Effect of Efficiency on the Relationship between Organization Characteristics and Financial Performance of Commercial Banks in Kenya

- Kennedy Ochuka

- Kennedy Okiro

- Fredrick Ogilo

- 2613-2623

- Aug 17, 2024

- Finance

Effect of Efficiency on the Relationship between Organization Characteristics and Financial Performance of Commercial Banks in Kenya

Kennedy Ochuka*, Kennedy Okiro, Fredrick Ogilo

University of Nairobi, School of Business, Department of Finance and Accounting

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2024.807203

Received: 27 June 2024; Revised: 10 July 2024; Accepted: 17 July 2024; Published: 17 August 2024

ABSTRACT

The purpose of the study was to establish the intervening effect of efficiency on the relationship between organization characteristics and financial performance of commercial banks in Kenya. The study used unbalanced panel data sourced from the Central Bank of Kenya for the period 2011 to 2021 across the 43 commercial banks. Organization characteristic was measured using weighted composite index of total assets, liquidity risk, asset quality, management quality, non-traditional activities and technological innovation; efficiency was captured using data envelopment analysis; while financial performance was measured using a weighted composite index derived from return on assets and net interest margin. The relationship was assessed using the Baron and Kenny (1986) model. The study found that there was statistically significant relationship between organization characteristics and financial performance (β = .575, p = .000, R2 = .801) in the absence of intervention effect. The interaction between organization characteristic and efficiency was statistically significant (β = -.133, p = .001, R2 = .025). The interaction between efficiency and financial performance was statistically significant (β = -.132, p = .003, R2 = .030). Further the overall interaction between organizational characteristic, efficiency and financial performance was statistically significant (β = .572, p = .000, R2 = .802). The results implied that efficiency mediates the relationship between organization characteristic and financial performance. The results imply organization characteristic are some of the critical determinants of financial performance of commercial banks. The banks should take into account their levels of efficiency in order to attain higher levels of financial performance. The study adds value to policy makers, banking regulators and managers in understanding the influence of organization characteristics of banks and efficiency on the financial performance of the banks. The banking regulations should aim to move banks to attain levels of efficiency that enhance financial performance.

Keywords: Organization Characteristics, Efficiency, Financial Performance, Commercial Banks.

INTRODUCTION

Organisational characteristics are demographic features, such as size, financial revenue, technological expertise, and location (Oncioiu, 2019) and are distinguishing features of an organization that influence its performance (Ondigo, 2019). When applied to banks, they are the internal determinants of bank performance that are unique to each bank, and which the management can control and manipulate to achieve different levels of performance (Abobakr, 2018). Efficiency is defined as the ratio of output to input of any system and is about achieving results with the optimal use of resources (Puteh Rasyidin, & Mawaddah, 2018). Financial performance is a critical determinant of the health of commercial banks. Taouab and Issor (2019) argue that scholars have not agreed on one accepted definition of performance, and the concept of performance can be better understood by looking at several parameters associated with it. It is anchored upon the idea that an organization is an association of productive assets, for the purpose of achieving a shared purpose (Jensen & Meckling, 1976). Banks are financial intermediaries which borrow funds from surplus units and transmit the funds to deficit units. Bank characteristics like size, liquidity and capitalization are closely associated with the financial performance of banks. Efficiency plays a critical role in that more efficient banks are more likely to be profitable than the less efficient banks.

The bank characteristics have been identified as loans to assets ratio, liquidity, deposits to assets ratio, capital adequacy, operating income to asset ratio, non-interest income to asset ratio, and bank size (Abobakr, 2018); size, credit risk, regulatory capital, efficiency and capital, (Ercegovac, Klinac & Zdrilic, 2020); size, off-balance sheet transactions, liquidity, quality of loans, concentration (Erdogan and Aksoy, 2016); and technological innovation, mobile banking, computer software, internet banking, and Automated Teller Machines (Chaarani & Abiad, 2018). Asongu and Odhiambo (2019) postulate that bank efficiency can be decomposed to its components of cost, revenue, captivity, concentration, X, scale, and scope efficiencies. Performance can be measured using objective measurements which tend to be quantitative and focus on results; and subjective measures which are qualitative and based on perception, and focus on the process of achieving results. Performance of banks can be assessed from market perspective or from accounting perspective. The market perspective looks at the stock returns for listed banks and interprets the changes in the returns as the market’s opinion of the performance and future prospects of the banks. The accounting perspective uses accounting measures like return on average assets (ROAA), return on average equity (ROAE), net interest margin (NIM), cost to income ratio (CIR). The study used ROA and NIM to measure performance. NIM is used for its ability to measure the spread, which some studies consider a better measure of performance than ROAA and ROAE (Ongore & Kusa, 2013), while ROA is seen as a superior indicator of performance as compared to return on equity (ROE) (Kalunda, 2015).

Organization characteristics, efficiency and financial performance have been studied with various outcomes. Some of the studies reviewed conceptualized efficiency as a function of bank characteristics (Oluitan, 2014; Jimenez-Hernandez, Palazzo & Saez-Fernandez, 2019) which is not the most adequate measure of bank performance as banks are set up to make profits. Other studies modelled firm characteristics as either a moderating variable in corporate governance-financial performance relationship (Ondigo, 2019), or as a determinant of financial stability (Wamalwa, Mungai & Makori, 2020). Some studies report that bank characteristics like size are related to performance (Kassem & Sakr, 2018; Wambugu & Koori, 2019; Nyabaga & Matanda, 2020) while others report no relationship (Ercegovac et al, 2020). The influence of efficiency on bank characteristics and financial performance is inconclusive. Jimenez-Hernandez et al. (2019); and Kamarudin, Sufian, Nassir, Anwar and Hussain (2019); report a positive effect while Asongu and Odhiambo (2019) reported a negative effect. It is important to continue empirically assessing these factors further and isolate those that affect performance.

Similar studies have been done at international and regional levels. In china, bank size and non-traditional activities had a positive impact on efficiency levels, while efficiency had a negative correlation with bank profitability (Antunes, Hadi-Vencheh, Jamshidi, Tan & Wanke, 2022). A study of 94 commercial banks from the Eurozone found that banking efficiency depends on set bank-specific characteristics like size and asset composition and that the effect of the determinants on efficiency differs from bank to bank depending on macroeconomic conditions, while bank specific characteristics were promoters of both efficiency and profitability (Neves, Gouveia, & Proença, 2020). Duho, Onumah, Owodo, Asare and Onumah (2020) reported that bank characteristics like credit risk and market risk are important in improving profit efficiency and return on equity in Ghana. Ozili and Ndah (2024) found that bank concentration, nonperforming loans and cost efficiency are significant determinants of the profitability of Nigerian banks.

Commercial banks in Kenya vary greatly in their characteristics as per the Central Bank of Kenya (2020) Bank Supervision Annual Report. While the banking sector in Kenya is critical in promoting investments in the economy, it has, in the recent past, seen the collapse or placement under receivership of several banks (Nyabaga & Matanda, 2020) due to poor capitalisation, liquidity and management. Wambugu and Koori (2019) state that the profitability of banks in Kenya has experienced a steady decline over the years. Small banks, poorly capitalized banks, banks lacking liquidity and banks without quality management are more likely to fail compared to the others (Ondigo, 2019; Musiega, Olweny & Mukanzi, 2017). With the frequent failures of banks in Kenya, it is important for stakeholders in the banking sector to understand bank characteristics and their effect on the financial performance of banks in Kenya.

Most of the studies reviewed focussed on the direct effect of bank characteristics on financial performance. Few studies tested the intervening effect of efficiency (Erdogan & Aksoy, 2016; Chaarani & Abiad, 2018; Ercegovac et al., 2020). The predictive power of an independent variable over a dependent variable is improved if an appropriate intervening variable is introduced. In addition, while the measures of efficiency in the banking sector is generally agreed on, measures of bank characteristics used are diverse and varied: (Erdogan & Aksoy, 2016; Ercegovac et al., 2020; Chaarani & Abiad, 2018; Kamarudin et al., 2019). There is a research gap to further empirically refine the measures of bank characteristics to determine which of them are applicable in the Kenyan context. The objective of this study was to assess the intervening effect of efficiency on the relationship between organization characteristics and financial performance of commercial banks in Kenya.

The null hypothesis stated that:

H1 Efficiency does not intervene the relationship between organization characteristics and financial performance of commercial banks in Kenya.

The objectives of the study were two: to determine the effect of organization characteristics on financial performance of commercial banks in Kenya; and to analyze the influence of efficiency on the relationship between organization characteristics and financial performance of commercial banks in Kenya

LITERATURE REVIEW

The study was anchored on the Financial Intermediation Theory (Gurley Shaw, 1955). The other supporting theories were Resource Endowment Theory (Barney, 1991) and Efficient Structure Theory, (Demsetz, 1973). Financial Intermediation Theory (Gurley Shaw, 1955) contends that commercial banks are financial intermediaries which transmit excess resources from surplus to deficit units and must attain minimum cost production to remain a viable alternative to self-financing or direct-financing. Resource Endowment Theory (Barney, 1991) argues that firms, including banks use their internal resources (labour, capital among others) as inputs in different ratios, and gain competitive advantage by using the resources with which they are heavily endowed. Efficient Structure Theory, (Demsetz, 1973) states that the structure of an industry is a result of superior operating efficiency held by organizations in that industry. Under this theory, when subjected to the pressure of competition, efficient firms win, become larger, acquire more market share leading to greater profits.

Several studies have examined the different aspects of organization characteristic, efficiency and financial performance with diverse and inconsistent findings. The studies, mostly from developed and developing economies had mixed results leaving doubt as to whether the findings could be generally accepted and applied, especially in developing economies like Kenya. Erdogan and Aksoy (2016) reported that financial performance showed positive and statistically significant relations with capital, size, off-balance sheet transactions, liquidity and loans; and strong negative and statistically significant relations with quality of loans and concentration. This finding was in agreement with Kassem and Sakr (2018), Petria, Caprarub and Ihnatovc (2015) and Rani and Zergaw (2017) who found that size was positively related with ROA and ROE. The result was however at variance with Ercegovac, et al. (2020) who found that size had no effect on bank performance. Rani and Zergaw (2017), Kassem and Sakr (2018), Abobakr (2018) established that capitalization was negatively related with ROE. Rani and Zergaw (2017) however found a positive relationship with NIM. When ROA was used, Erdogan and Aksoy (2016), Rani and Zergaw (2017), Kassem and Sakr (2018), Abobakr (2018) all found positive relation between capitalisation and performance. Ercegovac et al. (2020) however differed and found that capitalisation had no effect on performance. Kassem and Sakr (2018) found capitalization and ROE were negatively related, implying that banks with low capitalization are considered riskier and thus more profitable. Non-performing loans was established to have a negative relation with performance (Erdogan & Aksoy, 2016). Ercegovac et al. (2020) report that management efficiency have a negative correlation with performance. This was in agreement with Rani and Zergaw (2017) who attributed it to the substantial cost to the bank of keeping quality management which reduces its profits. Liquidity is negatively related with performance (Erdogan & Aksoy, 2016). Rani and Zergaw (2017) found that non-interest income was negatively related with both ROA and ROE indicating that this source of income may be more volatile and less profitable. Chaarani and Abiud (2018) found that investment in internet banking and Automated Teller Machines (ATMs) positively impacted bank performance, while mobile banking and investment in computer software had no significant impact. Okiro and Ndungu (2013) found that adoption of internet banking enhances efficiency, effectiveness and productivity of financial institutions. Jimenez-Hernandez et al. (2019) found that internal variables like size and loans to total assets had a positive correlation with efficiency. Increasing the size of banks and the loans disbursed to customers enhanced the efficiency and performance of the banks. The increase in credit risk, measured by increase in non-performing loans decreased bank efficiency, leading to lower performance. The findings agree with the findings of Andries (2011) and Oluitan (2014).Kamarudin et al. (2019) reported that size and capitalization are positively related with revenue efficiency while liquidity is positively related with revenue efficiency. Management quality had a negative relation with revenue efficiency, capitalization enhanced revenue efficiency and profitability, while liquidity lowered both revenue efficiency and profitability

Based on the literature, the definition of bank characteristic variables is not uniform across the reviewed studies. This makes cross comparison difficult. The three most commonly used measures, size, liquidity and capitalization tend to give inconsistent results depending on the country the study is done (Erdogan & Aksoy, 2016). The results leave doubt as to the exact nature of the relationship between organization characteristic, efficiency and financial performance. This study attempts to add to the literature by studying this relationship among the commercial banks in Kenya.

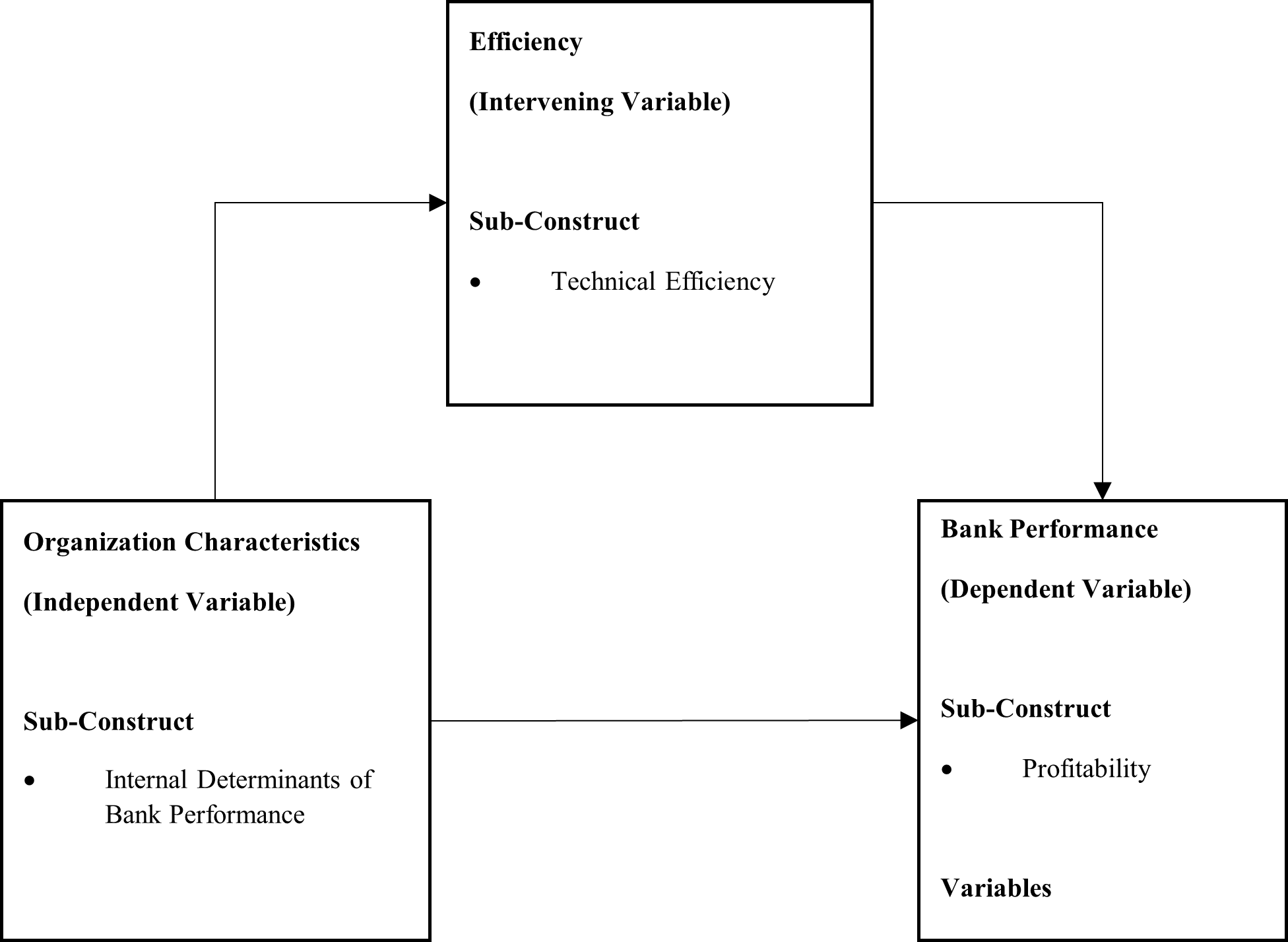

The conceptual model guiding the study is as presented in Figure 1.

Figure 1: Conceptual Model

The arrows in Figure 1 show the hypothesized relationships. The conceptual model postulates that organization characteristics influences financial performance in two ways. H1 tests the direct effect of organization characteristics on financial performance. H2 tests the intervention effect of efficiency on the relationship between organization characteristics and financial performance. Hypothesis two states that organization Characteristics can influence financial performance indirectly through the efficiency of the bank. Banks that attain higher levels of efficiency are expected to attain higher levels of profitability.

DATA AND METHODS

The study used secondary panel data extracted from the Central Bank of Kenya (CBK) Bank Supervision Annual Reports and the audited annual financial statements for 43 commercial banks and covered the period 2011 to 2021. The study adopted longitudinal descriptive research design. Organization characteristics was the independent variable and was measured using a composite index derived from six unique characteristics of commercial banks namely bank size, liquidity risk, asset quality, management quality, non-traditional activities and technological innovations. Efficiency was the intervening variable and was measured using Date Envelopment Analysis (DEA) Input – Output model as specified by Charnes, Cooper & Rhodes (1978). The input variables were labour, physical capital and cost of funds while the output variables were loans, other earning assets and non-interest income. Financial performance was the dependent variable and was proxied using composite index derived from Return of Assets (ROA) Net Interest Margin (NIM). The population in this study was the 43 (42 commercial banks and 1 mortgage institution) registered in Kenya as at December 2021. Two of the banks that were in receivership, one bank that was under statutory management and one mortgage institution were excluded from the study. Secondary data for eleven (11) year period from 2011 to 2021 was used. Secondary data on organization characteristics, efficiency and financial performance was collected from Central Bank of Kenya (CBK) Bank Supervision Annual Reports and from the audited annual financial statements of the commercial banks. The data was collected using Microsoft Excel and analyzed using the Statistical Package for the Social Sciences (SPSS) 26 software. The diagnostic tests of autocorrelation, linearity, multicollinearity, heteroscedasticity and normality were conducted before the data was analyzed.

The following baseline model was used:

Performance = f (Organization Characteristics, Efficiency, factors)

FP = β0+β1OC+β2EF+ε

Where:

- FP is financial performance

- β0 is the intercept

- β1 – β2 are the Coefficients

- OC is organization characteristics

- EF is efficiency

- ε is the error term.

RESULTS AND DISCUSSIONS

Descriptive Statistics

The descriptive statistics were as shown in Table below.

Table 1: Descriptive Statistics

| OC | EFF | FP | |

| N | 429 | 429 | 429 |

| Minimum | .000 | .200 | .120 |

| Maximum | .830 | 1.000 | .700 |

| Mean | .302 | .308 | .219 |

| Std. Deviation | .248 | .210 | .160 |

| Skewness | .498 | 1.527 | .545 |

| Kurtosis | -1.090 | 2.737 | -.658 |

Table 1 shows that the mean (x̄) scores and standard deviation (σ) for the variables. Organization characteristics level was 30 percent (x̄ = .302, σ = .248), efficiency was 31 percent (x̄ = .308, σ = .210), and financial performance was 22 percent (x̄ = .219, σ = .160). Further, both skewness and kurtosis were within the acceptable range of ± 2 and ±3 respectively. All the variables exhibit positive skewness. All the variables exhibited negative kurtosis except efficiency which displayed positive kurtosis.

Correlation was used to assess the strength of the relationship between the variables using Pearson correlation as shown in the table below:

Table 2: Correlation Analysis

| Efficiency | Organizational characteristics | Financial Performance | ||

| Efficiency | Pearson Correlation | 1 | ||

| Sig. (2-tailed) | ||||

| N | 429 | |||

| Organizational characteristics | Pearson Correlation | -.157** | 1 | |

| Sig. (2-tailed) | .001 | |||

| N | 429 | 429 | ||

| Financial Performance | Pearson Correlation | .173** | .895** | 1 |

| Sig. (2-tailed) | .000 | .000 | ||

| N | 429 | 429 | 429 | |

| **. Correlation is significant at the 0.01 level (2-tailed). | ||||

| *. Correlation is significant at the 0.05 level (2-tailed). | ||||

The results in Table 2 shows that there was a statistically significant positive correlation between Efficiency and Financial Performance (r = .173, p<.01). There was a statistically significant positive correlation between Organization Characteristic and Financial Performance (r = .895, p<.01). Finally efficiency and organization characteristic had statistically significant positive correlation (r = -.157, p<.01). The results suggest absence of autocorrelation problem between the variables.

The hypothesis tested was

H1 The relationship between organization characteristics and financial performance of commercial banks in Kenya is not significant.

H2 The relationship between organization characteristics and financial performance of commercial banks in Kenya is not intervened by efficiency.

The intervening effect was tested in four phases. Firstly, the direct effect of the independent variable on the dependent variable in the absence of the intervening variable. Secondly, the effect of the independent variable on the intervening variable in the absence of the dependent variable. Thirdly, the effect of the intervening variable on the dependent variable in the absence of the independent variable. And lastly the joint effect of the independent variable and the intervening variable on the dependent variable.

Table 3: Regression results of the effect of organization characteristic on financial performance.

| FP | Coefficient | Std. Err. | t | p>t | F(1, 427) | Prob > F | R2 | N |

| OC | .575 | .014 | 41.071 | 0.000 | 1686.827 | 0.000 | 0.801 | 429 |

| _cons | .046 | .005 | 9.200 | 0.000 |

Table 3 shows that there is .575 increase in Financial Performance for every unit increase in Organization Characteristic. The t-test of OC is 41.071 and is statistically significant (p<.05), meaning that the regression coefficient for OC is statistically different from zero. The R2 is .801 suggesting that OC accounts for 80.1% of the variance in Financial Performance of commercial banks in Kenya. It was deduced from the results that there was a significant relationship between Organization Characteristic and Financial Performance of commercial banks in Kenya. The analytical model was expressed as:

FPi=β0+β1OCi+ε

FPit = 0.046+0.575OCit+εit

Where: FP is the predicted Financial Performance, the dependent variable

0.046 is the predictive value of FP when the value of OC is zero,

0.575 is the estimate of change in OC on ROA

The second stage involved testing the relationship between Organization Characteristic and Efficiency without considering Financial Performance. The results are presented in Table 11 below.

Table 4: Effect of Organization Characteristics on Efficiency

| Efficiency | Coefficient | Std. Err. | t | p>t | F(1, 427) | Prob > F | R2 | N |

| OC | -.133 | .040 | -3.325 | 0.001 | 11.056 | 0.001 | .025 | 429 |

| _cons | .348 | .016 | 21.750 | 0.000 |

The results in Table 4 show that the F-test is statistically significant (F (1,427) = 11.056, p<.05) meaning the regression model is significant. Furthermore organization characteristic (β = -0.133, p<.05) is a significant predictor of efficiency. The relationship between organization characteristic and efficiency is positive and statistically significant. The results showed that there is 0.133 decrease in efficiency for every unit increase in organization characteristic. The t-test of OC is -3.325 and is statistically significant (p<.05), meaning that the regression coefficient for OC is statistically different from zero. The r2 is .025 suggesting that OC accounts for 2.5% of the variance in efficiency of commercial banks in Kenya. It was deduced from the results that there was a significant relationship between organization characteristic and efficiency of commercial banks in Kenya.

The third step assessed the relationship between financial performance and efficiency not considering organization characteristic. The results of the test are presented in Table 5.

Table 5: Effect of Efficiency on Financial Performance

| FP | Coefficient | Std. Err. | t | p>t | F(1, 427) | Prob > F | R2 | N |

| Efficiency | -.132 | .036 | -3.667 | 0.000 | 13.447 | 0.003 | .030 | 429 |

| _cons | .260 | .013 | 20.000 | 0.000 |

The regression results show that the values of prob. of F, regression coefficient, standard error value, t, and probability of t were 0.003, -.132, 0.36, -3.667, .000 respectively. The F test is statistically significant (F (1,427) = 13.447, p<.05). The results showed that there is 0.132 decrease in efficiency for every unit increase in financial performance. Efficiency is a significant predictor of Financial Performance. The t-test shows that the regression coefficient for Efficiency is statistically different from zero. The R2 is .030 suggesting that Efficiency accounts for 3.0% of the variance in Financial Performance of commercial banks in Kenya. It was deduced from the results that there was a significant relationship between efficiency and financial performance of commercial banks in Kenya. The results obtained in steps one to three confirm that Efficiency mediates the relationship between organization characteristic and financial performance of commercial banks in Kenya. The final step assessed the extent of the mediation, whether partial of full by assessing the relationship between organization characteristic, efficiency and financial performance together. The results of the test are presented in Table 6.

Table 6: Effect of Organization Characteristic, Efficiency on Financial Performance

| FP | Coefficient | Std. Err. | t | p>t | F(2, 426) | Prob > F | R2 | N |

| OC | .572 | .014 | 40.700 | 0.000 | 860.54 | 0.000 | .802 | 429 |

| Efficiency | -.026 | .017 | -1.529 | 0.122 | ||||

| _cons | .054 | .008 | 6.750 | 0.000 |

The results in Table 6 confirmed that the F-test is statistically significant F (2,426) = 860.54, p<.05) meaning the regression model is significant. Furthermore Organization Characteristic (β = .572, p<.05) is a significant predictor of Financial Performance. The relationship between OC and FP is positive and statistically significant. The results show that there is 0.572 incremental change in organization characteristic for every unit change in financial performance. There is 0.26 decrease in efficiency for every unit increase in financial performance. Efficiency (β = -.026, p>.05) is not a significant predictor of FP when mediating with OC as the independent variable. Finally, the coefficient relating the organization characteristics to financial performance (β = .575) is larger in absolute value than the coefficient relating the organization characteristics to financial performance with both the organization characteristics and efficiency predicting financial performance (β = .572). It was deduced from the results that efficiency partially mediated the relationship between organization characteristic and financial performance of commercial banks in Kenya. The two null hypotheses are therefore rejected.

The results of the intervening effect of Efficiency on the relationship between Organization Characteristics variables on Financial Performance of commercial banks consistent with previous studies. Modi and Mishra (2011) found that resource efficiency was positively associated with firm financial performance. However, the financial gains from resource efficiency exhibit diminishing returns. Makki and Lodhi (2014) that efficiency is determinant of financial performance. Kamarudin et al. (2019) found that efficiency was positively related to size, capitalization, and liquidity, as measured by loans-to-asset ratio was positively related with revenue efficiency, which in turn enhanced profitability. The findings agreed with, Puteh et al., 2018 and Jimenez-Hernandez et al., 2019. King’ori, Kioko and Shikumo (2017) found a positive and statistically significant relationship between operational efficiency and financial performance of microfinance banks in Kenya.

The study has put to test the Efficient Structure Theory and finds that banks have an inverse relationship with efficiency. The most efficient banks were not the most profitable. The findings agree with the critiques of this theory who argue that this theory it is not able to fully explain bank performance. Mala Sugiyanto and Jatmiko (2019) found that even though ASEAN banks reported high levels of efficiency, the efficiency did not seem to influence performance. Berger (1995) found that this theory is not very important in explaining bank profitability, and banks should look beyond the efficiency variables in their pursuit of profits.

CONCLUSIONS AND RECOMMENDATIONS

The study concluded that organizations characteristics determined the level of performance of commercial banks in Kenya. The study further concluded that efficiency intervened the relationship between organizations characteristics and financial performance of commercial banks in Kenya. The fact that there is a relationship between Organization Characteristics and Financial Performance of banks, policy makers must pay attention to these characteristics and aim to enhance the efficiency of the banks in order to attain higher levels of performance. There is therefore the need for the regulators to include efficiency as one of the indicators of bank health to be checked in the supervisory regime. The findings of this study will be beneficial to investors and depositors in commercial banks in making better investment decisions. Investors bear the risk when banks fail and collapse. The investors could better assess the bank characteristics that could lead to better financial performance and avoid those banks whose bank characteristics show likelihood of profit failure. The risk of the inconveniences caused by bank losses, failures and bankruptcy could be avoided or better managed.

REFERENCES

- Abobakr, M. (2018). Bank Specific, Industry Concentration, and Macroeconomic Determinants of Egyptian Banks’ Profitability. International Journal of Accounting and Financial Reporting, 8(1), 380-397.

- Andries, A. (2011). The Determinants of Bank Efficiency and Productivity Growth in the Central and Eastern European Banking Systems. Eastern European Economics, 49(6), 38-59.

- Antunes, J., Hadi-Vencheh, A., Jamshidi, A., Tan, Y., & Wanke, P. (2022). Bank efficiency estimation in China: DEA-RENNA approach. Annals of Operations Research, 315(2), 1373-1398.

- Asongu, S., & Odhiambo, N. (2019). Size, efficiency, market power, and economies of scale in the African banking sector. Financial Innovation, 5(4), 1-22.

- Barney, J. B. (1991). Firm Resources and Sustained Competitive Advantage. Journal of Management, 17(1), 99–120.

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173.

- Berger, A. (1995). The Profit-Structure Relationship in Banking–Tests of Market-Power and Efficient-Structure Hypotheses. Journal of Money, Credit and Banking, 27(2), 404-431.

- Charnes, A., Cooper, W. & Rhodes, E. (1978). Measuring efficiency of decision making units. European Journal of Operational Research, 2, 429-444.

- Central Bank of Kenya (2020). Bank Supervision Annual Report.

- Chaarani, H., & El Abiad, Z. (2018). The Impact of Technological Innovation on Bank Performance. Journal of Internet Banking and Commerce 23(3), 1-33.

- Cooper, D. R. and Schindler, P. S. (2014). Business Research Methods (12th). Boston: McGraw- Hill/Irwin.

- Demsetz, H. (1973). Industry Structure, Market Rivalry, and Public Policy. Journal of Law and Economics, 16(1), 1-9.

- Duho, K. C. T., Onumah, J. M., Owodo, R. A., Asare, E. T., & Onumah, R. M. (2020). Bank risk, profit efficiency and profitability in a frontier market. Journal of Economic and Administrative Sciences, 36(4), 381-402.

- R., Klinac, I., & Zdrilic, I. (2020). Bank Specific Determinants of EU Banks Profitability after 2007 Financial Crisis. Journal of Contemporary Management Issues, 25(1). 89-102.

- Erdogan, M., & Aksoy, E. (2016). Banking Regulation and Determinants of Banks’ Profits: Empirical Evidence from Turkey. Eurasian Journal of Business and Economics, 9(17), 109-124.

- Jensen, M., & Meckling, W. (1976). Theory of the firm: Managerial behaviour, agency costs, and financial times. New York. NY: Prentice Hall.

- Jimenez-Hernandez, I., Palazzo, G., Saez-Fernandez, J. (2019). Determinants of bank efficiency: evidence from the Latin American banking industry. Applied Economic Analysis 27(81), 184-206.

- Kamarudin, F., Sufian, F., Nassir, A., Anwar, N., & Hussain, H. (2019). Bank Efficiency in Malaysia a DEA Approach. Journal of Central Banking Theory and Practice, 8(1), 133-162.

- Kassem, N., & Sakr, A. (2018). The Impact of Bank-Specific Characteristics on the Profitability of Commercial Banks in Egypt. Journal of Finance and Bank Management, 6(2), 76-90.

- King’ori S., Kioko W., & Shikumo H. (2017). Determinants of Financial Performance of Microfinance Banks in Kenya. Research Journal of Finance and Accounting 8(16), 1-8.

- Makki, M. A. M., Lodhi, S.A. (2014). Impact of corporate governance on intellectual capital efficiency and financial performance. Pakistan Journal of Commerce and Social Sciences, 8(2) 305-330.

- Mala, C., Sugiyanto., Jatmiko. (2019). Analysis of Market Power Hypothesis and Efficiency Hypothesis in ASEAN Banking. Journal of Emerging Issues in Economics, Finance and Banking 8(1), 2681-2697.

- Modi, B.S., Mishra, S. (2011). What drives financial performance–resource efficiency or resource slack?: Evidence from U.S. Based Manufacturing Firms from 1991 to 2006. Journal of Operations Management, 29(3), 254-273.

- Musiega, M., Olweny, T., Mukanzi, C., & Mutua, M, (2017). Influence of Liquidity Risk on Performance of Commercial Banks in Kenya. IOSR Journal of Economics and Finance, 8(3) 67-75.

- Neves, M. E. D., Gouveia, M. D. C., & Proença, C. A. N. (2020). European bank’s performance and efficiency. Journal of Risk and Financial Management, 13(4), 67.

- Nyabaga, R.M., Matanda, J.W. (2020). Effect of Firm Characteristics on Financial Performance of Listed Commercial Banks in Kenya. International Journal of Economics and Financial Issues 10(3), 255-262.

- Okiro, K., & Ndungu, J. (2013). The Impact of Mobile and Internet Banking on Performance of Financial Institutions in Kenya. Euro Scientific Journal 9(13), 146-161.

- Oluitan, R. (2014). Bank Efficiency in Africa. The Journal of Developing Areas, 48(2), 205-221.

- Oncioiu, I., & IGI Global,. (2019). Throughput accounting in a hyperconnected world.

- Ondigo, H.O. (2019). The Moderating Effect of Firm Characteristics on the Relationship between Corporate Governance and Financial Performance of Commercial Bank in Kenya. International Journal of Current Science and Multidisciplinary Research 2(12), 248-276.

- Ongore, V.O & Kusa, G.B. (2013). Determinants of Financial Performance of Commercial Banks in Kenya. International Journal of Economics and Financial Issues, 3(1) 237-252.

- Ozili, P. K., & Ndah, H. (2024). Impact of financial development on bank profitability. Journal of Economic and Administrative Sciences, 40(2), 238-262.

- Petria, N., Caprarub, B. & Ihnatovc, I. (2015). Determinants of Banks’ Profitability: Evidence from EU 27 Banking Systems. Procedia Economics and Finance 20, 518-524.

- Puteh, A., Rasyidin, M., & Mawaddah, N. (2018). Islamic Banks in Indonesia: Analysis of Efficiency. Proceedings of MICoMS 2017 (Emerald Reach Proceedings Series), 1, 331-336.

- Rani, D.M.S. and Zergaw, L.M. (2017). Bank Specific, Industry Specific and Macroeconomic Determinants of Bank Profitability in Ethiopia. International Journal of Advanced Research in Management and Social Sciences, 6(3), 74-96.

- Taouab, O,. & Issor, Z. (2019). Firm Performance: Definition and Measurement Models. European Scientific Journal, 15(1) 1857-7881.

- Wamalwa, N., Mungai, J., & Makori, D. (2020). Moderating Effect of Exchange Rate on the Relationship Between Firm Characteristics and Financial Stability of Commercial Banks in Kenya. European Journal of Business and Management. 12(25), 71-76.

- Wambugu, A.M & Koori, J. (2019). Bank Characteristics and Profitability of Commercial Banks in Kenya. International Journal of Research in Business, Economics and Management, 10 (6) 34-56.