Domestic Debt, Price Stability and Economic Growth in Nigeria

- Nkemjika Nwosu.

- Uduakobong Sammy Inam.

- Paul Atanda Orebiyi

- 648-662

- Aug 1, 2024

- Economics

Domestic Debt, Price Stability and Economic Growth in Nigeria

Nkemjika Nwosu., Uduakobong Sammy Inam., Paul Atanda Orebiyi

Department of Economics, University of Uyo, Ikpa Road, PMB 1017, Akwa Ibom State, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.807054

Received: 14 June 2024; Accepted: 24 June 2024; Published: 01 August 2024

ABSTRACT

This study analyses the relationship between domestic debt, price stability and economic growth in Nigeria using annual data covering the period 1980 to 2023. Specifically, the study investigates the long and short run effects of domestic debt on price stability and economic growth in Nigeria. The study employs the Auto- Regressive Distributed Lag (ARDL) technique and the Granger Causality test. The results reveal that domestic debt has an indirect, but insignificant impact on economic growth in the long run and indirect and significant relationship in the short run. There are no causal relations between domestic debt, inflation and economic growth in Nigeria. The study recommends that domestic debt should be invested in productive sectors of the economy and more specifically in the real sector to create employment and reduce poverty incidence in the country. Furthermore, there should be proper formulation and implementation measures that would keep the inflation rate at a level that would not have adverse effects both in the short and long runs. Also, Government and relevant monetary authorities should adopt a suitable exchange rate policy that will allow for a realistic and stable exchange rate to enhance output performance.

Keywords: Domestic Debt, Price Stability, Economic Growth, Auto- Regressive Distributed Lag (ARDL), Nigeria.

JEL Classification: H63, H6, D49, F43

INTRODUCTION

The debt structure of a nation exerts a profound influence on numerous facets of its economy, spanning from capital accumulation to economic growth, and from income to employment stability. This complex interplay presents both challenges and opportunities for economic management by authorities. Nigeria’s domestic debt crisis, for instance, has wrought havoc, driving up inflation amidst declining real incomes, burgeoning budgetary deficits, and the erosion of social services and infrastructure (Nnol, 2003).

Despite these social costs, debt can serve as a strategic instrument for economic advancement. Government can finance important development initiatives, boost economic growth, and make investments in infrastructure, health care and education by borrowing money. Such investment can catalyze growth, enhance productivity, and foster long-term prosperity. Moreover, judicious debt utilization can facilitate the acquisition of technological expertise, attract foreign investment, and bolster the competitiveness of domestic industries.

Consequently, debt can be wielded as a potent tool for achieving developmental objectives and overcoming socio-economic challenges (Onwioduokit, 2012). However, in order to maximize its benefits and minimize its risks, careful debt management is essential. Government must place a high priority on accountability, sustainability, and transparency in borrowing practices to avert fiscal crises and ensure optimal utilization of borrowed funds for transformative purposes. By striking a delicate balance between debt accumulation and economic growth, nations can navigate the complexities of debt dynamics to achieve sustainable development and shared prosperity.

The classical principles of loan finance elucidate the rationale behind loans, emphasizing their role in promoting inter-generational equity, implementing a pay-as-you-use approach, fostering capital formation, providing old-age insurance, supporting self-liquidating projects, adjusting distribution, and reducing tax friction. Essentially, government borrowing becomes imperative when conventional revenue sources such as taxes and non-tax revenues prove insufficient to finance government expenditures. Such borrowing can originate from internal and/or external sources, aiming to bolster domestic investment and thereby catalyze economic growth and development.

No contention arises when a country resorts to borrowing, provided the borrowed funds are channeled into productive endeavors that facilitate the eventual servicing and liquidation of the debt. Borrowing emerges as a second-best alternative to money creation during periods of unemployment, serving as a vital instrument for economic management. Domestic loans serve as a mechanism for bridging domestic savings gaps, especially amid dwindling government revenues from domestic sources, exacerbated by volatile prices of primary commodity exports and diminishing foreign exchange earnings.

Governments grappling with substantial recurrent budget deficits may find themselves compelled to address these gaps by tapping into domestic savings, often through the issuance of domestic debt. Despite these theoretical underpinnings, the impact of debt borrowing in Nigeria has not been markedly significant. The intended benefits of borrowing, such as accelerating economic growth and development, have not materialized to the anticipated extent. Factors such as mismanagement of borrowed funds, corruption, inadequate infrastructure, and inefficient utilization of resources have hindered the transformative potential of debt borrowing in Nigeria, underscoring the importance of prudent debt management and effective utilization of borrowed funds to realize desired developmental outcomes. Additionally, domestic debt can initially exert a positive impact on economic growth in the short term.

However, over the long term, if the repayment obligations of the debt surpass the nation’s capacity to pay, there’s a risk of encountering a phenomenon known as debt overhang. This scenario unfolds when the debt service repayment obligations become burdensome, potentially exceeding the country’s ability to meet them with a certain probability. As debt overhang takes hold, the interest payments on the debt may surpass the principal, exacerbating the financial strain. Consequently, the overall effect on the economy turns negative.

At this critical juncture, a phenomenon called “crowding-out” emerges, wherein the government’s heavy debt burden restricts the availability of funds for private investment. This crowding-out effect is compounded by capital shortages, constraining the private sector’s ability to access the necessary resources for expansion and innovation, thereby hampering overall economic growth and development. In Nigeria, besides the factors already identified as contributing to the shifting domestic debt landscape—such as substantial budget deficits, sluggish output growth, rapid expenditure expansion, elevated inflation, and a limited revenue base—other factors come into play. These include oil shocks, manifested in price fluctuations, and the nation’s reliance on a single commodity economy due to a lack of diversification and the failure to expand non-traditional exports.

Consequently, in line with the fiscal theory of price level, domestic debt is implicated in inflation dynamics, with its impact lying not solely in the existence of the debt itself, but rather in the costs associated with it influencing the inflation rate. The interest rates accompanying domestic debt play a crucial role in determining the price level through intertemporal budget valuation. Conversely, high interest rates can exacerbate inflationary pressures, particularly during periods of high or hyperinflation in emerging economies.

The inflationary spirals which had been experienced by many emerging countries could be explained by the cost of domestic debt. Countries experiencing inflationary periods follow interest rate policies resulting from tight money policies, which increase domestic borrowing even further; decreasing maturity and increasing budget deficits. During the process, further rises in interest payments amplify domestic debt stock. The fact that, refinancing of debt by borrowing more lead budget constraint to deteriorate which resulted from continuing Ponzi game in fiscal policies.

Moreover, as domestic debt rises and maturity rates decline, an inflationary spiral becomes virtually inevitable due to wealth effects. If rational agents anticipate that the government’s response to domestic debt through primary surpluses is inefficient, the only equilibrium for the price level entails a trajectory of escalating inflation. This inflationary pressure triggers subsequent hikes in nominal interest rates and diminishes seigniorage. Consequently, the escalation of domestic debt is bound to precipitate economic turmoil through these same channels.

The rationale behind the creation of domestic debt in economically disadvantaged nations lies in its potential to stimulate the development of robust and liquid internal financial markets, shield countries from adverse external shocks, and mitigate foreign exchange risks (Del, 2003; Aizenman, 2004; Kumhof, 2005). Moreover, domestic debt can incentivize risky private sector investments by safeguarding bank balance sheets and profitability (Barajas, 1999; 2000), thereby fostering more efficient investments compared to those associated with lower risk. However, the primary concern regarding domestic debt centers on its crowding-out effect on private investment. When governments borrow domestically, they tap into domestic private savings that might otherwise have been available for private sector lending. Consequently, a diminished pool of loanable funds in the market drives up the cost of capital for private borrowers, dampening private investment demand, capital accumulation, economic growth, and overall welfare (Diamond, 1965). Additionally, domestic debt is often perceived as costlier than concessional external financing (Burguet, 1998), potentially leading to a scenario where interest payments on domestic debt consume significant government revenues, thereby displacing pro-poor and growth-enhancing expenditures. Economic theory suggests that moderate levels of borrowing, whether sourced domestically or externally, can potentially bolster the economic growth trajectory of developing nations.

Countries in the nascent stages of development typically possess a limited capital stock and are prone to encountering investment opportunities offering returns surpassing those found in more developed economies. However, Nigeria deviates from this pattern, as its domestic debt fails to yield a substantial impact on economic growth. Ideally, sustained economic growth enables timely debt repayment and fosters a virtuous cycle. As growth persists over time, it tends to elevate per capita income, which, in turn, serves as a catalyst for poverty reduction initiatives. This positive correlation between growth and poverty alleviation underscores the importance of nurturing an environment conducive to sustained economic expansion. Despite the theoretical expectations, Nigeria’s experience diverges, revealing a disconnect between domestic debt accumulation and its influence on economic growth. Factors such as inefficient allocation of borrowed funds, structural impediments, governance challenges, and macroeconomic instability may contribute to this disparity, highlighting the need for targeted reforms and prudent debt management strategies to align domestic borrowing practices with the imperatives of sustainable economic development and poverty reduction. An examination of Nigeria’s domestic debt reveals a consistent upward trend in recent years. Several factors contribute to this notable escalation. Firstly, there’s the heightened demand for government financing to address developmental objectives and various socio-economic priorities, predating the era of the oil boom. Additionally, there’s the imperative to bridge the substantial fiscal deficits ensuing from the post-oil boom period. Furthermore, financing gaps within the government’s revenue-expenditure framework, along with other funding requirements, have also propelled the expansion of Nigeria’s domestic debt stock.

Despite the persistent reliance on domestic borrowing, Nigeria’s economy remains marked by low per capita income, elevated unemployment rates, sluggish economic growth, inadequate public amenities, and deficient infrastructure development. These challenges persist despite the expectation that public funds obtained through domestic loans would address them. Paradoxically, the extent of Nigeria’s appetite for domestic borrowing appears disproportionate to the country’s modest economic growth, rising price levels, and developmental aspirations.

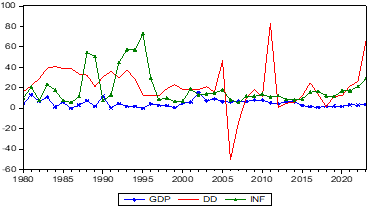

Figure 1: Trends in Gross Domestic Product, Domestic Debt and Inflation Rate in Nigeria from (1980 – 2023)

Source: Central Bank of Nigeria Statistical Bulletin (various issues)

From the above graph domestic debt, inflation rate, and economic growth in Nigeria showed a sign of volatility throughout out the study year. One significant factor contributing to this fluctuation in GDP is the country’s heavy reliance on oil exports. The global oil market fluctuations directly impact Nigeria’s economy, leading to unstable GDP growth rates. Additionally, external debt burdens and inadequate infrastructure development have posed challenges to economic stability, impacting GDP performance negatively. Aside other years like 1981, 1983, 1993 and 1994 the country experienced a negative GDP, specifically, in 1995, Nigeria experienced a significant downturn in its Gross Domestic Product (GDP), leading to negative economic growth. In 1995, global oil prices plummeted due to oversupply and weakened demand. This sharp decrease directly impacted Nigeria’s revenue from oil exports, leading to a substantial reduction in its GDP. Additionally, structural adjustment programs imposed by international financial institutions also influenced Nigeria’s negative GDP. These programs required the country to implement austerity measures and liberalize its economy. While these reforms aimed at long-term benefits such as improved efficiency and competitiveness, they initially led to economic contraction and negatively impacted the GDP. Nigeria, a prominent African economy, faced challenges leading to negative GDP growth in both 2016 and 2020. In 2016, Nigeria experienced a recession due to the significant drop in global oil prices. As an oil-dependent economy, the decline severely impacted government revenue and foreign exchange earnings. This led to reduced investment and consumer spending, ultimately resulting in negative GDP growth. Similarly, in 2020, Nigeria encountered another economic setback primarily caused by the COVID-19 pandemic. The pandemic disrupted global trade and led to a sharp decline in oil demand and prices. This had adverse effects on Nigeria’s export earnings and fiscal stability. From 2021 to 2023 Nigeria’s economic growth rate has become stable to an extent.

Furthermore, from the graph inflation rate has been volatile. Hence, this volatility has been affecting the economy. Its effect includes reduced purchasing power, increased uncertainty and risk, reduced government control, increased poverty and income inequality, and reduced confidence in the monetary system. However, these has affected the state of the economy. Nevertheless, from the graph above, Nigeria has experienced a significant increase in domestic debt from 1980 to date, and several factors have contributed to this surge. One of the primary reasons for this escalation is the country’s over-reliance on borrowing to finance budget deficits. The persistent gap between government revenue and expenditure has led to increased borrowing, resulting in a mounting domestic debt.

Hence, this study aims to elucidate the intricate dynamics between domestic debt, price stability, and economic growth in Nigeria, spanning the period from 1980 to 2023. It seeks to unravel the nuanced relationships and causalities underlying these variables. Specifically, the research endeavors to discern both the long-term and short-term impacts of domestic debt on inflation and growth within the Nigerian context. Furthermore, it endeavors to shed light on the nature and direction of causality between domestic debt, price stability, and economic growth.

By analyzing annual data over this extensive time frame, the study aims to provide valuable insights into the interplay among these crucial economic factors, thereby contributing to a deeper understanding of Nigeria’s economic landscape. This article delves into the complex relationship between domestic debt, price stability, and economic growth in Nigeria, providing insights crucial for economic policymaking and development strategies. Aside from this introductory section, Section 2 examines Theoretical and Related Empirical Literature, followed by Section 3, which outlines the Research Methodology. Section 4 presents the findings, while Section 5 encapsulates the Summary, Conclusions, and Recommendations

LITERATURE REVIEW

2.1 Theoretical Framework.

There are several theories on the subject of domestic debt, price stability and economic growth. However, for the purpose of this paper, the relevant theories are Learner’s Theory of Domestic Debt and new growth theory. Proponents of the new growth theory, including Romer (1995), have advanced an extension of the neoclassical theory to offer insights into the dynamics of economic growth. Building upon the foundations of neoclassical economics, the new growth theory maintains that output expansion stems from a combination of factors, notably increases in labor quantity and quality through population growth and education, augmented capital accumulation through savings and investment, and advancements in technology.

In contrast to the neoclassical model, which emphasizes the role of capital accumulation in driving medium-term economic growth, the new growth theory introduces a nuanced perspective. While acknowledging the importance of capital accumulation, the new growth theory suggests that steady-state growth is ultimately constrained by the rate of growth of the labor force. This insight highlights the interplay between labor dynamics and capital accumulation in shaping long-term economic growth trajectories.

The neoclassical model typically employs an aggregate production function characterized by constant returns to scale in labor and reproducible capital. This functional form serves as a foundational framework for analyzing the determinants of economic growth within the neoclassical paradigm.

Y = F (K, L) (1)

Where,

Y is output (or income), K is the stock of capital while L is the labour force. The function explains the output, Y under a given state of knowledge with a given range of available techniques and a given array of different capital, intermediate goods and consumption goods. With constant returns to scale, labour productivity measured by output per worker

y = Y/L (2)

Will depend on the capital stock per worker (i.e. capital intensity, k =K/L).

In the new growth theory, the rate of technological progress is made an endogenous factor. Having the model,

Y= F (K, N, A) (3)

Where,

Y is output, K represents capital; N represents labour and A represents technology.

2.2 Empirical Literature Review

Several studies have empirically investigated the relationship between domestic debt price stability and economic growth in most countries of the world. Some studies revealed a positive relationship between domestic debt, rice stability and economic growth. For instance, see Peter, Denis and Chukwuedo (2013), Igbodika, Jessies and Andabai (2016), Ayuba and Khan (2019), Maana, Owino and Mutai (2008), Sheikh, Faridi and Tariq (2010), Putunoi and Mutuku (2013), Umaru, Hamidu and Musa (2013)), Babu, Kiprop, Kaliol and Gisore (2015), Muhammed, Olaola, Abu and Umar (2021).

On the contrary, some studies reveal a negative relationship between domestic debt, rice stability and economic growth. For instance, see Adofu and Abula (2010), Islam (2012), Ozolina, Aruna and Kormay (2017), Odior and Arinze (2017), Peter et al (2013), Ayuba and Khan (2019), Okwu, Obiwuru and Oluwalaiye (2016) and Abula and Ben (2016).

RESEARCH METHODOLOGY

3.1 Nature and Sources of Data

Data used for this study are secondary in nature. They are annual time series data obtained from sources such as: Central Bank of Nigeria Statistical Bulletin (various issues) and National Bureau of Statistics publication of various issues. The data employed the spanned the period 1980-2023.

3.2 Model Specification

To the best of our knowledge, there seems to be paucity literature that have developed a model that addresses domestic debt dynamics, price stability and economic growth directly. However, works including Ahmad, Sheikh and Tariq (2012) have attempted the theorizing of domestic debt and Inflationary effects although in Pakistan. We will attempt the extension of the works Mba, Yuni and Oburota (2013) and Ayuba and khan (2019) to specify the model.

Economic Growthi=β0+β1⋅Domestic Debti+β2⋅Inflationi+β3⋅Unemploymenti+β4⋅Fiscal Deficiti+β5Exchange Ratei+β6⋅Money Supplyi+β7⋅Interest Ratei+ui

Where:

- EconomicGrowthi is the dependent variable representing the economic growth rate in period i.

- DomesticDebti represents the level of domestic debt in period i.

- Inflationi represents the inflation rate in period i.

- Unemploymenti represents the unemployment rate in period i.

- FiscalDeficiti represents the fiscal deficit as a percentage of GDP in period i.

- ExchangeRatei represents the exchange rate in period i.

- MoneySupplyi represents the money supply in period i.

- InterestRatei represents the interest rate in period i.

- β0 is the intercept term.

- β1 to β7 are the coefficients of the independent variables.

- ui is the error term capturing unobserved factors influencing economic growth in period i.

This model allows us to analyze the impact of domestic debt dynamics, price stability (proxied by inflation), and other important macroeconomic variables on economic growth in Nigeria. By estimating the coefficients (β1 to β7), we can assess the magnitude and significance of each variable’s effect on economic growth while controlling for other factors.

3.3 Analytical Technique

The analytical techniques employed for the purpose of this study is based on the specific objectives of the study.

Objective One: To examine the long and short run relationships between domestic debt dynamics, price stability and growth in Nigeria, the Auto Regressive Distributed Lag (ARDL) model was employed.

3.3.a The Auto Regressive Distributed Lag (ARDL)

The Auto Regressive Distributed Lag (ARDL) Model which uses a bounds test approach based on unrestricted error correction model (UECM) was employed here to measure the connection between fiscal deficit and inflation and to test for a long run relationship among the relevant variables. This model was developed by Pesaran and Pesaran (1997) and used by Pesaran, et al (2001). The main advantage of this approach lies in the fact that it can be applied irrespective of whether the variables are I (0) or I (1).

This approach also allows for the model to take a sufficient number lags to capture the data generating process in a general-to-specific modelling framework. Also, it provides very efficient and consistent test results in small and large sample sizes (Pesaran et al., 2001).

Following Shrestha and Chowdhury (2007), to illustrate the ARDL modelling approach, the unrestricted error correction model of the three equations is stated below:

n n n n n

ΔGDPt = α0 + Ʃα1 ΔGDPt-1 + Ʃα2 ΔlnDDt-1 + Ʃα3 ΔInUNEMPt-1 + Ʃα4 ΔlnEXRt-1 + Ʃα5 ΔInFD t-1

i=1 i=1 i=1 i=1 i=1

n n n

Ʃ α6 ΔInLIR t-1 + Ʃ α7 ΔInINF t-1 + Ʃ α8 ΔInMSt-1 δ1INFt-1 + δ2lnDDt-1 + δ3UNEMPt-1 +δ4EXRt-1

I=1 i=1 + δ5LIRt-1 + δ6FDt-1 + δ7MSt-1 εt-1…………… (4)

Having done this, there is also the need to perform a series of diagnostic tests on the stochastic properties established model. This is because the existence of a long run relationship does not necessarily imply that the estimated coefficients are stable (Bahmani- Oskooee and Brooks, 1999). This therefore, involves testing of the residuals (that is homoscedasticity, non- serial correlation, etc), as well as normality tests to ensure that the estimated model is statistically robust.

It Is also pertinent to note here that one of the arguments against the ARDL is that the estimators will be inefficient and biased (or even inconsistent) in the presence of auto correlation of the disturbances. However, Pesaran and Shin (1999) show that appropriately modifying the orders of the ARDL model is adequate to simultaneously correct for residual serial correlation and the problem of endogenous regressors, thus giving ARDL an advantage over other approaches to Cointegration.

In addition, Pesaran and Shin (1999), argue that endogeneity problems are addressed in this technique by modeling the ARDL with the appropriate lags, thus correcting for both serial correlation and endogeneity problems. Jalil et al (2008) in their study also show that endogeneity is less of a problem if the estimated ARDL model is free of serial correlation. In this approach, Khan el al, (2005) equally argue that where all the variables are assumed to be endogenous, the long run and short run parameters of the model can be estimated simultaneously.

Objective Two: To examine the causal relationship between domestic debt on price stability and economic growth in Nigeria the Granger causality test was employed.

3.3b The Granger causality test

The Granger causality test states that the cause and effect relationship is that the past value should affect the present value. The Granger causality equations for the purpose of this study are specified thus:

Model 1:

n n

GDPt = ƩαiDDt-1 + ƩBj GDPt-1 Uit ………………… (5)

i=1 j=1

n n

DDt = ƩαiGDPt-1 + ƩBj DDt-1 Uit ………………… (6)

i=1 j=1

The GDPt is affected by the past values of DD and GDP. DD is affected by past values of GDP and DD. The test is conducted by regressing the current GDP on all lagged value of GDP but not DD because it is being tested for causation. By this, we will obtain the RSSr. Afterwards, we regress the current GDP on its past value and the lagged values of DD, to obtain the unrestricted residual sum of squares.

The decision rule is that if αi = 0, then DDt-1 does not granger cause changes in GDPt. if δj=0 then GDPt-1 does not granger cause changes in DDt. Thereafter, the F-test is being applied. (RSSr–- RSSur)/m * N – K/RSSur. Where M represents the number of lagged terms. If Fcomp > Ftab at a chosen significant level, then the lagged values of the DDt causes changes in GDPt. To determine m, we use the AIC or SIC = nk/nEu2/n = nk/n RSS/n.

Model 2:

n n

INFt = ƩαiDDt-1 + ƩBj INFt-1 Uit ………… (5)

i=1 j=1

n n

DDt = ƩαiINFt-1 + ƩBj DDt-1 Uit ………… (6)

i=1 j=1

The INFt is affected by the past values of DD and INF. DD is affected by past values of INF and DD. The test is conducted by regressing the current INF on all lagged value of INF but not DD because it is being tested for causation. By this, we will obtain the RSSr. Afterwards, we regress the current INF on its past value and the lagged values of DD, to obtain the unrestricted residual sum of squares.

The decision rule is that if αi = 0, then DDt-1 does not granger cause changes in INFt. if δj=0 then INFt-1 does not granger cause changes in DDt. Thereafter, the F-test is being applied. (RSSr–- RSSur)/m * N – K/RSSur. Where M represents the number of lagged terms. If Fcomp > Ftab at a chosen significant level, then the lagged values of the DDt causes changes in INFt. To determine m, we use the AIC or SIC = nk/nEu2/n = nk/n RSS/n.

ANALYSIS OF RESULTS

We began our empirical assessment with some preliminary checks beginning with the descriptive statistics and then the unit roots tests. The outcomes are reported in Tables 4A and 4B respectively.

Table 1A: Descriptive Statistics

| Inflation Rate | Fiscal Deficit | GDP Growth Rate | Domestic Debt | Exchange Rate | Broad Money Supply | Lendig Interest Rate | UEMP | |

| Mean | 17.01 | 1297.76 | 3.01 | 18.78 | 116.24 | 22.96 | 17.27 | 3.10 |

| Median | 13.30 | 198.80 | 3.30 | 18.95 | 115.20 | 19.10 | 16.90 | 3.81 |

| Maximum | 75.40 | 6404.70 | 15.30 | 21.10 | 448.80 | 87.70 | 31.60 | 6.00 |

| Minimum | 0.60 | -861.40 | -13.10 | 12.30 | 0.60 | -0.70 | 8.90 | 0.00 |

| Std. Dev. | 14.04 | 1914.38 | 5.29 | 6.40 | 120.68 | 17.60 | 4.81 | 1.93 |

| Skewness | 2.12 | 1.32 | -0.82 | -0.04 | 1.07 | 1.50 | 0.36 | -0.77 |

| Kurtosis | 8.69 | 3.57 | 4.74 | 1.50 | 3.40 | 5.97 | 3.60 | 2.21 |

| Jarque-Bera | 88.26 | 12.84 | 10.14 | 0.28 | 8.32 | 31.38 | 1.54 | 5.37 |

| Probability | 0.00 | 0.00 | 0.00 | 0.86 | 0.01 | 0.00 | 0.46 | 0.06 |

| Sum | 714.59 | 54506.00 | 126.70 | 56.35 | 4882.40 | 964.59 | 725.50 | 133.63 |

| SumSq. Dev. | 8092.12 | 1.50 | 1150.91 | 81.96 | 597157.1 | 12704.72 | 950.92 | 156.58 |

| Observations | 43 | 43 | 43 | 43 | 43 | 43 | 43 | 43 |

Source: Author’s computation using E-views

As seen in Table 1A, the descriptive statistics showed a mean of 3.03 and median 3.30 for gross domestic rate. Moreover, the statistic also showed that the data for gross domestic rate was a leptokurtic distribution because the kurtosis value is greater than three indicating a positive kurtosis, though positively and insignificantly skewed. Also, the descriptive statistics showed a mean of 18.78 and 18.95 for domestic debt. Moreover, the statistics also showed that the data for domestic debt was a leptokurtic distribution because the kurtosis value is greater than three indicating a positive kurtosis though negatively skewed. Furthermore, the total variability within the data for GDP is 1159.9. Though all other variables have reflected diverse values.

Table 1B: Augmented Dickey-Fuller (ADF) and Philip-Perron (PP) Unit Root Analysis

| ADF | Philip Perron | ||||||||||

| Levels | First | Difference | Levels | First | Difference | Order of | |||||

| Variables | T-Statistic | P-Value | T-Statistic | P-Value | T-Statistic | P-Value | T-Statistic | P-Value | Integration | ||

| Inflation Rate | -6.075 | 0.0000 | -6.0759 | 0.0000 | I (I) | ||||||

| Gross Domestic product | -5.215 | 0.0001 | -3.786 | 0.0000 | I (0) | ||||||

| Fiscal Deficit | -6.151 | 0.0000 | -6.652 | 0.0000 | I (I) | ||||||

| Lending Interest Rate | -5.512 | 0.0000 | -7.093 | 0.0000 | I (I) | ||||||

| Exchange Rate | -3.830 | 0.0054 | -3.750 | 0.0068 | I (I) | ||||||

| Domestic Debt | -5.358 | 0.0001 | -5.351 | 0.0001 | I (0) | ||||||

| Broad Money Supply | -4.019 | 0.0033 | -4.018 | 0.0032 | I (0) | ||||||

| Unemployment Rate | -3.881 | 0.0177 | -3.861 | 0.0165 | 1(1) | ||||||

Source: Author’s computation using E-views

The outcomes of the unit root test validated the use of Auto regressive Distributed Lag (ARDL) technique in analyzing the data used for this study. The level of stability showed by the statistical significance further enhanced the level of certainty in the prediction that ARDL technique will yield reliable results from the analyses of the data used for this study.

Table 2: Bounds Test Dependent variable: GDP

| F- statistics = 5.3778 K= 4 | ||

| Critical Values | Lower Bound 1(0) | Upper Bound 1(1) |

| 10% | 2.45 | 3.52 |

| 5% | 2.86 | 4.01 |

| 2.5% | 3.25 | 4.99 |

| 1% | 3.74 | 5.06 |

Source: Author’s computation using E-views

It can be observed that the f- statistic of 5.3778 was both greater than the upper bound value of 3.52 with a degree of freedom, K=4. This implies that, in this model, there exist long run relationships between the dependent and independent variables. Based on this, the long run and short run error correction models can be estimated.

Table 3: long run estimates on the domestic debt dynamics, price stability and economic growth in Nigeria

| Dependent Variable: GDP | |||

| Regressor | Coefficient | Std rror | Prob |

| C | 62.10592 | 65.95270 | 0.3827 |

| DD | -0.36553 | 0.229413 | 0.1863 |

| Exr | 2.99023 | 1.058094 | 0.0475 |

| MS | 0.79951 | 0.817942 | 0.3661 |

| Inf | -4.84055 | 9.676841 | 0.8758 |

| UEMP | -1.438369 | 0.679064 | 0.0602 |

| FD | -0.070453 | 0.073543 | 0.3587 |

| LIR | -1.96334 | 1.47524 | 0.2316 |

Source: Author’s computation using E-views.

The coefficient of domestic debt (DD) is -0.365, implying that in the long run, there is a negative link between domestic debt and economic growth. This means that a 1% increase in domestic debt will result in a 0.365% decrease in economic growth. This also implies that in the long run, government borrowing debt do not result in large economic growth in Nigeria. This is in consonance with the findings of Ewubara, Ntegah and Okpo (2017). This entails that government borrowed funds needs a close monitoring to avoid embezzlement. There is need to ensure that these borrowed funds are used for infrastructural building and for attainment of peace and security as this would trigger economic growth mostly in the long run.

As seen in the Table, the result showed that exchange rate would transmit economic growth to the tune of about 2.990 percent, though statistically insignificant. The implication is that about 2.990 percent of exchange rate can distort economic growth. Theoretically, the depreciation of the naira is expected to boost export trade and attract foreign investment with potentials for increased growth in the domestic economy. However, depreciation of the naira implies that while exports would adjust upward considerably for every Nigerian purchase of imported items. The implication of this result is that, government should allow for a realistic and stable exchange rate policy to enhance output performance. Also, occasional devaluation of the naira by the government and the monetary authorities should be allowed as it is capable of enhancing output performance and boosting the Nigerian economy.

Furthermore, the result affirms the fact that money supply total has a positive impact on economic growth in Nigerian economy. With the coefficient of 0.799, though statistically insignificant, the result indicated that there would be about 0.799 percent increase in economic growth. Thus, there exists a direct and significant relationship between broad money supply and economic growth. This variable conform to the a priori expectation. This implies that higher money supply lowers interest rate which spurs investment through putting more hands in the hands of consumers, making them feel wealthier and thus stimulating spending. Also, business firms respond to increased sales by ordering more raw materials and increasing production, hence improving economic output.

The coefficient of fiscal deficit (FD) is -0.07, implying that in the long run, there is a negative link between fiscal deficit and economic growth. This means that a 1% increase in fiscal deficit will result in a 0.07% decrease in economic growth rate. Nevertheless, its probability level is insignificant; the statistical insignificance may be due to distortions associated with time series data in Nigeria amongst other factors. This result points that fiscal deficit operation has not been channeled to productive uses, as such, leading to a huge debt burden and a corresponding debt overhang annually that has negatively affected growth. This result is in line with the study by Aworinde (2013). The negative results stems from the fact that Nigeria’s chronic fiscal deficit led to the accumulation of public debt levels, which also leads to the widening of the current account deficits; as the current account deficit worsens, it turns into depreciation of the domestic currency which impacts the economy negatively due to the inflationary pressures and thus causes increase in interest rates which crowds out domestic investment. As a consequence, the cost of borrowing goes up for the government and this exerts pressure on the government budget due to high debt service and thus the spiral of high deficit levels continues.

The coefficient of unemployment rate (UEMP) is -36.09, implying that in the long run, there is a negative link between unemployment and economic growth. This means that a 1% increase in unemployment rate will result in a 36.09% decrease in economic growth rate. Nevertheless, its probability level is insignificant; the statistical insignificance may be due to distortions associated with time series data in Nigeria amongst other factors. However, the result is in line with the Okun’s Law. This implies that there is a trade-off relationship between the variables. There should be creation employment opportunities in order to absorb the teeming population of the unemployed work force in the country.

The coefficient of interest rate (LIR) is -1.963, implying that in the long run, there is a negative link between interest rate and economic growth. This means that a 1% increase in interest rate will result in a 1.963% decrease in economic growth rate. Nevertheless, its probability level is insignificant; the statistical insignificance may be due to distortions associated with time series data in Nigeria amongst other factors. This implication of this result is that the monetary authorities should maintain a single digit interest rate so as to encourage real sector investment which would be beneficial to the Nigerian economy rather than keeping a high rate of interest that will encourage investment in financial assets which does not have so much impact on the masses but rather poses more threat on the country’s real sector.

The negative relationship between inflation rate and economic growth. This means that a 1% increase in inflation rate will result in a 4.8% decrease in economic growth. This implies that the inverse relationship of inflation and economic growth makes investment less desirable, since inflation creates uncertainty for the future and also affect the balance of payment because exports become more expensive; as a result, economic growth decreases further

Table 4: short run estimates on the domestic debt, price stability and economic growth in Nigeria

| Dependent Variable: GDP | |||

| Regressor | Coefficient | Std Error | Prob |

| DD | -1.499493 | 0.655168 | 0.0291 |

| EXR | -0.020341 | 0.020046 | 0.3181 |

| LIR | -1.499493 | 0.655168 | 0.0291 |

| INF | -1.240135 | 0.157138 | 0.0000 |

| UEMP | -0.332163 | 0.277208 | 0.2399 |

| MS | 0.016042 | 0.139051 | 0.9089 |

| FD | -0.02257 | 0.139051 | 0.0000 |

| ECM | 1.000000 | 0.484705 | 0.0476 |

| (-1) | -3.462431 | 10.94930 | 0.7540 |

| R2 | 0.803975 | D.W 1.146854 | |

Source: Author’s computation using E-views.

It was also pertinent to investigate the short run relationship between domestic debt, price stability and economic growth with other macroeconomic variables considered in the study. On the other hand, the short-run effect did not reflect much difference from the foregoing results analyzed. As seen in Table 4.4, the coefficient estimates of fiscal deficit (-0.0225) in the short run showed that, ceteris paribus, a rise in the level of domestic debt will truncate the possibility for economic growth at about 0.0225 percent rate.

Also, this short run result is in consonance with Adoufu and Abula (2016) and Onyeiwu (2012), but Singh (2015) made contrary findings. This negative relationship, albeit statistically significant is worrying because pubic finance theories show that such short-run effects could also carry on in the long run, especially when such borrowings are not properly channeled into investment or development projects.

Furthermore, exchange rate showed a negative relationship with economic growth. The implication of this result is that in the short run, when economic growth is the target of policymakers, manipulating the exchange rate regime will induce an increase in economic growth though this relationship dissolves in the long run.

There is a negative impact of inflation on economic growth. Other findings in the literature such as Mudiare and Orubu; (2022); Sulaiman and Azeez (2012), and Adoufu and Abula (2016) also made the same findings. Inflation, which is an upward and persistent increase in price affects output, and when unchecked, can harm economic growth both in the short and long runs.

Also, the ECM represents the percentage of correction to any deviation in the long run equilibrium in a single period and also represent how fast the deviations in the long run equilibrium is corrected. The ECM (-1) showed -3.46 but insignificant. This implies that whenever there is any disturbance in the system in the long run, in every short –run period, a 36% correction to disequilibrium will take place.

Table 5: Causality result Causality for domestic debt and economic growth

| Null Hypothesis: | Obs | F-Statistic | Prob. |

| DD does not Granger Cause GDP | 41 | 0.54781 | 0.5830 |

| GDP does not Granger Cause DD | 0.76462 | 0.4729 |

The result showed that there is no causality between domestic debt and economic growth at 5% level of significance. If domestic debt does not causally affect GDP, policymakers may need to reassess the effectiveness of using debt as a tool for stimulating economic growth. They might focus more on other factors such as infrastructure investment, education, or institutional reforms to boost GDP. Furthermore, without a direct causal link, the focus on managing domestic debt shifts towards ensuring sustainability rather than solely using it as a lever for growth. Governments would prioritize managing debt levels to avoid potential risks such as crowding out private investment or debt servicing burdens.

Causality for domestic debt and price stability

| Null Hypothesis: | Obs | F-Statistic | Prob. |

| DD does not Granger Cause INF | 41 | 0.99626 | 0.3792 |

| INF does not Granger Cause DD | 0.01585 | 0.9843 |

The result showed that there is no causality between domestic debt and inflation at 5% level of significance. The economic implication of no causality between domestic debt and inflation is significant because it challenges traditional economic theories and policies related to debt management and inflation control. Many economic policies are based on the assumption that increasing domestic debt could lead to inflationary pressures due to increased money supply or government spending. If no causal relationship exists, policymakers may need to reevaluate how they manage debt and inflation.

SUMMARY, CONCLUSION AND POLICY RECOMMENDATIONS

The major objective of this study was to analyse domestic debt dynamics, price stability and economic growth in Nigeria. Specifically, it sought to: investigate the long and short run effects of domestic debt on price stability and economic growth in Nigeria; and also ascertain the causal relations between domestic debt, inflation and economic growth in Nigeria. The study employed the Auto Regressive Distributed Lag (ARDL) and the Granger Causality test to address the specific objectives. The (ARDL) uses bounds test to test for a long run relationship among the relevant variables. Since there was an existence of long run then error correction model was done. The study has revealed that domestic debt has an indirect and insignificant impact on economic growth in the long run and indirect significant relationship in the short run in Nigeria and there are no causal relations between domestic debt, inflation and economic growth in Nigeria.

Conclusion

This study has revealed domestic debt dynamics, price stability and economic growth. Thus, the Nigerian government reliance on borrowing from the banking sector, primarily the CBN, to finance its financial plan has slowed down the attainment of macroeconomic stability and sustainable economic growth. This has resulted in the crowding out of the private sector from the credit market, thereby slowing down investment and output growth.

Conclusively, Nigeria’s rising level of domestic debt does not contribute to the economic growth of the nation over the period under study. Therefore, it should be discontinued as a means of promoting economic growth in Nigeria.

Recommendation

- Domestic debt should be invested in productive sectors of the economy and more specifically in the real sector to create employment and reduce poverty incidence in the country.

- There should be proper formulation and implementation measures that would keep the inflation rate at a level that would not have adverse effects both in the short and long runs.

- The Government and relevant monetary authorities should adopt a suitable exchange rate policy that will allow for a realistic and stable exchange rate to enhance output performance. The depreciation of the nation’s currency is likely to increase the cost of imported raw materials as well as the cost of imported finished goods. Thus, producers would prefer domestically sourced input Similarly, locally made products would become more preferable to consumers as they will be cheaper than their foreign substitutes. Thus, exchange rate depreciation has a way of encouraging local production and boosting national output.

- Occasional devaluation of the naira by the government and the monetary authorities should be allowed as it is capable of enhancing output performance and boosting the Nigerian economy. On the other hand, exchange rate appreciation has the tendency of making imported raw materials and imported finished goods cheaper, thereby impeding local production and reducing national out

- The monetary authorities should maintain a single-digit interest rate so as to encourage real sector investment which would be beneficial to the Nigerian economy.

REFERENCE

- Adetokunbo, A. M, Ebere C. E. (2019). Determinants and Analysis of Domestic Debt in Nigeria: 1970-2015. AUDOE, 15(2): 275-287

- Ahmad, M.J, Sheikh, M.R and Tariq. K (2012) Domestic Debt and Inflationary Effects: An Evidence from Pakistan. International Journal of Humanities and Social Science 2(18) :256-263.

- Adofu, I and Abula, M. (2010). Domestic debt and the Nigerian economy, Current Research Journal of Economic Theory 2(1):22-26

- Aworinde, O.B. (2013). Budget deficits and economic performance (Doctoral dissertation). Department of Economics, University of Bath, United Kingdom.

- Ayuba K.I and Khan S.M (2019). Domestic Debt and Economic Growth in Nigeria: An ARDL Bounds Test Approach. Economics and Business 33,50-68

- BabuO Kiprop, S, Kalio, A.M and Gisore, M. Effect of Domestic Debt on Economic Growth in the East African Community. American Journal of Research Communication 3(9): 73-95

- Bildirici, M., and O. O. Ersin (2007). Domestic debt, inflation and economic crises: a panel cointegration application to emerging and developed economies. Applied Econometrics and International Development, 7(1), 1–17.

- Bossou, N.C and Duke, E.S (2020). Effect of Domestic Debt on Economic Growth in Nigeria. International Journal of Innovative Finance and Economics Research 8(2):42-47

- Boukraine, W (2021) Debt, Economic Growth and Inflation in Tunisia. Journal of Smart Economic Growth 6(1): 75-82.

- Diamond, P., 1965. National Debt in a Neoclassical Debt Model”, Journal of Political Economy, .55, 1126- 1150.

- Del, V. C. (2003) The Development of Domestic Markets for Government Bonds. The Future of Capital Markets in Developing Countries

- Nnol, O. (2003). Globalization and African Political Science. African Journal of Political Science, 8(2) 28-42.

- Maana, I., Owino. R. and Mutai. N. (2008): “Domestic Debt and its Impact on the Economy-The Case of Kenya”. Paper Presented During the 13th Annual African Econometric Society Conference in Pretoria, South Africa.

- Mudiare, Orerhime Monica and Christopher O. Orubu; (2022); The Effects of Domestic Debt on the Nigeria Economy. Hmlyan Jr Eco Bus Mgn; 3(6), 68-7

- Marshal, I (2020). Granger Causality Analysis Between Domestic Debt and Inflation in Nigeria. Journal of Development Economics and Finance 1(1), 135-149

- Mboto, H.W, OkoI, I. O, Edom, E.O and Ukongim, M.A (2022). Implication of Domestic Debt on Economic Growth in Nigeria. Aksu Journal of Management Sciences 7 (1 and 2) :43-56

- Onyeiwu, C (2012) Domestic Debt and the Growth of Nigerian Economy. Research Journal of Finance and Accounting 3(5): 45-56.

- Onwioduokit, E.A. (2002). Fiscal deficit and Inflation: An Empirical Investigation of causal Relationships. Economic and Financial Review. 37(2), 1-21.

- Onwioduokit, E.A. (2012). An Empirical Estimation of Optimal Level of fiscal deficit in the West African Monetary Zone. Journal of Monetary and Economic Integration. 12(1), 1-33

- Putunoi, G. K. and Mutuku, C. M. (2013): “Domestic Debt and Economic Growth Nexus in Kenya”. Current Research Journal of Economic Theory, 5(1): 1-10.

- Romer, P. M. (1995). The Origins of Endogenous Growth. The Journal of Economic Perspectives, 8(1), 3–22.

- Haffner, Ozolina C. E; Aruna, Alfred J. H.; Adams, Kormay (2017): Impact of domestic debt on economic growth in Sierra Leone: An empirical investigation, West African Journal of Monetary and Economic Integration, ISSN 0855-594X, West African Monetary Institute (WAMI), Accra, 17(2): 1-24

- Sheikh, M. R., Faridi, M. Z. and Tariq, K. (2010): “Domestic Debt and Economic Growth in Pakistan: An Empirical Analysis”. Pakistan Journal of Social Sciences, 30 (2):373-387.