Effect of Environmental Information Disclosure on Stock Price Reaction among the Listed Consumer Goods Firms in Nigeria

- Mary John

- Leo U. Ukpong

- 453-463

- Mar 22, 2025

- Management

Effect of Environmental Information Disclosure on Stock Price Reaction among the Listed Consumer Goods Firms in Nigeria

Mary John1, Leo U. Ukpong2*

1American University of Nigeria, Nigeria, Department of Accounting and Finance

2Jackson State University, USA, Department of Accounting, Finance, and Entrepreneurship

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2025.914MG0035

Received: 04 February 2025; Accepted: 11 February 2025; Published: 22 March 2025

ABSTRACT

This study assesses the effect of environmental information disclosure on stock price reactions among the listed consumer goods firms in Nigeria. Data for the study was collected from 16 consumer-goods firms listed in the Nigerian Stock Exchange (NSE) from 2014 to 2022. The statistical analysis technique utilized for the study is the panel data regression. The study used secondary data from 28 consumer goods firms listed on the Nigeria stock exchange. Empirical results show that environmental information disclosure positively affects stock price reactions after controlling for firm size and leverage. It was also found that the disclosure of environmental information significantly impacts the return on assets, which is the proxy for the firm’s profitability. Based on these findings, the study concludes that environmental information is an essential tool for improving the information content of a firm’s value and profitability. It is therefore recommended that a robust legal and regulatory framework for environmental information disclosure be established in the country and that firms should strive to provide more awareness about environmental information disclosure to their stakeholders.

Keywords: Environmental Disclosure; Stock Price Reaction; Profit; Consumer Goods Market, Nigerian Stock Exchange.

INTRODUCTION

Issues surrounding the environment in which businesses operate are increasingly becoming a critical aspect of business responsibility. This represents a shift from the previous trend, when the primary focus of firms was to achieve the highest possible profit, to a new one in which firms aim to maximize overall corporate value, with one way of achieving this being to show more care for the environment in which they operate (Ifada et al., 2021). As Luluk et al. (2019) have pointed out, a good indicator of corporate value is a firm’s stock prices, where an increase in stock prices amounts to an increase in the prosperity of shareholders. Based on this, various scholars and researchers have proposed that there may be a link between environmental responsibility performance and firm stock prices (Harjoto & Jo, 2015; Jo & Harjoto, 2011; McBarnet et al., 2007; El Ghoul, Guedhami & Kim, 2017).

The environmental responsibility performance of a firm is one of the key criteria upon which stakeholders positively or negatively assess the firm’s progress and overall corporate performance (Amsir et al., 2020). This can be explained using various theories, including the legitimacy theory, which infers that the expectations of stakeholders concerning the environmental performance of a firm can seriously impact the legitimacy of the firm, which in turn translates to the sustainability of the firm’s businesses (Cho & Patten, 2006). This is probably why a firm’s environmental disclosure becomes an important tool for obtaining and maintaining its legitimacy status to its stakeholders (van de Burgwal & Vieira, 2014). Secondly is the signal theory, which indicates the ability of a firm to communicate with its stakeholders, consistently making environmental disclosures that may signal to the stakeholders that the firm is a good corporate citizen and has behaved in a responsible manner (Razaee, 2016). This theory presupposes that firms that have had superior performance in terms of the environment will usually have greater incentives to disclose their environmental activities and publish Environmental, Social and Governance (ESG) reports along with mandatory financial reports (Rezaee, 2016).

Another theory that lends credence to the link between environmental information disclosure and stock price reaction is the efficient market hypothesis (EMH) (Fama, 1970). According to the EMH, a stock market can only be deemed efficient if all valuable information is promptly reflected in the stock price trends (Yang, Zhang & Li, 2023; Zhang & Yang, 2023). The implication is that, in an efficient stock market, investors should be able to get accurate information, including accurate environmental information, that would reflect the stock prices, as this facilitates investors’ actual decision-making (Edmans, Jayaraman & Schneemeier, 2017). For this reason, the yearly announcement by a firm about its environmental performance has been hypothesized to be linked with the stock prices and overall success of the firm. Such environmental disclosures give investors and analysts additional information that they need to be able to make investment decisions (Ifada et al., 2021).

The emphasis on consumer goods firms listed in the Nigeria Stock Exchange (NSE) for this study arises from the fact that the operations and products of these companies exert a lot of pressure on the environment, leading to environmental degradation (Chukwu & Nkak, 2020). These companies operate in more environmentally sensitive sectors, and as such, they are expected to make more extensive environmental disclosures (Qiu, Shaukat & Tharyan, 2015). Yet, the rate of environmental disclosure among them has been largely poor (Chukwu & Nkak, 2020). Today, there are genuine concerns about the steady degradation of the environment in Nigeria and whether firms whose activities have been a significant source of this situation are taking adequate steps to remedy it (Ajike et al., 2016). In this regard, it is believed that the ability of firms to disclose the environmental burdens of their activities to society and publish the strategies that have been taken to alleviate any damage that may have been caused indicates environmental responsibility and promotes brand reputation that can drive positive stock price reactions (Hart, 1995).

However, within the environmental disclosure literature, the debate on the value-relevance of these disclosures is still ongoing. While for some scholars and researchers, these disclosures are merely ‘legitimation tools’ in the hands of firms (Cho & Patten, 2007), for others, particularly the proponents of the resource-based view (RBV) and voluntary disclosure theory (VDT), they argue that environmental disclosures are value-relevant (Cormier & Magnan, 2013; Clarkson et al., 2011). Nevertheless, environmental disclosure in relation to stock price reactions has received relatively scant attention in the information disclosure literature. More so, most of these studies have been carried out in developed market environments (see Yadav et al., 2016; Cormier et al., 2011; Harjoto & Jo, 2015; Plumlee et al., 2015), with only a very few focused on emerging markets (e.g. Siagian et al., 2013; Malarvizhi & Matta, 2016). This is even worse in Nigeria, where the various studies examining environmental disclosures have done so from contexts other than its relation to stock price reactions, for example, Ofoegbu et al.’s (2018) study that investigated environmental disclosure from the perspective of integrated and traditional reporting. There has, in fact, been no study investigating the effect of environmental disclosures on stock price reactions among listed consumer goods firms in the Nigeria Stock Exchange. This represents the gap in research that this study will attempt to fill.

LITERATURE REVIEW AND HYPOTHESIS

The impacts of environmental disclosure on stock price reactions have attracted a lot of debate in academic literature over the years, with contrasting opinions and results. For many, environmental disclosure positively impacts stock price changes (see Dedman et al., 2008; Clarkson et al., 2013; Plumlee et al., 2015; Wang, 2015; Zhou & Yin, 2017; Harjoto & Jo, 2015). For example, Dedman et al.’s (2008) investigation of the impact of voluntary disclosure on market reactions, measured as abnormal stock returns, in a sample of listed UK pharmaceutical firms, demonstrated that good voluntary disclosures were positively associated with stock prices, while on the other hand, negative news announcements lowered stock prices. Similarly, Clarkson et al. (2013) demonstrated that firms with higher-quality environmental disclosure generate higher Returns on Assets (ROA) than their competitors. Plumlee et al. (2015) found a positive impact of voluntary environmental disclosure on firm value when they studied the top polluting US-listed companies from five industries between 2000 and 2005.

On the other hand, some studies have either found a negative impact of environmental disclosure on stock price changes (Fatemi et al., 2017; Malarvizhi & Matta, 2016; Dhaliwal et al., 2011; Dhaliwal et al., 2014; de Villiers and van Staden, 2011; Brammer et al., 2006), or no significant impact at all (Deswanto & Siregar, 2018; Dejean & Martinez, 2014; Plumlee et al., 2015; McWilliams & Sigel, 2000; Horvathova, 2010). In the study by Deswanto and Siregar (2018), it was discovered that the effect of environmental disclosure on a firm’s financial performance was positive but insignificant. Also, Malarvizhi and Matta’s (2016) study did not find any significant relationship between the level of environmental disclosure and firm performance when the listed firms in the Bombay Stock Exchange in India were investigated. Dejean and Martinez (2014), from their study of companies listed in the SBF 120 stock market index, found no convincing evidence to indicate that environmental disclosure leads to reduced cost of equity.

Furthermore, the finding made by Fatemi et al. (2017) showed that ESG disclosures, in fact, decrease firm valuation. This finding agrees with that made by Allessi et al. (2020), which states that there is a significant negative and highly statistically significant effect of “Greenium” (risk premium associated with firms’ environmental transparency and greenness) on European individual stock returns. Finally, Aryani’s (2021) study of the effect of carbon disclosure on firm value revealed that carbon disclosure significantly negatively affected firm value, with firm (foreign) ownership acting as a significant moderator in this relationship. In addition, studies have shown that environmental disclosure only adds value to a firm under certain conditions. An example is the study by Aerts et al. (2008) that showed that the association between environmental disclosure and a lower cost of equity is mediated by certain factors like the industry to which the company belongs, with the result being weaker for environmentally sensitive industries; the country in which the company is operating, usually stronger for European than North American companies; as well as the venue of the disclosure, often more substantial for web-based disclosures for European companies, and print for North American companies.

The foregoing review has only confirmed that opinions and results concerning the relationship between environmental disclosure and stock price reaction are contrasting. This study aims to provide empirical evidence of this relationship in the context of consumer goods firms listed on the Nigeria Stock Exchange.

Therefore, the hypothesis for this study is:

H0: Environmental disclosure significantly positively affects the stock price reaction of listed consumer goods companies in Nigeria.

RESEARCH METHODOLOGY

A longitudinal research design has been adopted to establish the relationship between environmental disclosure and the stock price reaction of listed consumer goods firms in Nigeria. The study population comprised all the 28 listed consumer goods firms on the Nigerian Stock Exchange (NSE) as of 31st of December 2021. The purposive sampling method was used, and the entire population was targeted. However, only 16 firms (with 144 firm-year observations) that provided environmental disclosure were considered. While data concerning the environmental disclosure of the sample firms were retrieved from the Bloomberg database, the stock price information was collected from the Nigerian Stock Exchange (NSE) website. Other data like the firm size, leverage, and profitability were retrieved from the financial reports of the sampled firms for the period under study (2014 – 2021).

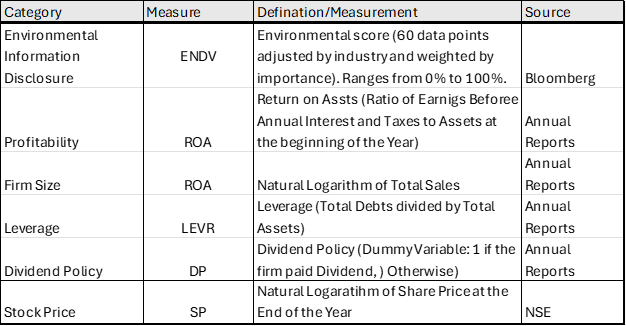

Table 1 presents the sampled firms and their industries, while Table 2 describes the variable names, measurements, and data sources. Information on the financial variables was obtained from each firm’s annual reports. The environmental information disclosure scores of the firms were obtained from Bloomberg; the profitability of firms, proxied by the return on assets (ROA), was obtained from the firms’ annual reports; and the stock prices of the firms (i.e. the share price at the end of the year) were obtained from the Nigerian Stock Exchange (NSE). Other firm characteristics, such as firm size, leverage, and dividend policy, were all retrieved from the annual reports of the sampled firms and are included as control variables for the study. The estimated model is based on panel feasible generalized least square (FGLS) regression.

Two related regression equations were developed to test the hypothesis (H0) that firm stock price movement is associated with environmental information disclosure (in addition to the control variables). While equation (1) models the theoretical relationship between stock price and environmental disclosure, equation (2) presents the explicit estimated regression equation.

Table I Sampled Firms and their Industries

Table II Variable definitions, measures, and data sources

The functional model for the study is presented in equation (1) as

SP = ƒ (ENVD, ROA, FSIZE, LEVR, DP) (1)

The above model is transformed into an explicit estimable model, as shown in (2) below.

\[

SP_{it} = \beta_0 + \beta_1 ENVD_{it} + \beta_2 ROA_{it} + \beta_3 FSIZE_{it} + \beta_4 LEVR_{it} + \beta_5 DP_{it} + \mu_{it}

\]

(2)

where:

SP = Stock price

ENVD = Environmental disclosure

ROA = Return on assets (profitability)

LEVR = Leverage

DP = Dividend policy

β0 = Regression intercept

βi,1 – βi,5 = Coefficients of the estimated variables

μit = Stochastic variable

The stock price is the dependent variable in these equations following previous related studies (Olagunju & Ajiboye, 2022; Amiolemen et al., 2018). Alternatively, the firm’s stock price could be viewed as the extent to which prospective investors are interested in having a stake in the firm. The primary independent variable for the study is environmental information disclosure. Environmental information or sustainability disclosure is measured in this study using the binary scores (between 0 and 100%) computed by Bloomberg ESG Disclosure ratings. Bloomberg assigns environmental disclosure scores to companies based on data points collected through multiple sources, including annual reports, standalone sustainability reports, and company websites. Sixty (60) different environmental data points are collected, capturing standardized cross-sector and industry-specific metrics. Also, within each environmental category, individual firms are scored in percentages to make the scoring comparable across companies. The scoring is also tailored to be relevant to industries, so each company is evaluated only based on relevant data from its industry sector. Previous studies have also chosen this measure by testing the association between environmental disclosure and profitability (Clarkson et al., 2008; Cormier et al., 2009).

Following prior literature, the study uses the natural log of total sales to control for firm size (Dhaliwal et al., 2011; Brammer & Pavelin, 2006; Cho and Patten., 2007) and each firm’s leverage – as defined in Table 2 to capture other unique financial characteristics of the firms (Cormier et al., 2011; Brammer & Pavelin, 2006).

RESULTS

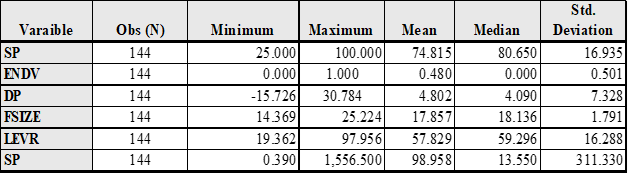

As shown in Table 3, the minimum and maximum values of environmental information disclosure are 25% and 100%, respectively, while the mean value is 74.82%. The standard deviation is 16.935, showing that the average environmental information disclosure is widely spread around the average mean value. In contrast, the mean value indicates a high degree of environmental information disclosure among the sampled firms, which is higher than those reported by Ahmadi and Bouri (2017). The return on assets had a mean of 4.802, a median of 4.090, and a standard deviation of 7.328, respectively. Table 3 also shows the estimated mean/average of the firm size, measured as the natural logarithm of total sales, to be 17.857, with a relatively low standard deviation of 1.791, while the mean values for the leverage, stock price, and dividend policy are 57.296, 98.958, and 0.48, with standard deviations of 16.288, 311.333, and 0.501, respectively.

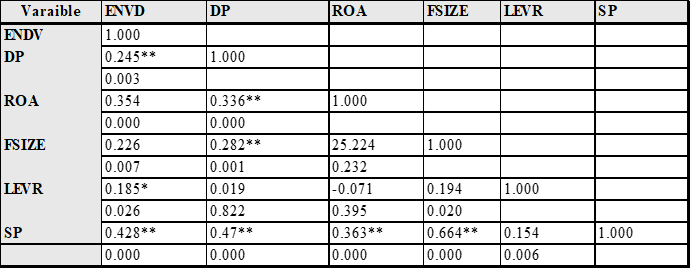

Table 4 shows a high correlation between the environmental information disclosure score and stock price (coefficient = 0.428; p < 0.000), suggesting a strong positive correlation between these two variables. This implies that once a firm sets a precedence of voluntary reporting in a particular area, it continues doing so in subsequent periods. This shows consistency with the argument on commitment costs. The table also shows a significant and positive association of environmental disclosure score with the stock price (coefficient = 0.428; p < 0.001) and return on assets (coefficient = 0.354; p < 0.001). However, the relationship of the environmental disclosure score with firm size (coefficient = 0.226; p < 0.007) and leverage (coefficient = 0.185; p < 0.026), were positive but insignificant. However, the table shows no multicollinearity problem between the variables since the correlation coefficients between the predictor variables do not exceed 80%.

Table III Descriptive Statistics

Table IV Pearson correlation coefficient

** p < 0.01, * p < 0.05

It is important to test for violation of other statistical assumptions before the regression test can be conducted, including the normality of distribution, stationarity, multicollinearity, autocorrelation, and heteroscedasticity. Regarding the normality assumption, because the sample for this study is small (<0 50), the Shapiro-Wilk test was applied, and the result is presented in Table 5. While the test result showed that the environmental disclosure, return on assets, firm size, and stock price variables were not normally distributed since the p-values of these variables are less than 0.05, the p-value for leverage was higher than 0.05 and, as such, is normally distributed. However, this is not expected to contribute to bias or inefficiency in the regression model (Li, Wong, Lamoureux & Wong, 2012).

Table V Shapiro-Wilk test for normality

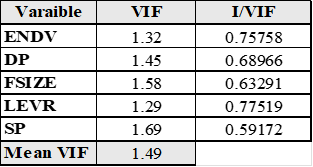

Multicollinearity between the predictor variables has been tested using the variance inflation factor (VIF). The maximum value of VIF in the regression models, as shown in Table 6, is 1.69, which is below 10 and indicates the absence of multicollinearity among the independent variables, as Hair et al. (1998) suggested.

Table VI Variance inflation factor

Similarly, autocorrelation was tested using the Wooldridge test. The result presented in Table 7 shows that with the F-value of 1716.085 and a corresponding value of 0.0000, the null hypothesis of no autocorrelation is rejected. Finally, heteroscedasticity was tested using the Breusch Pagan /Cook-Weisberg test, as shown in Table 7. The p-value of 0.000 and chi-square value of 25.61 indicates that the null hypothesis of no heteroskedasticity is rejected at all conventional significance levels.

Table VII Model Regression Diagnostic Test

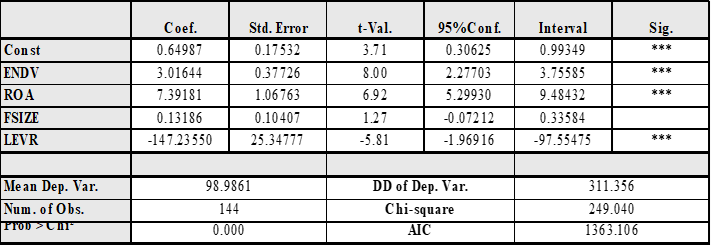

Based on the results of the various diagnostic tests that show non-normality of the variables, the presence of serial correlation and heteroskedasticity, the study controls for the used feasible generalized least square regression (FGLS) method that has an in-built mechanism for accommodating non-normally distributed data as well as controlling for the existence of serial correlation and heteroskedasticity (Baltagi, 2010). As such, the results of the FGLS are outlined in Table 8.

Table VIII Estimated Panel Feasible Generalized Least Square Regression

*** p < 0.01, ** p<0.05, *p<0.1

As shown in Table 8, environmental information disclosure (ENVD) positively influences the stock price reaction among the listed firms in Nigeria (coefficient = 0.6498702; p-value = 0.000). Similarly, return on assets (a proxy for firms’ profitability) and firm size assert significant positive influences on the stock price reaction of the firms. However, leverage, another of the control variables, has a weak and insignificant influence on stock prices.

DISCUSSION

The primary focus of this research was to assess the influence of environmental information disclosure on the stock prices of firms listed on the Nigerian Stock Exchange. The regression result shows a positive and significant influence of environmental information disclosure on the firm’s stock prices. This result confirms the key assumptions of the environmental disclosure theories discussed in this study. For example, in line with the legitimacy theory, the result confirms van de Burgwal and Vieira’s (2014) assertion that a firm’s environmental disclosure is critical for obtaining and maintaining legitimacy for its stakeholders. In other words, these firms’ integration of environment reporting to adhere to regulatory requirements positively impacts their stock prices. Also, the results could be interpreted to support the signal theory that a firm’s ability to communicate with its stakeholders regarding its environmental disclosures sends signals to the stakeholders that the firm is a good corporate citizen and has behaved responsibly (Razaee, 2016). Furthermore, the result agrees with the efficient market hypothesis (Fama, 1970) that holds that a stock market can only be deemed efficient if all valuable information is promptly reflected in the stock price trends. This position is also affirmed by Yang and Li (2023) and Zhan & Yang (2023), indicating that investors have accurate information concerning the firm’s environmental responsibility practices.

Beyond authenticating these key theories, the result of this study is also in line with several other previous studies (Dedman et al., 2008; Clarkson et al., 2013; Plumlee et al., 2015; Wang, 2015; Zhou & Yin, 2017; Harjoto & Jo, 2015), while at the same time negating the results of others (Fatemi et al., 2017; Malarvizhi & Matta, 2016; Dhaliwal et al., 2014; de Villiers and van Staden, 2011; Brammer et al., 2006; Deswanto & Siregar, 2018; Dejean & Martinez, 2014; Horvathova, 2010). One study revealed the conditions that mediated the relationship between environmental disclosure and the stock price reaction of firms, including the industry to which the company belongs, the country in which the company is operating, and the disclosure venue. Since this study was conducted with firms domiciled in Nigeria and within the NSE, the effect of country of location was not tested. This, therefore, represents a topic for future research.

One critical limitation of this study was that only the bigger listed firms on the NSE were considered at the exclusion of the smaller firms, even though the topic under discussion is equally important for all firms regardless of size and industry. Therefore, future studies must consider this, especially considering that future regulations may have similar implications for all firms, notwithstanding their sizes.

CONCLUSION

This research was conducted to understand the relationship between environmental information disclosure and the stock price reaction of firms listed in the NSE. The results show that environmental information disclosure directly relates to stock price reaction. This finding is important considering how much impact the activities of organizations, particularly the larger firms, have on the environment, which makes it critical that firms and their stakeholders show greater interest in avoiding environmental damage and depletion of natural resources. Concerns about the environment should not only be the purview of firms but also that of other internal and external stakeholders of the firm. Therefore, providing environmental information helps the firm to build trust among these stakeholders and enhance the reputation and credibility of the business. Most importantly, this research demonstrates that environmental information disclosure influences firms’ stock prices and how it affects a firm’s profitability, particularly its return on assets. It was discovered that environmental disclosure has a significant and positive impact on firms’ profitability, like the result found by previous studies (Sulaiman & Mokhtar, 2009; Saleh et al., 2011; Mahoney et al., 2007).

The following recommendations are put forward to achieve and sustain this in Nigeria. A precise legal framework for environmental information disclosure must be established in Nigeria. As it currently stands, environmental information disclosure is basically voluntary and without any benchmark. The result is that while the larger firms in the country sometimes provide such information to the public, most smaller ones often do not feel inclined to do so. The reasons are vast and varying; some are unfamiliar with environmental information disclosure, some do not see how it benefits them both in the short- and long-run, and some are indifferent to the concept. Creating the legal framework and benchmark will not only make it mandatory for firms to provide their environmental information disclosure but also show them how to go about it.

Finally, awareness campaigns should be undertaken, especially for smaller and non-listed firms unaware of environmental information disclosure, do not know how to go about it, or are not mandated to report such. Such awareness campaigns should show firms why it is essential and how it can be done and tell them how they stand to benefit from this endeavor vis-à-vis price discovery and added value to the firm.

REFERENCES

- Aerts, W., Cormier, D., Magnan, M. (2008). Corporate Environmental Disclosure, Financial Markets and the Media: An International Perspective. Ecological Economics, 64(3), 643-659.

- Ahmadi, A. and Bouri, A. (2017), “The Relationship Between Financial Attributes, Environmental Performance and Environmental Disclosure: Empirical Investigation on French Firms listed on CAC 40”, Management of Environmental Quality, Vol. 28 No. 4, pp. 490-506. https://doi.org/10.1108/MEQ-07-2015-0132

- Aggarwal, P. (2013). Relationship Between Environmental Responsibility and Financial Performance of Firm: A Literature Review. IOSR Journal of Business and Management, 13(1), 13-22.

- Alessi, L., Ossola, E., & Panzica, R. (2020). The Greenium matters : Greenhouse Gas Emissions, Environmental Disclosures, and Stock prices. JRC Working Papers in Economics and Finance, 2019/12. doi:10.2760/49586

- Amiolemen, O.O., Uwui gbe, U., Uwuigbe, O.R., Osiregbemhe, I.S., Opeyemi, A. (2018). Corporate Social environmental Reporting and Stock prices: An Analysis of Listed Firms in Nigeria. Investment Management and Financial Innovations, 15(3), 318-328. doi : 10.21511/i mfi .15(3).2018.26

- Amsir, L., Nurdiawansyah, N., Aminah, A., Haninun, H., Damayanti, T. (2020). Board Characteristics and Environmental Performance in Indonesian Family Business. Int. J. Trade Glob. Mark. 13(1), 1. https://doi.org/10.1504/ijtgm.2020.10023036

- Aryani, Y. A. (2021). The Impact of Carbon Disclosure on Firm Value with Foreign Ownership as A Moderating Variable. Jurnal Dinamika Akuntansi dan Bisnis, 8(1), 2021, 1-14

- Badi H. Baltagi (2021), Econometric Analysis of Panel Data; 6th edition, Spring Cham, https://doi.org/10.1007/978-3-030-53953-5.

- Brammer, S., Brooks, C. and Pavelin, S. (2006), “Corporate Social Performance and Stock Returns: UK Evidence from Disaggregate Measures”, Financial Management, 35, 97–116.

- Cho, C.H., Patten, D.M. (2007). The Role of Environmental Disclosures as Tools of Legitimacy: A Research Note. Account Organizations and Society, 32(7–8), 639–647. https://doi.org/10.1016/j.aos. 2006.09.009

- Chukwu, G.J. & Nkak, P.E. (2020). Board Attributes and Environmental Disclosure Quality of Consumer Goods Firms in Nigeria. GOUni Journal of Faculty of Management and Social Sciences, 8(1): 14-26

- Clarkson, P. M., Fang, X., Li, Y., & Richardson, G. (2013). J . Account. Public Policy The Relevance of Environmental Disclosures : Are Such Disclosures Incrementally Informative? Journal of Accounting and Public Policy, 32(5), 410–431. https://doi.org/10.1016/j.jaccpubpol.2013.06.008

- Clarkson, P.M., Li, Y., Richardson, G.D., Vasvari, F.P. (2008). Revisiting the Relation Between Environmental Performance and Environmental Disclosure: An empirical analysis. Accounting, Organizations and Society, 33(4), 303–327.

- Clarkson, P.M., Li, Y., Richardson, G.D., Vasvari, F.P. (2011). Does it Really Pay to Be Green? Determinants and Consequences of Proactive Environmental Strategies. Journal of Accounting and Public Policy, 30(2), 122–144.

- Cormier, D. Magnan, M. (2013). The Economic Relevance of Environmental Disclosure and its Impact on Environmental Legitimacy. Business Strategy and the Environment, (wileyonlinelibrary.com) DOI: 10.1002/bse.1829.

- Cormier, D., Aerts, W., Ledoux, M.J., Magnan, M. (2009). Attributes of Social and Human Capital Disclosure and Information Asymmetry between Managers and Investors. Canadian Journal of Administrative Sciences, 26(1), 71-88.

- Cormier, D., Ledoux, M.J., Magnan, M. (2011). The Informational Contribution of Social and Environmental Disclosures for Investors. Management Decision, 49(8), 1276-1304.

- De Villiers, C. & van Staden, C. J. (2011), “Where Firms Choose to Disclose Voluntary Environmental Information”, Journal of Accounting and Public Policy, 30; 504–525.

- Dedman, E., Lin, S. W., & Prakash, A. J. (2008). Voluntary Disclosure and its Impact on Share Prices : Evidence from the UK Biotechnology Sector. Journal of Accounting and Public Policy, 27, 195–216. https://doi.org/10.1016/j.jaccpubpol.2008.02.001

- Déjean, F., & Martinez, I. (2014). Environmental Disclosure and the Cost of Equity : The French Case. Accounting in Europe, 6(1), 57-80. https://doi.org/10.1080/17449480902896403

- Deswanto, R.B., & Siregar, S.V. (2018). The Associations Between Environmental Disclosures with Financial Performance, Environmental Performance, and Firm Value. Social Responsibility Journal, 14(1), 180-193. https://doi.org/10.1108/SRJ-01-2017-0005

- Dhaliwal, D. S., Li, O. Z., Tsang, A. and Yang, Y. G. (2011), “Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The initiation of Corporate Social Responsibility Reporting, The Accounting Review, 86(1): 59-100.

- Dhaliwal, D. S., Li, O. Z., Tsang, A. and Yang, Y. G. (2014), “Corporate Social Responsibility Disclosure and the Cost of Equity Capital: The roles of Stakeholder Orientation and Financial Transparency”, Journal of Accounting and Public Policy, 33, 328–355.

- Edmans, A., Jayaraman, S., & Schneemeier, J. (2017). The source of information in prices and investment-price sensitivity. Journal of Financial Economics, 126(1), 74-96. https://doi.org/10.1016/j.jfineco.2017.06.017.

- El Ghoul, S., Guedhami, O. and Kim, Y. (2017), “Country-level Institutions, Firm Value, and the Role of Corporate Social Responsibility Initiatives”, Journal of International Business Studies, 48(3): 360-385.

- Fama EF. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance; 25(2):383-417. Available from: http://www.jstor.org/stable/2325486

- Fatemi, A., Glaum, M., & Kaiser, S. (2017). ESG Performance and Firm Value: The Moderating Role of Disclosure. Global Finance Journal, 38, 45-64. https://doi.org/10.1016/j.gfj.2017.03.001

- Harjoto, M. A. and Jo, H. (2015), “Legal vs. Normative CSR: Differential Impact on Analyst Dispersion, Stock Return Volatility, Cost of Capital, and Firm Value”, Journal of Business Ethics, 128(1): 1-20.

- Hart, S.L. (1995). A Natural Resource Based View of the Firm. Academy of Management Review, 20(4), 986–1014.

- Horvathova, E. (2010), “Does Environmental Performance Affect Financial Performance? A Meta-analysis”, Ecological Economics, 70, 52–59.

- Ifada, L.I., Munawaroh, I.K. & Fuad, K. (2021). Environmental Performance Announcement and Shareholder Value: The Role of Environmental Disclosure. L. Barolli et al. (Eds.): pp. 426–434. https://doi.org/10.1007/978-3-030-79725-6_42

- Jo, H. and Harjoto, M. A. (2011), “Corporate Governance and Firm Value: The Impact of Corporate Social Responsibility”, Journal of Business Ethics, 103(3): 351-383.

- Li, X., Wong, W., Lamoureux, E.L. & Wong, T.Y. (2012). Are Linear Regression Techniques Appropriate for Analysis when the Dependent (outcome) Variable is not Normally Distributed? Investigative Ophthalmology & Visual Science, 53, 3082-3083; https://doi.org/10.1167/lovs.12-9967

- Luluk, I., Faisal, , Ghozali, I.: (2019). Company Attributes and Firm Value: Evidence From Companies Listed on Jakarta Islamic index. Espacios 40(2018), 11

- Mahoney, L., Roberts, R. W. 2007. Corporate Social Performance, Financial Performance and Institutional Ownership in Canadian Firms. Accounting Forum, 31 (3), 233-253.

- Malarvizhi, P. and Matta, R. (2016), “Link between Corporate Environmental Disclosure and Firm Performance”–Perception or Reality?”, The British Accounting Review, 36(1): 107-117.

- Maliah Sulaiman, Norsyahida Mokhtar (2012), Ensuring Sustainability: A Preliminary Study of Environmental Management Accounting in Malaysia; International Journal of Business and Management Science, Volume 51(2). 85-102.

- McBarnet D., Voiculescu, A. and Campbell, T. (2007), The New Corporate Accountability: Corporate Social Responsibility and the Law, (Eds), Cambridge University Press: Cambridge, UK.

- McWilliams, A. & Siegel, D. (2000). “Corporate Social Responsibility and Financial Performance”, Strategic Management Journal, 21(5): 603-609.

- Plumlee, M., Brown, D., Hayes, R.M., Marshall, R.S. (2015). Voluntary Environmental Disclosure Quality and Firm Value: Further Evidence. J. Account. Public Policy 34(4), 336–361. https://doi.org/10.1016/j.jaccpubpol.2015.04.004, https://doi.org/10.1016/j.jaccpubpol.2013.06.008

- Ofoegbu, G. N., Odoemelam, N., & Okafor, R. G. (2018). Corporate board characteristics and environmental disclosure quantity: Evidence from South Africa (integrated reporting) and Nigeria (traditional reporting). Cogent Business & Management, 5(1). https://doi.org/10.1080/23311975.2018.1551510

- Qiu, Y., Shaukat, A. & Tharyan, R. (2015). Environmental and Social Disclosures: Link with Corporate Financial Performance.

- Rezaee, Z. (2016). Business Sustainability Research: A Theoretical and Integrated Perspective. J. Account. Lit. 36, 48–64. https://doi.org/10.1016/j.acclit.2016.05.003

- Saleh, M., Zulkifli, N., Muhamad, R. 2011. Looking for Evidence of The Relationship between Corporate Social Responsibility and Corporate Financial Performance in an Emerging Market. Asia-Pacific Journal of Business Administration, 3 (2), 165-190.

- Siagian, F., Siregar, S. V. and Rahadian, Y. (2013), “Corporate Governance, Reporting Quality, and Firm Value: Evidence from Indonesia”, Journal of Accounting in Emerging Economies, 3(1): 4-20.

- van de Burgwal, D., Vieira, R.J.O. (2014). Environmental Disclosure Determinants in Dutch Listed Companies. Revista Contabilidade & Finanças – USP 25(64), 60–78

- Wang, M. (2015). The Relationship Between Environmental Information Disclosure and Firm Valuation : The Role of Corporate Governance. https://doi.org/10.1007/s11135-015-0194-0

- Yadav, P. L., Han, S. H. & Rho, J. J. (2016), “Impact of Environmental Performance on Firm Value for Sustainable Investment: Evidence from Large US Firms”, Business Strategy and the Environment, 25(6): 402-420.

- Yang, Y, Zhang, J. & Li, Y. (2023). The Effects of Environmental Information Disclosure on Stock Price Synchronicity in Heliyon, 9, https://doi.org/10.1016/j.heliyon.2023.e16271, 1-18

- Zhang, J. & Yang, Y. (2023). Can Environmental Disclosure Improve Price Efficiency? The Perspective of Price Delay, Finance Research Letters, 52, 103556, https://doi.org/10.1016/j.frl.2022.103556.

- Zhou, H., & Yin, H. (2017). Stock Market Reactions to Environmental Disclosures : New Evidence from China. Applied Economics Letters, 00(00), 1–4. https://doi.org/10.1080/13504851.2017.1383590