Do Small and Medium Enterprises Spur Economic Growth? Evidence from Nigeria (1999-2020)

- Oladipo, Abimbola Oluwaseun

- Nwokocha, Azuka Florence.

- Nkamnebe, Ogochukwu Edith.

- 801-811

- Oct 4, 2023

- Economics

Do Small and Medium Enterprises Spur Economic Growth? Evidence from Nigeria (1999-2020)

Nkamnebe, Ogochukwu Edith., Nwokocha, Azuka Florence., & *Oladipo, Abimbola Oluwaseun.

Nnamdi Azikiwe University, Awka

*Correspondence Author

DOI: https://dx.doi.org/10.47772/IJRISS.2023.70968

Received: 25 August 2023; Accepted: 05 September 2023; Published: 04 October 2023

ABSTRACT

This study investigates if Small and Medium Enterprises (SMEs) contribute to economic growth in Nigeria between 1999 and 2020. The data used for the study were obtained from CBN statistical bulletin and National Bureau of Statistics in collaboration with Small and Medium Enterprises Development Agency of Nigeria on the variables such as the number of SMEs in Nigeria (NSMES), Commercial Banks Credit to SMEs (CBSME), SMEs employment generation (SMEEG) and interest rate (INTRT). Since the data for the variables are time series which are always not stationary, the test of staionarity was conducted using Augmented Dickey-Fuller unit root test. ARDL Bounds test for co-integration was employed to check the long run relationship while Autoregressive Distributed Lag (ARDL) technique was employed to estimate the parameters of the model. From the results of the regression, some variables such as NSMES, CBSME and INTRT have positive impact on the economic growth while SMEEG has negative impact on economic growth in Nigeria in the short run. The result further shows that only NSMES has significant impact on economic growth, while CBSME, SMEEG and INTRT are insignificant. The study therefore, recommends that government should create enabling environments for the SMEs to thrive well. Also, commercial banks should encourage financial inclusion, that is, SMEs should be given easy access to loans. This can go a long way to help investors to bring their ideas into reality.

Keywords: SMEs, Economic Growth, interest rate, ARDL, Nigeria.

INTRODUCTION

The major drivers of growth in developing economies are the small and medium enterprises. They serve as engines of socio-economic transformation, including industrialization of many economies the world over. SMEs also offer opportunities to drive jobs and wealth creation as well as income redistribution within society ((National Bureau of Statistics [NBS]/Small and Medium Enterprises Development Agency of Nigeria [SMEDAN], 2017). According to the report by NBS/SMEDAN (2017), SMEs accounts for about 90 percent of the businesses worldwide, while 50 percent of the employment generation across the world comes from the SMEs. This shows how important the SME is in enhancing economic growth.

In the Nigeria context, SMEs has contributed immensely to job creation, exports and gross domestic product. In 2017 alone, the total number of small and medium enterprises (SMEs) stood at 73081 million (NBS/SMEDAN, 2017). This number however reduced to 69910 in 2020 due to the emergence of COVID-19 pandemic that disrupted all economic activities in the world. This has affected both the number of SMEs and employment generation by the enterprises.

Another challenge that has bedeviled the SMEs is access to finance. Having access to finance will not only boost the existing businesses but also encourage more SMEs, increase employment generation and foster economic growth (Price water house Cooper [PwC], 2020). Lack of access to finance is the second most notable obstacle after their low participation in the international trade. SMEs lack access to bank loans than large firms. As such, they relied on internal funds, or cash from friends and family to set up businesses. This makes their size and scope limited to what can be globally competitive in the international trade (PwC, 2020). The International Finance Corporation (IFC) estimates that about 65 million firms, or 40% of formal micro, small and medium enterprises (MSMEs) in developing countries need financial help of $5.2 trillion every year to expand and thrive well. This is equivalent to 1.4 times the current level of the global lending to MSMEs (World Bank, 2023).

The rate at which commercial banks lend money to SMEs is also high. In 2007, lending interest rate was 16.94 percent while it increased to 16.95 in 2021 (NBS, 2021). This is too high for businesses that want to survive in the competitive market. Due to all these problems mention, the contribution of SMEs to gross domestic product in Nigeria has reduced. According to the report by NBS/SMEDAN (2017), MSMEs in Nigeria contributed 49.78 percent to the country’s gross domestic product (GDP). However, in 2020, the percentage contribution of SMEs to GDP reduced to 46.3 percent (NBS, 2021).

As part of the effort to help SMEs contribute largely to gross domestic product, the Nigeria government formulated and implemented policies such as National Economic Empowerment and Development Strategy (NEEDS) in 2003-2007, enactment of the SMEDAN Establishment Act of 2003, National MSMEs Policy of 2007, National Social Investments Programme of 2016 amongst others. Despite all these programmes and initiatives by the government, the contributions of SMEs to GDP continue to decline which may be due to the failure of the government in tackling the problems of access to finance, high interest rate, insecurity, and infrastructural facilities such as electricity, good roads, portable water and so on (NBS/SMEDAN, 2017).

From the empirical review, there exists no consensus among scholars as some found that SMEs has positive impact on economic growth while some established that SMEs does not have any linkages with the growth of the economy. The disparity in their findings may however be differences in method employed, variables in the study as well as the scope of the study. Thus, this study examines the impact of SMEs on economic growth in Nigeria between 1999 and 2020, using ARDL method.

The following research questions were proffered answers to in the course of the study.

- To what extent has small and medium enterprises impacted the growth on the Nigerian economy?

- Does commercial banks credit to small and medium enterprises have significant impact on economic growth in Nigeria?

- Is there any significant impact of SMEs employment generation on economic growth in Nigeria?

- What is the impact of interest rate on economic growth in Nigeria?

LITERATURE REVIEW

2.1. Theoretical Literature

Resource-Based View Theory

The theory of resource-based view was developed by Penrose (1959). The theory argued that the available resource that is effectively allocated would enhance businesses and foster economic growth and development, than other industrial structure. Penrose (1959) maintains that firms can create economic value due to effective and innovative management of resources at their disposal. The bone of contention of this theory is that even with lack of access to bank loans and high lending rate, the available funds by the SMEs can still boost their investments and help contribute to economic growth if effectively and efficiently utilized (Penrose, 1959).

This theory can be criticized on the ground that in some economies, even in Nigeria context, many entrepreneurs who have vision and resources at their disposal to create new ideas cannot bring them to reality due to various challenges that range from lack of infrastructural facilities, insecurity, lack of finance either from friends, family or personal. Penrose failed to realize that adequate infrastructural facilities such as electricity, good roads amongst others, secured environment, access to finance are the supporting ingredients that can make the available resources at the disposal of the existing firms or potential businesses to enhance their businesses and stimulate economic growth.

However, this study is anchored on the theory of resource-based view theory propounded by Penrose (1959) because the theory maintains that despite all odds, firms can still create economic value if the available resources at their disposal are efficiently and effectively utilized.

2.2. Empirical Literature

Several works have been done on the impact of SMEs on economic growth across the globe. Thus, some of these studies are reviewed here.

Emmanuel and Willie (2021) empirically studied the impact of SMEs on economic growth in Nigeria between 1986 and 2018. The study employed vector autoregressive model (VAR) and the result showed that SMEs output growth rate has significant positive impact on economic growth in Nigeria. Oluyemi and Ayodele (2021) studied the impact of small and medium enterprise formation on economic growth in Nigeria. The study covers the period of 1990 to 2016 and utilized error correction model (ECM) to estimate the parameters of the model. The result however found that increasing number of SME formation contributes to the growth of Nigeria economy. The result further reveals that the elasticity of employment is positive and statistically significant.

Lyndon and Opinion (2021) evaluate the impact of small and medium enterprises development on economic growth in Nigeria from 2000 to 2018, using OLS multiple regression model. It was found from the result that aggregate asset base and aggregate capitalization of SMEs is insignificant on economic growth in Nigeria. Aladin et al. (2021) empirically investigate the impact of SMEs on economic growth in Indonesia between 1999 and 2019. The study employed Johansen cointegration, vector error correction model, granger causality and Impulse response function. The result revealed that there is long run relationship between SMEs and economic growth in Indonesia. It further revealed that number of SMEs has positive but insignificant impact on economic growth while workforce of SMEs has positive and significant impact on economic growth. Also, the result found that there is no causal relationship between SMEs and economic growth. The result of the impulse response showed that the response has a positive direction.

Mairiga et al. (2021) also employed Autoregressive Distributed Lag Model (ARDL) to study the impact of small and medium enterprises performance on economic growth in Nigeria between 1980 and 2017. The study found that SMEs output, domestic credit to private sector and commercial banks credit to SMEs have positive impact on economic growth in the long run. However, lending interest rate has negative but insignificant impact in the short run.

Ameh et al. (2020) employed library and desk research method to analyze the impact of SMEs on economic growth in Nigeria. Questionnaires were distributed to collect data and 300 responses from the respondents were analyzed. From the result, it was found that SMEs are the important contributors to the growth of Nigeria economy.

Bello et al. (2018) examine the impact of SMEs on economic growth in Nigeria from 1986 to 2016. The study utilized modified OLS method and the result revealed that SMEs has positive and significant impact on economic growth in Nigeria. Grisejda and Krisdela (2016) studied the impact of SMEs on economic growth in Albania, covering the period of 1995 to 2015. The study employed OLS method and it was revealed from the findings that SMEs does not drive economic growth in Albania. Opafunso and Adepoju (2014) investigate the impact of SMEs on economic development of Ekiti State. The study covered the period from 2006 to 2013, using a survey research design. The result however found that there is positive and significant impact of SMEs on economic development of Ekiti State, Nigeria.

Taiwo et al. (2012) investigate the impact of SMEs on economic growth and development in Nigeria. The study covered registered SMEs operating in five local governments of Ogun state. These local governments comprise of Ijebu North, Yewa South, Sagamu, Odeda and Ogun Waterside. A survey method, using questionnaires was employed to collect the data and descriptive statistics was adopted to analyze the questionnaires. Summarily, the study reveals that there are constraints hindering the contribution of SMEs to economic growth in Nigeria. The study therefore states the problems as poor infrastructural facilities, lack of financial support, poor management, corruption, insufficient profits and low demand of goods and services. Offor (2012) employed OLS to investigate the impact of SMEs on economic growth in Nigeria from 1986 to 2010. The study found that despite the poor funding by commercial banks to SMEs, SMEs still contribute to economic growth in Nigeria.

DATA AND METHODOLOGY

3.1. Model Specification

The study examines the impact of SMEs on economic growth in Nigeria between 1999 and 2020. However, this study adopts the model of Aladin et al. (2021) with a slight modification. In the model of Aladin et al. (2021), economic growth was modeled as the function of number of SMEs and workforce of SMEs. The model is specified as in equation 1;

GDP = f (Nu SMEs, Lo SMEs) 1

Where, NuSMEs is number of SMEs and LoSMEs is workforce of SMEs. This study thus includes the variables such as number of SMEs, SMEs employment generation, commercial banks’ credit to SMEs, interest rate and GDP. It is specified as;

RGDP = f(NSMES, SMEEG, CBSME, INTRT) 2

Where, RGDP is real gross domestic product; NSMES is number of SMEs; SMEEG is SMEs employment generation; CBSME is commercial banks’ credit to SMEs; INTRT is interest rate. Equation 2 can be re-written in econometrics form as thus:

RGDPt = ![]() 0 +

0 + ![]() 1NSMESt +

1NSMESt +![]() 2CBSMEt +

2CBSMEt + ![]() 3SMEEGt +

3SMEEGt + ![]() 4INTRTt +

4INTRTt + ![]() t 3

t 3

Where: t = time subscript, ![]() 0 = Intercept of relationship in the model,

0 = Intercept of relationship in the model, ![]() 1 –

1 – ![]() 4 = Coefficient of each exogenous or explanatory variable,

4 = Coefficient of each exogenous or explanatory variable, ![]() t = Stochastic error term.

t = Stochastic error term.

The ARDL model is specified thus;

3.2. Data Analysis Techniques

To analyze the data obtained from NBS and CBN on the variables of interest in this study, the autoregressive distributed lag (ARDL) model was employed. This method was chosen because it is suitable for time series data with small sample sizes. It can also be applied if the order of integration is at zero and first difference, that is I (0) and I (1). Before employing ARDL, the Augmented Dickey Fuller test was employed to test for unit root, then, the ARDL bounds test for cointegration was conducted. This is to ascertain if there is long run relationship among the variables or not.

RESULTS AND DISCUSSION OF FINDINGS

4.1. Descriptive Statistics Test

The test was carried out to show the mean, variance, average, standard deviation, kurtosis and skewness of the variables.

Table 1: Summary of Descriptive Statistics

| RGDP | NSMES | CBSME | SMEEG | INTRT | |

| Mean | 4.682821 | 4.853345 | 1.466415 | 1.651176 | 17.84955 |

| Median | 4.723948 | 4.859241 | 1.511972 | 1.647675 | 16.92000 |

| Maximum | 4.857900 | 6.093760 | 2.093176 | 1.752816 | 24.77000 |

| Minimum | 4.384098 | 4.543223 | 1.031408 | 1.633468 | 11.35000 |

| Std. Dev. | 0.160468 | 0.293997 | 0.338935 | 0.024629 | 2.904778 |

| Skewness | -0.529058 | 3.541031 | 0.195557 | 3.323000 | 0.509189 |

| Kurtosis | 1.914869 | 15.91269 | 1.629593 | 14.54344 | 3.800779 |

| Jarque-Bera | 2.105690 | 198.8188 | 1.861737 | 162.6354 | 1.538479 |

| Probability | 0.348944 | 0.000000 | 0.394211 | 0.000000 | 0.463365 |

| Sum | 103.0221 | 106.7736 | 32.26114 | 36.32587 | 392.6900 |

| Sum Sq. Dev. | 0.540748 | 1.815124 | 2.412410 | 0.012738 | 177.1925 |

| Observations | 22 | 22 | 22 | 22 | 22 |

Source: Eviews 10.0 Output

From Table 1, the mean values for real gross domestic product (RGDP), number of SMEs (NSMES), commercial banks credit to SMES (CBSME), SMEs employment generation (SMEEG) and interest rate (INTRT) are 4.6828, 4.8533, 1.4664, 1.6512 and 17.849 respectively. This shows that INTRT has the highest mean value while the value for CBSME is the lowest. The standard deviations for the variables reveal that RGDP has the value of 0.1605, NSMES has the value of 0.2940, CBSME has the value of 0.3389, SMEEG has the value of 0.0246, while INTRT has the value of 2.9048. This implies that the variables have low variability due to their low standard deviations. The result of the descriptive statistic further reveals that the RGDP is negatively skewed, that is, skewed to the left, while NSMES, CBSME, SMEEG and INTRT are skewed to the right. The probability values of Jarque Bera reveal that RGDP, CBSME and INTRT are normally distributed as their p values are greater than 5 percent level. However, the probability values of NSMES and SMEEG which is 0.0000 and 0.0000 respectively, shows that NSMES and SMEEG are not normally distributed.

4.2. Stationarity Test

A test of stationarity is necessary to ensure that the estimates produce consistent, robust and reliable results. In this study, ADF unit root test was used and the result is presented in Table 2.

Table 2: Summary of the ADF Unit Root Test

| Variables | ADF Stat | Critical Value @5% | Order of Integration | P Values | Remarks |

| RGDP | -4.0216 | -3.0124 | I(0) | 0.0000 | Stationary |

| NSMES | -3.7506 | -3.0207 | I(1) | 0.0000 | Stationary |

| CBSME | -4.2603 | -3.0207 | I(1) | 0.0000 | Stationary |

| SMEEG | -4.5377 | -3.0207 | I(1) | 0.0000 | Stationary |

| INTRT | -3.4873 | -3.0207 | I(1) | 0.0008 | Stationary |

Source: Eviews 10.0 Output

Table 2 presents the summary of the results of unit root test carried out for this study. The result shows that NSMES, CBSME, SMEEG and INTRT are stationary at first difference while RGDP is stationary at level. This means that NSMES, CBSME, SMEEG and INTRT are integrated of order one, that is, I(1) while RGDP is integrated of order zero, that is, I(0). It is then concluded that all the variables are stationary and the null hypothesis of no stationarity is rejected. Due to this mixed order of integration, the ARDL Bounds test is required.

4.3. Lag Length Selection

To select the appropriate lag length for the variables of the model, the VAR lag selection criteria was employed and the result is presented in Table 3.

Table 3: Summary of VAR Lag Selection Result

| VAR Lag Order Selection Criteria | ||||||

| Endogenous variables: RGDP NSMES CBSME SMEEG INTRT | ||||||

| Exogenous variables: C | ||||||

| Date: 02/20/23 Time: 18:00 | ||||||

| Sample: 1999 2020 | ||||||

| Included observations: 21 | ||||||

| Lag | LogL | LR | FPE | AIC | SC | HQ |

| 0 | 53.98866 | NA | 6.48e-09 | -4.665587 | -4.416891 | -4.611614 |

| 1 | 158.2839 | 148.9932* | 3.69e-12* | -12.21752* | -10.72534* | -11.89368* |

| * indicates lag order selected by the criterion | ||||||

Source: Eviews 10.0 Output

From the result in Table 3, the appropriate lag length is one since all the criteria chose lag one. Thus, this study chose lag one as the appropriate lag length.

4.4. Cointegration Test

After ascertain that the variables are integrated of order one and order zero, the ARDL Bounds test for cointegration was employed to check the long run relationship among the variables. The result is thus presented in Table 4.

Table 4: Summary of ARDL Bounds Testing for Cointegration

| ARDL Bounds Test | ||

| Date: 02/20/23 Time: 18:28 | ||

| Sample: 2000 2020 | ||

| Included observations: 21 | ||

| Null Hypothesis: No long-run relationships exist | ||

| Test Statistic | Value | K |

| F-statistic | 2.730455 | 4 |

| Critical Value Bounds | ||

| Significance | I0 Bound | I1 Bound |

| 10% | 2.45 | 3.52 |

| 5% | 2.86 | 4.01 |

| 2.5% | 3.25 | 4.49 |

| 1% | 3.74 | 5.06 |

| Source: Researcher’s Computation Using Eviews 10. | ||

Source: Eviews 10.0 Output

From Table 4, the value of the F-statistic is 2.730455. This shows that the value is lower than the critical value bonds at 5 percent level of significance. Therefore, the study concludes that there exists no long run relationship among NSMES, CBSME, SMEEG and INTRT. Based on this, the null hypothesis of no cointegration is accepted. Thus, the study estimates the short run ARDL model.

4.5. Autoregressive Distributed Lag Model

Since there is no long run relationship among the variables, the short run ARDL was conducted and the result is shown in Table 5.

Table 5: Summary of ARDL Result

| Dependent Variable: D(RGDP) | ||||

| Method: Least Squares | ||||

| Date: 05/22/23 Time: 10:57 | ||||

| Sample (adjusted): 2001 2020 | ||||

| Included observations: 20 after adjustments | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | -0.006718 | 0.006256 | -1.073848 | 0.3024 |

| D (RGDP (-1)) | 1.356750 | 0.250412 | 5.418059 | 0.0001 |

| D (NSMES (-1)) | 0.115693 | 0.052740 | 2.193626 | 0.0470 |

| D (SMEEG (-1)) | -1.888779 | 2.594639 | -0.727954 | 0.4795 |

| D (CBSME (-1)) | 0.001651 | 0.010865 | 0.151935 | 0.8816 |

| D (INTRT (-1)) | 0.002313 | 0.001556 | 1.486588 | 0.1610 |

| ECM (-1) | -1.184689 | 0.315979 | -3.749260 | 0.0024 |

| R-squared | 0.734542 | Mean dependent var | 0.022234 | |

| Adjusted R-squared | 0.612023 | S.D. dependent var | 0.016390 | |

| S.E. of regression | 0.010209 | Akaike info criterion | -6.061907 | |

| Sum squared resid | 0.001355 | Schwarz criterion | -5.713401 | |

| Log likelihood | 67.61907 | Hannan-Quinn criter. | -5.993875 | |

| F-statistic | 5.995330 | Durbin-Watson stat | 2.250438 | |

| Prob(F-statistic) | 0.003412 | |||

Source: Eviews 10.0 Output.

The short run estimate is presented in Table 5 and the coefficient of the lagged value of NSMES exerts a positive value of 0.1157. This implies that 1 percent increase in NSMES will increase RGDP by 0.12 percent. This finding conforms to the a priori expectation because having more people operating SMEs businesses should help reduce unemployment level, increase productivity, reduce poverty rate and enhance economic growth. However, the variable is statistically insignificant at 5 percent level This finding supports the findings of Oluyemi and Ayodele (2021) who found a positive impact of SMEs formation on economic growth in Nigeria.

The coefficient of one period lagged of Credit to SMEs (CBSME) is 0.0017 and it implies that 1 percent increase in CBSME will increase RGDP by 0.0017 percent. The implication of this small percentage is that commercial banks have not been given enough credits to SMEs. Even, the rate at which they give out loan is too high for businesses to cope. This has not helped the SMEs to grow and the resultant effect is low contributions to employment generation and economic growth in Nigeria. The variable conforms to a priori expectation because it is expected that commercial banks credit to the SMEs should grow the businesses of the SMEs. This study’s finding is in line with the findings of Mairiga et al (2021).

The coefficient of one period lagged of SMEs employment generation (SMEEG) is -1.8888, meaning that SMEEG has a negative impact on the economic growth. The implication of this negative value implies that a percentage increase in SMEEG will have a negative effect on economic growth by reducing the value of the real gross domestic product by approximately 1.89 percent. This shows that SMEEG is not a contributing factor to the growth of the economy. The finding does not conform to the a priori expectation and also contrasts the finding of Oluyemi and Ayodele (2021) on the impact of SMEs on economic growth in Nigeria.

The coefficient of interest rate (INTRT) stands at 0.0023. This shows that the variable has a positive impact on economic growth. This implies that 1 percent increase in interest rate will lead to approximately 0.023 percent increase in real gross domestic product. This finding does not conform to the a priori expectation because any further increase in interest rate would discourage SMEs to borrow money from bank and the effects would be reduction in the number of SMEs operating in the country, low employment generation and reduced output. This finding is not in support of the findings of Mairiga et al (2021) who found a negative impact of lending interest rate on economic growth.

Furthermore, the R2 which shows the goodness of fit is 0.7345. This suggests that about 73 percent variation in economic growth can be explained by Number of SMEs (NSMES), Commercial Banks Credit to SMEs (CBSME), Interest Rate (INTRT), and SMEs Employment Generation (SMEEG). The remaining 27 percent can be attributed to other variables which influence the economic growth but not explicitly captured in the model. The error correcting term of -1.1847 indicates that 1.18 percent disequilibrium in the previous years will be corrected for in the current year. The ECM is correctly signed and statistically significant.

The probability value of F-statistic which is 0.0034 means that the variables (NSMES, CBSME, SMEEG and INTRT are jointly statistically significant at 5 percent level. The DW statistic of 2.25 is approximately 2 and it suggests that the model is free from autocorrelation.

4.6. Post Estimation Tests

Table 6. Summary of Serial Correlation Test

| Breusch-Godfrey Serial Correlation LM Test: | |||

| F-statistic | 0.739985 | Prob. F (1,12) | 0.4065 |

| Obs*R-squared | 1.219757 | Prob. Chi-Square (1) | 0.2694 |

Source: Eviews 10.0 Output

The result of the serial correlation test shows that the model is free from serial correlation since the probability value of F-statistics of is greater than the critical value at 5 percent. This makes the study to accept the null hypothesis which states that there is no serial correlation in the model.

4.7: Test for Heteroscedasticity

Table 7: Summary of Heteroscedasticity Result

| Heteroskedasticity Test: Breusch-Pagan-Godfrey | |||

| F-statistic | 1.057636 | Prob. F (7,13) | 0.4405 |

| Obs*R-squared | 7.619912 | Prob. Chi-Square (7) | 0.3673 |

| Scaled explained SS | 3.210814 | Prob. Chi-Square (7) | 0.8648 |

Source: Eviews 10.0 Output

From the result in Table 7, the calculated F-test statistic of 0.4405 is greater than the 0.05 level of significance. This implies that there is no heteroscedasticity in the model. As such, the null hypothesis which states that there is no heteroscedasticity in the residuals is accepted. Consequently, the data is reliable for predication.

Test for Normality

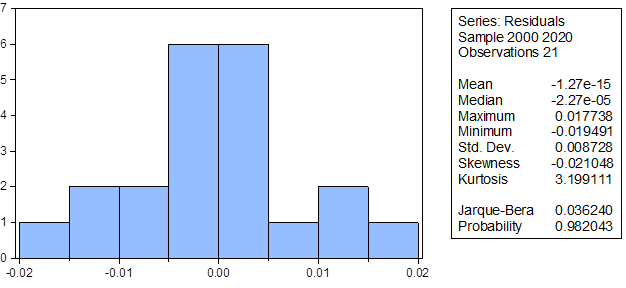

Figure 1: Histogram Normality Test

Source: Eviews 10.0 Output

The result in Figure 1 shows that the probability value of Jaque-Bera is 0.9820. This is greater than the critical value at 5 percent level of significance and it suggests that our residual is normally distributed based on the decision rule which states that the null hypothesis should be accepted if the Prob(Jaque-Bera) is greater than 0.05. The study therefore accepts the null hypothesis that the residual is normally distributed.

CONCLUSION AND POLICY RECOMMENDATIONS

5.1. Conclusion

This study examines the impact of SMEs on economic growth in Nigeria for the period of 22 years (1999-2020), using ARDL model. A unit root test, using Augmented Dickey-Fuller, was carried out on the time series data to ensure stationarity of the variables. Then, ARDL Bounds test for co-integration was employed since the variables exhibit mixed order of integration. After ascertaining that the variables are co-integrated, ARDL Model was carried out to estimate the parameters of the model. Some diagnostic tests were also carried out to ensure reliability, validity and consistency of the model.

From the findings, the Augmented Dickey-Fuller test shows that NSMES, CBSME and INTRT were stationary after their first difference, while RGDP was stationary at level. The co-integration test carried out using ARDL bounds test reveals that there is no long-run relationship between the variables. This outcome therefore makes it necessary to use short run ARDL. The result of ARDL shows that NSMES, CBSME and INTRT have positive impact on economic growth while SMEEG has negative impact. It further shows that only NSMES is statistically significant at 5 percent level. The study reveals that the variables of this model can be used to predict economic situation in Nigeria based on the high R2 of 0.73. The result of Durbin Watson statistic also shows that the model is free from autocorrelation. The study therefore concludes that SMEs are important drivers of economic growth of any nation, even in Nigeria.

5.2. Policy Recommendations

- Government should create enabling environments for the SMEs. This would encourage innovators/investors to invest in Nigeria and the number of SMEs would increase. Even, the issue of unemployment will be solved to a large extent because there will be employment opportunities in different fields.

- Commercial banks should encourage financial inclusion, that is, SMEs should be given easy access to loans. This can go a long way to help investors bring their ideas into reality as we know that capital is the major determining factor in any business plan.

- There should also be a reduction in the rate of interest because high interest rate can deter aspiring SMEs. Banks should as well give reasonable collateral conditions to business owners so as to access loans easily.

ACKNOWLEDGMENT

The paper is the independent work of the authors and the authors assume the full responsibility of the ideas expressed here.

REFERENCES

- Aladin, A., Evada, D., Yuliana, S., & Yuli, A.A. (2021). The role of small and medium enterprises and economic growth in Indonesia: The VECM analysis. Atlantis Highlights in Social Sciences, Education and Humanities, 1, 95-99.

- Ameh, P.O., Alao, M.M., & Amiya, B. (2020). Effect of small and medium enterprises on Nigeria’s economy. World Journal of Innovative Research (WJIR), 8(3), 87-92.

- Bello, A., Jibir, A, & Ahmed, I. (2018). Impact of small and medium scale enterprises on economic growth: Evidence from Nigeria. Global Journal of Economics and Business, 4(2), 236-244.

- Emmanuel, I. J. & Willie, E.E. (2021). Small and medium scale enterprises and economic growth in Nigeria. IAR Journal of Business Management, 2(1), 38-43.

- Grisejda, M., & Krisdela, K. (2016). Impact of SMEs in economic growth in Albania. European Journal of Sustainable Development, 5(3), 151-158.

- Lyndon, M.E. & Opinion, B.L. (2021). An evaluation of the impact of SMEs development on economic growth in Nigeria. International Journal of Small Business and Entrepreneurship Research, 9(1), 54-70.

- Mairiga, H.T., Ibrahim, A., & Babawulle, D.H. (2021). Small and medium enterprises performance and economic growth nexus in Nigeria: ARDL Bounds testing evidence. Asian Journal of Economics, Finance and Management, 5(3), 33-54.

- NBS/SMEDAN (2017). National survey of micro, small and medium enterprises 2017.

- National Bureau of Statistics (2021). Micro, Small and Medium Enterprises survey report. https://nigerianstat.gov.ng/elibrary/read/966

- Offor, S.U. (2012). The impact of small and medium scale industries on the economic growth of Nigeria. A project submitted to the Department of Economics, Faculty of Social Sciences, Caritas University, Enugu State, Nigeria.

- Opafunso, Z.O., & Adepoju, O.O. (2014). The impact of SMEs on economic development of Ekiti State, Nigeria. Journal of Economics and Sustainable Development, 5(16), 115-122.

- Penrose, E.T. (1959). The theory of the growth of the firm. John Wiley.

- Oluyemi, T.A. & Ayodele, I.S. (2021). Small-medium enterprise formation and Nigerian economic growth. Review of Economics and Political Science, 7(4), 286-301.

- Price water house Cooper (2020). PwC’s MSME Survey 2020: Nigeria Report. pwc.com/ng

- Taiwo, M.A., Ayodeji, A.M., & Yusuf, B.A (2012). Impact of small and medium enterprises on economic growth and development. American Journal of Business and Management, 1(1), 18-22.

- World Bank (2023). Small and Medium Scale Enterprises Finance. https://www.worldbank.org