Assessing the Effects of CEO Characteristics on the Financial Performance of Firms in Nigeria

- Ilemobayo Akindayomi

- Ologunwa, O.P. (PhD.)

- Adigun, A.O. (PhD.)

- 559-571

- Mar 4, 2024

- Accounting & Finance

Assessing the Effects of CEO Characteristics on the Financial Performance of Firms in Nigeria

Ilemobayo Akindayomi1,Ologunwa, O.P. (PhD.)2 and Adigun, A.O. (PhD.)3

1,2,3Department of Project Management Technology, School of Logistic and Innovation Technology,

Federal University of Technology, Akure, Nigeria.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.802037

Received: 16 November 2023; Revised: 30 November 2023; Accepted: 05 December 2023; Published: 02 March 2024

ABSTRACT

This study investigated the relationship between CEO characteristics and the financial performance of listed firms in Nigeria (2005 –2022). The regression analyses employed in this study are pooled panel regression, random panel regression and fixed panel regression. Under the firm performance indicator – ROA, the Hausman-statistics p-value of 0.23 indicated that we accept the null hypothesis which says that random effect prevails. But the fixed effect result was adopted because it best explains the model as it considers the constant variables and solves the omitted variable bias problem. The result showed that CEO origin has a positive and significant impact on return on assets (2%). Whereas, CEO gender showed a negative and insignificant effect on return on assets (30%). CEO tenure impacts a negative and insignificant relationship with return on assets (62%). Furthermore, this result showed a positive and insignificant relationship between leverage and return on assets. While capital expenditure shows a negative and insignificant relationship with return on assets. The study recommends that, Firms should adopt internal recruitment in appointing CEO, as they tend to possess insider-knowledge and experience peculiar to the firm’s nature of work and relationship with the staff that an outsourced CEO may not have opportunity to immediately after his appoint and could be a major set-back in fulfilling the goal of the firm.

Keywords; CEO characteristics, financial performances, return on assets, return on equity

INTRODUCTION

Studies have identified ownership as one of the good sources of power both in theory and in practice (Marwan, et al.2020). The major determinant of agent-principal relationship in agency theory is the ownership of the company. Unlike the case of agency relationship, the Chief Executive Officer (CEO) who acquires a good proportion of company shareholding will be an agent-cum-principal officer which gives a good ground to influence almost every activity in the organization (Mio et al. 2016). When the CEO has significant stock ownership, he can influence the selection of other directors, hence giving him an edge over board members.

Having significant ownership will enable the CEO to influence the determination of the board member’s remuneration, scuff ling their dismissal if need be, and dominate in most of the board decisions (Zhang et al.2016). The mind-boggling question as to whether ownership in companies could result in firm performance and value across all settings still remains not satisfactory. The board structure and the position of the chief executive officer (CEO) within the firm as a topic are continuously growing. It is one of the most discussed topics in corporate finance. The board of directors is appointed by the shareholders of the firm and who act on behalf of the shareholders to run the day to day activities of the business.

Each year, the company holds annual general meeting (AGM) where the board of directors provide a report on the performance of the company and what its future plans and strategies are (Jelle Diks, 2016). The board is accountable for all the actions taken by the firm, and in nearly all companies, the CEO holds a seat on the board of directors. Most often than not, the CEO is actually the chairman of the board and has a significant impact on the firm through the position just as the board of directors has its own on the decisions and policies of the firm. The job description of a CEO is deeper than what most people expect. Its description includes everything that cannot be delegated to co-workers. The most important task is to set a strategy for the firm. Besides, the CEO has to model and set the company’s culture, build and lead the senior executive team, and allocate capital to the company’s priorities. Linck, Netter, and Yang (2008) suggest that the CEO position and the Chairman of the Board (COB) position are combined in large firms when the CEO is older and has a longer tenure. This means that the CEO has significant impact throughout his own position and the board of directors on the decisions and policies of the firm.

In every organisation, the performance of the firm is the measure of how well the organisation can use its resources to generate a desired level of returns and objectives of the firm. There are several measures used in determining the financial performance of firms, but Return on Asset (ROA) and Return on Equity (ROE) are usually considered as the performance measurement in business research (Binacci, et al, 2016; Murphy, Trailer, & Hill, 1996). This study resolves to unravel the agency issue in CEO ownership with its implication in firm performance in Nigeria’s highly regulated sector as to ascertain the effect of CEO characteristics on firm’s performance and to further investigate which of these characteristics has a positive impact on firm’s performance and what characteristics has a negative impact.

STATEMENT OF THE PROBLEM

In spite of the general agreement that CEO characteristics influence firm performance, in some specific ways, theorist and scholars have divided opinions and have been able to provide little evidence to substantiate that fact that managerial characteristics, educational background or CEO attributes have significant effect on firm performance (Fligstein, 1990). Some researchers revealed that some of these CEO characteristics does not have effect on the financial performance of firm, while some said it affects, for example, Saidu (2019) established that, CEO level of education often improve profitability and that CEO with previous experience often make the stock market performance better. Also, when Companies promote Senior Executive to CEO, it is always a healthy development for the firm.

Also the financial crises that took place when CEOs of global companies such as Enron and WorldCom engaged in some corporate scandals led to the collapse of some firms which was attributed by stakeholders to lack of transparency, lack of accountability and elongated CEO tenure (Marwan, et al. 2020). This has triggered a lot of researchers to examine the relationship between the characteristics of CEOs and its performance on firms (Uyagu, 2017). Also Suherman, et.al. (2023) argued that individual characteristics should be considered when appointing CEOs, because their characteristics enhances firm performance. while the older CEOs long year of experience often ad a competitive advantage, the female CEOs bring new perspective and the educated CEOs have better ability to deals with challenging intellectual activities and foreign CEOs understand international market regulation better.

The age of CEO has no obvious influence on firm performance, their tenure also has a high significant negative impact on high valuation firms. In addition, while CEO political affiliation are positively related to low valuation firms, the exact opposite effect is evidenced in relation to high-performance firms, Liu & Jiang (2020). Many of the recent studies ascribed agency situation to CEOs, and most of the studies employed variables that have to do with managerial discretion such as; (Gupta et al. 2016; Veprauskaite & Adams 2013). Findings from most of the studies reported the negative impact of CEO power. Although, the motive to study the CEO managerial discretions is not connected to the recent happening in the governance structure whereby some CEOs of global companies such as Enron and WorldCom engaged in some corporate scandals. However, this study takes a different approach by looking into those qualities that denote CEO Characteristics.

Also, an important source of CEO wisdom is when the CEO is experienced in terms of origin, gender and tenure. Experience is power, and it is presumed that when better experiences are merged with firms’ management, there is a high tendency of acquiring a greater managerial skill and thereby delivering the organization even during the hardest time. CEO’s characteristics might affect the firm performance positively or negatively. However, it is not possible to generally state that there is a relationship between a CEO’s characteristics and the firm performance. Different characteristics, firm performance indicators and other factors, such as the country where the firm operates in, have to be taken into account in order to be able to examine whether there is a relationship (Meltschakow, 2020). Therefore, this research work seeks to contribute to the literature by examining and concentrating on the following quantitative CEO characteristics experience in term origin, gender, and tenure. And there fore examine their respective relationship with the financial performance of firm.

Having significant ownership will enable the CEO to influence the determination of the board member’s remuneration, scuff ling their dismissal if need be, and dominate in most of the board decisions. The question as to whether ownership in companies could result in firm performance and value across all settings still remained not fully answered. Hence, the need for this study to examine the effect of CEO Characteristics on the financial performance of listed firms in Nigeria. This study is important for all firms across all the sectors as it will help the shareholders of these firms to make a proper decision on CEO and to know what characteristics to watch out for in appointing a CEO so as not to only help enhance the performance of the firm but to also enhance its goodwill, accountability, integrity, competence and also attract investors and customers (both local and foreign). The study spans between the periods 2005-2019, which will cut across the listed firms in different sectors of the economy.

CONCEPTUAL FRAMEWORK

CEO is recognized as one of the good sources of power both in theory and in practice. The major determinant of agent-principal relationship in the agency theory is the ownership of the company. Zhang et al. (2016) established that CEO ownership in company has connection with some important board decisions such as selections, determination of the members’ remunerations and many other decisions. Chief Executive Officers (CEOs) is perceived as someone who has the ability to revive a dying firm back to life and infuse energy into the firm to enable it bounce back to its feet. Hambrick and Mason (1984) contended that the strategic vision and the organizational direction followed by the CEO is subject to his/her understanding of the changing business world.

Hambrick (2007) later added that CEOs’ actions are built on their personal understandings of the strategic circumstances they are faced with, and this intention depends on the CEO’s educational background and beliefs. Some schools of thought assert that CEOs are also involved in strategic decision making process and choices that impact directly on the performance of the firm. CEOs actions reshape organizational structures and make them adaptive to the environmental and economic challenges. The proponents of this school of thought argue that in a competitive economy, the quality and performance of the managers determine the success and sustainability of the business. Some are of the opinion that the financial crisis that took place in the last decade and the 2016 stock market turmoil in the U.S and Europe led to changes in the ways firms perform business, changes in ownership structures and consumers’ needs have also significantly changed.

THEORETICAL REVIEW

Agency Theory

Agency theory was originated from the work of Berle and Means (1932) thesis entitled “The modern corporation and private property”. The thesis describes the fundamental agency problems inherent in modern firms where separation of ownership and control exist. The modern firms are those firms that go public as a means of effectively sourcing for funds to expand the business operation. As a result, modern firms have multiple owners or shareholders, called principals and executives called agents. According to this theory, the principals of the firm hire the agents to run the business on their behalf and act in the best interest of the shareholders (principals).

The advocates of agency theory emphasized on the ownership, which is the key divide of the relationships between the shareholders and the managers such that each party is trying to maximize benefits of the relationships. The theory projects that powerful CEOs can use their power in achieving their own end which in many cases is not in line with those of the shareholders (Tien & Chuang 2014). Some studies show that greater degree of decision-making discretion of CEO widens the information asymmetry and the chances for the CEO to make decision that may not benefit the shareholders (Brown & Sarma 2007; Veprauskaite & Adams 2013). This entails that any attempt to increase the CEO power may affect the performance adversely.

Agency theory in corporate finance is gaining momentum for all the right reasons. With markets getting volatile as ever, it becomes imperative that both, the interests of the shareholders and the company are taken care of. The shareholders should trust the management of the company and go an extra mile to understand their day-to-day business decisions. Similarly, the management should also keep the interests of the true owners of the company in their mind. A clear communication should be sent out explaining the rationale behind major business decisions to help shareholders understand and appreciate changes if any. A robust corporate policy can help to keep differences at bay (Sanjay, 2019).

According to Agency Theory, managers (CEOs) possess more information about the businesses because of having operational control over the firm as compared to owners. Consequently, these managers may act opportunistically and seek private rents at the expense of shareholders (owners) wealth. The resultant loss to shareholder’s wealth is called agency cost. On the basis of these assumptions, the theory advises to give less control in the hand of managers who are insiders to the firm. The agency theory literature suggests three mitigation mechanisms to control this agency cost: Monitoring of managers’ actions by board members. Market for corporate control where external market oversees a firm’s performance and allows aggressive takeovers of poorly performed firms and Concentrated ownership incentivizes majority owner to oversee the actions of managers (CEOs).

EMPIRICAL REVIEW

Rupinder and, Balwinder (2018) studied the association between chief executive officer (CEO) characteristics and firm performance. Employing a sample of 500 firms, the support found recommends that demographic and job-related characteristics may be related with the firm’s financial performance. They consider Specifically, the findings indicate a positive relationship between CEO remuneration and firm performance, thus suggesting that compensation acts as a good inducement for executives to yield finer firm performance while CEO nationality appears to inhibit it, steering foreign directors to a minority spot.

Saidu (2019) look at the effects of CEO ownership, education and origin on firm performance, adopting balanced panel data for six years between 2011 & 2016. Finding revealed that CEO Education, improve profitability, also, stock market performance improve hen the CEO ha prior knowledge/ experience before his appointment. Waqas and Ma (2020) in their study of the relationship between CEO characteristics and firm’s performance in Pakistan. had been debated over decades now and yet there is no conclusive evidence about what characteristics leave more impact The results of this research will bring up new evidence supporting the theories brought in to light years ago.

Liu & Jiang (2020) examined the influence of CEO Characteristics on firm performance between 2008 & 2016 in China. The study adopted Quantile regression approach and finding showed that CEO age has no obvious impact on firm’ performance, a clear cut deviation from previous finding. Also, Philip and Wanggao (2022) on the effect of individual chief executive officers’ (CEOs’) characteristics and corporate performance. CEOs across 50 Chinese firms were selected and it was discovered that CEOs’ specific factors play a significant role in their firms’ performance. CEOs’ demographic characteristics include their legal background, dual position (that is, as both CEO and chairman of the same firm), shareholding ratio, gender, and tenure. The findings showed that CEOs with a legal background have a positive influence on return on assets. Robustness tests support the validity of the main results.

Suherman, et.al. (2023) investigated how CEO Characteristics like education, age, gender & nationality influence firms’ performance in Indonesia, adopting balanced firm-level panel data for 203 nonfinancial companies listed on the Indonesia Stock exchange market between 2010-2020 and the use of panel data regression analysis. Finding hoed that female CEO education & nationality often boot firm performance but CEOs age does not have any effect. Some scholars argued that female CEOs are better managers of resources because they are more prudent in spending than their male counterpart (Benmelech & Frydman 2013; Bertrand & Schoar, 2003). Khan and Vieito (2013) employed panel data of U.S. firms from 1992 -2004 to ascertain the relationship between CEO gender and firm’s performance. Their empirical results revealed that a firm’s risk level is smaller when the CEO is a female, resulting in a performance increase as measured by return on assets. In the same vein, Carter, D’Souza, Simkins, and Simpson (2010) argued that competent women and ethnic minorities should have the opportunity to participate in the board of directors and upper management as they are said to possess external networks, information, and other characteristics that can be useful for firms. The problem that arises is that firms do not want to recruit females just because they are female. They have to be sure that it will be beneficial for the company and performance.

MODEL SPECIFICATION

The basic framework for panel data regression takes the form:

Yit=βXit‘+ αZi‘+εit……………………………………………………………(1)

In the equation above, the heterogeneity or individual effect is αZi‘ represents a constant term and a set of observable and un observable variables (Individual effect). Meanwhile, it is important to know that when the individual effect Zi‘ contains only a constant term, OLS estimation provides a consistent and efficient estimates of the underlying parameters (Kyereboah-Coleman, 2007); but if Zi” is un-observable and correlated with Xit‘, then emerges the need to use other estimation method because OLS will give rise to biased and inconsistent estimates.

Therefore, Capital Expenditure (CAPE) and Leverage (LEVG) were used as the control variables as they are being considered as factors that affects the financial performance of firm.

The model is generally specified as;

FPit= β0 +β1(CEOO)it+β2(CEOG)it+β3(CEOT)it+εit ……………..(2)

However, the subscript i represents the entity of each quoted firm at time (t), while subscript t represents the year, t = 2005… 2019.The explicit models for Pooled, Fixed and Random effects models are presented below;

RESULTS AND DISCUSSION

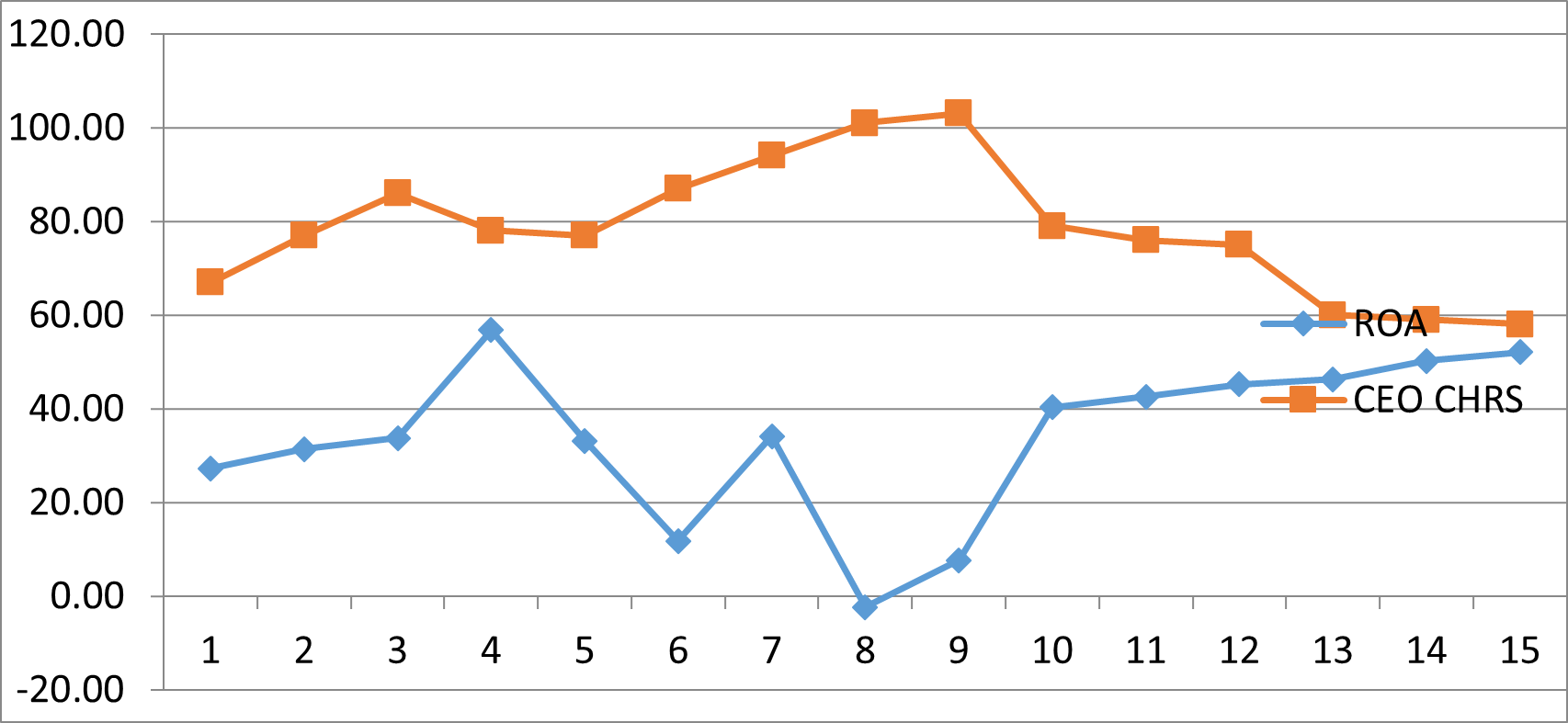

Trend Analysis of CEO Tenure on ROA

Figure 1: Trend result of CEO Tenure on Firm Performance Indicator ROA

Source: Author’s Computation (2023).

Figure 1 showed the trend of the average tenure spent in office as CEO yearly for the selected firms, and the trend of the total ROA of all the selected firms within 2005 to 2019. It showed that the average financial performance of firms fluctuated over the years. Particularly, ROA hit the highest point of almost 60% in the year 2008 before falling drastically in the next two years to around 10%. It never got to that highest point again but fell further to a negative figure in 2012 after a slight uptrend in 2013. Comparing this trend of ROA with the average tenure of CEO within this period, we can infer that there was countertrend movement between the two, using the linear trend lines (dotted lines) to know the uptrend or downtrend, between 2014 and 2019 CEO tenure was in a downtrend while the ROA was in a strong uptrend. This showed that an increase in the tenure of a CEO in office, the less the financial performance of firm indicator – ROA.

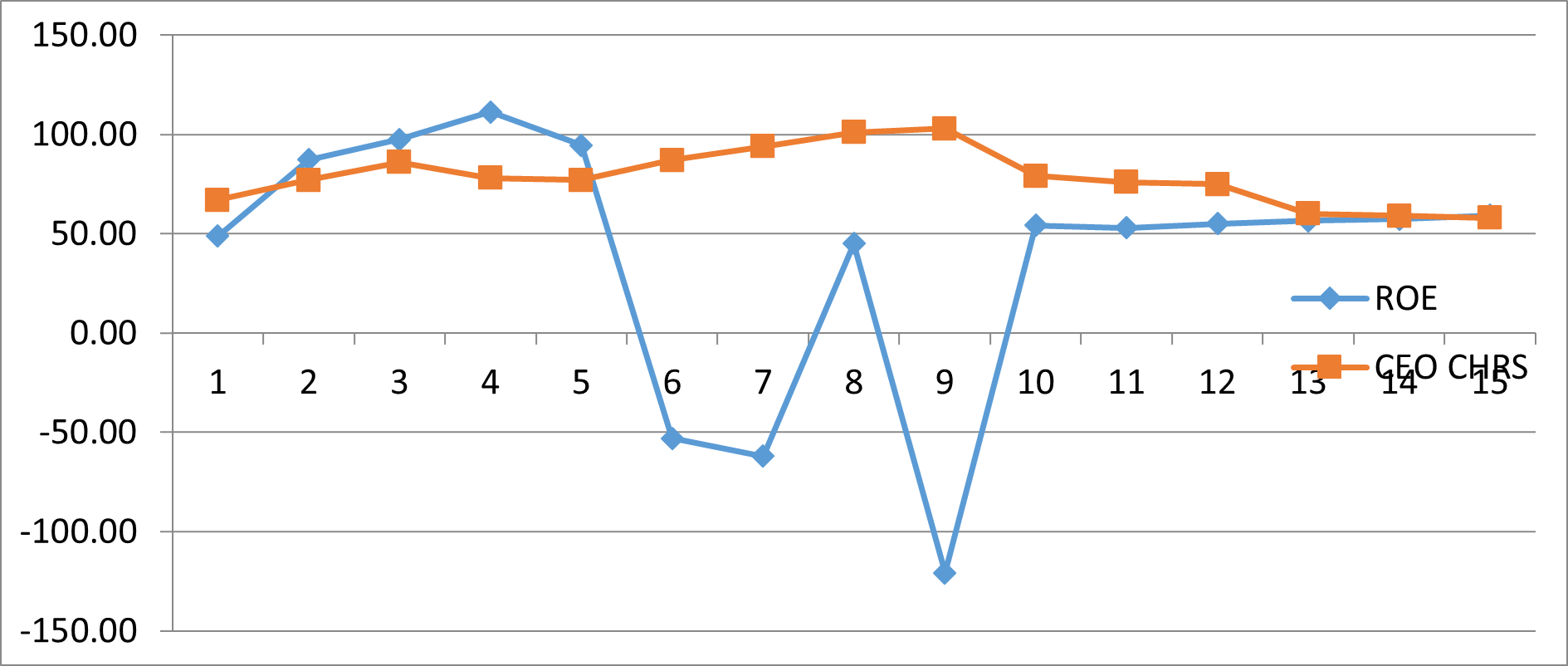

Trend Analysis of CEO Tenure on ROE

Figure 2: Trend result of CEO Tenure on Firm Performance Indicator ROE

Source: Author’s Computation (2023).

Figure 2 showed the trend of the average tenure spent in office as CEO yearly for the selected firms, and the trend of the total ROE of all the selected firms within 2005 to 2019. The results showed that the average financial performance of firms fluctuated over the years. Particularly, ROE fell dramatically from the highest point of 110% in the year 2009 to a negative figure of about -60% in 2011, there was a boost in 2016 as the total ROE of firms rose back to a positive digit of 50% in 2012 and then fell to the least point it ever had in the decade -120% in 2013.

Comparing this trend of ROE with the average tenure of CEO within this period, we can infer that there wasn’t a clear cut relationship between the two as they move simultaneously in the same direction and sometimes move countertrend. Using the linear trend lines (dotted lines) to know the uptrend or downtrend, in 2014, as well as 2018 CEO tenure was in a downtrend while the ROE was in a strong uptrend. This is an indication that an increase in CEO Tenure has a decrease effect on the performance of Returns on equity.

DESCRIPTIVE STATISTICS RESULT

Table 1 Descriptive Results for CEO Characteristics and the financial performance of firms

| Minimum | Maximum | Mean | Std. Dev. | Skewness | Kurtosis | |

| Firm Performance Indicators | ||||||

| ROA | -19.17 | 27.68 | 1.88 | 9.181 | 0.81 | 3.89 |

| ROE | -149.69 | 64.79 | 2.23 | 32.99 | -2.072 | 10.87 |

| CEO Characteristics | ||||||

| CEOO | 0.00 | 1.00 | 0.72 | 0.45 | -0.99 | 1.99 |

| CEOG | 0.00 | 1.00 | 0.98 | 0.148 | -6.48 | 43.02 |

| CEOT | 0.00 | 26.00 | 8.41 | 6.73 | 0.75 | 2.71 |

| Control Variables | ||||||

| LEVG | 0.00 | 84.97 | 29.29 | 17.25 | 0.44 | 2.99 |

| CAPE | 0.00 | 90555.00 | 8192.62 | 14483.54 | 3.12 | 14.62 |

Source: Author’s Computation (2023).

From table 1, the firm performance indicators are the return on assets (ROA) and return on equity (ROE), CEO characteristics are CEO origin (CEOO), CEO gender (CEOG) and CEO tenure (CEOT). While the control variables are leverage (LEVG) and capital expenditure (CAPE). Between the year 2005 and 2019, the highest value for ROA was 27.69% with the lowest value of -19.17%, but on the average the ROA of these firms is 1.88%. The ROE has its highest value within this period to be 64.79% and has the lowest of -149.69% with an average of 2.23% amongst the selected firms showing that they have a high level of performance when their net asset is compared to their shareholder’s equity than when compared with their total assets.

The CEO origin assumed a dummy variable of “1” if CEO was appointed from the company and “0” if outsourced, it’s mean value showed that about 72.22% of the firm’s CEO were appointed from the company while the rest were outsourced. In the same vein, CEO gender assumed a dummy variable of “1” if CEO is a male and “0” if female, the mean value of 97.77% shows that the CEO position of these firms is fully dominated by male gender. The CEO tenure has a minimum value of 0 showing that the least duration spent by a CEO in office is less than a year while the highest service in this position by any CEO of these firms is 26years with an average tenure of about 8years and 4months in that position. Taking into consideration the control variables, the leverage rages from 0.00 to 84.97. It showed that the debt ratio increased from 17.2% to 29.29%, while the capital expenditure has 0.00, 90,555,000 and 8,192,626 as the least, highest and average amount spent on capital expenditure by these firms respectively.

Correlation Analysis

Correlation Analysis for CEO Characteristics and Return on Assets

Table 2 Correlation Result of CEO Characteristics and Return on Asset (ROA)

| ROA | CEOO | CEOG | CEOT | LEVG | CAPE | |

| ROA | 1 | |||||

| CEOO | 0.09 | 1 | ||||

| CEOG | 0.17 | 0.24 | 1 | |||

| CEOT | -0.25 | 0.23 | 0.16 | 1 | ||

| LEVG | -0.16 | -0.04 | -0.12 | -0.07 | 1 | |

| CAPE | 0.06 | 0.093 | 0.09 | -0.22 | -0.05 | 1 |

Source: Author’s Computation (2023).

Table 2 showed the correlation between CEO characteristics (CEOO, CEOG & CEOT), control variables (LEVG & CAPE) and return on assets (ROA). According to table 2, CEO origin and CEO gender have a positive but weak correlation with return on assets while capital expenditure also having a positive but a strong correlation. On the contrary, CEO tenure and leverage have a negative correlation with return on assets. The tenure of a CEO having negative relationship implies that the longer the CEO stays in the position, the lower is the performance of the firm. Also, low correlation amongst the explanatory variables indicate no dependency amongst them, thus indicating low likelihood of multi-collinearity in the result.

Correlation Analysis for CEO Characteristics and Return on Equity (ROE)

Table 3 Correlation Result of CEO Characteristics and ROE

| ROE | CEOO | CEOG | CEOT | LEVG | CAPE | |

| ROE | 1 | |||||

| CEOO | 0.22 | 1 | ||||

| CEOG | 0.09 | 0.24 | 1 | |||

| CEOT | -0.03 | 0.23 | 0.16 | 1 | ||

| LEVG | -0.28 | -0.04 | -0.12 | -0.07 | 1 | |

| CAPE | 0.28 | 0.093 | 0.09 | -0.22 | -0.05 | 1 |

Source: Author’s Computation (2023).

Table 3 showed the correlation between CEO characteristics (CEOO, CEOG & CEOT), control variables (LEVG & CAPE) and return on equity (ROE). According to table 3, CEO origin, CEO gender and capital expenditure have a positive but weak correlation with return on equity. On the contrary, CEO tenure and leverage have a negative correlation with return on equity. This implies that, the appointment of CEO within the firm or outsourced has a strong relationship on the performance of the firm, same as the gender, as they positively affect return on equity. But the tenure of a CEO having negative relationship tells that the longer the CEO stays in the position, the lower is the performance of the firm.

Regression Analysis

Regression Analysis for CEO Characteristics and ROA

Table 4 CEO Characteristics and ROA

| Variable | Pooled OLS | Random Effect | Fixed Effect | |||||||

| Coeff. | t-stat. | prob. | Coeff. | t-stat. | prob. | Coeff. | t-stat. | prob. | ||

| C | -4.91 | -0.87 | 0.39 | 0.79 | 0.16 | 0.87 | 1.69 | 0.39 | 0.70 | |

| CEOO | 1.22 | 0.66 | 0.51 | 6.77 | 2.24 | 0.03** | 8.47 | 2.40 | 0.02** | |

| CEOG | 7.77 | 1.39 | 0.17 | -3.25 | -0.65 | 0.52 | -5.64 | -1.05 | 0.30 | |

| CEOT | -0.26 | -2.04 | 0.04** | -0.11 | -0.84 | 0.40 | -0.06 | -0.49 | 0.62 | |

| LEVG | -0.07 | -1.55 | 0.13 | 6.45 | 0.94 | 0.35 | 2.50 | 0.33 | 0.74 | |

| CAPE | 0.00 | 5.49 | 0.00** | -0.01 | -0.22 | 0.83 | -0.00 | -0.06 | 0.95 | |

| R-squared | 0.37 | 0.07 | 0.75 | |||||||

| Adjusted R-squared | 0.34 | 0.01 | 0.71 | |||||||

| Prob(F-stat.) | 0.00** | 0.28 | 0.00** | |||||||

| Durbin-Watson | 1.278836 | 2.428536 | 2.757549 | |||||||

| Hausman Statistics | 0.2323 | |||||||||

Source: Author’s Computation (2023). (**Significant at 5% level)

For the regression models, pooled (OLS), random effect (RE) and fixed effect (FE) models were considered. The choice between FE and RE was determined by the Hausman-statistics test. The Hausman-statistics probability value of 0.23 as shown in table 4 indicated that we accept the null hypothesis that the preferred model is random effect because the p-value of the test is greater than 0.05 significant levels. But the Fixed Effect model was adopted to analyse this result because it helps account for variables that are constant across individuals (example include CEO origin and CEO gender) which doesn’t change or change at a constant rate over time.

Also the model (FE) removes omitted variable bias by measuring changes within groups across time, usually by including dummy variables for the missing or unknown characteristics. Therefore, the model’s (FE) probability value of 0.00 (P<0.05) rejects the null hypothesis of this research work that the explanatory variables are jointly statistically significant in explaining the variations in ROA, and on this ground, the study rejects the null hypothesis and conclude that the explanatory variables are jointly having an effect on the ROA of the listed firms.

Specifically, the result showed that CEO origin has a positive and significant effect on return on assets (ROA). According to the result, the implication of this is that when a CEO is appointed from within the company, it will improve the financial performance of firms in terms of return on assets (ROA) by 8.47%. This result is consistent with the conclusion made by Datta and Guthrie (1994); Khan and Vieito (2013) that Firms should search internally for a successor before going to external executives. In support of the conclusion Marwan, et al. (2020) used panel data of U.S. firms from 1992 -2004 to ascertain the relationship between CEO gender and firm’s performance. Their empirical results revealed that a firm’s risk level is smaller when the CEO is a female, resulting in a performance increase as measured by return on assets, this result showed that male CEOs has a negative and insignificant effect on the return on assets of firms (ROA).

Furthermore, the tenure of a CEO on the return on asset of a firm is not significant showing that the longer the tenure of a CEO will cause a 0.06% fall in their ROA. This supports the work of Kyereboah (2007) who performs a study in Ghana to ascertain the relationship between CEO tenure and firm performance. His result showed that there is a negative relationship between CEO tenure and firm performance. Table 5 also showed the relationship between the debt ratio (i.e., leverage) and return on assets. The result showed a positive and insignificant relationship between leverage and return on assets. This indicated that the higher the debt ratio of the firms, the higher their return on assets, which means that a unit increase in leverage of firms, will increase ROA by 2.50%. The capital expenditure has a negative and insignificant effect on the ROA, which means a unit increase in the capital expenditure incurred by the firm, will result to a 0.00% fall in her ROA. The regression result showed that the R-squared value of 0.71, this is an indication that the CEO characteristics successfully explains 71% of the changes in the firm’s return on assets.

Regression Analysis for CEO Characteristics and ROE

Table 5 CEO Characteristics and ROE

| Variable | Pooled OLS | Random Effect | Fixed Effect | |||||||

| Coeff. | t-stat. | prob. | Coeff. | t-stat. | prob. | Coeff. | t-stat. | prob. | ||

| C | 2.15 | 0.09 | 0.93 | 2.60 | 0.11 | 0.91 | 2.51 | 0.11 | 0.91 | |

| CEOO | 14.12 | 1.84 | 0.07 | 15.09 | 1.09 | 0.28 | 13.52 | 2.75 | 0.04** | |

| CEOG | 1.48 | 0.06 | 0.95 | -6.27 | -0.26 | 0.80 | -5.74 | -0.21 | 0.84 | |

| CEOT | -0.19 | -0.37 | 0.71 | -0.30 | -0.48 | 0.63 | -0.31 | -0.46 | 0.65 | |

| LEVG | 0.00 | 2.36 | 0.02** | 0.00 | 0.67 | 0.50 | 8.25 | 2.21 | 0.03 | |

| CAPE | -0.49 | -2.59 | 0.01** | -0.15 | -0.74 | 0.46 | -0.09 | -0.41 | 0.68 | |

| R-squared | 0.18 | 0.03 | 0.49 | |||||||

| Adjusted R-squared | 0.13 | -0.03 | 0.40 | |||||||

| Prob(F-stat.) | 0.00** | 0.78 | 0.00** | |||||||

| Durbin-Watson | 1.031251 | 0.919822 | 1.574935 | |||||||

| Hausman Statistics | 0.8420 | |||||||||

Source: Author’s Computation (2021). **Significant at 5% level.

The Hausman-statistics probability value of 0.84 as shown in table 5 indicated that we accept the null hypothesis that the preferred model is random effect because the p-value of the test is greater than 0.05 significant level. Therefore, the model’s (FE) probability value of 0.00 (P<0.05) rejects the null hypothesis of this research work that the explanatory variables are jointly statistically significant in explaining the variations in ROE, and on this ground, the study rejects the null hypothesis and conclude that the explanatory variables are jointly having an effect on the ROE of the selected companies. Table 5 also showed the relationship between the debt ratio (i.e., leverage) and return on equity.

The result showed a positive and significant relationship between leverage and return on equity. This implied that the higher the debt ratio of the firms, the higher their return on equity, which means that a unit increase in leverage of firms, will increase ROE. The capital expenditure has an insignificant effect on the ROE, which means a unit increase in the capital expenditure incurred by the firm, will result to a 0.09% fall in her ROE. The regression result showed that the R-squared value of 0.40 indicates that the CEO characteristics successfully explained 40% of the changes in the firm’s return on equity.

Table 5 results like in Table 4 showed that CEO origin has a positive and significant impact on return on equity. According to the result, the implication of this is that when a CEO is appointed from within the company, it will improve the financial performance of firms in terms of return on equity (ROE). This result is consistent with this conclusion that says better performance through an increase in shareholder’s return is attributed to CEO insider (Marwan, et al. 2020; Khan & Vieito, 2013; and Rhim et al. 2006; Favaro, K., Per-Ola, K., & Neilson, G. L. 2011).

Zhang and Rajagopalan (2010; Barber & Odean, 2001) showed that men trade more excessively than woman. They are more confident that their investment will result in profit, regardless the level of knowledge they have on their investment opportunity, which most times lead to their underperformance, Furthermore, the tenure of a CEO on the return on equity of a firm is insignificantly negative showing that the longer the tenure of a CEO will cause a 6.50% fall in their ROE. This supports the Agency Theory which asserts that elongated tenure of CEO can lead impaired board independence as such, longer tenures of CEO affect board’s monitoring and hence firm performance.

In a bid to examine the effect of CEO characteristics on the financial performance of firms in Nigeria, the study concludes that two of the characteristics employed in this study (CEO gender & tenure) have no effect with the firm’s performance indicators used (ROA & ROE), while the third characteristics (CEO origin) showed a positive effect with both ROA and ROE. Two variables were adopted to serve as control in the analysis, leverage has a positive effect on both ROA and ROE but capital expenditure has a negative effect on the firm’s performance. It can be concluded that Male dominates the CEO position of the selected firms across the sectors listed on the NSE which brings a negative effect on the performance of the firms which open to us that their female counterpart could have a positive effect on the performance of the firms in support of Khan and Vieito (2013) who examined the relationship between CEO gender and firm performance by looking at a panel set of companies situated in the United States during 1992-2004. Their initial hypotheses, similar to that of Davydov et al. (2017), are also that female CEOs exhibit stronger firm financial performance on average, compared to their male counterparts. In addition to this, they also hypothesize female-led firms to exhibit lower risk levels. Both these hypotheses were proven to be correct since the coefficient for a female CEO is both positive and statistically significant. Furthermore, the longer the CEO stays in this office, the decrease the performance of the firm which concur to the paper of Miller (1991).

CONCLUSION

This study concludes that CEO appointed from the company has a positive effect on the firms which could be as a result of many reasons like familiarity with the nature of the firm and the industry, ability to relate with the board and staff of the firm to achieve the objective of the firm which an outsourced CEO may not enjoy or achieve within his early years of appointment. This study hereby recommends that: Firms should adopt internal recruitment in appointing CEO, as they tend to possess insider-knowledge and experience peculiar to the firm’s nature of work and relationship with the staff that an outsourced CEO may not have opportunity to immediately after his appointment and could be a major set-back in fulfilling the goal of the firm.

Furthermore, due to the domination of the male gender in the CEO position of most of the Nigerian firms, it’s hereby recommended that room should be given to the female gender to take up this responsibility as studies has shown that there are competent women that possess external networks, information, and other characteristics that can be useful for firms. Also, firms should reduce the tenure a CEO can span in his/her office by setting a maximum number of years’ tenure should last, but could extend if the performance of the firm has a reasonable increasing rate since such CEO assume office. Finally, firms should try as much as possible to increase their debt ratio (leverage), because increase in debt level does commensurate to an increase in firm performance.

REFERENCE

- Adams, R. B., Almeida, H., & Ferreira, D. (2005). Powerful CEOs and their impact on corporate performance. Review of financial studies, 18(4), 1403-1432.

- Al-Matari, E. M., Al-Swidi, A. K., & Fadzil, F. H. B. (2014). The measurements of firm performance’s dimensions. Asian Journal of Finance & Accounting, 6(1), 24-49.

- Alutto, J. A., & Hrebiniak, L. G. (1975). Research on commitment to employing organizations: Preliminary findings on a study of managers graduating from engineering and MBA programs. In annual meeting of the Academy of Management, New Orleans.

- Berle, A. and G. Means. (1932) The Modern Corporation and Private Property (New York, Macmillan).

- Binacci, M., Peruffo, E., Oriani, R., & Minichilli, A. (2016). Are all non-family managers? (NFMs) equal? The impact of NFM characteristics and diversity on family firm performance. Corporate Governance: An International Review, 26(6), 569–583.

- Brown, R., & Sarma, N. (2007). CEO overconfidence, CEO dominance and corporate acquisitions. Journal of Economics and Business, 59(3), 358–379.

- Caiyun Liu & Hui Jiang (2020) Impact of CEO Characteristics on Firm Performance: Evidence from China Listed Firm, Applied Economic Letter, 27(14), 1-5

- Finkelstein, S., & Boyd, B. K. (1998). How much does the CEO matter? The role of managerial discretion in the setting of CEO compensation. Academy of Management journal, 41(2), 179-199.

- Favaro, K., Per-Ola, K., & Neilson, G. L. (2011). CEO Succession 2010: the four types of CEOs. Strategy Business, 63, 1–14.

- Finkelstein S, & Hambrick D.C. (1990) Top-management-team tenure and organizational o outcomes: the moderating role of managerial discretion. Administrative Science Quarterly 35(2)84–503.

- Fligstein, N. (1990). The transformation of corporate control. Cambridge, MA: Harvard U University Press

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of management review, 9(2), 193-206.

- Jelle Diks (2016). The impact of CEO characteristics on firm value. International Journal of Economics and Finance, 3(1), 105–115.

- Khan, W.A. & Vieito, J.P. (2013). CEO gender and firm performance. Journal of Economics and Business. 67, 55-66.

- Linck, J. S., Netter, J. M., & Yang, T. (2008). The determinants of board structure. Journal of Financial Economics, 87(2), 308-328.

- Mio, C., Fasan, M., & Ros, A. (2016). Owners’ preferences for CEOs characteristics: did the world change after the global financial crisis? Corporate Governance: The International Journal of Business in Society, 16(1), 116–134.

- Sani Saidu (2019) CEO characteristic and Firm Performance: Focus on Origin, Education and Ownership, Journal of Global Entrepreneurship Research, 9:29, 1-15.

- Suherman S., Malifirah, T.F., Usman, B., Kurniawati, H. & Kurmati, D. (2023) CEO Characteristics and Firm Performances: Evidence From Southeast Asian Country, Corporate Governance, 23(7), 1526-1563.

- Uyagu, D.B. (2017). CEO characteristics and financial performance of Nigerian banks. IMSU Journal of Business, 6(3), 123-132.

- Veprauskaite, E., & Adams, M. (2013). Do powerful chief executives influence the financial performance of UK firms? British Accounting Review, 45(3), 229–241.

- Victoravich, L. M., Xu, P., Buslepp, W., & Grove, H. (2011). CEO power, equity incentives, and bank risk taking. Banking & Finance Review, 3(2), 1–30.

- Waqas Ali and Ma Xin (2020) Impact of CEO Characteristics on Firm’s Performance Evidence from Pakistan Stock Exchange. International Journal of Academic Management Science Research (IJAMSR) 4(2), 1-14

- Zhang, X., Tang, G., & Lin, Z. (2016). Managerial power, agency cost and executive compensation–an e empirical study from China. Chinese Management Studies, 10(1),119–137.