Determinants of Crop Insurance Uptake by Tobacco Farmers in Zimbabwe

- Lawrence Dumisani Nyathi

- Nothando Tshuma

- 1037-1049

- Jul 5, 2024

- Agriculture

Determinants of Crop Insurance Uptake by Tobacco Farmers in Zimbabwe

Lawrence Dumisani Nyathi, Nothando Tshuma

National University of Science and Technology, PO Box AC 939, Ascot, Bulawayo, Zimbabwe.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.806079

Received: 15 May 2024; Accepted: 01 June 2024; Published: 05 July 2024

ABSTRACT

Agriculture serves as the cornerstone of Zimbabwe’s economy, supplying more than 60% of the raw materials needed by various industries. Additionally, it constitutes 40% of the country’s total exports, making it the primary contributor to export revenue. Notably, tobacco accounts for 50% of these exports, solidifying its position as the largest contributor within the agricultural sector. The remarkable growth in tobacco production can be attributed to small-scale producers who gained empowerment through the Fast Track Land Reform Program (FTLRP).

Despite the prosperity and expansion observed in tobacco production, an inherent risk persists, particularly among new farmers. The absence of safety nets to cushion against adverse events poses a significant challenge in this critical sector. Consequently, this study aims to examine the factors influencing crop insurance adoption by tobacco farmers. We employed a concise and validated closed-ended questionnaire, collecting data from 121 farmers. Subsequently, we conducted an econometric analysis using a logistic model in STATA V 11 to explore the determinants of crop insurance uptake.

The research findings indicate that several factors significantly influence the uptake of crop insurance among tobacco farmers. These factors include tobacco farming experience, level of education (measured in school years), frequency of extension officer visits, and the farmer’s income. Despite these influential factors, the adoption of tobacco insurance remains low, with a considerable number of tobacco farmers unaware of the insurance schemes offered by insurance companies.

In summary, the study underscores the pivotal role of tobacco as a major contributor to foreign currency and employment in Zimbabwe. Recognizing the economic significance of tobacco exports, the paper recommends that Zimbabwean tobacco farmers embrace more formal risk management strategies, such as agricultural insurance, to safeguard and consolidate the gains they have achieved thus far.

Keywords: crop insurance, tobacco, agriculture, farmers, Zimbabwe

INTRODUCTION

Agriculture is regarded as the backbone of Zimbabwe’s economy, creating employment for 70% of the population as well as contributing 33.9 % GDP (Ministry of Foreign Affairs & international Trade, 2024). The agricultural sector also provides about 60% of the raw materials for the manufacturing industries and contributes 45% of the exports from various crops such as flowers, cotton, fruits, and vegetables.50% is contributed by tobacco making it the biggest contributor in exports and revenue in agriculture (GoZ, 2023; TIMB, 2023). Furthermore, Makamure et al (2001) also alludes that tobacco peaked by 78 percent to the value of agriculture exports as early as 1992. FAO (2003) weighs that the flue-cured tobacco generates around USD132.00 per hectare in government revenue making it an important source of government revenue in 2001.

Takawira (2013) mentions that tobacco production in 2013 was 20 percent more than production in 2012 that is it rose from 129 million to 155.9 million kilograms. Moreso, in 2014 tobacco production increased as the sector registered 20 000 new farms as compared with the previous period. Small-scale producers account for 75 percent of the tobacco produced which rakes in over USD 300 million annually which is the biggest contribution in the agricultural purse (The Sunday Mail, 2015). In this farming season Zimbabwe recorded the highest tobacco production in its history reaching 261 million kilograms surpassing the previous record of 259 million kilograms this is against the backdrop of the fact that 85% of the tobacco is being produced by smallholder farmers (Reuters, 2023). The total value of tobacco sold raked USD 696, 7 million up from US$445.4 million the previous year (The Herald, 01 June 2023).

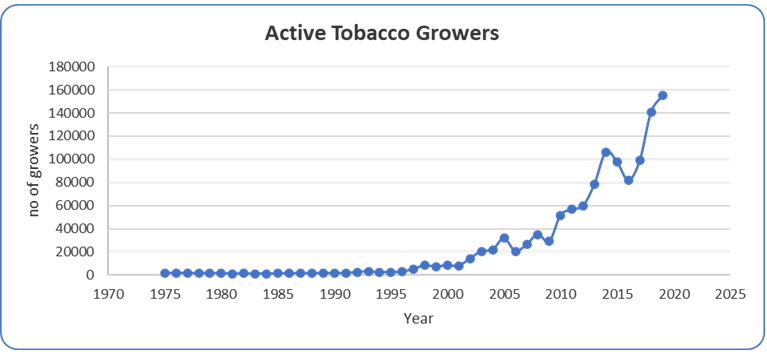

According to the Tobacco Industry and Marketing Board (TIMB, 2023) sales increased 54.72 percent from the same period in 2022. The number of farmers involved in tobacco has grown exponentially over the years and have increased by 5 171.2% from 1980 to 2013, and has grown by 325% from 2006 to 2013 to 85 000 registered growers. The number of registered growers increased from 98 927 in 2017 to 145 725 in 2018. Of these registered growers, 40 894 were new. Active tobacco growers who delivered tobacco crop in the year 2018 also rose by 43% from 97 066 growers who delivered in 2017 to 140 895 growers in 2018. In 2018, the percentage of active growers to registered growers stood at 97% compared to 98% for 2017 (TIMB, 2018). According to TIMB (2021), 155 097 tobacco growers registered for the 2020/21 season. 1% of the total registered growers registered for the first time whilst the rest were renewals. In comparison, 166 959 registered in the 2019/20 season.

The tobacco growers were mostly concentrated in Mashonaland Central and Mashonaland West provinces of which each had 35% of total registered growers. Communal and A1 growers constituted 89% of the total registered growers whilst the commercial growers constituted the remaining 11%. Active growers who delivered tobacco at various selling points were 120 467 which represents 78% of the total registered growers. In the 2019/20 season, 122 367 out of 166 959 registered growers were active. In 2023, the area planted to tobacco reached 117 000ha, up from the 110 000ha planted in 2022. The country currently has 148 527 tobacco farmers (Farmer’s weekly, 2023) as shown by figure 1 below.

Figure 1: Number of Active Tobacco Farmers in Zimbabwe

Source: TIMB, 2021

Tobacco is produced by commercial, small-scale and communal farmers. The number of communal farmers participating in the tobacco farming has been on an upward trend reaching 73 378 in 2018 from 46 621 in 2017 as shown in table 1 below. Further, there was an increase in registered growers from small scale farmers from 6 545 to 8 423. Meanwhile A1 farmers rose from 38 103 to 54 282 farmers indicating a 42 percent increase from 2016/17 growing season to 2017/18 season. The increase in more farmers participating in tobacco farming has seen farmers earning foreign currency, empowering themselves with employment community development and most important poverty reduction.

Table 1: Registered Growers by Grower Sector

| SECTOR | 2016/17 | 2017/18 | % Change |

| A1 | 38 103 | 54 282 | 42% |

| A2 | 7 658 | 9 641 | 26% |

| Communal | 46 621 | 73 378 | 57% |

| Small Scale Com | 6 545 | 8 423 | 29% |

| Total | 98 927 | 145 725 | 47% |

Source: TIMB, 2018

Tobacco is the largest foreign exchange earner and Zimbabwe is ranked second the second important producer of flue-cured tobacco in the world and in the 2011/12 season tobacco accounted for about US$517 million from 140 million kg (TIMB, 2012). According to the 2013 budget statement from the Treasury tobacco received 55.4% of the 625 million availed by the banking sector (GoZ Ministry of Finance & Economic Development, 2013). This indicates the importance of tobacco to the Zimbabwean economy, it the confidence that the banking sector has in the sector indicates it’s potential. Hence the need to insure such a sector.

Agricultural insurance has been available in Zimbabwe prior independence in 1980, accessed by at least 1 500 commercial farmers, now 75 percent of tobacco is produced by small scale farmers who were empowered of land after the land reform program Takawira (2013). The bulk of these farmers are not insured at all. In Zimbabwe agricultural insurance is provided by the private sector on a voluntary and individual basis.

The loss ratio in crop insurance in Zimbabwe in the 90s stood at 20.65 percent which was low compared to other countries like India which had a loss ratio of 686,53 percent which was unsustainable and would require that the sector be subsidized by the government (UNCTAD Secretariat, 1994). The low loss ratio mean that the private sector can offer a competitive unsubsidized and affordable insurance package. Based on this the number of insurance companies offering agricultural insurance has grown to 23 insurance companies. Insurance companies in Zimbabwe mainly cover loss against fire, hailstorm and against other disasters Takawira, (2013). Insurance revenue from farmers dropped from USD4.9 million in 2012 to 1.9 million in 2013 a 68% drop in premiums (demand) and this resulted in 13 insurance companies remaining in the sector Sunday Mail (2014).

The concept of agricultural insurance is not popular in Africa except among the large-scale farmers although in the recent years, crops insurance has emerged as an important policy tool for enhancing household resilience against climatic risks. Whilst globally there is a vast body of literature that seeks to understand patterns and structure of crop insurance with respect to behaviour of the farmers under risk and their attitude, embedded information asymmetry problems such as moral hazard and adverse selection and the likely outcomes on household welfare, existing literature has been seriously biased towards indemnity-based insurance products. Nonetheless, recent innovations in the derivative financial intermediaries has seen a remarkable evolution of index insurance products in developing countries, but very little has been documented with regard to the quality of indexed products (Jensen et al, 2014 cited by Kirimi et al 2018).

Factors that affect uptake of crop insurance are yet to be fully understood partly because of lack of sufficient data and over-reliance on hypothetical evidence that seem to underscore theoretical viability of crop insurance yet the empirical evidence from pilot programs show mixed results on performance of agricultural insurance. Previous studies (Mohammed & Ortmann, 2005; Sundar & Ramakrishnan 2013; Falola, et al, 2013; Kwadzo et al, 2013; Aidoo et al, 2014; Daninga & Qiao 2014; Takahashi et al, 2014) have looked at determinants of crop uptake decision such as price of the insurance, knowledge of the farmers, resource endowment and rights but these studies tend to imply that insurance uptake is a binary mechanism yet there is an incremental feature that defines the intensity of uptake Kirimi et al (2018).

Over the past decade there has been a growing interest in agriculture insurance as a financial mechanism of mitigating against risk especially in the developing world Lecachuer, et al (2013). From almost being unknown in the developing world agriculture insurance is now considered as a viable option in risk management by governments, farmers and the insurance sector to the effect that governments in the developed and developing world and insurance companies have initiated such programs Nnadi, et al (2013).In the absence of formal market risk mitigating strategies households self-insure and this is not effective in safeguarding or mitigating against disasters like drought that affect almost all farmers in an area or country limiting the ability of farmers to aid each other. Farmers often draw down on their own saving often diminishing agricultural activities productivities Cole et al (2012).

Despite the fortunes and growth that have been witnessed in tobacco production there is an ever-present risk especially with the new farmers and the lack of safety nets necessary to absorb shock in case of unpleasant eventualities in this key sector. Agriculture risk’s mainly stems from the unpredictability biological, climatic and market variables which are often not within the control of the farmer (USDA, 2023). Agriculture production is highly exposed and subjected a multitude of these risks and uncertainties especially environmental and weather, the sector also faces risks in the form of prices, market, production and political. Agricultural production is heavily dependent on nature in order to succeed. Tobacco despite it being drought resistant depends on amount of rainfall, type of precipitation (hail destroys tobacco), prevalence of pest and diseases (low or absence is ideal) and it is also affected by biological agents which cannot be easily suppressed. Availability and stability of the ideal growing conditions cannot be guaranteed. In most developing countries agriculture is not insured by insurance/reinsurance providers or by capital markets or even government budgets hence they tend to be adversely affected by natural disasters (events) and non-natural risks (AMA,2021).

Tobacco as one of the key generators of foreign currency and jobs in Zimbabwe. In spite of the immerse contribution from tobacco it still remains highly risky, considering the degree of exposure to uncertainty due to its reliance on nature. Henceforth, the Zimbabwean tobacco farmer has little room for error due to limited wealth endowments hence it is imperative that the farmer safeguards and secure the gains they have so far experienced through engaging in more formal and protecting risk management strategies such as agriculture insurance. In order to maintain the impressive growth, stability and sustainability in tobacco farming there is need for farmers to take up insurance. Agricultural insurance schemes are a potential tool to cope with income losses through indemnity payments and therefore stabilize income and economic performance of farmers Anseeuw et al (2012). Therefore, this study seeks to analyze the determinants of crop insurance uptake by tobacco farmers.

METHODOLOGY

The study made use of logit model to analyse the determinants of crop insurance uptake by tobacco farmers in Zimbabwe. When a model has a dichotomous dependent variable (Yi), where one represents insured and zero not insured, different regression methods can be used (e.g., discriminant analysis, linear probability model, logit and probit). The assumption of multivariate normality that discriminant analysis is based on limits its use as the assumption may be violated. The logit model is based on the cumulative distribution function and yields results that are not sensitive to the distribution of sample attributes when estimated by maximum likelihood. If the aim is to examine which variables are significant in explaining a dependent dummy variable using the logit model, disproportionate sampling is not a problem as it only affects the constant term and not the estimated slope coefficients (Maddala, 1992).

The logit regression model is a unit or multivariate technique which allows for estimating the probability that an event occurs or not by predicting a binary dependent outcome from a set of independent variables. The logit model is based on cumulative logistic probability function and it is computationally tractable. According to Gujarati and Porter (2009), it is expressed as:

Pi = E(Y=1|Xi) = B1 + B2Xi……………………………………………………… (1)

The explicit logic model is:

![]() …………………………………………………….1

…………………………………………………….1

Where:

Y = dichotomous response variable (1 for farmers who participated in Agricultural insurance scheme; 0 otherwise)

X1 = Age of farmers (Years)

X2= Educational level of farmers (years of schooling)

X3=Farm size of farmers (hectares)

X4= Number of years in tobacco farming

X5= Household size (number)

X6= Membership of associations (number of associations a farmer belongs to)

X7=Accessibility to credit (amount of loans a farmer accessed over last 5 years)

X8= Contact with extension agents (number of contacts)

X9= income (last season’s income from tobacco)

β1 – β9= coefficients of stimulus variables

α = constant term

ε= error term

Henceforth the logit model for the study will be expressed as follows:

………………….2

………………….2

The model was examined of Heteroscedasticity and Multicollinearity tests. The data analysis was performed with the STATA V 11.

Study Area

The study was conducted during the tobacco selling season at the auction floors in Harare, where all of Zimbabwe’s tobacco is auctioned. Harare hosts three major auction floors: Boka Tobacco Auction Floors, Premier Tobacco Auction Floors, and TSF Auction Floors. Additionally, there are several contract auction floors also situated in Harare. The cultivation of tobacco primarily occurs in the northern regions (provinces) of Zimbabwe, specifically Mashonaland East, West, and Central. Notably, dry regions such as Matebeleland, Masvingo, and the Midlands have witnessed an increase in the number of farmers engaged in tobacco cultivation.

Study Population

In this study, a sample of 121 tobacco farmers was randomly selected using a convenient sampling approach. Baxter (2015) highlights that convenience sampling is commonly employed. Rather than aiming for a truly representative sample of the entire population, this method involves recruiting participants from a convenient subset. These individuals are readily accessible at a specific moment, such as those present in public buildings or workplaces. Galloway (2005) similarly posits that convenience sampling involves using respondents who are easily accessible to the researcher. There is no specific pattern in selecting these participants; they may be recruited simply by approaching people present in a given location. Edgar and Manz (2017) concur with Galloway (2005), emphasizing that convenience sampling collects samples from conveniently located individuals. In our case, we selected tobacco farmers centralized at auction floors, representing diverse geographical origins.

Sampling Instrument

To analyse the determinants of crop insurance uptake by tobacco farmers a well-structured questionnaire was developed. The information obtained from the farmers include their socioeconomic characteristics such as income of famer, household size, educational status, farm size, sex, marital status and membership of associations, information on level of awareness of insurance and information on the constraints encountered by the farmers in the process of participation in insurance scheme.

Ethical considerations

Prior to conducting this research, necessary permits were obtained from the relevant organisations (Insurance Pension Commission, Tobacco Industry and Marketing Board, Auction floors managers). Participation of farmers was voluntary and confidentiality was guaranteed.

RESULTS

Awareness and Participation of Tobacco farmers in Tobacco insurance

Table 2: Level of awareness of tobacco crop insurance

| Awareness | Number of Respondents | Percentage |

| Yes | 104 | 85 |

| No | 17 | 15 |

| Totals | 121 | 100 |

Source: Survey

Despite the relatively high level of awareness of tobacco insurance crop insurance remains relatively low. The findings shown in table 2 above revealed that small scale farmers are mainly engaged in field cover tobacco insurance, while commercial farmers are mainly engaged in field and field to floor insurance. Inspite the high levels of awareness of crop insurance to farmers tobacco insurance uptake remains low because insurance companies are not fully marketing their products and there are indications that they only appear at auction floors and rarely visit farmers to market their products. This view was also highlighted by contracting companies interviewed.

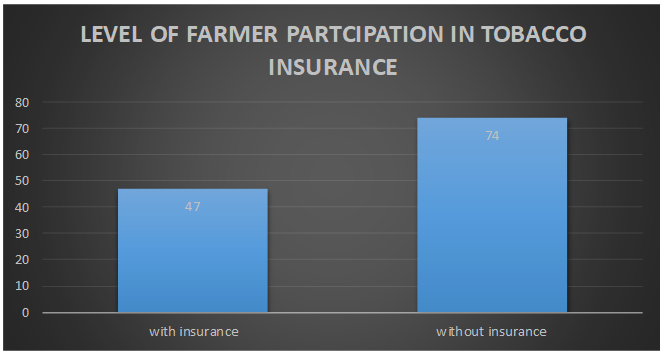

Table 3: Level of Participation in Tobacco Insurance

| Participation | Number of Respondents | Percentage |

| Yes | 47 | 39 |

| No | 74 | 61 |

| Totals | 121 | 100 |

Source: Survey

Figure 2: Level of Participation in Tobacco Insurance

Source; Survey

The level of participation is 39% of the 121 farmers, for farmers with a total land holding of less than 6 ha the level of participation goes down to 12.7 percent as shown in table 3 above. Figure 2 further reveals that the level of participation is generally low as farmers indicated that they were not satisfied by the service that they are getting and that has been one of the greatest let down in terms of insurance uptake. Additionally, insurance companies are not fully marketing their products and they only appear at auction floors and rarely visit farmers to market their products. More so, farmers are highly sceptical about engaging in insurance and that they indicated that they are willing to face the consequences of risk since insurance companies lack integrity.

Constraints to the uptake of agricultural insurance in Zimbabwe

Firstly, agricultural insurance remains unpopular in this country largely because the insurance products are not addressing the needs of smallholder and subsistence farmers who are the majority in Zimbabwe following the land redistribution exercise. Furthermore, general mistrust in insurance services, and reliance on traditional self-insurance in risk and loss management are some of the factors that hinder uptake of agricultural insurance. This view is in line with IPEC (2018) study which revealed that farmers have lost confidence in insurance firms who take advantage of gullible communal farmers by not fully explaining the fine print to them. While on the same note, the Insurance Council of Zimbabwe has emphasised the need for insurance companies to come up with products with the agricultural insurance segment that cater to the needs of the recently emergent indigenous farmers (ICZ, 2020).

Agriculture insurance remains relatively a largely untapped sector. The levels of insurance in the farming sector in Zimbabwe are very low, with agriculture contributing barely five percent to gross premium income of insurance products. Agricultural insurance is one of the most ignored tools for risk management yet it can play a pivotal role in managing the risks related to farming. Furthermore, farmers surveyed mentioned that they are not insured as it is difficult for them to access insurance services. Most insurance providers rely on antiquated distribution channels like agents and brokers, which are highly unproductive. Farmers view insurance as an expense with no benefits, but those who have experienced disasters now appreciate the importance of insurance. The results concur with IPEC (2018) report which posite that agricultural insurance has the potential to address some of these constraints by facilitating access to means of production and changing behaviour by reducing uncertainty.

Agriculture insurance products have low demand from the majority of farmers as insurance companies demand hefty collateral demands which were beyond their reach. Tsikirayi et al (2013) postulates that collateral requirements by financiers for farm insurance was the major determinant followed by past losses experienced by farmers and degree of risk aversion. This view is in line with Makaudze and Miranda (2009) who assert that the farmers who purchase insurance are likely to have experienced significant losses in the past. Farmers in geographical areas that are prone to disaster tend to have high levels of insurance uptake, as they seek to protect themselves against the high risk of loss. Nature of farming enterprise was also cited as important, for example, a tobacco farmer tends to insure because of the higher costs and profitability of the enterprise (unlike a grain farmer). Level of production, herd behaviour and geographical location are other factors. In addition, purchase of inputs could be given priority over insurance uptake due to limited resources.

Furthermore, low incomes served as an impediment to uptake of insurance. This indicates that the premiums are beyond the farmers’ means, hence the low uptake of insurance. This is also worsened by unstable economic environment that farmers find themselves in. This has an overall effect of reducing agricultural insurance uptake. Furthermore, low uptake of insurance is largely driven by thin profit margins in the sector particularly for small scale commercial and subsistence farmers, and the lack of knowledge on the benefits of insurance and risk management services.

The low regard for the insurance providers emanates from respondents’ registered dissatisfaction with the service delivery. The dissatisfaction shown in the current study stems from late or non-payment of insurance when disaster strikes. This supports earlier findings by the Commodity Risk Management Group of the World Bank (2006) which showed that high uptake of an agricultural weather insurance policy in India resulted from quick pay out of the policy and high awareness of policy features possessed by farmers that contributed to insurance satisfaction.

Constraints in Accessing Tobacco Insurance

Small scale farmers with less than 6 ha of total land holding indicated that even if they were aware of tobacco crop insurance, they were not familiar with how it works hence they found it difficult to subscribe to a product that they were not well versed. Of the 61 % not insured 22% were not aware of tobacco insurance, 80 % of the 78 % aware of tobacco insurance indicated that the premiums of USD210 on the low side were too expensive for them. 89% of farmers without insurance also indicated that insurance companies did not visit them at their farmers or at meeting to market their production hence little familiarity with tobacco insurance. Small scale farmers indicated that they had little income and farmed small pieces hence there was no need to insure against risk of loss on field or floor, this is in line with Tsikirayi et al (2013) findings. They also indicated that if they increased production, they would participate in tobacco insurance. All farmers located far from Harare indicated that they feared that insurance companies would not come to assess loss in cases of the risk occurring hence they were hesitant to insure.

Table 5: Logit Model Results for Tobacco insurance uptake in Zimbabwe

| Variables | Coefficients(β) | S.E | Significance | Odds Ratio |

| Age of farmer | 0.04 | 0.04 | 0.295 | 1.04 |

| Tobacco Farming Experience | 0.25 | 0.08 | 0.002* | 1.29 |

| Education(years in school) | 0.54 | 0.15 | 0.000* | 1.73 |

| Farm Size | -0.02 | 0.02 | 0.313 | 0.98 |

| Household size | 0.06 | 0.11 | 0.534 | 1.08 |

| Member of Association | 0.03 | 0.53 | 0.949 | 0.99 |

| Credit (Number of loans accessed over the past 5 years | -0.37 | 0.34 | 0.913 | 1.06 |

| Frequency of extension officer visits | 0.18 | 0.08 | 0.036* | 1.21 |

| Income | 0.000083 | 0.000451 | 0.025* | 1.00 |

| Cons | -12.73 | 3.04 | 0.000 | |

| N=121 | ||||

| R2 =0.7552 |

NB: * Statistical Significance at 5% level

DISCUSSION OF FINDINGS

Farmers with more years in tobacco farming tend to purchase tobacco insurance more than farmers with fewer years in tobacco farming. It is highly likely that these farmers have faced a loss at some point in their farming life hence will see the importance of tobacco insurance. Also farmers with long periods of tobacco farming have higher harvests and tend to lose much if risk occurs such as hail, wind, fire or rain when delivering crops. They also produce better quality tobacco, therefore have potential to get higher revenue so they insure to protect against loss. This is also supported by Mohammed et al (2005) who in their study of livestock farmers in Eritrea found out that uptake of livestock insurance was high to farmers who were aware of the livestock insurance and further enabled by formal education received by the household head. Farmers with more experience farming tobacco are highly likely not have off-farm employment therefore have no other sources of income that can sustain them in case of a loss. Farmers with more years in tobacco farming were opting to purchase insurance because they have received some awareness of the usefulness of hedging crops against risks through field events organised by local agriculture extension workers and other relevant NGOs.

Education also is significant in determining the uptake of insurance by farmers, the result is consistent with Oyinbo, et al (2012) and Mohammed & Ortmann, (2005), in their studies education was significant at 5 and 10 percent respectively. Akter et al. (2008) found out that education and income influenced insurance uptake amongst farmers. Farmers who are educated are likely going to appreciate the role insurance plays in the global business environment. Most of the young professionals are now engaging in farming and most of the time it’s for commercial purposes and this has been necessitated by Fast Track Land Reform Programme (FTLRP) which has seen the rise of younger farmers. Educated farmers are more likely to understand the insurance contracts such that lack of understanding does not hinder their participation in insurance and such is Zimbabwe farmers who possess a formal education. Despite farmers awareness of tobacco insurance some farmers indicated that they were not very conversant with the insurance concept hence not involved in tobacco crop insurance.

While on the same note, frequency of extension worker visits was a significant determinant in tobacco insurance uptake, this is consistent with Cole S (2012) and Oyinbo, et al (2012) in their study as well. Farmers which received high number of extension worker visits are contract farmers and those that are in the vicinity of contracted farmers. These farmers are highly likely to produce a better crop and to farm large pieces of land (tobacco) such that their loss would be greater if they don’t insure. Also knowledge from extension workers is some form of education hence increases the farmer’s awareness of tobacco insurance. Frequency of visits by extension work also increases the farmer’s knowledge on the events taking place in the tobacco sector hence increase one’s chances of getting information on tobacco insurance. Contact with external consultants is likely to assist farmers to improve their quality since they get free advice and technical knowhow to address some of the shortcomings they will be facing to produce a tobacco crop fetching higher prices in the market.

Level of income of farmer was also found to be significant hence increases the probability of farmer participation in tobacco insurance. Farmers with larger income face higher losses if they don’t insure hence the need to insure. The results were consistent with Falola et al (2011) studies in Nigeria found out that the more income one has the more capable one is of covering against risk hence low uptake of agricultural insurance. Higher level of income also means that they can afford to pay the insurance premiums which have been cited before as one of the hindrances to insurance uptake. Since, the fast track land reform black farmers who commenced tobacco farming are young farmers with no significant income and hence uptake has been low since the majority are still budding farmers.

Meanwhile, credit as well as farmsize were found to be insignificant in the study largely because there was no harmony between farmers and financial institutions. Over the years agriculture finance in Zimbabwe has dwindled down. Climate change has also contributed with agricultural output decreasing as rain fed agriculture has been affected by frequent dry spells thus reducing farm income and surpluses. The infamous land reform disrupted farm ownership and hence financial institutions can’t guarantee agriculture finance where there is no security of lease. Tsikirayi et al (2013) in his study of Zimbabwean farmers revealed that limited knowledge on insurance, unaffordability of insurance, low income levels, low agriculture production, remoteness of farms from service providers and negative perceptions about insurance in general. Farmers have also been found to be reluctant in hedging substantial amounts of risk with different types of instruments and the reasons have not been clear whether it is due to poor product design, lack of demand, or barriers to demand linked to liquidity, financial literacy or lack of trust Cole et al (2012). Credit to tobacco farmers has been elusive largely because of no affordable agriculture finance schemes in the local market, a general decay of economy has also influenced agriculture fiancé to migrate outside the country. Furthermore, credit in Zimbabwe has been expensive coupled with high rates against a freefalling currency with no stability. Farmers finance their farming activities through little private savings and borrowing from relatives which usually has higher premiums.

CONCLUSIONS

The study investigated the determinants of demand for tobacco insurance among Zimbabwean tobacco farmers. Uptake of tobacco insurance in the country is still low with a number of tobacco famers not even aware of the insurance schemes provided by insurance companies. The study shows that there is an un-healthy relationship between farmers and insurance companies and that there is need to address the failure and short comings of the insurance sector through all stakeholder meetings. The study also reveals that there is need for the following to be done to mitigate the risks that farmers face in agriculture in Zimbabwe.

RECOMMENDATIONS

The study makes the following recommendations

a. Product Quality and Design:

- Develop insurance products that align with farmers’ needs and risks.

- Ensure transparent terms, coverage, and benefits.

- Tailor insurance options to specific crops and regions.

b. Affordability:

- Offer cost-effective premiums that smallholder farmers can afford.

- Subsidize premiums or explore group insurance models.

- Link insurance to credit or input packages.

c. Information and Education:

- Raise awareness about the benefits of insurance.

- Educate farmers on how insurance works, claims procedures, and risk management.

- Use local channels (community meetings, radio, mobile apps) for outreach.

d. Behavioural and Sociocultural Factors:

- Address trust issues related to insurance providers.

- Leverage social networks and community leaders to promote insurance.

- Highlight success stories from early adopters.

e. Government Support:

- Create an enabling policy environment.

- Subsidize premiums or provide incentives for insurers.

- Collaborate with NGOs and development agencies to promote insurance.

f. Innovative Approaches:

- Explore index-based insurance (linked to weather or crop yield).

- Use mobile technology for premium payments and claims.

- Bundle insurance with other services (e.g., extension advice, credit).

Further studies can also come up with a demand function of insurance. Further, there is also need to investigate challenges that insurance companies face in offering tobacco insurance and agricultural insurance at large.

There is need of more synergies with international organisations to cushion farmers. World Bank Group member the International Finance Corporation (IFC) can partner with Zimbabwean insurance regulator the Insurance and Pensions Commission (IPEC) to create a market for agricultural insurance products in Zimbabwe to protect smallholder farmers from weather-related crop damage and other shocks. Through the partnership, the IFC can assess the risks smallholder farmers face, how they are coping with those risks and will gauge farmers’ appetite for agricultural insurance to protect livelihoods.

The IFC can also help the IPEC develop a regulatory framework and enabling environment for agricultural insurance and determine the features of insurance products appropriate for Zimbabwe’s farmers. The Zimbabwe agriculture market lacks knowledge for insurance best practices to develop agri-insurance markets and such synergies can facilitate such exchanges.

The government should assist farmers in improving the quality and quantity of tobacco farmers produce through providing or allowing the provision of necessary infrastructure like dams and roads and communication. Better infrastructure will increase output, reduce assessment times and improve farmer output if water is made available. Increased output means that increases revenue/income which will increase farmer participation. Markets should work more perfectly so that farmers get better revenue/income which will increase insurance participation. In the past seasons farmer have complained about unattractive prices at the auction floors.

The study included both large and small-scale farmers hence there is need to categorize the two farmers because they share different characteristics and this resulted in some variables being insignificant. Categorizing farmers also allows us to compare the differences in factors influencing insurance uptake which will help in creating policy or strategies that increase farm participation in insurance. Since there are different kinds of tobacco insurance products which generally fall under field and field to floor insurance, there is need to investigate the determinants of farmer choice of insurance. This will help insurance companies come up with better products that are suitable to the different farmers in the market. Even the government can come up with policy that is more informed and appreciate determinants of farmer choice of insurance if they choose to intervene.

Lastly, coverage can enable farmers to invest in riskier but potentially more lucrative farm activities. Timely insurance pay-outs after crop losses can help smallholders’ smooth consumption and prevent the sale of assets. Insurance can also be a catalyst, as lenders will be more likely to extend credit to farmers covered by insurance, allowing them to make productivity Further studies can also come up with a demand function of insurance. There is also need to investigate challenges that insurance companies face in offering tobacco insurance and agricultural insurance at large.

REFERENCES

- Anseeuw, W., Kapuya, T. & Saruchera, D., 2012. Zimbabwe Agricultural Reconstruction: Present State, On-going projects and prospects of Investment, Pretoria: Development Bank of Southern Africa Limited.

- Ariel, S., Hart, C. & Lence, S., 2010. Demand for Crop Insurance by Organic Corn and Soyabean Farmers in Three Major Producing States, IOWA: IOWA University.

- Cole, S., Bastian, G. G., Vyas, S., Wendel, C., & Stein, D. (2012). The effectiveness of index-based micro-insurance in helping smallholders manage weather-related risks. http://doi.org/978- 1-907345-35-7

- Falola, A., Ayinde, O. E., & Agboola, B. O. (2013). Willingness To Take Agricultural Insurance By Cocoa Farmers in Nigeria. International Journal of Food and Agricultural Economics, 1(1) 97-107. Retrieved from http://foodandagriculturejournal.com97.pdf

- FAO, 2001. Issues in the Tobacco Global Economy. [Online] Available at: www.fao.org/docrep/006/y4997e/y4997e0k.htm#TopofPage [Accessed 5 March 2014].

- GoZ Ministry of Finance & Economic Development, 2013. The 2014 National Budget Statement, Harare: GoZ.

- https://allafrica.com/stories/202011100183.html. Accessed November 2021.

- https://ipec.co.zw/crop-insurance-freeing-farmers-from-risk. Accessed November 2021

- https://www.engineeringnews.co.za/article/ifc-zimbabwe-regulator-to-develop-agricultural-insurance-to-protect-smallholder-farmers-2021-02-15

- https://www.farmersweekly.co.za/agri-news/africa/zimbabwe-sells-record-of-261-million-kilograms-of-tobacco/ accessed 12 July 2023.

- https://www.herald.co.zw/tobacco-output-surpasses-2023-target/ accessed 12 August 2023

- https://www.reuters.com/world/africa/zimbabwe-tobacco-output-expected-rise-85-2023-2023-03-08/ accessed 12 August 2023.

- M. A. Mohammed, G. Ortmann (2005) Factors Influencing Adoption of Livestock Insurance by Commercial Dairy Farmers in 3 Zobatat of Eritrea.DOI:10.1080/03031853.2005.9523708.

- Maddala G S (1992) Introduction to Econometrics 2nd Edition, MacMillan Publishing Company. ISBN 0-02-374545-2.

- Makamure J, Mur K, Muchopa L.C (2001) ‘Liberalisation of agricultural markets’ unpolished report, SAPRI/ Zimbabwe, Harare.

- Makaudze, E., M. and Miranda, M., J (2009) Catastrophic Drought Insurance Based on the Remotely Sensed Normalized Difference Vegetation Index for Smallholder Farmers in Zimbabwe. Contributed Paper Presented at the Joint 3rd African Association of Agricultural Economists (AAAE) and 48th Agricultural Economists Association of South Africa (AEASA) Conference, Cape Town, South Africa, September 19-23, 2010.

- Nnadi, F. N., Chikaire, J., Echetama, J. A., Ihenacho, R. A., & Umunnakwe, P. C. (2013). Agricultural insurance: A strategic tool for climate change adaptation in the agricultural sector. Net Journal of Agricultural Science, 1(March), 1–9.

- Oyinbo.O, Abdulmalik, R. & Sami, R., 2012. Determinants of Crop Farmer Participation in Agricultural Insurance in the Federal Capital Territory, Abuja, Nigeria. Greener Journal of Agricultural Sciences, 2(3), pp. 021-026.

- Takawira, 2013. Tobacco Insurance Conference on Cards, Harare: Sunday Mail.

- Tsikirayi, C. M. R., Makoni, E., & Matiza, J. (2013). Analysis of the uptake of agricultural insurance services by the agricultural sector in Zimbabwe. Journal of International Business and Cultural Studies, 7, 1–14.

- UNCTAD Secretariat, 1994. Agricultural Insurance in Developing Countries. Geneva, UNCTAD.

- “World Bank. 2003. The World Bank Annual Report 2003: Volume 1. Year in Review. Washington, DC. © World Bank. https://openknowledge.worldbank.org/handle/10986/13929 License: CC BY 3.0 IGO.”

- “World Bank. 2005. The World Bank Annual Report 2005: Year in Review, Volume 1. Washington, DC. © World Bank. https://openknowledge.worldbank.org/handle/10986/7537 License: CC BY 3.0 IGO.”