Effects of Loan Management on Financial Performance of I&M Bank, Rwanda

- Emilienne Nsomandera Kayumba

- 1105-1130

- Jun 7, 2024

- Financial management

Effects of Loan Management on Financial Performance of I&M Bank, Rwanda

Emilienne Nsomandera Kayumba

Business Administration, Accounting and Finance Department,

University of Kigali

DOI: https://dx.doi.org/10.47772/IJRISS.2024.805077

Received: 29 April 2024; Accepted: 07 May 2024; Published: 07 June 2024

ABSTRACT

Managing loan successfully has always been a challenge for bankers: Lend funds or not lend funds to clients. This paper examined the effects of loan management on financial performance of I&M Bank, Rwanda between 2018 and 2022. The specific goal of the study was to ascertain the effects of credit risk assessment practices on financial performance, the effect of loan monitoring procedures and loan recovery strategies on financial performance of the bank. The developed theories of loan pricing theory, modern portfolio theory and agency theory served as the foundation stone for this investigation. These theories were tested by descriptive statistics of mean, standard deviation coupled with multiple regression analysis from the questionnaire as the instrument and return on assets document. The results show that, credit risk assessment practices regressed at β1 = 0.640 with a value of p<0.05, had a significant positive effect on I&M Bank’s financial performance. This is evidenced by the return on asset that successively ran as follows: 3.4% in 2018, 3.7% in 2019, 1,7% in 2020 and 5.9% in 2021, then 6.5% in 2022, with the return on equity that was 14% in 2018, 14.3% in 2019, 12.9% in 2020 and 16.3% in 2021, then 17.3% in 2022. Therefore, these results demonstrate that credit risk assessment improves Rwanda banking institutions’ financial performance.

Keywords: Loan pricing theory, modern portfolio theory, agency theory, Credit, monitoring procedure, risk assessment, practices, effect, technology, guidelines, financial performance, and I & M Bank

INTRODUCTION

Background to the study

Commercial banks are essential to the world economy because, they mobilize savings and lend money to both individuals and companies. For this reason, to sustain financial stability and spur economic growth, the financial performance of banks is crucial. One of the main duties of commercial banks is loan management. Banks’ financial health can be greatly impacted by how they manage their loan portfolios, including loan quality, interest rates, and risk assessment. The banking industry continues to play a crucial role in funding economic activity, and its success may have a positive effect on the economy as a whole because, a healthy and profitable banking sector is better equipped to withstand shocks and support the financial system stability. Consequently, academic research has become interested in the factors that influence bank performance, bank management, financial markets and bank supervisors since the knowledge of the internal and external determinants of banks’ profits and margins is essential for various parties as(Athanasoglou, 2015) has equally put it.

The majority of developments in Africa that increase the liquidity of the loan portfolio have an impact on price risk. Price risk has historically had no impact on the lending operations of the majority of Ghanaian banks. Accounting doctrine required book value accounting treatment because loans were typically held to maturity. However, as the market for loans grows and deepens, and banks adopt more active credit risk assessment practices, the loan portfolio became more vulnerable to price risk (Nnanna, 2015).

As financial intermediaries that serve as a bridge between the surplus and deficit economic units, commercial banks dominate the Kenyan financial system. The global financial crisis, according to the Kenyan Union of Savings and Credit Cooperative, has caused savings growth rates to decline. In 2018, savings growth was 7.6%, down from 31.2% in 2017. According to interviews, Kenyan banks have noticed an increase in loan demand, but they have responded cautiously. Lending money to clients is how banks make the most money. Indeed, loans account for 50–75% of all assets of commercial banks, making them their most valuable assets. Thus, loans make major contributions to economic growth of any country. Therefore, effective loan management benefits the lending organization as well as the borrowers and the nation as a whole (George, 2019).

On the other hand, Wackers, Smit Rick, Stadhouders, and Jeurissen (2023) argued in their abstract on the evaluation of the relationship between financial performance, and long-term bank loan interest rates, for healthcare providers in the Netherlands with a panel data analysis. They support that, commercial loans are the primary source of funding for the Dutch health system, particularly; in light of the abandonment of government investment guarantees, following the market-oriented reform of 2006. The goal of commercial capital was to enhance effective capital management and allocation. They examined how interest rates, investments, and allocative efficiency were affected by commercial bank loans in the Dutch healthcare industry. Thus, they proposed that the reform lowered interest rates for financially successful providers be applied in an effort to explain the variation in interest rates. This can be done by using financial performance data from publicly available annual reports of healthcare providers.

The method used for this study was pooled linear regressions. The findings demonstrated that between 2011 and 2023, financial reserves grew consistently in spite of low profitability. Interest rates on capital loans did not significantly correlate with the financial performance of healthcare providers, and capital costs do not seem to be improved by maintaining larger financial reserves. Consequently, this study recommended that healthcare providers think about whether or not financial reserves would be better off used for direct investments or kept at their current levels.

However, in their research on the factors that contribute to non-performing loans, Manz (2019) questioned: What do we know? For the non-performing loan (NPL) issue, policy makers credit high relevance like the European Central Bank, and this is currently addressed with a variety of measures. This systematic review identifies avenues for future research on the subject. Therefore, a thorough understanding of the underlying factors is required for any policy admissive response. Additionally, the NPL sector’s data availability increased, enabling researchers to conduct more advanced studies to date. The literature is presented in three overarching themes—macroeconomic events, bank and loan-specific factors by offering innovative interpretations, all of which overlap. The findings indicate that more empirical research is needed to fully understand how loan and asset-specific events interact with macroeconomic and ban-specific factors.

These previous research studies mentioned have shed light on the problems with loans and financial performance worldwide, specifically non-performing loans. The veins that have streamlined and guided this research are loan, financial performance, long-term bank interest rates, loan portfolio, loan quality, interest rates, and risk assessment. Now, “Does loan management affect the financial performance of banks?” was the main query of this investigation.

Statement of the problem

Because more banks are using credit standards, credit analysis, appraisal, and credit control as they try to employ best practices in loan management, there are more credit risks associated with this increase in banks. Even though these businesses have tried to adhere to credit guidelines and policies with practice prudent lending, many are still confronted with the problem of loan delinquency (Mathra, 2016). Despite better loan management practices in banking institutions, the World Bank’s quarterly financial report of 2019 shows that, the non-performing rate rose by 15% and the loan default rate increased by 16%. This trend not only threatens the institutions’ survival, butalso prevents them from fulfilling the purpose for which they were established. These consist of offering high-quality loans and services that can meet the requirements of people who are unable to obtain loans from conventional financial institutions (Parrenas, 2018). Commercial banks have created standards that ensure loans are timely returned, and without causing conflicts with the borrowers to maintain friendly transformational relationships with their clients. Evidence has revealed that, a sizable portion of these loans are not repaid, even with commercial banks’ best efforts to guarantee timely recovery of all loans. This problem endangers not just the achievement of objectives, but also the effectiveness and long-term viability of the bank. As a result, efficient loan management is required, and loans must be carefully managed to reduce any risks that might have negative impact on the bank’s performance as (Gudmundsson, 2019) put it.

To guarantee that Loan Exposure Risk are reduced, the government established the National Bank of Rwanda (2019). Accordingly, this Bank established several forms of inadequate loan management that affect the banking industry in Rwanda. The National Bank of Rwanda (2019) reported that, from the last quarter of 2017 to the first quarter of 2018, the majority of Rwanda financial institutions experienced a sharp decline in the loan-granting process. This sharp decline is thought to be related to an inability to apply appropriate credit risk management techniques, which is why the ratio of non-performing loans (NPLs) increased from 1.7% in 2018 to 14.8% in 2019. By analyzing the effects of credit risk assessment practiceson the financial performance of I&M Bank, Rwanda, this research study aimed to close the gap.

Significance of this research study

This study has contributed to commercial bank policy makers’ strategies to identify the main challenges facing agent banking operations, and create solutions that will improve financial performance. To ensure the institution’s ongoing existence and financial success, this study has also provided plans, strategies, and guidelines that can be put into practice, making I&M Bank recognize and understand the loan management environment.

Research objective

The main objective of this paper is to determine the effects of loan management on financial performance of I&M Bank, Rwanda.

This paper rests on the following objectives:

1. To determine the effect of credit risk assessment practices on financial performance of I&M Bank, Rwanda.

2. To assess the effect of loan recovery strategies on financial performance of I&M Bank, Rwanda.

3. To determine the effect of loan monitoring procedures on financial performance of I&M Bank, Rwanda.

H01. There is no effect of credit risk assessment practices on financial performance of I&M Bank.

H02. There is no effect of loan recovery strategies on financial performance of I&M Bank.

H03. There is no effect of loan monitoring procedures on financial performance of I&M Bank.

LITERATURE REVIEW

The primary goal of a conceptual review is to offer a comprehensive understanding of the conceptual underpinnings of a research area. This study focuses on the characteristics and components of loan management and financial performance in commercial banks.

Credit risk assessment practices

Financial institutions use basic procedures known as credit risk assessment practices to determine a borrower’s creditworthiness and estimate the likelihood that they will default on their loan. These procedures are necessary for controlling credit risk in a loan portfolio and for making well-informed lending decisions (Baesens, 2017). In this framework, banks are meticulous in verifying the borrower’s financial capacity of loan reimbursement to ensure, whether or not, they will be able to return the money they had borrowed.

Indeed, banks typically audit the data that customers have submitted in their loan files to the credit department to obtain loans before providing money to their customers. Concerned bank officials demand a mortgage in this exercise, or any asset that could serve as a guarantee that they would be able to return the money they had borrowed. If they do not, the mortgage would compensate the loss of the bank’s money. But occasionally, this requirement prevents clients from being given the chance to borrow money from banks because, some of them have trouble providing sufficient affidavits. In this case, financial institutions have the right to refuse a client a loan.

Based on the borrower’s data, credit scoring models are mathematical algorithms that determine a credit score. Unfortunately, some borrowers fail to return funds they had borrowed from the bank because of lack of financial management skills, or they simply misuse the funds for futilities.

This is why credit risk assessment is a critical metric for the Debt-to-Income Ratio (DTI). It evaluates the difference between a borrower’s monthly income and debt payments. A high DTI indicates a greater risk of credit. Depending on their willingness to take on risk, lenders set the maximum permissible DTI ratios. Moreover, when comparing loan amount to the estimated value of the collateral (for secured loans), the Loan-to-Value Ratio (LTV) should be taken into account. Lenders are exposed to more risk when LTV ratios are higher because borrowers may have less equity at stake. As a result, maximum LTV ratios are set by lenders based on the kind of collateral and the state of the market (JoEtta, 2017). This review process is always carried out against assets the borrowers possess, and bank lenders capitalize on this to assess how much they can benefit from the borrowers in terms of interest rate, which is in line with their financial performances. However, not all credit borrowers’ own assets since some rely only on monthly salary income to get loan from the financial institutions, and, thus; the institution face a challenge to let go their funds.

Loan recovery strategies

Loan recovery strategies are necessary for financial institutions to lessen their losses in the event that the borrower’s default on their loans. For this reason, diverse techniques and methods are utilized to retrieve money from past-due debtors and oversee non-performing loans (NPLs). Indeed, the performance of the loan portfolio of a financial institution is directly impacted by loan recovery techniques. Metrics like the percentage of non-performing loans (NPLs), charge-off rates, and the overall quality of the loan portfolio are all impacted by how well these strategies work (Mjinair, 2016). That is why banks require beforehand from borrowers any guarantee of reimbursing funds they need to perform their businesses. Otherwise, they will demonstrate a strong reservation vis-à-vis potential borrowers that may not be capable of returning funds of the bank.

For sure, strategies for recovering loans are intimately related to a financial institution’s risk management. Besides, various recovery tactics have the potential to reduce or increase credit risk. Effective strategies can raise credit risk, whereas; successful loan workouts or efficient liquidation of collateral can lower it. The amount of loan loss provisions that a financial institution must set aside can change depending on loan recovery tactics. Lower provisions as a result of successful recovery techniques can enhance the institution’s financial situation. Depending on the loan recovery strategies, selected financial institution’s underwriting standards during the loan origination process may vary. Knowing that there are efficient recovery options available may give lenders more latitude when making lending decisions when a recovery strategy is well-established (Mjinair, 2016). To this end, bankers are very critical with loaning funds to individuals because, they want to ensure what secures their interest rate in lending funds out to their clients. This is the only best way for bankers to identify their prestigious clients.

The operational expenses of loan management may be impacted by the efficacy and efficiency of loan recovery techniques. For example, cost savings can result from the use of data analytics and streamlined processes. Loan recovery tactics have the power to change borrowers’ opinions of financial institutions. Recuperation techniques that are moral and customer-focused can support preserving a good reputation and clientele (Sinkey, 2015). Indeed, this author concluded that, financial institutions must ensure that their recovery plans comply with all applicable laws and regulations. Effective loan management requires compliance; non-compliance can lead to fines and harm to one’s reputation.

Procedures for loan monitoring are essential to efficient administration of loans in financial institutions. These procedures involve ongoing monitoring and assessment of a loan portfolio to ensure that loans remain in good standing, borrowers are meeting their obligations, and any potential signs of risk or distress are identified early on. The purpose of loan monitoring procedures is to spot new risks and weaknesses in the loan portfolio. Thus, financial institutions can take proactive steps to reduce these risks, like restructuring loans or building reserves, thanks to early detection (Engle, 2014). On the contrary Engle misses the point that, when banks experience shortage of clients to borrow funds, they recur to market department and cry out for customer care and offer opportunities of loaning to their clients in such slogans; “mortgage loan,” “fee or tuition loan”, “housing loan” to attract clients when they are desperately in need of financial performance increase. Still, Engle confirms that, loan portfolio health, on the whole, can be understood through ongoing loan monitoring. Tracking important indicators like delinquency rates, credit quality trends, and non-performingloan (NPL) ratios is part of this evaluation. The results of loan monitoring processes may have an impact on future loan underwriting requirements for a financial institution.

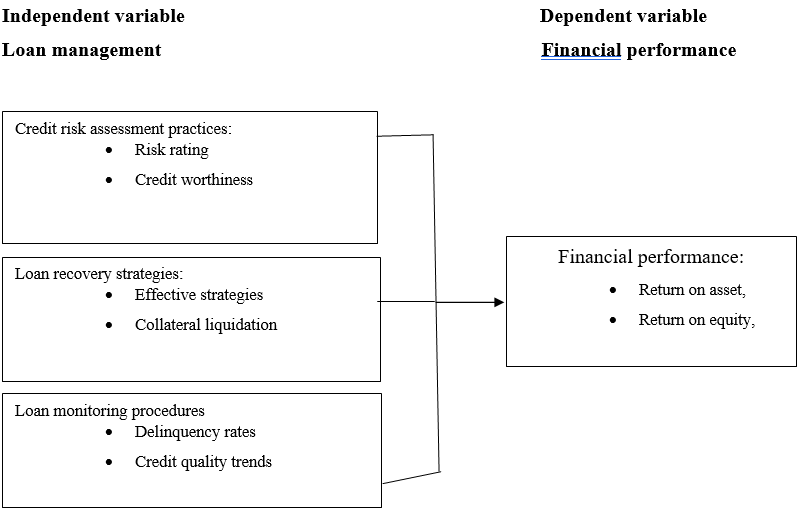

Conceptual framework

A conceptual framework includes an overview of the research characteristics that have shaped the study. In contrast to the dependent variable attributes, it has both independent attributes. The conceptual framework was created following a thorough analysis of the body of prior research. The relationship between the variables under investigation is explained by the model.

Figure 1: Conceptual framework

Source: Research conceptualization, 2023

Financial performance

Most recent studies qualified bank financial stability as extremely important and requires careful management and supervision. For sure,banking institutions need to use strong financial management strategies, such as competent risk assessment, careful loan portfolio supervision, cost containment, and competent investment oversight, to maintain a strong financial foundation. This approach enables banks to maintain their competitiveness in the industry, grow their operations, and provide their clients with essential financial services (Haripriya, 2017) confirmed it. Although bank financial performance management optimizes balance sheets made up of assets and liabilities, it ignores the fact that people are the most important asset for loan repayment to cover loans and improve bank financial performance. Additionally, the debt that banks owe to others has a negative impact on their performance as financial institutions, since equity is defined as the sum of all assets less all liabilities. Besides, human resources are practically intangible, and it can be difficult to understand how they can be assets that improve a financial institution’s performance, as Maiti and Vulcovic (2020) similarly proved it. Nonetheless, there will not be any improvement in the bank’s overall financial performance if there is not any human capital to appraise the interest-generating activities for the organization.

Thus, financial performance indicators play a major role in assessing the operational and financial well-being of banking institutions. These metrics are essential instruments for measuring and evaluating the overall financial health of the institution. They assess critical factors like the organization’s ability to manage risks well, profitability, liquidity, and sound financial standing as Haripriya (2017) stated that, they comprise among other things:

One financial metric that evaluates a company’s profitability in relation to its total assets is the Return on Assets, ROA for short. It provides information about how well a company’s management uses its resources to turn a profit. ROA is usually expressed as a percentage and is computed by dividing a company’s annual earnings by its total assets. Similarly, “Return on investment” (ROI) is another term that may be used to describe ROA in some situations. Thus, it is crucial to remember that a company’s assets are made up of both debt and equity, both of which are necessary sources of funding for the business’s ongoing operations and long-term goals. For investors and analysts, return on assets (ROA) is to make a profit. This is a useful indicator of how well business uses its resource to make profits (Haripriya, 2017).

Because a company’s total assets can fluctuate over time, it is common practice to use the average total assets when calculating Return on Assets (ROA). These variations can be caused by a number of factors, including changes in inventory, seasonal shifts in sales, and the purchase or sale of cars, land, and equipment. As a result, using the average total assets for the particular period in question produces a more accurate ROA calculation than using the total assets from a single period. Usually, the beginning and ending total assets for the period are added together and divided by two to get the average total assets. With this method, the asset base of the company for the relevant period is measured in a more consistent and representative manner. A company’s balance sheet, a financial statement that gives you an overview of its financial position at a specific point in time, is a convenient place to find the total assets reported for that company (Haripriya, 2017). This gauges how well the bank uses its resources to turn a profit. ROA is calculated as follows:

Net Income/Average Total Assets

Furthermore, a financial metric called return on equity (ROE) evaluates the connection between a company’s net earnings and the total equity held by its investors. The fundamental idea is that, a greater ROE indicates a quicker rate of dividend growth and, as a result, a rise in the intrinsic value of the business. In essence, return on equity (ROE) gauges how well investor contributions have converted into profits for the business. Indeed, ROE serves as a barometer of the company’s ability to make money relative to the equity that investors have put in it (Haripriya, 2017). This way companies and investors can mutually benefit their interests to harvest.A financial performance metric called return on equity (ROE) is calculated by dividing net income by shareholders’ equity to determine how profitable a company is. In essence, return on equity (ROE) calculates a company’s profitability in relation to the equity that its investors have contributed. The difference between a company’s total assets and total debt is known as its shareholders’ equity, and it represents the ownership stake in that business.For this reason, return on equity (ROE) is often interpreted as the return on the net assets owned by the company’s shareholders. It is a vital indicator of a business’s capacity to pay returns to equity holders and a crucial metric in evaluating its financial performance and shareholder value (Haripriya, 2017). This measures the bank’s profitability in relation to its equity. The formula for ROA is:

Net Income/Shareholders’ Equity

After navigating through conceptual review, it is time this paper turned to theoretical review. The purpose of the theoretical review is to define a term in terms of the theories of a particular field. It clarifies the idea and supports the assumption of knowledge about and acceptance of theories pertaining to financial performance and loan management. This is what follows in the thread of argument hereafter.

Credit risk assessment practices and financial performance

Nyamwange’s (2010) research was to determine how the credit risk of Kenyan SACCOs correlated with their financial performance. Forty-one (41) SACCOs made up the study’s sample size. Questionnaires were employed to gather crucial data about the population. The Statistical Package for Social Science (SPSS version 17) was used to modify, categorize, code, and tabulate to analyze quantitative data after the respondents’ answers to questions. For easier comprehension and analysis, data were represented through tables and charts. The data were carefully scrutinized and verified against accuracy for comprehension. After that, they were tallied, coded rand summarized. According to the study’s findings, SACCOs implemented credit risk management procedures to mitigate the credit risks to which they are exposed. The association SACCOs’ financial performance and their credit risk management was determined using inferential statistics. The study also found that, to reduce loan loss, SACCO uses a variety of methods for risk screening and analysis prior to granting credit to clients. This included using security and collateral to establish conditions competition, and capacity.

In their 2012 study, Grace N. Mwangi examined how credit risk management affected commercial banks’ bottom lines. Descriptive research design was the method employed for this investigation. The study’s design was appropriate because it looked closely at credit risk management. This gave a thorough explanation of how credit risk management and the financial performance of commercial banks are closely related. Thus, commercial bank’s annual reports from 2007to 2011 provided secondary data that were used. Multiple regression analysis revealed the information obtained from the bank’s annual reports. Results of the regression were acquired using Statistical Package for Social Sciences (SPSS version 18). The profitability indicator in the model was return on equity (ROE), and the credit risk management indicators were the capital adequacy ratio (CAR) and the non-performing loans ratio (NPLR).

This study demonstrated a substantial correlation between credit risk management which is measured by loan performance and capital adequacy, and financial performance that is measured by profitability. According to the analysis’s findings, return on equity (ROE) is negatively and relatively significantly impacted by both the non-performing loans ratio (NPLR) and the capital adequacy ratio (CAR), with NPLR’s impact being more pronounced than CAR’s. Because of this, the regression on the whole is significant, indicating that ROE can be reliably predicted by NPLR and CAR. After demonstrating a link between commercial banks’ financial performance and credit risk management, the researcher recommends that all banks implement a credit risk grading system. The borrower’s risk profile should be defined by the system to guarantee account balances. Thus, credit applications should make it clear that the borrower risk grades are measured against their loaning capacity.

At last, Poudel (2015) examined a confluence of variables related to credit risk management and how they impact on the bottom line of banks. Indeed, the study’s parameters included the capital adequacy ratio, cost per loan asset, and default rate. For eleven years (2001–2011), 31 banks’ financial reports were analyzed using descriptive, correlation, and regression analysis to compare the profitability ratio to the default rate, cost of per loan asset, and capital adequacy ratio. The best measure of a bank’s financial performance, according to this study, is its default rate, that is all other factors have the opposite effect on it. As a result, banks ought to create and carry out strategies that will lower their expose to credit risk while raising profitability at the same time.

Research gap

As previously established empirically, Elizabeth Yost (2021) aimed to analyze restaurant financial performance in the United States following the COVID-19 pandemic; Ravi Prakash Sharma Poudel (2015) investigated different aspects of credit risk management as they related to banks’ financial performance, considering 31 Indian banks over an 11-year period from 2001 to 2011; and Grace N. Mwangi (2012) looked at 41 Kenyan banks over a five-year period to determine how credit risk management affected the financial performance of commercial banks. Their objective was to show a relationship between the performance of commercial banks and other microfinance organization and loan management. To close the gap, however, this study used I&M as a case study and looked at how the effect of credit risk assessment practices affects financial performance of I&M Bank, Rwanda over a five period, that is from 2018 to 2022.

METHODOLOGY

This study utilized descriptive survey design to study how loan management affects financial performance today. A descriptive and correlation research design were applied tovalidate the hypothesis connected to the study objectives to turn data into intelligent and knowledgeable information.

Population and sample size

The researcher purposefully chose to sample 14 I&M Bank branches in Rwanda to accomplish this. Indeed, the researcher must ascertain how many participants are required for the study following Grinnell and Williams’ technique (1990).The sample size that was chosen is extensive and includes a cross-section of I&M Bank employees in addition to the branches themselves. One manager, one credit officer, one credit recovery officer, and one accountant from each of the 14 branches make up the sample specifically I&M Bank (2023).

Based on this definition of small population, this study opted to select participants using non-probability sampling to save costs, time and obtain pertinent data that have generated pertinent information regarding the solution to the research problem at hand. Thus, in order to conduct a thorough analysis, the researcher selected a sample size of 14 managers, 14 credit officers, 14 loan recovery officers, and 14 accountants, for a total of 56 participants in this study. The study aimed to obtain a thorough understanding of loan management practices and their impact by including individuals from these crucial roles within the banking institution.

Questionnaires were the main tool used in this study to accomplish the goal of the investigation. A 5-point Likert scale was used to make respondents air their views on the research issues, that is the effects of loan management on financial performance of I&M Bank that were established through statements. The scale ranges as follows: Strongly Agree (SD=1, verynegative attitude), Disagree (S=2, negative attitude), Neutral (N=3, reserved attitude), Agree (A=4, positive attitude), Strongly Agree (SA=5, very positive attitude). The interval between scales is the same. The researcher set the questionnaires directly to collect data from I&M Bank employees. Staff responses were carefully gathered and served as the foundation for further scientific interpretation and analysis. In addition, textbooks offered a variety of relevant literature with numerous reports and journals that contain data on the financial performance of I&M Bank and the Head Office branch’s loan management procedures. The researcher used this to analyze and interpret financial performance data.

Reliability and validity measurements

The consistency of one’s measurement, or the measurement accuracy of an instrument under identical conditions with comparable objects is reliability. The most popular internal consistency metric was utilized. A subset of respondents, or (10%) of the sample, responded to the survey twice, spaced out by a predetermined amount of time. To ensure that the measurements remained stable over time, the correlation between their answers was computed. Significant reliability was indicated by a high correlation.

Thus, Cronbach’s alpha was calculated to evaluate internal consistency of data because the study used multiple items to measure variables such as credit risk assessment, loan recovery, and loan monitoring. Items within each variable were indicated by high alpha values. The survey responses were subjected to exploratory factor analysis in order to evaluate the degree to which the items were collaborating. Thus, items were changed or eliminated if they did not load properly on the corresponding factors. Consequently, this played a role in the correlation between the two variables that was discovered. In addition, a correlation analysis was performed to verify that the measurements remained stable over time. Given that the Cronbach’s Alpha of 0.623 is fairly high and indicates strong internal consistency among the items, a high correlation suggests significant reliability. This implies a strong correlation between the questionnaire’s items.

The relevance and accuracy of conclusions that are typically based on research findings are known as validity. The questionnaire was evaluated to ensure the respondents understood it. Six randomly selected bank professionals participated in a pilot study. They offered comments regarding the survey questions’ comprehensibility and clarity. The purpose of the pilot test aimed to ascertain participants comprehended the survey questions. The review of previous research studies and literature in the field served as confirmation that, the variables selected had been effectively employed in comparable studies. This aided in proving the content validity.

As a result, the power comparison of Shapiro-Wilk test’s p-value, which is also relatively high, is 0.346 when subjected to the normalcy test. The findings do not provide compelling evidence that the data materially deviates from a normal distribution. This is a better outcome suggesting that, the data in this study may fairly follow a normal distribution. This aided in proving the content validity.

Analyzing involves looking for and locating significant patterns in data. Analysis of data is the process of classifying, arranging, modifying, and summarizing them to provide answers to research questions. After being edited, coded, and categorized according to similarity, the data of this research were tabulated.

This study used descriptive statistics which was performed by applying SPSS software tool, including measures of central tendency and dispersion, which concerns Mean and Standard Deviation, and were performed and activated to screen the data. For this reason, tables displaying descriptive statistics were based on means and standard deviations.

Regression analysis and correlation analysis served as the foundation for inferential statistics in this research. The multiple regression model that was used is:

Y= β0+β1X1+ β2X2+ β3X3+ɛ

Key:

Y = Financial performance

X1 = Credit risk assessment practices

X2 = Loan recovery strategies

X3 = Loan monitoring procedures

β0 = Coefficient of intercept (Constant).

β1… β3 = Coefficient of estimates X1… X3

ɛ: Standard Error of Estimate (Std Error)

Studies of correlation

In this study, the relationship between one dependent variable, or the measure, and several independent variables, or predictors, was examined using multiple regression tests. Pearson product-moment correlation was used to determine how much variation in one variable explains variation in the other. The square of the multiple correlation or R2, between the two variables was used to calculate the degree of correlation between the independent and dependent variables. This relationship between two variables is always indicated by the correlation coefficient, which goes from -1, 00 (a perfect negative relationship) to +1, 00 (—a perfect positive relationship) and 0, 00 (a relationship of no significance).The critic should keep in mind that, these kinds of perfect relationships are uncommon and that coefficients like 0.86 or -0, 58 are more frequently preceded by decimals. However, since (Struwig& Stead, 2003, pp. 160-162) supported this approach, Analysis of Variance, or ANOVA, was also utilized to ascertain whether or not there is a statistically significant difference between independent variables in terms of mean differences of a measure or dependent variable.

DATA ANALYSIS, INTERPRETATION AND DISCUSSION OF FINDINGS

The presentation, interpretation, and analysis of the results are introduced in this chapter. Based on the various study objectives, the effects of loan management on financial performance at I&M Bank were examined throughout this chapter.

Information for this research was acquired from a substantial sample of key roles at I&M Bank. Overall, by responding to the questionnaires, fourteen managers, fourteen credit officers, fourteen credit recovery officers, and fourteen accountants from different bank branches participated in the study. The remarkable 100% response rate, which indicates that every person who was contacted completed the surveys, is remarkable. The high response rate enhances the representativeness and reliability of the data because, it shows a deep understanding of the thoughts and perspectives from various bank functions. The study’s validity and the reliability of the conclusions reached from the data gathered are enhanced by the respondents’ willingness and active participation in the research.

Demographic characteristics of respondents

As indicated in tables 4.1 and 4.2, the respondents’ profiles include their working experiences in addition to their age, gender, marital status, and level of education.

Table 4.1. Demographic characteristics of respondents

| Frequency | Percentages | ||

| Age | Below 30 years | 12 | 21.4% |

| 31-40 years | 29 | 51.8% | |

| 41-50 years | 10 | 17.9% | |

| Above 50 years | 5 | 8.9% | |

| Total | 56 | 100.0% | |

| Gender | Male | 33 | 58.9% |

| Female | 23 | 41.1% | |

| Total | 56 | 100.0% | |

| Marital status | Single | 13 | 23.2% |

| Married | 43 | 76.8% | |

| Total | 56 | 100.0% | |

| Education | Diploma | 7 | 12.5% |

| Bachelor’s | 41 | 73.2% | |

| Master’s | 8 | 14.3% | |

| PhD | 0 | 0.0% | |

| Total | 56 | 100.0% | |

Source: Field data (2023)

Table 4.1. shows that demographic characteristics of the respondents, consisting of 56 individuals, which provide a comprehensive picture of the sample’s composition. In terms of age distribution, the majority of respondents fall within the age range of 31-40 years, constituting 51.8%, followed by those below 30 years at 21.4%. A smaller proportion comprises individuals between 41-50 years (17.9%), and those above 50 years (8.9%). Regarding gender, the majority of respondents are male, accounting for 58.9%, while females make up 41.1% of the sample. In terms of marital status, a significant percentage of respondents are married (76.8%), with the remaining 23.2% identifying as single. The educational background of the respondents reveals a diverse group, with 73.2% holding Bachelor’s degrees, 14.3% with Master’s degrees, and 12.5% possessing Diplomas. Notably, no respondents reported having a Ph.D. These demographic perceptions provide a foundation for understanding the diversity and representation within the study’s sample, which is crucial for interpreting and generalizing the study’s findings.

Therefore, this is influential in contextualizing the study’s exploration of the effects of loan management on the financial performance of I&M Bank in Rwanda. The age distribution reflects a balanced representation across different age groups, ensuring insights from various career stages within the bank. Given that the majority fall into the 31-40 of age range, it is possible that this demographic has a big influence on loan management. The gender distribution highlights a predominant male presence, emphasizing the need to consider potential gender-specific perspectives in this study. The marital status and educational backgrounds provide additional dimensions for understanding the respondents’ professional experiences and decision-making capacities within the banking environment. This diverse demographic composition underscores the relevance and applicability of the study’s findings, contributing to a holistic understanding of the impact of loan management practices on the financial performance of I&M Bank in Rwanda.

| Frequency | Percent | ||

| Experience | Below 1 year | 7 | 12.5 |

| Between 2-5 years | 22 | 39.3 | |

| 6 years and over | 27 | 48.2 | |

| Total | 56 | 100.0 | |

Source: Field data (2023)

Table 4.2. The distribution of respondents according to their professional experience within the framework of the academic research study is shown in Table 4.2. Almost half of the respondents, accounting for 48.2%, have 6 years of experience or more, indicating a substantial pool of seasoned professionals within the sample. Another significant portion, 39.3%, falls within the 2-5 years of experience range, suggesting a considerable group with intermediate expertise. A smaller but significant proportion, 12.5%, reported having less than 1 year of experience. This distribution highlights a diverse range of professional backgrounds among the respondents, encompassing both experienced and relatively newer individuals within the banking industry. Such diversity is crucial for capturing a comprehensive understanding of the effect of loan management on the financial performance of I&M Bank, as it combines perceptions from individuals with varying levels of industry exposure and expertise.

Based on the objective of the study, the researcher had to both quantitatively and qualitatively examine the effects of credit risk assessment practices of I&M Bank, from 2018 up to 2022, using descriptive statistics, specifically measures of central tendencies (Mean) and dispersion (Standard Deviation).

Table 4.3. Effects of credit risk assessment practices on financial performance

| N | Mean | Std. Deviation | |

| The risk rating and credit worthiness systems used at I&M Bank are effective in assessing borrower creditworthiness. | 56 | 4.7679 | .73833 |

| I&M Bank’s credit risk assessment practices has improved financial performance, over the past year, as measured by its assets. | 56 | 4.9107 | .39436 |

| The I&M Bank’s equity has been positively impacted by credit risk assessment practices. | 56 | 4.9286 | .32233 |

| The risk rating and credit worthiness practices at I&M Bank contribute to better loan portfolio quality. | 56 | 4.9643 | .18726 |

| The credit risk assessment practices at I&M Bank align with industry best practices. | 56 | 4.9107 | .43804 |

| Valid N (listwise) | 56 |

Source: Field data (2023)

Table 4.3 shows that, respondents were asked to rate the effectiveness of credit risk assessment practices at I&M Bank on financial performance. The data indicates a high level of agreement among the participants. Specifically, respondents strongly agree (mean = 4.7679, Std. Deviation = .73833) that the risk rating and credit worthiness systems employed by I&M Bank are effective in assessing borrower creditworthiness. Moreover, the participants express even stronger agreement that these credit risk assessment practices have led to improved financial performance over the past five years, as measured by assets (mean = 4.9107, Std. Deviation = .39436). The positive effect of credit risk assessment practices on I&M Bank’s equity is also evident, with respondents strongly agreeing (mean = 4.9286, Std. Deviation = .32233). Additionally, the risk rating and credit worthiness practices are perceived to significantly contribute to better loan portfolio quality (mean = 4.9643, Std. Deviation = .18726), and the credit risk assessment practices align well with industry best practices (mean = 4.9107, Std. Deviation = .43804). This high level of agreement suggests a positive perception among respondents regarding the effectiveness of credit risk assessment practices at I&M Bank in enhancing financial performance.

Therefore, this implies that the respondents hold a collectively positive view regarding the effects of credit risk assessment practices on I&M Bank’s financial performance. The mean scores consistently indicate strong agreement with statements asserting the effectiveness of these practices. The lowest mean score, 4.7679, still reflects a higher level of agreement that the risk rating and credit worthiness systems are effective in assessing borrower credit worthiness. The narrow standard deviations across all items suggest a high level of consensus among respondents. This implies a consistent and positive perception of the impact of credit risk management on various aspects of financial performance, including assets, equity, loan portfolio quality, and alignment with industry best practices. The findings suggest that, according to the respondents, I&M Bank’s credit risk assessment practices play a pivotal role in positively influencing its financial performance and adherence to industry standards.

Table 4.4. Effects of loan recovery strategies on financial performance

| N | Mean | Std. Deviation | ||

| The loan recovery strategies employed at I&M Bank are effective in reducing non-performing loans. | 56 | 4.9464 | .40089 | |

| Loan recovery strategies have contributed to an increase in the bank’s overall profitability. | 56 | 4.8214 | .76532 | |

| Loan recovery strategies have improved the bank’s liquidity position. | 56 | 4.9107 | .54861 | |

| Loan recovery strategies at I&M Bank prioritize finding mutually beneficial solutions with borrowers. | 56 | 4.9464 | .22721 | |

| I&M Bank’s loan recovery strategies are aligned with industry best practices. | 56 | 4.9643 | .18726 | |

| Valid N (listwise) | 56 | |||

Source: Field data (2023)

Table 4.4 shows that, respondents rated the effectiveness of loan recovery strategies at I&M Bank on financial performance. The data reveal a higher level of agreement among respondents regarding the positive effect of these strategies. Specifically, respondents strongly agree (mean = 4.9464, Std. Deviation = .40089) that the loan recovery strategies employed at I&M Bank are effective in reducing non-performing loans. Additionally, participants express strong agreement that these strategies have increased the banks’ overall profitability (mean = 4.8214, Std. Deviation = .76532) and have improved the bank’s liquidity position (mean = 4.9107, Std. Deviation = .54861). Respondents also strongly agree that I&M Bank’s loan recovery strategies maximize mutually beneficial solutions with borrowers (mean = 4.9464, Std. Deviation = .22721), and that these strategies align well with industry best practices (mean = 4.9643, Std. Deviation = .18726). The consistently high mean scores across these dimensions suggest a shared positive perception among respondents regarding the effectiveness of I&M Bank’s loan recovery strategies in enhancing financial performance.

Moreover, respondents uniformly hold a positive view regarding the effects of loan recovery strategies on I&M Bank’s financial performance. The mean scores consistently reflect strong agreement with statements asserting the effectiveness of these strategies in reducing non-performing loans, increasing overall profitability, and improving liquidity. The standard deviations, while slightly higher than in the previous analysis, still indicate a relatively low level of variability in responses, indicating a consensus among participants. This collective positive perception suggests that I&M Bank’s loan recovery strategies are perceived as effective in addressing financial challenges and aligning with industry best practices. The findings imply that, according to respondents, these strategies play a significant role in enhancing the bank’s financial performance through effective reduction of non-performing loans, increased profitability, and improved liquidity.

Table 4.5. Effects of loan monitoring procedures on financial performance

| N | Mean | Std. Deviation | |

| Loan quality trends are closely monitored, and deviations from expected trends are promptly addressed. | 56 | 4.7500 | .85812 |

| The delinquency rate within our loan portfolio has decreased due to proactive loan monitoring. | 56 | 4.9107 | .34519 |

| The return on equity (ROE) of I&M Bank has been positively influenced by the effectiveness of loan monitoring. | 56 | 4.8929 | .36574 |

| I&M Bank’s return on assets (ROA) has improved due to the implementation of robust loan monitoring procedures. | 56 | 4.9643 | .18726 |

| The loan monitoring process at I&M Bank is systematic and well-documented. | 56 | 4.8571 | .67227 |

| Valid N (listwise) | 56 |

Source: Field data (2023)

Table 4.5 shows that, participants were asked to rate the impact of loan monitoring procedures on I&M Bank’s financial performance. The data illustrates a consistently positive perception among respondents. Specifically, respondents strongly agree (mean = 4.7500, Std. Deviation = .85812) that loan quality trends are closely monitored, with deviations promptly addressed, indicating a proactive approach to managing loan quality. Furthermore, participants strongly agree that the delinquency rate within the loan portfolio has decreased due to proactive loan monitoring (mean = 4.9107, Std. Deviation = .34519). Respondents also strongly agree that the return on equity (ROE) of I&M Bank has been positively influenced by the effectiveness of loan monitoring (mean = 4.8929, Std. Deviation = .36574), and that the bank’s return on assets (ROA) has improved due to the implementation of robust loan monitoring procedures (mean = 4.9643, Std. Deviation = .18726). Additionally, participants express strong agreement that the loan monitoring process at I&M Bank is systematic and well-documented (mean = 4.8571, Std. Deviation = .67227). These consistently high mean scores suggest a shared positive perspective among respondents regarding the effectiveness of loan monitoring procedures at I&M Bank in positively influencing financial performance.

Therefore, this implies that respondents uniformly hold a positive view regarding the effect of loan monitoring procedures on I&M Bank’s financial performance. The mean scores consistently indicate strong agreement with statements asserting the effectiveness of these procedures in closely monitoring loan quality trends, reducing delinquency rates, and positively influencing key financial metrics such as return on equity (ROE) and return on assets (ROA). The standard deviations, while slightly higher than in previous analyses, still indicate a relatively low level of variability in responses, implying a consensus among respondents. This collective positive perception suggests that, I&M Bank’s systematic and well-documented loan monitoring procedures are perceived as effective in maintaining loan quality, reducing delinquency, and contributing to improved financial metrics. The findings imply that, according to respondents, these procedures play a significant role in positively influencing the bank’s financial performance.

Table 4.6. Financial performance in I&M Bank

| N | Mean | Std. Deviation | |

| I&M Bank has demonstrated strong financial performance in recent years. | 56 | 4.8036 | .79589 |

| Loans are managed efficiently to mitigate risks to the bank’s financial performance. | 56 | 4.9107 | .54861 |

| I&M Bank consistently maintains sufficient liquidity to meet its obligations and lending requirements. | 56 | 4.9286 | .32233 |

| The bank has effectively managed its resources to achieve its financial goals. | 56 | 4.8929 | .36574 |

| The bank actively monitors and addresses non-performing loans to maintain a healthy loan portfolio. | 56 | 4.8929 | .45442 |

| Valid N (listwise) | 56 |

Source: Field data (2023)

Table 4.6 demonstrates respondents’ assessments of I&M Bank’s financial performance, offering valuable observations into their perceptions. The data reveals a consistently positive viewpoint among participants regarding the bank’s financial standing. The mean scores consistently indicate strong agreement with statements asserting that, I&M Bank has demonstrated strong financial performance in recent years (mean = 4.8036, Std. Deviation = .79589). Respondents also express strong agreement that, loans are managed efficiently to mitigate risks to the bank’s financial performance (mean = 4.9107, Std. Deviation = .54861) and that the bank consistently maintains sufficient liquidity to meet its obligations and lending requirements (mean = 4.9286, Std. Deviation = .32233). Furthermore, respondents strongly agree that the bank has effectively managed its resources to achieve its financial goals (mean = 4.8929, Std. Deviation = .36574), and actively monitors and addresses non-performing loans to maintain a healthy loan portfolio (mean = 4.8929, Std. Deviation = .45442). These high mean scores collectively suggest a shared positive perception among respondents regarding I&M Bank’s strong financial performance and effective management practices.

Furthermore, it is evident that, the respondents uniformly hold a positive view regarding I&M Bank’s financial performance. The mean scores consistently reflect strong agreement with statements asserting the bank’s strong financial performance, efficient loan management, sufficient liquidity maintenance, effective resource management, and proactive measures in addressing non-performing loans. The standard deviations, while indicating slightly higher variability compared to previous analyses, still suggest a relatively low level of variability in responses, indicating a consensus among participants. This collective positive perception implies that, I&M Bank is perceived by respondents as having a strong financial position, efficient risk management practices, and effective resource utilization, aligning with the broader goals of the bank. The findings suggest that, according to respondents, I&M Bank’s financial performance is viewed positively across various key aspects.

Table 4.7. Return on asset in I&M Bank (figures in RWF ’000)

| Years

Options |

2018 | 2019 | 2020 | 2021 | 2022 | |

| Net income | 10, 226, 290 | 11, 865, 985 | 8, 086, 172 | 29, 620, 409 | 33, 589, 881 | |

| Total asset | 294, 165, 633 | 317, 899, 026 | 466, 926, 163 | 498, 221,433 | 516,095,461 | |

| ROA | 3.4% | 3.7% | 1.7% | 5.9% | 6.5% | |

Source: I&M Bank, November, 2023

Table 4.7. presents the Return on Assets (ROA) figures for I&M Bank for the past five years. It demonstrates a mixed, but; generally positive trend. The bank’s ROA increased from 3.4% in 2018 to 3.7% in 2019, but experienced a decline to 1.7% in 2020. However, the subsequent years saw a significant recovery, with ROA reaching 5.9% in 2021 and further improving to 6.5% in 2022. These figures indicate that, the bank has managed to efficiently utilize its assets to generate profits, especially surpassing the generally considered good threshold of 5% in 2022. The dip in 2020 might be attributed to external factors like COVID-19, but the subsequent years’ positive performance suggests effective management and a strong financial position. Overall, the trend in ROA reflects I&M Bank’s resilience and ability to adapt, ultimately achieving excellent financial performance by efficiently converting its assets into earnings.

Table 4.8. Return on equity in I&M Bank (figures in FRW ’000)

| Years

Options |

2018 | 2019 | 2020 | 2021 | 2022 | |

| Net income | 10,226,290 | 11,865,985 | 8,086,172 | 29,620,409 | 33,589,881 | |

| Total Equity | 72,567,498 | 82,786,882 | 62,203,967 | 181,321,733 | 193,475,404 | |

| ROE | 14% | 14.3% | 12,9% | 16.3% | 17.3% | |

Source: I&M Bank, November, 2023

Table 4.8. displays that the Return on Equity (ROE) figures for I&M Bank reveal a generally positive trend for the past five years. The bank’s ROE increased from 14% in 2018 to 14.3% in 2019, reflecting a steady performance. Although there was a slight dip into 12.9% in 2020, subsequent years witnessed a notable recovery. In 2021, the ROE increased to 16.3%, and in 2022, it further improved to 17.3%. These figures indicate that the bank efficiently utilized its equity to generate returns for shareholders. Importantly, the ROE for both 2021 and 2022 falls within the generally considered good range of 15% to 20%. This suggests that, I&M Bank has not only maintained a sound financial position, but; has also demonstrated the ability to provide favourable returns to its shareholders. The positive trajectory in ROE aligns with the objectives of the academic research study, affirming the bank’s effective financial management and its contribution

In order to ascertain whether or not credit risk assessment practices, loan recovery strategies, and loan monitoring procedures in I&M Bank are correlated with independent variables and financial performance, as well as dependent variables, statistical tests were conducted as follows.

Table 4.9. Correlation analysis

| Credit risk management practices | Loan recovery strategies | Loan monitoring procedures | Financial performance | ||

| Credit risk assessment practices | Pearson Correlation | 1 | .726 | .586 | .753 |

| Sig. (2-tailed) | .023 | .003 | .004 | ||

| Loan recovery strategies | Pearson Correlation | .726 | 1 | .624 | .643 |

| Sig. (2-tailed) | .023 | .015 | .023 | ||

| Loan monitoring procedures | Pearson Correlation | .586 | .624 | 1 | .523 |

| Sig. (2-tailed) | .003 | . 015 | .031 | ||

| Financial performance | Pearson Correlation | .753 | .643 | .523 | 1 |

| Sig. (2-tailed) | .004 | .023 | .031 | ||

| N | 56 | 56 | 56 | 56 | |

Source: Field data (2023)

Table 4.9.demonstrates that, the objective of the correlation analysis is to investigate the associations between the financial performance of I&M Bank (considered the dependent variable) and the practices used for credit risk assessment, loan recovery strategies, and loan monitoring procedures (all treated as independent variables). As of right now, Table 4.9 Pearson correlation coefficients show a moderately positive linear relationship between I&M Bank’s financial performance, and its practices for credit risk assessment, loan recovery, and loan monitoring. Therefore, a striking look at table 4.10 demonstrates a perfect Pearson Moment Correlation visually expressed diagonally across the table by number 1, which indicates that, Credit risk management practices, credit risk assessment, loan recovery strategies, loan monitoring procedures all simultaneously, positively and heavily weigh on financial performance of I&M Bank.

In other words, all those treatment variables, that are the predictors, concur with financial performance of I&M Bank which is the measure of the treatment variables. Indeed, the correlations which vary from 0.523 to 0.753, indicate a stronger relationship than the one found in earlier studies. Thus, there is confidence in the dependability of the observed relationships because, the p-values for these correlations are less than 0.05, which indicates statistical significance. According to this updated analysis, there is a moderately positive correlation between changes in financial performance and variations in credit risk assessment practices, loan recovery strategies, and loan monitoring procedures. Indeed, these higher correlation coefficients indicate a stronger relationship between these variables and indicate that improvements or changes to these practices will likely have positive effect on I&M Bank’s financial performance. This correlation does not, however, prove that loan recovery tactics, credit risk management techniques, or loan monitoring protocols will always improve I&M Bank’s financial performance. Other unanticipated factors could theoretically come into play and obstruct this balance between loan management and financial performance. In other words, a correlation is not and never will be a cause. Said another way, there may be other uncontrollable factors that muddy the relationship between good loan management and improved bank financial performance. It is merely an estimation.

Regression analysis

In order to determine whether there is sufficient evidence to accept or reject the null hypothesis, regression analysis was required for statistical tests.

Table 4.10. Summary model

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

| 1 | .620a | .384 | .141 | .36690 |

| a. Predictors: (Constant), loan monitoring procedures, loan recovery strategies., Credit risk management practices. | ||||

Source: Field data (2023)

The predictors of the variation in financial performance (the dependent variable) are credit risk assessment practices, loan recovery strategies, and loan monitoring procedures. Using the given predictors as a basis, the multiple regression analysis aims to forecast I&M Bank’s financial performance. According to the R Square of 0.384, the combination of loan recovery strategies, credit risk assessment techniques, and loan monitoring procedures accounts for approximately 38.4% of the variability in financial performance. The average variability between the expected and actual financial performance values is shown by the estimate’s standard error, which stands at 0.36690. The overall R of 0.620, which indicates a moderately positive linear relationship, suggests that the combination of loan recovery strategies, credit risk assessment practices, and loan monitoring procedures has a moderate impact on financial performance values of I&M Bank. However, considering the negative Adjusted R Square, which might indicate potential limits in the model’s capacity to capture the complexities of financial performance, care should be taken when interpreting the predictive power of the model. This can be observed through the Analysis of Variance, ANOVA.

Table 4.11. Analysis of Variance (ANOVA)

| Model | Sum of Squares | Df | Mean Square | F | Sig. | |

| 1 | Regression | 22.356 | 3 | 7.452 | 2.320 | .047b |

| Residual | 167.024 | 52 | 3.212 | |||

| Total | 189.38 | 55 | ||||

| a. Dependent Variable: Financial performance. | ||||||

| b. Predictors: (Constant), loan monitoring procedures., loan recovery strategies, credit risk management practices. | ||||||

Source: Field data (2023)

The model evaluates the statistical significance of the predictors (loan recovery strategies, credit risk assessment practices, and loan monitoring procedures) in explaining the variability in financial performance using the Analysis of Variance (ANOVA) shown in Table 4.11. A significant F-statistic of 2.320 and a corresponding p-value of 0.047 are reported in the Regression section. This means that, the predictors as a whole account for a sizable portion of the variance in financial performance. The regression model’s sum of squares, which stands at 22.356, represents the percentage of the overall variability in financial performance that can be attributed to the predictors. The unexplained variability is displayed in the Residual section, where the sum of squares is 167.024. The combination of predictors appears to have a statistically significant effect on financial performance. Overall, the ANOVA results point to a statistically significant impact of the predictor combination on financial performance, highlighting the significance of loan recovery strategies, credit risk assessment practices, and loan monitoring procedures in shaping I&M Bank’s financial performance.

Table 4.12. Regression model

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | 23.900 | 2.361 | 10.123 | .000 | |

| Credit risk assessment practices. | .640 | .266 | .205 | 2.406 | .006 | |

| Loan recovery strategies | .610 | .265 | .051 | 2.302 | .007 | |

| Loan monitoring procedures. | .649 | .251 | .054 | 2.586 | .004 | |

| a. Dependent Variable: Financial performance | ||||||

Source: Field data (2023)

The unstandardized coefficients in the Regression Model shown in Table 4.12 provide insight into how predictors affect financial performance. When all predictors are zero, the expected financial performance is represented by the constant term (23.900). Higher values in these predictors are linked to better financial performance, according to the positive unstandardized coefficients for credit risk assessment practices (0.640), loan recovery strategies (0.610), and loan monitoring procedures (0.649). The strength of the relationship is confirmed and reinforced by the statistically significant (p < 0.01) t-values for all the predictors. The standardized coefficients, or beta, provide insights into how important each predictor is in relation to the others.

The practices of credit risk assessment have the highest standardized coefficient (0.205), which is followed by loan recovery strategies (0.051) and loan monitoring procedures (0.054). These results imply that, in comparison to the other predictors, credit risk assessment procedures have a comparatively greater impact on financial performance in this model. Consequently, since the financial performance is Y, it equals β0, the model’s coefficient of the intercept (constant), which is equal to 23.900; β1, β2, and β3 are the coefficients of estimates for X1, which represents credit risk assessment practices; X2, which represents loan recovery strategies; and X3, which represents loan monitoring procedures. The change in the dependent variable for a one-unit change in each respective predictor is indicated by these coefficients (0.640, 0.610, 0.649).

As a result, the regression model analysis offers confirmation against the first null hypothesis (H01), which holds that, credit risk assessment procedures have no impact on I&M Bank’s financial performance. The quality of credit risk assessment and financial performance appear to be significantly correlated, according to the statistically significant positive coefficient (0.640) associated with credit risk assessment practices.

Given that the p-value (Sig. = 0.006) is below the conventional significance level of 0.05, the alternative is accepted and the null hypothesis is rejected. This suggests that I&M Bank’s financial performance is significantly impacted by its credit risk assessment procedures. The idea that a more successful assessment of borrower credit worthiness positively influences the bank’s overall financial outcomes is supported by the positive coefficient, which further suggests that, improvements in credit risk assessment procedures are linked to an increase in financial performance.

Moreover, the data runs counter to the second null hypothesis (H02), which holds that loan recovery strategies have no impact on I&M Bank’s financial performance. The statistically significant positive coefficient (0.610) linked to loan recovery strategies indicates a noteworthy correlation between the efficacy of these strategies and the achievement of financial objectives. Since the p-value (Sig. = 0.007) is below the conventional significance level of 0.05, the alternative hypothesis is accepted and the null hypothesis is rejected. This confirms that loan recovery strategies do, indeed, significantly improve I&M Bank’s financial performance. The idea that a more successful approach to recovering loans positively influences the bank’s overall financial outcomes is supported by this positive coefficient, which indicates that improvements in loan recovery strategies are associated with an increase in financial performance.

As a result, the regression model analysis offers evidence against the third null hypothesis (H03), which holds that, loan monitoring practices have no impact on I&M Bank’s financial performance. There appears to be a significant correlation between systematic loan monitoring and financial performance, as indicated by the statistically significant positive coefficient (0.649) linked to loan monitoring procedures. Since the p-value (Sig. = 0.004) is below the conventional significance level of 0.05, the alternative hypothesis is accepted instead of the null hypothesis. This suggests that, loan monitoring practices do affect I&M Bank’s financial performance in a noticeable way. The idea that a more systematic and well-documented approach to loan monitoring positively influences the bank’s overall financial outcomes is supported by the positive coefficient, which suggests that improvements in loan monitoring procedures are associated with an increase in financial performance.

Table 4.13. Correlation analysis

| Credit risk management practices | Loan recovery strategies | Loan monitoring procedures | Financial performance | |||

| Credit risk assessment practices | Pearson Correlation | 1 | .726 | .586 | .753 | |

| Sig. (2-tailed) | .023 | .003 | .004 | |||

| Loan recovery strategies | Pearson Correlation | .726 | 1 | .624 | .643 | |

| Sig. (2-tailed) | .023 | .015 | .023 | |||

| Loan monitoring procedures | Pearson Correlation | .586 | .624 | 1 | .523 | |

| Sig. (2-tailed) | .003 | . 015 | .031 | |||

| Financial performance | Pearson Correlation | .753 | .643 | .523 | 1 | |

| Sig. (2-tailed) | .004 | .023 | .031 | |||

| N | 56 | 56 | 56 | 56 | ||

Table 4.13 demonstrates that, the objective of the correlation analysis is to investigate the associations between the financial performance of I&M Bank (considered the dependent variable) and the practices used for credit risk assessment, loan recovery strategies, and loan monitoring procedures (all treated as independent variables). As of right now, Table 4.9 Pearson correlation coefficients show a moderately positive linear relationship between I&M Bank’s financial performance, and its practices for credit risk assessment, loan recovery, and loan monitoring. Therefore, a striking look at table 4.10 demonstrates a perfect Pearson Moment Correlation visually expressed diagonally across the table by number 1, which indicates that, Credit risk management practices, credit risk assessment, loan recovery strategies, loan monitoring procedures all simultaneously, positively and heavily weigh on financial performance of I&M Bank. In other words, all those treatment variables, that are the predictors, concur with financial performance of I&M Bank which is the measure of the treatment variables. Indeed, the correlations which vary from 0.523 to 0.753, indicate a stronger relationship than the one found in earlier studies. Thus, there is confidence in the dependability of the observed relationships because, the p-values for these correlations are less than 0.05, which indicates statistical significance. According to this updated analysis, there is a moderately positive correlation between changes in financial performance and variations in credit risk assessment practices, loan recovery strategies, and loan monitoring procedures. Indeed, these higher correlation coefficients indicate a stronger relationship between these variables and indicate that improvements or changes to these practices will likely have positive effect on I&M Bank’s financial performance. This correlation does not, however, prove that loan recovery tactics, credit risk management techniques, or loan monitoring protocols will always improve I&M Bank’s financial performance. Other unanticipated factors could theoretically come into play and obstruct this balance between loan management and financial performance. In other words, a correlation is not and never will be a cause. Said another way, there may be other uncontrollable factors that muddy the relationship between good loan management and improved bank financial performance. It is merely an estimation.

Through the determination of the effects of credit risk assessment practices, loan recovery strategies, and loan monitoring procedures on the financial performance of I&M Bank, Rwanda from 2018 up to 2022—discussed below—the effects of loan management on the financial performance of banking institutions in Rwanda, with a case study of I&M Bank, were examined throughout this research work.

The results of this study’s Table 4.4, which includes a case study of I&M Bank, demonstrate that respondents strongly agreed that credit risk assessment procedures are effective. There is broad consensus among participants regarding the contribution of risk rating and credit scoring systems to enhanced financial performance, including favorable effects on equity and loan portfolio quality, as well as alignment with industry best practices. This supports the findings of Gisemba Peter Nyamwange’s (2010) research on SACCOs, which found a beneficial correlation between financial performance and credit risk management techniques. This is further supported by Grace N. Mwangi’s (2012) research on commercial banks, which emphasizes the significance of credit risk grading systems. Similar results are found in Poudel’s (2015) study on credit risk assessment parameters, which highlights the negative effect on financial performance. Together, these studies highlight how crucial efficient credit risk assessment is to improving the financial performance of various financial institutions and highlight the necessity of strong risk-reduction and profitability-boosting strategies.

Moreover, as shown in the table 4.5, respondents to this study generally felt that, loan recovery strategies were a good way to improve financial performance. The majority of respondents firmly believe that, these tactics are effective in lowering the percentage of non-performing loans, boosting total profitability, enhancing liquidity, giving priority to win-win solutions with borrowers, and being in line with industry best practices. This is consistent with Elisabeth Yost’s (2021) analysis of the restaurant business, which identified cost recovery techniques, investing in personnel, and emphasizing carry-out as critical financial recovery strategies.

As per Jonathan Morduch’s (2016) analysis of microfinance organizations, serving the poor is also not correlated with profitability. Instead, this author highlights the significance of comprehending profitability patterns, loan recovery, and cost reduction. The significance of efficient loan recovery in preserving financial performance is further supported by Njeru Duncan’s (2015) research on deposit-taking SACCOs in the Mount Kenya Region. When taken as a whole, these studies focus on the importance of effectively implemented loan recovery strategies in promoting financial stability across a range of industries, emphasizing the necessity of flexible approaches to meet unique challenges and contexts.

Furthermore, as table 4.6, shows it, results of this study regarding the loan monitoring practices of I&M Bank indicate that, participants generally have a favorable opinion of the procedures’ ability to improve financial performance. It is obvious from the respondents’ strong agreement that a proactive approach is taken in closely monitoring loan quality trends and promptly addressing any deviations. Strong agreement is also found in the study to suggest that, proactive loan monitoring is responsible for the decline in the delinquency rate within the loan portfolio, and that effective loan monitoring practices have improved return on assets (ROA) and return on equity (ROE). There is broad consensus among participants regarding the systematic and well-documented nature of the monitoring process.

These results are consistent with Arellano’s (2005) analysis of loan monitoring procedures around the world, which highlighted the link between effective loan monitoring and improved financial performance. Prudent monitoring techniques, such as routine portfolio reviews and precise loan loss provision estimation, were advised by the study. These results are corroborated by Akhtar’s (2020) study, which highlights the beneficial effects of efficient loan monitoring on credit availability and financial performance. It emphasizes the value of fostering trust and offering borrowers continuous support through improved monitoring procedures, a viewpoint that is in line with the optimistic opinions shared by study participants from I&M Bank.

As a result, Table 4.7 shows that respondents’ favorable opinions of I&M Bank’s financial performance are consistent with the conclusions drawn by Grace N. Mwangi (2012) and Poudel (2015), who highlighted the importance of sound credit risk management and financial management techniques in guaranteeing stable financial performance in the banking industry. The respondents appear to have a positive outlook regarding the bank’s strong financial performance and management practices, as evidenced by the consistently high mean scores across multiple dimensions. The upward trend in Return on Equity (ROE) and Return on Assets (ROA) over time (Tables 4.8 and 4.9) is indicative of I&M Bank’s tenacity, effective use of its assets, and capacity to give shareholders positive returns. These results support the findings of Jonathan Morduch (2016), who highlights the significance of profitability in microfinance organizations.

Thus, the idea that enhancements to these practices may have an effect on I&M Bank’s financial performance is supported by the correlation analysis in Table 4.10, which shows a moderately positive linear relationship between credit risk assessment practices, loan recovery strategies, loan monitoring procedures, and financial performance. This is in line with the findings of Arellano’s (2005) study, which showed that stronger loan monitoring procedures were positively correlated with improved bank financial performance. The Summary Model (Table 4.11)’s multiple regression analysis delves deeper into the overall impact that loan recovery strategies, credit risk assessment methods, and loan monitoring protocols have on financial performance. The importance of these predictors in explaining the variability in financial performance is further supported by the statistically significant F-statistic in the Analysis of Variance (ANOVA) (Table 4.12).