012) used the dispersion of innovation hypothesis to examine Saudi Arabia’s choice in mobile banking. The study evaluated a variety of specialised characteristics and their effect on how flexible banking is received in third-world countries like Saudi Arabia. To evaluate the hypotheses and investigate factors that might affect mobile banking usage and reception, dispersion of progress was used. The report recommended that Saudi Arabian financial institutions offer mobile good banking services that take into account a variety of customers’ requirements, convictions, prior experiences, and habits while also satisfying customers’ needs. The study recognised and distinguished the impact of varied trade volumes on the financial planning of commercial banks.

Muisyo, Alala and Musiega (2014) evaluated the effect of mobile money services on banking institutions in Kenya. The study focused on commercial banks operating in Kakamega County. The study reveals that the introduction of a myriad of mobile money services (MMS) by various mobile money service providers to customers has become common in the recent years as a way of gaining competitive advantage through diversification, maintaining customer loyalty and increasing market share in order to grow their profitability and improve their financial position. The roll out of these services in developing countries has generated a lot of interest among various players in the financial sector of the economy. Such services include person to person (P2P) mobile money transfer (MMT), pay bill services, loan to customers and access to a wide range of banking services e.g. a/c balances, mini statements, transfer of money from one`s mobile line a/c to one`s own bank account.

Mutua (2013) examined how flexible savings affected the financial health of commercial banks in Kenya. The research outline was either descriptive or illustrative. The sample size included mobile utility administrators and 43 business banks operating in Kenya as of December 2012. The total amount of money transferred over mobile devices for the previous five years was gathered, and the number of customers was compared to the profitability of the bank as determined by investment returns. According to the study, there is only a weakly favourable association between mobile savings and Kenya’s business banks’ financial performance.

Kithaka (2014) studied how Kenyan business banks’ budgetary performance was impacted by their versatility. For this case, a cross-sectional survey research plan was used. This provided who, how, and what information about Kenya’s commercial banks’ use of mobile banking. All of the commercial banks in Kenya that offer mobile banking were examined as part of the study, which included a census survey. Secondary data were utilised in the study. The study concluded that mobile banking had a good and significant impact on Kenyan business banks’ financial performance.

Kathuo, Rotich and Anyango (2015) conducted a study on how mobile banking has affected Kenyan business banks’ financial success. In the study, a descriptive research plan was used. A total of 42 active Kenyan business banks were included in the sample as of December 2014. Primary data were gathered through questionnaires. Clear measurements were used for the analysis of measurable data, while descriptions were used to display subjective data. According to the survey, the number of mobile exchanges has dramatically increased in the most recent five years since the introduction of mobile banking. They concluded that banks that embraced mobile money services had an unfathomably wide customer base and, as

a result, had significantly improved their financial performance.

Katema and Lungu (2019) looked into the variables affecting Kitwe commercial banks’ adoption of mobile banking in Zambia. The study used simple random sampling to get a sample size of 60 while using purposive sampling to choose the commercial banks. The researchers employed descriptive statistics (measures of central tendency). According to the study findings, the majority of account holders are knowledgeable about using electronic banking services and are eager to adopt them for their banking requirements. According to the study findings, clients may now access their money whenever they want and believe that mobile banking is a cost-effective solution to reach the un-banked.

Mwiya et al. (2017) conducted an empirical study examining factors influencing e-banking adoption in Zambia. The study examined the influence of e-banking technology’s PU, PEU and trust (safety and credibility) on e-banking adoption. The findings indicated that modified TAM was applicable to the Zambian scenario for assessing, monitoring and increasing the adoption of e-banking services and that that PU, PEU and trust significantly and positively influences attitude to e-banking. In turn attitudes to e-banking influence intention and the actual adoption of e-banking services.

Lusaya and Kalumba (2018) conducted a research in Zambia, which was aimed at investigating the challenges of adopting the use of e-banking by customers. The results of the study found that e-banking usage dependent on the availability of e-banking information. This means that there is increased publicity on e-banking, it is expected that if many customers would use the service. The results also showed that education levels also have a statistically significant influence on e-banking usage. This means that the higher the level of education, the more the usage of e-banking services. This is in line with the technological acceptance model. The study found that at 5% level of significant, concern for personal security was not related to usage of e-banking services.

THEORETICAL LITERATURE REVIEW

Diffusion Theory

Rogers (2003) defined diffusion as the process by which an innovation is communicated through certain channels over time among the members of a social system. Rogers’ theory of diffusion contains four elements that are present in the diffusion of innovation process. The first is innovation which he defines as an idea, practice, or object that is perceived as new by an individual or other unit of adoption. The other is communication channel which is the means by which messages get from one individual to another. Time is the other that encapsulates innovation-decision process, relative time (innovation is adopted by an individual or group) and innovation’s rate of adoption. Last element is social system which is a set of interrelated units that are engaged in joint problem solving to accomplish a common goal. It seeks to explain how, why and at what rate new ideas and innovations spread through cultures. This can explain how financial innovation has evolved over time in the commercial banks in Zambia. Banks efficiency due to innovation takes time as it involves transmission of new ideas and processes to its customers and employees. This new idea has to be accepted by all stakeholders, shareholders to the customers, so that the social systems can understand the importance of the innovation despite high costs and work towards streamlining the processes (Honor, 1998).

Innovation Diffusion Theory is found most appealing in underpinning what the study attempts to achieve, largely due to the theory’s approach in identified four elements of innovation, time, communication channels, and the social framework that boast the spread of technological innovations as indicated by the works of Moris (1996) and Rogers (1983, 2003). Similarly, these elements are crucial and vital to commercial banks on any successful implementation of payments system technology project.

Silber’s Constraints Theory of Innovation

Silber (1975) attributes financial innovation to attempts by profit maximizing firms to reduce the impact of various types of constraints that reduces profitability. The theory points out that the purpose of profit maximization of financial institutions is the key reason of financial innovation. Moreover, their decrease in profitability, which can be attributed to external competition or government regulation, has provided these firms with the necessary motivation to increase profitability. Silber considers the main historical causes of innovation by US banks as a response to a reduction of their utility or adversity in innovation: The interest rate ceiling, where banks tried to endogenize exogenous items of the balance sheet (Certificate of Deposit and bank related commercial paper); decline in the market for particular assets; a declining growth rate of sources of funds (new products in order to get new sources of funds) and an increase of the risk of a particular asset or of all assets due to the economic environment are reason for financial innovation. On the hand, success innovations are the extensive use of cost reducing information technology and elaborate new finance theories in the financial sector and several new products designed to cope with the rising yield of assets in order to attract new funds.

Generally, Silber proposes that the three possible ways a financial institution could innovate, by endogenizing an exogenous item of the balance sheet, introducing an existing financial instrument from another country and thirdly as the mixture of the ways above, taking the form of modification of an existing instrument. The importance of Silber’s theory is that, by using the concept of financial innovation, he provides us with a wider spectrum of potential reason contributing to the innovating process that helps to improve the performance of financial institutions. The suggestion in the work of Silber is that investment in innovation is a rational response to an unfavourable competitive position (Silber, 1983).

Kane’s Theory of Innovation

Kane (1984) sees financial innovation as an institutional response to financial costs created by changes in technology, market need, and political forces, particularly laws and regulations. Financial industry is special, it has stricter regulations and financial institutions have to deal with these regulations in order to reduce the potential risks to minimum. Kane’s theory where an institution responds to the changes in its operating environment is the rise of the shadow banking system in the US Economics believes the current financial current crisis was triggered by the shadow banking system. As shadow banking institutions do not receive traditional deposits like a depository bank, they have escaped most regulatory limits and laws imposed on the traditional banking system. Members are able to operate without being subjected to regulatory oversight for unregulated activities. This parallel banking system essentially caused the credit market to freeze, due to lack of liquidity in the banking system. These entities which make up the shadow banking system include hedge funds, “borrowed short term in the liquid market and then purchased long term, illiquid risky assets”.

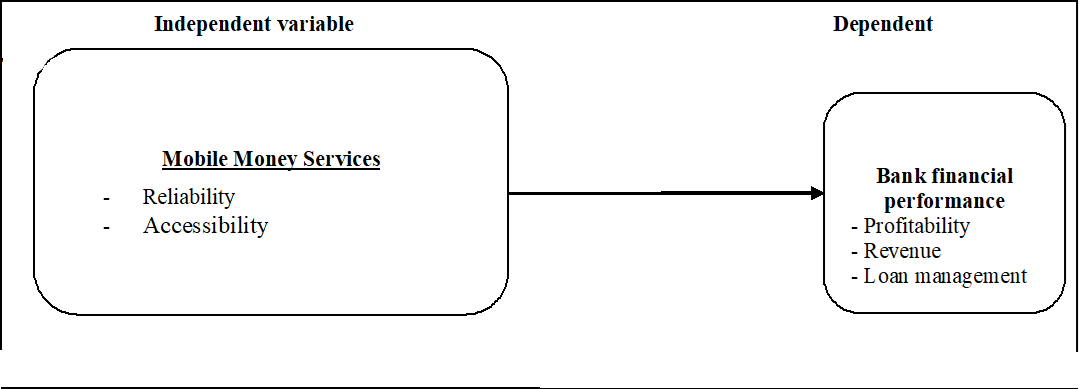

Conceptual Framework

The conceptual framework presents an integrated way of looking at a problem under study, as in Figure 1.0.

Figure 1.0: Conceptual Framework

Source: Researcher (2023)

Therefore, the effects of the services being provided by mobile money operators are presented well in the conceptual framework as shown. Based on how the behaviour influences the use of these services is fully much dependent on the reliability and accessibility of the services. This framework as said was used in helping to fully understand the way the mobile money services influence the financial performance of commercial banks due to less time taken to transact, easy accessibility to money, minimal transaction costs and also increased efficiency of the service.

Measures of “mobile money service” can be justified as connected to the reliability and accessibility of mobile money services based on several factors. These factors include transaction success rates, system uptime and downtime, network coverage and connectivity, agent distribution and availability, and customer support and service quality. High transaction success rates and system uptime indicate a reliable system, while comprehensive network coverage and reliable network connectivity ensure accessibility. Additionally, a wide network of agents and effective customer support contribute to the accessibility and reliability of mobile money services. By monitoring and improving these measures, mobile money service providers can enhance the reliability and accessibility of their services, ultimately promoting financial inclusion and facilitating economic transactions for users.

The present study had used these variables to investigate how the mobile money services provided by Airtel, MTN and ZAMTEL have impacted the profitability of the commercial banks in Zambia. Following the conceptual framework above, the general hypotheses below were generated:

H0: Mobile money services have no effect on the financial performance of commercial banks.

H1: Mobile money services have an effect on the financial performance of commercial banks.

RESEARCH METHODOLOGY

Research design

This study employed a descriptive research design involving both the qualitative and quantitative techniques. The mixed method approach involved a closed-ended questionnaire and an interview guide administered to different sets of respondents (Bank and MMO employees and regulators respectively). The choice of this design is supported by Silverman (1995) who says that “depending on theories, hypothesis and research questions, methods from both approaches can be used in the same research project.” The qualitative data was used because of the intention to gather information which could not be expressed in numbers and to enable the researcher to investigate the impact of mobile money services on the profitability of commercial banks in depth in Zambia.

Population of the Study

The target population of this study was 1,020 employees which included senior managers/executives in retail banking, customer services, operations and finance departments from all the 16 commercial banks in Zambia and mobile money operators (MMOs) while key informants were drawn from ZICTA and Zambia Institute of Bankers (ZIOB) as regulators and professionals with the knowledge about MMOs and commercial banks respectively.

Sample Size and Sampling Procedure

The sampling procedure involved purposive sampling and stratified random sampling of respondents from the study institutions. The process involved purposive selection of individuals from commercial banks, MMOs, ZICTA and ZIOB based on the researcher’s knowledge and judgement. The sample of the study was 156 successful respondents determined using De Vaus’ (2016) formula as follows:

X=n/(1+n(e)²)

X=Sample size, n=total population, e=level of error which is 5% at 95% confidence level.

Therefore, the calculation for sample size in this study is as follows:

= 1020/ (1+1020(0.05) ²)

= 1020/ (1+1020(0.0025)

= 1020/ (1+2.55)

= 1020/ (3.55)

= 287 respondents

A total of 287 questionnaires were administered using Google forms via WhatsApp contacts and email addresses. From the total questionnaires sent to respondents in 12 banks out of the 16, and all three MMOs, only 156 questionnaires were returned, representing a 54% response rate.

Data Collection

This research cannot be complete without raw unpublished data being collected from the field. It is important to this study because the data was unique and answers specific research questions. This data were collected using quantitative and qualitative data collection tools such as questionnaires and the interview guides. The research tools were tested before conducting the main study using a pilot study in an environment with similar characteristics as the environment in which the main study was to be conducted. This was done in order to determine stability of the data collection tool.

Data Analysis

The quantitative primary data were analysed using SPSS package to generate descriptive and inferential statistics. The strength and connection between the independent factors and financial performance were evaluated using Pearson’s correlation method. Analysis of Variance (ANOVA) and regression of coefficients were used in the analysis, and regression analysis was also used to evaluate the model’s fitness (R-squared). Tables and figures were used to present the data. The degree to which all of the independent variables together predict financial performance was explained by the model’s fitness. Using the standard threshold of significance of 0.05, ANOVA statistics explained the model’s overall significance. Qualitative data that were collected through the use of the interview guides with the key informants were analysed qualitatively through revelation themes that emerged from the collected data. Qualitatively, the researcher transcribed all the interview responses from key informants to make descriptive representations of study findings that emerged from this study.

RESEARCH RESULTS AND ANALYSIS

Level of Use of Mobile Money Services in Zambia

The descriptive statistics provided knowledge on the level of mobile money services available in the banking industry. Means were used as a basis for determining the level of reliability and accessibility of mobile money services while ranks were used to identify the factors that were most rated and least rated by participants. Six (6) items were used to measure the reliability of mobile money services where participants were asked to rate the items on a 5-point Likert scale. The findings from the analysis revealed that the reliability on mobile money services in the banking industry is generally high observed from an overall mean of 3.71.

Table 1: Reliability of mobile money services

| Factors | Mean | Std Dev. | Rank | Interpretation |

| Mobile money services have improved on the financial performance of commercial banks. | 4.40 | 0.721 | 1 | Very high |

| Most companies have tried to develop their own mobile money service platforms. | 4.37 | 0.687 | 2 | Very high |

| Mobile money services affect the financial performance of commercial banks. | 4.02 | 1.038 | 3 | High |

| Most customers use both mobile money services and banking services simultaneously. | 3.62 | 1.207 | 4 | High |

| Mobile money service charges are cheap compared to bank charges. | 2.12 | 0.878 | 5 | Low |

| Overall mean | 3.71 | High |

Source: Field data (2023)

It was observed that the level of accessibility to mobile money services in the banking industry is high indicated by a general mean of 4.17. This was supported by a very high level at which mobile money services are available at commercial banks in Zambia, this being ranked the first in the construct with a mean response of 4.83 and a very small standard deviation of 0.43.

Table 2: Accessibility of mobile money services

| Factors | Mean | Std Dev. | Rank | Interpretation |

| Mobile money services are available at all banks | 4.83 | 0.430 | 1 | Very high |

| Mobile money services enable customers to receive, send or pay for any utilities anywhere at any time. | 4.63 | 0.525 | 2 | Very high |

| Your organization adopted any mobile money services. | 4.54 | 0.670 | 3 | High |

| Mobile money services are easily accessible than banking services. | 4.50 | 0.672 | 4 | High |

| Overall mean | 4.63 | Very high | ||

| Table 1 & 2 | ||||

| General mean (Reliability + Accessibility) | 4.17 | High |

Source: Field data (2023)

Measures of Financial Performance in the Banking Industry

Financial performance according to Bodie, Kane and Marcus (2005) is the level of performance of a firm over a specific period of time and expressed in terms of the overall profits or losses incurred over the specific period under evaluation.

Table 3: Profitability of commercial banks

| Factors | Mean | Std Dev. | Rank | Interpretation |

| Much of banks’ profits are from customers deposits | 4.73 | 0.528 | 1 | Very high |

| Banks earn a lot of profits from their customers | 4.69 | 0.579 | 2 | Very high |

| Giving out too much loans generate more profits | 4.67 | 0.550 | 3 | Very high |

| Loans, mortgages and bank charges provide banks with high margins | 4.50 | 0.754 | 4 | Very high |

| The size of the bank affects its profits | 4.02 | 1.146 | High | |

| Overall mean | 4.52 | Very high |

Source: Field data (2023)

Financial performance is measured in terms of profitability, loan supervision and revenue sources of the commercial banks. Profitability was used to measure how banks earn their profits from their operations.

Table 4: Loan portfolio management

| Factors | Mean | Std Dev. | Rank | Interpretation |

| Banks put pressure on the borrowers to retire the loan from earning. | 4 63 | 0.687 | 1 | Very high |

| The loan will customarily be accompanied by written covenant of the borrower to conduct activities in a way agreed upon by Very high the bank. | 4.48 | 0.779 | 2 | Very high |

| Substantial credit is advanced for a period of more than one year | 4.40 | 0.799 | 3 | Very high |

| Commercial banks are able to meet their long term obligation such as loans from the central bank. | 3.35 | 1.327 | 4 | Medium |

| Banks are quick to sell off property that is given to them as collateral. | 2.40 | 1.125 | 5 | Low |

| Overall mean | 3.85 | High |

Source: Field data (2023)

It was indicated from the overall mean that there was a high level of loan supervision in the banking industry observed from an overall mean of 3.85.

Table 5: Revenue sources

| Factors | Mean | Std Dev. | Rank | Interpretation |

| Banks receive revenue from interests | 4.65 | 0.556 | 1 | Very high |

| Revenue that is earned by banks is gotten from

investments that the bank is involved in (e.g. securities) |

4.54 | 0.699 | 2 | Very high |

| Banks aim to grow revenue by expanding their customer base. | 4.46 | 0.699 | 3 | Very high |

| Banks have a lot of liquid assets at their disposal,

i.e. assets that can be easily turned into cash. |

4.08 | 1.064 | 4 | High |

| Banks are able to meet their short-term obligations. | 2.83 | 1.133 | 5 | Medium |

| Overall mean | 4.11 | High | ||

| Table 4 & 5 | ||||

| General mean | 4.16 | High |

Source: Field data (2023)

The evidence from the findings shows that the level of bank revenue is generally high implied by an overall mean response of 4.11. It was thus observed from the general mean (4.16) that there was a relatively high level of financial performance in the banking industry.

Relationship between Mobile Money Services and Financial Performance of Commercial Banks

Pearson correlation coefficients were computed to determine the strength of the relationships between the different measures of use mobile money services and those of financial performance.

Table 6: Pearson’s Correlation Co-efficient

| Covariates (Predictors) | Reliability of mobile money services | Accessibility of mobile

money services |

| Profitability | Pearson Correlation | |

| -0.149 (0.292) | 0.197 (0.161) | |

| Loan portfolio | 0.132 (0.350) | -0.052 (0.712) |

| Revenue | -0.021 (0.884) | 0.182 (0.198) |

| (**)= p. values and Correlation is significant if p. value <0.05 | ||

Source: SPSS Output (2023)

The correlation coefficient between reliability of mobile money services and profitability was -0.149 with a p-value of 0.292. This implied that there is a very weak negative relationship between reliability on mobile money services and profitability of the banking industry. Also, the p-value suggests that the relationship is not statistically significant at 5% and 1% levels of significance. Similarly, the correlation coefficient between reliability and loan supervision was indicated by r=0.132 with a p-value of 0.350. This signified a very weak positive relationship between reliability of mobile money services and loan supervision. The p-value indicated that the relationship is not statistically significant at both 5% and 1% levels of significance since it is greater than 0.05 and 0.01 respectively. Looking at the reliability on mobile money services and revenue of the bank, it was indicated from r=0.021 that there is a very weak positive relationship between the two indicators. Also, the p-value of 0.884 suggested that the relationship is not statistically significant at both 5% and 1% levels of significance.

Relative to the relationship between reliability and the different measures of performance of banks, it was also indicated from the r value (0.197) and p-value of 0.161 that there is a very weak positive and insignificant relationship between the accessibility of mobile money services and profitability of banks. Furthermore, it was observed from r = -0.052 and value of 0.712 that a weak negative and insignificant relationship exists between accessibility to mobile money services and loan supervision of banks. Lastly, the relationship between accessibility and revenue of banks was indicated to be weak, positive and insignificant at 5% and 1% levels of significance as observed from the r. value of 0.182 and p-value of 0.198.

In general, it was observed that all measures of use of mobile money services are not significant at both 5% and 1% and that they have weak relationships with financial performance of commercial banks. This could be because most bank customers do not use the services provided on mobile money due to high charges and also the distribution of bank branches around the country also makes customers easily access banks in their localities and has reduced congestion in banks. From the findings in the table, the F. value of the model is 1.06 1, overall sig. value = 0.212 and R squared value 0.061. This implied that the relationship between the use of mobile money services and profitability of commercial banks is not statistically significant observed from the overall sig. value which is greater than 0.05 and a relatively a very small F-value. The R squared value indicated that there is 0.061 (6.1%) variability between the use of mobile money services and profitability of the banking industry. The unstandardized coefficient for reliability as presented in the table is -0.133, t-value = -1.083, and sig. value = 0.284. Therefore, as it is observed that the sig. value is greater than 0.05, level of significance and the magnitude of t-value is less than 2, then this implies that reliability of mobile money services is not statistically significant. However, it was observed from the coefficient that a negative relationship exists between reliability on mobile money services and profitability of the banking industry.

Table 7: Multiple regression analysis

| Model | Unstandardised

Coefficients |

Standardised coefficients | Std. Error | t. value | Sig. value

|

|||

| B | Beta | |||||||

| (Constant) | 3.886 | 1.167 | 3.159 | 0.003 | ||||

| Profitability | ||||||||

| Reliability | -0.133 | -0.150 | -1.083 | -0.025 | 0.284 | |||

| Accessibility | 0.244 | 0.198 | 1.429 | 1.278 | 0.159 | |||

| F. value = 1.601, R. Square = 0.061, overall sig. value=0.212 and df~= 2 | ||||||||

| Loan portfolio | ||||||||

| Reliability | 0.147 | 0.133 | 0.157 | 0.937 | 0.353 | |||

| Accessibility | -0.082 | -0.053 | 0.219 | -0.375 | 0.709 | |||

| F. value = 0.508, R. Square = 0.020, overall sig. value=0.605 and df~ 2 | ||||||||

| Revenue of the banking industry | ||||||||

| Reliability | -0.021 | -0.021 | 0.132 | -0.152 | 0.880 | |||

| Accessibility | 0.238 | 0.182 | 0.182 | 1.293 | 0.202 | |||

| F. value = 0.8471, R. Square 0.033, overall sig. value=0.435 and di~= 2 | ||||||||

Source: SPSS Output (2023)

Similarly, the unstandardized coefficient for accessibility B =0.244, t-value =1.429, and sig. value= 0.159. Since the sig. value is greater than p=0.05 and t-value is small then this implies that accessibility of mobile money services is not significant at 5%. But as indicated from the B value of 0.244, a positive relationship exists between accessibility of mobile money services and profitability and as accessibility increases by a unit, profitability of the banks increases by 0.133 (13.3%).

Loan portfolio and use of mobile money services

From the findings in the table, the F-value of the model is 0.508, overall sig. value = 0.605 and R squared value = 0.020. This implied that the relationship between the use of mobile money services and loan supervision of the banking industry is not statistically significant observed from the overall sig. value which is greater than 0.05 and a relatively a very small F-value. The R squared value indicated that there is 0.0.02 (2%) variability between the use of mobile money services and loan supervision of the banking industry. The unstandardized coefficient for reliability as presented in the table is 0.147, t-value = 0.937, and sig. value = 0.3 53. Therefore, as it is observed that the sig. value is greater than 0.05, level of significance and the magnitude of t-value is less than 2, then this implies that reliability of mobile money services is not statistically significant. However, it was observed from the coefficient that a negative relationship exists between reliability on mobile money services and loan supervision of the banking industry.

Similarly, the unstandardized coefficient for accessibility is β-0.082, t-value -0.375, and sig. value 0.709. Since the sig, value is greater than α=0.05 and t-value is small then this implies that accessibility of mobile money services is not significant at 5%. But as indicated from the β value of -0.082, a negative relationship exists between accessibility of mobile money services and loan supervision and as accessibility increases by a unit, loan supervision of the banks increases by 0.147 (14.7%).

Revenue and use of mobile money services in the banking industry

From the findings in the table, the F-value of the model is 0.847, overall sig. value = 0.43 5 and R squared value = 0.033. This implied that the relationship between the use of mobile money services and revenue of the banking industry is not statistically significant observed from the overall sig. value which is greater than 0.05 and a relatively a very small F-value. The R squared value indicated that there is 0.033 (3.3%) variability between the use of mobile money services and revenue of the banking industry. The unstandardized coefficient for reliability as presented in the table is -0.021, t-value = -0.152, and sig. value 0.880. Therefore, as it is observed that the sig. value is greater than 0.05, level of significance and the magnitude of t-value is less than 2, then this implies that reliability of mobile money services is not statistically significant. However, it was observed from the coefficient that a negative relationship exists between reliability on mobile money services and revenue of the banking industry. Similarly, the unstandardized coefficient for accessibility is β =0.238, t-value =1.293, and sig. value= 0.202. Since the sig. value is greater than α=0.05 and t-value is small then this implies that accessibility of mobile money services is not significant at 5%. But as indicated from the β value of 0.238, a positive relationship exists between accessibility of mobile money services and revenue and as accessibility increases by a unit, revenue of the banks increases by 0.020 (2%). From the summary of the analysis, therefore, the regression models on the use of mobile money services and financial performance is derived from the coefficients and is given by:

Profitability = 3.886 – 0.133REL + 0.244ACC

Loan supervision = 3.688 + 0.147REL – 0.O82ACC

Revenue = 3.086 – 0.O2OREL + 0.238ACC

Where:

REL = Reliability of mobile money services

ACC = Accessibility of mobile money services

The value 3.886 shows the level of profitability of the banking industry given non-usage of mobile money services.

The value 3.688 shows the level of loan portfolio of the banking industry given non-usage of mobile money services.

The value 3.086 shows the level of revenue of the banking industry given non-usage of mobile money services.

Table 8: Summary of hypotheses testing

| Hypothesis | Sig. value | Decision | |

| H01 | Reliability of MMS has no significant effect on profitability of banking sector | 0.284 | Supported |

| H02 | Accessibility of MMS has no significant effect on profitability of banking sector | 0.159 | Supported |

| H03 | Reliability of MMS has no significant effect on loan portfolio management | 0.353 | Supported |

| H04 | Accessibility of MMS has no significant effect on loan portfolio management | 0.709 | Supported |

| H05 | Reliability of MMS has no significant effect on revenue of the banking sector | 0.880 | Supported |

| H06 | Accessibility of MMS has no significant effect on revenue of the banking sector | 0.202 | Supported |

SUMMARY, CONCLUSION AND RECOMMENDATIONS

Summary of Findings

Level of Use of MMS in the banking Industry

The findings revealed that there is generally a high level of use of mobile money services in commercial banks. This is attributed by the fact that there is high reliability on services provided by mobile money evidenced by a mean response of 3.71 and also the services being highly accessible to customers indicated by a mean response of 4.63. Also, MMS’ efficiency does not require standing in queues when making transaction, as it is in the banking industry. This in other words saves banks from crowds that would flow in to make elementary transactions like paying school fees, paying electricity, and water and TV bills. This finding is further explained by the study carried out by Yao et al. (2018) which asserted that mobile devices, especially smart phones, are the most promising way to reach the masses and to create “stickiness” among current customers, due to their ability to provide services anytime, anywhere, high rate of penetration and potential to grow.

Measures of financial performance in the banking industry in Zambia

There was a high level of profitability in the banking industry as it was indicated by an overall mean of 4.52, a high level of loan supervision observed from a mean response of 3.85 and relatively high revenue indicated by a mean response of 4.11. This is explained by the dominance of very few top banks in the banking sector implying that despite having a market driven banking industry, the industry is oligopolistic in nature, dominated by few and short of competitiveness efficiency advantage. To a great extent, the market behavior of interest rates is influenced by these top banks. They become market price setters and the clients who desperately crave for bank loans are price takers. The study finding is also supported by Siame’s (2019) study concerning the best and worst performing banks in Zambia which indicated that the number of banks making the top five in profitability had ROA ranging from 24% to 43%.

Relationship between MMS and financial performance of Commercial banks

From the findings of this study, it was indicated that the relationship between mobile money services (reliability and accessibility) and financial performance (Profitability, revenue and loan portfolio management) in the banking industry was generally a weak, negative and insignificant one observed from a small correlation coefficient of r= -0.149 and sig. values greater than 0.05. These findings are in line with the findings of Opare (2018). In his study about mobile banking and financial performance of commercial banks in Ghana, he concluded that there is a weak direct relationship between mobile banking and financial performance.

Conclusion

There is a high level of use of MMS in Zambia due to the reliability, accessibility and convenience of the services. Various studies point to the vital role MMS can play in improving the flow of resources in emerging economies of Africa. This potential lies in the ability that MMS have to allow money to flow electronically rather than physically, thereby eliminating or reducing the spatial and temporal barriers to money transfer.

The measures of financial performance of the banking sector were found to be profitability, loan portfolio management and revenue. These were the financial performance measurement indicators adapted and consequently interrogated with the various respondents.

A weak positive and insignificant relationship between the use of MMS and financial performance of commercial banks was the major study finding. While findings of the study indicated that the MMS have a weak positive effect on financial performance, it would require an open business model that involves all stakeholders to establish a truly national solution. Furthermore, the contribution of MMS to financial performance is in improving money transfer by lowering the transaction costs for big volumes. In addition, the mobile money accounts do not necessarily increase the number of account holders in the banks making their contribution to financial performance limited to improving payments and money remittances.

Recommendations

To get maximum benefits from mobile money innovation, and arising from the findings and analysis of the study results, the following recommendations are made:

- Free training and refreshing training should be provided to staff of the financial institutions and if possible to customers to equip them with skills in the ever changing technology.

- Commercial banks in Zambia should provide toll free lines to enable query resolutions as the MMOs are currently doing, in case of any problem that deserves attention of the banking institution.

- Agency banking should take a center stage in the banking institutions’ short term strategic plans to deepen financial services further and ensure inclusion of the unbanked and the under banked as this is a huge market that remains a priority focus of the mobile money service providers.

- If possible banks should target to recruit as many agents as mobile money service providers have done as well as reduce agency banking fees to make their services affordable to the low-income earners.

- Commercial banks which have not yet entered partnerships in sharing platforms with MMOs should urgently collaborate with MMS providers in order to forge synergies for sustainable competitiveness.

REFERENCES

- Al-Jabri, I. M., & Sohail, M. S. (2012). Dispersion of innovation and its effect on mobile banking adoption in Saudi Arabia. The Electronic Journal on Information Systems in Developing Countries, 52(2), 1-15.

- Aziz, R. A., Badrawy, E. M., & Hussein, R. (2014). Investigating the factors affecting the adoption of alternative self-service banking technologies: The case of Egypt. International Journal of Marketing Studies, 6(5), 41-55.

- Banda, S. (2022). Impact of near alternatives on mobile money transactions in Zambia. Journal of Financial Innovation, 8(2), 78-92.

- Bodie, Z., Kane, A., & Marcus, A. (2005). Investments. McGraw-Hill Education.

- Chipa, M., & Mwanza, L. (2021). Impediments to greater adoption of mobile money in Zambia. Journal of African Business, 13(4), 245-262.

- Cooper, M., et al. (2019). The evolution of mobile money services in Zambia: A historical perspective. Journal of Financial Technology, 5(3), 112-127.

- De Vaus, D. (2016). Surveys in social research. Routledge.

- (2019). Mobile money in Zambia: Recent trends and future prospects. Retrieved from [link]

- Handema, S., & Haabazoka, F. (2020). Factors influencing financial performance of commercial banks in Zambia. International Journal of Economics, Commerce and Management, 8(1), 45-62.

- Heinle, M. C., & Verrecchia, R. E. (2016). Consumer intention to use mobile banking: The case of Ireland. Journal of Banking & Finance, 70, 6-14.

- Islam, M. M., & Muzi, M. K. (2020). Empirical evidence on the effects of traditional financial services and mobile money on bank profitability. Journal of Financial Services Research, 58(3), 215-230.

- Islam, M. M., et al. (2018). Coexistence of mobile money and traditional financial services: Evidence from developing countries. Review of Development Finance, 8(2), 146-157.

- Kabala, P., et al. (2018). Impact of mobile money on financial inclusion in Zambia. Journal of African Economics, 20(4), 213-228.

- Kabala, P., & Seshamani, V. (2016). Mobile money adoption in Zambia: A comparative analysis. African Journal of Business Management, 10(3), 56-68.

- Kane, E. J. (1984). Financial innovation and regulation in the twentieth century. Journal of Economic History, 44(3), 674-677.

- Katema, M., & Lungu, I. (2019). Factors affecting adoption of mobile banking in Kitwe, Zambia: A qualitative study. Journal of Banking and Finance, 7(1), 32-45.

- Kathuo, N. A., Rotich, P., & Anyango, W. (2015). Impact of mobile banking on the financial performance of Kenyan commercial banks. International Journal of Business and Commerce, 4(1), 1-15.

- Kithaka, W. M. (2014). Influence of mobile banking on the financial performance of commercial banks in Kenya. European Journal of Business Management, 10(2), 76-88.

- Lusaya, C., & Kalumba, M. (2018). Challenges of e-banking adoption in Zambia: A case study of Lusaka. Journal of Finance and Accounting, 6(4), 132-145.

- Muisyo, D., Alala, O. B., & Musiega, D. (2014). Impact of mobile money services on banking institutions in Kenya. International Journal of Finance and Banking Research, 1(2), 15-30.

- Mwiya, B., et al. (2017). Factors influencing e-banking adoption in Zambia: An empirical study. Journal of Information Technology and Economic Development, 8(1), 25-40.

- Mutua, J. W. (2013). Flexible savings and financial health of commercial banks in Kenya. African Journal of Economic Review, 1(1), 12-28.

- Njele, C., & Phiri, M. (2021). Drivers behind increasing adoption of mobile money in Zambia. International Journal of Economics, Commerce and Management, 9(1), 78-93.

- Opare, M. A. (2018). Mobile banking and financial performance of commercial banks in Ghana. Journal of Economics and Business Management, 6(3), 123-135.

- Pelletier, A., et al. (2020). Role of mobile network operators in mobile money services delivery in sub-Saharan Africa. Journal of African Studies, 7(2), 56-67.

- Popkova, E. G., & Haabazoka, F. (2019). Mobile banking in Zambia: A technological perspective. Journal of Information Systems in Developing Countries, 45(1), 34-47.

- Rogers, E. M. (2003). Diffusion of innovations (5th ed.). Free Press.

- Siame, G. (2019). Best and worst performing banks in Zambia. Zambia Daily Mail. Retrieved from: www.zambiadailymail.co.zm.

- Silber, W. L. (1975). Constraints on the creation of innovation in financial services. Journal of Money, Credit and Banking, 7(2), 115-131.

- Sy, A., et al. (2019). Leading role of mobile network operators in mobile money services: Insights from sub-Saharan Africa. Journal of Business Economics Research, 13(3), 98-112.

- Yao, L., et al. (2018). Mobile devices and financial services: A promising future for banking. Journal of Financial Innovation, 9(2), 87-99.

- ZICTA. (2016). Mobile phone subscribers in Zambia. Retrieved from https://www.zicta.zm/services/consumer-protection/mobile-phone-security.