Financial Management Practices and Achievement of Financial Outcomes of Primary Schools in Kilifi Sub-County, Kenya

- Dr. Charles Omwanza

- Prof. Anne Ndiritu

- Dr. Maurice Odondo

- 4507-4517

- Feb 22, 2025

- Education

Financial Management Practices and Achievement of Financial Outcomes of Primary Schools in Kilifi Sub-County, Kenya

Dr. Charles Omwanza1, Prof. Anne Ndiritu2, Dr. Maurice Odondo3

1,3Kenya Education Management Institute

2University of Nairobi

DOI: https://dx.doi.org/10.47772/IJRISS.2025.9010344

Received: 09 January 2025; Accepted: 15 January 2025; Published: 22 February 2025

ABSTRACT

The Kenyan Basic Education Act (2013) requires effective financial management in public schools, entrusting Boards of Management and school heads with the responsibility of adopting sound financial practices. This responsibility includes managing government grants, donations, parental contributions, and other funds to achieve both academic and financial goals. Effective financial management is essential to constructing school infrastructurprovidingide learning materials, hire staff, and enhance student and staff welfare. However, poor financial management can lead to fraud, misallocation of resources, and unrest, which can hinder schools’ performance. This study explored the financial management practices of primary schools in Kilifi County, Kenya, examining the impact of budgeting, record-keeping, cash flow management, procurement, and revenue generation on achieving financial objectives. The research revealed that, despite significant adherence to budgeting and stakeholder engagement, some schools show weaknesses in documentation and record-keeping, indicating an area for development. While most schools maintain solid cash flow policies and meet financial obligations, a few face challenges with consistent cash flow. Additionally, findings suggest that many schools have robust procurement and expenditure management processes, though improvements in transparency and documentation could enhance accountability. Schools generally exhibit strong accountability and reporting practices, ensuring stakeholders are informed about financial performance. However, challenges remain, including insufficient funding, delays in fund disbursement, and limited revenue diversification, which impact some schools’ ability to meet financial targets. The study concludes that while primary schools in Kilifi County demonstrate commitment to financial management, the attainment of financial goals is hampered by external funding constraints and occasional lapses in financial planning. It recommends that schools strengthen documentation, enhance staff financial training, improve cash flow strategies, diversify revenue streams, and advocate for timely funding to promote financial resilience and sustainability.

INTRODUCTION

The Kenyan Basic Education Act (2013) prescribes how schools should manage their financial resources. It mandates the Boards of Management and the Heads of Institutions to ensure the adoption of prudent financial management and utilization of school funds (Republic of Kenya, 2013). These finances are obtained from government capitation grants, income-generating activities, donations, parental contributions, and other voluntary contributions from interested parties. Effectively managed financial resources affect the ability of the schools to attain their financial goals. Uddin &Ahsan (2019) posits that proper financial management practices are associated with achieving financial objectives, as it aligns day-to-day operations with strategic goals.

Schools worldwide are established to deliver quality education and achieve learning outcomes for the students they serve. Attaining this objective is contingent upon the allocation of financial resources, as no institution has successfully operated in the absence of adequate funding, and schools are no exception (Vicente et al., 2023). Beyond academic goals, which are the primary focus of educational institutions, schools also pursue financial objectives. Financial resources are the foundation of educational institutions, enabling them to construct necessary infrastructure, procure teaching and learning materials, employ staff, and enhance the overall welfare of students and staff members (Jilani & Mbirithi, 2022). Poor financial management results in high levels of fraud, embezzlement of funds, stagnated growth, poor welfare of learners, and indiscipline, and may eventually lead to unrest which may lead to poor performance of these schools (Atieno & Kiganda, 2020).

To effectively manage these financial resources, school leaders adopt various financial management practices. These practices include financial planning and budgeting, procurement and asset disposal, revenue collection and payment systems, inventory management, cash flow management, and financial auditing (Idris, 2018). Such practices are integral to the sustainable management of school finances, ensuring that resources are utilized effectively to support both academic and operational goals.

Financial management is fundamental for the improvement of the efficient and effective use of finances in schools for the attainment of schools’ financial goals. It facilitates the achievement of growth and stability of educational institutions (Munyalo & Njoka, 2022). Amidst the evolving landscape of educational finance, there is a growing need to examine and understand the key themes and characteristics of financial management practices in public primary schools and its relationship with the attainment of financial goals (Baaru, 2019). While existing literature offers insights into financial management practices in schools, there remains a gap in systematically synthesizing and analyzing the prevailing practices and emerging trends various parts and counties of Kenya. This study sought to establish the relation between financial management practices and the achievement of financial outcomes of primary schools in Kilifi County in Kenya.

Namai (2018) opined that financial management entails fundraising and utilization of the financial resources of a school. According to the Basic Education Act (2013) and TSC Act (2012) heads of institutions are the accounting officers of the schools. They are accountable to the government and all other stakeholders for the use and management of school finances (Baaru, 2019). Accordingly, they are expected to adopt financial management practices to achieve the financial goals of their schools. According to Eya (2019), financial management practices in schools entails budgeting, record keeping, reporting, procurement as well as revenue generation and utilization.

Budgeting is a critical component of school planning, essential for upholding fiscal discipline and achieving both operational and allocative efficiency within educational institutions. It is incumbent upon school administrators to ensure accountability and prudent management of financial resources (Kagendo, Onyango, & Kyalo, 2019). Institutional leaders must possess a comprehensive understanding of income and expenditures, meticulously document financial activities, and be prepared to communicate these aspects to various stakeholders. A thorough grasp of the financial workings of their institution is imperative for each school leader (Simiyu & Kaplelach, 2018). Moreover, schools are required to systematically record financial transactions in their accounting ledgers to accurately assess any surpluses or deficits, thus supporting informed financial decision-making.

Statement of the Problem

The Basic Education Act (2013) mandates the Boards of management to ensure that prudent financial practices are adopted in the schools. Further, the TSC act also charges heads of institutions with the role of accounting officers of the schools (Republic of Kenya, 2013). Whereas progress have been made on the adoption of good financial practices in schools, there is little progress made in the attainment of financial goals of learning institutions.

The systematic literature review conducted in this study unveiled a diverse array of financial management practices adopted by public schools. These practices spanned various areas, including planning and budgeting, record keeping, resource allocation, procurement, internal auditing, and stakeholder involvement (Idris, 2018). Despite the existence of these practices, the majority of the primary schools in Kenya have not embraced them (Kalume & Ng’ang’a, 2024). Limited studies have also been conducted in Kenya to determine the effect of these financial management practices on the attainment of schools’ financial goals (Dadu, Njeri, & Kemunto, 2024). Few studies have also highlighted the presence of robust financial management systems in certain schools, which lacked the attributes of good governance such as participation, transparency, accountability, effectiveness, efficiency, and inclusivity (Munyalo & Njoka, 2022). Further, schools are grappling with the challenge of being unable to attain their financial objectives (Atieno & Kiganda, 2020). These schools also did not demonstrate any understanding of good practices in financial management that are essential to help public primary schools to set and pursue financial goals for each financial year.

Research Objectives

- To determine the effect of planning and budgeting on the attainment of financial goals of primary schools in Kilifi County

- To establish the effect of financial record keeping on the attainment of financial goals of primary schools in Kilifi County.

- To determine the effect of procurement and expenditure management on the attainment of financial goals of primary schools in Kilifi County

- To determine the effect of accountability and reporting on the attainment of financial goals of primary schools in Kilifi county

- To find out the effect of revenue generation and utilization on the attainment of financial goals of primary schools in Kilifi County.

LITERATURE REVIEW

Kinyanzii (2023) examined how financial management practices, including budgeting, procurement, and financial recording, influence the financial performance of public secondary schools in Kathiani sub-county, Machakos County. Targeting 30 schools, it? utilized empirical literature and theories like Stakeholder Theory, Iceberg Theory of Money Management, and Agency Theory to identify research gaps. A descriptive survey design and questionnaires filled by school leaders gathered data, analyzed using SPSS and Microsoft Office Suite. The findings revealed a statistically significant impact of financial management practices on financial performance, with budgeting having the most notable effect, closely followed by procurement and financial recording. The study recommended ongoing training for school leaders on these practices and suggested further research on additional variables, as well as a comparative analysis between public and private schools to explore factors affecting financial performance.

Kalume and Ng’ang’a (2024) sought to establish the effect of financial management practices on fund management in secondary schools in Kilifi County. Using a descriptive design and stratified sampling technique, the study sampled 85 secondary schools out of 107 possible schools. The study results showed that the budgeting process significantly improved fund management in secondary schools in Kilifi County. The study recommended that schools involve all stakeholders in the budgeting process. The study focused only on budgeting practices as the only financial management practice.

METHODOLOGY

The study utilized concurrent mixed research methods, incorporating both quantitative and qualitative approaches. This choice was warranted by the collection of both primary and secondary data. Purposive sampling was employed to identify target respondents during the initial phase. The financial management practices focused on primary schools in Kilifi County, Kenya, and their Heads of Institutions (HOIs). Primary data was gathered from 162 respondents through questionnaires. Data was collected using a structured, online survey questionnaire. The survey was designed to gather qualitative and quantitative data on the financial management practices in place, as well as respondents’ perceptions regarding the strengths, weaknesses, and challenges within the school’s financial system. Data entry and analysis were conducted using SPSS version 26 and MS Excel, with descriptive analysis performed that included frequencies, percentages, and crosstabulations, all presented through tables and graphs along with appropriate interpretations. The research adhered to ethical guidelines, ensuring that participation was voluntary and that all responses remained confidential. Respondents were informed of the purpose of the research and were assured that the data would be used solely for academic and improvement purposes.

DISCUSSION OF FINDINGS

The findings were based on the online survey questionnaires administered to the primary school heads in Kilifi.

Biodata

Age by Gender

| Age Group | Female (%) | Male (%) |

| 36 – 45 Years | 12.5% | 87.5% |

| 46 – 55 Years | 23.9% | 76.1% |

| Above 56 | 48.1% | 51.9% |

This data indicates that male HOIs are more prevalent in the younger age groups (36-45 years and 46-55 years), while the gender disparity decreases significantly among HOIs over 56 years.

Length of service in the current position

This shows that the majority of HOIs (39.5%) have served between 1-5 years, while a significant number have served for more than 10 years (28.4%)

Thematic Areas

Financial Planning and Budgeting

The analysis of financial planning and budgeting practices in Kilifi Kenyan primary schools reveals a robust and well-structured approach to financial management across institutions. The findings demonstrate that an overwhelming majority of primary school heads actively participate in comprehensive financial management practices, with particularly strong performance in regular financial review and stakeholder engagement. Notably, 92.7% of school heads actively engage in reviewing and adjusting their financial plans according to available funds and needs, while a similar percentage (92.6%) ensures inclusive participation of key stakeholders such as board members, teachers, and administrators in the budgeting process.

The commitment to fiscal discipline is evidenced by 87.8% of schools closely adhering to their approved budgets throughout the academic year, while 82.9% maintain well-documented financial plans to guide their management practices. This systematic approach to financial management suggests a strong foundation for sustainable school operations and resource allocation. However, despite these positive indicators, there remain opportunities for enhancement in certain areas. The presence of neutral responses ranging from 4.9% to 12.2% across various aspects of financial management, along with a small percentage (1.2-2.4%) of negative responses, indicates room for improvement. Particularly, the slightly higher neutral responses (12.2%) regarding well-documented financial plans suggest this as a potential area for focused development.

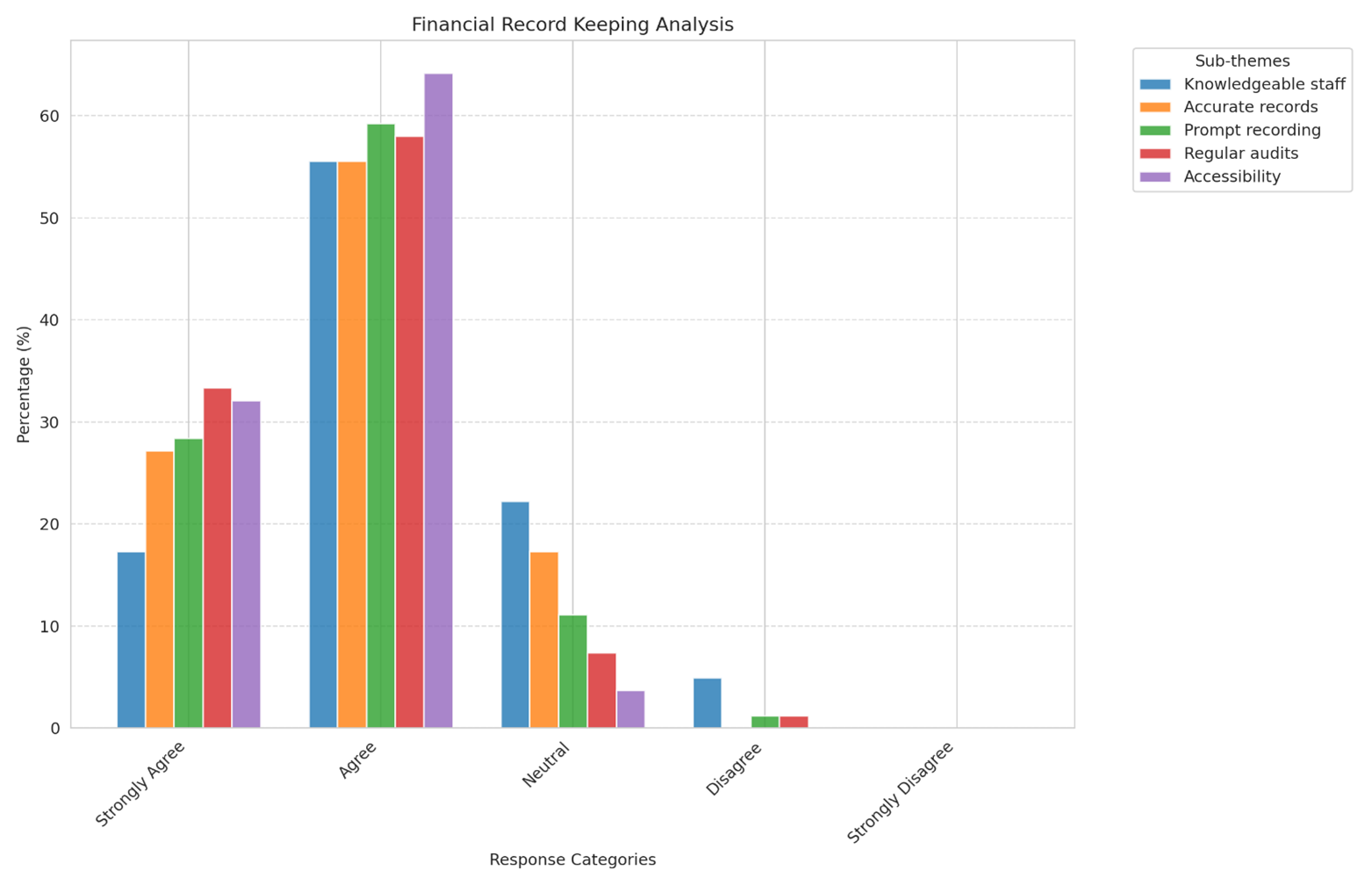

Financial Record Keeping

The findings suggest that primary schools in Kilifi generally maintain solid financial record-keeping practices, including easy access to records, regular audits, and timely transaction entries. However, there is room for improvement in enhancing staff expertise in financial record keeping, as only a small percentage strongly agree that their schools have highly knowledgeable personnel in this area.

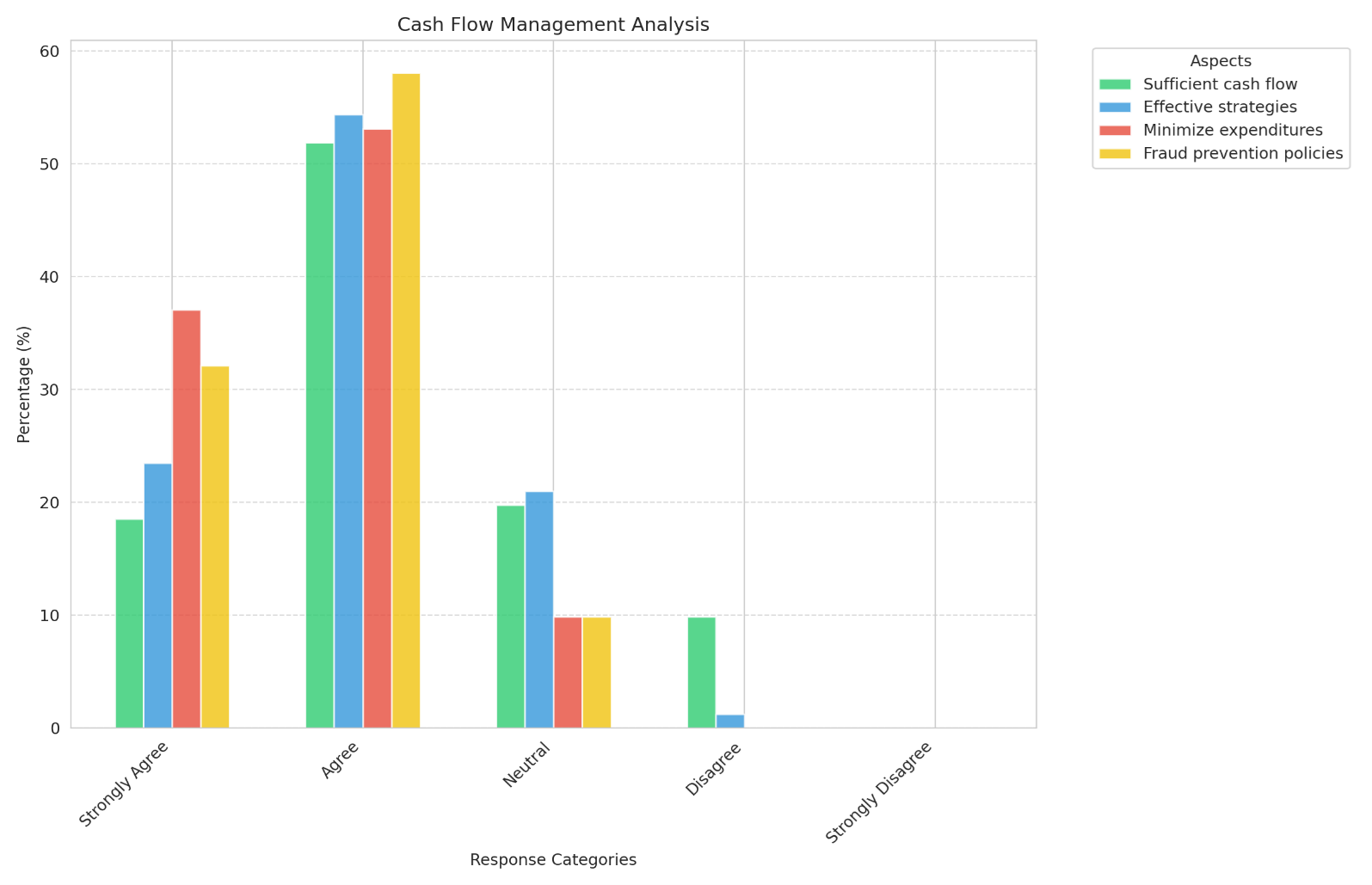

Cash Flow Management

The findings indicate that the majority of primary schools in Kilifi have policies in place to prevent cash mismanagement, reduce unnecessary spending, and manage cash flow effectively throughout the year. However, the results also imply that some schools may need to enhance their strategies to ensure adequate cash flow for consistently meeting their financial obligations.

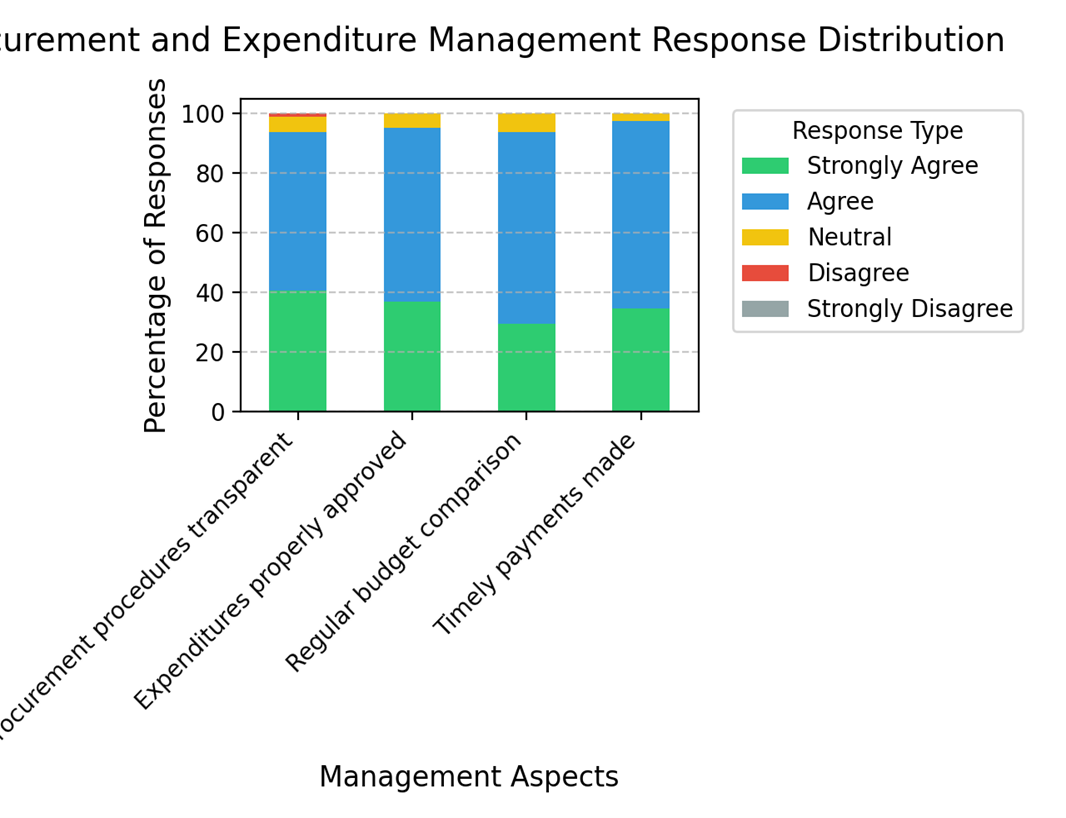

Procurement and Expenditure Management

The findings indicate that procurement and expenditure management in Kilifi primary schools are largely effective, as schools make timely payments, frequently compare expenditures against budgets, and adhere to approval processes. While the transparency of procurement procedures is a positive element, ongoing efforts to enhance documentation and accountability would be advantageous.

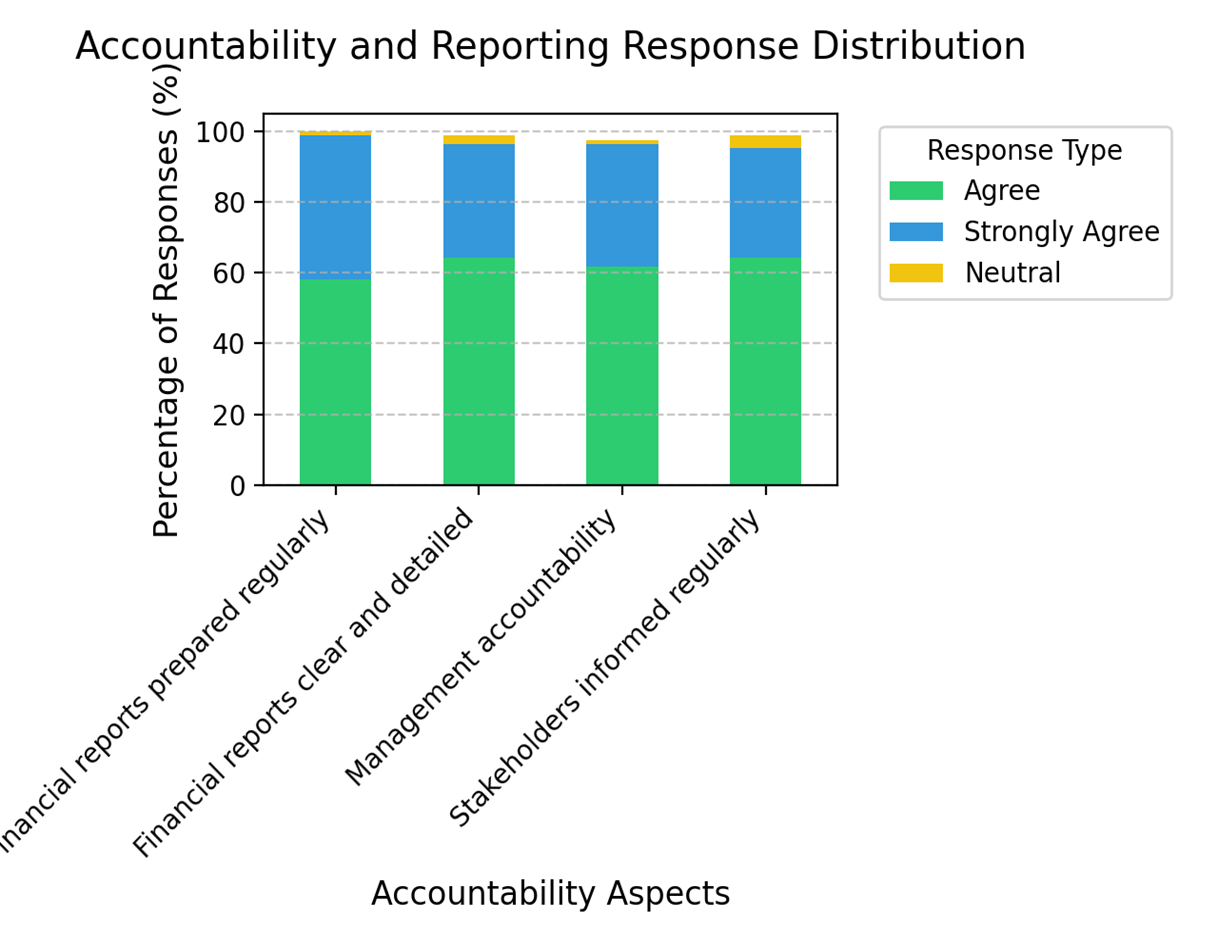

Accountability and Reporting

The findings show that primary schools in Kilifi exhibit a strong commitment to accountability and transparency in their financial reporting. Most schools consistently communicate their financial performance to stakeholders, hold management accountable for any financial mismanagement, and provide clear and detailed financial reports. Established reporting practices ensure that stakeholders are kept well-informed.

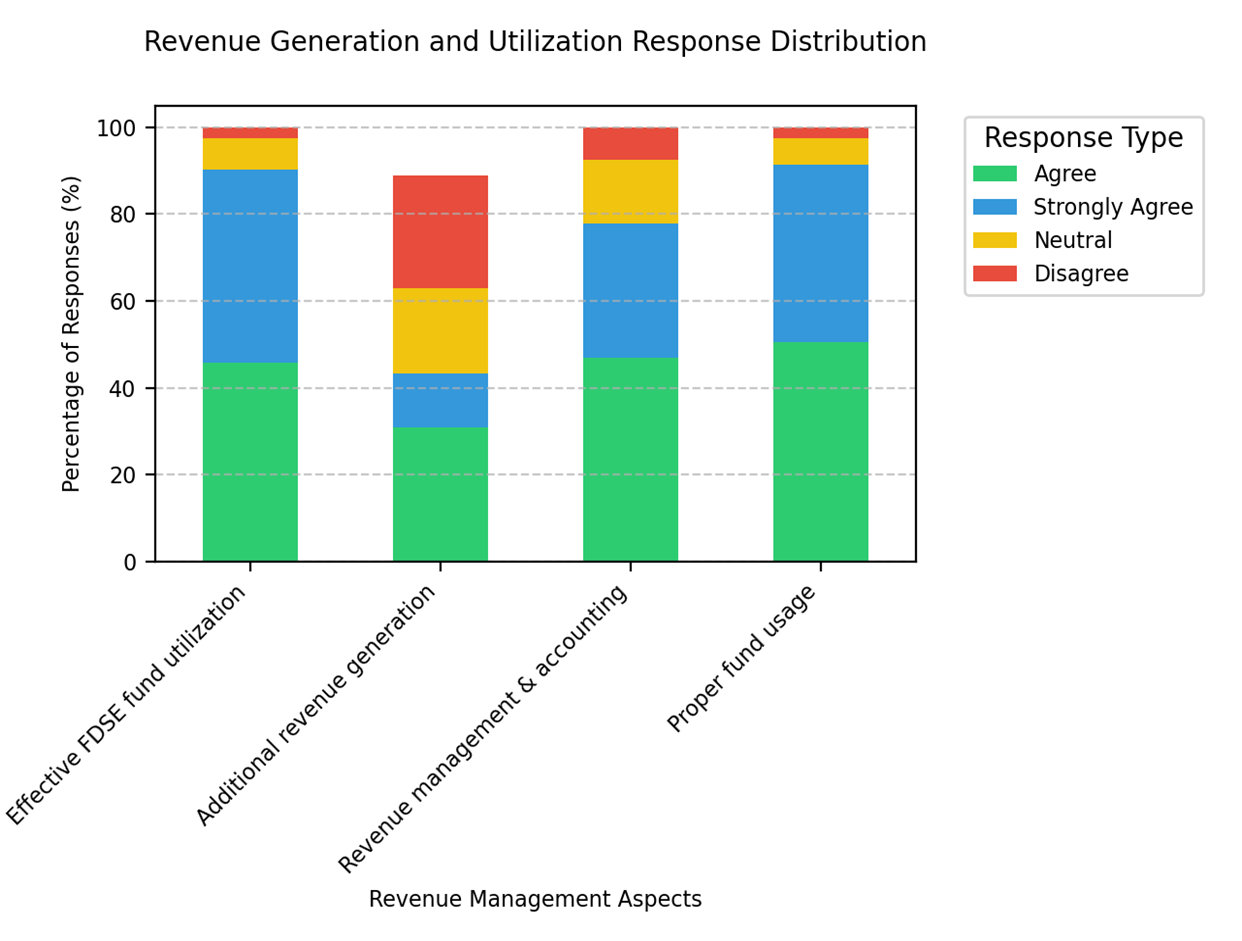

Revenue Generation and Utilization

The findings suggest that the majority of schools in Kilifi manage and utilize their funds effectively, especially in preventing misuse and making efficient use of government funding. However, there is a notable shortfall in generating additional income from legitimate sources, such as income-generating projects, which could contribute to financial sustainability. Strengthening efforts to diversify revenue sources could be advantageous for many schools.

Achievement of Financial Targets

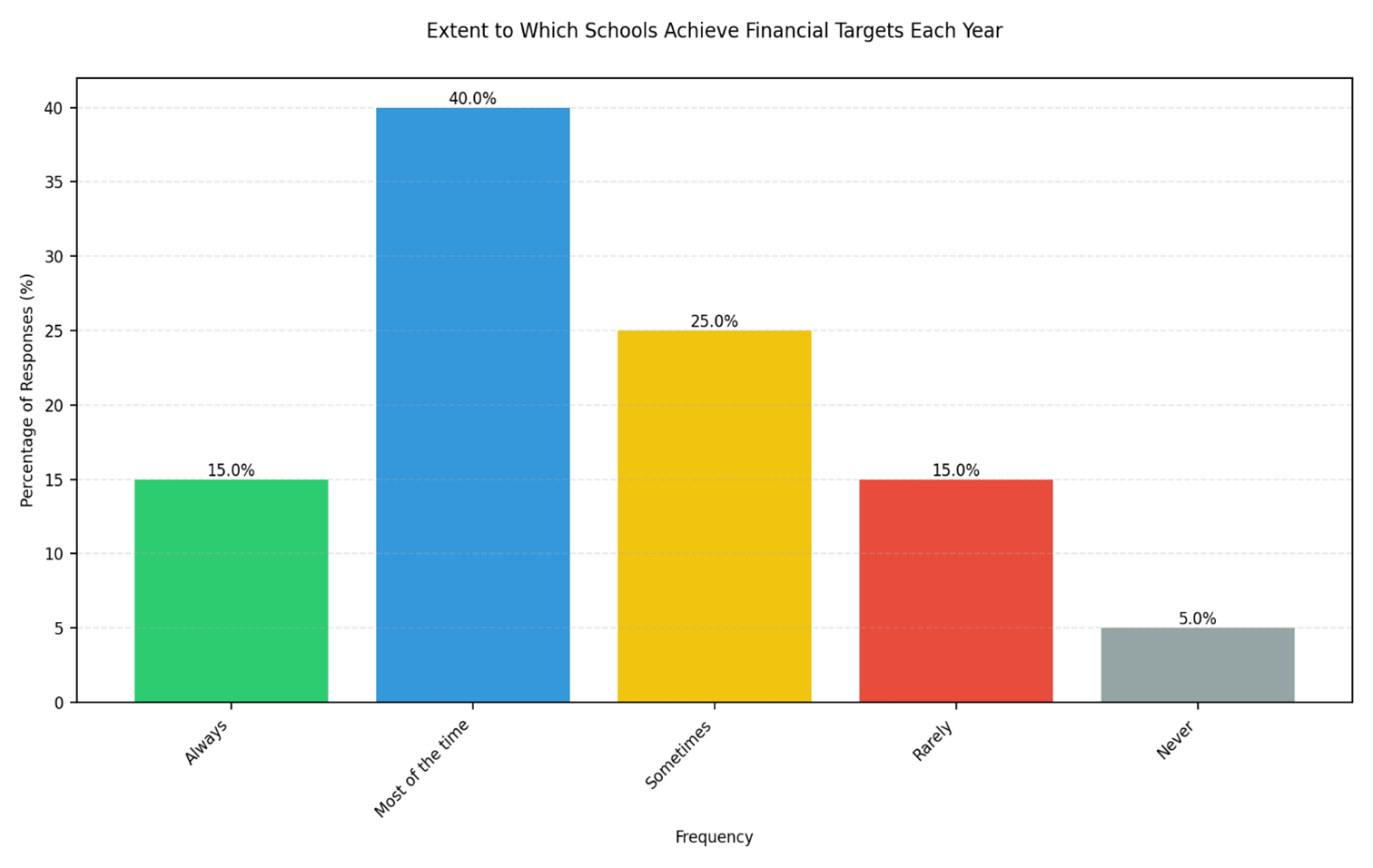

Extent to which schools achieve financial target each year

Most Kilifi primary schools (40.0%) report meeting their financial targets frequently, while a quarter (25%) achieve them only occasionally. A small proportion of schools (15.0%) rarely meet their financial goals, and 5.0% never do so. This suggests that while many schools show a moderate to high level of financial success, there is still potential for improvement in financial planning and implementation to ensure consistent achievement of their financial targets.

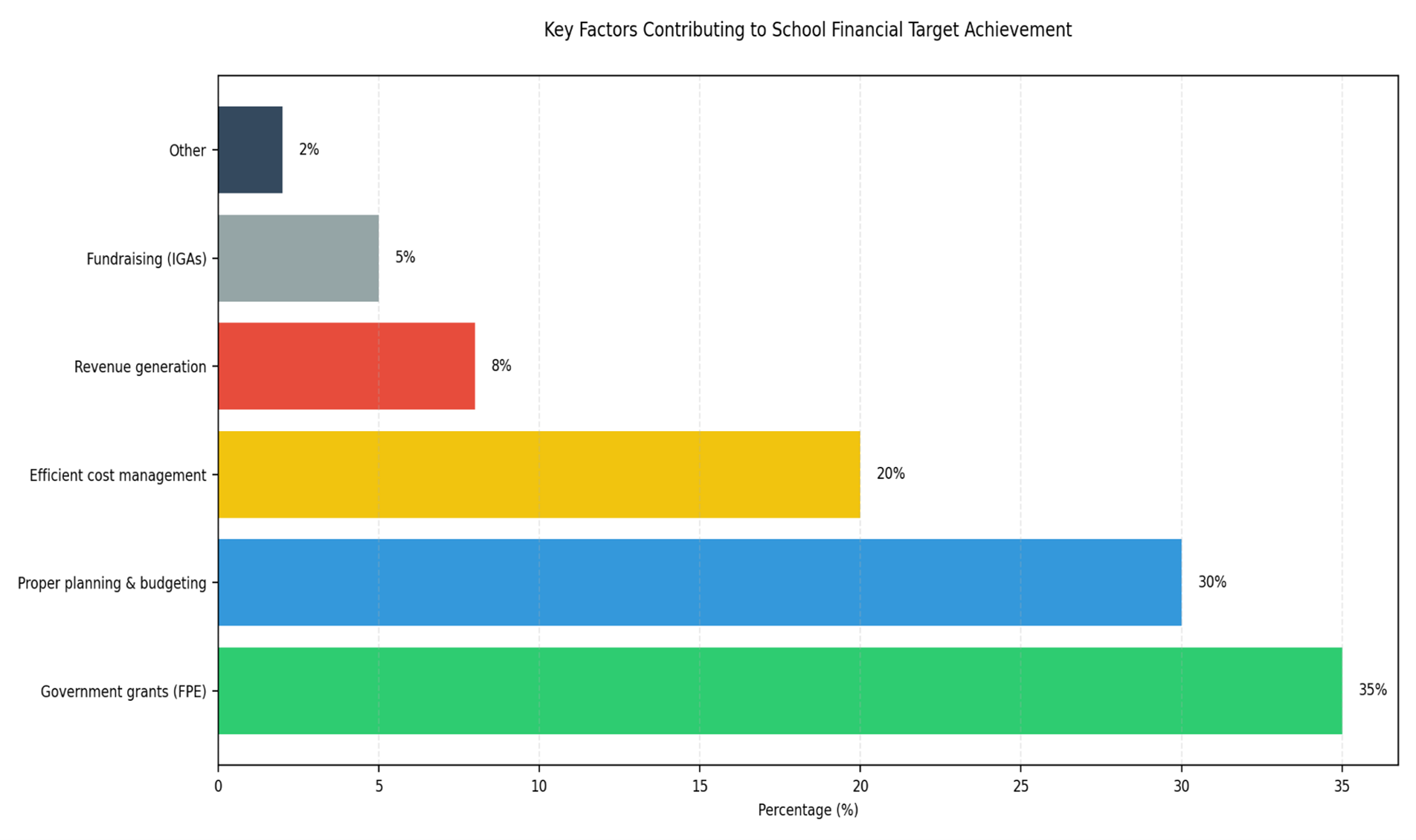

Key factors that contribute to the achievement of financial targets schools

The findings indicate that government funding and effective planning/budgeting are the key factors enabling Kilifi primary schools to meet their financial targets. Although some schools emphasize efficient cost management, revenue generation and fundraising efforts have a limited impact, implying that schools could enhance their financial stability by seeking more diverse revenue streams.

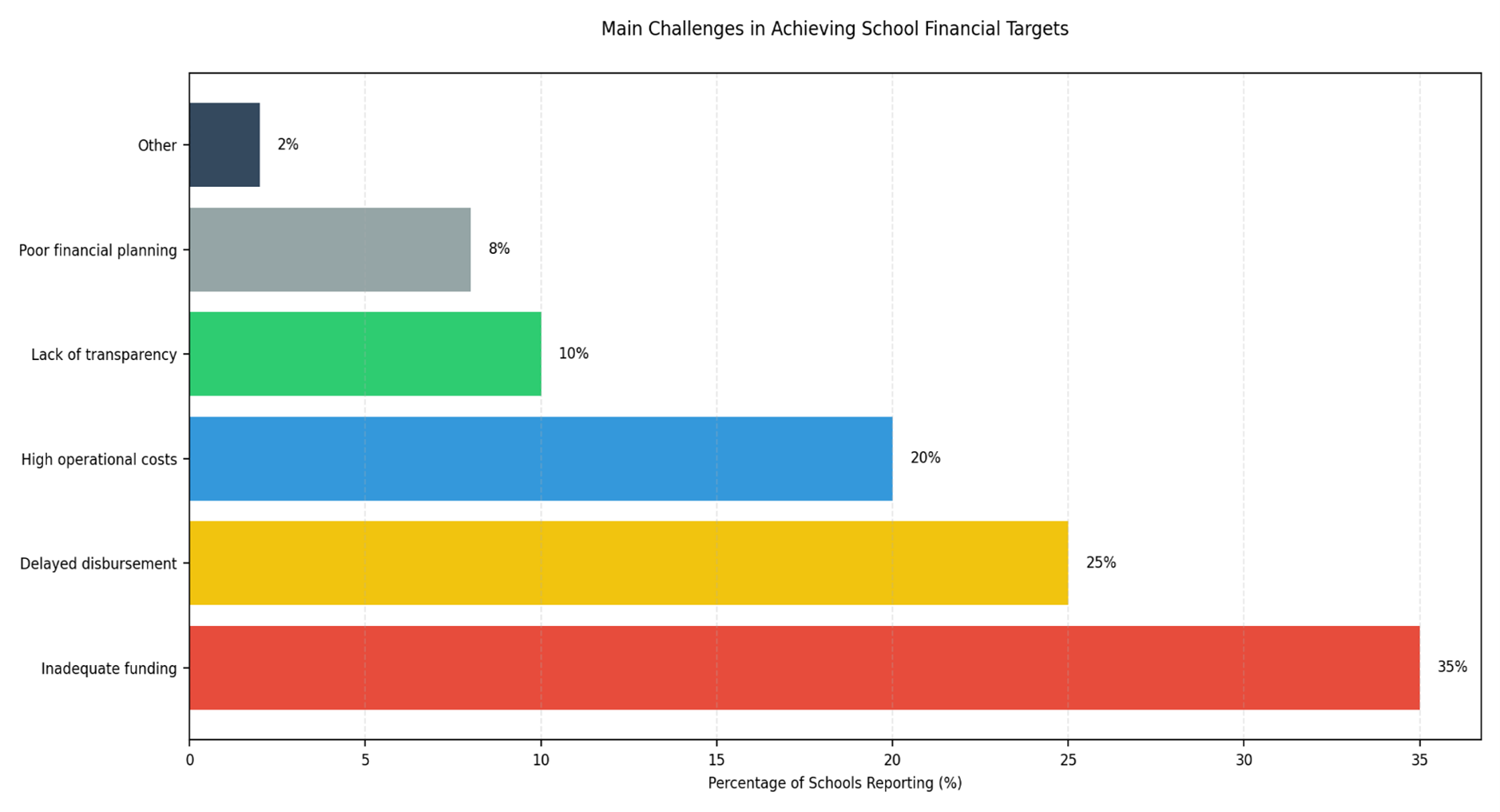

Main challenges in achieving the school’s financial targets

The findings highlight that insufficient funding is the most significant challenge impacting the financial performance of primary schools in Kilifi, followed by delays in fund disbursement and high operational costs. A smaller number of schools experience difficulties related to inadequate financial planning, suggesting that while planning may be sufficient for most institutions, external financial constraints continue to be the primary concerns.

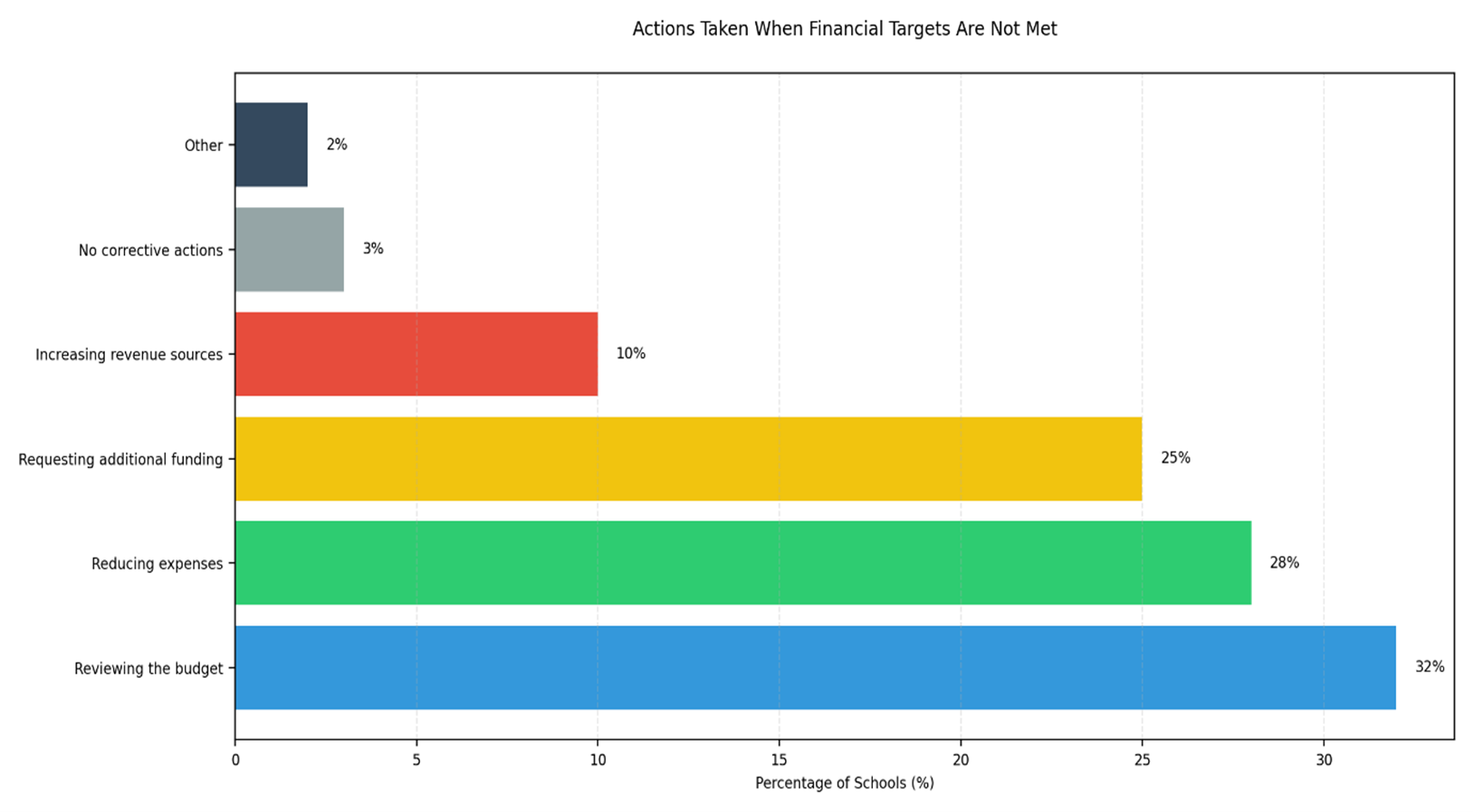

Actions taken by schools to address situations where financial targets are not met

The findings indicate that the majority of Kilifi primary schools address unmet financial targets by revising their budgets and cutting expenses. Seeking additional funding and expanding revenue sources are less frequently employed strategies, with very few schools opting not to take any corrective measures. This underscores the significance of budget adjustments and expense management as key approaches to tackling financial difficulties in schools.

CONCLUSIONS

Based on the study’s findings, several key conclusions can be drawn regarding the relationship between financial management practices and the achievement of financial goals in primary schools within Kilifi County, Kenya:

- Financial Planning and Budgeting: The study demonstrates a strong commitment to financial planning and budgeting among primary schools, with high engagement from school heads in reviewing and adjusting financial plans. This robust approach, involving stakeholder participation, significantly contributes to achieving financial targets. However, slight gaps in maintaining well-documented financial plans suggest opportunities for improvement.

- Financial Record Keeping: Primary schools generally maintain solid financial record-keeping practices, ensuring accessible records and regular audits. Nonetheless, limited expertise in financial record-keeping among staff indicates the need for additional training to enhance accuracy and transparency in financial management.

- Cash Flow Management: Schools largely prevent cash mismanagement and control unnecessary spending through effective cash flow management policies. Yet, some schools face challenges in maintaining consistent cash flow, impacting their ability to meet financial obligations on time.

- Procurement and Expenditure Management: Effective procurement and expenditure practices, such as adherence to budgets and transparent approval processes, are common among Kilifi schools. However, there is room to strengthen documentation and accountability, which could further support financial integrity.

- Accountability and Reporting: Most schools in Kilifi uphold accountability through regular financial reporting and transparency, thereby ensuring stakeholders are well-informed. This commitment enhances trust and aligns with responsible financial stewardship.

- Revenue Generation and Utilization: Although schools effectively utilize funds and prevent misuse, many lack diverse revenue streams, which limits their financial sustainability. Efforts to create additional income from projects could improve long-term financial stability.

- Achievement of Financial Targets: While many schools regularly meet their financial targets, some struggle due to factors like insufficient funding, delayed fund disbursements, and high operational costs. This reveals the need for enhanced financial planning and diversification of income sources to sustain financial health.

RECOMMENDATIONS

To address the challenges identified and enhance the attainment of financial outcomes, the following recommendations are proposed:

- Strengthen Documentation in Financial Planning: Schools should develop well-documented financial plans and conduct regular reviews to ensure fiscal discipline. This would improve accountability and allow for better alignment with financial goals.

- Enhance Financial Training: To improve record-keeping practices, schools should invest in financial management training for staff. By increasing their expertise, schools can ensure accurate record-keeping and greater transparency in financial transactions.

- Implement Cash Flow Improvement Strategies: Schools should assess their cash flow management policies to ensure adequate cash reserves are maintained. Developing strategies to manage seasonal variations in funding could help in meeting financial obligations consistently.

- Increase Accountability in Procurement and Expenditure: Schools should enhance the transparency and documentation of procurement processes. By establishing clear procedures and regular audits, schools can improve accountability, which would minimize financial risks.

- Diversify Revenue Streams: Schools are encouraged to explore income-generating projects, such as small businesses, which can provide additional funds. This diversification would reduce reliance on government funding and strengthen financial resilience.

- Address Funding Challenges through Advocacy: Schools, together with education authorities, should advocate for timely disbursement of government funds. Schools could also seek partnerships with community organizations to supplement financial resources.

- Review Financial Targets Regularly: Schools should conduct regular assessments of financial target achievement and adjust their strategies as needed. This would allow for timely corrective measures, such as budget adjustments, to mitigate the effects of financial shortfalls.

REFERENCES

- Atieno, O. M., & Kiganda, E. (2020). Internal Control Systems on Financial Accountability in National Public Secondary Schools in Kenya. European Journal of Economic and Financial Research, 4(3)

- Baaru, C. M. (2019). Effectiveness of Sch ool Boards in Managing Financial and Human Resources in Public Primary Schools in Nyeri County, Kenya. Journal of Arts and Humanities, 8(6), 77-87.

- Dadu, T. Z., Njeri, I., & Kemunto, A. (2024). Grant Management Practices and Financial Sustainability Among Non-Governmental Organizations in Taita-Taveta County: A Case of World Vision Kenya. International Academic Journal of Economics and Finance, 4(2), 104-140.

- Eya, L.O. (2019). Financial Management Practices of Secondary School Principals in Enugu State. Journal of Research and Method in Education, 2 (6) 14-18.

- Idris, O. S. (2018). The Role of Principal in School Financial Management: The Current Status A Case Study in Four Public Secondary Schools in Zoba Debub, Eritrea. Journal of Education and Practice, 9(33), 53-60.

- Jilani, A. K., & Mbirithi, D. M. (2022). Management Challenges Faced by Public Primary School Headteachers in the Implementation of Performance Contracting in Ganze Sub- County, Kilifi County Kenya. International Academic Journal of Social Sciences and Education (IAJSSE), 2(3), 94-109.

- Kagendo, A. D., Onyango, G., & Kyalo, D. (2019). Extent of Student Participation in Management of School Finances and Physical Resources in Secondary Schools in Tharaka-Nithi And Nairobi Counties, Kenya. Journal of Education and Practices ISSN 2617-5444 (ONLINE) & ISSN 2617-6874 (PRINT), 2(1), 10-10.

- Kalume, S. B., & Ng’ang’a, P. (2024). Financial Management Practices and Funds Management in Public Secondary Schools in Kilifi County, Kenya. International Academic Journal of Economics and Finance, 4(2), 306-323.

- Munyalo, A., & Njoka, C. (2022). Financial Management Capabilities and Financial Health of Public Secondary Schools in Nyeri County, Kenya. African Journal of Emerging Issues, 4(3), 11-41.

- Namai, L. B. A. (2018). Utilization of Free Primary Education Funds in Public Primary Schools in Kenya: Exploring Administrative Antecedents. International Journal of Educational Administration and Policy Studies, 10(11), 160-168.

- Republic of Kenya. (2013). The Basic Education Act 2013 No.14 0f 2013. Nairobi.

- Simiyu, S. N., & Kaplelach, M. S. (2018). Integrated Financial Management Information System Implementation and Public Finance Management in Kilifi County, Kenya. Strategic Journal of Business and Change Management, 12(2), 1-68.

- Uddin, M. N., & Ahsan, M. T. (2019). “Role of Financial Management Practices on Performance of Micro Enterprises in Bangladesh.” Journal of Business & Management, 21(1), 13–21

- Vicente, R. S., Flores, L. C., Almagro, R., Amora, M. R. V., & Lopez, J. P. (2023). The Best Practices of Financial Management in Education: A Systematic Literature Review. International Journal of Research and Innovation in Social Science (IJRISS) Doi, 10.