Assets Management and Financial Performance of Listed Consumer Goods Manufacturing Companies in Nigeria

- Victor, Adediran Elumaro

- Okwo, Mary Ifeoma

- Nwoha, Chike E.

- Eze, Charles Uzodinma

- 1468-1482

- May 13, 2024

- Financial management

Assets Management and Financial Performance of Listed Consumer Goods Manufacturing Companies in Nigeria

Victor, Adediran Elumaro1, Okwo, Mary Ifeoma2, Nwoha, Chike E.3, & Eze, Charles Uzodinma4*

1,2,3Enugu State University of Science and Technology, Enugu, Nigeria

4The West African Examinations Council, Abakaliki, Nigeria

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804108

Received: 19 March 2024; Revised: 30 March 2024; Accepted: 04 April 2024; Published: 13 May 2024

ABSTRACT

The increasing shift in asset composition toward intangible components coinciding with a substantial decline in asset tangibility of companies across the globe has escalated extensive discourse among researchers in the developed economies. The aim of this study is to evaluate the effect of assets management on financial performance of the Nigeria’s consumer goods manufacturing company. The specific objectives of this study were to evaluate the effect of assets turnover ratio, assets tangibility ratio, intellectual assets ratio on return on assets of the selected consumer goods manufacturing companies in Nigeria. The study adopted an ex-post facto design. Data were generated from the audited financial reports of the seven selected listed consumer goods manufacturing company from 2012-2022. Panel multiple regression technique was employed to analyze the data using Stata 14.2. The study found that assets turnover ratio and assets tangibility have significant positive and negative effect on return on assets with t-statistics and (p-values) 2.04 (0.045) and -3.20 (0.013) respectively whereas intellectual assets ratio exerted a non-significant positive effect on return on assets with t-statistics and (p-values) 1.29 (0.232). These results imply that the shiftability concern is negligible in the listed consumer goods manufacturing companies in Nigeria. However, the proportion of tangible assets seems to have over-stretched beyond the optimal level, thereby impacting negatively on their financial performance.

Keywords: Asset Management, Total Assets Turnover Ratio, Assets Tangibility Ratio, Intellectual Assets Ratio, Return on Assets

INTRODUCTION

Statistics has shown that the Nigeria’s manufacturing sector has being playing a crucial role in Nigeria’s economy, offering immense potential for growth and development. Apart from the slight drop in the contribution of the Nigeria’s manufacturing sector to the gross domestic product (GDP) from 14.60% in 2021 to 13.99% in 2022, their contributions to the GDP has been on increasing trend since 2012. However, the sector is confronted with numerous external obstacles and some internal managerial challenges. External obstacles include issues with high rate of inflation, political and security instability, power supply and diesel costs, inadequate physical infrastructure, high interest rate on borrowing, bottlenecks surrounding access credit and excessive taxes from various government agencies. Internal challenges involve issues tethered on how to properly utilize available assets and resources in an optimal manner. Companies hold different type of assets for several reasons. However, there is always a conflict on how to ration available resources on the investment on different classes of assets and the proportion of each asset to hold at a given time on one part, and the concerns utilization, maintenance and adaption of assets to the scale of operation and changes in innovations and market trend on the other part.

An asset is a resource controlled by an entity as a result of past events and from which future economic benefits or service potential is expected to flow to the entity (Olatunji & Eyitope, 2019). Historically, assets is categorized into two, current and non-current assets. Current assets are organizational short-term benefits which usually fall within an accounting period, usually one year; while non-current assets are resources which extend beyond one accounting period. The past few decades has witnessed a transformative shift from the traditional interest in assets to the recognition of the ability of organization in harnessing their innovative potential and capitalizing on their intellectual resources (Olaoye et al., 2020; Lehenchuk et al., 2022). Lehenchuk (2022) observed that this paradigm was drive by the shift from the traditional emphasis on physical assets and labor to the limelight of intellectual properties and exchange of knowledge capital, sustained by intellectual property rights, patents and advancement in technology. Consequently, intellectual assets such as patents, brands, software, organizational structure and employee training have become an integral part of corporate assets structure; and assets classified either as tangible or intangible assets.

Assets tangibility refers to physical nature of the assets while intangible assets are the knowledge or intellectual assets possessed by a firm which reflect the core competitive competence of the firm (Tsai et al., 2012). As a norm, extensive discourse has erupted among researchers on how the evolving role of diverse types of assets is shaping the economic value and sustainability of businesses, and paving way for their lasting success (Lehenchuk et al., 2022). In this regard, Nnado and Ozouli (2016) opined that it is normal for most businesses to own several types of assets which are expected to produce benefits for the business. Hence, the belief is that no business can be sustained without adequate investment in corporate assets (Reyhani, 2012; Nnado & Ozouli, 2013; Olatunji et al., 2014).

At the moment, the business landscape has become increasingly competitive and ever dynamic; and asset management has evolved a key driver for sustainable business growth and success. Consequently, businesses have realized that intangible assets have become the core competitive advantage in dynamic marketplace. However, despite the established importance and necessity of intangible assets, the arguments on recognition of assets in the financial statements seem to have favoured the tangible assets especially in the manufacturing companies and under-developed economies in particular. The supporters of this position believed that because intangible assets are not traded in the open market, it is surrounded with problems of imperfect property rights and information asymmetries, coupled with the classification and valuation issue at the firm level which is reasonably complicated and volatile; and in event of bankruptcy, determination of the liquidation value carries uncertainties due to the fact that they tend to be more firm-specific and not easily transferrable (Berger & Udell, 1990; Black, et al., 1996; Bae & Goyal, 2009; Lei et al., 2018; Demmou et al, 2019; Pyoko, 2023). Others argued that tangible assets are pledgeable assets which can be used as collateral to support more borrowing especially in countries where the financial market is under-developed, and access to credit and alternative financing sources are scarce. (Lei et al., 2018; Arilyn 2019; Iltaş & Demirgüneş, 2020).

Meanwhile, studies from the background of intellectual capital argued that intangible assets have become a critical component of corporate financial statements in knowledge-based economies (Kogan et al., 2017; Olaoye et al., 2020; Lehenchuk, 2022), thus the rationale behind the advocacy of finance for intangible assets and the role of these assets on financial performance is a subject of substantial debate (Lei et al., 2018; Demmou et al, 2019; Pyoko, 2023). They stressed that to unlock opportunities for success, organizations need to prioritize effective assets management by optimally recognized all form of assets in their assets management strategy to position themselves toward sustainable growth and long-term profitability. Asset management refers to systematic approach to the governance and realization of value from the things that a group or entity is responsible for, over their whole life cycles (Olatunji & Eyitope, 2019). Proper assets management is a driver of operational efficiency, informed decision-making, financial performance, scalability, and customer satisfaction as well as a catalyst for business growth (Umadevi & Babu, 2015, Joseph et al., 2023). Thus, the ability to integrate these assets into a broad assets management strategy and its effective utilization can significantly impact business operations, profitability, and overall performance.

Hence, any mismatch can escalate a detrimental cost effect on the company. For instance, it has been argued that an assets model with an increase in cash reserves associated with declining asset tangibility is potentially costly for firms from financial under-developed economies because as the framework of corporate assets shifts toward intangibles, companies have to forgo some investment in tangible assets which could introduce constrain and deter growth. The other side of the argument held that this asset composition trade-off could have important implications on a firm’s external borrowing capacity, liquidity management and investment strategy. Yet, empirical evidence on strategic assets management from the background of manufacturing consumer goods companies is lacking, and little is known about how corporate assets trade-off (tangible and intangible assets) affects operational efficiency and financial performance of companies. Based on extant empirical evidence, studies on the link between assets management and financial performance produced series of inconsistent outcome. In the Nigeria instance, empirical studies from the manufacturing sector which is characterized by high assets tangibility are scarce. Consequently, this study is an attempt to fill this gap by evaluating the effect of asset management on the financial performance of consumer goods manufacturing companies in Nigeria.

LITERATURE REVIEW

Asset Management

An asset is resource controlled by an entity as a result of past events and from which future economic benefits or service potential is expected to flow to the entity (Olatunji & Eyitope, 2019). Umadevi and Babu (2015) defined an asset as a resource with economic value that an individual, corporation or country owns or controls with the expectation that it will provide future benefit. In their view, anything tangible or intangible that is capable of being owned or controlled to produce economic value or held to have positive economic value is considered an asset.

Basically, assets are classified in two ways, either in terms of nature (tangible or intangible) or in terms of duration (current or non-current assets). According to International Accounting Statndards [IAS] 38, intangible asset is an identifiable non-monetary asset without physical substance. Logically, tangibility concerns all assets of physical substance. On the contrary, Current assets are those resources that are used up within one accounting period (Babatunde, 2022). It then means that non-current assets are resources which extend beyond one accounting period. The ability of a firm to continually recombine or reconfigure diverse types of resources is the cornerstone of creating competitive advantage and improved performance. (Joseph et al, 2023). Hence, assets management became an indispensable aspect of business.

According to Olatunji and Eyitope (2019), asset management is a systematic process of deploying, operating, maintaining, upgrading, and disposing of assets in the most cost-effective manner (including all costs, risks and performance attributes). Asset management considers the entire assets lifecycle. It involves policy decisions about asset investment, use and disinvestment, and managing the asset portfolio. In recent time, assets management goes beyond management of non-current assets such as property, plant and equipment (PPE), but encompasses management of other resources such as intellectual resources, financial and information assets, and the effectiveness depends on well integration of relevant capabilities of other assets.

Assets Turnover

Asset management ratios are used to measure how effectively a company manages its assets (Purba & Bimantara, 2019). If a firm holds too much assets, the capital costs will be too high, so the profits will be depressed. On the other hand, if the assets are too low, profitable looting will also be lost. In this regard, Purba & Bimantara (2019) further stated that asset ratios are designed to answer the question whether each assets class as stated in the statement of financial position looks reasonable when compared to the level current sales and other projections. A good number of studies have asserted that total assets turnover ratio is a good measure of asset management (Prasetio et al., 2021). Zager et al. (2008) cited Zhang (2017) used the total asset turnover as a measure of firms’ efficiency in assets management and financial position. A high total assets turnover value means that the company is getting better at using its assets to generate operational income. The better the company uses its assets to get operational income; it shows that the company’s activity is quite good.

Assets Tangibility

Assets tangibility is the term used in reference to tangible assets. In contemporary literature, asset tangibility has been defined as the proportion of non-current assets to the overall assets of the company (Juma, 2018 in Pyoko, 2023), likewise as the measure of tangible goods with value that are utilized to produce income but are not offered for sale to customers (Musah et al., 2019). The possession of non-current assets of tangible nature is in determining a company’s debt level, revenue, and ultimately profitability. In fact, most studies have agreed that the possesses non-current tangible assets to a large extent serve as a guarantee for creditors that they will recover their funds in case of financial distress. As posited by Serghiescu and Văidean (2014), Tangible assets as part of the total assets are perceived by investors as a positive measure and extending the level of debt in this situation would be something perfectly normal. Nonetheless, Vo (2017) posited that in as much as tangible assets that can be used as collateral, so a high fraction of tangible assets could allow the firm to obtain external financing easily resulting in a high leverage. Therefore, the proportion of these assets should be optimized for maximum efficiency in the utilization of the assets. The current trend in the management of non-current assets of tangible nature is the strategic property asset management (SPAM). By this approach, effective policies and strategies of achieving efficiency in the deployment of non-current assets could be achieved. Nevertheless, this study measures assets tangibility as the proportion of property plant and equipment and inventory to the total assets of the firms.

Intellectual Assets

The term intellectual assets have been used interchangeably with “Intangible assets, Intellectual capital, and Knowledge assets” (Fincham & Roslender, 2003). Guthrie and Petty (2000) defined intangible assets as the soft or weightless wealth of an organisation. Zhang (2017) referred to it as the non-physical properties which are used for creating future wealth. According to the International Accounting Standard (IAS) 38, intangible asset is an identifiable non-monetary asset without physical substance. It includes patented technology, franchise agreements, computer software, licensing and trademarks among others. From intellectual capital point of view, intellectual assets include human capital, organisational structure and relational assets. Intellectual assets are very crucial for several organisations in industrial and service sectors. In his view, Zhang (2017) held that companies owned their intellectual assets as competitive advantages to generate more revenue. Lopes and Rodrigues (2007) classified intellectual assets into two, the ones that can be distinguished independently, such as copyright, patent, technologies and so on and the others that cannot be distinguished among firms or other assets, such as employee skills and experience and administrative efficiency.

Intangible assets have gained an increasingly recognition and an important component of the corporate statement of financial position in knowledge-based economies. However, some scholars still hold the belief that investments in the intangible assets are riskier compared to tangible asset for several reasons such as the problems of imperfect property rights and information asymmetries, the classification and valuation of investments on intangible asset at firm level is pretty volatile and complicated (Himmelberg & Petersen, 1994; Demmou et al., 2019).

Financial Performance

Corporate performance is a broad concept used to measure the effectiveness and efficiency of an organization in a specific area, for instance financial, productivity, market, management and so on. In this case, corporate performance will be likened to financial performance of the firms. Financial performance of a firm are usually measured using financial ratios such as liquidity ratios, profitability ratios, solvency ratio among others. Profitability is the ability of the firms to generate returns using available resources. Several studies have used several indicators to measure profitability such as gross profit margin (GPM), net profit margin (NPM), return on investment (ROI), return on sales (ROS), return on assets (ROA) and return on equity (ROE). However, this study measured performance through return on assets (ROA) that is the ability of the firm to generate profit using the assets at the disposal of the firm.

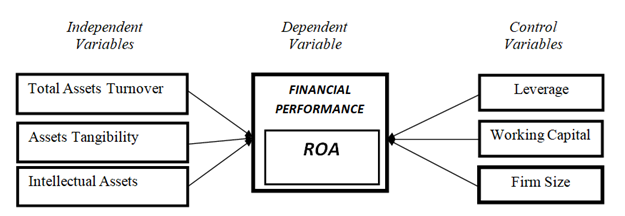

Logically, there are other indicators that have been empirically proven to have significant connection with return on capital (ROA) which did not form part of our objective. These financial indicators such as leverage ratio, working capital turnover, and firm size form the control variables in this study. Hence, the connection between asset management and financial performance as proposed in this study is conceptualized in Figure 1.

Figure 1: Conceptual framework of the study.

Theoretical Framework

The two fundamental theories connected to the work are Trade-off Theories and Resource Based Theory.

1. Trade-off Theories

The Static Trade-off Theory (STT) was first introduced by Stewart C. Myers in 1977 when he asserted that growth opportunity is inversely connected to debt, given that firms with greater investment potentials are prone to agency problems because the managers have great motivation to under-invest. The trade-off theory assumed that firms will choose a financial means level by balancing the costs and benefits of both the debt and equity financing because as they increase their debt, the marginal benefit of the debt begins to decline as the marginal cost increases (Irungu et al., 2018). This suggests that there is an optimal mix that will integrate both the costs and benefits in such a way that the marginal costs are minimized while the marginal benefit is maximized, and managers must ascertain this level.

On the other hand, Edwin O. Fischer, Robert Heinkel and Josef Zechner introduced the Dynamic Trade-off Theory (DTT) in 1989 and explicitly emphasized the concept of value maximization. They assumed that firms have a target that maximizes its value and deviations from that target are costly. In their view, firm’s capital structures may not always be as per their target assets ratios, but firms may allow the ratio to vary considering the costs and the benefits of the use of debt and equity and also the financing margin that the firm anticipates in the next period (Irungu et al., 2018). The assumption is that firms have an optimal leverage range within which they let their leverage ratios vary and can only adjusts their capital structure when leverage reaches either of the two boundaries.

2. Resource Based Theory

The second theoretical background is the Resource Based Theory (RBT) proposed by Jay Barney in 1991. The cornerstone of this theory is based on two foundational assumptions, the resource heterogeneity and resource immobility. Barney argued that the collections of assets and capabilities owned by firms are heterogeneous, that is diverse in character or content and that a firm possession of unique assets can ultimately create competitive advantage. He further argued that they complexities which arise in the management of resources may create persistence in uniqueness in the assets. Hence, firms’ attributes are not just modified, but the orientation needs to be corrected to succeed and achieve sustainable competitive advantage. In the view of Porter (1989), firm’s internal factors, such as resources and capabilities, determine a firm’s performance.

These two fundamental theories are very critical to understanding the underlying concept of asset management in the present knowledge economy. While the trade-off theories provide the basis of optimal combination of assets based on the capital structure desirability for the firms, the RBT provides a framework to highlight and predict the fundamentals of firms’ performance and competitive advantage. Resource based theoretical perspective suggests that firms can achieve competitive advantage not only by utilising critical assets, but also by building new potential capabilities via learning, skill acquisition and the accumulation of tangible and intangible assets over time. To this end, this work is anchored on the resource-based theory.

Empirical Review

The idea of using the assets turnover ratio as a measure of asset management has been conceptualized and empirically examined in the studies of the listed sea transportation companies on the Indonesia Stock Exchange for the period 2013 to 2017 and PT Pelabuhan Indonesia (Persero) from 2015 to 2021 by Purba and Bimantara (2019) and Setyawan et al. (2023) respectively. The duo measured financial performance with return on assets and employed Panel Data Regression Techniques for data analysis. The results in Purba and Bimantara (2019) showed that the fixed assets turnover has a positive and significant effect on return on assets of the listed sea transportation companies on the Indonesia Stock Exchange, but the outcome in Setyawan et al. (2023) revealed a statistically significant negative effect of total asset turnover on return on assets of PT Pelabuhan Indonesia (Persero)., In Setyawan et al. (2023), BOPO and debt-to-asset ratio exhibited a negative significant effect on the return on assets of the sampled firms. These outcomes are pointers that efficiency in asset management is needed to improve the profitability of the company.

An empirical examination of the capital structure of the consumption industry sector companies in the Indonesia stock exchange from 2016-2018 conducted by Nurlaela et al. (2019) revealed that the debt-to-equity ratio (DER), liquidity current ratio (CR), and asset turnover (TATO) have a significant effect on financial performance (return on assets). Whereas a study of 10 listed industrial firms on the Nigerian Exchange Group (NGX) from 2007 to 2016 by Olatunji and Eyitope (2019) showed that assets management improved financial performance significantly, but current assets exerted a non-significant positive impact on profit for the year; debt-equity ratio exerts a non-significant negative impact on profit for the year, and non-current assets exert significant positive impact on profit for the year. This outcome showed that assets management. However, while the former adopted a simple regression technique the latter used multiple regression.

In addition, the effect of asset tangibility on financial performance has received reasonable attention in recent times, especially in the developing economy however, the outcome seems inconsistent. Ansari and Gowda (2017) employed Pearson correlation and linear regression analysis in a study of 11 oil and gas companies listed on the Bombay Stock Exchange (BSE) and found a positive and significant relationship between capital structure and financial performance, but asset tangibility indicated a significant negative relationship with the financial performance of listed oil and gas companies in India. On the other hand, Irungu et al. (2018) used a non-experimental research design with a dynamic panel data regression model to show that asset tangibility and financial performance of the listed financial and nonfinancial firms on the Nairobi Security Exchange exhibited a direct relationship. Additionally, Arilyn (2019) used the purposive sampling method and multiple regression techniques in a study of 8 listed chemical firms on the Indonesian Stock Exchange (IDX) to empirically reveal that the effects of profitability, liquidity, and tangibility on assets turnover are statistically significant but negative whereas the effects of firm size and asset turnover were statistically non-significant.

In the study of İltaş and Demirgüneş (2020), the one-break Gregory and Hansen (1996) cointegration test and Long-run coefficients estimated by Stock and Watson (1993) DOLS methodology reveal that the long-run coefficients estimated revealed a statistically significant positive effect of tangibility, liquidity, financial leverage and operating efficiency on return on assets till the break which turned negative thereafter. While Joseph et al. (2023) and Pyoko (2023) used dynamic panel data estimation and general method of moments (GMM) and panel regression model respectively to empirically support that physical property maintenance costs and property living costs exhibited a positive effect on the return on assets of manufacturing companies in Nigeria and a a strong positive relationship between asset tangibility and long term debt indicating that asset tangibility is critical in determining the level of long term debt.

Likewise, studies that empirically examined the effect of intellectual assets on the financial performance of firms have shown that the connection between intangible assets and financial performance is positive (Zhang, 2017; Mohammed & Al-Ani, 2019; Olaoye et al., 2020; Lehenchuk et al., 2022), but in terms of magnitude, the outcome is mixed. Zhang (2017) used a sample of 17 listed telecommunication firms in China from 2014 to 2016 to show that the intangible assets ratio has a statistically strong positive effect on return on assets. Hence the study concluded that the intangible assets ratio has a positive and significant effect on firms’ financial performance. Mohammed and Al-Ani (2019) sampled 46 industrial companies listed on the Muscat securities market in Oman from 2010 to 2014 and revealed intangible assets, financial policies and financial performance have a significant influence on firm value. In a study of 9 deposit money banks in Nigeria, the result of Olaoye et al. (2020) showed a positive but insignificant relationship between intangible assets and the profitability of Nigeria’s deposit money banks. While Lehenchuk et al. (2022) used the Slovak ICT companies in Ukraine to show that research and development intensity, research and development intensity squared, and acquired intangible assets exerted a positive effect on some indicators of financial performance. Although these studies adopted analytical approaches, the results support the theoretical assumptions of intellectual assets as the source of a firm’s competitive advantage and a positive driver of financial performance.

METHODOLOGY

The study adopted an ex post facto research design. This is because it used historical data of past event which is verifiable and can be validated. Nine (9) firms from the twenty-one (21) listed consumer goods manufacturing firms on the Nigeria Exchange Group (NGX) were purposively sampled for a period of eleven years from 2012 to 2022. The sampled firms include Cadbury Nigeria Plc, Champion Breweries Plc, Floor Mill Nigeria Plc, Guinness Nigeria Plc, Honeywell Plc, Nelstle Nigeria Plc, Nigerian Breweries Plc, PZ Cussons Nigeria Plc and Uniliver Plc. This study adapted one of the Panel Multiple Regression Models used in Lehenchuk et al. (2022).

The model is stipulated below:

ROA𝑖𝑡 = 𝛼 + 𝛽1ATR𝑖𝑡 + 𝛽2TGR𝑖𝑡 + 𝛽3iaITR𝑖𝑡 + 𝛽4LQR𝑖𝑡 + 𝛽5LER𝑖𝑡 + 𝛽6WCR𝑖𝑡 + 𝛽7 LnFZ𝑖𝑡 + 𝜖𝑖𝑡

Where:

ROA = Return on Assets

β = The Coefficient

ATR = Assets Turnover Ratio

TGR = Assets Tangibility Ratio

ITR = Intellectual Assets Ratio

LER = Leverage Ratio

WCR = Working Capital Ratio

LnFZ = Natural Logarithm of Firm Size

𝜖 = error term

it = firm & time.

The Description of Variables in the Model is presented below:

Table 1: Variable and Proxies

| Variable | Name | Measurement | Source | Proxy |

| Dependent | Return on Assets

(ROA) |

|

Purba & Bimantara, 2019 | Corporate Performance |

| Independent Variables | Assets Turnover Ratio (ATR) |  |

Nurlaela et al. (2019) | Assets Management |

| Assets Tangibility Ratio (ATR) | Irungu et al. (2018) | Tangible Assets Management | ||

| Intellectual Assets Ratio

(IAR) |

|

Zhang (2017) | Intellectual Assets Management | |

| Control Variables | Leverage Ratio (LER) |  |

Nurlaela et al. (2019) | Capital Structure |

| Working Capital Ratio (WCR) | Yahaya et al. (2015) | Current Assets Management | ||

| Firm Size (LnFZ) | Natural Logarithm of Total Assets | Lehenchuk et al. (2022) | Size of Firms |

Source: Author’s Compilations (2024)

DATA ANALYSES

Summary Statistics and Normality Test

Table 2 shows the mean and median a powerful statistical measure of mid-point even though vulnerable to extreme values for the periods in ninety-nine observations. The difference between the mean and the median values indicated that return on assets and natural logarithm of total assets skewed left as signaled by the negative values -0.0082 and -0.1574, whereas assets turnover ratio, assets tangibility, intellectual assets, leverage, and working capital ratio skewed right as inferred by the values 0.1670, 0.2028, 0.0280, 0.0904 and 0.2230 respectively. Again, the standard deviation showed that the assets tangibility, assets turnover ratio, natural logarithm of total assets, leverage and working capital ratio of listed consumer goods companies in Nigeria were most volatile in the period. Finally, the standard errors of the mean, the most valuable estimator showed that apart from assets turnover ratio (0.1594) assets tangibility (0.2098), and natural logarithm of total assets (0.1178), other variable exhibited quite small values and conformed to the theoretical proposition of getting lesser as the sample size advances to the population.

Table 2: Summary Statistics and Normality Tests

| stats | roa | atr | tgr | itr | ler | wcr | lnfz |

| obs | 99 | 99 | 99 | 99 | 99 | 99 | 99 |

| Summarize Statistics: | |||||||

| mean | 0.0312 | 1.0969 | 1.0187 | 0.0314 | 0.6901 | 0.1994 | 18.3538 |

| median | 0.0394 | 0.9299 | 0.8159 | 0.0034 | 0.5997 | -0.0236 | 18.5112 |

| sd | 0.2207 | 1.5864 | 2.0873 | 0.0739 | 0.9777 | 0.7845 | 1.1695 |

| se(mean) | 0.0222 | 0.1594 | 0.2098 | 0.0074 | 0.0983 | 0.0788 | 0.1175 |

| min | -2.0176 | 0.2444 | 0.6188 | 0.0000 | 0.1936 | -0.9260 | 15.1177 |

| max | 0.2649 | 16.4477 | 21.5594 | 0.2824 | 10.1017 | 3.8039 | 20.3183 |

| Normality tes: | |||||||

| skewness | -8.1584 | 9.2816 | 9.7729 | 2.5346 | 9.1492 | 1.9252 | -0.5787 |

| Pr(skweness) | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0183 |

| kurtosis | 76.6092 | 90.3760 | 96.6799 | 7.7960 | 88.5411 | 8.0756 | 2.7934 |

| Pr(kurtosis) | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.8615 |

| joint… Prob>chi2 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0659 |

| Shapiro-Wilk: | |||||||

| Prob>z | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0275 |

Source: Stata 14.2 Output, 2024.

Normality tests are used to determine whether a data set is modeled for normal distribution. The null hypothesis of this test statistic states that the distribution is normal. Also, the decision rule is such that the p-value of the test is greater than the significance levels at 5%. Table 4.1 presents the outcome of skewness/kurtosis tests and Shapiro-Wilk W’ test. The overall probability (Prob>chi2) and Shapiro-Wilk ‘w’ outcomes for all the variables suggest that the distribution is not normally distributed.

Pairwise Correlations

Table 3: Correlation Matrix with P-values involving 99 Observations

| roa | atr | tgr | itr | Ler | wcr | lnfz | |

| roa | 1.0000 | ||||||

| atr | -0.8891* | 1.0000 | |||||

| tgr | -0.9459* | 0.9796* | 1.0000 | ||||

| itr | 0.0082 | 0.0325 | 0.0163 | 1.0000 | |||

| ler | -0.9293* | 0.9677* | 0.9767* | 0.0384 | 1.0000 | ||

| wcr | 0.0436 | 0.1841 | 0.1008 | -0.3135* | 0.0721 | 1.0000 | |

| lnfz | 0.3520* | -0.1997* | -0.2912* | 0.3968* | -0.2365* | -0.0118 | 1.0000 |

Source: Stata 14.2 Output, 2024

Table 3 portrays a significant negative connection between assets turnover ratio, assets tangibility and leverage, and return on assets of listed consumer goods companies in Nigeria. It also showed that the natural logarithm of total assets a proxy of firm size is directly related to return on assets.

Diagnostic Tests

To gain an insight about the dataset, several regression diagnostic tests were carried out. Firstly, the Breusch-Pagan test for heteroskedasticity shows a Prob > chi2 = 0.2820 which statistically non-significant at 5% indicating no heteroskedasticity problem on the dataset. The Ramsey Reset test revealed F(3, 89) =4.71 with Prob > F = 0.0043 which indicating that the model is not over-specified. A test of multicollinearity revealed the variance inflation factors ranging between 1.00 and 9.23 and a mean VIF of 20.62 > 5 for the comprehensive model. The result indicated the presence of severe multicollinearity problems connected to assets tangibility ratio, assets turnover ratio and leverage with VIF values 51.24, 42.70 & 25.21 respectively. Nonetheless, this problem was corrected by employing a robust regression model that adjusted for multicollinearity.

The Levin-Lin-Chu unit-root test for all variables based on Augmented Dickey-Fuller tests indicated a range of p-value from 0.0000 to 0.0371 at lag 1 which are less that 5% indicating Stationarity. The Breusch and Pegan Lagrangian Multiplier test shows chi2 (1) = 77.92 and Prob > chibar2 = 0.0000 suggesting that the random effect model is appropriate for the model estimation. Therefore, we decide that the Random Effect Model (REM) is better. Finally, given the Hausman test result Prob>chi2 = 0.6056, we concluded that the fixed effect model is the most appropriate model for the panel dataset. However, given the presence of severe multicollinearity challenge identified in this diagnostic test, we employed fixed effect model that adjusted for robust standard error to test the hypotheses proposed in this study.

Test of Hypotheses

Table 4.3 Fixed Effect Panel Multiple Regression (Robust Standard Error) Results of Return on Assets, Explanatory Variables and Control Variables of Listed Consumer Goods Firms in Nigeria

| roa | Coef. | Robust Std. Err. | t | P>|t| | [95% Conf. Interval] | |

| atr | 0.094597 | 0.046337 | 2.04 | 0.045 | -0.012256 | 0.201450 |

| tgr | -0.115865 | 0.036209 | -3.20 | 0.013 | -0.199364 | -0.032366 |

| itr | 0.251331 | 0.194293 | 1.29 | 0.232 | -0.196708 | 0.699370 |

| ler | -0.126704 | 0.011134 | -11.38 | 0.000 | -0.152378 | -0.101030 |

| wcr | 0.010968 | 0.006580 | 1.67 | 0.134 | -0.004206 | 0.026141 |

| lnfz | -0.020674 | 0.018160 | -1.14 | 0.288 | -0.062551 | 0.021203 |

| _cons | 0.502296 | 3477996.00 | 1.44 | 0.187 | -0.299731 | 1.304323 |

| R-sq, overall | = 0.9165 | Number of obs = 99 | ||||

| F(6,8) | = 370557.47 | Number of groups= 9 | ||||

| Prob > F | = 0.0000 | corr(u_i, Xb) = -0.0037 | ||||

| sigma_u | 0.05395549 | |||||

| sigma_e | 0.04117707 | |||||

| rho | 0.63194173 | (fraction of variance due to u_i) | ||||

Source: Stata 14.2 Output, 2024

Hypothesis One: Total assets turnover ratio has no significant effect on return on assets of food and beverage manufacturing firms in Nigeria.

The result of the examination of the hypothesis one, assets turnover ratio, (a ratio of sales to total assets) exhibited a strong statistical positive effect on the return on assets of listed consumer goods manufacturing companies in Nigeria with a p-value [0.045] and coefficient (β) [0.094597]. Albeit significant, this result provides useful insight into the efficiency in utilization of assets to generate sales. This outcome implies that the assets utilization contributes significantly and positively to the financial performance of consumer goods manufacturing companies in Nigeria. This result is in alignment with the finding in Nurlaela et al. (2019), Purba and Bimantara (2019), and Olatunji and Eyitope (2019). It also negates the results of Setyawan et al. (2023) that revealed a negative significant effect on return on assets of the sampled firms.

Hypothesis Two: Assets tangibility ratio has no significant effect on return on assets of food and beverage manufacturing firms in Nigeria.

Hypothesis two tested the effect of assets tangibility ratio on return on assets of listed consumer goods manufacturing companies in Nigeria. Assets tangibility measures the ratio of tangible assets to the total assets disclosed in the statement of financial position of the companies. The outcome of this test revealed a statistical strong negative significant effect of the assets tangibility ratio on return on assets of the listed consumer goods manufacturing companies in Nigeria with coefficient [-0.115865], t-statistic [-3.20] and p-value: [0.013]. This implies that the volume of tangible assets held by the listed consumer goods manufacturing companies has exceeded the optimal level of positive contribution to profitability hence has turned to demise the return on assets of the companies. The outcome of this test agrees with the findings of Ansari and Gowda (2017) that revealed a significant negative relationship of assets tangibility with financial performance but inconsistent with the findings of Irungu et al. (2018) which concluded that asset tangibility and financial performance has a strong direct relationship.

Hypothesis Three: Intellectual assets ratio has no significant effect on return on assets of food and beverage manufacturing firms in Nigeria.

The test of hypothesis three, the intellectual assets ratio revealed coefficient (β) [0.251331], p-value [0.232] and t-statistic [1.29] which indicated a statistical non-significant positive effect on return on assets. This result implies that the ratio of intellectual assets to the total assets of the listed consumer goods manufacturing companies in Nigeria as disclosed in the statement of financial position is below optimal level yet contributes positively but non-significantly to financial performance of the companies. However, this result supports the finding of Olaoye et al. (2020) that showed a positive but non-significant relationship between intangible assets and profitability and disagree with the outcome in Zhang (2017) and Mohammed and Al-Ani (2019) that intangible assets’ ratios have a strong positive effect on return on assets.

CONCLUSION AND RECOMMENDATIONS

Subsequent to the findings of this study, it was possible to conclude that the assets turnover ratio has a positive significant effect on return on assets which implies that the extent of utilization of companies increases profitability; excessive accumulation of tangible assets has a strong negative impact on financial performance. There is also clear evidence to conclude that intellectual assets ratio as disclosed in the statement of financial position of listed consumer goods manufacturing companies in Nigeria add non-significantly to the financial performance of the companies.

Overall, there is clear evidence to affirm that the indicators of tax sheltering activities modeled in this study (assets turnover ratio, assets tangibility, intellectual assets,) and the control variables (leverage, and working capital ratio and the natural logarithm of total assets) have a very significant explanatory power to explain the variations in return on assets of the listed consumer goods manufacturing companies in Nigeria. Given these findings, the study offered the following recommendations:

- The sales of the listed consumer goods manufacturing companies should be monitored in relation to the total assets to ensure that it does not drop significantly. By effective management of assets, assets turnover ratio could be held within the acceptable intervals to boost financial performance of the listed consumer goods manufacturing companies.

- The proportion of tangible assets held by the consumer goods manufacturing companies proved to be two large and seems to have overstretched the yielding point. Therefore, genuine efforts must be channeled to trimming down the asset tangibility ratio for better performance.

- Intellectual assets ratio as in the ratio of intangible assets to total assets is still at the infancy stage of contributing to financial performance. Hence, consumer goods manufacturing firm must consent effort to utilize this opportunity presented in this trade-off between tangible and intangible assets because it will enhance their overall efficiency and foster financial performance.

Data availability on most of the consumer goods manufacturing firms led to the sampling of only nine (9) firms from the population of twenty-one (21) listed consumer goods firms in the NGX. It is also notable that consumer goods manufacturing firms are characterized by capital-intensive with high tangible manufacturing equipment disposition, therefore the outcome might differ from a study of highly knowledge-based sectors such as financial sectors, ICT and services sectors. A similar study is required in those sectors to critique or validate the empirical findings of this study. Despite these limitations, the current study has extended the academic dimension on the growing concerns on strategic assets management probing the role of intangible assets and the rational for the trade-off between tangible and intangible assets in corporate financial reporting by providing evidence from developing economy and Nigeria consumer goods manufacturing firms in particular. Again, based on extensive literature, most accounting studies have focused on silo management of a particular type of assets, but this study provide a holistic approach to assets management and assets efficiency measurement. Lastly, the current study has extended the scope of extant literature to 2022.

REFERENCES

- Ansari, M. & Gowda, M. S. (2017). Impacts of asset tangibility and capital structure on financial performance of listed oil and gas companies in India. EPRA International Journal of Economic and Business Review, 5(12), 110-114. https://eprajournals.com/IJES/article/8167

- Arilyn, E. J. (2019). The effects of profitability, liquidity, tangibility, firm size, and asset turnover on capital structure in chemical industry listed on Indonesia stock exchange from 2014 to 2018. Advances in Economics, Business and Management Research, 145, 399-404. DOI: 10.2991/aebmr.k.200626.068

- Babatunde, O. J. (2022). Current asset investment and financial performance for sustainable development of industrial goods. International Journal of Management, Accounting and Human Development, 11(1), 19-24. https://bwjournal.org/index.php/bsjournal/article/view/1056

- Bae, K.-H. & Goyal, V. K. (2009). Creditor rights, enforcement, and bank loans. Journal of Finance, 64(2), 823-860. https://econpapers.repec.org/article/blajfinan/v_3a64_3ay_3a2009_3ai_3a2_3ap_3a823-860.htm

- Berger, A. N. & Udell, G. F. (1990). Collateral, loan quality and bank risk. Journal of Monetary Economics, 25(1), 21-42. https://www.sciencedirect.com/science/article/abs/pii/0304393290900423

- Black, J., de-Meza, D. & Jeffreys, D. (1996). House prices, the supply of collateral and the enterprise economy. Economic Journal, 106(434), 60-75. https://econpapers.repec.org/article/ecjeconjl/v_3a106_3ay_3a1996_3ai_3a434_3ap_3a60-75.htm

- Demmou, L., Stefanescu, I. & Arquie, A. (2019). Productivity growth and finance: The role of intangible assets – a sector level analysis. OECD Economics Department Working Papers 1547, OECD Publishing, Paris. https://ideas.repec.org/p/oec/ecoaaa/1547-en.html

- Fincham, R., & Roslender, R. (2003). Intellectual capital accounting as management fashion: A review and critique. European Accounting Review, 12(4), 781–795. https://econpapers.repec.org/article/tafeuract/v_3a12_3ay_3a2003_3ai_3a4_3ap_3a781-795.htm

- Fischer, E. O., Heinkel, R. and Zechner, J. (1989), Dynamic capital structure choice, Journal of Finance, 44, 19-40. https://www.jstor.org/stable/2328273

- Gujarati, D. N., Porter, D. C. & Gunasekar, S. (2009). Basic econometrics: (5th ed.). New Delhi: Tata McGraw-Hill Education private Ltd.

- Gutherie, J. & Petty, R. (2000) Intellectual capital literature review: measurement, reporting and management Journal of Intellectual Capital, 1, 155-176. https://doi.org/10.1108/14691930010348731

- Himmelberg, C. P. & Petersen, B. C. (1994). R&D and internal finance: A panel study of small firms in high-tech industries. Review of Economics and Statistics, 76(1), 38-51. https://www.jstor.org/stable/2109824

- İltaş, Y. & Demirgüneş, K. (2020). Asset tangibility and financial performance: A time series evidence. Ahi Evran Üniversitesi Sosyal Bilimler Enstitüsü Dergisi, 6(2), 345-364. https://dergipark.org.tr/en/download/article-file/1211578

- Irungu, A. M., Muturi, W., Nasieku, T. & Ngumi, P. (2018). Effect of asset tangibility on financial performance of listed firms in the Nairobi securities exchange. Journal of Finance & Accounting, 2(3), 55-74. https://stratfordjournals.org/journals/index.php/journal-of-accounting/article/view/236

- Joseph, S. M.; Ismaila, I. & Omotunde, A. O. (2023). Assets Management and Organizational Performance among Listed Manufacturing Companies in Nigeria. Oguya International Journal of Contemporary Issues, 3(1), 16-27. https://oguyajournal.com/index.php/oijci/article/view/111

- Kogan, L., Papanikolaou, D., Seru, A. & Stoffman, N. (2017). Technological innovation, resource allocation, and growth. The Quarterly Journal of Economics, 132(2), 665-712. https://academic.oup.com/qje/article-abstract/132/2/665/3076284?login=false

- Lehenchuk, S., Vakaliuk, T., Nazarenko, T., Kubaščíková, Z. & Juhászová, Z. (2022). Empirical evidence of intangible assets improve the financial performance of Slovak ICT Companies, in S. Semerikov, V. Soloviev, A. Matviychuk, V. Kobets, L. Kibalnyk, H. Danylchuk, A. Kiv (Eds.), Proceedings of 10th International Conference on Monitoring, Modeling & Management of Emergent Economy – M3E2, INSTICC, SciTePress, 2023 38–52. doi:10.5220/0011931000003432.

- Lei, J., Qiu, J. & Wan, C. (2018). Asset tangibility, cash holdings and financial development. Journal of Corporate Finance, 50(C), 223-242. https://econpapers.repec.org/article/eeecorfin/v_3a50_3ay_3a2018_3ai_3ac_3ap_3a223-242.htm

- Lopes, I. & Rodrigues, A. M. G. (2007). Intangible assets identification and valuation: a theoretical framework approach to the Portuguese airlines companies. The Electronic Journal of Knowledge Management, 5(2), 193 – 202. https://academicpublishing.org/index.php/ejkm/article/view/772/735

- Musah, M., Kong, Y. And Osei, A. A. (2019). The nexus between asset tangibility and firms’ financial performance: a panel study of non-financial firms listed on the Ghana stock exchange (GSE). European Academic Research, 12(1), 450-474. https://euacademic.org/UploadArticle/3947.pdf

- Mohammed, Z. O. & Al-Ani, M. K. (2017).The Effect of intangible assets, financial performance and financial policies on the firm value: evidence from Omani industrial sector. Contemporary Economics, 14(3), 379-391. DOI:10.5709/ce.1897-9254.411 https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3751925

- Nnado, I. C. & Ozouli, C. N. (2016). Evaluating the effect of intangible assets on economic value added of selected manufacturing firms in Nigeria. European Journal of Business and Management, 8(15), 174-181. https://core.ac.uk/download/pdf/234627301.pdf

- Nurlaela, S., Mursito, B., Kustiyah, E. Istiqomah & Hartono, S. (2019). Asset turnover, capital structure and financial performance consumption industry companies in Indonesia stock exchange. International Journal of Economics and Financial Issues, 9(3), 297-301. https://www.econjournals.com/index.php/ijefi/article/view/8185

- Olaoye, S. A., Akingbade, A. O. & Okewale, J. A. (2020). Intangible assets and financial performance of Nigeria’s deposit money banks. KIU Journal of Humanities, 5(2), 391– 395. https://www.ijhumas.com/ojs/index.php/kiuhums/article/view/932

- Olatunji, T and Adegbite, T (2014). Investment in fixed assets and firm profitability: Empirical evidence from the Nigerian banking sector. Asian Journal of Social Sciences and Management Studies, 13(1), 78-82. https://ideas.repec.org/a/aoj/ajssms/v1y2014i3p78-82id442.html

- Olatunji, C. O. & Eyitope, A. J. (2019). Assets management and performance of selected quoted firms in Nigeria. American International Journal of Business Management (AIJBM), 2(11), 65-76. https://www.aijbm.com/wp-content/uploads/2019/11/H2116576.pdf

- Porter, M. E. (1989). How Competitive Forces Shape Strategy. Readings in Strategic Management, 133- 143. https://link.springer.com/chapter/10.1007/978-1-349-20317-8_10

- Prasetio, A. E, Azizah, U. S. A, Daulay, Y. (2021). The effect of total assets turnover, current ratio and financial technology on the profitability of banking companies in Indonesia. Jurnal Ilmiah Manajemen dan Bisnis, 7(2), 253-262. https://publikasi.mercubuana.ac.id/index.php/jimb/article/view/11742

- Purba, J. H. V. & Bimantara, D. (2019).The influence of asset management on financial performance, with panel data analysis. 2nd International Seminar on Business, Economics, Social Science and Technology (ISBEST 2019) Advances in Economics, Business and Management Research, 143, 1-7. https://www.atlantis-press.com/proceedings/isbest-19/125940917

- Pyoko, O. M. (2023). Assets tangibility and long term debt of firms listed on Nairobi securities exchange, Kenya. Iosr Journal of Economics and Finance (Iosr-Jef), 14(5/2), 16-20. https://www.iosrjournals.org/iosr-jef/papers/Vol14-Issue5/Ser-2/C1405021620.pdf

- Reyhani, A. G. (2012). The investigation of effect of assets structure on performance of accepted companies of Tehran Stock Exchange (TSE). Journal of Basic and Applied Scientific Research, 2(2), 1086-1090. https://www.textroad.com/pdf/JBASR/J.%20Basic.%20Appl.%20Sci.%20Res.,%202(2)1086-1090,%202012.pdf

- Serghiescu, L. & Văidean, V. L. (2014). Determinant factors of the capital structure of a firm – an empirical analysis. Procedia Economics and Finance. 15, 1447-1457. https://www.infona.pl/resource/bwmeta1.element.elsevier-1e0423ef-1cef-3802-8755-c6890e54f84b

- Setyawan, N. B., Paidi, W. S., & Ishak, G. (2023). Effect of total asset turnover (TATO), BOPO, debt to asset ratio through firm size as moderation variables on return on asset (ROA) at PT Pelabuhan Indonesia (Persero). Journal of Social Research, 2(8), 2863-2971. https://ijsr.internationaljournallabs.com/index.php/ijsr/article/view/1348

- Tsai, C. F., Lu, Y. H., Yen, D. C. (2012). Determinants of intangible assets value: The data mining approach. Elsevier, 31, 67-77. https://doi.org/10.1016/j.knosys.2012.02.007

- Umadevi, C. & Babu, P. C. (2015). The effect of asset management practices on profitability in select textile companies in India. The International Journal Of Business & Management, 3(8), 142- 154. https://www.internationaljournalcorner.com/index.php/theijbm/article/view/137831

- Utami, H. & Alamanos, E. (2023). Resource-based theory: a review. In S. Papagiannidis (Ed), TheoryHub Book. https://open.ncl.ac.uk/theory-library/resource-based-theory.pdf

- Vo, X. V. (2017). Determinants of capital structure in emerging markets: evidence from Vietnam. Research in International Business and Finance, 40. 105 – 113. https://www.sciencedirect.com/science/article/abs/pii/S0275531916302689

- Yahaya, O. A., Kutigi, U. M., Solanke, A. A., Onyabe, J. M. & Usman, S. O. (2015). Current assets management and financial performance: evidence from listed deposit money banks in Nigeria. International Journal of African and Asian Studies,, 13, 46 – 56. https://iiste.org/Journals/index.php/JAAS/article/view/25607

- Zhang, N. (2017). Relationship between intangible assets and financial performance of listed telecommunication firms in China based on empirical analysis. African Journal of Business Management, 11(24), 751-757. https://academicjournals.org/journal/AJBM/article-full-text-pdf/60F58C355210