Comparative Study of the Effect of Personal Income Tax Amendment Act 2011 on Internally Generated Revenue of Adamawa State, Nigeria

- ABDULLAHI, Inuwa NJidda

- Aliyu, Sa’ad

- 2330-2346

- Apr 19, 2024

- Accounting

Comparative Study of the Effect of Personal Income Tax Amendment Act 2011 on Internally Generated Revenue of Adamawa State, Nigeria

ABDULLAHI, Inuwa NJidda and Aliyu, Sa’ad

Department of Accountancy, School of Administrative and Business Studies (SABS) Numan, Adamawa State Polytechnic

DOI: https://dx.doi.org/10.47772/IJRISS.2024.803163

Received: 27 February 2024; Revised: 09 March 2024; Accepted: 14 March 2024; Published: 19 April 2024

ABSTRACT

This study been anchor on the practical gap, it identified the poor level of internally generated revenue, as one of the banes that results in the inability of the various state governments in Nigeria to defray workers’ salaries and provide for other basic infrastructural and social needs of its citizens. In the light of this, the study sets its main objective of taking a comparative examination on the effect of personal income tax amendment Act 2011 on internally generated revenue of Adamawa state. Specifically, the study examined the effect of direct assessment; pay-as-you-earn, and other taxes on internally generated revenue of Adamawa state; and make comparism on the contribution of direct assessment, Pay-as-you-earn and other taxes on internally generated revenue of Adamawa State; The study employed quantitative methodological approach, which allows it to use archival and ex post facto designed to generates secondary data from the annual reports and the revenue statement of Adamawa state board of Internal revenue for a period from 2001-2022. The data collected were analysed using descriptive statistics, trend/performance analysis, regression analysis and paired t-test. The study found that PAYE, and Other Taxes Revenue have positive and significant effect on IGR of Adamawa State, while Direct Assessment have Negative and insignificant effect on IGR of Adamawa State. The study recommends that PITA 2011 should be fully implemented by Adamawa state government and that taxpayer education/awareness should be embarked upon by Adamawa State Board of Internal Revenue with respect to the benefits of complying with the new PITA regime. And equally adopt the use of E-taxation in the tax collection process.

Keywords: PITA 2011, Internally Generated Revenue, Personal Income tax. Paye, Direct Assessment, Other Taxes.

INTRODUCTION

The Main responsibility of every government all over the world is to ensure security, freedom and welfare of its citizen. To effectively carry out its primary function and other subsidiary functions, governments need adequate funding. Development of any nation depends on the amount of revenue generated and this led to the provision of infrastructural facilities and other services. The issue of domestic resource mobilization has attracted considerable attention in many developing countries coupled with un abating debt difficulties, domestic and external financial imbalances confronting them, it is not surprising that many developing nations have been forced to adopt stabilization and adjustment policies which demand better and more efficient methods of mobilizing domestic financial resources with the view to achieving financial stability and promoting economic growth (Kiabel & Nwokah, 2009). Nigerian economy being a monopolistic economy depending heavily on oil revenue for execution of its primary functions and other economic activities has seriously being affected by the volatility in price of oil in recent years, this led to a decrease in the funds available for distribution to the three tiers of government in Nigeria. Moreover, Internally Generated Revenue refers to those revenue sources that are generated solely within the bounds of the State and Local Governments.

Tax revenue is the income collected by governments through taxation. Unfortunately, in Nigeria the tax to GDP Ratio is nothing to write home about which stood at 6% lowest of all the sub-Saharan countries. This is a ratio of a nation’s tax revenue relative to its gross domestic product. Recent data from NBS indicates that Nigerian’s GDP stood at N173.5 trillion Naira Over (407 Billion U.S dollars) in the second quarter of 2021 (Q2 2021) while the total government collection in taxes was barely N 6.405 trillion in that quarter. Nigerian’s tax to GDP ratio remains one of the poorest in Africa the figure which stand at just 7% is significantly lower than Ghana and Egypt at 16% morocco 22% and South Africa 27% China 20.1% USA 26% (Tobi, 2018).

Statement of the Problem

The fall in the price of crude oil at the international market creates short-fall in the amount to be shared between the three tiers of government, including the government of Adamawa State. Most state governments relied heavily on the share of revenue from the Federation Account, thereby neglecting other internal sources of revenue generation available to them. Although Personal Income Tax has the potential of generating sufficient internal revenue to state governments if given the desired attention, but it seems not (Arowolo (2018). Adamawa State with a GDP of over $ 4 Billion its tax to GDP is nothing to write home about as it less than 5%, this is quite regrettable that despite all the series of amendments ensued by many governments on Personal Income Tax act, it still faces many limitations. The Economic Confidential in its annual State Viability Index (ASVI) for 2018 shows that 17 states of 36 states are insolvent as their IGR in 2018 were far below 10% of their receipts from the federation allocations (FAA)in the same year. These states include: AKwa Ibom, Ekiti, Ebonyi, and Bayelsa, Benue, Nasarawa, Gombe, Zamfara, Niger, Bauchi, Jigawa, Taraba, Adamawa, Borno, Katsina, Yobe and Kebbi. From the studies review, it is easier to draw policy implication from them. More so, the individual effect of the components of personal income tax such as Pay as You Earn (PAYE), Direct Assessment (DA), Other taxes (OT) was carried out but none have assessed the magnitude of response of Internally Generated Revenue (IGR) to the rate of change in Personal Income Tax Act 2011 and the resultant effect of the post-amended Act on Internally Generated Revenue of Adamawa State in the work reviewed to the best of my knowledge. This study is therefore carried out to fill all these gaps left opened and update the previous studies and fill the gap in literature.

Objective of the Research

The main objective of the study is to make comparism of the effect of Personal Income Tax Amendment Act 2011 on the internally generated revenue in Adamawa State. The specific objectives of the study are to:

- Examine the effect of direct assessment on Internally Generated Revenue of Adamawa State.

- Examine the effect of pay-as-you-earn on Internally Generated Revenue of Adamawa State.

- Examine the effect of other taxes on Internally Generated Revenue of Adamawa State.

- To make Comparism on the contribution of direct assessment, Pay-as-you-earn and other Taxes on Internally Generated Revenue of Adamawa State.

Hypotheses of the Study

- Direct assessment does not have significant effect on Internally Generated Revenue of Adamawa state.

- Pay-as-you-earn do not have significant effect on Internally Generated Revenue of Adamawa State.

- Other taxes do not have significant effect on Internally Generated Revenue of Adamawa State.

- Direct assessment, pay-as-you-earn and other taxes do not have significant effect on Internally Generated Revenue of Adamawa State.

Significance of the Study

This research will be of significance to Adamawa State Government, Board of Internal Revenue, other States in Nigeria, the general public and other researchers on areas related to the work. The findings of the research will help the State towards improving its internally generated revenue, to enable the provision of essential amenities which would improve the standard of living of the citizenry.

The remaining part of the paper is organized as follows section two provide a review of literature (covering a review of related studies) and the third section titled methodology, which presents the study‘s designs methods and techniques. Result and Discussion section four, and Conclusion and Recommendation in section five.

LITERATURE REVIEW

Conceptual Framework

Many scholars have defined tax in different ways. Asabor (2012) looked at tax as the mandatory contributions from business organizations and individuals for the purpose of financing the expenditure of government. This agrees with Justice Robert’s assertions, that it is an exaction of money from members of the public for the purpose of supporting government expenditure (Chris & Elizabeth, 2001).

Concept of Pay-as-you-earn

PAYE focuses on the income of individuals as a result of employment and the employee’s income are taxed using a graduated scale. The tax calculated is usually deducted at source and is done by the employer who will then remit the amount to the tax authorities. Mballos (2005), described PAYE as a tax system whereby the employee pays tax on whatever income he earned from his employment in any particular month at the end of that month.

Concept of Direct Assessment

Direct assessment tax, is a tax imposed on the income of an individual who engages in a self-employed venture. The payment of this tax, however, occurs after the individual has collected his/her gross income and filed in a return on the gross income. This category of income tax covers income from trade, business, profession, or vacation this is achieved through self-assessment by the tax payer (Mballos 2005).

Concept of other Taxes

These include various taxes Such as levies on market traders, land registration and other land related fees, development levies on individuals, pool betting/lottery/gaming fees, stamp duties on individuals. Capital Gains Tax of Individuals: Capital gains accruing to individual from the sale of a capital asset is payable to the state government. Stamp Duties on instruments executed by individuals, pools betting and lotteries, gaming and casino taxes, road taxes, business premises registration fee in respect (Oseni 2013).

Concept of Personal Income Tax

Personal income tax (PIT) which forms part of direct tax refers to all taxes or levies imposed on the income, salaries and wages, profit, gratuities, of individuals as well as interest and dividends from companies accruing to them. One of the major changes identified from the amendment of the new law expands the revenue base of the personal income tax by mandating the payment of tax by those earlier exempted for example, the official emoluments of the President, Vice President, Governors and Deputy Governors, also temporary staff such as casual workers, interns and other contract staff are now specifically liable to tax, and the non-formal sector is now properly structured.

Old and New Tax Rates

| OLD BANDS | OLD RATES | NEW BANDS | NEW RATES |

| First ₦30,000 | 5% | First ₦300,000 | 7% |

| Next ₦30,000 | 10% | Next ₦300,000 | 11% |

| Next ₦50,000 | 15% | Next ₦500,000 | 15% |

| Next ₦50,000 | 20% | Next ₦500,000 | 19% |

| Above ₦160,000 | 25% | Next ₦1,600,000 | 21% |

| Above ₦3,200,000 | 21% |

Source: PITA 2011

Challenges of Personal Income Tax

There are many problems encountered with the generation of personal Income tax revenue. Therefore, there is still a lot of dissatisfaction in the country over collection and assessment of personal Income tax. The assessment and collection of personal Income tax from taxable individuals have been difficult in Nigeria (Angahar &Sani, 2012). In Nigeria, it is safe to say that personal Income tax is mostly paid by civil servants (Formal sector) than Direct assessment (informal sector). This is because the taxes are deducted before the employees receive their pay.

Internally Generated Revenue

Internally Generated Revenue in normal day to day parlance refers to those revenue sources that are generated solely by the State and Local Governments from various sources such as (pay as you earn, direct assessment, capital gain taxes, withholding tax on individual, motor vehicle license), among others (Udeh 2015).

Review of previous Studies

Many studies have been conducted and tested as in Nassar and Taiwo (2006), carried out study on Effect of Personal Income Tax on Internally Generated Revenue Performance in Oyo State Nigeria. Secondary data sought from the approved budgets of Oyo state from years 2000-2006 was used for the study. They used stepwise regression technique to select the revenue source that has the greatest effect on Internally Generated Revenue (IGR) in the state. Their findings indicated that personal income taxes have systematic variation of 68.4% effect on IGR in Oyo state. Ogbonna and Ebimobowei (2012) examined the impact of tax reforms and economic growth of Nigeria using relevant descriptive statistics and econometric analysis. Their finding revealed that tax reforms is positively and significantly related to economic growth. The study also revealed that tax reforms improves on the revenue generating machinery of government to undertake socially desirable expenditures that will transform to economic growth in real output and per capita basis. In line with their study, if tax policies are stringent, it makes tax revenue to decline; therefore, there is need for constant reforms in the system. Samaila and Maimuna (2014), found out that PAYE does contribute significantly to the total IGR in Kano state. Its contribution to the IGR is 25% on average and 82% of the board of internal revenue collection which is quite significant. The study further revealed that direct assessment as a component of personal income tax does not contribute significantly to the IGR due to the loopholes and inefficiency in the tax system. Onyekwelu and Uguanyi (2014) carried out a study on the implication of PITA 2011 amendment Act on revenue generation in Nigeria, a case study of Enugu state. The responses elicited from their survey showed that the amendment has some positive influence on the tax system. Also,

Dabo, Aimuyedo and Tanko (2014) examined the effect of the amended personal income tax Act on revenue generation in Nigeria. The study revealed that PITA 2011 has not successfully encouraged tax payers to comply with self-assessment and compliance; stressing that the amendment has not succeeded in driving the force of change that will minimize the incidence of tax avoidance and evasion. Onyekwelu and Ugwuanyi (2014) Assessed Personal Income Tax Amendment Act 2011and its Effects on Revenue Generation in Nigeria. Their study exposed the possible challenges and prospects it poses to the Nigerian tax payers. The primary data was used for this study, using a structured questionnaire in conjunction with secondary data sourced from textbooks, academic journals and the internet. Their study reveals among other things that the increase in the tax rate affected the tax payers revenue generation, and the retroactive nature of our tax laws constitutes a major problem thus: resulting in double taxation during the assessment and collection of taxes. In another Study conducted, by Alpheaus, Ihendinihu & Azubike (2015) measured the effects of changes in Personal Income Tax Act on chargeable income of individual taxpayers in Nigeria. The main objective was to resolve speculations that chargeable income under the new Act is higher than previously existed among taxpayers of different income brackets. Data on income and domestic circumstances of sampled taxpayers in 2014 tax year were collected from Abia State Board of Internal Revenue. Results indicate that PITAM 2011 produces a significantly lower chargeable income than PITA 2004, and that this difference cuts across taxpayers in the identified income groups. The extensive literature reviewed indicated that the effect of personal income taxes on tax liability and tax burden have not been empirically investigated in Nigeria.

So also study conducted by Igyo e-tal (2016), who critically evaluated the contribution of Personal Income Tax on Internally Generated Revenue in Benue State. Their study specifically examined the effect of PIT sources on IGR of Benue state government. The research utilized secondary sources of data from the budget office of ministry of finance from 1999 to 2014. The data were analyzed using multiple regression The Augmented Dicky-fuller test ADF and diagnostic test were carried out to test for data stationarity, multicollinearity and serial correlation. Their findings show that PIT contributes significantly to IGR in Benue State and it is a genuine source through which the government deficits finances can be solved.

Theoretical Framework

Faculty Theory of Taxation

There are quite a number of theories underlining the concept of taxation, which have the objective of assisting in the systematic resolution of practical problems surrounding government financing through exercising the fiscal muscles of taxation. According to Anyafo (1996), this theory states that one should be taxed according to the ability to pay. Therefore, the theory that best explains or underpin the study is the faculty theory of taxation since the ability to pay of the tax payer is a key issue that is considered in both Pay-as-you –earn system direct assessment and other taxes and the theory is built on fairness and equity principles of taxation, which treats individuals with the same characteristics/circumstances.

Research Gap

The review revealed that tax is a compulsory levy imposed by the government through its agents and for which it is not bound to offer services or consideration that is commensurate to the tax paid by an individual taxpayer. More so, the individual effect of the components of personal income tax such as Pay as You Earn (PAYE), Direct Assessment (DA) and other taxes (OT) was carried out, but none have assessed the magnitude of the response of the amendment on Internally Generated Revenue (IGR) in the work reviewed to the best of my knowledge. This study is therefore carried out to fill these gaps opened in literature and update the previous studies.

RESEARCH METHODOLOGY

This section discusses the overall methodology the study adopted in achieving its set objectives in line with research objective and hypotheses formulated earlier. It adopted a positivism paradigm which is based on values of reasons and validity and it focuses on facts garnered from theories which can be measured empirically using quantitative method. The researcher adopted Archival and ex post facto research design using time series data over a period of twenty two (22) years (2001-2022) the choices of the period was to enable the researchers to assess the effect of PITA 2011 amendment Act on the internally generated revenue of Adamawa state and to explain the interrelationship between the study variables while the methodology was mixed as data were collected for facts investigations.

Data were sourced through secondary source from the Revenue Statement of Board of Internal Revenue and Reports of the Accountant General Adamawa State for the period under review (2001-2022). Data were analyzed using Trend/performance analysis, regression analysis, paired t-test, and STATA 13. Some statistical tests carried out include Normality Test, Reliability Test and Ordinal Regression. The study resorted to the Ordinal Regression upon discovering that that our data were not normally distributed.

The research was evaluated using the following model specification adopted by Haruna, Kumshe, Magaji and Bani (2014) with some modification. The variables in this study include the internally generated revenue as the dependent variable. While the independent variable is Personal Income Tax, further broken down to pay as you earn, direct assessment and Other taxes.

The model is expressed as thus:

Revenue Generation =f (Personal Income Tax Amendment Act 2011)

IGRt = αt + β1PAYEt+ β2DAt+β3OTt+et

Log IGR = Logα + Logβ1PAYE+ Logβ2DA+Logβ3OT+Loge

Where:

IGR = Internally Generated Revenue

PAYE = Pay-As-You-Earn

DA = Direct Assessment

OT = Other taxes

β1β2 β3 = are regression coefficient

α = is a constant (intercept)

e = is the error term

t= is the time

The error term is captured because there are other factors that affect IGR which are not included in the models.

Variables and Measurements: Independent Variables: PITA 2011 Measures

| Variable | Measure | Symbol | Source |

| Paye | Natural Log of Actual PAYE Collected (Archive record of Adamawa State Board of Internal Revenue) | PAYE | Muhammad T. (2015), Igyo, Jatau & Ashami (2016), Samuel Y & Gabriel O, (2016). |

| Direct Assessment | Natural Log of Actual Direct Assessment Collected (Archive record of Adamawa State Board of Internal Revenue) | DA | Muhammad T. (2015),Igyo, Jatau & Ashami (2016), Samuel Y & Gabriel O, (2016). |

| Other Taxes Revenue | Natural Log of Actual Other Taxes Collected

(Archive record of Adamawa State Board of Internal Revenue) |

OT | Muhammad T. (2015), Igyo, Jatau & Ashami (2016), Samuel Y & Gabriel O, (2016). |

Dependent Variable: Internally Generated Revenue (IGR) Measures

| Variable | Measure | Symbol | Source |

| Internally Generated Revenue | Natural Log of Actual Internally Generated

Revenue Collected. (Archive record of Adamawa State Board of Internal Revenue) |

IGR | Agu (2010), Nnanseh and Akpan (2013) Samuel Y & Gabriel O, (2016). |

RESULTS AND DISCUSSIONS

This section is devoted for the presentation, analysis and interpretation of data used in the study. The data relating to each of the statistical hypotheses of the study were presented and analyzed, using regression models. It starts with the robustness tests, descriptive statistics, correlation matrix, trend/Performance analysis, regression analysis and paired t-test of the dependent and the independent variables of the study. It also shows the results obtained from the test of hypotheses formulated for the study.

Table 4.1 Descriptive Statistic and Normality test of residuals

| Variables | Obs | Mean | Std.Dev. | Min | Max | Skewness | Kurtosis | Prob>chi2 |

| IGR | 22 | 9.536616 | .4693979 | 8.486629 | 10.11978 | 0.0171 | 0.3639 | 0.0489 |

| PAYE | 22 | 9.253119 | .5086164 | 8.257238 | 9.912961 | 0.0623 | 0.9285 | 0.1486 |

| DA | 22 | 8.002899 | .5020383 | 6.77389 | 8.566803 | 0.0263 | 0.2102 | 0.0490 |

| OT | 22 | 8.593113 | .8105812 | 5.458437 | 9.322676 | 0.0000 | 0.0001 | 0.0000 |

Source: Author’s compilation 2023 Stata 13

The descriptive statistics is presented on Table 4.1 showing the mean, standard deviation, minimum and maximum of the variables. All the variables have been converted from their logarithms. From Table 4.3 IGR recorded a mean value of (9.536616) and Standard deviation of (.4693979) implying that average IGR collection for the period is five billion, seventeen million four hundred and forty nine thousand, seven and forty six naira six kobo (N5,017,449,746.06). It also recorded a minimum value of (8.486629) implying a minimum amount of Three hundred and six million, six hundred and forty thousand, six hundred and ninety seven naira sixty six kobo (N306,640,697.66) and a maximum value of (10.11978) implying a maximum amount of Thirteen billion, one hundred and seventy five million, seven hundred and seventy four thousand, nine hundred and sixty nine naira fifty three kobo (N13,175,774,969.53) for the study period. This result also indicates a low variation of IGR collection as depicted by the value of standard deviation of Three billion, five hundred and forty six million, seven hundred and forty four thousand, three hundred and twenty seven naira thirty six kobo (N3,546,744,327.36) which is lower than the mean value.

PAYE recorded a mean value of (9.253119) implying that average PAYE collection for the period is two billion, eight hundred and forty one million, six hundred and sixty thousand, three hundred and thirteen naira seventy six kobo (N2,841,660,313.76). It also recorded a minimum value of (8.257238) implying a minimum amount of One hundred and eighty million, eight hundred and sixteen thousand, six hundred and twenty seven naira thirteen kobo (N180,816,627.13) and a maximum value of (9.912961) implying a maximum amount of Eight billion, One hundred and Eighty Three million, Nine Hundred and four thousand, Eighty four naira fifty six kobo (N8,183,904,084.56) for the study period. This result also indicates a lower variation of PAYE collection as depicted by the value of standard deviation of Two billion, two hundred and sixty-three million, four hundred and three thousand fifteen naira (N2,263,403,015) which is lower than the mean value.

Direct assessment recorded a mean value of (8.002899) implying that average direct assessment collection for the period is One hundred and Fifty six million, seven hundred and nine thousand, one hundred and forty three naira thirty six kobo (N156,709,143.36). It also recorded a minimum value of (6.77389) implying a minimum amount of Five million, Nine hundred and Forty-One thousand, Three hundred and Seventy-naira seventeen kobo (N5,941,370.17) and a maximum value of (8.566803) implying a maximum amount of Three hundred and Sixty-Eight million, Eight hundred and Ten fourteen thousand, Five hundred and Six-naira fifty-seven kobo (N368,810,506.57) for the study period. This result also indicates a lower variation of direct assessment as depicted by the value of standard deviation of One Hundred and Twenty million, eight hundred thousand, one hundred and Thirty-Eight naira Twenty-one kobo(N120,800,138.21) which is lower than the mean value.

Other Taxes recorded a mean value of (8.593113) implying that average of Other taxes collected for the period is Seven hundred and Forty Seven million, Nine hundred and Twenty Three thousand, Two hundred and forty One naira Twenty one Kobo (N747,923,241.21). It also recorded a minimum value of (5.458437) implying a minimum amount of Two hundred and Eighty-Seven thousand, three hundred and Sixty-seven naira four kobo (N287,367.04) and a maximum value of (9.322676) implying a maximum amount of Two billion One hundred and Two million, two hundred and Nine thousand and Four Hundred and Fifteen naira sixty four kobo (N2,102,209,415.64) for the study period. This result also indicates a higher variation in other taxes assessment as depicted by the value of standard deviation of Five hundred and Sixty-Seven million, seven hundred and Fifty eight thousand, Seven hundred and Ninety Three naira seventy one Koo (N567,758,793.71) which is higher than the mean value. The variation is as a result of the PITA 2011 Amendment which give room for the widening of the tax net.

Normality implies that errors (residuals) should be normally distributed and this can be tested using Skewness and Kurtosis tests for normality. The results show that Pay as you earn PAYE is normally distributed because its Prob>chi2 values of 0.1486 are greater than 5%, while, Internally Generated Revenue, Direct Assessment and Other taxes are not normally distributed because their Prob>chi2 values of 0.0489, 0.0490 and 0.0000 are less than 5% respectively (See Appendix VI).

Table 4.1.2 Correlation Matrix, Multicollinearity and Heteroskedasticity Test

| IGR | PAYE | DA | OT | VIF | heteroskedasticity | |

| Prob > chi2 = 0.0487 | ||||||

| IGR | 1.0000 | |||||

| PAYE | 0.9645 | 1.0000 | 2.17 | |||

| DA | 0.6004 | 0.6446 | 1.0000 | 1.71 | ||

| OT | 0.6567 | 0.5694 | 0.3758 | 1.0000 | 1.48 |

Source: Author’s compilation 2023 Stata 13

Table 4.1.2 shows the correlation values between the dependent and independent variables and also the relation among the independent variables. The correlation coefficients on the main diagonal are 1.0, because each variable has a perfect positive linear relationship with itself. As shown on Table 4.2 the relationship between PAYE, Direct Assessment and Other Taxes revenue with IGR are strong and positive with correlation coefficient values of 0.9645, 0.6004, and 0.6567 respectively. PAYE was found to be Strong and Moderately correlated with all the other explanatory variables with correlation coefficient values of 0.6446 and 0.5694 for Direct Assessment and Other taxes revenue respectively. Finally, Direct Assessment is found to have a weak but positively relationship with Other taxes with correlation coefficient value of 0.3758. Multicollinearity test was carried out to check whether there is high correlation between independent variables which will mislead the result of the study. The Variance Inflation Factor (VIF) was used to test for multicollinearity. The VIF of all the variables were found to be consistently smaller than ten (10) (Appendix IV). This indicates that multicolinearity was not a problem (Tobachnick & Fidell, 1996). Heteroskedasticity test is useful in determining whether or not the variability of error terms is constant or not. The Breusch-pagan/Cook-weisberg test for heteroskedasticity was carried out and the result reveals that pooled OLS estimators have the minimum variance of all unbiased estimators, and also the P-value will be reliable. This is evidenced by the insignificant Prob > chi2 = 0.0487 (Appendix V).

Table 4.1.3 Total Pit as a Percentage of Internallay Generated Revenue

| YEAR | IGR(N) | PIT(N) | % OF PIT TO (IGR) |

| 2001 | 342,455,678.73 | 278,845,081.75 | 81 |

| 2002 | 496,545,994.93 | 291,512,691.82 | 59 |

| 2003 | 306,640,697.66 | 282,319,492.22 | 92 |

| 2004 | 783,759,044.61 | 568,665,851.59 | 73 |

| 2005 | 3,555,814,620.72 | 2,166,916,166.73 | 61 |

| 2006 | 4,838,210,897.17 | 3,006,293,221.53 | 62 |

| 2007 | 2,083,151,098.40 | 1,460,573,927.87 | 70 |

| 2008 | 3,909,198,796.54 | 2,563,038,125.44 | 66 |

| 2009 | 3,128,368,184.46 | 2,968,192,574.05 | 95 |

| 2010 | 4,458,673,408.48 | 4,208,037,781.45 | 94 |

| 2011 | 4,916,830,839.26 | 4,117,975,681.45 | 84 |

| 2012 | 5,099,594,516.81 | 4,615,407,803.09 | 91 |

| 2013 | 4,482,158,314.83 | 4,149,550,775.70 | 93 |

| 2014 | 4,645,824,257.97 | 4,580,416,905.78 | 99 |

| 2015 | 4,666,739,288.11 | 4,451,736,117.84 | 95 |

| 2016 | 6,379,819,412.87 | 5,268,721,522.43 | 83 |

| 2017 | 6,044,493,705.80 | 3,882,177,482.98 | 64 |

| 2018 | 6,613,764,897.92 | 4,383,706,619.35 | 66 |

| 2019 | 9,704,650,185.42 | 6,109,562,879.78 | 63 |

| 2020 | 7,739,814,375.08 | 5,894,466,459.65 | 76 |

| 2021 | 13,011,611,228.12 | 8,424,493,083.27 | 65 |

| 2022 | 13,175,774,969.53 | 8,745,829,117.59 | 66 |

Source: Adamawa State Accountant General Report and ASBIR Statement 2001-2022

Table 4.1.3 shows that personal income tax contributes 59% to the internally generated revenue of Adamawa state in 2002 which is the least in the period under review, the figure rose to 99% in 2014 this sharp increase is a result of increase in PIT from 278,845,081.75 in 2001 to 4,580,416,905.78 in 2014. This sharp increase from 59% to 99% was as a result of increase in PIT collection following the implementation of PITA 2011. The decrease from 99% in 2014 to 83% in 2016 this is due to the electioneering period were attention is mostly given to political issues rather than economic issues. The figure decreases to 64% due to increase in IGR from other source rather than PIT. This increase continues to the extent of attaining 76% in 2020 and drop to 66% in 2022 and still good enough as a contributor to the internally generated revenue. This shows that personal income tax contributes an average 77 % to the internally generated revenue of Adamawa state.

Table 4.1.4 Comparative Performance Evaluation Based On Trend/Ratio Analysis

| YEAR | IGR(N)000,000 | PAYE(N)000,000 | % OF PAYE TO IGR | DA(N)000,000 | % OF DA TO IGR | OT(N)000,000 | % OF OT TO IGR |

| 2001 | 342,455,678.73 | 191,161,260.41 | 56 | 87,396,454.30 | 26 | 287,367.04 | 0.1 |

| 2002 | 496,545,994.93 | 180,816,627.13 | 36 | 6,904,677.04 | 1 | 103,791,387.65 | 21 |

| 2003 | 306,640,697.66 | 183,941,584.19 | 60 | 5,941,370.17 | 2 | 92,436,537.86 | 30 |

| 2004 | 783,759,044.61 | 385,207,160.28 | 49 | 76,827,654.27 | 10 | 106,631,037.04 | 14 |

| 2005 | 3,555,814,620.72 | 1,088,425,194.66 | 31 | 45,813,750.12 | 1 | 1,032,677,221.95 | 29 |

| 2006 | 4,838,210,897.17 | 855,271,560.61 | 18 | 48,812,245.28 | 1 | 2,102,209,415.64 | 43 |

| 2007 | 2,083,151,098.40 | 968,704,209.61 | 47 | 68,947,365.00 | 3 | 422,922,353.26 | 20 |

| 2008 | 3,909,198,796.54 | 1,665,974,781.54 | 43 | 179,412,668.78 | 5 | 717,650,675.12 | 18 |

| 2009 | 3,128,368,184.46 | 2,039,325,173.13 | 65 | 105,773,480.18 | 3 | 823,093,920.73 | 26 |

| 2010 | 4,458,673,408.48 | 2,735,224,557.94 | 61 | 294,562,644.70 | 7 | 1,178,250,578.81 | 26 |

| 2011 | 4,916,830,839.26 | 2,676,684,192.94 | 54 | 288,258,297.70 | 6 | 1,153,033,190.81 | 23 |

| 2012 | 5,099,594,516.81 | 3,000,015,072.01 | 59 | 323,078,546.22 | 6 | 1,292,314,184.87 | 25 |

| 2013 | 4,482,158,314.83 | 2,697,208,004.21 | 60 | 290,468,554.30 | 6 | 1,161,874,217.20 | 26 |

| 2014 | 4,645,824,257.97 | 3,042,270,988.76 | 65 | 327,629,183.40 | 7 | 1,210,516,733.62 | 26 |

| 2015 | 4,666,739,288.11 | 2,893,628,476.60 | 62 | 311,621,528.25 | 7 | 1,246,486,113.00 | 27 |

| 2016 | 6,379,819,412.87 | 3,424,668,989.58 | 54 | 368,810,506.57 | 6 | 1,475,242,026.28 | 23 |

| 2017 | 6,044,493,705.80 | 3,516,923,822.72 | 58 | 33,162,524.80 | 1 | 332,091,135.46 | 5 |

| 2018 | 6,613,764,897.92 | 4,011,726,920.18 | 61 | 90,597,288.31 | 1 | 281,382,410.86 | 4 |

| 2019 | 9,704,650,185.42 | 5,763,355,874.97 | 59 | 118,856,369.70 | 1 | 227,350,635.11 | 2 |

| 2020 | 7,739,814,375.08 | 5,610,830,677.17 | 72 | 60,082,278.46 | 1 | 223,553,504.02 | 3 |

| 2021 | 13,011,611,228.12 | 7,401,257,689.59 | 57 | 108,054,805.52 | 1 | 915,180,588.16 | 7 |

| 2022 | 13,175,774,969.53 | 8,183,904,084.56 | 62 | 206,588,960.95 | 2 | 355,336,072.08 | 3 |

Source: Author’s compilation 2023

The table 4.1.4 above shows the individual Contribution of Pay As You Earn Direct Assessment and other taxes on the total IGR of Adamawa States. Direct assessment contributed an average of 5% percent of the total revenue generated for the period under review, despite the large number of people in business, trade, and vocations in Adamawa State. This implies that either tax evasion/avoidance has eaten deep into the fabrics of our system or that the tax administration is poor, this attest to the fact that in spite of the amendment of Personal Income Tax (PIT) Act 2011 which was aimed at increasing revenue generation, it does not affect positively on tax evasion, nor tax avoidance neither does it improve revenue generation in Adamawa State from the findings. This indicates weak effort on the part of the revenue collectors in the states in assessing and collecting revenue from internal sources. However, the Pay as You Earn, has some reasonable contribution as its contributes an average of 54% Percent toward the Internally Generated Revenue, the other taxes also plays significant role as its contributed an average of 18% Percent to the Internally Generated Revenue during the period under review.

The results presented in tables 4.1.3 and 4.1.4 provides the basis for the rejection of the null hypothesis (Ho2 Ho3) of the study, which state that Pay-as-you-earn does not have significant effect on Internally Generated Revenue in Adamawa State, Other taxes does not have significant effect on Internally Generated Revenue in Adamawa State, this lead to the acceptance of the alternative hypothesis which states otherwise. And equally fail to reject the null hypothesis (H01) which states that Direct assessment does not have significant effect on Internally Generated Revenue in Adamawa state.

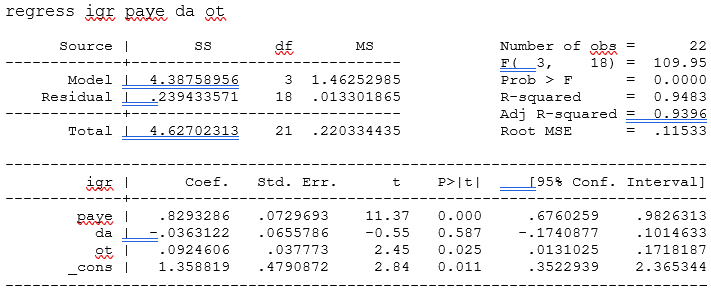

Table 4.1.5 Regression Results

| SS | df | MS | Number of obs = 22 | ||

| F(3, 18) = 109.95 | |||||

| 4.38758956 | 3 | 1.46252985 | Prob > F = 0.0000 | ||

| .239433571 | 18 | .013301865 | R-squared = 0.9483 | ||

| Adj R-squared = 0.9396 | |||||

| 4.62702313 | 21 | .220334435 | Root MSE = .11533 | ||

| Coef. | Std. | Err. | t | P>|t| | [95% Conf.Interval] |

| .8293286 | .0729693 | 11.37 | 0.000 | .6760259 | .9826313 |

| -.0363122 | .0655786 | -0.55 | 0.587 | -.1740877 | .1014633 |

| .0924606 | .037773 | 2.45 | 0.025 | .0131025 | .1718187 |

| 1.358819 | .4790872 | 2.84 | 0.011 | .3522939 | 2.365344 |

Source: Author’s compilation 2023 Stata 13 Note: *, **, and *** for the significance level @10%, 5% and 1% respectively.

This section explains the effect of all the independent variables (PAYE, Direct Assessment and Other Taxes revenue) on the dependent variable (IGR). The results were presented on Table 4.1.5 The regression results show the value of the overall R2 as 0.95 which is the multiple coefficient of determination that gives the proportion or percentage of the total variation in the dependent variable explained by the explanatory variables jointly. Hence, it signifies that approximately 95% of total variation in IGR is caused by PAYE, Direct Assessment and Other Taxes revenue. The Table also shows the F-statistics values of 109.95 with the corresponding P-value of 0.0000. This implies that the explanatory variables reliably predict the dependent variable of the study. PAYE, and Other Taxes Revenue have positive and significant effect on IGR with the following coefficients and t-values (ceff=0.829, t=11.37, p<.01), and (ceff=0.092, t=2.45, p<.05) respectively. While Direct Assessment have Negative and insignificant effect on IGR with the coefficient and t-value of ( ceff= -0.036, t = -0.55, p>.05). The positive effect of PAYE on IGR implies that for every increase in PAYE by N1, the IGR of the state will increase by 83 kobo. The positive effect of Other taxes revenue on IGR implies that for every increase in Other taxes revenue by N1, the IGR of the state will increase by 92 kobo. The Negative effect of Direct Assessment on IGR implies that for every Increase in Direct Assessment by N1, the IGR of the state will decrease by 4 kobo.

Test of Hypotheses

From the analysis in respect of all the variables, the null hypothesis one (1) of the study which states Direct assessment does not have significant effect on Internally Generated Revenue of Adamawa state is tested. The regression results in Table 4.1.5, shows that Direct Assessment has Negative and insignificant effect on IGR with the coefficient and t-value of ( ceff= -0.036, t = -0.55, p>.05) at more than 5% level of significant, thus, based on this we fail to reject the null hypothesis one (1) of the study. This implies that Direct Assessment has insignificant negative effect on IGR of Adamawa state. This finding is inconsistent with the findings Onyekwelu and Uguanyi (2014) Igyo e-tal (2016), who found significant Positive relationship between PIT and IGR, and It is however consistent with the findings of Dabo, Aimuyedo and Tanko (2014) who concluded that the PIT laws have not successfully encouraged tax payers to voluntarily comply with self-assessment and compliance and hence, not improve the revenue generation of the state.

In addition, the null hypothesis two (2) of the study which states that PAYE does not have significant effect on IGR of Adamawa state is tested. The regression results in Table 4.1.5, shows that PAYE has significant positive effect on IGR of Adamawa state at 1% level of significant with (ceff=0.829, t=11.37, p<.01), thus, based on this the null hypothesis two (2) is rejected. This implies that PAYE has significant positive effect on IGR of Adamawa state. This finding is consistent with the findings of Onyekwelu and Uguanyi (2014) and Igyo e-tal (2016), who found that PIT has a significant Positive Contribution to the IGR and Contradict that of Dabo,Aimuyedo and Tanko (2014).

Furthermore, the null hypothesis three (3) of the study which states that Other Taxes does not have significant effect on IGR of Adamawa state is tested. The regression results in Table 4.1.5, shows that Other taxes revenue has significant positive effect on IGR of Adamawa state at 5% level of significant (ceff=0.092, t=2.45, p<.05), thus, based on this the null hypothesis three is rejected. This implies that Other taxes revenue has significant positive effect on IGR of Adamawa state. This finding is consistent with the findings of Onyekwelu and Uguanyi (2014), Igyo e-tal (2016) and Samaila and Maimuna (2014) who found that PIT has a significant Positive Contribution to the IGR respectively and contradict that of Dabo,Aimuyedo and Tanko (2014).

The Pre and Post PITA 2011 IGR of Adamawa State-Nigeria

This section presents the test results of the paired sample test made to compare the IGR of Adamawa state-Nigeria between the pre-PITA 2011 and post PITA 2011 periods. The Paired-Samples test procedure compares the means of the variable that represent the IGR of same group at different times (That is before and after the PITA 2011). This section analyses how PITA 2011 affects overall IGR of Adamawa state and which is presented and the mean values for the two periods are shown in table 4.3.1

Table 4.3.1 Paired t test

| Mean | Obs | Std Deviation | Std Error Mean | |

| Pair 1 Pre-PITA 2011 IGR | 9.23582 | 11 | .4839189 | .145907 |

| Post PITA 2011 IGR | 9.837412 | 11 | .1716749 | .1763639 |

Source: Generated by the Author from ASBIR Annual Revenue Statement using Stata 13

The Paired Samples t-test provide for comparism of the means for the two periods, it is important to know what the mean values and All the variables have been converted from their logarithms. The results from table 4.3.1 show a mean of 9.23582 implying the mean value of Two Billion Six Hundred and Nineteen Million Nine Hundred and Sixty-Eight Thousand One Hundred and Fourteen Naira Sixty-Three Kobo (N 2,619,968,114.63) for Adamawa State before PITA 2011. This figure is lower than the mean value of 9.837412 implying the mean value of Seven Billion Four Hundred and Fourteen Million Nine Hundred and Thirty-One Thousand Three Hundred and Seventy-Seven Naira Fifty Kobo (N 7,414,931,377.50) after the PITA 2011 which implies that the average ADSBIR PIT collection has improved after the PITA 2011 amendment. The increase in mean revenue can be attributed not only to increase in personal income taxes as a result of economic and policy changes, but also other taxes that constitute the ADSBIR revenue.

CONCLUSION AND RECOMMENDATIONS

Based on the results and data collected from both primary and secondary source, the following findings were made and conclusion reached.

- There is significant positive improvement in the IGR of Adamawa state after the amendment of PITA in 2011.

- Poor information furnished by the tax payers, inadequate staff and working facilities, politics, corruption and lack of tax payers’ identification are the major problems militating against revenue generation in Adamawa State.

- PAYE contribution to the IGR is significant and its collection is effective for the period under review in view of the fact that it was deducted at source. The major component of IGR in Adamawa State are taxes particularly PAYE which contributes on the average about 51% to IGR of Adamawa State.

- Though PAYE have contributed significantly to the IGR, the contribution of direct assessment which is also a component of PIT to the IGR which is Negative and insignificant and the collection is ineffective during the period of the study (2001-2022). The average contribution of direct assessment to IGR is 5% of the Adamawa State. This is due to some loopholes in the area of assessment and collection of those taxes. Thus, effective collection of tax through direct assessment is essential for the improvement of PIT of Adamawa State.

- Other Taxes Revenue on the other hand play significant role toward the enhancement of the Internally Generated Revenue of Adamawa State as it’s contributed an average of 26%, to the IGR which is quite impressive.

On the basis of the findings and conclusions, it is recommended that:

- PITA 2011 should be fully implemented by Adamawa state and that taxpayer education/awareness should be embarked upon by Adamawa State Board of Internal Revenue with respect to the benefits of complying with the new PITA regime.

- There should be political will on the part of the government and the government should be up and doing. The issue of tax should be taken very serious and anybody liable to pay tax must be made to pay the tax. Similarly, any tax official found wanting should be severely punished by making him to refund the monies he/she has taken together with penalties and or jailed. Adequate working facilities like computers, office accessories, motor cycles and motor vehicles should be provided by the government to enhance effective tax administration.

- Adamawa State board of internal revenue whose jurisdiction it is to collect the Personal Income Tax should widen its tax base to include the informal sector that has not been captured into the tax net,

- Adamawa State Government should adopt the use of E-taxation and the tax system should be automated so as not to give room for tax evasion/avoidance and equally address issue of fraud on the part of tax officials.

REFERENCES

- Adam, R. A. (2006). Public sector accounting and finance: Lagos, corporate publishers ventures, 2nd Edition.

- Angahar, P. A. & Alfred, S. I. (2012). Personal income tax administration in Nigeria: challenges and prospects for increased revenue generation from self-employed persons in the society. Global Business and Economics Research Journal, 1(1): 1-11.

- Anyafo, A.M.O. (1996), Public Finance in a developing economy, the Nigerian Case. Enugu University of Nigeria press.

- Alpheaus, O. E, Ihendinihu J. U. & Azubike J. U. (2015). Effects of Changes in Personal Income Tax Act on Taxable Income of Individual Taxpayers in Nigeria. Journal of Sustainable Social and Management Sciences. Michael Okpara University of Agriculture, Umudike, (1)(1).

- Arowolo O. (2018): Tax conference theme: understanding tax and its effect on Nigeria businesses by NACCIMA in partnership with Lagos internal revenue service in Lagos.

- Asabor, M. (2012). Personal income tax amendment act and its effects on tax payers. http://www.tribune.com.ng/Index.php/taxation/39566-PersonalIncomeaccessed7.57am 14/3/2013

- Central Bank Of Nigeria CBN (2007). Annual report and statistical bulletin

- Chris, W.H. & Elizabeth, S.B. (2001). Revenue law, principles and practice in Nigeria. (8th ed.). London: Butter Worths Publishers.

- Dabo, Z; Aimuyedo, M. & Muhammad, T. (2014). The Effect of Personal Income Tax (Amendment) Act on Revenue Generation in Nigeria. Social Science Research Network. Available at http://ssrn.com/abstract=2488098 or http://dx.dol.org/102139/ssrn.2488098

- Haruna, A. D. Kumshe, H. M. Magaji, B. Y. & Bani, L. M. (2015). Value Added Tax (VAT) and Its Impact on Growth of Adamawa State. European Journal of Business and Management. 30(7): 2222-2839

- Igyo A, J., Jatau S. &Ashami Philip I. (2016) Beyond Statutory Federal Allocation: A Critical Evaluation of the Contribution of Personal Income Tax on Internally Generated Revenue of Benue State British Journal of Economics, Management & Trade13(3): 1-13.

- Jimoh, B. (2007). Public sector accounting and finance. Lagos: Magic Plus Publishers.

- Kiabel, B. D., &Nwokah N. G. (2009). Curbing tax evasion and avoidance in personal income tax administration: A study of the south-south states of Nigeria. European J. Econs. Fin. Admin. Sci., 15: 16-61.

- Krejcie, R.V., & Morgan, D. W. (1970). Determining sample size for research activities Educational and Psychological Measurement,30, 607-610.

- Nassar, M.I &Taiwo F.H. (2006) Effectof Personal Income Tax on Internally Generated Revenue Performance in Oyo State, International Journal of African Culture and Ideas vol 5(1): January 2006.

- Mballos, O. O (2005). PIT ‘Returns & processing’, A paper presented at a workshop organised by FIRS, Abuja (unpublished)

- Ogbonna, G.N, and Appah, E (2012). Impact of petroleum revenue and the economy of Nigeria. Current Research Journal of Economic Theory 4(2):11–17.

- Onyekwelu, U.L. &Ugwuanyi, U.B. (2014). Assessing personal income tax amendment Act 2011: Effects on revenue generation in Nigeria. International Journal of Economics and Finance, 6(9), 199-212.

- Oseni, M. (2013). Internally Generated Revenue (IGR) in Nigeria: A Panacea for State Development. European Journal of Humanities and Social Sciences, 12(1).

- Ososami, L. (2003). A closer look at taxation as a Tool for revenue generation and promotion of Investment in Nigeria.

- Personal Income Tax Act, CAP P8 Laws of the Federation of Nigeria (2004).Official Gazette of the Relationship between Tax Revenue and Economic Growth in Nigeria: 1986 to 2012.The SIJ Transactions Retrieved from http://www. Bjournal.co.uk/payers/on 3/01/2018.

- Samaila I.A, & Maimuna A. S (2014). Effect of personal income tax act 2011 on the internally generated revenue of Kano State-NigeriaPaper Presented at the M. Sc Seminar. Department of Accounting, Bayero University Kano.

- Sosanya, S.O. (1996). Economics of taxation as a source of revenue generation, The National accountant, 6(1)

- Tobi A. (2018): Tax Conference themed understanding tax and its effect on Nigeria businesses by NACCIMA in partnership with Lagos internal revenue service in Lagos.

- Udeh J. (2015): Petroleum Revenue management-The Nigeria perspective-World bank Petroleum Revenue Management Workshop 2002.

APPENDIX

APPENDIX I

APPENDIX II

APPENDIX III

APPENDIX IV

APPENDIX V

estat hettest

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

Ho: Constant variance

Variables: fitted values of igr

chi2(1) = 3.89

Prob > chi2 = 0.0487

APPENDIX VI

APPENDIX VII

Pre Amendment 2011 Paired t test

Post Amendment 2011 Paired t test