Financial Technologies (Fintech) and Financial Development in Nigeria

- James Obilikwu

- 3111-3123

- Jul 23, 2024

- Economics

Financial Technologies (Fintech) and Financial Development in Nigeria

James Obilikwu

Department of Economics

Ibrahim Badamasi Babangida University, Lapai, Niger State, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.806235

Received: 13 June 2024; Revised: 30 June 2024; Accepted: 04 July 2024; Published: 23 July 2024

ABSTRACT

A developed financial sector plays critical roles in economic growth of nations as such it is important to know what determine financial development in a country. This study investigated the impacts of financial technologies on financial development in Nigeria. The study applied Auto-Regressive Distributed Lag (ADRL) estimation technique using quarterly data from 2009 to 2023 for the estimation. Findings indicate that, among the financial technology (fintech) variables, internet banking (IB) has a positive effect on financial development in the long run, but no significant effects in the short run. While, point of sales (POS) exerted a positive effect in the short run but has no significant effect in the long run. On the economic factors included as control variables, inflation rate (IFR) has negative effects on financial development in the short run and positive effects in the long run. Interest rate (INT) exerted negative effects on financial development the long run but no significant effect in the short run. Economic growth (RGDP) positively affects financial development only in the short run but negative effects in the long run. Consequent upon the findings, the study makes the following recommendation: (i). Internet banking should be highly promoted as increment in its usage improved financial development in Nigeria. (ii). Economic and financial policies should be fine-tuned in a way that as the economy grows it will stimulate financial development as against boosting financial development only in the short run but retarded it in the long run. (iii)The government should embark on more programmes and policies that will dampen lending interest as high rate of interest reduces financial development.

Keywords: Financial development, financial technologies, Auto-Regressive Distributed Lag.

INTRODUCTION

A well-developed financial sector plays critical roles in economic well-being and advancement of nations. The financial sector does these by mobilizing idle savings from surplus spending units and channeling it to deficit spending units for investment (Olulu-Briggs and Sunday-Goya, 2023; Albert et al., 2021; Umar, et al., 2021; Okunlola et al., 2020; McKinnon, 1973; Schumpeter, 1911; Bagehot, 1873). However, for a financial sector to play this important role expected of it, it must be well developed. In the pursuit of developing the financial sector, several factors such as economic growth, inflation, interest rate, institutional quality, government intervention, trade openness, culture, remittance and financial technology have been identified as drivers of financial development (Khan, Khan and Zuojun,, 2022; Akintola et al. 2020, Chowdhury, 2011). These determining factors have been investigated in several countries with varying degrees of results (Doucouliagos, De Haan & Sturm, 2022; Ajayi and Musyimi, 2022; Asratie 2021; Amissah and Świerczyńska, 2021; Muhammad and Ka’Oje, 2021; Takyi and Obeng, 2013)

In Nigeria, several initiatives, programs and reforms have been embarked upon over the years with the aim of developing the financial sector, but with limited success (Maduka & Onwuka, 2013; Imoagwu & Ezeanyeji, 2019). However, the most recent initiative in the Nigerian financial sector is the Financial Technology (fin-tech). Financial technology (fin-tech) is the application of technologies and innovative business models that are based on information and communications technology to provide financial services (Nicoletti, 2017). Although it is hoped that fin-tech would improve the performance of the Nigerian financial sector, most of the existing studies on the determinants of financial sector development in Nigeria often bypass the role of fin-tech (Fagbemi and Ajibike, 2018; Muhammad and Ka’oje, 2021; Ajayi and Musyimi, 2022). The study of Islam,Yusuf and Shuaibu (2022) though included fin-tech as an explanatory variable, but only focused on its effects on banks services delivery and not on financial sector development. This study seeks to fill this gap by investigating the effect of fin-tech on financial sector development in Nigeria.

LITERATURE REVIEW

2.1 Empirical Review

The determinants of financial development have been a long-standing area of research over the years, given the importance of financial development to economic growth and development. For instance, Muhammad and Kaoje (2021) examined the determinants of financial development in Nigeria over the period of 1981 to 2016. Autoregressive Distributive Lag (ARDL) model was employed to estimate the influences of institutions, inflation, interest rate, debt service, foreign direct investment, economic growth, quality of life, government expenditure, trade openness, and quality of human capital on financial development. The finding reveals that quality of life, foreign direct investment, and debt service had positive impact on financial development while inflation, economic growth, government expenditure, and trade openness have negative impact on financial development. More so, institution’s impacts were not significant.

Farouq, Sulong, Ahmad, Jakada, and Sambo (2020) focused on economic growth as well as the interacting role of foreign direct investment and economic growth on the Nigerian financial sector development. The study used data from the period 1970-2018, applying Gregory and Hansen (1996) co-integration, Non-linear ARDL as the elasticity estimator. The finding shows asymmetry in economic growth concerning financial development. Further findings indicate the existence of unidirectional non-linear causality between economic growth and financial development. The study also found a one-way causality between foreign direct investments running to financial development. The study, therefore, conclude that economic growth and foreign direct investment have an overall positive and significant effect on financial development.

Ajayi and Musyimi (2022) examined the impact of globalization on Nigerian financial development using foreign direct investment, trade openness, exchange rate, government expenditure, interest rate and inflation as control variables. Autoregressive distributed lag (ARDL) model was used for the study. The Findings show that foreign direct investment, trade openness and government expenditure have positive impact, while exchange rate, interest rate and inflation exert negative impacts on financial development.

Studies that investigated the impact of financial technology (fintech) on financial sector development in Nigeria include that of Islam, Ysuuf and Shuaibu (2022) which examined the impact of financial technology on financial service delivery of deposit money banks in Nigeria for the period of ten years from 2012 to 2021 using ex-post facto method descriptive statistics, correlation and regression analysis for the analysis. The study shows that mobile banking, internet banking and POS have impact on the financial service of deposit money banks in Nigeria.

Aduba, Asgari and Izawa (2023) studied fintech’s effects on financial development using data from emerging and developing economies. Three measures of financial development (broad money, Private credit, and bank deposits) and two conditional factors (financial performance and financial inclusion) were investigated vis-`a-vis Fintech penetration. Findings show that fintech penetration not only drives financial development but also strongly impacts the financial development of countries with weak financial performance and low financial inclusion. This indicates that countries with weak financial performance could leverage fintech to improve financial development.

Takyi and Obeng (2013) investigated the determinants of financial development in Ghana using ARDL approach with quarterly data from 1988 to 2010. The finding shows that trade openness and per capita income are important determinants of financial development in Ghana. Further, inflation, interest rate, and reserve requirement exerted negative effects on financial development both in the short-run and long-run suggesting that these variables adversely influence financial development in Ghana. However, government borrowing did not have any significant effect on financial development both in the long-run and short-run.

In a similar but slightly different dimension, study by Najimu (2019) examined the determinants of financial sector development in Ghana using data from 1976 to 2017 using the Ordinary Least Squares (OLS). The finding suggests that trade openness and economic growths are key determinants of financial development in Ghana and positively boost the level of the financial sector development.

Asratie (2021) examined the determinants of financial development in Ethiopia with annual data from 1980 to 2019 using ARDL estimation technique. Financial development was positively affected by political freedom index, economic growth and trade openness both in the short run and long run. While it is negatively affected by interest rate and reserve requirement. However, real exchange rate has negative effect in the long run and insignificant effect in the short run. On the other hand, financial development was positively affected by inflation, and political freedom, economic growth and trade openness. While it is negatively affected by external debt, reserve requirement and lending interest rate

Boopen, Kesseven Jashveer and Binesh (2011) investigated the determinants of financial development using data for the period 1970 to 2010 for Mauritius, by means of ARDL approach. The findings show that trade openness and financial liberalization are the important determinants of financial development. In addition, investment rate, income per capita and literacy rates were also important factors that stimulated financial development while inflation adversely influence financial development both in the short and long run.

Badeeb & Lean (2015) studied the main determinants of financial development in the Republic of Yemen. The finding indicates that economic growth and trade openness have a positive impact on the pace of financial development; the natural resource dependence has a negative impact.

Doucouliagos, Haan and Sturm (2021) meta-regression analysis of the literature on the drivers of financial development based on 1,900 estimates shows that institutional quality and domestic financial openness are positively correlated to financial development, while trade openness seems only important for stock market capitalization. Inflation has an adverse effect on financial development. Alshubiri, Jamil, and Elheddad (2019) investigated the impact of information and communication technology (ICT) on the financial development index of six Gulf Cooperation Council (GCC) countries from the period 2000 to 2016. The findings were presented in terms of two main ICT variables: fixed broadband and Internet users as a proxy of information and communication technology (ICT). Finding shows that ICT has positive effect on financial development. In terms of domestic credit as a percentage of the GDP proxy, the positive effects of ICT (broadband) are greater than the one from Internet users. A 1% increase in fixed broadband leads to approximately 2% increase in financial development, but the Internet user variable resulted in about a 0.09% increase.

2.2 Theoretical Framework

There are many theories that have been put forward to explain the determinants of financial sector development. These theories include the Technology Acceptance Model (TAM) advanced by Davis (1989) which explains the adoption behavior of clients and evaluation that are normally carried out to identify a system to be employed that will be useful to customers improves job performance and at the same time advance the system. The model postulates that the ease at which technology is used is applied to forecast its benefits to the industry (Gefen, Karahanna and Straub, 2003). The import of the model is that it provides an explanation that financial technology must gain acceptance through its usage then it will contribute significantly to development. This theory is the theoretical base of the study as it provides a link between technology application and system’s development. The other theories under pinning the study are Inflation and Finance Theory which was developed by Huybens and Smith (1999) states that high inflation levels suppress financial development. Its argument is that macroeconomic instability causes financial institutions to ration credit, reducing financial market activity and profitability and hence development (Rousseau and Wachtel, 2002).

Demand-Following (Growth-Led) Hypothesis which is an argument by Robinson (1979) that growing economic activity leads to greater demand for financial services by the real sector, enhancing the utilization of financial products and services.

Financial Liberalization Theory McKinnon (1973) and Shaw (1973) which states that both domestic savings and credit to the private sector increase if there is a moderately high and positive interest rate. Their argument is that financial repression results in market disequilibrium, consequently limiting allocative efficiency and retarding financial performance.

2.3 Conceptual Framework

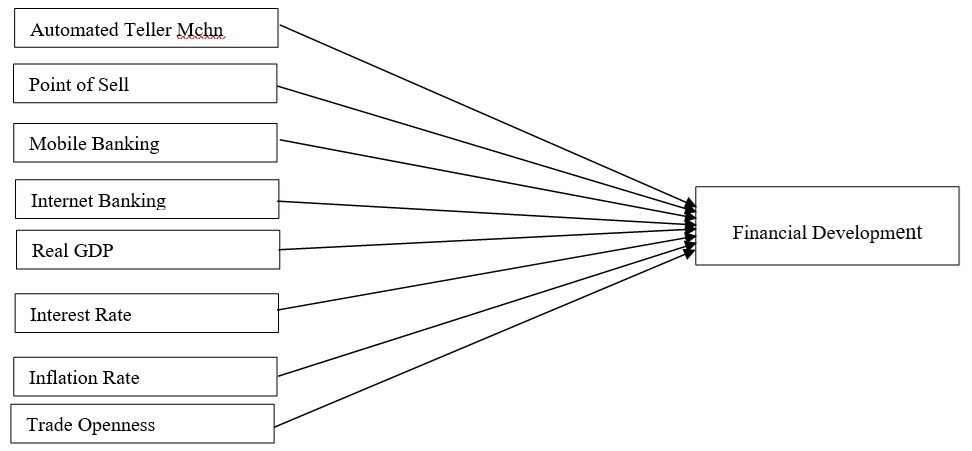

Figure 1 is the conceptual framework, with the financial development as the dependent variable, while automated teller machine, point of sell, mobile banking and internet banking as the explanatory variables of interest that were not previously studied. The other explanatory variables that were previously studied but used in this study as controls include the real GDP, interest rate, inflation rate and trade openness.

Figure 1: Conceptual framework

METHODOLOGY OF THE STUDY

3.1 Research Design

Descriptive design was employed for the study as it provides an authentic and correct representation of the study variables and brought out the state of affairs as they actually exist.

3.2 Sample and Sampling Design

The study uses secondary data. Quarterly data from the period 2009 to 2023 for the estimation were obtained from the Central Bank of Nigeria (CBN), National Bureau of Statistics (NBS), World Bank and International Monetary Fund (IMF) publications and websites. The data were on Automated Teller Machine (ATM) transactions value, Point of Sales (POS) transactions value, Mobile Banking (MB) transactions value, Internet Banking (IB) transactions value, Real Gross Domestic Product Growth rate (RGDP), Interest Rate (INT), Inflation Rate (IFR) and Trade Openness (TOP) as determinants of Financial Development (FINDEV) based on the literatures.

3.3 Procedure for Data Analysis

The study used Auto-regressive distributed lag estimation technique with. Several diagnostic tests for normality, stationarity, multicollinearity, homogeneity and autocorrelations were carried out on the series data to ascertain the variability of the model. To investigate the effects of financial technology on financial development in Nigeria, the study adapted specification by Chinn and Ito (2002) empirical model with incorporation of fintech variables. Generally, a mathematical relationship for the study is expressed as:

FINDEV= f (ATM, POS, MB, IB, RGDP, ITR, IFR, TOP) …………….. ……………. (1)

Where:

FINDEV = Financial development measured as financial intermediaries’ credits to the private sector divided by Gross Domestic Product.

ATM = Automated Teller Machine (ATM) measured as log of the transactions value

POS = Point of Sales (POS) measured as log of the transactions value via it.

MB = Mobile banking measured as log of the transactions value via it.

IB = Internet banking measured as log of the transactions value via it.

RGDP = Real gross domestic product growth rate was measured as percentage changes in

inflation adjusted gross domestic product.

INT = Interest rate

IFR = Inflation rate measured as the percent change in Consumer Price Index (CPI).

TOP = Trade openness measured as the total of export and import divided by the Gross Domestic

Product.

The economic model equation (1) is then remodel to an econometric model as:

\[

\text{FINDEV}_t = \beta_0 + \beta_1 \text{ATM}_{t-1} + \beta_2 \text{POS}_{t-1} + \beta_3 \text{MB}_{t-1} + \beta_4 \text{IB}_{t-1} + \beta_5 \text{RGDP}_{t-1} + \beta_6 \text{INT}_{t-1} + \beta_7 \text{IFR}_{t-1} + \beta_8 \text{TOP}_{t-1} + \mu_t \quad \text{(2)}

\]

With a priori expectations as:

\[

\beta_1 > 0, \, \beta_2 > 0, \, \beta_3 > 0, \, \beta_4 > 0, \, \beta_5 > 0, \, \beta_6 > 0, \, \beta_7 > 0, \, \beta_8 > 0

\]

Equation (2) is then remodeled in a conditional ARDL as:

\[

\Delta \text{FINDEV}_t = \alpha_0 + \beta_1 \text{FINDEV}_{t-1} + \beta_2 \text{ATM}_{t-1} + \beta_3 \text{POS}_{t-1} + \beta_4 \text{MB}_{t-1} + \beta_5 \text{IB}_{t-1} + \beta_6 \text{RGDP}_{t-1} + \beta_7 \text{INT}_{t-1} + \beta_8 \text{IFR}_{t-1} + \beta_9 \text{TOP}_{t-1} + \sum_{i=1}^{p} \phi_{1i} \Delta \text{FINDEV}_{t-i} + \sum_{i=1}^{p} \phi_{2i} \Delta \text{ATM}_{t-i} + \sum_{i=1}^{p} \phi_{3i} \Delta \text{POS}_{t-i} + \sum_{i=1}^{p} \phi_{4i} \Delta \text{MB}_{t-i} + \sum_{i=1}^{p} \phi_{5i} \Delta \text{IB}_{t-i} + \sum_{i=1}^{p} \phi_{6i} \Delta \text{RGDP}_{t-i} + \sum_{i=1}^{p} \phi_{7i} \Delta \text{INT}_{t-i} + \sum_{i=1}^{p} \phi_{8i} \Delta \text{IFR}_{t-i} + \sum_{i=1}^{p} \phi_{9i} \Delta \text{TOP}_{t-i} + \mu_t

\]

The null hypothesis is tested against the alternative hypothesis:

\[

H_0: \beta_1 = \beta_2 = \beta_3 = \beta_4 = \beta_5 = \beta_6 = \beta_7 = \beta_8 = \beta_9 = 0

\]

\[

H_0: \beta_1 \neq \beta_2 \neq \beta_3 \neq \beta_4 \neq \beta_5 \neq \beta_6 \neq \beta_7 \neq \beta_8 \neq \beta_9 \neq 0

\]

When cointegration is established then the next step is to estimate the following ARDL (p, q1, q2, q3, q4, q5, q6, q7, q8) model to obtain the long run coefficients:

\[

\text{FINDEV}_t = \alpha_0 + \sum_{i=1}^{p} \beta_1 \text{FINDEV}_{t-1} + \sum_{i=0}^{q_1} \beta_2 \text{ATM}_{t-1} + \sum_{i=0}^{q_2} \beta_3 \text{POS}_{t-1} + \sum_{i=0}^{q_3} \beta_4 \text{MB}_{t-1} + \sum_{i=0}^{q_4} \beta_5 \text{IB}_{t-1} + \sum_{i=0}^{q_5} \beta_6 \text{RGDP}_{t-1} + \sum_{i=0}^{q_6} \beta_7 \text{INT}_{t-1} + \sum_{i=0}^{q_7} \beta_8 \text{IFR}_{t-1} + \sum_{i=0}^{q_8} \beta_9 \text{TOP}_{t-1} + \nu_t

\]

The estimation of the long-run parameters is followed by the estimation of the short-run parameters of the variables with an error correction model of the ARDL and the determination of the speed of adjustment to equilibrium. With the establishment of a long-run relationship among the variables, the unrestricted ARDL error correction is estimated as:

\[

\text{FINDEV}_t = \alpha_0 + \sum_{i=1}^{p} \phi_{1i} \Delta \text{FINDEV}_{t-i} + \sum_{i=1}^{q_1} \phi_{2i} \Delta \text{ATM}_{t-i} + \sum_{i=1}^{q_2} \phi_{3i} \Delta \text{POS}_{t-i} + \sum_{i=1}^{q_3} \phi_{4i} \Delta \text{MB}_{t-i} + \sum_{i=1}^{q_4} \phi_{5i} \Delta \text{IB}_{t-i} + \sum_{i=1}^{q_5} \phi_{6i} \Delta \text{RGDP}_{t-i} + \sum_{i=1}^{q_6} \phi_{7i} \Delta \text{INT}_{t-i} + \sum_{i=1}^{q_7} \phi_{8i} \Delta \text{IFR}_{t-i} + \sum_{i=1}^{q_8} \phi_{9i} \Delta \text{TOP}_{t-i} + \lambda \text{ECT}_{t-1} + \nu_t

\]

Where \(\lambda\) is the speed of adjustment to long-run equilibrium following a shock and \(\text{ECT}_{t-1}\) is the error-correction term, the residuals from the cointegration equation lagged one (1) period is expressed as:

\[

\text{ECT}_t = \text{FINDEV} – \alpha_0 + \sum_{i=1}^{p} \phi_{1i} \Delta \text{FINDEV}_{t-1} + \sum_{i=1}^{q_1} \phi_{2i} \Delta \text{ATM}_{t-i} + \sum_{i=1}^{q_2} \phi_{3i} \Delta \text{POS}_{t-i} + \sum_{i=1}^{q_3} \phi_{4i} \Delta \text{MB}_{t-i} + \sum_{i=1}^{q_4} \phi_{5i} \Delta \text{IB}_{t-i} + \sum_{i=1}^{q_5} \phi_{6i} \Delta \text{RGDP}_{t-i} + \sum_{i=1}^{q_6} \phi_{7i} \Delta \text{INT}_{t-i} + \sum_{i=1}^{q_7} \phi_{8i} \Delta \text{IFR}_{t-i} + \sum_{i=1}^{q_8} \phi_{9i} \Delta \text{TOP}_{t-i}

\]

RESULTS PRESENTATIONS AND DISCUSSION OF FINDINGS

4.1 Result Presentations

Table 1: Result of ADF Unit Root Test

| LEVEL | 1ST DIFF | Order of stationarity | |||

| Variables | Constant | Constant with trend | Constant | Constant with trend | |

| FINDEV | 0.8086 | 0.0101 | I (0) | ||

| ATM | 0.1689 | 0.5412 | 0.0000 | 0.0000 | I (1) |

| POS | 0.1856 | 0.6297 | 0.0000 | 0.0000 | I (1) |

| MB | 0.1466 | 0.5010 | 0.0096 | 0.0176 | I (1) |

| IB | 0.2413 | 0.7727 | 0.0000 | 0.0000 | I (1) |

| IFR | 0.6203 | 0.6459 | 0.0000 | 0.0000 | I (1) |

| INT | 0.5542 | 0.5905 | 0.0000 | 0.0000 | I (1) |

| RGDP | 0.9173 | 90.6036 | 0.0011 | 0.0000 | I (1) |

| TOP | 0.0014 | 0.0203 | I (0) | ||

Source: Author’s computation using E-view.

In summary the results of the ADF unit root test in Table 1 reveal that the variables were either I(0) or I(1). Thus, since the variables are shown to be non-stationary and also their order of integration mixed, we can

proceed to test for co integration.

Table 2: Bounds Test for Co-Integration

| F-Bounds Test | Null Hypothesis: No levels relationship | |||

| Test Statistic | Value | Signif. | I(0) | I(1) |

| Asymptotic: n=1000 | ||||

| F-statistic | 4.318003 | 10% | 1.85 | 2.85 |

| K | 8 | 5% | 2.11 | 3.15 |

| 2.5% | 2.33 | 3.42 | ||

| 1% | 2.62 | 3.77 | ||

Source: Authors’ computation using E-view.

As shown in Table 2, the joint null hypothesis of lagged level variables (that is, variable addition test) of the coefficients being zero (no co integration) is rejected at 5 percent significance level. This is because the calculated F-statistic value of 4.318 exceeds the upper bound critical value of 3.15 at 95% level. This means there exist a long run relationship between financial development and its determinants.

Table 3: Result of Long Run Relationship

| ARDL(2, 2, 0, 2, 1, 2, 0, 2) | Dependent variable: Findev | |||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | -56.05955 | 22.72841 | -2.466497 | 0.0196 |

| ATM | -0.080764 | 0.110225 | -0.732722 | 0.4694 |

| IB | 0.081319 | 0.020229 | 4.019933 | 0.0004 |

| MB | -0.026119 | 0.059180 | -0.441341 | 0.6621 |

| POS | -0.002896 | 0.080971 | -0.035765 | 0.9717 |

| IFR | 61.61345 | 20.68611 | 2.978493 | 0.0057 |

| INT | -2.012357 | 0.563776 | -3.569425 | 0.0012 |

| TOP | 100.8178 | 1254.364 | 0.080374 | 0.9364 |

| RGDP | -54.04296 | 18.22091 | -2.965987 | 0.0059 |

Source: Author’s computation using E-view.

The results as presented in Table 3 indicate that the fintech variables; automated teller machines (ATM), mobile banking (MB), and point of sale (POS), reveals coefficients extremely close to zero. Additionally, their associated t-statistics and probabilities indicate that these variables except internet banking (IB), do not have a statistically significant impact on financial development in the long run. This implies that the widespread adoption or usage of these banking technologies may not directly contribute to overall financial development.

Similarly, the economic variables; inflation rate (IFR), interest rate (INT), and economic growth (RGDP) except trade openness (TOP) demonstrate statistically significant t-statistics and probabilities, suggesting that changes in these economic indicators significantly influence financial development over the long run.

Overall, the results of the ARDL (2, 2, 0, 2, 1, 2, 0, 2) model indicate no significant long-run relationships between most of the examined variables and financial development in Nigeria.

Table 4: Results of Short run Relationship

| ARDL(2, 2, 0, 2, 1, 2, 0, 2) | Dependent variable: Findev | |||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| D(FINDEV(-1)) | -0.293665 | 0.083156 | -3.531486 | 0.0012 |

| D(ATM) | 0.059988 | 0.034758 | 1.725865 | 0.0947 |

| D(POS) | 9.53E-17 | 1.56E-17 | 6.094871 | 0.0000 |

| D(MB) | -0.058408 | 0.034556 | -1.690254 | 0.1013 |

| D(IB) | 0.003221 | 0.006516 | 0.494298 | 0.6247 |

| D(IFR) | -9.917243 | 0.452288 | -21.92682 | 0.0000 |

| D(INT) | -0.177949 | 0.190958 | -0.931872 | 0.3588 |

| D(RGDP) | 8.710995 | 0.404683 | 21.52547 | 0.0000 |

| D(TOP) | -9.814096 | 0.456179 | -21.51369 | 0.0000 |

| CointEq(-1)* | -0.440703 | 0.058821 | -7.492265 | 0.0000 |

| R-squared | 0.963919 | Durbin-Watson stat | 2.255876 | |

| Adjusted R-squared | 0.948191 | |||

Source: Author’s computation using E-view.

The results of the short run relationship as presented in Table 4 indicate that the lagged change in financial development (D (FINDEV (-1)), has a negative effect on financial development. Automated teller machine (D (ATM)) usage positively affects financial development. Mobile banking usage (D (MB)) usage does not significantly affect financial development. Point of sale (POS) usage positively affects financial development. Furthermore, Inflation rate (IFR) and trade openness (TOP) have negative effects on financial development.

The coefficient for the error correction term (CointEq(-1) is negative and statistically significant, suggesting an adjustment towards the long-run equilibrium in the short term. This indicates that deviations from the long-run relationship between the variables are corrected in the short run, contributing to the stability of the financial system.

The R-squared value of 0.963919 indicates a better fit of the model, with more of the variability in the dependent variable being accounted for by the independent variables. The Durbin-Watson statistic value of 2.255876, suggests that there is no significant autocorrelation present in the residuals of the model. A value between 1.5 and 2.5 generally indicates that the assumption of no autocorrelation is reasonable.

Table 5: Post Estimation Test

| Breusch-Godfrey Serial Correlation LM Test: | |||

| F-statistic | 0.903420 | Prob. F(2,28) | 0.4167 |

| Obs*R-squared | 3.455244 | Prob. Chi-Square(2) | 0.1777 |

| Heteroskedasticity Test: Breusch-Pagan-Godfrey | |||

| F-statistic | 1.569383 | Prob. F(26,30) | 0.1172 |

| Obs*R-squared | 32.84881 | Prob. Chi-Square(26) | 0.1665 |

| Scaled explained SS | 24.74307 | Prob. Chi-Square(26) | 0.5336 |

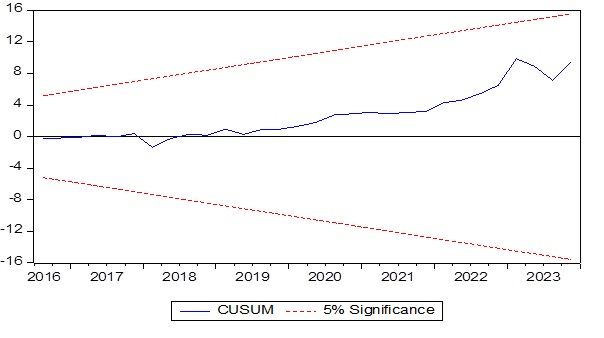

The diagnostic post estimation test shows that the model passes both serial correlation test and heteroskedasticity test as indicated by the probability values. However, the CUSUM test for stability shows that the model is stable since it falls within the boundary of stability at 5% level of significant.

Based on the results of the short run and long run as presented in Tables 3 and 4, among the financial technology (fintech) variables, internet banking (IB) has a positive effect (a unit increase in IB enhanced financial development by 0.8%) in the long run, but no significant effects in the short run. Point of sales (POS) has a positive effect in the short run but no significant effect in the long run. On the economic factors included as control variables in the model, inflation rate (IFR) has negative effects on financial development in the short run and positive effects in the long run. Interest rate (INT) has no significant effect in the short run but exerts negative effects on financial development in the long run (a unit increase in INT reduced financial development by 2%). Economic growth (RGDP) positively affects financial development only in the short run but negative effects in the long run.

4.2 Discussion of Findings

The study’s finding of internet banking (IB) positive effect on financial development in the long run in Nigeria is in line with Technology Acceptance Model and the expectation of the study. It is consistent with Aduba, Asageri and Izawa (2023)’s finding that internet banking improved financial development in emerging and developing economies. The finding that inflation rate (IFR) has negative effects on financial development in the short run is in line with the inflation and finance theory which states that high inflation levels suppress financial development, and it is consistent with the findings of Muhammmad and Ka’Oje (2021); Ajayi and Musyimi (2022); Takyi and Obeng (2013); Boopen, et al. (2011); and Badeeb and Lean (2015). However, in the long run it turned positive suggesting that the financial institutions factored in the cost of inflation and even used moving interest rate into their lending policy in the long run. The finding that economic growth (RGDP) has positive effect on financial development in the short run corroborates the findings of Farouq, et al. (2020); (Najimu (2019); Asratie (2021); Boopen, et al. (2011); and Badeeb and Lean (2015). However, it turned to negative effects in the long run corroborating Muhammmad and Ka’Oje (2021)s finding, Meaning that in the long run, there were challenges on the roles of real economic growth rate on financial development in Nigeria that rather than RGDP enhancing financial development, it retard financial development . The study’s finding that interest rate (INT) exerts negative effects on financial development both in the long run is consistent with theory and corroborates Ajayi and Musyimi (2022); Takyi and Obeng (2013); and Asratie (2021).

CONCLUSION AND RECOMMENDATIONS

5.1 Conclusion

A well-developed financial sector plays critical roles in economic well-being and advancement of nations as such there is need to know the factors that determine financial sector development in a country. However, none of the existing studies on the determinants of financial development has considered the effect of financial technologies (fintech) on financial development in Nigeria. Hence this study was carried out to investigate the effects of financial technologies on financial development in Nigeria. The study applied Auto-regressive distributed (ADRL) lag estimation technique using quarterly data from the period 2009 to 2023 for the estimation. Findings shows that, among the financial technology (fintech) variables, internet banking (IB) has a positive effect on financial development in the long run, but no significant effects in the short run. While, the point of sales (POS) exerted a positive effect in the short run but has no significant effect in the long run. On the economic factors included as control variables, inflation rate (IFR) has negative effects on financial development in the short run and positive effects in the long run. Interest rate (INT) exerted negative effects on financial development both in the short run and the long run. Economic growth (RGDP) positively affects financial development only in the short run but negative effects in the long run.

5.2 Recommendations

Consequent upon the findings from the investigation, the study provides the following recommendation:

- Internet banking should be highly promoted as increment in its usage improved financial development in Nigeria.

- Economic and financial policies should be fine tuned in a way that it will make economic growth to stimulate financial development as against what it is currently enhancing financial development only in the short run but retarding it in the long run.

- The government should embark on more programmes and policies that will dampen lending interest as high rate of interest reduces financial development.

REFERENCE

- Aduba, J. J., Asgari, B. & Izawa, H. (2023). Does FinTech penetration drive financial development? Evidence from panel analysis of emerging and developing economies Borsa Istanbul Review 23-5 (2023) 1078–1097 http://www.elsevier.com/journals/borsa-istanbul-review/2214-8450

- Ajayi, J. A. & Musyimi, K.S. (2022). Impact of globalization on financial development in Nigeria, Financial Law Review, 25 (1) (2022), 158-178.

- Akintola, A.A., Oji-Okoro, I., & Itodo, I.A. (2020). Financial sector development and economic growth in Nigeeia: An empirical re-examination. Central Bank of Nigeria Economic and Financial Review, 58(3), 59-84.

- Albert, S. M., Samson, A. A., Gbeminiyi, A. T., & Sennuga, S. O. (2021). Financial development and economic growth in Nigeria: The case study of Nigeria. GPH-International Journal of Business Management, 4(04), 21-39.

- Alshubiri, F., Jamil, S. A., & Elheddad, M. (2019). The impact of ICT on financial development: Empirical evidence from the Gulf Cooperation Council countries, International Journal of Engineering Business Management, 11(2019), 184797901987067. https://doi.org/ 10.1177/1847979019870670

- Amissah, E. and Świerczyńska, K. 2021 Is religion a determinant of financial development? Int Adv Econ Res https://doi.org/10.1007/s11294-021-09835-2

- Asratie, T. M. (2021). Determinants of financial development in Ethiopia: ARDL approach. Cogent Economics & Finance, 9(1), 1-15. DOI: 10.1080/23322039.2021.1963063

- Badeeb, R. & Lean, H. H. (2017). The determinants of financial development in the Republic of Yemen: Evidence from the principal components approach, Capital Markets Review, 25 (2) 32-48.

- Bagehot, W. (1873). Lombard Street: A description of the money market. Pages 48-233 in St. John-Stevas (1978), Vol. IX.

- Boopen, S., Kesseven, P., Jashveer, H, & Binesh, S. (2011). Determinants of financial development: The case of Mauritius, Finance and Corporate Governance Conference 28 – 29, April 2011 , Melbourne,RACV Club, Australia.

- Chinn, M.D., and Ito, H. (2000). What matters for financial development? Capital controls, institutions and interactions”, Journal of Development Economics, 81(1), pp. 163-192

- Chowdhury, M.B. (2011). Remittances flow and financial development in Bangladesh. EconomicModelling, 28(6), pp. 2600-2608.

- David, F.D (1989). Perceived usefulness, perceived case of use, and user acceptance of information technology, MS Quarterly 13(3) 319 – 339

- Doucouliagos, C., De Haan, J., & Sturm, J. E. (2022). What drives financial development? A Metaregressionanalysis. Oxford Economic Papers, 74(3), 840-868. https://doi.org/10.1093/oep/gpab044

- Fagbemi, F., & Ajibike, J. O. (2018). Institutional quality and financial sector development: Empirical evidence from Nigeria, American Journal of Business and Management, 7(1), 1-13.

- Farouq, I. S., Sulong, Z., Ahmad, A. U., Jakada, A. H., & Sambo, N. U. (2020). The effects of economic growth on financial development in Nigeria: Interacting role of foreign direct investment: An application of NARDL. Volume 9, issue 03, pp 6321- 6328

- Gregory, A. & Hansen, B. (1996). Residual-based tests for co integration in models with regime shifts. Journal of Econometrics 10: 321 – 335.

- Gefen, D., Karahanna, E., & Sraub, D. W. (2003). Trust and TAM in an online shopping: An integrated model. MIS Quarterly, 27(1), 51-90.

- Hicks, J. (1969). A Theory of Economic History. Oxford; Clarendon Press.

- Huybens, E. & Smith, B. (1999). Inflation, financial markets, and long-run real activity, Journal of Monetary Economics, 43: 283–315.

- Imoagwu, C. P., & Ezeanyeji, C. I. (2019). Financial development and economic growth nexus in Nigeria. International Journal of Business and Management Invention, 8(3), 50-63.

- Islam, M.S.N.; Ysuuf, A.A. and Shuaibu, H. (2022). The impact of financial technology (fintech) on financial service delivery of deposit money banks in Nigeria, Sapientia Foundation Journal of Education, Sciences and Gender Studies (SFJESGS) 4(2). 83 – 93 ISSN: 2734-2522 (Print); ISSN: 2734-2514 (Online).

- Khan, H., Khan, S., & Zuojun, F. (2022). Institutional quality and financial development: Evidence from developing and emerging economies. Global Business Review, 23(4), 971-983.

- Maduka, A. C., & Onwuka, K. O. (2013). Financial market structure and economic growth: Evidence from Nigeria data. Asian economic and financial review, 3(1), 75-98.

- McKinnon, R. (1973). Money and capital in economic development, Brookings Institution Press.

- Muhammad, S. and Ka’oje, M.R. (2021). Determinants of financial development in Nigeria: a bound testing approach, Contemporary Journal of Finance and Risk Management Vol. 1, No.3 , P1

- Najimu, A. (2019). Determinants of financial sector development in Ghana, The international journal of innovative research and development 8(10)

- Nicoletti, B. (2017). The future of fintech. In B. Nicoletti, integrating finance and technology in financial services (pp. 2, 3). Palgrave Macmillan, [2017].

- Olulu-Briggs and Sunday-Goya (2023). Financial sector development and economic growth in Nigeria, South Asian Research Journal of Business and Management 5(4).

- Robinson J., (1979). The Generalization of the General Theory and Other Essays. London, Macmillan.

- Rousseau, P. L., and P. Wachte l. (2002). Inflation thresholds and the finance-growth nexus. Journal of International Money and Finance 21: 777–793.

- Schumpeter, J.A. (1911). The theory of economic development, Harvard University Press, Cambridge, MA

- Shaw, E.S. (1973). Financial deepening in economic development, Oxford Univ. Press, New York

- Schueffel, P. (2016). Taming the beast: A scientific definition of fintech, Journal of Innovation Management, 4(4): 32-54.

- Takyi, P.O. and Obeng, C.K. (2013). Determinants of financial development in Ghana, International Journal of Development and Sustainability, Vol. 2 No. 4, pp. 2324-2336

- Umar, N., Sambo, I., Ahmad, A. U., & Hassan, A. (2021). Financial development and economic growth in Nigeria: New evidence from a threshold autoregressive and asymmetric analysis. International Journal of Business, 8(3), 207-218.