Assets Liability Management, Macro-Economic Factors and Performance of Pension Funds Administration in Nigeria

- Moses Tunde Oyerinde

- Dr. Folake Feyisayo Olowokudejo

- Prof Musa Adebayo Obalola

- 2429-2440

- Jul 17, 2024

- Finance

Assets Liability Management, Macro-Economic Factors and Performance of Pension Funds Administration in Nigeria

Moses Tunde Oyerinde, Dr. Folake Feyisayo Olowokudejo, Prof Musa Adebayo Obalola

Department of Actuarial Science & Insurance, Faculty of Management Sciences, University of Lagos

DOI: https://dx.doi.org/10.47772/IJRISS.2024.806184

Received: 18 May 2024; Revised: 08 June 2024; Accepted: 14 June 2024; Published: 17 July 2024

ABSTRACT

The paper aims to investigate the impact of macroeconomic factors on the performance of pension funds administration in Nigeria. The paper utilized a purposive and convenience sampling method, collecting secondary data from 12 pension fund administration (PFA) companies for the years 2010-2021. The availability of audited financial statements was crucial in selecting the sample. The research design adopted was ex post facto, and descriptive analysis and inferential statistics were conducted to assess the suitability of the data. The research question was addressed through regressions, with the Hausman test rejecting the null hypothesis of a random effect model. The findings indicate that the real GDP growth rate has a negative and insignificant relationship with the performance of PFAs, as measured by the return on assets (ROA). This study highlights the importance for policy-makers and regulators in the pension funds industry to recognize the varying contributions of different assets and liabilities to company performance. It is recommended that pension funds focus on managing their assets and liabilities creatively to maintain performance despite fluctuations in macroeconomic factors.

Keywords: Administration, Pension, fund, performance, and Macro-economic

BACKGROUND OF THE STUDY

Pension fund management plays an important role, not only in the performance of the organization but also contributes significantly to the overall economic development. An effective management of assets and liabilities can improve performance of any companies and investors, Pandey, et, al (2022). An asset-liability management is noted to be an internal factor and values within a company while external factors such as the economic environment can affect the performance/ performance of pension management companies. These external and internal factors are seen to be micro and macro-economic factor of an organization. Thus, this study investigates on the impact of macroeconomic factors on the performance of pension funds administration in Nigeria.

Furthermore, evaluating the impact of macroeconomic factors seeks to provide insight into strategies that can improve the overall performance and sustainability on the performance. Hence, this is set to analyzed the organization strategies, administrator, policy-makers and regulators, thus, examining how macroeconomic factors of assets and liabilities impacts a pension fund’s financial results, and pension fund management in the country.

Over the year, the problem of pension fund administration has been associated to improper operating procedures, inability to effectively manage assets and liabilities Kwiatkowski, et al (2020). Also, Outdated or manual systems, fragmented data management, and lengthy administrative processes can hinder accurate, reconciliation, and decision-making by the pension administrator. These deficiencies can lead to increased costs, errors, delays in fund transfers, and difficulties in managing commitments, ultimately affecting the financial performance, and macroeconomic factors on the performance.

Furthermore, to rationalized the research aim, the study set a hypothesis from different author, if there is/no significant relationship between GDP, shareholder funds and the performance of pension funds” in other to understand and examine macroeconomic factor on pension fund, scholars have examine the correlations between real GDP growth and the performance of pension firms Wanjiku ( 2014) Sanusi and Kapingura (2021), Ertuğrul, and Gebeşoğlu (2020),but little evident about the Nigeria situation.

Moreso, this study add to the body of knowledge by analyzing the great importance to PFA companies as it would aid them in seeking macroeconomic investments in assets that are capable of bringing in higher returns. This will make them to maximize returns and attract patronage in form of retirement savings contributions from employees.

LITERATURE REVIEW

Overview

Macro-economic determinants refer to statistical indicators that reflect the present condition of a state’s economy within a specific sector Chetthamrongchai et, al(2020). These indicators are typically released on a regular basis at scheduled times by both governmental bodies and private entities within the economy. Investment analysts who specialize in macroeconomics offer valuable insights into potential fluctuations that may occur in response to significant fundamental announcements and events. By considering these macro-economic variables before making investment decisions, individuals and institutions can leverage these resources such as asset liability management to enhance their investment strategies.

Steindal and Grung (2021) asserted that asset liability management (ALM) plays an important role in determining the financial performance especially in PFAs. Thus, they must effectively handle administrative expenses, pension payments, and other liabilities to increase costs. By implementing streamlined processes, leveraging technology solutions, and adopting efficient operating practices, PAs can reduce costs, improve performance, and improve their overall financial performance. Hence, Pandey, et al (2022) viewed effective cost management also enables program assistants to offer competitive rates to donors while ensuring sustainable growth and performance.

However, Widjaja (2024), seen asset-liability management (ALM) as the practice of managing a business in a way that ensures coordination between asset and liability decisions, leading to optimal use of an organization’s assets and increased profit. ALM involves intelligent management of qualification risks to achieve high returns and performance Kizito (2021). Hence, a comprehensive understanding of the concept of Asset Liability Management (ALM) provides organizations with a clear understanding of the risk-return trade-offs they are making.

Aliu, Salam, Haliru and Kasum (2020) noted that asset and liability management has a significant impact on the financial performance of Pension Fund Trustees (PFAs) in Nigeria. By focusing on maximizing investment returns, aligning assets and liabilities, ensuring regulatory compliance, controlling costs, and improving transparency, by this pension financial administrator can achieve sustainable financial results. Rigorous asset and liability management is essential to meet pension obligations, maintain financial stability, and provide reliable pension benefits to shareholders, ultimately contributing to the growth and stability of the pension industry in Nigeria.

Empirical Framework

The asset and liability management (ALM) framework refers to the practical application of managing a business by making coordinated decisions and actions regarding assets and liabilities Widjaja (2024). ALM is a crucial endeavor for any enterprise that receives and invests money to meet capital requirements and future financial needs. The Society of Actuaries defines ALM as an ongoing strategy for pension fund administration, involving the formulation, implementation, monitoring, and revision of strategies related to assets and liabilities. The objective is to achieve the organization’s pension fund goals, taking into account risk tolerances and other constraints. Depending on the specific context, ALM can have various characteristics. For example, in the case of derivative businesses and investors, assets and liabilities are seen as comparable entities traded in the pension fund market. On the other hand, the ALM of pension funds focuses on determining an optimal investment policy when liabilities cannot be altered. The primary goal of such pension funds is to ensure the payment of lifelong benefits through investment contributions. Therefore, the investment policy must satisfy two conditions: long-term solvency and short-term liquidity. The ALM of a pension fund involves finding the most effective investment policy considering the stochastic nature of asset returns and liability cash flows. A multi-stage stochastic programming model would be the ideal approach for a dynamic portfolio. However, computational limitations prevent the entire planning horizon of the pension fund from being covered.

There are numerous essential factors crucial for asset liability management in pension funds. Kozak (2011) conducted a study on the determinants of performance of non-life insurance companies in Poland. By utilizing a panel dataset from various pension administration agencies between 2012-2019, the results of the regression model indicated that an increase in gross premiums and a decrease in total operating costs had a positive impact on the performance of these companies. Ajibola (2016) examined the relationship between ALM and bank performance in Nigeria using time series and cross-sectional data from selected credit pension fund administrations. The results showed that asset variables were positively correlated with equity returns, while liability variables had the opposite effect.

For pension funds, proactive ALM necessitates the integration of pension liabilities into the asset allocation process. Liabilities can be viewed as negative cash flows projected to occur at different points in the future to measure market risk. Sayeed and Hoque (2010) explored the impact of ALM on performance by comparing public and private commercial banks in Bangladesh. Through panel data analysis, they discovered a significant negative relationship between assets, liabilities, and bank performance in Bangladesh.

The relationship between ALM and the performance of pension fund administration in companies is an area that has received limited attention, as evidenced by the lack of literature on the subject. Furthermore, while the SCA model has been applied to the pension fund administration industry, its full application to the pension fund administration sector, particularly in life pension funds, remains incomplete. Given that pension funds administration, banks, and insurance sectors operate within the same domain, further research in this area is warranted.

METHODOLOGY

The research design used is a descriptive research, focusing on describing and explaining the current situation regarding asset and liability management and pension fund management in impact of macroeconomic factors on pension fund financial performance. Secondary data (electronic) is used as a primary data collection tool because of its ability to collect highly confidential information without exposing the researcher to the risks associated with other methods such as observation.

The studies analyze twelve years (2010 to 2021) of pension data from selected pension administration institutions in Nigeria, including a population of 19 PENCOM-licensed entities. Hence 12-sample size were duly selected for the study this was determined based on audited requirements of the company presence, the complete audited financial statements are available for analysis, resulting in the selection of 12-PFAs including FCMB Pension, ARM Pension, FUG PFA, Radix PFA, OAK PFA, Fidelity PFA, IEI ANCHOR PFA, Leadway PFA; Crusader Sterling PFA, Trust Fund PFA, STANBIC IBTC PFA and PAL PFA. This selection called for purposeful sampling techniques which are used to draw a portion of the population that meets the criteria, of ensuring that complete audited financial statements are available for analysis and the fact that the PFAs are in existence during the period of study.

Secondary data collected through databased are essential to the study, as they provide relevant information that is analyzed using the e-view method for full testing and interpretation. The study used secondary data, specifically the electronic presentation method, to collect and analyze information relevant to the study. This secondary data were obtained from the National Pension Commission database and the websites of selected pension administration companies.

The data cover a 12-year period from 2010 to 2021, focusing on 12 selected pension fund management companies in Nigeria. The analysis method involves using panel data (time series: electronic presentation format) to analyze the financial statements of pension administration companies. The study aims to examine the impact of asset and liability management on the performance of pension funds in Nigeria. The concept of asset liability management is based on return on assets (ROA) in the context of Nigerian pension fund management.

The data were analyzed using Pearson product moment correlation and logistic regression; this was done to understand the relationship between the independent and dependent variables. Regression models are developed to explore the effect of independent variables on dependent variables, with equations formulated to represent these relationships.

Financial Performance (Y) = α₀ + β₁x₁ + β₂x₂ + β₃x₃ +β₄x₄+ β₅x₅+ е it

Where

β₁, β₂, β₃, β₄, β₅ = represents the coefficients for the independent variables.

α₀ = represents the intercept for X variable of performance of PFA.

The basic theoretical framework is based on the fact that ALM has potentially positive or negative energy on the performance of financial firms in the presence of other factors such as the market structure and macroeconomic conditions. These macroeconomic factors have been incorporated by Owusu and Alhassan (2021). Liu, et, al (2021) and Ceylan, (2021) in a bid to present the traditional model in a modified way. Liu, et, al (2021) posits that if these factors are not included in the model, the regression results may be unreliable and the coefficients biased. Thus, the SCA model is basically:

![]()

Where Y represents the profit of the firm

At, is the ith asset, i = 1,2…..m

Lj is the jth liability, j = 1,2,….n

l represents the number of firms, l = 1,2.,..k,

t is the time period, t = 1,2,…..T

α2iis the rates of return and shows the variations in profit by replacing one unit of cash with one unit of the ith asset and is expected to be positive or non-negative.

α2i represents the rate of cost of liabilities and indicates the changes in profit by adding one unit of cash and one unit of jth liability and is expected to be negative or non-positive.

α3j is a constant term, and

elt, is the stochastic error term accounting for stochastic differences among the firms Owusu and Alhassan, (2020)

Kramaric, Miletic and Pavic (2017) in adopting this model for the Pension industry stated it thus:

Yit ![]() .(2)

.(2)

εit = Zi + Uít

where Yit is the performance of the PFA company i at time t, with i = 1…, N; t = 1…, T.

Xit are k independent variables;

εit is the disturbance term with Zi being the unobserved Pension-specific effect and uit being the

idiosyncratic error as a one-way error component regression model.

In order to incorporate the effect of macro-economic factors in the analysis, the growth rate of GDP and inflation rate is introduced into the model. This is in line with the works of (Liu, Wang, & Xu, 2024). Thus, the modified model used in this study is presented as:

Yit = αj + Σα2i Ait + Σα3 Ljit + GDP + LNFR – eit…………………………………(3)

Where Yit is the performance ratio (ROA) of PFA company l at time t,

At is the ith asset, i1,2,3,4

Lj is the jth liability, j = 1,2,3,4

l represents the number of firms, l =1,2,….10

t is the time period, t = 1,2,…12

GDP is the real GDP growth rate for years 2010-2021; and

INFR is the corresponding inflation rates.

αj is a constant term, and el, is eit the stochastic error term.

A description of both the explained and explanatory variables and their apiori expectations is as follows:

| Variablc Performance | Description | Expected sign |

| ROA Assets | Return on assets

Profit after tax/total assets |

|

| Cash and cash equivalents | Positive (+) | |

| Financial assets | Positive (+) | |

| Debtors and prepayments | Positive (+) | |

| Liabilities | Property and equipment | Positive (+) |

| Macro-economic factors | ||

| GDP | Real GDP growth rate | Positive (+) |

| INFR | Inflation rate | Negative (-) |

With the description of variables above, the model specification can be translated thus:

ROAit=αj + ![]() + + +

+ + + ![]() + + + GDP + 1NFR + eit………………………….. (4)

+ + + GDP + 1NFR + eit………………………….. (4)

Assumption:

This analysis assumes that companies with a negative return of assets are assigned a probability ratio (Y) of zero.

Secondary data collected is prepared in Microsoft excel and imported to E-views 9 for analysis. Panel data analysis is carried out in line with the objectives of the study. Mohajan (2020) opines that the advantage of using panel data is that it controls for individual heterogeneity and less collinearity among variables. Moreover, trends in the cross sectional data can easily be tracked which would have been difficult to achieve with either the trend series or the cross sectional data Liu, et, al (2024). The time series data also allows for dynamic adjustment. Data is subjected to descriptive statistics, correlations, and panel data regressions. The Hausman test is used to determine the preferred model out of fixed effect and random effect models.

The operationalization of Research Variables are Variables used in the analysis are chosen based on relevant theory and literature in line with similar studies on the subject and based on the availability of data (secondary source). The data collected are presented in a tabulated and are interpreted in relation to the research objectives.Then, in the study, nominal variables are used to measure the variables. Basically, nominal variables can be placed into categories like male/female, young, adult, senior or freshman junior/ senior etc. The study has two measurement variables (assets and liabilities management and pension funds administration), to analyzing the data (hypothesis test).Dependent Variables are Pension funds administration was the independent variable for the study, while the Independent Variables are Assets and liabilities management was independents variables of the study.

Data Presentation

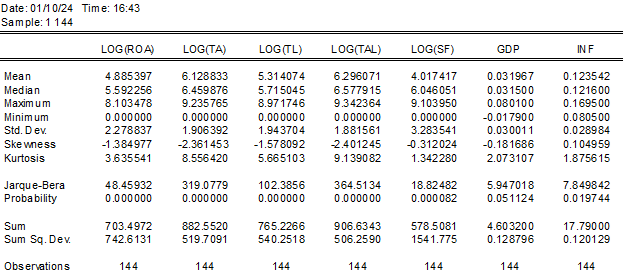

Table 1 below displays the statistical summaries of both the explanatory and explained variables, derived from a dataset amalgamated from 12 PFA firms, totaling 144 observations.

Table 1: Descriptive statistics

Source: researcher’s computation from Eviews 12

Regarding economic indicators, the Gross Domestic Product (GDP) growth rate holds a mean value of 0.031967, deviating by -0.181686, reflecting a relatively narrower variation from the mean. Conversely, the Inflation Rate (INF) ranges from a maximum of 16.95% to a minimum of 8.1%, with observations deviating by 2.898. In comparison to the mean GDP value, there appears to be less variability in GDP growth rates, similar to the pattern observed in inflation rates. Notably, all variables, except for INF, demonstrate negative skewness. Additionally, except for LOG(SF), GDP, and INF, all other variables exhibit leptokurtic characteristics, signalling a distribution with a higher frequency of values farther from the sample mean. Conversely, LOG(SF), GDP, and INF, with kurtosis values less than 3, display platykurtic tendencies, indicating a flattened distribution with more values clustered around the sample mean.

Furthermore, employing the Jarque-Bera test to assess normality, only GDP, despite being platykurtic, displays probabilities greater than 0.05, suggesting a normal distribution. The deviation from normality in the other variables could potentially be attributed to the considerable disparity in variations from the sample mean in the raw data.

Analysis of Data

A unit root test was conducted on the dataset to examine its stationarity. Given the substantial magnitude of assets and liabilities values, a logarithmic transformation to the base 10 was applied to the data for this and subsequent analyses. This transformation aimed to reduce data variability, ensure uniformity, and produce more reliable outcomes. Both the Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) tests using Fisher’s chi-square were utilized to assess stationarity. These tests evaluate the null hypothesis of a unit root against the alternative that the time series data for the variables are stationary. Rejecting the null hypothesis indicates that the series is stationary, implying it is integrated at order zero. Conversely, if the series is non-stationary, it is integrated at a higher order and must be differenced until it achieves stationarity or reaches the second order differencing, whichever occurs first.

Unit root test

| Variable | ADF | PP-Fisher chi square | Order of Integration | ||

| Statistics | Probability | Statistics | Probability | ||

| LOG(ROA) | -6.586044 | 0.0000 | -6.447905 | 0.0000 | I(0) |

| GDP | -12.25448 | 0.0000 | -6.322316 | 0.0000 | I(0) |

| INF | -7.919895 | 0.0000 | -8.895453 | 0.0000 | I(0) |

Source: researcher’s computation from Eviews 12

The table reveals that all the variables exhibited stationarity at level I(0). This suggests the absence of a unit root in all studied variables, indicating no shocks in the model and a likelihood that future statistical patterns will replicate past behavior.

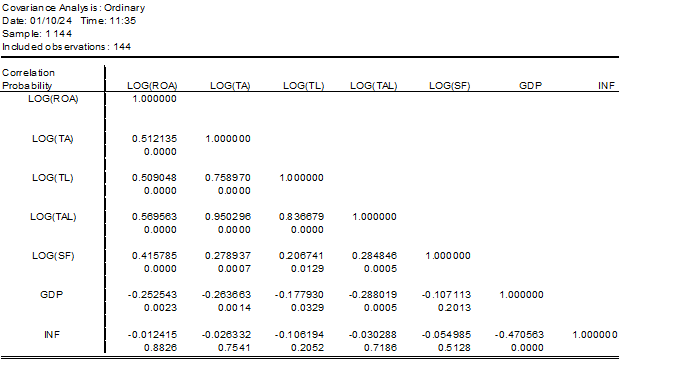

Correlation Analysis

To determine the degree of relationship between the variables, a correlation analysis was performed. This is due to the propensity of multiple independent variables in a research investigation to provide an inflated and deceptive contribution valuation while elucidating the dependent variable. When two or more independent variables have substantial collinearity (0.7 and above), this is typical. Regression coefficients with very large standard error estimates might result from multicollinearity. As a result, incorrect inferences regarding the importance of the independent variables in the model under study may be drawn. The idea that independent variables in a research analysis are interdependent would be violated by this.

Correlation coefficient values fall within the range of +1 to -1. A perfect positive link between the two variables is shown by a correlation value of +1, whilst a perfect negative association is indicated by a correlation coefficient of -1. There isn’t a linear relationship between the variables when the correlation coefficient is zero. This study employed the most popular bi-variant correlation statistic, the Pearson product correlation, and the results are shown in the table below.

Pearson Correlation Matrix

Source: Authors computation from Eviews 12 * probability values significant at 5% level

The correlation matrix of the variables, as determined using the Eviews 12 statistical software, is displayed in the table along with the coefficients and probability at the 0.05 level of significance. The correlation coefficient, which reflects the degree of correlation between the variables, is represented by the upper value, and its significance is shown by the probability values displayed in the lower value. It is evident that the majority of the variables’ correlation coefficients are less than 0.5. No relationship is perfect; none is positive (+1) or negative (-1). This lends support to the collected data and its appropriateness for the study by demonstrating the lack of multicollinearity among the variables. The table shows a positive correlation between assets and liabilities and performance, or ROA. This suggests that a rise in these factors causes a rise in performance. However, there is a negative correlation between ROA and the macroeconomic variables GDP and INFR. This suggests that a rise in GDP and INF simultaneously causes a fall in performance. Additionally, as the table shows, there is a negative correlation between GDP, INF, and the other independent variables.

P-values less than 5% at the 5% threshold of significance denote meaningful associations. Therefore, it is evident from the table that ROA and every other variable—aside from the inflation rate (INF)—have meaningful correlations. It is not possible to draw conclusions about the relationship between the variables’ causes and effects, despite the correlation analysis demonstrating the direction and strength of relationships between the variables. As a result, the researcher starts the regression analysis testing.

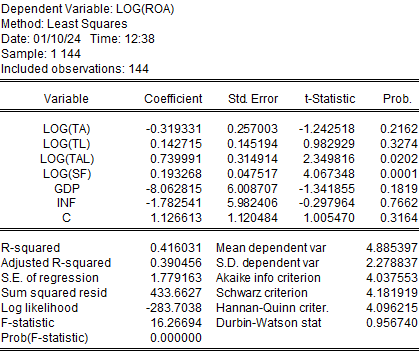

Regression Analysis

Interpretation

The Eviews 12 programme adds an intercept to the model, as shown in the table below, so that the estimations are relative to the constant term and add up to zero. The intercept does not reduce the degree of freedom because it is not a new variable to estimate. Instead, it is the mean of certain cross-sectional intercepts, which are already variables. Table shows that real GDP growth rate is negative and insignificant in relation to ROA.

The study’s factors can predict 41.6% of the performance of insurance firms, according to the coefficient of determination (R2) stat of 0.416031. How well the regression model describes the fluctuations in the dependent variable is indicated by the modified R2. With an adjusted R2 of 39%, it can be concluded that while changes in the independent variables account for 39% of the variation in ROA, additional factors not included in the model account for 61% of the change. The correlation between ROA and inflation rate was found to be positive but not statistically significant.

The p-value corresponding to the observed F-statistic is displayed by the F-statistic, which calculates the standard F-test of the joint hypothesis. An F-Stat Probability of 0.0000 in the regression strengthens the model’s validity and indicates that it fits the data well. This is because most of the models are significant.

CONCLUSION & RECOMMENDATIONS

The study aims to assess the impact of macroeconomic factors on pension fund management performance in Nigeria using a cost accounting (SCA) model and panel data approach that includes data from 2010 to 2021 across 12 pension management companies.

The central hypothesis of the SCA model is validated by analyzing the estimated rates to determine the degree of relationship between variables, which involves performing correlation analysis to address the issue of potential inflation and misleading contribution of multiple independent variables in the research study. .

The test is a test of the null hypothesis of a unit root against the alternative hypothesis that time series data for variables are stationary, while rejecting the null hypothesis indicating zero-order stationarity and non-stationarity requiring variation to reach stationarity or reach second-order variation.

The empirical results show that real GDP growth, as measured by macroeconomic factors, has no significant impact on the management and performance of pension fund management in Nigeria, which shows the importance of asset and debt management in determining function of PFAs.

The results indicate that strategic management of assets and liabilities plays an important role in addressing system risks, which is more important for pension management performance than the influence of economic factors.

Pension managers are encouraged to focus on managing their funds to reduce economic risk through asset liability management (ALM), which may explain the limited correlation observed between macroeconomic factors and the performance of PFAs.

Based on the implications of the study for policy makers and regulators of pension funds in Nigeria, it is clear that effective asset and liability management is important to a company’s performance. This highlights the importance of identifying high-return assets and low-cost liabilities to enhance performance. By managing these components well, public fund (PFA) managers can increase profits and generate value for shareholders. The recommendations that came out of the study emphasized diversifying assets to reduce risks and increase returns, providing clear information to clients, implementing strong risk management strategies, adhering to regulations, and taking macroeconomic factors into account in investment decisions. In addition, the study indicates that further research is needed to explore additional balance sheet assets and liabilities, as well as balance sheet factors, to enhance understanding of asset and liability management in pension fund management in Nigeria. This may include examining variables such as interest rates to provide further analysis of the topic.

REFERENCE

- Akwimbi, W. (2020). Effect of corporate governance, investment strategy and macroeconomic factors on financial performance of pension schemes in Kenya. Investment Strategy and Macroeconomic Factors on Financial Performance of Pension Schemes in Kenya (April 27, 2020).

- Akwimbi, W., Ochieng, D., &Lishenga, J. (2024).Corporate Governance, Investment Strategy, Macroeconomic Variables and Financial Performance of Pension Schemes in Kenya. Investment Strategy, Macroeconomic Variables and Financial Performance of Pension Schemes in Kenya (February 13, 2024).

- Aliu, O. A., Salam, M. O., Haliru, A. N., &Kasum, A. S. (2020).Effect of risk management on investment strategy and contributory pension scheme sustainability nexus in Nigeria.

- Aluoch, M. O., Mwangi, C. I., Kaijage, E. S., &Ogutu, M. (2020). The relationship between board structure and performance of firms listed at the Nairobi securities exchange. European Scientific Journal, 16(19), 337-364.

- Aminu, S. A. (2022). Financial performance of pension funds in Nigeria (Doctoral dissertation, Universidade de Lisboa (Portugal)).

- Černevičienė, J., & Kabašinskas, A. (2022). Review of multi-criteria decision-making methods in finance using explainable artificial intelligence. Frontiers in artificial intelligence, 5, 827584.

- Chetthamrongchai, P., Somjai, S., &Chankoson, T. (2020).The contribution of macroeconomic factors in determining the economic growth, export and the agricultural output in agri-based ASEAN economies. Entrepreneurship and Sustainability Issues, 7(3), 2043.

- Ceylan, I. E. (2021). The impact of firm-specific and macroeconomic factors on financial distress risk: A case study from Turkey. Universal Journal of Accounting and Finance, 9(3), 506-517.

- Ertuğrul, H. M., &Gebeşoğlu, P. F. (2020). The effect of private pension scheme on savings: A case study for Turkey. Borsa Istanbul Review, 20(2), 172-177.

- Feinberg, B., &Zanardi, M. (2022). Analysis of the influence of operational costs on increasing the financial performance of american public helath corporation. MedalionjournaL: Medical Research, Nursing, Health and Midwife Participation, 3(2), 44-57.

- Hendrawan, R., Fadhyla, N. R., &Aminah, W. (2020). Portfolio selection and performance using active and passive strategies (Assessing SRI-KEHATI index in 2013-2018). JurnalSiasatBisnis, 199-212.

- Issah, M., &Antwi, S. (2017). Role of macroeconomic variables on firms’ performance: Evidence from the UK. Cogent Economics & Finance, 5(1), 1405581.

- Kajwang, B. (2022). Role of pension management on economic growth: A review of literature. International Journal of Research in Business and Social Science (2147-4478), 11(6), 635-641.

- Khoo, Y. C., Chang, T. X., Hooi, Y. P., Ng, K. H., & Soo, S. M. (2020). Effect of macroeconomic factors on selective mutual fund performance in Malaysia (Doctoral dissertation, UTAR).

- Kizito, F. (2021). Analysis of asset-liability management practices in financial institutions in Uganda. a case of Tropical Bank Uganda (Doctoral dissertation, Makerere University).

- Kizito, F. (2021). Analysis of asset-liability management practices in financial institutions in Uganda. a case of Tropical Bank Uganda (Doctoral dissertation, Makerere University).

- Kwiatkowski, C. F., Andrews, D. Q., Birnbaum, L. S., Bruton, T. A., DeWitt, J. C., Knappe, D. R., … & Blum, A. (2020). Scientific basis for managing PFAS as a chemical class. Environmental science & technology letters, 7(8), 532-543.

- Liu, F., Li, L., Zhang, Y., Ngo, Q. T., & Iqbal, W. (2021). Role of education in poverty reduction: macroeconomic and social determinants form developing economies. Environmental Science and Pollution Research, 28, 63163-63177.

- Liu, L., Wang, Y., & Xu, Y. (2024).A practical guide to counterfactual estimators for causal inference with time‐series cross‐sectional data. American Journal of Political Science, 68(1), 160-176.

- Michael, A. O., Nwabuisi, N. A., &Trimisiu, S. T. (2022). Firm attributes and value of pension fund administrators in Nigeria. Journal of Finance and Accounting, 10(2), 96.

- Mohajan, H. K. (2020). Quantitative research: A successful investigation in natural and social sciences. Journal of Economic Development, Environment and People, 9(4), 50-79.

- Pandey, N., de Coninck, H., &Sagar, A. D. (2022). Beyond technology transfer: Innovation cooperation to advance sustainable development in developing countries. Wiley Interdisciplinary Reviews: Energy and Environment, 11(2), e422.

- Sanusi, K. A., &Kapingura, F. M. (2021). Pension funds as fuel for overall investment level and economic growth: An empirical insight from South African economy. Cogent Business & Management, 8(1), 1935661.

- Steindal, E. H., &Grung, M. (2021). Management of PFAS with the aid of chemical product registries—an indispensable tool for future control of hazardous substances. Integrated Environmental Assessment and Management, 17(4), 835-851.

- Wanjiku, E. (2014). The effect of macroeconomic variables on portfolio returns of the pension industry in Kenya (Doctoral dissertation, University of Nairobi).

- Widjaja, G. (2024). Asset and Liability Management (Alm) Strategy in Microfinance Institutions For Long-Term Financial Stability. Borjuis: JurnalOf Economy, 2(1), 25-38.

- Yamani, A., Hussainey, K., &Albitar, K. (2021). Does governance affect compliance with IFRS 7?. Journal of Risk and Financial Management, 14(6), 239.