Financial Inclusion and Community Empowerment for Inclusive Growth and Sustainable Development in Turkana County, Kenya, East Africa.

- Logiel Lokwawi Samson

- Professor John Ndefru

- 2126-2140

- Apr 17, 2024

- Accounting & Finance

Financial Inclusion and Community Empowerment for Inclusive Growth and Sustainable Development in Turkana County, Kenya, East Africa.

1Logiel Lokwawi Samson and 2Professor John Ndefru, (FDA, FPPA, FCAI)

1PhD student (PAUGHSS) University of Yaoundé 11

2Professor of Public Administration and Public Policy Analysis, University of Buea

DOI: https://dx.doi.org/10.47772/IJRISS.2024.803149

Received: 31 January 2024; Accepted: 02 February 2024; Published: 17 April 2024

ABSTRACT

The academic community has shown a great deal of interest in the relationship between financial inclusion and community empowerment. However, despite efforts to promote financial inclusion in line with SDG goals, not much is known about its accessibility, usability, or affordability, particularly among vulnerable population in marginalized counties in Kenya. The study aimed at evaluating the effects of financial inclusion on community empowerment for inclusive growth and sustainable development, with particular focus on employment, education, access to financial services, products, and poverty alleviation, in Turkana County, Kenya. Phyllis A. Mason and Donald C. Ham brick introduced the community echelon theory of financial inclusion in 1984, which served as the basis for this investigation. According to the theory, the community leaders should serve as a conduit for the excluded members of the community to obtain financial services and capital. In addition, the study’s informants included civil servants, policy specialists, employers from private sectors, community members, livestock and business merchants, and community leaders. The study’s respondents and key informants were selected using the judgmental sampling approach, and snowballing respectively. Moreso, the researcher collected both qualitative and quantitative data using interviews and structured questionnaires with closed-ended questions which were analyzed through content thematic analysis and inferential statistics respectively. Based on the research findings, financial institutions enhanced access to education, employment, financial products and services in Turkana County with support from the local county government and development partners with an aim of alleviating vulnerable population from extreme poverty. However, poverty, peer pressure, poor infrastructures, cultural norms, values, and insecurity were identified as the challenges affecting financial inclusion in Turkana County. Moreover, the regression analysis results showed a significant value of r = 0.845; p < 0.05 revealing existence of a strong and positive correlation between the variables. The study recommended the establishment of the special unit in the department of economic planning in the county government to coordinate implementation of all financial inclusion activities in Turkana County to reduce duplications. Furthermore, the concepts, values and principles of the financial inclusion should be incorporated into the legal and policy frameworks and monitored to determine its effectiveness.

Keywords: Financial inclusion; community empowerment: inclusive growth: Sustainable development

INTRODUCTION

According to Lenka and Barik, (2018), financial inclusion is defined as having access to the financial resources needed to promote macro and micro-economic growth that is sustainable. Financial inclusion has become more popular on both sides of the aisle and is a priority for both developed and developing nations (Dymski, 2005). In order to spur economic progress, the majority of industrialized nations have facilitated citizen access to financial services; nevertheless, in less developed nations, the financial sector has failed to achieve universal financial inclusion for all citizens (Lenka & Barik, 2018).

In 2011, 1.2 billion people worldwide had access to financial services, while 1.7 billion people were unable to do so; the majority of these people were either unemployed or lived in poverty. The World Bank views financial inclusion as a catalyst for economic growth (World Bank, 2018). According to 2014 Nobel laureate Amartya Sen, poverty is defined as both a deprivation of basic requirements and an inability to receive money. As per the 2009 study by the consultative group, it was demonstrated that about 1.4 million people living in Madagascar’s rural areas, or 70% of the country’s total population, lack access to financial services, which hinders their ability to receive government services.

Many microfinance satellites, including Self-Help Groups (SHGs), Village Saving and Loan Associations (VSLAs), and Savings and Credit Cooperatives (SACCOs), were established in rural Mexico to increase community members’ access to financial services and products, as in the case of ACLEDA Banambodia. However, due to internal and external market forces, these satellites had to cease operations in these areas. This information was reported by Nagarajan, G., and Meyer, R. in 2006.

In the Middle west, the international labor organization has developed financial training resources for quite a number of countries e.g., Mongolia, Indonesia, Moldova, and Cambodia to educate the community Members in order to make informed financial decisions at household or business level (ILO,2011). To help 13,000 target beneficiaries who make less than $1 per day, more than 200 local trainers in Cambodia have received financial literacy training. Their training covers topics including saving, lending, and diversifying company features to increase profitability and financial prospects. The ILO’s 2008 adoption of the Microinsurance Innovation Facility (MIF) enhanced government efforts to close the financial literacy gaps by protecting the majority of low-income individuals who reside in developing countries’ rural areas from shocks and stresses related to poverty by making insurance coverage more accessible (ILO, 2008). In addition to providing financial support in the form of grants to local and international organizations, the MIF offers additional assistance to households that are vulnerable by enabling them to design creative financial sector tools and systems that tailor their services to the specific needs of the community (ILO, 2004).

Access to the financial services and products are estimated to be game changers to Africa which is the poorest continent in the world in terms of the creation of the employment, investment, increment and income improvement from generations to generations leading to reduction of poverty (Musau et al., 2018). This is because it is estimated that 80% of the population in the sub-Sahara representing approximately 325 million are less accessible to the banking services and it is essential to remove these barriers inhibiting them from accessing the financial services which has detrimental effect to the national economy outcome (Achugamonu et al. 2020).

According to Nkoa and Song (2020), all signs point to the African government’s incapacity to create and carry out well-informed policies and the actions necessary to advance inclusion in the financial industry. Additionally, Nkoa and Song hinted that the lack of access to financial information within the community is a result of weak and fragile institutions that exist in Africa, exacerbating the situation and widening the social class divide that results from it. Chu et al. (2019) alludes that unless the government strengthen the institutional and legal framework to enhance inclusion of the households in Africa into the financial sector, it will still struggle to reduce the poverty rate among the citizens.

Financial inclusion in South Africa has given communities, particularly those headed by women, the ability to overcome cultural norms and values, which has increased their bargaining power and allowed them to make informed financial decisions about the ownership of assets, the purchase power of goods like food, the education of their children, and reproductive health. It has also enabled them to enter the labor force. (Van Biljon et al. (2018).

According to Wokabi and Fatoki (2019), income level and place of residence—such as rural areas—are important factors that determine financial inclusion and have a substantial impact on an individual’s involvement in the financial sector in East African nations like Tanzania, Burundi, Rwanda, and Uganda. Wokabi and Fatoki also hinted that the creation of savings banks, which function as post offices, has greatly increased community members’ access to financial services and goods in the nation’s rural areas; examples of these include South Africa, Kenya, and Tanzania, which have helped people get money through loans and education while also protecting them from the shocks and strains brought on by climate change. These countries are becoming important suppliers of deposit services in rural regions.

In Kenya, especially for households headed by women, the introduction of mobile money by companies like Safaricom, Airtel, Orange, and others has lifted the majority of households out of extreme poverty, claim Suri and Jack (2016). Interest has been shown in the marginalized counties, and while I applaud the efforts of the county government and developmental partners to guarantee that community members have access to financial services and products. There is a knowledge gap that has not been filled in any significant way, particularly with regard to the effect of financial inclusion on community empowerment for inclusive growth and sustainable development in Turkana County, Kenya.

CONCEPTUAL REVIEW

Studies conducted by Brune et al. (2015) and Kenyan counterparts Dupas and Robinson (2013) on the online accounts provides avenue for households to access the funds through the account outside the household set ups and this enhances control of the power of the head of the household unit over the management and use of the account. Moreso using the online or liquid account which are accessible over the mobile devices or the ATM cards, increases the account accessibility and withdrawal charges or fees. Studies have shown that it increases the control power to the owner than the individual whose account is not linked to services (Schaner, 2016). The study by Nandru et al., (2016) supports the Brunes et al 2015 findings as it states that financial inclusion provides a wide range of services such as opening account, insurance services and access to credit and remittances at a cost that is affordable to meet the financial needs of the disadvantaged communities’ members in the society.

Hanning and Jansen (2010) mentioned that, financial inclusion allows the population excluded to access the formal financial systems for them to access the financial products and services which they might have not wished to access from other services. Furthermore, it also brings together both banked and unbanked members of the communities making the services available to them with an aim of ensuring each and everyone benefits from the allocation of productive services or resources with a view to bridge the socio-economic inequality gap (Yorulmaz, 2013). Moreso Yorulmaz mentioned that there are other benefits for the financial systems at micro and macro levels and this includes at micro-level; the households’ units can plan for use of the income in organized way the sometime having access to the credit while at macro-level the financial institutions can provide access to other services such as education policies for the school going to have a better future. Finally, Blando, 2013 argues that financial inclusion encourages the entrepreneurs in the community to access credits to start new businesses which will boost the countries’ economic output.

The results of a research by Kondo (2007), which was centered on the Philippines, showed that microfinance lending significantly and favorably affects the creation of jobs. This implies that a home that obtained microfinance loans to launch a company would employ almost 17% of the community’s total population. In order to support the operationalization of the bank in Uganda, which had stagnated in terms of expansion leading to the introduction of new branches and the provision of the financial product making it accessible to everyone, Clarke et al. (2007) support the findings by arguing that the Uganda Commercial Bank made the right decision in privatizing the Stanbic bank to the South Africa associate bank.

Research by Tchamyou et al., (2019), Tchamyou, (2019), Tchamyou, (2020), and Asongu, (2015) confirms that access to financial services and products is linked to a decrease in income equality. This has implications for development outcomes like education, as a lack of funds at home can severely limit a child’s opportunities to enroll in and progress to higher education, which will open doors for social mobility and employment (Asongu et al, 2018a). Asongu et al., (2018a) contend that the development of new technologies and financial opportunities can increase access and coverage, thereby promoting integration of the excluded members of society into the financial circus and ensuring that education is accessible to everyone at the community level, regardless of financial status. These findings are consistent with those of Lenis Escobar et al. (2020) and Kong and Loubere (2021).

EMPIRICAL REVIEW

El-Bourainy, M., Salah, A., and ElSherif, M. (2020) studied how financial inclusion affected the unemployment rate in emerging nations. The study used a multifaceted methodology, including principal component analysis, to create an index of financial inclusion for forty-three (43) emerging African nations, with an emphasis on the three characteristics of financial service accessibility, quality, and usage. Furthermore, they used a dynamic two-step approach called the Generalized Method of Moments (GMM) to examine a sample of empirical data from 35 developing nations and evaluated the impact of financial inclusion on the unemployment rate from 2009 to 2018. According to their findings, financial inclusion reduced unemployment rates among citizens in developing nations. These findings aligned with empirical research that shows that greater financial inclusion in terms of financial services and products lowers unemployment rates and promotes economic empowerment of individuals and communities. In addition, the writers hinted that the unemployment rate in emerging nations is adversely impacted by the pace of inflation, economic expansion, and educational attainment.

A study by Deminrgue, Klapper, Singer, Ansar, and Hess (2018) support the findings of El-Bourainy et al. 2020 that religion affects financial inclusion. This is because Muslims prefer to give money to their close family for business purposes rather than their counterparts from other religions who prefer to save money in formal banks in Sub-Saharan regions. This hinders government efforts to have all walks of life access government services through financial platforms.

In a similar study, Aracil et al. (2021) used data from 75 developing and developed nations between 2004 and 2017 to examine the impact institutional quality plays in financial inclusion in supporting the battle against poverty. The value of inclusive finance for reducing poverty is accelerated by the quality of the institutions, according to research using the quintile regression analysis approach. The study highlights that emerging nations exhibit a greater degree of this institutional quality’s beneficial impact on poverty reduction than do developed nations.

Financial inclusion has country specific determinants as well as worldwide reasons that influence one’s involvement in the sector, in terms of the financial institutions delivering the financial service. Mose and Thomi (2021) explored the supply side determinants of financial inclusion due to its ability to complement efforts put up by government and financial institutions in making available financial services for use by households and firms. Using the OLS method, the study found that the number of internet usage and economic growth have a significant effect on the patronage of households and firms in the financial sector. Chinoda and Kwenda (2019) investigated the impact of mobile phones, economic growth, bank competition and stability on financial inclusion. With data from 49 countries from 2004 to 2016, the study was analyzed using a five variable panel structural vector autoregressive model. It was revealed that financial inclusion is significantly and positively related to shocks emanating from banking competition, mobile phones, economic growth and bank stability.

In 2007, Matu Mugo M. and Evelyne K. conducted a study on the overall effects of financial inclusion in Kenya, with a specific focus on the eradication of poverty and the creation of jobs. The study reviewed lessons learned from the implementation of financial services in 2007, microfinance banking legislation in 2006, the agency banking model in 2010, and shariah compliant services in 2005 of embracing innovative and inclusive finance throughout Kenya, including some of the key risks. The findings of the study demonstrated that financial inclusion can reduce poverty, create jobs, and advance sustainable economic development.

A study by Ibrahim et al. (2019) evaluated the effect of financial inclusion on poverty reduction using actual data from Sub-Saharan Africa. The static panel approach was utilized to evaluate data from 49 sub-Saharan nations between 1980 and 2018. The research findings indicate that various factors such as ATM accessibility, financial information availability, inflation, saving habits, private sector and microenterprise credit availability, and government spending directly affect the reduction of poverty. Notably, the sample size increased from 11.7 to 96.1 across all countries. The study also demonstrated how financial inclusion, when used as a tool to reduce poverty, can improve the nation’s employment and health index since it gives vulnerable women in households access to financial services and products, such as capital for microbusiness ventures, which improves food security and gives them more negotiating power over decisions about asset ownership and reproduction. In conclusion, the study suggested that the government lower the fiscal policy rate for financial institutions in particular so that low-income individuals in rural regions may afford financial services and goods.

The literature gaps; There are gaps in the literature, which the research aims to fill. The study aims to close this gap by using the Lodwar town in Turkana County as a case study and model for the urban’s areas in marginalized counties in Kenya. Previously, authors have conducted similar studies in developed countries, but there has been little research done in rural areas in undeveloped countries. Second, while this study examines this tenet as a whole within the framework of community empowerment, most previous research has focused on the principles of empowerment, such as economic, capital, education, and gender equality separately. Thirdly, whereas the majority of research remain mute on the target samples, this study offers criteria for choosing the target sample for both the pilot study and the real data collection.

Theoretical framework

In 1984, Phyllis A. Mason and Donald C. Hambrick propounded the community echelon theory of financial inclusion. According to the notion, those who are not included in the community should be able to obtain financial services and goods by going via the communal leaders. Reputable community leaders have the ability to convince other community members to join financial institutions by using their influence. An institution of this kind may easily reach the grassroots, benefiting not just the individual members but the community as a whole, thanks to strong cultural ties between members and communal leaders. The merit of the community echelon theory is that the community governance system led by the communal leaders plays a key role in influencing the decentralization of the financial systems to the community level with a view to having the community members benefit in terms of access to financial capital for business start-up which has positive impact to food security and investment in human capital.

As a drawback of the community echelon idea, the majority of African leaders are dishonest and should not be trusted working with private entities, as they may misuse them for personal gain. Second, the theory makes the assumption that community members are technologically literate and well-versed, but it ignores the fact that the majority of community members are illiterate hence necessitating provision of financial literacy training to improve their understanding of financial services and goods. Thirdly, the financial services providers may exert influence on community leaders to get benefits that are at odds with those of the community, which might damage the legitimacy of the leaders’ services.

RESEARCH METHODOLOGY

Research design, data collection, presentation, analysis, validity and reliability based on the context.

The majority of the people (90%) in Turkana County speaks Turkana, despite the county’s diversified population in terms of culture, values, and customs. People throughout the nation as well as overseas population make up the cosmopolitan Turkana Central Division, which serves as the study’s main focus area. With an emphasis on employment, education, financial capital access, and poverty reduction in particular, mixed research design was used in this respect to assess effect of financial inclusion on community empowerment. Google Form was used to gather data from 60 samples of the target population, and a research assistant helped those in the illiterate category by guiding them through the process. Pie charts and graphs, respectively, were used to display the quantitative data generated during data collection and analyzed using descriptive statistics. The relationship between the dependent and independent variables was also discovered through the use of regression analysis. To further assess validity and reliability, 10% of the sample was chosen at random from the sampling frame and the Crombach alpha α was applied. The Likert scale had five points, with SD representing strongly disagree and D representing disagree, U = Undecided, A = Agree, and SA = strongly agree.

RESULTS AND DISCUSSION

The 10% data collected from the pilot study was analyzed to determine the reliability of the tools and the findings were as follows;

| S/N | Variables assessed | Numbers of items | Alpha Cronbach | Comments |

| 1. | Employment | 6 | 0.725 | Reliable |

| 2. | Education | 6 | 0.756 | Reliable |

| 3. | Financial products and service access | 6 | 0.823 | Reliable |

| 4. | Challenges | 6 | 0.811 | Reliable |

Source: Field Survey ,2024

Regarding reliability, the alpha Cronbach was within the (≥ 0.7 < 0.9] range, in which challenges recorded (0.811), employment (0.725), education (0.756), financial products and services access (0.823), and education (0.756), indicating strong statistical reliability. During the pilot study, it was crucial to conduct reliability tests on 10% study samples to minimize errors resulting from misinterpretations and inconsistencies in the data. This ensures the tools produces consistent results when tested again with a wider population. The data tools were very trustworthy, valid, and acceptable for the study according to Cronbach Alpha results in (Table 1).

Table 2: Descriptive analysis of Employment parameters

| Parameters assessed | Total | Strongly disagree | Disagree | Undecided | Agree | Strongly agree | Mean | Std deviation |

| 1. Financial institutions provide jobs opportunities to community members | 60 | 3

(5%) |

2

(3.3%) |

3

(5%) |

35

(58.3%) |

17

(28.3%) |

4.02 | .965 |

| 2. Getting a job in a financial institution is very difficult | 60 | 20

(33.3%) |

21

(35%) |

13

(21.7%) |

6

(10%) |

0

(0%) |

2.08 | .979 |

| 3. Financial institutions prefer hiring staff from other counties rather than the from the community | 60 | 21

(35%) |

26

(43%) |

5

(8.3%) |

5

(8.3%) |

3

(5%) |

2.05 | 1.111 |

| 4. Financial institutions neither employ nor hire staff | 60 | 21

(35%) |

30

(50%) |

6

(10%) |

1

(1.7%) |

2

(3.3%) |

1.88 | .904 |

| 5. Financial institutions prefer employing graduates sponsored by institutions | 60 | 5

(8.3%) |

14

(23.3%) |

10

(16.7%) |

17

(28.3%) |

14

(23.3%) |

3.35 | 1.300 |

| 6. Financial institutions offer internship jobs opportunities only | 60 | 20

(33.3%) |

20

(33.3%) |

14

(23.3%) |

4

(6.7%) |

2

(3.3%) |

2.13 | 1.065 |

Source: Field Survey, 2024

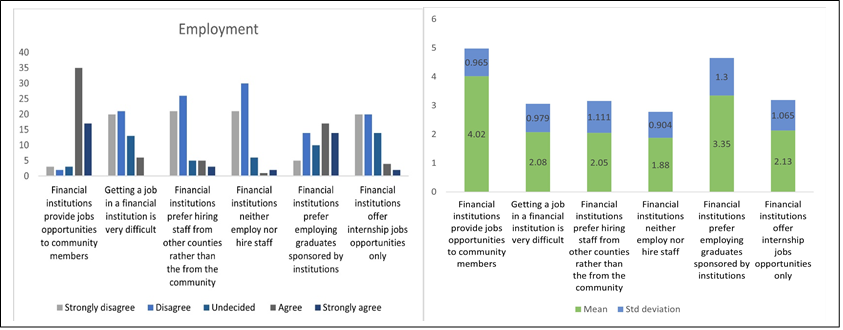

The study analysis (Table 2) established that, the financial institutions provide jobs opportunities to community members (x̄ =4.02, σ=.965), financial institutions prefer employing sponsored graduates (x̄ =3.35, σ= 1.300) and provision of internship opportunities (x̄ =2.13, σ=1.065) were the leading parameters assessed with a mean average of x̄ =3.17 translating to 53% of the target samples. Furthermore, other parameters assessed such as; getting a job in a financial institution is very difficult (x̄ =2.08, σ=.979), financial institution prefer hiring staff from the other counties rather than from the community (x̄ =2.05, σ=1.111), and financial institutions neither employ nor hire staff (x̄ =1.88, σ=.904) recorded the lowest average mean of x̄ =2.00 constituting 47% of the study participants.

The figure 1 below shows employment parameters’ mean and 5-point Likert scale data presentation

Source: Field survey, 2024

It was evidenced that financial institutions in Turkana County have provided jobs opportunities to community members at managerial level and junior levels in compliance with the article 56 of the constitution of Kenya 2010 and employment act 2015 which promotes equal employment and remuneration for the local citizens free from discriminations. Furthermore, as way to bridge unemployment among Turkana County members, the financial institutions give priority to the needy students sponsored by the institution after completing their studies before sending them to compete for job opportunities within and outside the community. Financial institutions internships opportunities provide real life experiences to the employees which enables them to grasp the career trajectory of their future employment.

The target participants attribute a decrease in Turkana County’s unemployment rate to employment opportunities provided by financial institutions to the local citizens, which cast doubt on the idea that these institutions either don’t offer job opportunities to locals or hire staff from other counties. The employment prospects available to the residents of the area include positions as secretaries, office messengers, managers, security personnel, and advisory board members.

Table 3: Descriptive analysis of Education parameters

| Parameters assessed | Total | Strongly disagree | Disagree | Undecided | Agree | Strongly agree | Mean | Std deviation |

| 1.Financial institutions provide grants inform of scholarships to the needy | 60 | 3

(5%) |

6

(10%) |

10

(3.3%) |

33

(55.0%) |

16

(26.7%) |

3.88 | 1.075 |

| 2. Financial institutions have policies to finance the education for needy students. | 60 | 5

(8.3%) |

4

(6.7%) |

5

(8.3%) |

36

(60%) |

10

(16.7%) |

3.70 | 1.094 |

| 3. Financial institutions provide loans to finance education | 60 | 0

(0%) |

0

(0%) |

5

(8.3%) |

29

(48.3%) |

26

(43.3%) |

4.35 | .633 |

| 4. Financial institutions do not offer education support to members and community. | 60 | 1

(1.7%) |

2

(3.3%) |

4

(6.7%) |

28

(46.7%) |

25

(41.7%) |

2.11 | .851 |

| 5. Financial institutions partners with the government to support education for the needy student | 60 | 2

(3.3%) |

1

(1.7%) |

2

(3.3%) |

31

(51.7%) |

24

(40%) |

4.23 | .871 |

| 6. Financial institutions prefer financing the education for members only. | 60 | 19

(31.7%) |

8

(13.3%) |

7

(11.7%) |

13

(21.7%) |

13

(21.7%) |

4.23 | 0.865 |

Source: Field survey, 2024

According to the table 3 below, the following parameters in relation to access to education recording the highest average mean of x̄ =4.078 (90.6% of the study participants) i.e., financial institutions provide loans to finance education (x̄ =4.35, σ=0.633); financial institutions prefer financing the education for members only (x̄ =4.23, σ=0.865); Financial institutions partners with the government to support education for the needy students (x̄ =4.23, σ=0.871); financial institutions provide grants inform of scholarships to the needy (x̄ =3.88, σ=1.075); Financial institution have policies to finance the education for needy students (x̄ =3.70, σ=1.094) while Financial institutions do not offer education support to members and community parameter recorded the lowest mean score of x̄ =2.11 (9.4% of the study participants)

The figure 2 below shows Education parameters’ mean and 5-point Likert scale data presentation

Source: Field Survey, 2024

Based on the study findings in Table 3 and figure 2, the financial institutions are keen in ensuring that members and their beneficiaries are able to access education support in terms of grants, loans and scholarships. According to the qualitative analysis results, it was evidenced that most of the financial institutions have incorporated elements of grants, loans and scholarships provision into their policies and legal frameworks. This initiative was necessitated by limited financial support from the government and other private entities targeting few beneficiaries leaving a large number of poor, vulnerable and bright students from marginalized counties. Furthermore, some of the financial institutions have partnered with the Kenya governments to provide education supports to needy students from vulnerable households across the country fostering collaboration for posterity. The Elimu scholarship, Wings to fly, cooperative bank foundation scholarships, ABSA Elimu scholarships and Aga khan scholarship were among the number of scholarships initiatives identified and offered by the financial institutions in partnership with the government of Kenya. Nevertheless, 9.4% target participants maintained that financial institutions do not offer education support to the community members and their beneficiaries but these assertions lacked basis during the triangulation of data.

Table 4: Descriptive analysis of financial services and products access parameters

| Parameters assessed | Total | Strongly disagree | Disagree | Undecided | Agree | Strongly agree | Mean | Std deviation |

| 1. Loans/salaries/gratitude/pension | 60 | 1

(1.7%) |

0

(0%) |

2

(3.3%) |

39

(65.0%) |

8

(30%) |

4.22 | .666 |

| 2. Trainings | 60 | 1

(1.7%) |

1

(1.7%) |

1

(1.7%) |

49

(81.7%) |

8

(13.3%) |

4.03 | .610 |

| 3. Online banking | 60 | 0

(0%) |

2

(3.3%) |

5

(8.3%) |

37

(61.7%) |

16

(26.7%) |

4.12 | .613 |

| 4. Education policy | 60 | 3

(5%) |

4

(6.7%) |

5

(8.3%) |

37

(61.7%) |

11

(18.3%) |

4.12 | .691 |

| 5. Banks account opening | 60 | 0

(0%) |

1

(1.7%) |

1

(1.7%) |

31

(51.7%) |

27

(45%) |

4.17 | .717 |

| 6. Personal assets security | 60 | 0

(0%) |

2

(3.3%) |

5

(8.3 %) |

34

(56.7%) |

19

(31.7%) |

3.82 | .983 |

Source: Field Survey, 2024

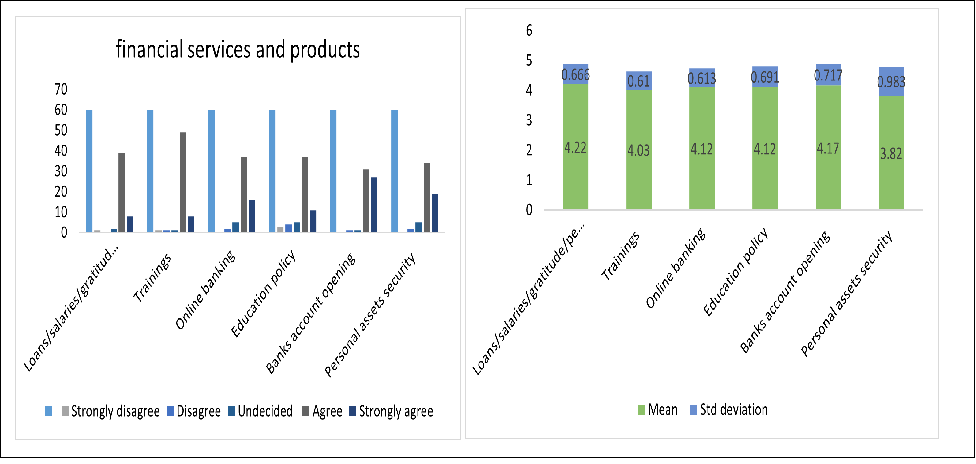

Table 4 study findings showed loans/salaries/gratitude/pension parameter assessed recording the highest value (x̄ =4.22, σ=0.666), followed by banks account ownership, online banking and education policy services with a value of (x̄ =4.17, σ=0.717), (x̄ =4.12, σ=0.691) and (x̄ =4.12, σ=0.613) respectively. Furthermore, personal assets and security services access recorded slightly the lowest value of (x̄ =3.82, σ=0.983).

The figure 3 below shows financial services and products access parameters’ mean and 5-point Likert scale data presentation

Source: Field Survey, 2024

The findings of the qualitative data analysis showed that the financial services and products provided to the locals and community members were essential to the financial institutions’ ability to survive in Turkana County. In order to stay up to date with the constantly shifting global financial dynamics, the majority of Turkana County’s financial institutions provide a variety of services and products, including loans, salaries, gratitude, and pensions; financial trainings for macro and micro enterprises and members; online banking; education policies; and bank account ownership rights. As a result of the members’ increased access to a wide range of financial services and products, banks have opened information booths and staff locations in rural Turkana County to accommodate the increasing demand for their services. Furthermore, the majority of respondents did not fully understand the parameter assessing personal asset security, as evidenced by their belief that assets should be used as loan security rather than being stored at home out of fear of theft. This resulted in the slightly lower average mean of x̄ =3.82 (see table 4).

Table 5: Descriptive analysis of challenges facing access to financial services and products parameters.

| Parameters assessed | Total | Strongly disagree | Disagree | Undecided | Agree | Strongly agree | Mean | Std deviation |

| 1. Cultural norms and values | 60 | 2

(3.3%) |

4

(6.7%) |

2

(3.3%) |

33

(55.0%) |

19

(31.7%) |

4.05 | .964 |

| 2. Peer pressure | 60 | 5

(5.0%) |

3

(5.0%) |

1

(1.7%) |

29

(48.3%) |

24

(40%) |

4.13 | 1.034 |

| 3. illiteracy | 60 | 2

(3.3%) |

2

(3.3%) |

3

(5.0%) |

33

(55%) |

20

(33.3%) |

4.12 | .904 |

| 4. Insecurity | 60 | 2

(3.3%) |

1

(1.7%) |

1

(1.7%) |

27

(45.0%) |

29

(48.3%) |

4.40 | .616 |

| 5. Poverty | 60 | 0

(0%) |

1

(1.7%) |

1

(1.7%) |

31

(51.7%) |

27

(45%) |

4.33 | .877 |

| 6. Poor infrastructure | 60 | 5

(8.3%) |

6

(10%) |

3

(5 %) |

17

(28.3%) |

29

(48.3%) |

3.98 | 1.308 |

Source: Field Survey, 2024

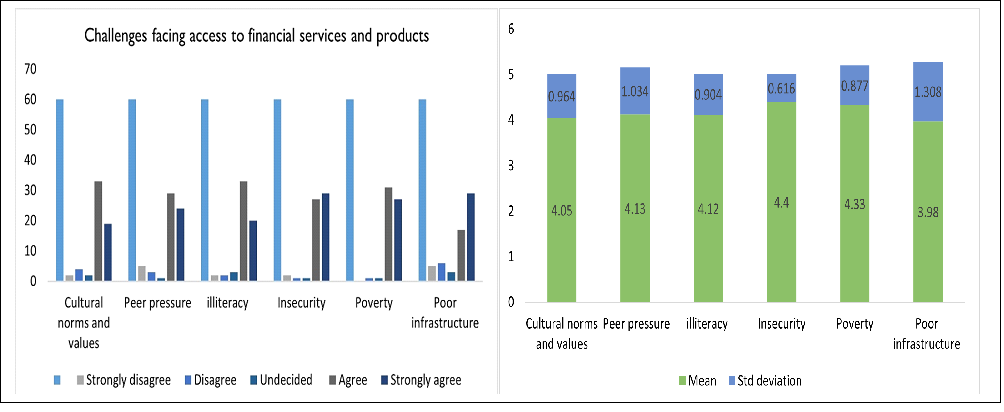

According to table 5, the poor infrastructure parameter recorded slightly the lowest value (x̄ =3.98, σ=1.308) while cultural norms and values (x̄ =4.05, σ=0.964), peer pressure (x̄ =4.13, σ=1.034), illiteracy (x̄ =4.12, σ=0.904) and insecurity (x̄ =4.40, σ=0.616) parameters recorded the highest value with an average mean of x̄ =4.206 translating to 84% of the target participants.

The figure 4 below shows Challenges facing access to financial services and products parameters’ mean and 5-point Likert scale data presentation.

Source: Field Survey, 2024

The results of both quantitative and qualitative data analysis demonstrated how Turkana County’s poor infrastructure, peer pressure, illiteracy, insecurity, poverty, and cultural norms and values prevent people from accessing financial services and goods. The idea that financial institutions expose people to western lifestyles that are at odds with traditional norms, values, and practices has been shown to represent the greatest damage to cultural norms and values. Furthermore, the low level of literacy among Turkana people has resulted in a decreased use of financial services and products, which has forced financial institutions to spend heavily on awareness-raising campaigns and capacity-building workshops to raise the general public’s level of financial literacy and numeracy. Additionally, border-related insecurity has resulted in a decline or lack of access to financial services and products, forcing suppliers to relocate their operations to other countries where there is little or no insecurity. Since most financial institutions have lost millions of dollars to hackers due to the growth in cybercrimes in Kenya, the situation has become worse as most people are turning to local conventional methods of saving money.

Relationship between financial inclusion and community empowerment

Table 6: Correlation between financial inclusion and community empowerment

| Community empowerment | ||

| Pearson Correlation | .845** | |

| Financial inclusion | Sig. (2-tailed) | .000 |

| N | 60 |

**. Correlation is significant at the 0.05 level (2-tailed).

The study finding in table 6 revealed a positive and strong correlation between the financial inclusion and community empowerment with a significant value (r = 0.845; p < 0.05). This implies that financial inclusion enhance access to financial products and services, education, and employment. The findings correlate with the qualitative analysis results in which access to financial inclusion in Turkana County has improved food security, reduced illiteracy level through access to education, increased access to information, social capital, health care, and improved nutrition status of the rural households.

CONCLUSION AND POLICY RECOMMENDATIONS

The results of the study showed how financial inclusion, with a focus on private companies, may empower community people and boost the nation’s economy. In addition to facilitating education, social capital, financial products and services, financial inclusion has lessened obstacles that prevent women in rural Turkana County from obtaining financial services and products, such as poverty, gender stereotypes, and cultural norms.

According to the qualitative analysis results, the financial institutions in partnership with local government and international organizations have designed programs targeting vulnerable households in rural parts of Turkana County to access financial capital through Biashara funds and Boma projects. Both Biashara funds and Boma project are tailored to address the household’s food insecurity and poverty. A robust system adopted in targeting process leads to the selection of the most vulnerable households which would then be trained, monitored and evaluated to ascertain their success rate prior to graduation from poverty. These approaches ought to be scaled up to target the growing population of the refugees in Kakuma camp to prevent future conflict arising between refugees and host community over the scarce resources and opportunities.

Although access to financial products and services in Turkana County faced challenges assessed in the study such as cultural norms and values, poor infrastructures, illiteracy, poverty, insecurity and peer pressure, the financial institutions have made strives to ensure they are able to withstand the market forces by developing new products and services and establishing outlet banking sites to meet the growing demands from both local and international citizens.

As policy recommendation based on the research finding, both the national and county government should incorporate financial inclusion concepts, principles and values in the legal and policy frameworks in order to leverage the private financial institutions support in addressing high unemployment rate, poverty and illiteracy levels among the Turkana community members. The department of economic planning in Turkana County should provide technical support in terms of designing monitoring system to track the effectiveness of implementation financial inclusion’s legal and policy framework.

Furthermore, financial literacy and numeracy training manuals must be contextualized to suite the local context’s needs and demand especially currently when the country’s economy is crippling due to global value chain disruptions. The gender mainstreaming aspects such as women empowerment must be incorporated into the training manuals to bridge the gender inequality gaps exacerbated by the community cultural forces.

Finally, the government should develop financial inclusion coordination mechanism with support of national drought management authority of Kenya to facilitate the implementation of financial inclusion interventions and develop framework for co-creation workshops to take stock of progress in terms of successes, challenges and explore more opportunities for future programming.

Areas of Further Studies

The study was restricted to secondary and primary data, which was primarily qualitative and quantitative in nature. As a result, statistical data in terms of analysis of poverty trends that led to the implementation of poverty graduation models, the number of households that benefited, the number of students who were sponsored and were able to access jobs at government and private companies, and the levels of investment in improving infrastructures are gray areas for future research.

Disclaimer

The arguments and views documented in the article are solely for authors and do not represent authors cited.

Conflict of interest

There was no conflict of interest in this article.

FUNDING STATEMENTS

The study was entirely conducted without any internal or external fundings.

REFERENCE

- Achugamonu, U. B., Adetiloye, K. A., Adegbite, O. E., Babajide, A. A., & Akintola, F. A. (2020). Financial exclusion of bankable adults: Implication on financial inclusive growth among twenty-seven SSA countries. Cogent Social Sciences, 6(1), 1730046. https://doi.org/ 10.1080/23311886.2020.1730046

- Aracil, E., Gomez-Bengoechea, G., & Moreno-de-Tejada, O. (2021). Institutional quality and the financial inclusion-poverty alleviation link: Empirical evidence across countries. Borsa Istanbul Review, 22(1), 179– 188

- Asongu et al, (2018). Inequality, information technology and inclusive education in sub-Saharan Africa: Technological Forecasting and Social Change: Volume 146, Pages 380-389

- Blando, S.C.F. (2013), Linking Financial Inclusion and Development. Spain: Facultad De Ciencias Económicas Y Empresariales.

- Brune, L., et al. 2015. “Facilitating Savings for Agriculture: Field Experimental Evidence from Malawi.” Economic Development and Cultural Change 64 (2): 187–220

- Chao-Béroff, R.: Reaching the Hard to Reach (Coady International Institute, Nova Scotia: 2008) “Rural Finance Today,” op. cit.

- Chu, L. K., Minh, P. N., & Huong, T. H. D. (2019). Determinants of financial inclusion: New evidence from panel data analysis. https://ssrn.com/abstract.

- Clarke, G.R.G., Cull, R., Fuchs, M. (2007), Bank Privatization in Sub-Saharan Africa: The Case of Uganda Commercial Bank. New Delhi: Policy Research Working Paper No. 4407.

- Deminrgue, Klapper, singer, Ansar and Hess J. (2018. Measuring financial inclusion and the fintech revolution. In the Global findex database. Washington, DC, USA: The World bank.

- El-Bourainy. M, Salah. A, ElSherif .M, (2020): Impact of the financial inclusion on the unemployment in rate in developing countries; International Journal of Economics and Financial;Vol, 11(1), pp 79-93.

- Ibrahim et al, (2019): An examination of the Impact of Financial Inclusion on Poverty Reduction: An Empirical Evidence from Sub-Saharan Africa: International Journal of Scientific and Research Publications, Volume 9, Issue 1, p8532 http://dx.doi.org/10.29322/IJSRP.9.01.2019.p853

- ILO: Financial Education for Youth: Trainers’ Manual and Trainee’s Guide: Nepal (2011).

- ILO: Financial Education: Trainer’s Manual: Cambodia (2008)

- ILO: Building Financial Capability for the Vulnerable Households: A Manual for Individual Training / Counselling Session: Moldova (2008)

- ILO: Village Banking in Lao PDR Materials: Lao PDR (2008) ILO: Guarantee Funds for Small Enterprises: A Manual for Guarantee Fund Managers (Geneva: 2004).

- Hannig, A., Jansen, S. (2010), Financial Inclusion and Financial Stability: Current Policy Issues. Japan: ADBI Working Paper.

- Kondo, T. (2007), Impact of Microfinance on Rural Households in the Philippines: A Case Study from the Special Evaluation Study on the Effects of Microfinance Operations on Poor Rural Households and the Status of Women. Philippines: Asian Development Bank.

- Lenka, S. K., & Barik, R. (2018). A discourse analysis of financial inclusion: post-liberalization mapping in rural and urban India. Journal of Financial Economic Policy, 10(3), 406–425.

- Musau, S., Muathe, S., & Mwangi, L. (2018). Financial inclusion, bank competitiveness and credit risk of commercial banks in Kenya. International Journal of Financial Research, 9(1), 203. https://doi.org/10.5430/ ijfr. v9n1p203.

- Matu Mugo M. and Evelyne K. (2007) UN-SDGs-Paper5May2017-Kenya-Financial-Inclusion.pdf.

- Nagarajan, G.; Meyer, R.: “Rural Finance Today,” in Finance for the Poor, Vol. 7 No. 4 (2006).

- Nandru, P., Anand, B., Rentala, S. (2016), Exploring the factors impacting financial inclusion: Evidence from South India. Annual Research Journal of Symbosis Centre for Management Studies Pune, 4, 1-15

- Nkoa, B. E. O., & Song, J. S. (2020). Does institutional quality affect financial inclusion in Africa? A panel data analysis. Economic Systems, 100836. https://doi. org/10.1016/j.ecosys.2020.100836.

- Schaner, S. 2016. “The Cost of Convenience? Transaction Costs, Bargaining Power, and Savings Account Use in Kenya.” Journal of Human Resources, 0815-7350R1.

- Suri, T., and W. Jack. 2016. “The Long-run Poverty and Gender Impacts of Mobile Money.” Science 354 (6317): 1288–1292

- Yorulmaz, R. (2013), Construction of a regional financial inclusion index in Turkey. Journal of BRSA Banking and Financial Markets, 7(1), 79-101

- Van Biljon, C., Von Fintel, D., & Pasha, A. (2018). Bargaining to work: The effect of female autonomy on female labour supply. Stellenbosch Working Paper Series No. 04/2018. Department of Economics, Stellenbosch University.

- World Bank. (2018). Financial inclusion is a key enabler to reducing poverty and boosting prosperity. Retrieved from https://www.worldbank.org/en/ topic/financial inclusion/overview. Consultative group to assist the poor: Financial Access (Washington: 2009)

- Wokabi, V. W., & Fatoki, O. I. (2019). Determinants of financial inclusion In East Africa. International Journal of Business and Management, VII (1), 125–143. https://doi.org/10.20472/BM.2019.7.1.009