Fragmenting World Geo-Economic Order: Making Sense of the Escalating United States-China Economic Tension

- Olusegun Obasun

- 2783-2808

- Aug 19, 2024

- Economics

Fragmenting World Geo-Economic Order: Making Sense of the Escalating United States-China Economic Tension

Olusegun Obasun

Smart Access Holdings Limited, Abuja, FCT, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.807216

Received: 05 July 2024; Accepted: 13 July 2024; Published: 19 August 2024

ABSTRACT

The unipolar dominance of the US after the Cold War era is fading as China’s economic and military rise reshapes the global order. This complex rivalry extends beyond economics, encompassing technological competition, with both countries vying for leadership in artificial intelligence, quantum computing, and 5G technology. Geopolitical tensions fueled by issues like Taiwan and the South China Sea further strain the relationship. The ongoing trade disputes and potential decoupling of economies could harm global growth and prosperity, increase the risk of military conflict, and fragment the global order.

This paper analyzes the economic, technological, and geopolitical factors driving the US-China trade war, drawing on hegemonic stability and power transition theories, It critiques competing narratives surrounding the conflict and explores potential solutions for managing tensions. A central question is whether “rules of the road” can be established to govern economic and technological competition in a multipolar world, fostering stability and cooperation amidst rivalry.

Keywords: Trade war, sanctions, forced technology transfer, industrial overcapacity, trade imbalance

INTRODUCTION

For over three decades since the collapse of the Soviet Union, the United States enjoyed a period of unipolar dominance in economy, military, and, to a certain extent, politics, with the US shaping the global order post-Cold War. However, China’s economic rise, particularly its manufacturing prowess and status as the world’s largest economy by PPP (purchasing power parity), has challenged this unipolarity. The relationship between the US and China is complex and multifaceted. It is not just economic; it encompasses technological competition, with both countries vying for leadership in areas like artificial intelligence, quantum computing, and 5G technology, military modernization as China’s rapid military modernization is seen by the US as a threat to its regional and global dominance and geopolitical competition manifesting in the disagreements over Taiwan, the South China Sea, and human rights creating further friction.

Today, the relationship between the governments of these leading world economic superpowers, the United States and China, appears to be suffused with rhetorics, threats, and tit-for-tat sanctions, fast changing the world economic order and fragmenting international trade and relations. US Treasury Secretary Janet Yellen was in China in April 2024 and, at the press conference capping off her five-day visit, told Chinese officials that the country’s export-driven economic model is again creating imbalances that threaten the global economy. She lambasted China for promoting industrial overcapacity, threatening the United States’ turbocharged, state-incentivized industrial revival (Johnson, 2024). Secretary Yellen also scolded China for its relationship with Russia and threatened that the United States would sanction Chinese banks, companies, and individuals facilitating transactions to channel military or dual-use goods to Russia. However, US Senator Rand Paul, in an op-ed published by Federal Times on 17 April 2024, questioned the audacity of US Treasury Secretary Janet Yellen to tell foreign country ‘how it should run its economy, what sectors the government may subsidize, what countries it can conduct business with, and then threaten economic retaliation if it does not comply” (Paul,2024). He asserted that the US government would not tolerate such behavior from other countries, which could damage US-China relations.

The White House Fact Sheet of 14 May 2024 with the header “President Biden Takes Action to Protect American Workers and Businesses from China’s Unfair Trade Practices” re-emphasized that the unfair trade practices of China are threatening American businesses and workers regarding technology transfer, intellectual property, and innovation further stating that China continues to flood global markets with artificially low-priced exports practices contributing to China’s growing overcapacity and export surges. According to the release, the Biden administration claimed that the Chinese government, for far too long, has used unfair non-market practices, forced technology transfers, and intellectual property theft, which have significantly enabled its control of “70, 80, and even 90 percent of global production for the critical inputs necessary for our technologies, infrastructure, energy, and health care—creating unacceptable risks to America’s supply chains and economic security” (The White House, 2024). The Biden government announced that to counteract the resulting harms to American workers and businesses, it had invoked Section 301 of the Trade Act of 1974 to increase tariffs on $ 18 billion of imports from China.

On 15 May 2024, the Biden administration announced the rollout of fresh tariffs on a range of Chinese imports.

| Product | Tariff Rate | Previous Rate | Effective Date |

| Syringes and needles | 50 | 0 | 2024 |

| Steel and aluminum | 25 | 0-7.5 | 2024 |

| Solar cells | 50 | 25 | 2024 |

| Ship-to-shore-cranes | 25 | 0 | 2024 |

| Semiconductors | 50 | 25 | 2025 |

| Rubber medical and surgical gloves | 25 | 7.5 | 2026 |

| Personal protective equipment | 25 | 0-7.5 | 2024 |

| Natural graphite and permanent magnets | 25 | 0 | 2026 |

| Lithium-ion non electric-vehicle batteries | 25 | 7.5 | 2026 |

| Lithium-ion electric-vehicle batteries | 25 | 7.5 | 2024 |

| Electric vehicles | 100% | 25% | 2024 |

| Critical minerals | 25 | 0 | 2024 |

| Battery parts | 25 | 7.5 | 2024 |

Source: The White House

It tripled tariffs on aluminum and steel to 25%, doubled them on semiconductors by 2025, quadrupled the tariff on electric vehicles to 100%, and doubled the rate on solar cells. The tariff measure appeared designed to protect sectors the Biden administration has invested in to bolster production, such as electric vehicles, clean energy, and semiconductors. The administration raised concern that China’s control of the production of critical inputs in sectors including energy, technology, and healthcare has led to a surge in exports that threatens American businesses and workers (Kapadia, 2024). The White House release also announced that the administration has invested $ 860 billion in industries of the future like electric vehicles (EVs), clean energy, and semiconductors, which, aided by the Infrastructure Law, Chips and Science Act, and Inflation Reduction Act has created nearly 800,000 jobs in manufacturing and clean energy, and doubled construction of new factory and thus brought the trade deficit with China to the lowest in a decade.

Drawing on hegemonic stability theory and power transition theory, this paper investigates the multifaceted nature of the escalating tensions between the US and China, analyzing the economic, technological, and geopolitical factors contributing to the trade war and its implications for the existing international order. Attempts will be made to explore the competing US narrative of China’s unfair trade practices, including technology transfer demands, intellectual property theft, and state-subsidized exports which threaten US economic interests, and the alternative narrative that the US, facing China’s rise and fearing a multipolar world, uses trade sanctions to contain China’s growth.

METHODOLOGY

Data are sourced from official documents -Policy documents, press releases, and statements from the White House, including the May 15, 2024 announcement of US tariffs, US Department of Commerce, US Trade Representative, and their Chinese counterparts will be analyzed. Another data source is from academic journals, particularly peer-reviewed articles on international relations, economics, and political science, that address the US-China trade tensions, technology transfer, intellectual property rights, and the emergence of a multipolar world order. Also, news articles utilizing credible news sources from both the US and China to gain insights into the trade war narratives and expert opinions and books by scholars on international trade, China’s economic development, US foreign policy towards China, and the future of the global order are consulted.

By employing a multi-method approach and considering different perspectives, this paper will contribute to a comprehensive understanding of the escalating US-China tensions, their root causes, and their potential impact on the future of the global order. The data analysis will include thematic analysis to identify key themes and arguments from official documents, academic articles, and news reports regarding the causes and consequences of the US-China tensions, comparative analysis to compare and contrast the US and China’s perspectives on trade practices, intellectual property, and geopolitical competition and case studies to analyze specific examples of US tariffs and Chinese industrial policies to understand their impact on specific industries and the broader trade relationship.

A Clash of Titans Through the Lens of Hegemonic Stability and Power Transition Theories

The escalating trade war between the United States and China represents a significant shift in the global order. This essay analyzes the economic, technological, and geopolitical factors driving this conflict, drawing upon hegemonic stability theory (HST) and power transition theory (PTT) frameworks.

Hegemonic Stability Theory and the Eroding Unipolar Order:

HST, as articulated by scholars like Kindleberger (1973 and Krasner (1976), posits that a dominant power (hegemon) fosters a stable international economic order by providing public goods like open markets and rule-making frameworks. Charles Kindleberger focused on the hegemon’s provision of public goods, the ultimate of which is international economic stability and altruistic leadership since it benefits all countries. These public goods make up the infrastructure of the international economy. The hegemon lets its “currency to become the principal reserve asset, providing sufficient liquidity for the growth of international trade, financing the expansion of trade and long-term economic development, and ensuring freedom of transit” (Campbell, 2009; p. 71).Following World War II, the US assumed this hegemonic role, crafting the post-war international economic architecture (e.g., the Bretton Woods system, General Agreement on Tariffs and Trade (GATT)). However, China’s economic rise challenges this established order. Krasner (1976) contends that hegemonic power’s primary policy goal is free trade because it has a solid technological lead, which enables the hegemon to realize a considerable proportion of the gains from free trade.

To equate the realities of today and the concepts espoused by Charles Kindleberger, Robert Gilpin, Immanuel Wallerstein, and other researchers, Khojayan, K. (2022), focusing on the concept of hegemonic stability, argued that the existence of hegemon, especially in the political and economic system is a necessary condition for maintaining global peace and stability. Campbell (2009), however, expressed a different opinion, pointing to observed weaknesses that limited the explanatory power of hegemonic stability theory and concluded that hegemonic power’s presence is not a necessity to establish a liberal economic regime and significantly “a hegemonic power’s economic policies do not always benefit members of the international system” [69].

Power Transition Theory and the Thucydides Trap:

Power Transition Theory (PTT) posits that these transitions are inherently conflictual, potentially leading to war – a notion captured by the evocative term “Thucydides’s Trap.” PTT draws from the realist tradition in international relations, emphasizing the centrality of power and national security concerns. Mearsheimer (2001) argues that states prioritize survival and act rationally to maximize their power. A security dilemma emerges when a rising power’s capabilities approach or surpass those of the established power. The established power perceives this rise as a threat, leading to preemptive measures or attempts to contain the rising power. The rising power, misinterpreting these actions as attempts to stifle its legitimate aspirations, responds assertively, potentially escalating tensions.

This theoretical framework finds historical support in Thucydides’ account of the Peloponnesian War between Athens, the established power, and Sparta, the rising challenger. Thucydides famously attributed the war not to specific events or personalities but to the “growth of Athenian power and the fear which this caused in Sparta” (Thucydides, 431 BCE). The analogy suggests that power imbalances alone can trigger conflict without immediate territorial or ideological disputes. However, PTT’s explanatory power has been challenged on several fronts. Critics argue that the theory is overly deterministic, neglecting the role of factors such as alliances, leadership decisions, and domestic politics. Additionally, historical examples do not always support the inevitability of war. For instance, the power transition between the United States and Great Britain in the 20th century was relatively peaceful. This suggests cooperation and accommodation are also possible outcomes of power transitions (Schweller, 2004).

The tension between the United States and China could be viewed from the perspective of relationship between an hegemon and a rising power and the strategic interactions between them during the power transition process. Zhou (2019) employed prospect theory, power transition theory, and nuclear deterrence theory to construct a theory of strategic competition that maintains that states take diplomatic actions to seek gains and avoid losses. The theory of strategic competition proposes that an hegemon will take action to avoid incurring losses before the rising power overtakes it. In response, the rising power will passively act to avoid losses.

China’s rapid economic growth and modernization threaten US dominance, potentially escalating tensions. Economic grievances on both sides fuel the trade war. The US accuses China of unfair trade practices, including intellectual property theft, currency manipulation, and industrial subsidies. China, in turn, resents the US trade deficit and its protectionist measures. These issues reflect a broader competition for global economic influence. The rivalry extends beyond traditional trade to the high-tech arena. Both countries vied for leadership in artificial intelligence, quantum computing, and 5G technology. This technological competition is intertwined with economic and national security concerns. The US fears China’s technological advancements could threaten its economic competitiveness and military edge. Geopolitical tensions add another layer of complexity. The US views China’s growing assertiveness in the South China Sea and its relationship with Taiwan as challenges to its regional hegemony. Additionally, China’s Belt and Road Initiative (BRI) is seen as an attempt to establish a China-centric global order.

Navigating this complex conflict requires acknowledging both theories. HST highlights the potential benefits of cooperation in maintaining a stable global economy. PTT warns that a peaceful power transition is not guaranteed. Therefore, a solution may lie in establishing new rules of engagement that address both countries’ concerns. This could involve:

- Strengthening international trade institutions for fair competition and dispute resolution.

- Negotiating technology transfer agreements to address intellectual property theft concerns.

- Establishing norms for responsible behavior in the South China Sea and other geopolitical flashpoints.

These solutions have not been embraced in a committed manner to resolve the escalating tensions. The US-China trade war is a symptom of a more significant power shift. Understanding the economic, technological, and geopolitical factors through the lenses of HST and PTT is crucial for navigating this complex rivalry. Finding a sustainable solution may require a combination of cooperation and competition, managed within a framework of new rules and norms for a multipolar world.

US-China Trade Relation

China obtained a temporary MFN in 1980 and retained it despite the annual US threat to impose high tariffs. The integration of China into the global trading system through its joining the WTO helped it obtain permanent most favoured nation (MFN) status. The United States would have reverted to Smoot-Hawley tariff levels had the MFN status been revoked, and a trade war may have ensued (Handley and Limão*, 2017). The revocation of the MFN status in 2000, for example, would have increased the tariff on imported Chinese goods from a US MFN tariff of 4% to an average tariff of 31%.

After China became a World Trade Organization (WTO) member in September 2001, the US granted China permanent normal trade relations (PNTR), which conferred permanent preferential treatment to Chinese manufactured goods and encouraged the offshoring of manufacturing. Since 2001, the US trade deficit with China has been growing to about USD 300 billion which is the largest run by the US with any country in the world. Trade tensions between the US and China began to rise when the US trade deficit with China reached an all-time high of USD 295.5 billion in 2011. The total US trade deficit for 2022 was USD 1.19 trillion, with China accounting for USD 382.9 billion, 32% of the total trade deficit (Heritage, 2023).

| U.S. Trade in goods with China (millions of US dollars) | |||

| Year | Exports | Imports | Balance |

| 1985 | 3,855.70 | 3,861.70 | -6.00 |

| 1990 | 4,806.40 | 15,237.40 | -10,431.00 |

| 1995 | 11,753.70 | 45,543.20 | -33,789.50 |

| 2000 | 16,185.20 | 100,018.20 | -83,833.00 |

| 2005 | 41,192.00 | 243,470.10 | -202,278.10 |

| 2010 | 91,911.10 | 364,952.60 | -273,041.60 |

| 2011 | 104,121.50 | 399,371.20 | -295,249.70 |

| 2012 | 110,516.60 | 425,619.10 | -315,102.50 |

| 2013 | 121,746.20 | 440,430.00 | -318,683.80 |

| 2014 | 123,657.20 | 468,474.90 | -344,817.70 |

| 2015 | 115,873.40 | 483,201.70 | -367,328.30 |

| 2016 | 115,545.50 | 462,542.00 | -346,996.50 |

| 2017 | 129,893.60 | 505,470.00 | -375,576.40 |

| 2018 | 120,341.40 | 539,503.40 | -419,162.00 |

| 2019 | 106,481.20 | 449,110.70 | -342,629.50 |

| 2020 | 124,581.50 | 432,548.00 | -307,966.50 |

| 2021 | 151,439.40 | 504,246.30 | -352,806.90 |

| 2022 | 154,125.40 | 536,259.30 | -382,133.90 |

| 2023 | 147,777.80 | 426,885.00 | -279,107.20 |

| Source: United States Census Bureau (https://www.census.gov/foreign-trade/balance/c5700.html) | |||

An Economic Policy Institute Report titled “Unfair China Trade Costs Local Jobs,” released in March 2010, estimated that American workers have lost 2.4 million jobs due to excess export practices of China since China joined the WTO in September 2001 (Rosefielde, 2011). A later study by Coalition for a Prosperous America published in May 2023 titled “Post PNTR: 3.8 Million Jobs Lost Due To China” revised the total jobs lost by the US since 2001 due to the trade deficit with China to 3.82 million with manufacturing accounting for 2.89 million jobs lost, 75% of the total jobs lost.

The Congressional Research Service report RL31403 on China’s Trade with the United States and the World, prepared for Members and Committees of Congress in January 2007, highlighted the challenges the surging imports from China are posing to some US industries and manufacturing employment. The Congress also examined, among others, access to the Chinese market, intellectual property rights (IPO) protection, mounting trade deficits, and allegations of dumping wherein China sells its goods in the international market below cost, engaging in “currency manipulation,” and exploiting its workers for economic gain (Congressional Research Service, 2007).

The US raised several policy concerns with trading with China, the most obvious being that it is highly unbalanced in China’s favour, and many in the US associate this trade deficit with the loss of jobs in industries competing with rapidly rising imports from China. The report claimed that some economists, policymakers, and industry and labour leaders blame China for unfair trade practices, particularly undervaluing its currency, deliberately creating an uneven playing field for US companies competing against China’s imports. The Congress resolved to support policies that address China’s unfair trade advantage conferred by its government manipulation of the value of its currency and introduced several bills that addressed China’s currency practices, other alleged unfair trade practices, including dumping and export subsidies, violation of intellectual property rights and non-compliance with WTO regulations (Congressional Research Service, 2007).

The mainstream view in the US is that China has no freehold property and no rule of law. As a result, the State manages the means of production owned by the people and controls trade directly and indirectly through its lessor, command, and administrative, supervisory, and regulatory managerial powers. The State also controls trading systems and frequently fixes foreign exchange rates at disequilibrium levels, causing over- or under-trade and, in the process, over- (under-) import and export in what is referred to as forced substitution (West, 1993).

Trade Tension

In March 2012, the US, the EU, and Japan filed a “request for consultation” at the World Trade Organization over China’s restrictions on exporting rare earth metals. The US and its allies contended that China’s quota violates international trade norms and forces multinational firms that use the metals to relocate to China. It was a surprise in October 2022 when the US restricted exports of U.S.-made advanced computing chips and related equipment to China, applying the same restriction on foreign companies that use any U.S.-made tools and software. Though the US gave China’s use of the items to produce advanced military systems and commit human rights abuses as reasons for the restriction, it is generally believed that the restriction was meant to undercut China’s ability to manufacture the same class of integrated circuits.

Trade between the US and China reached a record high in 2022 but has since fallen as many big US companies have moved their production outside of China due to the restrictions, and many Chinese companies have also moved their production to a third country to be able to access US market and avoid the tariffs and sanctions. The consequence of the tariff and sanction wars between the US and China was a 17% reduction in trade in 2023. The goods the US bought from China last year fell just over 20% to $ 427bn, with a 4% fall the other way to just under $ 148bn (Josephs & Hashmi,2024).

Both countries are attempting to diversify their trade based on the fear that the other side will suddenly weaponize trade flows, cutting off imports or exports in the name of security. China began shifting its purchase of foreign goods away from the US in 2018 when Trump’s trade confrontation began. US exports, according to 2022 data, have fallen behind foreign peers selling into the Chinese market – semiconductor sector sales declined in 2022. They may not recover due to the export control policy, and US manufacturing exports such as automobiles and Boeing jets have all but disappeared (Bown & Wang, 2023).

The US Tariff Sanctions

The United States has already imposed hundreds of sanctions on China for offenses ranging from human rights violations, unfair trade practices, intellectual property theft, and Chinese companies’ continued relationship with Russia, Iran, North Korea, and Burma, among others, all of which have not noticeably altered the behavior of China. In February 2018, President Trump imposed safeguard tariffs that targeted specific products from many countries after the US International Trade Commission conducted a Section 201 investigation of solar panels and washing machines and determined that imports of these products had injured domestic producers. Additional tariffs on steel and aluminum that targeted several countries, including China, were shortly after imposed based on Section 232 investigations by the US Department of Commerce, with China and other trade partners responding by imposing retaliatory tariffs.

Trump era witnessed continuous rolling out of tariffs on a wide range of Chinese imports, with China giving back as much as it got in a tit-for-tat. The Trump Administration’s tariffs on Chinese imports targeted various industrial and transport products, including steel, aluminum, electronics, and medical devices. It also restricted some Chinese investment in the United States, added dozens of Chinese companies, including the country’s biggest chipmaker, Semiconductor Manufacturing International Corporation (SMIC), to its trade blacklist, and banned US companies from using foreign-made telecommunications equipment that could threaten national security, which generally was believed to target Huawei. China retaliated by imposing tariffs on US agricultural products, targeting commodities such as beef, dairy, seafood, and soybeans.

The United States implemented five tariff rounds on Chinese exports—in July 2018, August 2018, September 2018, June 2019, and September 2019 after the Office of the US Trade Representative initiated a Section 301 investigation of China’s trade practices and determined on March 22, 2018, that China’s trade practices ranging from the forced transfer of technology to Chinese firms to intellectual property theft to be unfair with China retaliating at each stage. By late 2019, the United States had imposed tariffs on roughly $ 350 billion of Chinese imports, and China had retaliated on $ 100 billion of US exports. However, the Phase One agreement was signed in January 2020 by the US and China to de-escalate trade tensions and implement a 50% reduction of the September 2019 tariff wave, but the tariffs remained in place. The trade war marked a most significant turning point in US trade policy history, in which it played a leadership role in integrating global markets.

President Biden has retained most of Trump-era tariffs on Chinese imports and expanded the scope of the tariffs. The US Commerce Department in October 2023 sanctioned two Chinese companies, adding them to a government export control list over their support for Russia’s military and defense industrial base – support that includes the supply of U.S.-origin integrated circuits. Seven other entities from Finland, Germany, India, Turkey, the United Arab Emirates, and the United Kingdom were also added to the trade export control list. The Chinese government called US action “economic coercion and unilateral bullying” and “unreasonable suppression of Chinese companies” (Reuters, 2023).

The United States, on 1st May 2024, sanctioned more than a dozen companies in China and Hong Kong as part of a tranche of nearly 300 new sanctions unveiled for supporting Russia’s war in Ukraine, which, according to US officials, came after repeated warnings from top US officials, including Treasury Secretary Janet Yellen and Secretary of State Antony Blinken, to top Chinese officials (Hansler & Waldenberg, 2024).

China’s Countersanctions

The Chinese government announced on 19 May 2024 its imposition of sanctions against the Defense, Space & Security unit of Boeing, the world’s largest aerospace company and leading manufacturer of commercial jetliners and defense, space, and security systems, and two other defense companies, General Atomics Aeronautical Systems, and General Dynamics Land Systems for arms sales to Taiwan, placing the companies on its “unreliable entities” list which forbade their further investment in China and placed travel bans on senior management for the companies. The government of China followed up on 30 May 2024 with a shocking and bold move with the announcement of sweeping restrictions on billions of dollars worth of critical aviation and aerospace equipment, technology, and software to the US and the EU effective 1 July 2024 to better protect national security and fulfill international obligations such as non-proliferation (Chiang,2024). The items on the export restriction list, which, going forward, will require export licenses, include equipment, software, and technologies related to aerospace structural components, engine manufacturing, and manufacturing of gas turbines

The recent statements of Chinese officials have sought to underscore the irony of the US sanctioning Chinese companies while simultaneously relying on Chinese manufacturing and technology. They argued that the sanctions are unfair and counterproductive as they disrupt global supply chains and hurt businesses. Even though the Chinese government stated that the implementation of export controls on specific molds, special fiber materials, and other related items is an international practice and these measures are not targeted at any country or region, analysts believe that this is a direct and vehement counterattack against what Beijing perceives as relentless and hypocritical US aggression. This provocative stance will escalate tensions to unprecedented levels, potentially igniting a full-blown trade war that could hurt global markets and disrupt international relations (Norton,2023).

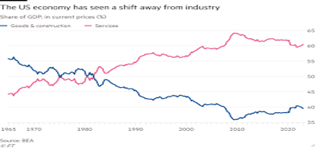

De-Industrialization of the US Economy

Over the years, the US economy has progressively shifted from manufacturing goods and construction to services. The graph below shows how the US economy has de-industrialized and become more financialized.

As shown above, over 55 percent of US GDP came from manufacturing and construction in 1965, and less than 45 percent from service sectors. However, the figure has declined since the shift of manufacturing industries from the US to China. This move was mainly driven by globalization and the rise of the neoliberal economic system, which, though it offered benefits to companies like lower cost of labor, access to new markets, and enjoyment of Chinese government incentives such as tax breaks and subsidies, has led to economic and social consequences for the US. By the 2000s, the service sector of the US economy made up 60 percent of the GDP. Statista said the service sector made up 77.6 percent of the US GDP in 2021.

The Meteoric rise of China’s economy

One of the most important developments of the 21st century is the meteoric rise of China’s economy, going from one of the poorest countries on Earth to building the world’s largest economy. China overtook the United States in 2016 as the world’s largest economy, measured in purchasing power parity. Since 2010, it has been the second-largest economy by nominal Gross Domestic Product (GDP) after the United States. China is the global manufacturing superpower, representing more than one-third of the entire world’s gross production of manufacturing goods, meaning China’s production surpasses that of the United States, Japan, Germany, India, South Korea, Italy, and France combined. Understanding how China has masterminded one of the most incredible examples of economic development in human history will explain why the United States has taken such an aggressive posture against China and possibly make the world live through a new Cold War.

China made up one-third of the global economy in 1820. However, its share of the global GDP contracted due to what is referred to as the century of humiliation when China was partially colonized by numerous foreign powers, including the European Colonial Powers, the U.S., and Japan, such that by 1950, it represented only 5% of the global GDP. The situation has fundamentally changed as it has become the largest economy measured at purchasing price parity. The International Monetary Fund (IMF) April 2023 data revealed that China’s GDP (PPP) is now 19% of the global economy, larger than the US at 15%. China has gone from being one of the poorest countries on earth to becoming the largest economy in just 70 years, a remarkable revolutionary economic transformation never undergone by any country.

The world’s manufacturing base migrated to China from 2001 when China joined the WTO, attracted by low-cost labour and favourable policies implemented by the Chinese government, including trade capacity enhancement, massive investments in infrastructure, and industrial policy to vastly increase industrial production (Norton, 2023). China has emerged as the world’s sole manufacturing superpower, and its industrialization has been both phenomenal and unprecedented, as its displacement of the US took about 20 years. In contrast, the US took over a century to displace the United Kingdom. China has been putting its industrial might to work, building two coal-fuelled power plants a month in 2023. Its Navy is now the largest in the world. China’s ship construction far exceeds India and the US, built more vessels than India, Japan, Australia, France, and the United Kingdom combined, and added the equivalent of the French navy to its fleet every four years (Baldwin, 2024). Pentagon’s annual report to the US Congress titled ‘Military and Security Development involving the People’s Republic of China” for 2023 reported that China has numerically the largest navy in the world with an overall battle force of over 370 ships and submarines, including more than 140 major surface combatants.

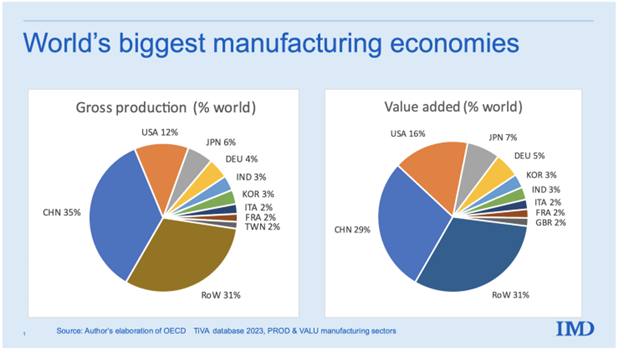

China has enjoyed much success in developing its industries, surpassing the United States in 2011, and in 1995 was responsible for 25% of global manufacturing. In contrast, China only represented around 5% of global manufacturing output. Richard Baldwin, professor of International Economics at IMD Business School, Lausanne, elaborated on the OECD TiVA database 2023 to produce charts explaining China’s manufacturing successes. The chart below shows the world’s biggest manufacturing economies, with the left panel showing the world’s share of gross production and the right panel showing the same in terms of value added. The gross production equals total sales, while value added is gross production minus the purchased intermediates. China is the biggest manufacturing economy at 35 percent, followed by the US at 12 percent, Japan at 6 percent, Germany at 4 percent, India at 3 percent, and South Korea at 3 percent. Six countries are noted to manufacture at least 3 percent of the global total.

The chart revealed an evolution in the world economic structure, showing that only three of the long-established industrial economies, three newly industrialized economies, and four of the G7 countries failed to make the 3 percent cut. China’s gross production is thrice the US’ share, six times Japan’s, and nine times Germany’s (Baldwin,2024).

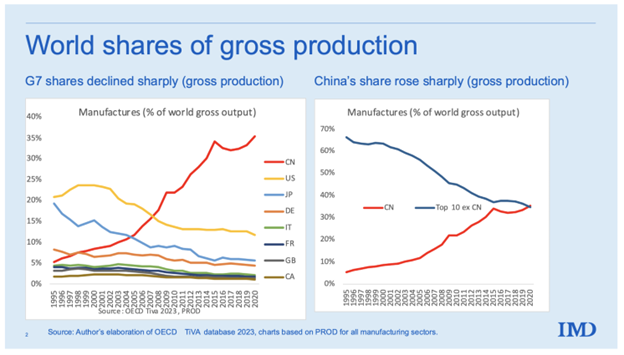

From the OECD data from 1995, China was a little ahead of Canada, Britain, France, and Italy, surpassed Germany in 1998, Japan in 2005, and the US in 2008. interestingly, since then, China has more than doubled its world share, and the US has fallen by three percentage points. China’s share now exceeds that of all the next largest manufacturers combined, as shown in the right panel of the graph below, showing China’s spectacular rise in manufacturing, 1995-2020 (world gross production shares), which explains the current US-China trade tensions.

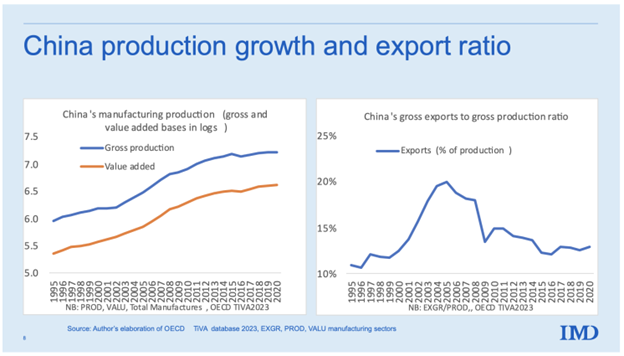

In the figure showing “China’s manufacturing growth and Gross Globalisation Ratio (GGR),” the right panel reveals China’s gross globalization ratio (GGR) in manufacturing, which is a measure of the share of manufactured production that is sold abroad, where production is measured as the total sales of all China-based manufacturers (includes all sales, not just final good sales). China’s GGR nearly doubled in the first decade, particularly from 1999-2004. However, the GGR has been steadily declining since 2004 as the middle class emerged to drive growth in domestic demand, tapering off the GGR by 2020 back to its position in 1995. This means that contrary to what many might believe, the level of dependence of China’s manufacturing on exports has waned (Baldwin,2024).

Socialist Market Economic System

China has masterminded the world’s most incredible economic development in the past three decades through massive industrialization. It has achieved this level of success by creating an economic system called ‘Market Socialism’ significantly guided by the state. However, China’s socialist market economy system significantly differs from the Soviet Union’s command economy system, which centralized planning, giving the government tight control of all aspects of the economy, dictating production quotas, prices, and resource allocation through Five-Year Plans. The Command economy has limited market forces since private ownership and market forces played a minimal role, innovation is limited as the lack of competition stifled innovation and efficiency, and most businesses were owned and controlled by the government. The socialist market economy of China incorporated market mechanisms like supply and demand to guide resource allocation and permit the co-existence of state and private sector.

China still has many state-owned enterprises (SOEs), but they operate with more commercial freedom and compete with private companies. China’s reforms have been gradual and controlled by the government, unlike the more abrupt changes seen in some former Soviet bloc countries. A key goal of China’s economic model is rapid economic growth, which has lifted eight hundred million people out of poverty. Therefore, unlike the rigid Soviet Union’s command economy that stifled innovation, China’s socialist market economy is a hybrid system with market elements alongside state control. This hybrid model has fueled China’s economic rise. China retains state control over the economy’s commanding heights, including finance, telecommunication, and infrastructure, and state-owned enterprises make up one-third of China’s GDP. The four largest banks in the world are state-owned Chinese banks, and significant parts of the manufacturing, telecommunications, and transportation sectors are owned by the state (Norton, 2023).

The disruptions to the global supply chains caused by Covid-19 pandemic escalated the calls to bring manufacturing back to home countries (‘reshoring’), closer home (or ‘nearshoring’) and following the intensification of the US-China trade war, more calls to move manufacturing out of China to friendly countries like India and Vietnam (‘friendshoring’) have grown louder. However, many companies are reluctant to move their production out of China despite the financial and political pressures. Professors Walid Hejazi and Bernardo Blum at the Rotman School of Management, University of Toronto, explained why foreign companies resist the significant pressures of exiting China. China has mastery of manufacturing that surpassed any other countries in the world such that even though labour costs are significantly higher in China compared to other emerging economies in Asia where the US is pressuring countries to move to, Chinese labourers are more very high skilled, making them more productive and these factors weigh heavily the decision to relocate production out of China.

In addition, manufacturing industries in China have access to a high level of agglomeration economies– or ecosystems such as those that exist in Silicon Valley for tech companies or Wall Street for financial institutions, and the proximate location of these related industries offers unique benefits. These benefits include sharing of resources providing easier access to specialized labour, suppliers, and infrastructure like transportation networks, spillovers of knowledge where ideas, innovations, and best practices can more readily flow between companies, fostering creativity and innovation, competition and efficiency pushing companies to innovate and become more efficient due to competition within the cluster and interdependence with different companies or organizations working together to create value in a well-functioning business ecosystem. China has deployed a strategy that ensures the entire manufacturing supply chain is located there, and has mastered each process step (Hejazi & Blum, 2023). For example, the entire production textile ecosystem is located in China. Therefore, Foreign companies are reluctant to leave China because the cost associated with leaving is prohibitive. It is, therefore, logical to reason that as long as the ecosystem for manufactured goods remains in China, a significant share of the world’s manufacturing will remain there.

According to a news release by Wood McKenzie dated 7 November 2023, China has achieved complete dominance in the solar supply chain. China is projected to control over 80% of the world’s solar manufacturing capacity until 2026, effectively meeting global demand for the next decade. The substantial capacity expansion has led to a significant decrease in solar panel prices this year, causing unease among US producers.

The Semiconductor war

AI is beginning to impact nearly every industry and is already changing our world. Everything from toasters to televisions, cars to smartphones, and every piece of electronics in between requires microchips. According to the research of PWC’s global artificial intelligence study, AI could contribute up to $ 15.7 trillion to the global economy in 2030, more than the current output of China and India combined. The semiconductor industry is crucial for technological advancements like artificial intelligence, electric vehicles, and factory automation, playing a vital role in a nation’s economic prosperity and security. However, the semiconductor manufacturing landscape has shifted due to globalization and economic factors, leading companies to move chip manufacturing to countries with lower labour costs, particularly in Asia. Even though the United States consumes a quarter of the world’s semiconductors, its manufacturing capacity has decreased from 37% in the 1990s to just 12%, raising concerns about national security threats due to China’s efforts to establish a significant presence in this essential industry.

The US National Security threat pertains to heavy reliance on foreign chip imports, which creates a potential vulnerability if there are disruptions in supply chains or political tensions with producer countries. Also, there is concern about technological dependence as the US might need to catch up in developing and innovating in this critical technology with a robust domestic chip industry. China is investing heavily in its domestic chip industry, aiming to become self-sufficient and a significant player in the global market. The US has long tried to limit China’s capabilities, particularly in semiconductors. While the US has defended its action as trying to restrict technology that its adversary could use to defeat it on the battlefield, China contended that the US is trying to kneecap its economy. The contention has triggered a geopolitical rivalry as the US sees China’s rise in chip production as a potential threat to its economic and technological competitiveness.

For years, the US was the dominant player in the microchip industry and is doing all it could to maintain its position. The United States has since 2022 implemented export controls as part of its containment strategy on China, particularly in the technology and semiconductor sectors. The US government has prohibited US persons from engaging in activities that support the production of advanced semiconductors in China and has urged its allies like Japan, South Korea, and the Netherlands to cease selling chips and advanced chip manufacturing equipment to China. Also, the US introduced the Chips and Science Act, a significant piece of legislation that allocated $ 52.7 billion over five years to boost domestic semiconductor (chip) production, research and development (R&D), and workforce development.

In the microchip industry, no country is entirely self-reliant and able to produce its own microchips. Thus, the collaboration between various countries. The Netherlands is arguably the most critical country in the world for microchip production, even though it does not produce a single microchip. This stems from the fact that ASMI, the Dutch company, is the only company on the planet with the machinery required to produce the world’s most advanced microchips. The Taiwan Semiconductor Manufacturing Company TSMC is the world’s third largest semiconductor manufacturer after Intel and Samsung, the world’s largest independent contract manufacturer of semiconductor products, and the world’s 8th most valuable company with a market capitalization of $ 954.18 Billion as of July 2024. Much of the global semiconductor supply chain relies on Taiwan. TSMC produces 90% of the world’s most advanced microchips and remains the cornerstone of tensions between the US and China relations (Janssen, 2024). The US government is concerned that China will invade Taiwan to complete its vision of a unified China and give it control of the entire future of the microchip industry. The microchip battle between the US and China is forcing both countries to innovate faster and constantly adapt to what the industry needs.

In one year from April 2023, Nvidia’s stock price grew from $ 270 to an all-time high of $ 950, taking its market capitalization well above the $ 2 trillion mark. NVIDIA’s A100 chip is the world’s foremost microchip powering AI technology and is undoubtedly well-positioned at the heart of the AI industry. The US government has restricted the sales of advanced microchips to China by Nvidia and other companies around the globe. Huawei, better known globally for its telecoms and smartphones businesses, has been building its stack of AI chip lines in the last five years and first launched its Ascend 910 chip in 2019, which immediately in the same year became the target of US export controls. The US restriction on the sales of advanced chips by Nvidia to China has allowed Huawei to fill the void created by winning the sizeable AI chip order from Baidu, the Chinese tech giant. However, in its just-released annual report, Nvidia, for the first time in its history, cited Huawei as a key competitor in several categories, including artificial intelligence (AI) chips. Nvidia listed Huawei as a significant competitor for the supply of chips designed for AI, such as graphics processing units (GPUs), central processing units (CPUs), and networking chips. It also identified Huawei as a cloud service company that designs its own hardware and software to improve AI computing. The Ascend AI chip series developed by Huawei is believed to rival Nvidia’s line of AI chips, with Huawei’s 910B chip main product rivaling Nvidia’s A100 chip (Cherney & Nellis, 2024).

The US government in October 2022 imposed a sweeping curb designed to curtail China’s access to advanced computing chips, with Japan and the Netherlands joining the US in early 2023 to curb the export of chip-making technology to China. The screw was further tightened by the Biden Administration, who, in October 2023, further restricted the sales of advanced semiconductors by US firms. As part of its retaliatory measures, China in April 2023 launched a cybersecurity probe into Micron Technology, a US producer of computer memory and data storage, before banning it from selling to Chinese companies working on key infrastructure projects and in July 2023, imposed export controls on two strategic raw materials, gallium and germanium, that are critical to the global chipmaking industry (He, 2024). The US effort to hold back Chinese technology development may fall short with the unveiling in August 2023 of Huawei’s Mate 60 Pro with 5G capabilities and a cutting-edge processor. A teardown of the new cutting-edge smartphone powered by advanced chips by Tech Insights for Bloomberg News revealed the chip powering the device was produced by China’s SMIC, raising questions about SMIC’s capabilities and the effectiveness of US-led controls (Webb, 2023).

The US government is now attempting to impose new restrictions on domestic suppliers supporting Huawei. However, the development of China’s chip industry appears undeterred, with Huawei restarting its vanguard project in April 2024 and launching the Pura 70 series in early May 2024. Reuters reported that Huawei’s new flagship Pura 70 Pro uses more domestic components than the Mate 60, equipped with improved Kieran chipsets and flash memory produced by local suppliers. A teardown by iFixit and Tech Search International for Reuters revealed that the flash memory might be packaged by Huawei subsidiary, Silicon, with other components made by Chinese companies. Researchers noted that the new device includes memory chips from South Korea’s SK Hynix, but the NAND chips might be supplied by Huawei’s in-house chip unit, HiSilicon.

Despite the expanding trade sanctions targeting Huawei and other Chinese companies to restrict their access to advanced technology, the proportion of Chinese components continues to rise, showcasing significant progress in capabilities, indicating that US sanctions have motivated China to close the technological gap and achieve self-sufficiency. In a recent move against Huawei, the US Department of Commerce revoked export licenses held by Intel and Qualcomm to supply smartphone and laptop chips to the company. According to the Global Times, a Chinese Ministry of Commerce spokesperson condemned the new restrictions as an abuse of export controls and typical economic coercion, violating WTO rules and severely harming US companies’ interests.

In 2020, TSMC was forced to halt chip production for a Chinese chip company, leaving several Chinese chip companies unable to use TSMC’s 7 nanometers or more advanced processes. However, just three years later, in 2023, the same Chinese company successfully produced a 5G chip close to the 7 nanometers process and reintroduced 5G smartphones. This breakthrough signifies that China has resolved the technical issues of advanced processes producing near 7-nanometer chips with existing lithography machines. On 23 May 2024, TSMC announced that the US Department of Commerce had granted its Nanjing plant an indefinite exemption, allowing it to purchase advanced lithography machines and other equipment from overseas.

This move is widely seen as a new strategy by the United States to curb the development of China’s chip industry. However, it may also reflect the US’s frustrations and challenges in suppressing China’s high-tech sector. The US initially aimed to stifle China’s advanced chip development by restricting cooperation with key supply chain companies like TSMC, but this strategy has failed following China’s rapid progress in chip development. Chinese companies are meeting the US’ efforts to suppress China’s technological development with innovative solutions and breakthroughs, and this dynamic questions the US’ strategy of relying only on sanctions and trade restrictions in the face of China’s growing technological capabilities.

Automotive Industry (Innovation and unmatchable cost efficiency)

China’s leading automaker, BYD, recently unveiled its latest hybrid car models, the Qin L DM-i and the Seal 06 DM-i, which feature the company’s fifth-generation DM (dual mode) hybrid technology. These new plug-in hybrid electric vehicles (PHEVs) boast an impressive driving range of up to 2,100 kilometers (approximately 1,305 miles) on a full charge and a full tank of gasoline (Fastepo, 2024). Launching these new models is a significant step for BYD as it aims to lead the global hybrid vehicle market, offering both environmental benefits and extended range for long-distance travel without frequent stops for recharging or refueling. The new car by BYD is a game changer that is revolutionizing the industry with its unprecedented range and advanced hybrid technology.

IEA Global EV Outlook 2024 report revealed that almost 14 million EVs were sold in 2023, with 95 percent being in China (just under 60 percent), Europe (just under 25 percent), and the United States (10 percent), bringing the total number of EVs on the roads to 40 million. EVs accounted for almost 18 percent of all cars sold in 2023, an increase of 14 percent over 202,2, with battery electric cars accounting for 70 percent of the sales. Several key countries continue to dominate the electric vehicle (EV) production landscape, with China, driven by a robust domestic market and significant export growth, leading the charge with 8.1 million sales in 2023, 35 percent more than in 2022, and an export of 1.2 million EVs (IEA, 2024).

The United States witnessed substantial growth in EV production, with new electric car registrations totaling 1.4 million in 2023, marking a 40% increase compared to the previous year. Federal incentives and policies aimed at boosting the adoption of electric vehicles have supported this growth. Europe is a major player in the EV market, with nearly 3.2 million new electric car registrations in 2023, a 20 percent increase over 2022.

In 2023, China remains the largest car producer in the world with an annual production of approximately 30.2 million vehicles solidifying its position as the leader in the automotive sector. The United States is the second largest producer, manufacturing about 10.61 million vehicles annually. Japan ranks third, producing approximately 9 million vehicles annually. These figures emphasize China’s significant role producing more vehicles than the USA and Japan combined which underscores its robust automotive market and its critical role in the global supply chain.

The other countries making the top ten global car producers according to Statista report of “Motor vehicle production volume worldwide in 2023, by country” are India ranked fourth with an annual production of approximately 5.9 million vehicles, leveraging its growth on the rising demand from its expanding middle class. South Korea has an annual production of about 4.2 million, in fifth place, thanks to major manufacturers like Hyundai and Kia. In the sixth position is Germany, widely renowned for its engineering prowess and home to major brands like Volkswagen, BMW, and Mercedes-Benz, which produce around 4.1 million vehicles annually, and in the seventh position is Mexico, with an annual production of about 4 million vehicles. The annual production of eighth-ranked Spain stands at around 2.5 million vehicles, and Brazil, South America’s only entrant in ninth position, produces approximately 2.3 million vehicles annually. Thailand rounds out the top 10 with an annual production of about 1.8 million vehicles, serving as a central production hub in Southeast Asia.

In 2023, China emerged as the world’s largest car exporter, exporting approximately 4.91 million vehicles, surpassing Japan, which shipped about 4 2 million vehicles. The 57.9% increase from the previous year’s rise in China’s exports was driven by the robust growth of its new electric vehicles EVs sector. Traditionally a major exporter, Germany remains a significant player in the global automotive export market. Advancements in EV technology, cost-effective manufacturing, and strategic international market expansion drive China’s rise as a dominant car exporter. Chinese automakers like BYD, SAIC, and Chery have significantly boosted exports, particularly to markets in the European Union, Southeast Asia, and Russia, which were secured following the exit of Western automakers due to sanctions.

The market shares of many green products made in China have risen compared to just five years ago, driven by market forces (Ebbers, 2024). Driven by the quest to protect its market from rampaging Chinese imports, the US has been using unilateral tariffs to reduce imports. The first four months of 2024 has witnessed a 23% increase in the sale of Chinese EVs in Europe despite the best efforts of the EU authorities to erect barriers to slow down these imports to protect local manufacturers (Slav,2024). This surge in the import of Chinese EVs to Europe is worrisome for the EU authorities, who have yet to figure out how to make local car makers competitive as they are not yet comparably reliable and cheap.

The EU announced in May 2024 that it is considering increasing the tariff on China’s EVs from 10% to 20,% which would cost 125,000 fewer Chinese cars to be sold in the EU, amounting to USD 4 billion in lost sales. The latest move by the EU to impose a staggering USD 4 billion worth of tariffs on Chinese electric vehicles has set the stage for an explosive showdown with China. There is also the European Commission’s investigation into alleged unfair subsidies received by Chinese EV makers. Critics brand these moves as a veiled attempt to justify protectionist policies and a desperate bid to shield European manufacturers from the relentless onslaught of superior and more affordable Chinese technologies. In a tit-for-tat tariff exchange, China immediately responded to the EU’s move by threatening to impose tariffs as high as 25% on vehicles with large engines, which could significantly impact luxury car manufacturers like Mercedes-Benz and BMW. This has sent shock waves through the continent’s high-end automotive sectors, with the future of brands like Mercedes-Benz and BMW in one of the world’s largest markets hanging in the balance.

If China decides to follow through with its threat to impose a 25% tariff on European high-end vehicles, EU automakers producing large engines could be significantly challenged, forcing a re-evaluation of export strategies and a potential shift in focus towards other markets less affected by trade tensions. The global supply chains are highly interconnected, and these trade policies will ripple across various sectors, not only the automotive industry but also related industries such as battery production, raw materials, and related technology. It is essential to critically examine the role of government subsidies in the EV market. While subsidies help nascent industries develop and compete globally, they also cause market distortions and trade imbalances; thus, policymakers are challenged to find the right balance between supporting domestic Industries and ensuring fair competition. Other countries and trade blocs looking to navigate similar challenges in the future will be closely monitoring the developments in the EU-China tariff situation, and the outcome could influence trade policies and negotiations worldwide. Therefore, a balanced approach is needed to address economic, environmental, and political considerations in these discussions as the European Commission prepares to make its decision (Innovative Check, 2024).

DISCUSSION

A common trend observed among US presidents for more than fifty years, except for Presidents George H. W. Bush and Bill Clinton, has been for them to introduce protectionist measures in their first terms. President Richard Nixon in 1971 imposed a 10% tariff on dutiable imports, President Jimmy Carter in 1977 placed a quota on shoe imports, and President Ronald Reagan pressured the Japanese government to implement a “voluntary export restraint” agreement limiting the exports of Japanese automobiles to the United States, President George W. Bush in 2002 imposed tariffs on steel and President Barack Obama in 2009 placed 35 percent tariffs on Chinese tires (Amiti, Redding and Weinsten, 2019). US trading partners had frequently complained about these past unilateral tariffs to WTO.

The administration of President Donald Trump followed this precedence of seeking trade protection in its first term but with more breadth and force. The Trump administration sought to renegotiate existing free trade agreements such as the North American Free Trade Agreement with Canada and Mexico and the US-Korea Free Trade Agreement. It withdrew from the Trans-Pacific Partnership (TPP) negotiations started under President George W. Bush and continued by President Barack Obama. TPP has taken off under a new name, Comprehensive and Progressive Agreement for Trans-Pacific Partnership, with the eleven remaining countries.

Offering various US-based legal justifications and failing to wait for the conclusion of the WTO dispute settlement process, the Trump administration in 2018 imposed tariffs on $ 283 billion worth of imports with rates ranging between 10 and 50%. The Administration relied on Section 201 of the Trade Act of 1974, which allows protection if an import surge is a substantial cause of serious injury to an industry to impose tariffs on imported washing machines and solar panels, Section 232 of the Trade Expansion Act of 1962, which allows for protection when imports threaten to impair national security to impose tariffs on imported steel and aluminum and Section 301 of the Trade Act of 1974, which allows the United States to impose tariffs if a trading partner is deemed to have violated a trade agreement or engages in unreasonable practices that burden US commerce to impose tariffs on US imports from China (Amiti, Redding and Weinsten, 2019). .

As an expected response to the US unilateral imposition of tariffs, China, the European Union, Russia, Canada, Turkey, Mexico, Switzerland, Norway, India, and Korea have all filed cases against the United States at the World Trade Organization, and many countries adopted retaliatory tariffs against the US actions. The EU, Mexico, Russia, and Turkey began to levy retaliatory tariffs averaging 16 % on US exports on approximately $ 121 billion of US exports. In 2018, China began levying tariffs on approximately $ 114 billion worth of US exports between April and September.

Protectionism impairs competition and can lead to beggar-thy-neighbor policies that partly or wholly cause mass unemployment and global depression. Beggar-thy-neighbor policies are economic tactics that aim to improve a country’s economic situation at the expense of its trading partners. The goal is to boost domestic industries and employment by making imported goods less competitive. The methods employed include introducing trade barriers such as tariffs on imports and quotas to limit import quantities to make foreign goods more expensive for domestic consumers. Another method is the devaluation of currency, which makes a country’s currency cheaper, encouraging exports (because they become less expensive for foreign buyers) but discouraging imports (because they become relatively more expensive). These policies often backfire, harming both the instigating country and its neighbors. Other countries may impose retaliatory trade barriers on the initiating country’s exports, leading to a trade war, such as the tit-for-tat tariff war between the US and China. Global trade reduction may be likely fallout as trade barriers and currency manipulation stifle international trade, harming all economies involved. Consumers in the initiating country may pay more for goods due to limited choices and higher import prices. Economists who promote free trade and international cooperation generally discourage beggar-thy-neighbor policies and encourage comparative advantage so that all countries can benefit from trade by specializing in what they produce most efficiently.

The tariff measures on Chinese EVs are expected to strain the relationship between the EU and China, hurt European consumers who would be made to pay higher prices, and undermine the EU’s ambitious climate goals as green technology becomes less accessible to citizens. This is a very highly contentious issue because it intersect economic, political and environmental considerations. A critical consideration for EU policymakers will be striking a balance between protecting local Industries and promoting both global trade and environmental sustainability, as this latest move by the EU highlights increasing complexities and challenges faced by international trade agreements and policies (Innovative Check, 2024). Resolving this matter and achieving a win-win will entail intricate negotiations and compromises by both sides trying to protect their interests as they strive to avoid a full-blown trade war.

Issue of Forced Technology Transfer

The United States’ concerns regarding China’s policy span a range of issues, but lying at the heart of it is a problem of “forced technology transfer.” The US accuses China of using unfair practices to gain access to foreign technology. This allegedly involves requiring foreign companies to partner with Chinese firms as a condition of doing business in China. Critics claim China uses various tactics to achieve this, including joint venture requirements, ownership limitations, and pressure to share intellectual property. The US argues that these practices disadvantage American companies, stifle innovation, and distort fair competition.

The issue of forced technology transfer is not just a concern of the US and China. Other countries, like Japan and the EU, have also raised similar concerns.

China denies these accusations, claiming that its policies align with WTO regulations and aims to promote technology development within China. China argued that it does not place the transfer of technology to Chinese entities as a formal condition to invest in China because having such contravenes China’s Protocol of Accession to the WTO elaborated in the new Phase One Trade Agreement with China. However, there are legal requirements in China that condition permission to invest in the formation of joint ventures with Chinese partners, and similar legal requirements that place a percentage cap on foreign equity ownership and thereby guarantee substantial indigenous participation in the investment enterprise (Sykes, 2021;p129). These requirements are used by potential Chinese investment partners as negotiating leverage to obtain technology transfer agreements. Even without a formal technology transfer agreement, Chinese venture partners can observe the operations of their foreign partners after becoming part of the venture to gain access to vital technology (Atkinson, 2012).

Weighing on the issue, Professor Alan Sykes of Stanford University offers a refreshing perspective, arguing that “foreign investors are free to reject such requirements and forego the associated investment opportunities, and in this sense, any technology transfer pursuant to China’s requirements is consensual” (Sykes, 2021; P127). This position aligns with that of the Chinese, who continue to argue that foreign investors are not forced to transfer their technology but willingly agree because they also have the option to refuse. While China insists that foreign investors have the prerogative to forgo the investment, critics argue that the Chinese market is so large and attractive that companies feel pressured to accept these terms, even if they are not ideal -a case of “choice” with limited options, a sentiment echoed by the US, who argues that these “choices” may be pressured or lack viable alternatives, making the technology transfer effectively “forced.

The Chinese government has imposed these requirements to secure technology transfer and develop its local industry by leveraging its cheap labour and growing market. China has capitalized on this policy, among other brilliant policies, to develop its industry. Today, in just forty years, it has become a world leader in technological production with massive technological innovators like Huawei. However, The issue is fraught with intricate legal complexities as defining and proving “forced” technology transfer can be challenging under international trade law. Overall, foreign technology transfer remains a contentious issue in the US-China trade relationship.

Impact of Trade War

The impact of the US-China trade war was evaluated by Itakura (2020), who conducted an ex-ante simulation analysis using a dynamic computable general equilibrium (CGE) model of global trade, exploring three scenarios to understand how the trade war affects import tariffs, investment, and productivity. The findings revealed that the escalating trade war reduces “gross domestic product (GDP) in China by -1.41% and the USA by −1.35%, and nearly all sectoral imports and outputs in both countries” (Itakura, 2020: pp77). Abiad et al. (2018) analyzed the impact of the current trade conflict on individual countries and on sectors within the countries in developing Asia and found that a full escalation of the US-China trade conflict would shave 1% off China’s GDP and 0.2% off US GDP with the rest of developing Asia enjoying small net gains thanks to trade redirection. They also observed that if the trade war extends to autos and parts, the EU and Japan would be hurt, and the conflict would have substantial adverse effects on China and US employment but only minor impacts on current account balances.

The research conducted by Fajgelbaum and Khandelwal (2022) revealed main takeaways of the trade war: US consumers bear the brunt of the tariff hikes on imported goods through higher prices. Although not by large magnitudes relative to GDP, the trade war has lowered the US and China’s aggregate real income. Amiti, Redding, and Weinstein (2019) found that the import tariffs imposed by the Trump Administration were costing US consumers an additional $ 3.2 billion per month in added tax by December 2018, another $ 1.4 billion in deadweight welfare (efficiency) losses and estimated that the combined effects of input and output tariffs have raised the average price of US manufacturing by 1%. They showed that the rise in tariffs reduced the variety of products available to consumers and estimated that if the tariffs were in place beyond 2018, approximately $ 165 billion of trade per year would continue to be redirected in order to avoid the tariffs.

Studies suggest some trade redirection occurred, with countries like Vietnam, Mexico, and Taiwan benefiting. Moody’s Analytics estimates that other countries might have captured around 21 billion USD of Chinese exports impacted by US tariffs between January and August 2019 (Mukherjee, 2020). The impact of subsidies on China’s manufacturing and export growth may have been overestimated. If subsidies drove the growth from $ 45 billion in 1990 with a forex reserve of $ 3.7 billion to the current $ 3.5 trillion but now exceed $ 3 trillion in reserves, where did China get the money to subsidize such huge volumes and yet have rising reserves (Ranganathan, 2023).

Power Politics

Mearsheimer (2001) explained in his book “The Tragedy of Great Power Politics” that the dynamic interplay between great powers is to compete with each other for power driven by fear for each other with the overriding goal being for one great power to gain more power at the expense of other states and ultimately become the hegemon. There was a divergence of opinions regarding what US foreign policy towards China should be at the dawn of the millennium. Many believe that a democratic China enmeshed in the global capitalist system will be content with the status quo in Northeast Asia. Therefore, the US should engage China to promote its integration into the world economy. Mearsheimer (2001) made an uncanny prediction that China and the US are destined to be adversaries as China’s power grows; thus, the engagement policy is doomed to fail. The reasoning is that if a democratic China deeply enmeshed in the global economy or autocratic and autarkic China becomes an economic powerhouse, it will most definitely translate its economic might into military might and attempt to dominate Northeast Asia. “Democracies care about security as much as non-democracies do, and hegemony is the best way for any state to guarantee its own survival” (Mearsheimer, 2001; p.2).

The US policy of economic engagement with China gave way to economic competition with the launch of a trade war by the Trump administration arising from prolonged dissatisfaction with China’s response to the US demand for a ‘fairer’ and more ‘reciprocal’ economic relationship. The National Security Strategy report unveiled by the Trump administration in December 2017 recognized the emergence of a new era of major power competition and branded China as a ‘revisionist power’ and ‘strategic competitor’ that wants ‘to shape a world antithetical to US values and interests’ (Zhao,2019: pp371). For the National Defence Strategy issued in 2018 by the US Department of Defence, the summary is that ‘central challenge’ to the Pentagon was how to tackle ‘the reemergence of long-term, strategic competition’ with China and other rival states (Zhao,2019: pp372). The release of the National Security Strategy of the United States of America and the Summary of the National Defence Strategy of the United States of America drew attention globally, particularly in China.

Chinese Perspectives on the Trade War

Professor Li Wei provided an overview of Chinese perspectives on the trade war in his journal article titled “Towards Economic Decoupling? Mapping Chinese Discourse on the China-US Trade War,” published in December 2019. In 2015, Professor Jin Canrong, a Chinese international relations scholar, stated without equivocation that, US-China relations would encounter significant challenges in the long term because the US is the established power and China is the emerging power. He viewed Sino-US relationship to have already fallen into the ‘Thucydides’ trap’. Thucydides’ Trap term was popularized by American political scientist Graham T. Allison in his book “Destined for War: Can America and China Escape Thucydides’s Trap?” and a theory used in international relations that suggests an increased risk of war when a rising power threatens to displace an established power. Professor Canrong asserted that the tension in US-China relations may be more complicated because it is also an ideological conflict apart from the geopolitical and economic dimensions (Wei,2019; Zhao,2019). The belief then was that strategic competition or even confrontation between the US and China would be unavoidable if the US adopted a policy of containment toward China’s rise.

At a seminar on China-US relations in May 2018, Li Ruogu, a retired Chinese banker and former chairman of the Export-Import Bank of China, opined that the China-US trade war is fundamentally about competition between development models because ‘the US believes that its free market economy cannot compete with China’s state capitalism’ (Wei,2019:pp. 532). This view was supported by Professor Jia Qingguo, a China-US relations expert at Peking University, who saw the trade war as driven by the divergence between the government-driven development model and the market-driven development model, in addition to power conflicts. He posited that many people in the US believe the “co-existence of and exchanges between two economic systems are detrimental to the United States” (Wei, 2019: pp. 533), considering China is now posing some degree of economic challenge to the US.

Most Chinese observers believe that economic and technological rivalry between the US and China has heightened. As the national power gap between China and the United States continues to close while the US strives to uphold its global hegemony, strategic competition between the two countries becomes inevitable, with the Western Pacific becoming the focal point of the US-China strategic competition (Zhao, 2019).

Failure of WTO Dispute Resolution Mechanism

Among the six key objectives of the World Trade Organization (WTO) are setting and enforcing rules for international trade to ensure fair and predictable trade practices among nations and resolving trade disputes. The WTO offers a dispute settlement system for member countries to resolve trade disagreements peacefully and according to established rules. Article 23 of the Dispute Settlement Understanding (DSU) of the World Trade Organization (WTO) deals with the obligation of WTO members to resolve trade disputes through the WTO dispute settlement system. Sub-section 1 emphasizes that WTO members must exclusively use the WTO’s dispute settlement procedures when seeking redress for violations of WTO agreements or benefits under those agreements with the implication that they cannot take unilateral actions like imposing sanctions outside the WTO framework. Sub-clauses of Article 23.2 further clarify that WTO members cannot make unilateral determinations about whether a violation has occurred. They must rely on the findings of the WTO dispute settlement process (panels and the Appellate Body). Members cannot impose sanctions or withdraw trade concessions (like raising tariffs) in response to perceived violations. Retaliation can only be authorized by the Dispute Settlement Body (DSB) after a successful WTO dispute settlement case.

The current trade war demonstrates that WTO is not serving its stated objectives and reflects the defectiveness of WTO dispute settlement mechanism. One of the reasons is the vagueness of the provisions of the many exceptions set up by the WTO that has allowed dispute settlement procedures to be circumvented, such as the “security exception” clause of Article 21 of GATT invoked by the US leading parties to directly resort to private remedies outside the procedure (Deng, 2021). Deng (2021) also observed that necessary protective measures are lacking in WTO’s dispute settlement mechanism because they are non-punitive and anticipatory, making it challenging to protect the performing party’s interest and leading to the absence of the power of deterrence in the relief of the corresponding rules of WTO. The implication is that a country in default can leverage its economic advantage to cause sustained trade harm to the actual performing country.