Analysis of Exchange Rate Fluctuations on Economic Growth in Nigeria

- Dr. David Ogwuche

- Jeremiah M. Tule

- Racheal L. Jeremiah Dandaura

- Gabriel Akogwu

- Emmanuel O. Nkpubre

- 128-141

- Jul 26, 2024

- Economics

Analysis of Exchange Rate Fluctuations on Economic Growth in Nigeria

Dr. David Ogwuche, Jeremiah M. Tule*, Racheal L. Jeremiah Dandaura, Gabriel Akogwu, Emmanuel O. Nkpubre

Bingham University, Nasarawa, Nigeria

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2024.807011

Received: 30 May 2024; Revised 20 June 2024; Accepted: 24 June 2024; Published: 26 July 2024

ABSTRACT

Motivated by the 2023 exchange rate reforms that led to significant depreciation of the domestic currency and macroeconomic instability, the paper examines the effect of exchange rate fluctuations on economic growth in Nigeria, using quarterly data from 2010:1 to 2023. The nonlinear autoregressive distributed lag approach was employed to analyse real GDP, exchange rate, crude oil price and macroeconomic instability. The overall result suggests a long run relationship between exchange rate and economic growth. The short run dynamic shows past and current exchange rate depreciation have positive and significant impact on economic growth while the past value of exchange rate depreciation exacts a negative and significant influence on growth. The results also reveal that positive oil price has stimulated economic growth while structural break has negative and strong effect on economic growth. The long-run result shows that both positive oil price and macroeconomic stability have positive effect on economic growth. This highlights the significance of oil price when assessing the relationship between exchange rate and economic growth in Nigeria. The paper recommends that the central bank should review sectoral credit policy to encourage lending to the productive sectors of the economy. The government should intensify economic reforms to diversify the economy by investing in the mining and agricultural sector with emphasis on refined and finished products. The government should address structural imbalance by building sustainable roads, rails, while policy related issues should be designed and carefully implemented to avoid shocking the economy.

Key words: Nonlinear ARDL, Exchange rate, real GDP, Oil Price

Jel Classification Code: C13; F31; O47; Q41

INTRODUCTION

Recent performance of the naira exchange rate following harmonised of the exchange rate market has renewed interest on the impact of exchange rate fluctuation on the domestic economy, particularly for resource rich countries. Exchange rate plays an important role on cross-border trade while serving as an indicator for economic performance. This can either be determined by either exogenous shock or policy induced factors which can influence trade flows with implications for macroeconomic performance of an economy (Nacita, 2013; ECB, 2016). Commodity exporting countries are prone to commodity price shocks. (Weeks, 2008; Wang, 2009). Empirical evidence on the link between exchange rate and economic growth have been established, however, most of the studies place emphasis on the real effective exchange while few consider the nominal exchange rate. For instance, Ahmad (2016) and Aloui et al. (2018) report a negative effect of exchange rate on growth in Asia, Saudi on the contrary Zoramawa et al. (2020) found a positive impact of exchange rate for Nigeria and Saudi. The impact of exchange rate fluctuation on growth is more pronounced for resource rich countries given their exposure to shock. However, Enilolobo et al. (2017) shows that exchange rate has no impact on output.

The dominance of oil sector in Nigeria exposes the economy to external shock, leading to depreciation of the domestic currency and low output. For instance, the 2008 global financial crisis (GFC), 2016 economic recession and the covid-19 pandemic induced shock all impacted the exchange rate and the domestic economy. Both monetary and fiscal policies were implemented to correct distortion. From 2000 to 2010, annual growth rate average 8.4 per cent, the GDP was rebased, thereafter, the economy declines to 2.7 percent by 2015, and in 2016, the economy slumps due to oil price shock. Thereafter, annual growth remains sluggish averaging 3.0 percent after a negative output in 2020. Annual exchange rate averaged US$/N130.00 before gaining value by 2008 at US$/N118.99, however, the GFC, the naira tumbled and maintained depreciation for the rest of the period reaching US$/N924.67 at the end of 2023. Despite the effort to stabilise the naira through supply of foreign exchange to the Bureau de change, banning of cryptocurrency and the unification of exchange rate, naira continued to depreciate reaching US$/N1505.30 by March 2024. This has created business uncertainty leading to mass exit of multinational companies. The emergence of cryptocurrency presents a threat to the monetary authority (Voice of America, 2024).

The objective of the paper is to assess the effect of exchange rate fluctuation on economic growth in Nigeria, amidst high domestic prices, structural imbalance, and crisis episodes. The research will fill the gap by employing a quarterly series and asymmetric approach to analyse exchange rate and growth nexus. It further accounts for the role of oil price, macroeconomic instability and structural changes on output in Nigeria. The research should provide insights to policymakers on the impact of exchange rate fluctuation on output for a resource rich economy.

CONCEPTUAL CLARIFICATION AND LITERATURE REVIEW

Exchange Rate Fluctuation

The concept of exchange rate fluctuation implies persistent change in the value of the domestic currency relative to another currency. This is common with exchange rates since currencies are being traded like other commodities. A currency fluctuates based on prevailing economic conditions. A country’s currency can be traded against another currency at a given period (OECD, 2024). There are five exchange rates—the average exchange rate, nominal effective exchange rate, real exchange rate, real effective exchange rate and bilateral effective exchange rate.

Economic Growth

This measures a country or a firm functionality in terms of efficiency to achieve a desired objective. It measures the overall productivity and health of an economy and the well-being of the citizens. There are different indicators of economic performance. These include Economic Growth proxy by gross domestic product (nominal and real GDP), Employment and Unemployment, Balance of Payments, inflationary rate and inequality.

Structural Breaks

An economic problem is far deeper with permanent effect than short term fluctuations. In economics, structural issues related existing policies or sudden change in government policies and unethical private sector practices that impede efficient and fair production and distribution of goods and services (Abdel-Kader, 2013). Structural imbalances range from the absence of correct exploitation and redistribution of resources; poor infrastructure and governance; trade barriers, multiple tax regime, and political stability (Cerami & Cerami, 2013), Weak institutions, monotonous economy, explosive population growth and low savings (Kappel, 2003).

Macroeconomic Index

The macroeconomic index developed is another measuring the overall health of the economy. It is very broad, encompassing various aspects of the economy beyond real GDP. Given that real GDP is the targeted variable in the study, we developed an index to eliminate biasness, arising from exclusion of variables. Negative values of the index imply instability while the positive values indicate relative stability of an economy.

Theoretical Framework

Mundel-Flemming Model

The Mundell–Fleming model was independently developed by Robert Mundell 1963; and Marcus Fleming in 1962. The model is also known as the Investment-Savings and Liquidity-Money ((IS-LM) model, with the extended version incorporating the balance of payments. This paper is underpinned by this model. The model describes how monetary and fiscal policy affect economy in fixed and flexible exchange rate regimes. The Mundel-Flemming model describes the case of a small open economy who trade in international goods, services, and financial assets. It assumes that domestic interest is the same with world interest rates.

When a country operates fixed exchange rate with perfect mobility, the fiscal authority maintains a fixed exchange rate such that monetary expansion or contraction will have no significant influence output and employment. On the other hand, fiscal policy can stimulate the economy, such that expansionary fiscal policy will raise domestic interest to attract capital inflow resulting to exchange rate appreciation. In the second case of flexible exchange rate with perfect capital mobility, the central bank does not intervene on regular basis. Exchange rates adjust to itself due to forces of demand and supply. The central bank can change the interest rate to affect the exchange rate and output money. Expansionary policy by central bank would cause capital reverse due to fall in interest rate.

Blanchard (2000) extended the model by introducing an arbitrage behaviour of financial investor who seeks the highest international rate of return on his investment such that at the equilibrium point the interest parity condition should hold (as cited in Fan & Fan, 2002). The theory explains that the behaviour of a country’s exchange rate dependents on the type of exchange rate regime, whether fixed or float or flexible exchange rate regime. The model is expressed as:

Y = real output, C is consumption NX as s net export, T is tax rate, I represent the domestic interest rate, r = world interest rate, G government spending, rate, e is the exchange rate, M real money supply, y. CA is current account while KA is capital account. Dornbusch, Fischer, and Startz assert for a small open economy with perfect capital mobility, such that BOP=0 at i=i therefore, there will be no equilibrium in the BOP unless domestic interest rate equals the global rate. The Mundel-Fleming model explain that the Bank can raise interest rate to attract foreign investment, which could impede output expansion due to increase in the cost of borrowing. On the other hand, increase in domestic production both from the oil and non-oil sector could generate foreign exchange earnings from export which stabilise the domestic exchange rate.

It has been argued that a country cannot pursue a fixed exchange rate regime with perfect capital mobility and at the same time maintain independency of the central bank. This argument led to the concept of impossible trinity. Consequently, a country must choose any two among the three options to pursue price stability.

Empirical Review

Several scholars have documented the link between exchange rate and economic growth, using different approach with different outcome. Some studies look at exchange rate volatility with little attention on exchange rate fluctuation. Nwikina et al. (2024) study exchange rate and economic growth using autoregressive distributed lag (ARDL) approach from 1985 to 2021. They conclude that the influence of exchange rate on GDP is weak.

Ewubare and Ushie (2022) also shows that the negative effect of exchange rate and inflation is detriment to output when they study exchange rate and output, using ARDL approach for the period 1981 to 2020. Notably, interest rate exhibits positive effect on output, a indicating the centrality of interest rate to stimulate the economy. Iheanachor and Ozagbe (2021) also study exchange rate and GDP during 1986 to 2019, while accounting for the role of inflation and foreign direct investment. The study shows that the naira exchange rate, capital reversal and inflation have negative and detrimental effect on output.

Kingsley et al. (2021) analyse the relationship between exchange rate and output, by accounting for the role of trade openness, gross capital formation, and inflation, the finding shows that inflation and exchange rate are key to output determination. Exchange rate movement can determine the level of output because of the pass-through of inflation to the domestic.

Henry et al. (2020) examines exchange rate fluctuation and economic growth in Nigeria, using the least square technique on annual frequency on inflation, exchange rate, public debt and from 1997 and 2017. The study reports a negative response of growth to exchange rate depreciation. Enilolobo et al. (2017) also adopt the least square estimator to test whether exchange rate influence growth, for the from 1981 to 2015. The authors report a weak relationship between exchange rate and output, however, oil price exhibits positive influence on output.

Kaharan (2020) considers exchange rate and growth nexus under an inflation targeting environment, using the Johansen cointegration, Ganger causality and innovation accounting techniques on quarterly series from 2002:1 to 2019:1. The findings suggest a negative relationship between the exchange rate and growth during the period.

In a standard VAR framework, Hoang et al. (2020) account for two exogenous factors (international price and Fed rate), however, their result present mixed outcome of exchange rate and growth nexus in Vietnam. The study establishes a negative relationship between exchange rate and economic growth in Turkey.

Ahmad et al. (2019) used the Generalized Method of Moment (GMM) and vector error correction model (VECM) to study exchange rate and output in Asian countries from 1970 to 2009. Their findings support the case of undervaluation of currency to boast cross-border trade and achieve growth.

Zoramawa et al. (2020) adopt the Johansen cointegration and error correction model to study the exchange rate dynamics and output for the period spanning. 1980 to 2019. Exchange rate stability during the period enhance economic growth but trade openness is a threat to sustaining the growth path.

Aloui et al. (2018) use Morlet’ wavelet technique to measure the relationship between exchange rate and output in Saudi Arabia, by accounting for oil price and inflation from 196 to 2014. Their findings suggest a strong lead-lag relationship, implying the exposure the economy to external shocks from oil price fluctuation. Dayo (2016) study account for oil price shocks and foreign reserves in an augmented Vector Autoregressive (SVAR) framework to analyse the impact of exchange rate on growth in Nigeria, using annual series from 1971 to 2014. The study finds a negative effect of oil price on real output, leading to the weakness of naira in the long run.

Stylised Facts

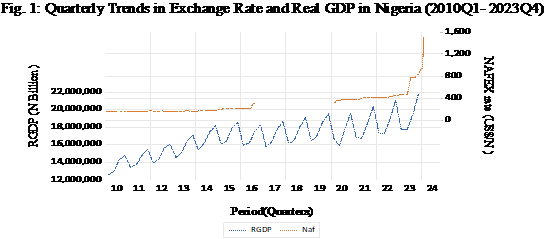

Fig.1 depicts the relationship between exchange rate and real output in Nigeria. Virtualization of the trend indicates a negative relationship. There was relative stability of exchange rate for most of the period until 2022 when exchange rate trend upward, following the adoption of a managed float and by 2023, the CBN switched from to a full flexible exchange rate regime where supply and demand forces determine the rate. However, the real GDP maintained an upward trajectory with stepwise movement, indicating some level of instability, occasioned by commodity shocks and macroeconomic uncertainty.

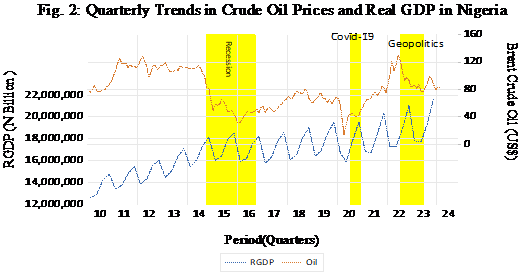

Fig.2 represents the trend between real GDP and crude oil prices. A glance at the trend reveals a co-movement between oil price and real GDP, as both moved in the opposite direction. This implies a negative relationship. We further identified three crisis episodes, the 2016 Nigerian recession, the COVID-19 pandemic, and geopolitical Risk in the shaded area. During oil price shock real GDP is more volatile compared to periods of positive outlook of international oil prices. The Nigerian recession coincides with dwindling oil prices, high uncertainty and low economic activities. The COVID-19 era is characterised by low aggregate demand, low output, and disruption in the supply chain. The geopolitical Risk is the period of geopolitical tension led by the Russian-Ukraine war, high global inflation, and interest rates hike.

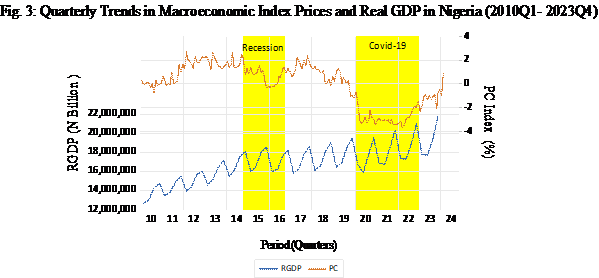

Fig.3 represents the macroeconomic index and real GDP. There is a co-movement between the index and real output. Increase in the saw growth in real output while a fall in the index coincides with a decrease in real GDP. Notably two episodes have between identified, the Nigerian recession and COVID-19 pandemic. Specifically, the pandemic caused a down shift in domestic prices, increase in foreign reserves and low interest rates as demand, due to the partial lockdown in Nigeria and some economies across the world.

To validate the relationship, we use of descriptive statistics and econometric technique will further reveal provide insight on the link between exchange rate fluctuation, oil price movement and real output in Nigeria. We further include the coefficient of variation which normalised series of different unit in the descriptive statistics.

METHODOLOGY

Data and Source

Quarterly time series on real gross domestic product (RGDP), average exchange rate, and bunny light crude oil price for the period 2010:01 to 2023:12. were sourced from the Central Bank of Nigeria (CBN) and used for the analysis. The time chosen for the analysis is to capture post-rebasing which allows for periodic monitoring and reporting of economic performance, as against the aggregated performance.

The average exchange rate expressed as the US dollar against the domestic currency is proxied by the Nigerian Autonomous foreign exchange (NAF). Brent-crude oil price represents commodity price in the model. Specifically, bunny light-crude (OIL) is produced by Nigeria, the major source of foreign exchange earnings for the country. The RGDP represents economic growth. It is the market value of goods and services produced by a country for a year and adjusted for inflation. The macroeconomic index is used to account for unknown variables that are important to the determination of economic activities. The principal component analysis was applied to obtain the index using market interest rate (maximum lending rate), consumer price index, monetary policy rate, import bills and external reserves, allowing us to circumvent biasness associated with single variable.

Model Specification

Following, Tumala, Afees and Atoi (2022), we incorporate oil price into the autoregressive distributed lag (ARDL) framework developed by Pesaran and Shin (1999). The ARDL looks at the short and long run dynamics. The necessary condition for estimating the ARDL is the mixed order of integration or same order of integration, and the frequency must be of same observation. Due to structural issues inherent in the GDP series for Nigeria, the Bai-Perron (1998) tests for multiple structural breaks was employed to uncover the break dates. Thereafter, the nonlinear autoregressive distributed lag (NARDL) approach proposed by Shin et al. (2014) was used to obtain the long run dynamics of exchange rate on economic activities. The advantage of NARDL over other techniques is that it decomposes the impact of the explanatory variable into favourable and unfavourable components.

Following the work of Shin et al. (2014), the asymmetric cointegration long run equation is expressed as:

![]()

Where represents the vector K x 1 as vector of multiple regressors such that ![]() is the autoregressive parameter.

is the autoregressive parameter. ![]() and

and ![]() represents the asymmetric parameters,

represents the asymmetric parameters, ![]() is an iid process with zero mean and constant variance. The inclusion of dummy (D) as structural break necessitates the adoption of a modified framework to account for the role of structural breaks. Consequently, we augment the work of Sharma and Kautish (2019) which carries the dummy variable. Our working model is expressed as:

is an iid process with zero mean and constant variance. The inclusion of dummy (D) as structural break necessitates the adoption of a modified framework to account for the role of structural breaks. Consequently, we augment the work of Sharma and Kautish (2019) which carries the dummy variable. Our working model is expressed as:

Where RGDPt is the dependent variable, α is the constant term, α₁ to αp are the coefficients of the lagged dependent variable on the right-side of the equation, β₁…..βp represents the coefficient of exchange rate, and oil price(OIL), D2 is the dummy representing structural break, γ is the coefficient of the dummy variable; t is time while ε is the error term. The + and – superscript represents the positive and negative disturbance. Determining the lag selection criterion requires estimating the model in standard var, however, the ARDL framework allows for automatic selection of the appropriate lag by varying the lag of the variables. The necessary condition for estimating the NARDL is that cointegration must be established.

Different economic episodes, the 2016 Nigerian economic recession, COVID-19 pandemic and exchange rate regime switch in 2023, necessitate the inclusion of structural break, hence the Bai-Peron (1998) test for multiple structural breaks reveal two break dates, 2014Q4 and 2021Q42. These break dates coincide with the period of economic recession and COVID-19 pandemic, respectively. This validates the inclusion of dummy as a proxy for structural break (see Table 3). The NARDL was estimated with structural break to account for structural changes while restricting the control variables. This allows a single regressor to be decompose into the partial sum processes (Shin et al., 2014). When the F-statistic is above the low I(0) and high 1(1) critical bound, we reject the null hypothesis that there is no cointegration but when the F-statistics lies between the critical bound, we accept the null hypothesis. Where the F-statistic lies between the low and high critical bound, we conclude that the test is inconclusive. Both real GDP and exchange rate enter the model as growth rate, oil price is logged.

Presentation of Result and Analysis

Descriptive Statistics

The first procedure for data analysis is to check the behavioural pattern of time series, hence we use descriptive statistics. The summary statistics shows that between 2010Q1 to 2023Q4, the average mean value of RGDP, NAF and OIL is N168,355.6 billion, U$/N284.76 and US$79.34, respectively. The standard deviation which measures variation of the variables indicates that RGDP has the highest dispersion among the series with a value of N196,1811.0 billion. However, standard deviation is not a suitable measure of stability since the series have different unit of measurement, therefore, the need to incorporate a better measure of volatility called coefficient of variation. The coefficient of variation tends to normalise series of different measurement. The mean is deflated by the standard deviation (std. Dev/mean) to obtain the coefficient.

The result from the coefficient shows that exchange rate (NAF) is more volatile with the value of 0.5 percent when compared to other series.

| Table 1: Descriptive Statistics | |||

| RGDP | NAF | OIL | |

| Mean | 16835555 | 284.7752 | 79.34417 |

| Coeff Var. | 0.116528 | 0.509343 | 0.330452 |

| Std. Dev. | 1961811 | 145.0483 | 26.21944 |

| Skewness | 0.097732 | 1.668519 | 0.021229 |

| Kurtosis | 2.899623 | 6.797246 | 1.795679 |

| Jarque-Bera | 0.112657 | 59.6281 | 3.388449 |

| Probability | 0.945229 | 0 | 0.183742 |

| Observations | 56 | 56 | 56 |

Note: where RGDP, real gross domestic product, NAF the official exchange rate, OIL brent crude oil price, Coff Var. Is the coefficient of variation, Std. Dev is the standard deviation.

Furthermore, the series are positively skewed, indicating right tail long. The result for the Kurtosis suggests that RGDP and OIL are leptokurtic while NAF is mesokurtic since the value is greater than three. The Jarque-Bera statistics show that only the exchange rate has no normal distribution as the coefficient is significant.

Stationarity Test

Preliminary analysis requires that we test for stationarity of time series. Non-stationarity is inherent in time series, particularly for financial time series because of uncertainties. The study employs the Augmented Dicky-Fuller (ADF) and Philip-Perron unit root test to ascertain the properties of our time series for the analysis. Both the ADF and PP test shows that exchange rate (NAF), crude oil price (OIL) and the macroeconomic index (MI) are stationarity at first difference I(1) at the 5% level of significance(see Table 2). The growth rate of RDGP and NAF were used to circumvent the problem of unit root. Consequently, the real GDP growth and NAF growth are stationary at levels I(0). The result indicates mixed order of integration, I(0) and I(1) which suggests the use of autoregressive distributed Lag (ARDL) framework.

| Table 3: Unit Root Test | |||||

| ADF | PP | ||||

| Level | First Difference | Level | First Difference | ||

| RGDPG | -2.7065* | -7.3285*** | -2.7648* | -7.3300*** | |

| NAFG | -1.38241 | -5.3619*** | 3.7627 | -1.6317*** | |

| OIL | -1.9721 | -5.5063*** | -1.7513 | -5.4709*** | |

| MI | -1.0995 | -5.7257*** | -1.3331 | -5.7484*** | |

| Where * Significant at the 10%; ** Significant at the 5%; *** Significant at the 1%, respectively. | |||||

Multiple Breaks Test

The Bai-Perron test for multiple break dates is used to identify multiple structural breaks of time series. The break date is a point where the statistical properties of the time series exhibit significant change. The test is a modified version of the chow test for single break date and the result reveals two break dates, 2014Q4 and 2021Q2 which coincides with crude oil price shock (see Table 4). However, the first dummy variable for 2014 was insignificant while the second dummy (2021) exhibited significant influence, hence the 2021 break date.

| Table 4: Bai-Perron test Multiple breakpoint test | ||||

| Sequential F-statistic determined breaks: | 2 | |||

| Break Test | F-statistic | Scaled F-statistic | Critical Value** | Break dates |

| 0 vs. 1 * | 11.92138 | 23.84275 | 11.47 | 2014Q4, 2021Q2 |

| 1 vs. 2 * | 10.97803 | 21.95606 | 12.95 | |

| 2 vs. 3 | 2.097348 | 4.194697 | 14.03 | |

| * Significant at the 0.05 level. | ||||

| ** Bai-Perron (Econometric Journal, 2003) critical values. | ||||

DISCUSSION OF RESULT

The NARDL bound test is reported in Table 5: The NARDL bond test reveal a cointegrating relationship between real GDP, exchange, and oil price in Nigeria. Given that the F-statistics is 5.1 above the lower critical bound and high critical bond at the 5% significance level. The short run dynamics from the nonlinear ARDL(NARDL) further shows that both oil, exchange rate and structural breaks matters for economic performance in Nigeria.

| Table 5: Bound Test | ||

| F-statistics | 5.108867 | |

| Significance | I(0) | I(1) |

| 10 | 1.90 | 3.01 |

| 5 | 2.26 | 3.48 |

| 1 | 3.07 | 4.44 |

* I(0) and I(1) are the critical bounds level. The estimation is based on first case ARDL (without constant).

Table 6 presents the short and long run estimates of the NARDL. The short run estimates show that the current, first and third lag of oil price exhibit positive influence on real GDP, implying high performance of the economy. However, the second lag of output has a negative but weak impact on economic activities, hence positive oil price outweighs the negative. Consequently, a unit change in current oil price caused a 4.4 percent rise in real GDP. Furthermore, a unit change in the first and third lag of oil price will lead to 3.9 and 2.8. percent increase in economic activity, respectively. Notably, the level of growth is decelerating, amidst exposure to commodity price shock and structural issues which retard economic performance.

| Table 6: NARDL Short and Long run coefficients with real GDP as the dependent variable with structural breaks | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| Short Run | ||||

| ∆LOG(OIL) | 4.405764 | 0.872218 | 5.051218 | 0.0000 |

| ∆LOG(OIL(-1)) | 3.888414 | 0.845902 | 4.596768 | 0.0001 |

| ∆LOG(OIL(-2)) | -0.15012 | 0.955449 | -0.15712 | 0.8761 |

| ∆LOG(OIL(-3)) | 2.836259 | 0.922966 | 3.072982 | 0.0042 |

| ∆(NAFG) + | -0.05124 | 0.027571 | -1.8584 | 0.0721 |

| ∆(NAFG) – | 0.061689 | 0.032666 | 1.888474 | 0.0678 |

| ∆(NAFG(-1)) + | -0.06026 | 0.035784 | -1.68407 | 0.1016 |

| ∆(NAFG(-1)) – | 0.026662 | 0.031286 | 0.852194 | 0.4002 |

| ∆(NAFG(-2)) + | -0.12451 | 0.040121 | -3.1033 | 0.0039 |

| ∆(NAFG(-2)) – | 0.043871 | 0.03132 | 1.400725 | 0.1706 |

| ∆(NAFG(-3)) + | -0.02666 | 0.039804 | -0.66979 | 0.5077 |

| ∆(NAFG(-3)) – | 0.077083 | 0.03171 | 2.430871 | 0.0207 |

| D2 | -4.09221 | 0.770268 | -5.31271 | 0.0000 |

| ECT* | -0.57704 | 0.107028 | -5.39145 | 0.0000 |

| Long run | ||||

| LOG(OIL(-1)) | 1.048033 | 0.202668 | 5.171179 | 0.000 |

| MI | 0.638119 | 0.282432 | 2.259373 | 0.029 |

| NAFG(-1) + | 0.130145 | 0.185599 | 0.701216 | 0.4869 |

| NAFG(-1) – | 0.044849 | 0.195679 | 0.229198 | 0.8198 |

| LM Test (2) | 0.854112 | 0.4368 | ||

| Heteroskedastic Test | 1.136063 | 0.3716 | ||

| R-squared | 0.784716 | |||

Note: where ∆ represents the change, superscript + and – represent the positive and negative values of exchange rate in an NARDL framework.

The result further shows that the current exchange rate has positive implication for real GDP, as depreciation causes negative growth whereas an appreciation of the domestic currency causes a rebound in economic activities. This finding is consistent to Iheanachor and Ozegbe (2021) who utilised lower frequency in ARDL. Furthermore, the first and second lag of exchange rate depreciation caused downward performance of the economy by 0.1 apiece, however, exchange rate appreciation failed to cause a rebound for the two periods. Notably, exchange rate appreciation in the third lag causes a rebound in economic activities as depreciation in the third lag did not impact significantly on real output.

The result also reveals that structural issues have a negative influence on real GDP, suggesting that structural changes will slow output by 4.1 percent more than any of the macroeconomic indicator. This is evident in the sudden change in government. For instance, removal of fuel subsidy led to a historical rise in inflation from 22.4 to 33.2 percent between May 2023 and April 2024 (NBS Report, 2024). Exchange rate unification led to significant depreciation in the exchange rate by 74.7 percent, from US$/N480.00 to from US$/N1900 between June 2023 and February 2024(CBN, 2024). The error correction term (ECT) is negative and significant at 0.58 percent. This suggests that the economy will converge to normalcy by 58 percent over the four quarters, whenever the economy is in disequilibrium.

The long-run dynamics shows that lag information about oil price has positive influence on real output. Therefore, a unit change in oil price will cause 1.0 percent increase in economic activities. In addition, the macroeconomic index also exhibits a positive impact on real GDP by 0.6 percent, amidst increase in foreign reserves, positive trade balance and FDI inflows. The result further indicates that changes in exchange rate depreciation/appreciation would not affect real output, given that the economy would be operating at full employment as structural issues may have been addressed. The implication for the results is that the inherent behaviour of real GDP in Nigeria is partly associated with the structural rigidities and commodity price shock faced by resource rich economy. The contribution of oil sector is a call for economic diversification to navigate the downturn associated with negative oil price shock.

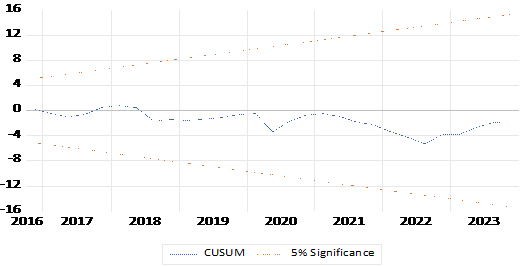

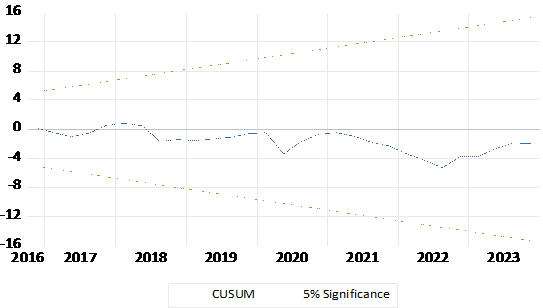

Post-diagnostic

The result of the Breusch-Godfrey Serial Correlation LM Test shows that there is no serial correlation as the F-statistics is statistically insignificant. The Breusch-Pagan-Godfrey Heteroskedasticity test further shows that the series are homoscedastic, implying the absence heteroskedasticity. The test for model stability using the CUSUM test and CUSUM of square shows that the model is stable since the blue line lies within the critical bound (see Figures 4 and 5)

Fig.4: CUSUM Test

Fig. 5: CUSUM of Square Test

Policy Implication

The implication of the result is that a weaker currency would make a country’s exports cheaper and more attractive as foreigners exploit the advantage of cheap products. However, the downside of depreciation is the increase in inflationary pressure due to pass-through inflation arising from the high cost of import in the short run. Where the country relies heavily on imports, the demand for foreign exchange will outweigh the supply, creating macroeconomic instability which makes it difficult for the central bank to manage the economy. The central bank can only raise interest rates to attract foreign capital. It is worthy of note that macroeconomic condition determines capital inflow. Foreign investors can lose confidence in a high uncertainty environment, denying the country capital flow. However, raising domestic rates will hurt the manufacturing sector and other businesses willing to undertake new investment.

The long run dynamics implies that exchange rate does not matter, on the assumption that structural issues may have been addressed as the country remains resilient to external shocks. If depreciation persists, it may serve as incentive for investment to export oriented industries, leading to sustained growth. The index shows that increasing exports and lowering interest rate while taming inflation could spur economic growth.

The result for crude oil price further emphasis on the need to diversify the economy while providing wide range of investment in the energy sector, particularly in the natural gas subsector to mitigate episodes associated with oil price fluctuation, as oil serves as the main source of vulnerability to the economy. This calls for investment in other sectors and an increase in investment in the national sovereign wealth fund for the future buffer against shock. Structural shocks such as conflict, political instability, weak institution, and unanticipated policy announcement are sources of economic distortion, leading to decline in output.

CONCLUSION

The primary objective of the paper is to analyse the impact of exchange rate fluctuation and economic growth. Preliminary analysis from the Bai-Perron test for multiple breaks suggest two break dates (2014Q4 and 2021Q2), while the coefficient of variation indicates unstable growth. The paper employs the nonlinear ARDL approach on quarterly data for the period 2010:1 to 2023:4 while controlling for oil price (OIL) and macroeconomic factors and structural breaks. The findings reveal a nuanced picture. The short run dynamics suggest that current and past exchange rate appreciation have a positive impact on economic growth. This highlights the importance of exchange rate in driving the economy, however, the long run dynamics suggest that exchange rate does not matter when productivity is at full employment.

The result also shows that current and past crude oil prices have significant influence on economic growth both in the short and long run. Oil price shocks present a double-edged sword. Increase in oil high prices presents a positive outlook due to revenue surge, signaling economic prosperity and macroeconomic stability. The result further shows that structural issues (events, policy change, among others) tend to distort the economy and retard growth. In the long run, the exchange rate does not matter because the economy is assumed to be operating at full potential. Consequently, understanding the impact of exchange rate fluctuation, commodity price shocks and structural changes on the economy, policymakers can develop strategies to mitigate negative effects, by leveraging on positive outlook for sustainable development of the economy.

RECOMMENDATION

- The central bank should review sectoral credit policy to encourage lending to the productive sectors of the economy. The central bank should be cautious about interest rates hike as continuous hiking of rates would hurt domestic industries and stifle growth, amidst structural imbalances.

- The government should intensify economic reforms to diversify the economy by investing in the mining and agricultural sector with emphasis on refined and finished products.

- The government should address structural imbalance by building sustainable roads, rails, while policy related issues should be designed and carefully implemented to avoid shocking the economy. Government can streamline regulations by reducing unnecessary bureaucracy and regulations to improve ease of doing business.

- Government spending should target sectors that could reduce import and address macroeconomic instability by issuing tax breaks to new businesses with potential to create jobs and grants to businesses with potential to expand production capacity.

REFERENCES

- Abdel-Kader, K. (2013). What Are Structural Policies? Finance & Development. https://www.imf.org/external/pubs/ft/fandd/2013/03/basics.htm

- Ahmad, F., Draz, M. U., & Yang, S. C. (2019). China’s economic development: does exchange rate and FDI nexus matter?. Asian‐Pacific Economic Literature, 33(2), 81-93 https://doi.org/10.1111/apel.12268.

- Ahmad, Fayyaz and Draz, Muhammad Umar and Yang, Su-chang, The Nexus between Exchange Rate, Exports and Economic Growth: Further Evidence from Asia (March 30, 2016). Available at SSRN: https://ssrn.com/abstract=2758505or http://dx.doi.org/10.2139/ssrn.2758505.

- Aloui, C., Hkiri, B., Hammoudeh, S., & Shahbaz, M. (2018). A Multiple and Partial Wavelet Analysis of the Oil Price, Inflation, Exchange Rate, and Economic Growth Nexus in Saudi Arabia. Emerging Markets Finance and Trade, 54(4), 935–956. https://doi.org/10.1080/1540496X.2017.1423469

- Bai, J., & Perron, P. (1998). Estimating and testing linear models with multiple structural changes. Econometrica, 47-78. https://www.jstor.org/stable/2998540

- (2024). Statistical database. Central Bank of Nigeria.

- Cerami, A., & Cerami, A. (2013). Systemic Problems and Structural Challenges. Permanent Emergency Welfare Regimes in Sub-Saharan Africa: The Exclusive Origins of Dictatorship and Democracy, 66-82. https://doi.org/10.1057/9781137318213_4

- (2016). What is the role of exchange rates? European Central Bank. https://www.ecb.europa.eu/ecb-and-you/explainers/tell-me-more/html/role_of_exchange_rates.en.html

- Enilolobo, O. S., Ajibola, A. A., & Theodore, N. I. (2017). Impact of oil revenue and exchange rate fluctuation on economic growth in Nigeria (1981-2015). Journal of Management & Administration, 2017(2), 77-104. https://hdl.handle.net/10520/EJC-f2de41b8d

- Ewubare, D. B., & Ushie, U. A. (2022). Exchange rate fluctuations and economic growth in Nigeria (1981-2020). International Journal of Development and Economic Sustainability, 10(1), 41-55. https://www.eajournals.org/

- Fan, L. S., & Fan, C. M. (2002). The Mundell-Fleming model revisited. The American Economist, 46(1), 42-49. https://www.jstor.org/stable/25604242

- Henry, E., Murtadho, A. M., & Bhaumik, A. (2020). The Relationship Between the Exchange Rate Fluctuations and Economic Growth in Nigeria. International Journal of Management and Human Science (IJMHS), 4(4), 11-18. https://ejournal.lucp.net/index.php/ijmhs/article/view/1235

- Hoang, T., Thi, V., & Minh, H. (2020). The impact of exchange rate on inflation and economic growth in Vietnam. Management Science Letters, 10(5), 1051-1060. http://www.m.growingscience.com/msl/Vol10/msl_2019_321.pdf

- Iheanachor, N., & Ozegbe, A. E. (2021). The consequences of exchange rate fluctuations on Nigeria’s economic performance: An autoregressive distributed lag (ARDL) approach. International Journal of Management, Economics and Social Sciences (IJMESS), 10(2-3), 68-87. https://doi.org/10.32327/IJMESS/10.2-3.2021.5%0A

- Kappel, R. (2003). Economic aspects of the African crisis low-level equilibria, traps and structural instability. In: Structural Stability in an African Context. Discussion Paper 24. https://www.files.ethz.ch/isn/96051/24%20-%20cannot%20split.pdf

- Kingsley, E. E., Chioma, A. E., & Martha, M. (2021). Effect of Foreign Exchange Fluctuations on the Economic Growth of Nigeria. Jalingo Journal of Social and Management Sciences, 3(4), 33-44. http://oer.tsuniversity.edu.ng/index.php/jjsms/article/view/80

- (2024). CPI and Inflation Report March 2024. National Bureau of Statistics https://nigerianstat.gov.ng/elibrary/read/1241484

- Nwikina, C. G., & Ekere, E. U. (2024). Impact of Exchange Rate on Economic Growth: Evidence from Nigeria. Global Journal of Arts, Humanities and Social Sciences, 12(3), 36-50. https://www.eajournals.org/

- OECD (2024), Purchasing power parities (PPP) (indicator). doi: 10.1787/1290ee5a-en (Accessed on 13 May 2024). https://data.oecd.org/conversion/purchasing-power-parities-ppp.htm

- Pesaran, M. H., & Shin, Y. (1995). An autoregressive distributed lag modelling approach to cointegration analysis (Vol. 9514). Cambridge, UK: Department of Applied Economics, University of Cambridge.

- Sharma, R., & Kautish, P. (2019). Dynamism between selected macroeconomic determinants and electricity consumption in India: An NARDL approach. International Journal of Social Economics, 46(6), 805-821. https://doi.org/10.1108/IJSE-11-2018-0586

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. Festschrift in honor of Peter Schmidt: Econometric methods and applications, 281-314. https://doi.org/10.1007/978-1-4899-8008-3_9

- Tumala, M. M., Salisu, A. A., & Atoi, N. V. (2022). Oil-growth nexus in Nigeria: An ADL-MIDAS approach. Resources Policy, 77, 102754. https://doi.org/10.1016/j.resourpol.2022.102754

- Voice of America (2024). Nigeria’s cryptocurrency crackdown will have consequences, experts say. https://www.voanews.com/a/nigeria-s-cryptocurrency-crackdown-will-have-consequences-experts-say/7523302.html

- Wang, P. (2009). The Mundell-Fleming Model. In: The economics of foreign exchange and global finance. Springer, Berlin, Heidelberg. https://doi.org/1007/978-3-642-00100-0_7

- Weeks, J. (2008). A note on Mundell-Fleming and developing countries. Department Of Economics Working Papers, No.155, School of Oriental and African Studies, University of London. https://www.soas.ac.uk/sites/default/files/2022-10/economics-wp155.pdf

- Zoramawa, L. B., Ezekiel, M. P., & Kiru, A. T. (2020). Exchange rate and economic growth nexus: An impact analysis of the Nigerian economy. Journal of Research in Emerging Markets, 2(4), 58-67. https://api.semanticscholar.org/CorpusID:224829362