Fraud Prevention and Internal Control Mechanisms in Selected Banks in Nigeria

- Adekunle Akinola, PhD

- 287-298

- Jul 27, 2024

- Banking

Fraud Prevention and Internal Control Mechanisms in Selected Banks in Nigeria

Adekunle Akinola, PhD.

Department of Political Science, Adekunle Ajasin University, Akungba Akoko.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.807023

Received: 14 June 2024; Accepted: 27 June 2024; Published: 27 July 2024

ABSTRACT

The internal control procedures and policies of two Nigerian commercial banks were investigated in this research. Semi-structured interviews were used in the study to collect data using a qualitative methodology. Data was gathered from employees of the chosen banks’ internal control units using a purposive sample technique. Thematic analysis was utilised to examine the gathered data and it was demonstrated from the findings that the internal control methods that banks used to identify fraud were centered on setting up a control environment and identifying, analyzing, and managing risks from both internal and external sources. The investigation showed also that Nigerian banks’ use of a number of internal control mechanisms to thwart fraud has increased, particularly in the areas of authorizations, approvals, reconciliations, reviews of operational performance, asset security, division of labor, an enhanced information system, and a regular assessment of the internal oversight structures already in place. Additionally, the study discovered that since Nigeria implemented the cashless policy in 2014, the introduction of technology advancements into the banking industry has contributed, if marginally, to the improvement in the prompt detection and effective prevention of fraud. The internal control procedures (ICPs) of most banks in Nigeria have effectively reduced bank fraud from external sources. The research comes to the conclusion that Nigerian banks must prioritize protecting the data of their clients and strengthening their security systems by adhering to international standards and recommended practices if they want ICPs to be successful in detecting and preventing fraud.

Keywords: fraud, internal oversight systems, detection and prevention

INTRODUCTION

Since no economy can operate efficiently without a sizeable quantity of suitable money, the finance and banking industry is a primary engine of economic growth in any nation that serves as a critical financial hub for economic growth (Isibor, 2022). The banking sector raises surplus capital through savings and uses loans and withdrawals to move capital to the sections of the economy that are experiencing deficits. To position them for successful and efficient financial performance, their operations are given the utmost thought, oversight, and regulation (Boloupremo & Ogege, 2019; Nyakarimi et al., 2020). The majority of corporate entities and enterprises are primarily focused on generating profits; this is particularly true for financial institutions, where it is essential to both maximize earnings and satisfy clients’ demands for liquidity.

However, monitoring is crucial to the performance of organizations to accomplish these objectives (Isibor, 2022). In a country with as much volatility as Nigeria, the banking sector is the most unstable, and financial institutions are particularly open to attack. Also, due to the nature of their operations, most banks are open to fraudulent attack (Tade, 2021). Thus, in order to combat the prevalence of fraud in the banking industry, risk management measures must be implemented (Nyakarimi et al., 2020). Furthermore, as trust and confidence are the foundations of banks, these organizations may suffer when banks display risky or unsound confidence.

Internal controls must therefore be implemented to support effective operation so that banks can fulfill their declared objectives and build public trust. Management-created techniques are needed to prevent and identify fraudulent conduct. Since effective internal control is essential to the smooth functioning of financial institutions, management bears the majority of the responsibility for its establishment and upkeep. A robust internal oversight structures helps a banking company to maximize profits over the long and short terms while also helping it to meet its goals (Isibor, 2022).

According to Saxena et al. (2020), the core of internal control is found in the extensive financial controls system that most businesses have established. These systems are designed to protect assets, carry out corporate processes in an orderly fashion, and guarantee record accuracy and dependability as much as feasible. A study published by the International Standard on Auditing (ISA) claims that financial fraud happens when many managements, staff members, or outside parties to a company purposefully utilize betrayal to earn an unfair or illegal benefit. Management is involved because they can alter records to present fraudulent accounting figures and get over security measures. Employees may receive instructions from management to conduct fraud (Donelson et al., 2017; Dagane, 2024). Among other things, fraud is the deliberate fabrication or alteration of financial information with the express objective of falsifying official documents and credentials of a company or an individual’s business dealings (Tade, 2021).

Although a lot of Nigerian financial companies have implemented certain internal oversight structures to boost productivity and lower fraud, nonetheless, Nigeria continues to rank highly in the prevalence of economic crimes brought on by fraud, according to a recent poll, despite these efforts (Nyakarimi et al., 2020; Otuogha, 2021). The research claims that inadequacies in management-set policies and unethical behavior are mostly to blame for the recent rise in fraud. The pervasive fraud that affects many financial institutions, especially banks, has prompted a recent restructuring of Nigeria’s banking sector, which involves the mergers and acquisitions of faltering banks by stable ones. This reform has reduced banks’ financial status relative to other Nigerian institutions, demonstrating the tremendous impact that fraud has brought to banks (Nyakarimi et al., 2020). The Nigeria Deposit Insurance Corporation (NDIC) reported that there was a 40.98% drop in bank workers’ losses and real banking losses from ₦204.65 billion in 2019 to ₦120.79 billion in 2020. Nevertheless, the NDIC reports that Deposit Money Banks (DMB) in Nigeria reported 177.10% rise in fraud occurrences from 52,754 to 146,183 between 2019 and 2020 (NIDC, 2020).

The frequency of fraud attacks and their possible consequences may have decreased in the banking industry owing to advancements in internal control protocols, regulatory and supervisory monitoring, and security architecture (Otuogha, 2021). However, the insufficiency of internal control measures in banks has hindered progress, based on the Central Bank of Nigeria’s (CBN) report analyzing the incidence of fraud in Nigeria. Research findings establishing the effectiveness of specific internal control measures adopted in Nigerian banks in minimizing fraud occurrences is scarce. Beyond the implementation of more internal control measures to bridge the insufficiency identified by the CBN, it is equally important that each of these measures are assessed to know which ones eventually meet the purposes for which they were put in place (Nyakarimi et al., 2020; Otuogha, 2021). As a result, this research ventures into the assessment of how procedures of internal control adopted by Nigerian banks can affect fraud detection and prevention in the Nigerian banking sector.

LITERATURE REVIEW

A number of studies (Agbenyo et al., 2018; Nyakarimi et al., 2020; Saxena et al., 2020; Dagane, 2024) have looked at the effectiveness of internal control policies on fraud detection and prevention, with varying degrees of success. Nyakarimi et al. (2020) made it known that if all five essential elements—control environment, exchange of information, control measures, risk evaluation, and monitoring—are actively and correctly operated, then the efficacy of internal control protocols (ICPs) in identifying and preventing fraud can be empirically determined. Agbenyo et al. (2018) found that environmental control over the effectiveness of practices, policies, and procedures has a weak and unfavorable impact on the caliber of financial reporting when investigating how governmental measures of internal control influence the financial state of a subset of Ghanaian companies. According to Saxena et al. (2020), insufficient control measures and an unfavorable control environment allow for an increase in financial reporting fraud in financial firms. Dagane (2024) observed a similar result despite focusing on manufacturing firms in Nigeria and emphasized the detrimental effect exerted on the financial performance of businesses. Haladu (2018) discovered a negative correlation between internal oversight structures and the methods of fraud detection put in place by a few DMBs listed on the Nigerian Stock Exchange. According to the outcome arrived at, one important aspect affecting the internal oversight structures used in the under-study organizations to prevent and identify fraud is the control environment. In the same vein, Koech & Kimani (2018) make a related argument that the control environment is a key element which significantly influences the prevention and detection of fraud in organizations, thus corroborating this finding.

While the aforementioned research looked at how internal oversight structures affect non-financial firms’ ability to detect and prevent fraud, other studies, such as those by Gee & Button (2019), Olulade, Ilugbusi & Awoniyi (2019) and Tade (2021) focused on financial firms. The subject of study for Thao (2018) and Olulade et al. (2019) was the banking sector. Tade (2021) discovered flaws in risk evaluations pertaining to possible problems resulting from projects overseen by the African Development Bank. He carefully assessed the effectiveness of the bank’s internal oversight structures in stopping and identifying fraud. Gee and Button’s (2019) investigation of commercial banks in Ethiopia revealed a substantial relationship between risk evaluation and fraud mitigation. Thao (2018) demonstrated how crucial the regulatory setting is to joint-stock commercial banks’ efforts to prevent and identify fraud. His research sought to determine how well certain banking institutions in the province of Thai Nguyen’s internal oversight structures detected and stopped fraud. The results highlight how much the likelihood of fraud affects commercial banks’ internal oversight frameworks. In their investigation of Nigerian DMBs’ control system’s impact on the identification and prevention of fraudulent occurrences, Olulade et al. (2019) found that risk assessment had the most significant influence on fraud prevention and detection, which was backed by a strong p-value. The study also shows that the lowest impact and lowest p-value are associated with information, communication, and monitoring.

In their investigation of the relationship between credit-related hazards and internal oversight in European banks, Akwaa-Sekyi & Gene (2017) discovered a strong and noteworthy correlation. They demonstrated how bank control techniques have a strong and notable impact on preventing fraud, which in turn significantly lowers credit risk. However, Ikeotuonye & Nnenna (2016) revealed important findings about how the internal oversight structures affect the prevention of fraud. They specifically emphasized the significant impact of crucial elements including risk evaluation, monitoring, and the control environment—all of which are essential for supporting the control system against fraudulent activity. The study focused on a subset of Nigerian commercial banks and examined the relationship between internal oversight structures, fraud prevention, and fraud detection. Likewise, in their investigation of the efficacy of GN Bank’s internal control procedures in Ghana, Owusu-Boateng, Amofa, & Owusu (2017) discovered that the bank’s management and board’s risk control techniques minimized fraud risks to statistically significant amounts.

Monitoring and risk assessment procedures are important internal oversight structures elements that support the prevention and identification of fraudulent occurrences, according to Shonhadi & Maulidi’s (2020) study on practices utilsed in the public sector for fraud minimisation. A poor and negligible correlation was found between internal oversight structures and attempts to prevent and identify fraud in Haladu’s (2018) study focusing on listed companies on the Nigerian Stock Exchange. Furthermore, Rafindadi & Olanrewaji (2019) contend that the purpose of transmitting such information is contradicted when information is verified without first ensuring that it is conveyed in a way that won’t jeopardize the internal oversight structures.

Stemming from the aforementioned researches, it is clear that internal control procedures and guidelines play a crucial role in aiding the prompt identification and prevention of fraud cases, particularly in the banking sector. Investigations on ICPs however remain a necessary area of research interest due to the rapid increase in fraud cases reported on a yearly basis; especially in Nigerian commercial banks (Adetiloye et al., 2016; Tade, 2021). The literature has offered a number of explanations as to why the rate of fraud incidences in financial firms like banks is rising. Adetiloye et al. (2016) discovered that the high rate of fraud in the industry is caused by the intensity of communication and digital technology advancement, which has led to the development of internet and mobile banking. On the other hand, Mwithi & Kamau (2015) contend that as human factors play a less part in fraud incidences, the banking sector will benefit from the effective and suitable deployment of technology. According to the study, quick information exchange, made possible by technology, can lessen the fraud cases recorded. In the banking industry, information sharing must be done carefully though, as depending on the information shared, there may be a rise or fall in fraud instances (Otuogha, 2021).

In his study, Pharm (2021) argues that prompt transmission of accounting processes; a high compensation package, efficient communication channels, and the prevention of technological failure are ways to bolster the internal control mechanisms used in detecting and preventing fraud cases. The effectiveness of the internal oversight structures can also be increased by timely and efficient external and internal audits as well as management meetings. The rationale for this study is that, although previous research has demonstrated the link between internal oversight structures and fraud prevention, additional research is required to determine which internal oversight structures is most successful in preventing and detecting fraud; most especially in the context of thriving commercial banks in Nigeria. Likewise, unlike most of the reviewed researches which employed a quantitative method, this study investigates the subject matter via a qualitative means. This is to gather better understanding of the specific ways ICPs have worked in minimizing fraud and to arrive at a more detailed finding. This study adds to knowledge already existing on the subject by analyzing the internal control procedures and policies at two leading commercial banks in Nigeria: Access bank Plc and Wema bank.

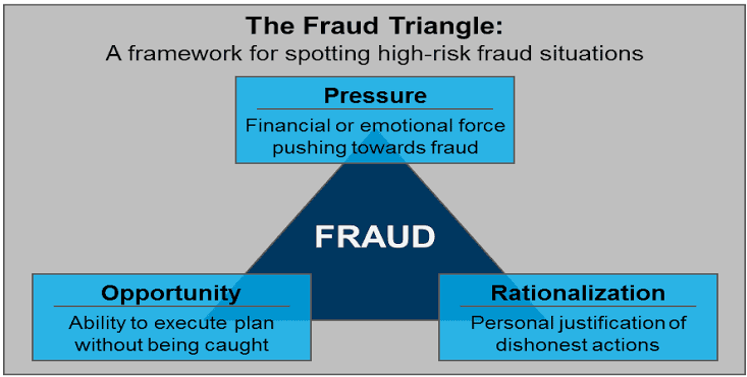

The Fraud Triangle Theory

This theory was developed in 1953 by Donald Cressey to assist in preventing and detecting fraud and to give a plausible explanation for the reason behind peoples’ fraudulent actions. The following three conditions, according to the notion, have to be met for someone to engage in fraudulent acts. (i) Perceived fraud opportunity, (ii) perceived pressure to initiate a fraudulent act, and (iii) perceived rationalization (the alteration of one’s self-perception). The coexistence of all three components is necessary for fraud to occur, but Suh et al. (2019) established that even in the event that one ingredient is not there, fraud can still happen. The link between the three components is depicted in Figure 2.1 below.

Figure 2.1: Fraud Triangle

Source: Villaescusa, 2022:33.

The foremost component displayed in the triangle is perceived pressure. According to Villaescusa (2022), guilt or a sense of achievement may motivate someone to commit fraud if they face pressure from a non-shareable financial situation. This could only occur if the individual is reluctant to communicate their financial hardship (Kranacher & Riley, 2019; Le et al., 2020). Because of this, an individual could be pressured to keep on maintaining a particular desired lifestyle even when they now earn much lower than they used to (Zakaria et al., 2016). Kranacher & Riley (2019) cite greed, familial pressure, financial losses, poor credit, and high debt burdens as other causes of fraud pressure. However, Lokanan (2018) made it known that non-financial causes like being discontent with working conditions can also exert pressure on someone to deceive others, thus leading to the next feature of fraud.

The ease with which an individual can commit fraudulent acts characterizes the perceived opportunity (Villaescusa, 2022). Because of this, environments with weak internal oversight structures tend to have perceived opportunities (Peltier-Rivest & Lanoue 2015; Riney, 2018; Sexana, 2020). According to Godfroid (2019), an individual’s job may also increase the risk of fraud. For example, in banks, the main culprits of fraud are mostly loan officers. This is so because the majority of banks give their loan officers the power to make decisions (Riney, 2018). Thus, Villaescusa (2022) assert that by implementing a robust internal oversight structures, an organization can reduce the likelihood of fraud and eventually eradicate it.

The third component of the triangle speaks of an individual’s ability to give rational explanations for their fraudulent actions. This rationalization refers to an individual’s viewpoints about the beliefs, expectations and contributions they anticipate from their employers/company for their work done (Villaescusa, 2022). The rationalization process makes a fraudster justify his/her dishonest actions and see his/her situation as an exceptional occurrence instead of an act of betrayal (Roszkowska, 2020). This makes people label themselves as the victims or use wrong justifications like “others are also doing it” or “they owe me” to defend their behavior. The reduction of fraud can be greatly aided by controlling and limiting these justifications.

Though the theory received some credit from researchers for being an invaluable tool for early fraud identification and prevention, it has suffered criticism for failing to effectively address issues linked with fraud occurrences. For instance, Kassem (2020) criticized the fraud triangle as being useless when financial fraud reports are to be assessed. Kassem (2020) asserts that if managers’ goals, integrity levels, and competencies are not recognized, fraud pertaining to financial statements may go undetected. Likewise, Lokanan (2015) opined that the theory is insufficient as a tool for detecting and preventing cases of fraud. The research emphasizes and draws the attention of researchers to the different ways through which the theory offers a necessary knowledge base but falls short of providing the objective criteria needed to fully and sufficiently address every single instance linked to fraud. Additionally, Villaescusa (2022) contend that certain people may be able to resist the urge to commit deception in spite of motive, opportunity, and pressure. Notwithstanding these doubts, the Fraud Triangle theory continues to play a crucial role in improving our understanding of the motivations underlying fraudulent activity. Businesses can effectively mitigate, if not completely eradicate, fraud by implementing strong internal control processes that meticulously address each element of the fraud triangle.

RESEARCH METHODOLOGY

The qualitative research methodology was used for this study; it was chosen due to its value in gathering thorough and in-depth data from a small sample. The employees of Wema Bank and Access Bank comprise the study’s population. In contrast to Access Bank, which reflects a more recent generational model, Wema Bank is an example of an established millennial bank (Okoye et al., 2017). As a result, the information gathered from these two institutions appropriately captures the characteristics of the Nigerian banking industry. This is the reason these particular banks were chosen for the research.

Sample Size and Technique

Twelve employees in total are included in the sample, six from each bank. Four employees from each of the national, regional, and branch fraud control divisions at Access and Wema banks were chosen to take part in the study. Purposive sampling, a branch of non-probability sampling, was used to determine the sample size used. Purposive sampling provides a way to choose study participants based on their familiarity with the research question (Taherdoost, 2016). Because the employees of the bank’s control units are in charge of creating and carrying out internal control procedures and policies for preventing and detecting fraud, purposive sampling was chosen for this study.

Instrument of data collection

The study used semi-structured interviews to gather qualitative data. In this interview type, participants are asked questions on a research problem and given the opportunity to share their opinions on the research questions. This tool’s ability to provide the study with research participants’ meanings and interpretations of the research topic is one of its main advantages (Fusch & Ness, 2015).

Data Analysis

A thematic analysis of qualitative excerpts was conducted for the data analytical process. After the data was categorized, themes, patterns, and connections were found to facilitate the examination of the data. The responses from the interviewees were coded as (AB1-12) and (WB1-12) where AB1 represents Access Bank Respondent 1 and WB1 corresponds to Wema Bank Respondent 1, in order to protect the participants’ anonymity.

FINDINGS

General Information on Frauds

Fraud is a serious, unregulated, and unappreciated problem. Scammers attack public organizations on a regular basis. Regrettably, during business transactions, many public bodies fail to give proper consideration to fraud incidences. Even at times when consideration for fraud occurs, it is often quite challenging for public authorities to correctly define and measure the problem on their own (Sexana, 2020).

Fraud Types Reported in the Bank

According to academics like Mangala & Soni (2022), fraud incidences have been since the inception the banking business. The definition provided by Sood & Bhushan (2020) defines fraud as a calculated and premeditated act committed by an individual or a number of individuals who have the intention of falsifying reality or facts in order to benefit financially from it. It calls for the application of trickery, guile, and occasionally a great deal of experience. One of the study’s participants observed that the nature of fraud has changed as the banking industry has moved toward digitalization, with banks continuously juggling new cases and emerging trends. He stated, elucidated that:

While there are many distinct kinds of bank fraud, online banking scams are currently the most prevalent (AB1).

In agreement with the foregoing qualitative extracts:

Another research participant believed that the largest fraud in Nigerian banks involves technologically enabled transactions, such as those conducted on the internet and using ATMs. In terms of internal involvement in the fraud, all employees were found to be involved, despite the fact that most of them were temporary employees (WB2).

According to a different research participant:

The majority of frauds in the Nigerian financial sector are: Mixed frauds, which are committed by both outsiders and bank employees. These thefts frequently result from breaches in cyber security and digital banking (AB2).

The claims made above highlight the serious danger that banking sector scams pose to almost every nation on the planet. Such fraudulent activity affects both financial and non-financial parts of the economy, causing significant harm to banks, consumers, other interested parties, and the economy as a whole (Tade, 2021).

Internal Control Procedures that Financial Institutions use to Identify Fraud

Umar & Dikko (2018) provide a thorough explanation of internal control, describing it as an extensive concept which is inclusive of all policies, guidelines, and safeguards put in place by a company to raise the chances that business goals would be met without hindrances. Yousef (2017) presents an alternative viewpoint on internal control, characterizing it as a unified system of guidelines and protocols intended to supervise an entity’s activities and guarantee absolute compliance with the business goals as itemized by the organisation’s board of directors and management.

A research participant said:

Establishing a control environment is a very essential internal control strategy in a bank (WB5).

The assumption that certain elements of the control environment that are made feasible include the “integrity, ethical ideals, and competency of its people” is supported by this paragraph (Moughalu et al., 2018).

Furthermore, a different respondent thought that:

The environment of control maintains rigorous standards of ethics and gives the organization rules and regulations for a variety of reasons (WB4).

In support of this section, one of the participants stated that:

The operating theory, leadership style, and human resource policies such as proper training, compensation and development criteria, and the distribution of control and responsibility—are essential control measures (AB4).

Moreover, an additional respondent expressed that:

The verification, evaluation, and administration of risks from both internal and external sources are an essential control strategy that the majority of Nigerian banks should implement (AB2).

This result supports the evidence from the literature and demonstrates that risk assessment procedures are dynamic systems that are susceptible to alterations, as well as the importance of risk assessment in accomplishing control goals (Tade, 2021). Therefore, appropriate goal-setting is necessary for effective risk evaluation. According to Moughalu et al. (2018) and Ohiani (2020), risk assessment broadens its scope to include threats that arise from both internal and external sources within the organization, such as individuals within the organizational framework, management’s operational philosophy and approach, the delegation of authority and accountability, and the structure and promotion of employee development.

Internal Control Measures that Nigerian Banks Employ in Preventing Fraud

A wide range of tasks are covered by most internal oversight measures, such as “authorizations, permits, confirmations, settlements, operating performance reviews, assets security, and division of tasks.” The most visible aspect of internal control is control actions, which also happen to be the most important in stopping wrong conduct. According to a study participant’s explanation:

One of the knowledge and interaction challenges that, if addressed, will allow the Nigerian banking system to minimize fraud is the quick detection, capture, and exchange of data related to finances, operations, and compliance (AB6).

A different respondent expressed the opinion that:

The need for information to prevent fraud to be available, timely, precise, and relevant in Nigerian banks is the most significant control mechanism (AB4).

Another research participant stressed the need for ongoing appraisal of the effectiveness of internal control measures in an attempt to provide more information on the most effective internal control practices to prevent fraud in Nigerian banks. As he put it, he clarified that:

Details on possible and implemented control methods evaluation and oversight activities—which could include self-examination external audits, or direct oversight testing—always reveal prior shortcomings (WB4).

Nigerian Banks’ Unique Measures for Preventing and Detecting Fraud

Every nation whose economy is negatively impacted by fraud and forgeries does so. Banks are particularly vulnerable to fraud because of the nature of their business and the peculiarities of modern payment technology. As a result, they have had to implement new rules over time to fend off fraudsters’ attempts (Isibor, 2022). As stated by one of the respondents:

Like the bank where I work, the majority of Nigerian banks create distinctive rules that regulate internal control procedures and practices that aid how easily frauds are prevented and detected. However, the majority of these autonomous policies consistently adhere to the Central Bank of Nigeria’s functional instruction regarding the avoidance and control of fraud (WB6).

According to a different research participant, a critical policy approach that can support how easily and early fraud can be detected and avoided is the regular evaluation of bank corporate government policies. He said in his own words that:

Adherence with Nigerian sector banking ethics has a substantial impact on the banking sector’s attempts to avoid fraud, and good bank corporate governance that is regularly assessed annually will play a key role in these efforts. (AB3).

Another respondent confirmed that one strategy that has helped Nigeria identify and prevent fraud is the usage of the Bank Verification Number (BVN). The individual clarified that:

The BVN policy has made it possible for Nigerian residents to verify their identities through digital means for both electronic and non-electronic bank transactions. The BVN policy has been very helpful in identifying and stopping Nigerian bank scammers (AB1).

Internal Control Practices (ICP) Used Specifically in Nigerian Banks for the Avoidance and Detection of Fraudulent Practices

As a crucial corporate governance strategy, control procedures have drawn increased attention in a number of research studies in recent years (Kravet et al., 2018). According to Ahmad (2019), a sincere system of measures enables the explicit investigation of every fraud as well as the causes of the frauds in question. Regarding the particular ICP that Nigerian banks use to identify and stop fraud, one of the study’s respondents said:

Preventive, detective, and corrective techniques are used by the majority of Nigerian banks to identify and stop fraud. The employment of one-time passwords, card pins, and CVC codes, as well as the role played by two-step verification codes for the majority of digital transactions, are clear examples (AB4).

A respondent held the opinion that:

Nigerian banks primarily use a consistent system of checks and balances to ensure that nobody has total authority over financial transaction (WB5).

Drawing on the body of research on internal control, fraud, and justice in organizations, Roszkowska (2020) developed two original models for worker fraud and QCA practices. The main model, which is predicated on the data, demonstrates how the ICP standard positively affects the connection between employee fraud and structural justice beliefs. The alternative model highlights the many beneficial relationships that exist between ICP and a few essential organizational elements, such as staff risk mitigation training, business culture, and internal audit activity level (IA). In bolstering this claim, a respondent clarified that:

The technique of regularly reconciling bank transaction balances and efficiently monitoring and assessing bank systems can minimize fraudulent activities (AB5).

Furthermore, an additional respondent expressed the belief that:

Another essential procedure that might lessen frauds against financial systems is cyber security surveillance (WB3).

Many legal regulations have been passed in Nigeria in an attempt to close the gap left by the absence/inadequacy of suitable legislation for prosecuting fraud (Tade, 2021). One of the study’s respondents said that this had decreased bank fraud, saying that:

ICPs, particularly the BVN, have significantly reduced fraud since the majority of Nigerians are aware of how competitive banks are and how important online secure banking is (WB5).

Supporting this, an additional respondent held the opinion that:

Internet banking and recognition of fraud have improved since most Nigerian banks established credit risk evaluation and cyber security departments (AB4).

In a similar vein, a different participant said:

Many Nigerians are now more than ever conscious of crucial procedures that can expose them to attacks from fraudsters, which has improved the banking system thanks to internal oversight techniques implemented by the majority of banks (WB4).

Additionally, the results of the qualitative excerpts showed that most banks’ efforts to detect and prevent fraud have been supported by the existence of a control staff that keeps an eye out for fraudulent activity. The respondent clarified that:

The establishment of a specialized customer support team in Nigeria to handle fraud complaints, as well as enhanced identification of fraud and prevention, particularly in bank cyberspace (AB6).

DISCUSSION OF FINDINGS

This study’s main goal was to assess the internal oversight practices and policies (ICPs) in place for spotting and stopping fraud incidences in the banking sector of Nigeria. The results showed that ICPs placed a strong emphasis on how well commercial banking institutions procedures work to identify, track, and evaluate fraud risk. This is in line with the findings of Maaroufi & Hajar’s research from 2022, which showed that organizational frameworks, regulations, and procedures can effectively guarantee the accomplishment of business goals and the identification and correction of unfavorable risk events when they are followed consistently. This is the perfect example of management-initiated measures and compliance. This suggests that the internal control framework in the financial industry should be primarily centered on how to reduce fraud risks. Therefore, the main goals of the internal control techniques banks employ to identify fraud are the establishment of a strong control environment as well as the correct risk identification and the careful analysis and the management of risks that can emanate from both internal sources and external ones.

According to the research, Nigerian banks use a range of internal control procedures to thwart fraud. These safeguards consist of division of roles, improved information systems, operating performance reviews, asset security, secure routine approvals, authorizations, verifications, and reconciliations, as well as regular assessments of internal measures of control put in place. This outcome is consistent with Saxena et al. (2020), who noted in their investigation that preventative measures were put in place to lessen fraud and other security risks that were detected. As a result, the best internal control techniques should cover people, systems, infrastructures, and procedures. In particular, the Central Bank of Nigeria’s operational directives against fraud prevention and control, the BVN (Bank Verification Number) policy, Good Bank Corporate Governance, and individual independent policies all have a bearing on how Nigerian banks implement fraud detection and prevention. This conclusion is further supported by successful policies that have developed since Nigeria’s cashless policy was put into place (Tade, 2021).

According to the research, the main internal control policies (ICPs) used by banks includes processes to evaluate and monitor bank systems effectively, and the application of measures to prevent detect and correct fraudulent activities as promptly as possible. These results are consistent with the preliminary investigation conducted by Hussaini et al. (2018) regarding the influence the management of risks and the adopted risk culture have on Nigeria’s banking sector’s performance. According to this report, in order to obtain the best security systems in the sector, Nigerian banks should standardize on the three pillars of fraud risk management: corrective, preventative, and detective control procedures.

According to the report, there has been some reduction in fraud since the Bank Verification Number (BVN) was introduced. Improved cyber fraud prevention and detection, heightened awareness of crucial activities that expose institutions to cyber attacks, and expanded electronic banking and fraud detection capabilities are some of the main outcomes of ICPs. As a result, the sector’s ongoing ICP improvement will promote the banking industry’s long-term, sustainable growth (Tade, 2021; Saxena et al., 2020).

CONCLUSION

The study found that internal control strategies used by banks to spot fraud were mostly focused on creating a control environment and recognizing, evaluating, and controlling risks coming from both internal and external sources. Improved information systems, a consistent and effective internal control mechanisms assessment, and a greater focus on performance evaluations, asset security, permits, approvals, verifications, and checks are some of these methods. Furthermore, with regard to the first goal, this study found that Nigerian banks’ distinct policies on the avoidance and detection of fraud are more like independent, one-of-a-kind type that adhere to the CBN’s operational directive mitigating and managing fraud; Good Bank Corporate Governance; and BVN policy.

Concerning the second objective, which assessed the internal control practices selected Nigerian banks employ in an attempt to detect and thwart fraud. This study’s findings showed that Nigerian banks employ a variety of specific internal control practices (ICPs) to detect and prevent fraud. These include the avoidance, identification, and correction of fraud are supported by strategic operating practices, regular check-and-balance procedures, daily financial transaction balance reconciliation, and efficient monitoring and evaluation of bank systems. A discussion of the specific consequences that ICP has on fraud avoidance and detection in Nigerian banks was another outcome that addressed the second goal. The main effects of ICPs adopted by most Nigerian banks involve enhanced digital banking and identification of fraud, increased customer-awareness on important activities that can leave them at risk of fraud attacks, and improved structures and processes for fraud detection and prevention, particularly in the digital banking space. The study’s results specifically showed that BVN significantly reduced fraud.

REFERENCES

- Adetiloye, K. A., Olokoyo, F. O., & Taiwo, J. N. (2016). Fraud prevention and internal control in the Nigerian banking system. International Journal of Economics & Financial Issues, 6(3), 1172-1179.

- Agbenyo, W., Jiang, Y., & Cobblah, P. K. (2018). Assessment of government internal control systems on financial reporting quality in Ghana: A Case Study of Ghana Revenue Authority. International Journal of Economics & Finance, 10(11), 40-52.

- Ahmad, A. A. B. (2019). The Moderating role of internal control on the relationship between accounting information system and detection of fraud: the case of the Jordanian banks. Journal of Academic Research in Economics & Management Sciences, 8(1), 37-48.

- Akwaa-Sekyi, E. K., & Gené, J. M. (2017). Internal controls and credit risk relationship among banks in Europe. Intangible Capital, 13(1), 25-50.

- Boloupremo, T., & Ogege, S. (2019). Mergers, acquisitions and financial performance: A study of selected financial institutions. EMAJ Emerging Markets Journal, 9(1), 36-44.

- Cressey, D. R. (1953). Other people’s money: a study in the social psychology of embezzlement. Glencoe, IL: The Free Press.

- Dagane, M. D. (2024). Effect of internal controls on fraud detection of manufacturing firms in Garissa County, Kenya. International Journal of Finance, 9(1), 20-42.

- Donelson, D. C., Ege, M. S., & Mclnnis, J. M. (2017). Internal control weaknesses and financial reporting fraud. Auditing a Journal of Practice & Theory, 36(3), 45-69.

- Fusch, P. I., & Ness, L. R. (2015). Are we there yet? Data saturation in qualitative research. The Qualitative Report, 20(9), 1408.

- Gee, J., & Button, M. (2019). The financial cost of fraud 2019: The latest data from around the world. Available at: https://www.crowe.com/uk/croweuk/insights/financial-cost-of-fraud

- Godfroid, C. (2019). Relationship lending in microfinance: How does it impact client dropout? Strategic Change, 28(4), 289-300. https://doi.org/10.1002/jsc.2271

- Haladu, A. (2018). Fraud detection and internal control measures in deposit money banks listed in Nigerian stock exchange. International Journal of Science & Management Studies, 1(4), 43-54.

- Hussaini, U. Bakar, A. A., & Yusuf, M. B. O. (2018). The Effect of fraud risk management, risk culture, on the performance of Nigerian banking sector: Preliminary analysis. International Journal of Academic Research in Accounting, Finance & Management Sciences, 8(3), 224-237.

- Ikeotuonye, Victor, D. O., & Nnenna Linda, E. (2016). Internal control techniques and fraud mitigation in Nigerian banks. IOSR Journal of Economics & Finance, 07(05), 37–46.

- Kassem, R. (2020). Fraudulent financial reporting risk assessment: external auditors’ perceptions versus the traditional fraud triangle theory. The 9th Counter Fraud Conference and Forensic Accounting Conference, Portsmouth, United Kingdom.

- Koech, J. C., & Kimani E. M. (2018). Effect of control environment on fraud detection and prevention at University of Eldoret, Kenya. Africa International Journal of Management Education & Governance (AIJMEG), 3(2), 43-51.

- Kranacher, M. J., & Riley, R. (2019). Forensic accounting and fraud examination. John Wiley & Sons.

- Kravet, Todd D. and McVay, Sarah E., & Weber, David P. (2018). Costs and benefits of internal control audits: Evidence from m&a transactions. Review of Accounting Studies, Forthcoming. Available at SSRN: https://ssrn.com/abstract=2958318 or http://dx.doi.org/10.2139/ssrn.2958318

- Le, N.-T.-B., Vu, L.-T.-P., & Nguyen, T.-V. (2020). The use of internal control systems and codes of conduct as anti-corruption practices: Evidence from Vietnamese firms Baltic. Journal of Management, Vol. ahead-of-print No. ahead-of-print. https://doi.org/10.1108/BJM-09-2020-0338

- Lokanan, M. (2018). Theorizing financial crimes as moral actions. Journal of European Accounting Review, 27(5), 901-938, https://doi.org/10.1080/09638180.2017.1417144

- Lokanan, M. E. (2015). Challenges to the fraud triangle: Questions on its usefulness. In Accounting Forum, 39(3), 201-224. http://dx.doi.org/10.1016/j.accfor.2015.05.002 0155-9982

- Maaroufi, A., & Hajar, E.L. (2022). The effect of internal control components on the organizational performance of Moroccan public organization: a theoretical exploration. Revue du Contrôle, de la Ccomptabilité et de l’audit, 6(2).

- Mangala, D., & Soni, L. (2022). A systematic literature review on frauds in banking sector. Journal of Financial Crime ahead-of-print. Doi:10.1108/JFC-12-2021-0263

- Muoghalu, A. I. Okonkwo, J. J., & Ananwude, A. (2018). Effect of electronic banking related fraud on deposit money banks financial performance in Nigeria. Discovery, 54(276), 496-503.

- Mwithi, J. M., & Kamau, J. N. (2015). Strategies adopted by commercial banks in Kenya to combat fraud: a survey of selected commercial banks in Kenya. International Journal of Current Business & Social Sciences, 1(3), 1-18.

- Nigeria Deposit Insurance Corporation (NDIC) (2020). NDIC: bank fraud, forgeries amounted to ₦120.79bn in 2020. Available at:

- Nyakarimi, S. N., Kariuki, S. N., & Kariuki, P. (2020). Application of internal control system in fraud prevention in banking sector. International Journal of Scientific & Technology Research, 9(3), 6524-6536.

- Ohiani, A. S. (2020). Technology innovation in the Nigerian banking system: prospects and challenges. Rajagiri Management Journal ahead-of-print. Doi:10.1108/RAMJ-05-2020-0018

- Okoye, L.U., Adetiloye, K.A., Erin, O., & Evbuomwan, G.O. (2017). Impact of banking consolidation on the performance of the banking sector in Nigeria. Journal of Internet Banking & Commerce, 22(1), pp.1-16.

- Olulade, K. A., Ilugbusi, B. S., & Awoniyi, C. O. (2019). Impact of internal control on fraud prevention in deposit money banks in Nigeria. Nigerian Studies in Economics & Management Sciences, 2(1), 42-51.

- Otuogha, I. M. (2021). Internal control and fraud in deposit money banks in Bayelsa State. IOSR Journal of Business & Management, 23(4), 28-39.

- Owusu-Boateng, W., Amofa, R., & Owusu, I. O. (2017). The internal control systems of GN Bank- Ghana. British Journal of Economics, Management & Trade, 17(1), 1-17.

- Peltier-Rivest, D., & Lanoue, N. (2015). Cutting fraud losses in Canadian organizations. Journal of Financial Crime, 22(3), 295-304. https://doi.org/10.1108/JFC-11-2013-0064

- Pham, H.N. (2021). How does internal control affect bank credit risk in Vietnam? A Bayesian analysis. The Journal of Asian Finance, Economics, & Business, 8(1), 873-880

- Rafindadi, A. A., and Olanrewaju, Z. A. (2019). The impact of internal control system on the financial accountability of non-governmental organisations in Nigeria: evidence from the structural equation modelling. International Review of Management & Marketing, 9(3), 49-63.

- Riney, F. A. (2018). Two-step fraud defense system: Prevention and detection. Journal of Corporate Accounting & Finance, 29(2), 74-86. https://doi.org/10.1002/jcaf.22336

- Roszkowska, P. (2020). Fintech in financial reporting and audit for fraud prevention and safeguarding equity investments. Journal of Accounting & Organizational Change.

- Saxena, N. Hayes, E. Bertino, E. Ojo, P. Choo, K.K.R., & Burnap, P. (2020). Impact and key challenges of insider threats on organizations and critical businesses. Electronics, 9(9), 1460.

- Shonhadji, N., & Maulidi, A. (2020). Is it suitable for your local governments? Journal of Financial Crime

- Sood, P., & Bhushan, P. (2020). A structured review and theme analysis of financial frauds in the banking industry. Asian Journal of Business Ethics, 9(2), 305-321.

- Suh, B.J., Nicolaides, R., & Trafford, R. (2019). The effect of reducing opportunity and fraud risk factors on the occurrence of occupational fraud in financial institutions. International Journal of Law, Crime & Justice, 56, 79-88. https://doi.org/10.1016/j.ijlcj.2019.01.002

- Tade, O. (2021). Nature of frauds in Nigeria’s banking ecosystem, 2015-2019. Journal of Financial Crime, ahead-of-print. Doi:10.1108/JFC-08-2021-0185

- Taherdoost, H. (2016). Sampling methods in research methodology; how to choose a sampling technique for research. How to choose a sampling technique for research.

- Thao, N. P. (2018). Joint-stock commercial banks in Thai Nguyen Province. Vietnam, (April), 766-780.

- Umar, H., & Dikko, M.U. (2018). The effect of internal control on performance of commercial banks in Nigeria. International Journal of Management Research, 8(6), 13-32.

- Villaescusa, N., (2022). The fraud triangle: Assessing fraud risk. In handbook of research on the significance of forensic accounting techniques in corporate governance (85-101). IGI Global.

- Yousef, A. B. (2017). The impact of internal control requirements on profitability of Saudi shareholding companies. https://doi.org/10.1108/IJCOMA-04-2013-0033

- Zakaria, K. M., Nawawi, A., & Salin, A. S. A. P. (2016). Internal controls and fraud–empirical evidence from oil and gas company. Journal of Financial Crime, 23(4), 1154-1168. https://doi.org/10.1108/JFC-04-2016-0021