Barriers to the Adoption of E-Marketing in The Banking Sector in Nigeria

- Ikechukwu Njoku

- Prof. Wilson Ani

- 1455-1470

- Aug 15, 2023

- Social Science

Barriers to the Adoption of E-Marketing in The Banking Sector in Nigeria

Ikechukwu Njoku, Prof. Wilson Ani

Enugu State University of Science and Technology, Enugu, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2023.70815

Received: 03 July 2023; Revised: 11 July 2023; Accepted: 15 July 2023; Published: 15 August 2023

INTRODUCTION

1.1 Background of the study

In the world today, technology is evolving rapidly. Today, artificial intelligence, robotics, smartphones and gadgets, computer programming, remote controls, and other advancements in information technology are new technologies that have triggered a revolution and altered completely the traditional world order. In most developing economies, e-marketing is somewhat a contemporary issue among practitioners, academics, and policymakers. It is one of those concepts that were birthed with rapid advancements in technology. E-marketing is a modern business tool used in the marketing of goods, services, information, and ideas through the Internet and other electronic means (El-Gohary, 2010). Coviello (2004), notes that businesses in the services sector, primarily the consultancy and professional service providers like banks, have shown a robust interest in adopting Internet technologies for marketing purposes as their type of business integration necessitates the use of computer technologies as a core activity. The practice of marketing has been redefined to a level that seeks to change the traditional concept of marketing propelled by technology. As a result, e-marketing has gained prominence as a vital tool for carrying out strategic marketing activities and gaining competitive advantage which has wide-range implications for marketing practice . Firms must take advantage of information technology, especially the internet to survive in the 21st century (Weihrich and Koontz,2005). Nnolim, and Nkamnebe (2007) opine that it is becoming obvious that firms, and consumers who continue to ignore the internet technology would soon discover the difficulty of surviving outside it beacuse it is redefining the relationship between exchange parties and determines the exchange mechanism. Rapid growth in information technology has revolutionized marketing activities and business operations worldwide. Because, businesses are adopting technology and other electronic means in conducting marketing activities, e-marketing has now developed as a new marketing philosophy.

1.2 Statement of The Problem

Some studies have been conducted on the barriers to the adoption of e-marketing in both developing and developed economies with mixed findings as documented below. For instance, research carried out by Singh (2002) noted that bank customers are reluctant to transact electronically due to poor knowledge and limited trust in the use of online platforms as well as the issue of incessant failures of online transactions. Again, adoption is often impeded by information barriers such as uncertainties concerning the performance of the internet or the future development of these technologies globally (Hollenstein, 2004). However, the studies did not dwell much on the contemporary environmental factors militating against the adoption of e-marketing in developing nations like Nigeria thus necessitating further inquiry. Some of the identified factors include; network issues, literacy level, and rising cost of living. This study, therefore, seeks to examine these barriers not covered by previous studies as they relate to the banking sector in Nigeria.

1.3 Objectives of the Study.

The broad objective of this study is to examine the barriers to the adoption of e-marketing in the Nigerian banking sector while the specific objectives are to;

- Examine the effects of the high cost of living on the adoption of e-marketing in the banking sector in Nigeria.

- Identify the effects of network issues on the adoption of e-marketing in the banking sector in Nigeria.

- Assess the effects of Literacy levels on the adoption of e-marketing in the banking sector in Nigeria.

1.4 Research Questions:

- To what extent does the high cost of living affect the adoption of e-marketing in the banking sector in Nigeria?

- How do network issues affect the adoption of e-marketing in the banking sector in Nigeria?

- In what way does literacy level affect the adoption of e-marketing in the banking sector in Nigeria?

1.5 Statement of hypotheses:

We formulated the following hypothesis to address the research questions;

Ho1: High cost of living has no significant effect on the adoption of e-marketing in the banking sector in Nigeria.

Ho2:Network issues have no significant effect on the adoption of e-marketing in the banking sector in Nigeria.

Ho3: Literacy level has no significant effect on the adoption of e-marketing in the banking sector in Nigeria.

1.6 Scope of The Study

The scope of this study covers barriers to the seamless adoption of e-marketing in the banking sector in Nigeria. Such barriers include network issues, literacy level, and the rising cost of living, as they tend to inhibit the smooth adoption of e-marketing by bank customers in Nigeria.

REVIEW OF RELATED LITERATURE

Conceptual Review.

2.1.1 E-Marketing

E-marketing is a contemporary and rapidly growing field of study in marketing such that a universally acceptable definition is still very difficult to ascertain. However, several researchers have given definitions based on their understanding of e-marketing at any point in time. As cited by Hassan and Tibbits (2000), E-marketing was defined from different perspectives by Kalakota and Whinston (1997).

- Communication perspective: Delivery of information, products/services, or payment using telephone lines, computer networks, and other electronic means.

- Business perspective: Application of technology towards the automation of business transactions and other workflows.

- Service perspective: As a tool that addresses the desire of firms’, consumers and management to cut costs of services and improves the quality of goods and speed of service delivery.

- Online perspective: Provides the capability of buying and selling products and information on the Internet and other online services;

This definition forms the basis for other definitions of e-marketing. We shall discuss some of the identified barriers below.

2.1.2 High cost of living.

In Nigeria today, inflation rate and the general cost of living is high. The current inflation rate as at April 2022 is 16.82% as released by the National Bureau of Statistics. This has affected the customers of banks who struggle to meet other needs rather than the adoption of electronic marketing.

2.1.3 Network Issues.

Network issues in Nigeria has continued to hamper the smooth operation of electronic marketing in the banking sector. Most telecommunication companies in Nigeria do not have coverage in most rural areas and sometimes they also witness epileptic power supplies. This affects electronic marketing negatively.

2.1.4 Literacy level.

Level of education and low literacy level is also one of the factors identified as a barrier to the adoption of electronic marketing in the banking sector. The higher the literacy level of a customer, the higher the probability of the customer adopting electronic marketing.

2.1.5 Conceptual Framework.

E-marketing as a process of planning and executing the conception, distribution, promotion, and pricing of products and services in a computerized, networked environment, such as the Internet and the World Wide Web, to facilitate exchanges and satisfy customer demand. (encyclopedia.com). Jansson and Soi (2000), opine that e-marketing as the new way of doing business as a result of technological development, which translates the message. EL-GOhary, (2010), sees e-marketing as a contemporary business tool applied in the marketing of goods, services, information, and ideas through the Internet and other electronic means. Strauss and Frost (2001) opine that e-marketing is the use of electronic data and applications for planning and executing the conception, distribution, promotion, and pricing of ideas, goods, and services to create exchanges that satisfy individual and organizational goals.

We define, e-marketing as a process by which organizations render or obtain goods and services, through internet-enabled computers and other gadgets to satisfy customers’ needs at a profit to the organization.

2.2 Theoretical Framework.

No doubt that e-marketing is still developing in both theory and content. However, it shares some basic theories with the traditional marketing discipline. We shall anchor our research on the Decision-Making Process Theory.

Consumer Decision-Making Process

This theory is used to understand how buyers make decisions when they are first exposed to a brand or product to the point of purchase. It is broadly divided into five sections:

- Awareness: This happens when customer becomes aware of a problem he needs to solve.

- Interest: This happens when the customer starts looking around and searching for potential solutions.

- Consideration: This is when the customer has narrowed down his choice and debates the pros and cons of each of the choices. Customer eventually makes a choice based on certain factors like quality, price, or past experiences.

- Purchase: After search, the customer is now able to make a purchase. They go to the purchase platform, add the product to their cart, and buy it.

- Loyalty: The customer’s journey ends at the purchase stage. Nevertheless, providing an excellent after-sales experience is important in ensuring that the customer will make a repeat purchase in the future and recommend the product to others customers. This is where loyalty begins.

This theory relates to both the first, second, and third objectives enumerated in this study. Both costs of living, religious considerations, and literacy level are taken into cognizance before customers decide what to buy, when, and how. For a customer of a bank to become aware of the product, they need to be literate enough to understand the relevance of that product to their daily needs, and consider the cost of getting that product and its implications on their religious belief.

2.3 Empirical Review.

Researchers and marketing experts have made various attempts to study barriers that militate against the adoption of e-marketing in both financial organizations and other sectors of the economy at different periods. Generally, many authors are of the view that technology comes first, and then other factors that impede the adoption of e-marketing follow. They also identified the fact that the role of ICT in every society influences the practice of e-marketing in that society. Other variables include high cost of living, religious beliefs, and literacy level.

Shohei Nakamura, e tal (2020) compared costs of living across different cities. The International Comparison Program (ICP;2020) reports price levels across world economies in its calculation of purchasing power parity through an extensive scale of price data collection and rigorous methodology. Even though, the price levels are reported only at the national level, it was possible to compare the cost of living across a group of cities in the world. This helped to highlight important issues regarding the data required to measure costs of living in developing world. This study is relevant in the study of barriers to the adoption of e-marketing in the banking sector in Nigeria. The higher the cost of living, the more likely that bank customers will prioritize other needs than e-marketing adoption. Al-muala& Al-Qurneh(2012) agrees with Mammon (2012) that e-product and e-price have a significant impact on sales increase and customer satisfaction. The high cost of living in Nigeria today determines the level at which customers can operate with the adoption of e-marketing in the banking sector. This study postulates that the common man is affected mostly by the inflation (cost of living) because the daily expenditure of the common man will be increased and he has to consider taking some aspects of the expenditure such as medical, education, travel social media more important than others. It is important however to note that despite all these studies, there has been no major extensive research on such contemporary issues as the rising cost of living, network issues and literacy level as factors militating against the adoption of e-marketing in Nigeria. Therefore, for this research, we believe that there is a significant positive relationship between these variables (rising cost of living, network issues, and literacy level) and the adoption of e-marketing in the banking sector in Nigeria.

2.4. Summary of Empirical review.

We shall use the table below to summarize some of the empirical studies we highlighted above.

| Name of the Author | Year | Title of the Paper | Methodology | Findings |

| Shohei Nakamura, e tal (2020) | (2020) | The International Comparison Program (ICP). Comparing the cost of living in cities. | Theoretical review. survey and designs | They found that richer cities have higher price levels than poor cities. |

| Al-muala& Al-Qurneh(2012) | (2012) | Effects of prices on e-marketing. | Theoretical review | Found that price have a significant impact on sales increase and customer satisfaction. |

2.5 Gap in Empirical Review.

Most studies on barriers to the adoption of e-marketing center mainly on internet cost, network issues, availability of technology and its application by organizations to reach a wider range of customers. However, the studies did not dwell much on other environmental factors that inhibit customers from adopting e-marketing in the banking industry. In this research, we identified such variables as network issues, literacy level, and the rising cost of living, that impede the customer’s ability to adopt e-marketing in the banking sector in Nigeria.

METHODOLOGY

3.0 Introduction

Welman and Kruger (1999), defined methodology as the application of various methods, techniques, and principles to create scientifically based knowledge utilizing objective methods and procedures within a particular discipline. This study utilized a quantitative research approache.

3.1 Research Design

Research design is a specific procedure, which is adopted in the collection and analysis of data necessary to address a problem.(Tull and Hawkins,1993).

For this study, the survey method was used; The samples chosen from the population were studied to ascertain the relationship between variables which was done through designed questionnaires, and observation. The survey method focused on self-designed and data collection from various respondents.

3.2 Area Of Study

This study centers on the barriers to the adoption of e-marketing in the banking sector in Nigeria with specific emphasis on the variables that hinder the smooth adoption of e-marketing by customers. It identified such variables as the rising cost of living, network issues, and literacy level, as contributing to the reasons why customers do not adopt e-marketing in the banking sector in Nigeria.

3.3 Sources Of Data

In this study, the researcher sourced data from the Primary sources.

3.3.1 Primary sources of Data – The researcher collected primary data through the administration of questionnaires to selected customers of banks that make use of e-marketing applications. Questionnaires were administered to the respondents after identification and were asked to tick appropriately and return same to the researcher.

3.4 Population Of The Study

The population of the study are from customers of Access, UBA, First and GT banks in Nigeria based in Owerri.

3.5 Determination Of Sample Size.

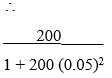

The population of the study involves the customers of banks living in Owerri. Because of the density of the Owerri population, the researcher limited the scope of this study to only some specific areas in Owerri which include: Douglas, New Owerri, Ikenegbu, Aladinma, and Orji and the customers residing in these specific areas constitute the actual population of this study. The population of the consumers selected is 200 however a sample population of 133 was determined using Taro Yamane method.

n = ![]() Where

Where

n = Sample size

e = level of significant 0.05

N = population size

200

1.5 = 133.3 = 133 sample size

3.6 Sampling Techniques

A simple survey method was used to administer the questionnaires.. The questionnaires were later collected back from each of the customers after completion and the completed questionnaires were examined for correctness and accuracy which were later arranged and analyzed for the result.

Table 3.1 Sample Size Distribution.

| S/N | Areas/ population zone | No of Respondents |

| 1

2. 3. 4. 5. |

Douglas

New Owerri Ikenegbu Aladinma Orji |

50

50 25 25 50 |

| Total | 200 |

Source: Field survey 2022.

3.7 Method of Data Collection

The instrument used for data collection was questionnaire which is both structured and unstructured. The questionnaire was distributed by the researcher by hand to the respondents. The researcher surveyed samples of the population using structured and unstructured questionnaires within the selected towns in Owerri. As the researcher noted earlier, this was chosen to easily describe, record, analyze and interpret the responses.

3.8 Validation Of Research Instrument

Validity here means to confirm the extent to which the research instrument used was able to achieve the desired results. The survey method was used to determine the validity of the study. The test methods were also used in administering the questionnaire and conducting the survey.

The questions in the questionnaire were examined by the supervisor to remove ambiguity and to ensure that the questions were not complex to understand and answer. This practice helped to make the outcome valid.

3.9 Reliability Of The Research Instrument

Although the researcher constructed the questionnaires himself, they were given to experts to analyze and make inputs. Their input and advice helped the researcher to make sure it measured the right thing. Lastly, the supervisor for this research checked and approved them before they were given to the respondents.

3.10 Method Of Data Analysis

The completed questionnaire was analyzed using the nonparametric techniques of chi-square. This was done to establish the degree of variation between the observed frequencies and expected frequencies.

DATA PRESENTATION AND ANALYSIS

In this chapter, the presentation, analysis, and interpretation of the results of the hypothesis stated were done.

The Chi-square method was used to test and examine if there is a significant relationship between the various variables used and adoption of e-marketing in the banking sector in Nigeria.

4.1 Data Presentations

The table below shows details of responses from the questionnaire distributed and collected.

Table 4.1: Showing Distribution of Questionnaire

| RESPONDENTS | FREQUENCY | PERCENTAGE |

| RETURNED | 133 | 100 |

| UNRETURNED | 0 | 0 |

| TOTAL | 133 | 100 |

Source: Field Survey, 2022

The statistical analysis above shows that 100% of the respondent filled the questionnaire correctly, which is 100%. This makes the data valid.

Analysis Of Respondents’ Bio-Data

The following are the characteristics and bio-data of the sample in the study.

Table 4.1.2

| RESPONDENTS | FREQUENCY | PERCENTAGE |

| MALE | 50 | 37.6 |

| FEMALE | 83 | 62.4 |

| TOTAL | 133 | 100 |

Source: Field Survey, 2022

The table above shows that 50 representing 37.6% were male, while 83 respondents are female which represents 62.4% of the respondents. This indicates that there were more female respondents than male respondents.

Table 4.1.2: Analysis Based on Marital Status

| RESPONDENTS | FREQUENCY | PERCENTAGE |

| SINGLE | 40 | 30.1 |

| MARRIED | 93 | 69.9 |

| DIVORCED | – | – |

| TOTAL | 133 | 100 |

Source: Field Survey, 2022

The analysis above shows that 30 respondents are single which is 30.1%, 93respondents are married which represents 69.9% while there are no divorced respondents. This implies that there are more married people in the banks than single.

Table 4.2: Analysis Based on Age

| RESPONDENTS | FREQUENCY | PERCENTAGE |

| BELOW 25 YEARS | 2 | 1.5 |

| 25 – 35 YEARS | 43 | 32.3 |

| 35 – 45 YEARS | 73 | 54.9 |

| 45 – 55 YEARS | 5 | 3.8 |

| ABOVE 55 YEARS | 10 | 7.5 |

| TOTAL | 133 | 100 |

Source: Field Survey, 2022

From the table above, it shows that 2 respondents are below 25 years and it is 1.5%; 43 respondents are within 25 -35% years which is 32.3%, and 73 respondents are within 35-45 years which is 54.9%. 5 respondents are 45 – 55 years and this represents 3.8%. Lastly, 10 respondents are above 55years and the percentage is 7.5%. This indicates that there are more respondents within 35 – 45years of age in these organizations.

Table 4.5: Analysis Based on Academic Qualification

| RESPONDENTS | FREQUENCY | PERCENTAGE |

| Primary Six | 3 | 2.3 |

| WAEC/GCE/SSCE | 10 | 7.5 |

| OND / NCE | 62 | 46.6 |

| HND/B.Sc. | 45 | 33.8 |

| M.Sc./MBA | 13 | 9.8 |

| TOTAL | 133 | 100 |

Source: Field Survey, 2022

The analysis shows that there are 3 respondents which are 2.3% having primary six certificates; 10 respondents which are 7.5% have WAEC/GCE/SSCE; 62 of the respondents are with OND/NCE qualifications which are 46.6%; 45 respondents are HND/B.Sc holders are 33.8%; 13 respondents are Master’s Degrees holders and 13%. From the above analysis, it can be seen that most of the respondents are holders of HND/B.Sc certificates.

Table 4.7. The high cost of living has a significant effect on e-marketing adoption in the banking sector in Nigeria.

| INDICATION | FREQUENCY | PERCENTAGE |

| AGREE | 83 | 62.4 |

| STRONGLY AGREE | 32 | 24.1 |

| DISAGREE | 18 | 13.5 |

| STRONGLY DISAGREE | – | – |

| TOTAL | 133 | 100 |

Source: Field Survey, 2022

The above table shows that 83 respondents agree with the question which represents 62.4%; 32 respondents agree and is 24.1%; 18 respondents disagree which represents 13.5%; none of the respondents strongly disagree. It shows that the highest percentage of the respondents agree with the statement.

Table 4.8: Network issues have a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

| INDICATION | FREQUENCY | PERCENTAGE |

| AGREE | 75 | 56.4 |

| STRONGLY AGREE | 38 | 28.6 |

| DISAGREE | 20 | 15.0 |

| STRONGLY DISAGREE | – | – |

| TOTAL | 133 | 100 |

Source: Field Survey, 2021

The table above shows that 75 respondents agree which represents 56.4%; 38 respondents agree and is 28.6%; 20 respondents disagree which represents 15%; while no respondent strongly disagrees. The analysis shows that more people agree that Network issues have a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

Table 4.9: Literacy level has a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

| INDICATION | FREQUENCY | PERCENTAGE |

| AGREE | 34 | 25.6 |

| STRONGLY AGREE | 78 | 58.6 |

| DISAGREE | 11 | 8.3 |

| STRONGLY DISAGREE | 10 | 7.5 |

| TOTAL | 133 | 100 |

Source: Field Survey, 2022

The table indicated that 34 respondents agree which is 25.6%; 78 respondents strongly agree which is 58.6%; 11 respondents disagree which is 8.3%; 10 respondents strongly disagree which is represented by 7.5%. This means that more respondents strongly agree that literacy level has a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

Test of Hypotheses

In this part of the section, the formulated hypotheses are tested one after the other using the chi-square non-parametric test.

Hypothesis One

Ho1: High cost of living has no significant effect on the adoption of e-marketing in the banking sector in Nigeria

The chi-square (x2) test of goodness of fit was used to test this hypothesis. The formula is as follows:

X2 =∑ ![]()

Where:

0 = Observed frequency.

E =Expected frequency

Σ =Summation

E = 133 ÷ 4 = 33.25

| (This is because there are 133 respondents and four responses) | |||||

| Response | O | E | O-E | (O-E)2 | (O-E)2/

E |

| A | 83 | 33.25 | 49.75 | 2,475.10 | 74.44 |

| S.A | 32 | 33.25 | -1.25 | 1.56 | 0.05 |

| D | 18 | 33.25 | -15.25 | 232.56 | 6.99 |

| S.D | – | 33.25 | -33.25 | 1,105.56 | 33.25 |

| TOTAL | 133 | 133 | – | 3,814.75 | 114.73 |

Thus, X2 = 114.73

To establish the degree of freedom, we multiply the number of rows in the table less one, by the number of columns less one.

In Table I

Number of Rows = 4

Number of Columns = 2

To get degree of freedom, V = (Rows -1) (Columns -1)

V= (4-1) (2-1)

V= 3 x 1

V= 3

In the chi-square table, the value of of X2 for 3 degrees of freedom at 5% significant level is giving as (7.815).

Decision Rule/Criterion

If the calculated chi-square (x2c) is greater than the tabulated (X2t), we, reject the null hypothesis (Ho) and accept the alternative hypothesis (H1) and vice versa.

Decision

Given the above calculation, the calculated chi-square (114.73) is greater than the tabulated chi-square (7.815) x2t. We therefore rejected the null hypothesis and concluded that high cost of living has a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

Hypothesis Two

Ho2: Network issues have no significant effect on the adoption of e-marketing in the banking sector in Nigeria.

| Response | O | E | O-E | (O-E)2 | (O-E)2 |

| /E | |||||

| A | 75 | 33.25 | 41.75 | 1,743.06 | 52.4 |

| S.A | 38 | 33.25 | 4.75 | 22.56 | 0.68 |

| D | 20 | 33.25 | -13.25 | 175.56 | 5.28 |

| S.D | – | 33.25 | -33.25 | 1,105.56 | 33.25 |

| TOTAL | 133 | 133 | – | 3,046.74 | 91.63 |

Thus, X2 = 91.63

We find the appropriate X2 value from the chi-square table. But we first establish the degree of freedom. We multiply the number of rows in the table less one, by the number of columns less one and got 3.

In second Table

In the chi-square table, the value of X2 for 3 degrees of freedom at 5% level is (7.815).

Research Result

The calculated chi-square (91.61) is greater than the tabulated (7.815) . We rejected the null hypothesis and concluded that Network issues have a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

Hypothesis Three

H03: Literacy level has no significant effect on the adoption of e-marketing in the banking sector in Nigeria.

| Response | O | E | O-E | (O-E)2 | (O-E)2 |

| E | |||||

| A | 34 | 33.25 | 0.75 | 0.56 | 0.02 |

| S.A | 78 | 33.25 | 44.75 | 2,002.56 | 60.23 |

| D | 11 | 33.25 | -22.25 | 495.06 | 14.89 |

| S.D | 10 | 33.25 | -23.25 | 540.56 | 16.26 |

| TOTAL | 133 | – | – | 3,038.75 | 91.39 |

Thus, X2 = 91.39

In the third Table

In the chi-square table, the value of X2 for 3 degrees of freedom at a 5% level is (7.815)

Decision

The calculated chi-square (91.4) is greater than the tabulated (7.815) . We rejected the null hypothesis and concluded that literacy level has a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

4.4 Discussion of Findings.

In the course of this research, we set out objectives, raised some research questions, and then developed a research hypothesis from the objectives. In testing the first hypothesis which states that the high cost of living does not have a significant effect on the adoption of e-marketing in the banking sector in Nigeria, we found that the calculated chi-square 114.73 is greater than the tabulated (7.815) . We therefore, rejected the null hypothesis and concluded that the high cost of living has a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

In testing the second hypothesis which postulates that network issue does not have a significant effect on the adoption of e-marketing in the banking sector in Nigeria, the calculated chi-square (91.61) is greater than the calculated chi-square (7.815). We therefore rejected the null hypothesis and concluded that Network issue has a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

After testing the third hypothesis which states that literacy level has no significant effect on the adoption of e-marketing in the banking sector in Nigeria, we found that the calculated chi-square (91.4) is greater than the tabulated chi-square (7.815) . We therefore rejected the null hypothesis and concluded that literacy level has a significant effect on the adoption of e-marketing in the banking sector in Nigeria.

SUMMARY OF FINDINGS, CONCLUSION, AND RECOMMENDATIONS

5.1 Summary of Findings

This research has extensively reviewed the barriers to the adoption of e-marketing in the banking sector in Nigeria.

Highlights of our findings are shown below;

- There is indeed a significant relationship between the high cost of living and the adoption of e-marketing in the banking sector in Nigeria. This shows that the higher the cost of living, the lower the rate of adoption of e-marketing in the banking sector.

- There is also a significant relationship between network issues and the adoption of e-marketing in the banking sector in Nigeria

- We also found that there is a significant relationship between literacy level and adoption of e-marketing in the banking sector in Nigeria. The higher the level of education of a customer, the higher the chances that he will adopt e-marketing in the banking sector in Nigeria.

5.2 Conclusion

In conclusion, we found that factors like the network issue, high cost of living, and literacy level are very important factors to consider by banks before launching e-marketing applications in the market. Our findings show that even though e-marketing is a very important tool for the conduct of marketing activities, there are still a lot of barriers to its adoption in the banking sector in Nigeria.

5.3 Recommendations

Given the findings from this research, the following recommendations are provided;

- The management of banks should put into consideration various environmental factors like cost of living, network issue and literacy level before launching e-marketing applications in the market.

- Banks should do more to improve the network that supports seamless adoption of electronic marketing in Nigeria.

- The education sector in Nigeria should be given adequate attention by the government to ensure that more Nigerians are educated.

5.4Suggestions for Further Studies.

Given the above findings, the following suggestions are made for further studies.

The reasons why there is constant network issues in Nigeria should be investigated and documented.

The remote reasons why the cost of living is increasing every day in Nigeria should also be investigated in a study.

A similar study should be carried out in other organizations in other sectors to see if similar results would be obtained.

5.5 Contribution to Knowledge

The primary aim of this research is to examine the barriers to the adoption of electronic marketing in the banking industry in Nigeria from a new perspective.

So far, most studies on electronic marketing adoption looks at the various activities of banks and their efforts in developing and implementing electronic marketing products but did not dwell on the reasons why people fail to key into the process.

In this study, the researcher tried to shift the focus from banks to the individual customers and this has led to the discovery of barriers based on contemporary issues. These barriers that include; Cost of living, Network issues and Literacy level are issue based. They will help in proper understanding of the reasons why customers of banks fail to adopt e-marketing in the banking sector in Nigeria.

REFERENCES

- Abor, B. (2004), “Use of E- Banking in 21st Century: The major Challenges”, Journal of Business and Finance.

- Agbonifoh, Ogwo, Nnolim, and Nkamnebe (2007); “Understanding, Customer Complaint Behaviour for Sustainable Business Development”; Journal of Economics and Management Sciences.

- Al-muala& Al-Qurneh(2012): “Assessing the Relationship between Marketing

- H.G. (2000); “Evaluating the role of Intermediaries in the electronic Value chaim” Internet Research: Electronic networking application and Policy,

- Henry, L. (2000), “The Adoption of Internet Banking in Nigeria: An Empirical Investigation, Journal of Internet Banking and Commerce.

- Hassan, R and Tibbits, ELR. (2000); “Strategic Management of Electronic commerce; An Adaptation of the Balanced Score Card” Internet Research: electronic networking Applications and Policy.

- Ibittoye, T.A. and Ajayi, O.A. (2001); Elements of Banking: commercial Banking in Nigeria, Ibadan. Bash-Moses Printing Company.

- Palmer, A. (1999); ‘The Marketing of Services Chartered institute of Marketing”. Read Educational and Professional Publishing Limited. 4th Edition.

- Prentice Hall, USA. Osuagwu, I. (2003) “Internet Appreciation in Nigerian Business Organizations” Journal of Internet Commerce,.

- Rasiah and Ming (2010); “A theoretical review of improving self service effectiveness using customer feedback at commercial banks; European journal of economics, finance.

- Sathye, M. (1999); “Adoption o Internet Banking by Australian Consumers”: An Empirical Investigation. “International Journal of Bank Marketing”. .

- Shohei Nakamura, RawaaHarati, Somik V. Lall, Yuri M. Dikhanov, Nada Hamadeh, William Vigil Oliver, Marko OlaviRissanen, and Mizuki Yamanaka (2020); comparing costs of living across world cities. The International Comparison Prog; world bank economic review

- Sheth and Sharma (2005); “International e‐marketing: opportunities and issues”; International Marketing Review

- Shih, B. & Fang, K. (2004), “The Use of Decomposed Theory of Planned Behavior to Study Internet Banking in Taiwan”, Internet Research.

- Smith, P.R. and Chaffey, D. (2005) ; E-Marketing Excellence: At the Heart of E-Business. Butterworth Heinemann, Oxford, UK.

- Strauss, J. and Frost, R. (2001);E-Marketing Prentice-Hall,. Upper Saddle River, NJ.

- Tornatzky and Fleischer (1990); “Literature Review of Information Technology Models at Firm”; Level AdoptionThe Electronic Journal of Information Systems Evaluation

- Thulani, D, Tofara, C. & Lanton, R. (2009), “Adoption and Use of Internet Banking in Zimbabwe, An exploratory study”, Journal Internet Banking and Commerce. .

- Turbid, E. Lee. J, King, D. and Chung, MH (2003) ‘‘Electronic Commerce: A managerial perspective”. New Delhi. Pearson Education Inc. Jassen, M and Soul,’

QUESTIONNAIRE ADMINISTRATION

INSTRUCTION: Please endeavor to complete the questionnaire by ticking the correct answer (s) from the options or supply the information required where necessary.

SECTION A: Personal Information/Data

Gender

- Male

- Female

Age grade

- Below 25yrs

- 25-35yrs

- 35-45yrs

- 45-55yrs

- Above 55yrs

Educational qualification

- WASCE/SSCE

- OND/HND/BSC

- MSC/PGD/PhD

- Others

Marital status

- Single

- Married

- Divorced

- Widowed

SECTION B:

Questions on the barriers to the adoption of e-marketing in the banking sector in Nigeria.

The high cost of living has a significant effect on e-marketing adoption in the banking sector in Nigeria..

- Agree

- Strongly Agree

- Disagreed

- Strongly disagree

Religious belief has a significant effect on e-marketing adoption in the banking sector in Nigeria..

- Agree

- Strongly Agree

- Disagree

- Strongly disagree

The Literacy level has a significant effect on e-marketing adoption in the banking sector in Nigeria..

- Agree

- Strongly Agree

- Disagree

- Strongly disagree

Briefly outline what you think that are the barriers to the adoption of e-marketing in the banking sector in Nigeria.