Impact of Monetary Policy on Unemployment Reduction in Nigeria: 2000-2023

- Elizabeth Obiaje

- Eunice Aondoakaa

- 322-333

- Mar 27, 2025

- Economics

Impact of Monetary Policy on Unemployment Reduction in Nigeria: 2000-2023

Elizabeth Obiaje., Eunice Aondoakaa

Bingham University, Karu, Nasarawa State, Nigeria Faculty of Social Sciences Department of Economics

DOI: https://dx.doi.org/10.47772/IJRISS.2025.915EC0019

Received: 18 February 2025; Accepted: 22 February 2025; Published: 27 March 2025

ABSTRACT

This paper examined the monetary policy impact on unemployment reduction in Nigeria. The data there were used in the study were annual data which span from 2000 to 2023.Monetray policy in this study was proxied using monetary policy rate, Money supply and inflation rate, unemployment rate, on the other hand is the dependent variable. Given the nature of the study, this paper adopted the ex-post Facto study design. Data on monetary policy rate, inflation, money supply, and unemployment were obtained from the CBN data bulletin. The hypotheses of this study were tested using the ARDL statistics. Findings unveiled that inflation and money supply has a significant relationship with unemployment while monetary policy rate has a negative but significant relationship with the dependent variable. The researcher recommended that the monetary authorities should ensure that the money supply should be increased significantly so that there will be money in the economy this will lead to increase in employment, poverty reduction, improve standard of living amongst others.

Keywords: Monetary Policy, Money supply, Unemployment rate, Exchange rate, inflation rate

JEL Classification: E52; E51, J24, F31, E31

INTRODUCTION

The Central Bank of Nigeria (CBN) defined monetary policy as specific actions taken by the apex bank to regulate the value, supply and cost of money in the economy with a view to achieving government’s macroeconomic objectives. The objectives of monetary policy may vary from country to country but there are two main views. The first view calls for monetary policy to achieve price stability, while the second view seeks to achieve price stability and other macroeconomic objectives including unemployment reduction which is the focus of this paper. The major instrument of monetary policy in Nigeria is the monetary policy rate (MPR). The policy rate was adjusted four times in the last six months of 2023 from 16.50 percent in December, 2023 to 17.75 percent in July, 2023 (Eyone et al., 2024). The other policy parameters, such as the Cash Reserve Ratio (CRR) and Liquidity Ratio) were retained at 32.5 percent and 30.0 percent respectively (NESG, 2023).

However, unemployment has being a long time chronic country disease especially in under developed economy like Nigeria. Its consequences are numerous as it does more harm than good in a country. According to the International Labour Organisation (ILO), unemployment is defined as an individual aged 15 or older who concurrently satisfies three criteria: being unemployed during a specific week; being available to commence employment within two weeks; and having actively sought employment in the preceding four weeks or having secured a position starting within three months. The escalation of unemployment in Nigeria is evident, with the unemployment rate rising to 4.122% in 1992 from 1.027% in 1986. Furthermore, the rate of unemployment increased to 9.773% in 2011 and in 2015 increased to 14.912%, while in 2021 the rate got up to 28.788% (CBN, 2021). The rate of unemployment in Nigeria was observed from the data to have increased significantly between 2015 to 2021 and has been fast climbing to the present day.

Unemployment is a significant issue at both in the macro and the micro stages. At the individual or microeconomic level, it diminishes personal incomes, hence leading to a reduction in the household wages and future savings potential. It results in diminished self-esteem and identity, adversely affecting individuals’ mental health and consequently impairing their productivity. Moreover, it results in elevated instances of both physical and mental health deterioration, as well as mortality. Furthermore, it results in impoverishment, diminishing persons’ ability to acquire and consume nutritious food, secure housing, and access healthcare. At the macro level, it results in the depletion of essential productive resources, undermining sustained economic growth and the enhancement of living standards across the nation. Consequently, it elevates dependency ratios and reallocates monies intended for developmental reasons to social welfare expenditures (Linus et al., 2024).

Nigeria has undergone some basic structural adjustments since attaining democratic independence in 1960. These local structural adjustments have not yielded any significant or satisfactory economic growth and development (Linus et al., 2024). Monetary policy was implemented to achieve full employment and consistent economic growth. Abayomi (2022) asserts that monetary policy is a policy document indicating that an increase in the money supply, with other variables held constant, will result in a fall in interest rates, while private investment in the economy is likely to increase along this policy trajectory.

Conversely, monetary policy has seen price instability over the years. The ineffectiveness of monetary policy non controlling price volatility has resulted in growth instability, as seen by Nigeria’s development record (Onyeiwu, 2012). Research indicates that ineffective monetary policies combined with elevated and volatile inflation disturb the allocation of resources for productive activities, ultimately leading to increased unemployment rates in the long run period (Okoro, 2015).

In the initial three quarters of 2017, more than 4 million jobs were eliminated, resulting in a joblessness and underemployment rate that rose to 40 percent (Nigerian Economic Summit Group, (NESG) 2018). KPMG (2023) contends that unemployment will persist as a challenge due to insufficient economic development and the Nigerian economy’s inability to accommodate the 4 to 5 million new entrants into the job market annually. Unemployment in Nigeria is rapidly reaching alarming levels. The high unemployment rate exacerbates unhappiness, poverty, and jeopardises social cohesiveness. The reduction of the unemployment rate has emerged as a primary policy focus of the Nigerian government. Nigeria is the sixth largest oil producer globally and the first in Africa; nonetheless, the country’s unemployment rate is among the highest worldwide (Linus et al., 2024).

Unemployment, conversely, is a fundamental underlying developmental challenge facing Nigeria at present. It is generally inadvisable to assume that governments at any level have not taken measures to reduce unemployment in Nigeria. For example, the formation of National Directorate of Employment (NDE) and its propensity for acquisition programs like National Poverty eradication programme (NAPEP), Poverty alleviation programme (PAP), Subsidy, Reinvestment and empowerment program (SUREP) and Youth enterprise with innovation in Nigeria (YOUWIN) are a portion of the various adjudication rich with job creation opportunities (Aganga, 2010 & Ogunmade, 2013). Nevertheless, research conducted by Fasanya et al., (2013) and Onyemu (2012) observed that, despite endeavours to attain the desired macroeconomic objectives via monetary policy, the outcomes have been insufficiently stable, evidenced by a persistently high unemployment rate, a continuous rise in poverty levels, a low standard of living, and an unacceptable inflation rate, particularly in underdeveloped nations. Notwithstanding all monetary policy measures implemented to mitigate unemployment, the problem has been escalating.

From the reviewed studies, the following conclusions are made: some previous studies focused on monetary policy and economic growth (Fasanya et al., 2013; Okafor et al., 2015; Udude, 2014; Ufoeze et al., 2018). Others focused on unemployment and monetary policy: (Okegwo & Ogbuehi, 2016; Okeke & Chukwu, 2021; Amasonma, 2015; Ekwe, 2018; Attan et al, 2019; Nwamuo, 2022). These studies concluded on the positive relationship between monetary policy of different indicators and unemployment. These studies focused on monetary policy and economic growth on the premise of the linkage between economic growth and unemployment) Fasanya et al., 2013; Okafor et al., 2015; Udude, 2014; Ufoeze et al., 2018), while (Nwosa, 2016; Onwuka, 2022) focused on monetary and fiscal policy and unemployment on the premise of the potency of economic policy mixture (Nwosa, 2016; Onwuka, 2022). In terms of methodology and analytic applications, the following is the most commonly used in these studies: Error correction mechanism, vector autoregressive (VAR); vector error correction (VECM); Ordinary least square; non-linear autoregressive distributed lag(NARDL) and data envelope analysis(DEA), few studies used autoregressive distributed lag model. In term of the variables used, the following have been used in studying the relationship between monetary policy and unemployment: output growth, exchange rate; economic growth, fiscal policy, macroeconomic policy; cash reserve, interest rate, unemployment rate, consumer price index, treasury bill rate, credit to the private sector, government tax, lending rate and deposit interest rate. Few studies used the monetary policy rate, inflation rate and money supply which are the value addition of this paper.

Therefore, this paper seeks to examine the impact of monetary policy on unemployment reduction in Nigeria; investigate the impact of money supply on unemployment reduction in Nigeria; assess the impact of inflation on unemployment reduction in Nigeria; determine the impact of monetary policy rate on unemployment reduction in Nigeria.

The hypotheses of this paper are stated as follows:

H01: Money supply has no significant impact on unemployment reduction in Nigeria

H02: Inflation rate has no significant impact on unemployment reduction in Nigeria

H03: Monetary policy rate has no significant impact on unemployment reduction in Nigeria.

LITERATURE REVIEW

Conceptual Review

Monetary Policy

Monetary policy is perceived as a mechanism by which a nation’s central bank regulates the money supply, inflation, the demand for commodities, and the corresponding demand for labour necessary for their production (Gideon & Paul, 2020). Monetary policy is a strategy established and implemented by a nation’s central bank (Adeagbo, 2021). Ndife (2020) asserted that monetary policy has to do with the deliberate adjustment of the supply of money by monetary authorities such as the central banks to achieve specific macroeconomic objectives. It encompasses activities by central banks designed to influence the macroeconomic sector to achieve price stability.

Unemployment

Unemployment is defined as the proportion of individuals within the workforce – excluding the entire active population or the total population – who are actively seeking employment but have been unable to secure a job for at least twenty-four hours during the active period, relative to the total currently active population (National Bureau of Statistics, 2019).

Empirical Review

Linus et al., (2024) analysed impact of monetary policy measures and unemployment in Nigeria for a time series period of 35 years (1986 to 2021). The paper used ARDL technique for the analysis. It was revealed in the study that the monetary policy rate significantly negatively affects the rate of unemployment rate, the exchange rate negatively impacts unemployment, and the money supply has a considerable positive effect on unemployment. The researchers asserted that the administration of monetary policy had a substantial adverse effect on the unemployment rate. The CBN is advised to consider sustaining the existing money supply, since it facilitates greater liquidity for banks to provide loans, so promoting investment and ultimately mitigating unemployment in the long term.

In a similar study, Eyone et al., (2024) empirically examined the monetary policy impact on unemployment reduction from 1986 to 2022, the paper employed dynamic autoregressive distributed lag and the Granger causality approaches for the analysis. Thus, findings depicts that prime lending rate was positive and significant at the 5 % level of significance, money supply was observed to be negative and significantly related with the rate of unemployment. Also, the lagged values of inflation rate were positively and significantly correlated with unemployment. According to the paper it was recommended that economic stability is sacrosanct through job creation thus promoting productivity of the Nigerian economy through access to credit by the private sector.

Chukwuemeka (2022) investigated the impact of monetary policy on unemployment rate in Nigeria for a time series data spanning from 1981 to 2020. The ARDL bounds testing approach to co-integration was used to analyse the data. Based on these findings, the paper recommended that the monetary authority should come up with policies that will reduce minimum rediscount rate as this will encourage borrowing of funds for investment purposes as this will help to reduce unemployment rate. Monetary authorities should also come up with policies that will stabilize exchange rate.

Chinonye (2022) empirically examined the impact of fiscal and monetary policy on unemployment rate using data between the periods 1981 to 2020 by the use of Vector Autoregressive (VAR) model as technique of analysis. The findings show that government expenditure and interest rate has negative and significant effect on unemployment rate at lag period 2. Government tax was found to be negative and insignificant at lag period 2. Money supply was found to have a positive and significant at lag period 1. By implication, the findings show that government expenditure, money supply and interest rate are major determinants of unemployment rate in Nigeria since they were found to be statistically significant. The study concludes that there is need for diverse strategies that will be targeted towards employment creation in Nigeria. Thus, an expansionary fiscal and monetary policy should be encouraged to support employment generation in the country.

Yiyao (2021) analysed monetary policy and unemployment of the United States from the first quarter of 1983 to the second quarter of 2018. This paper uses an extended version of the original Taylor’s rule by adding the concept of unemployment degree. The results suggest that in both periods, the unemployment gap degree does make a positive impact on the Fed interest rate and has a constantly significant impact on the Fed rate. As a result, Central Banks should adopt an easy monetary policy to stimulate the domestic economy from recession.

Okeke and Chukwu (2021) examined the effect of monetary policy instruments on unemployment in Nigeria from 1986 to 2018. The study adopted an Autoregressive Distributed Lag technique. The study found that cash reserve ratio and monetary policy rate had positive and insignificant effect on the employment rate in Nigeria, broad money supply had positive and significant effect on the employment rate in Nigeria, exchange rate and liquidity ratio had negative and significant effect on the employment rate in Nigeria. The authors recommended that the Monetary policies should be used to create a favourable investment climate by facilitating the emerging of market based interest rate and exchange rate administration that will attract both domestic and foreign investments and create jobs.

Gideon and Paul (2020) investigated the asymmetric pass-through of monetary policy rate to unemployment in Nigeria using the asymmetric ARDL model over the period 2000Q1 to 2018Q4. The study found dissimilar long-run effects of tightening and easing the MPR on unemployment. While tightening the MPR had positive, elastic and statistically significant effect on unemployment, implying complete pass-through, easing the MPR had negative, inelastic and statistically insignificant effect on unemployment, suggesting incomplete pass-through. The authors recommended that to curb unemployment using the interest rate channel, the monetary authority (Monetary Policy Committee) should ease the MPR by a higher magnitude compared to the magnitude that is required to tighten it for the purpose of price stability.

Ekwe (2018) analysed the impact of monetary policies on Nigeria’s unemployment using the regression method of analysis. The unit root (Augmented Dickey Fuller) test was used to determine the stationarity of the variables. Drawing from the recent development in cointegration analysis and the error correction model (ECM), the study found as follows: that Treasury bill rate and money supply have positive relationship with unemployment in Nigeria, that there is a negative relationship between monetary policy rate and exchange rate with unemployment in Nigeria. The paper concludes that there is a significant negative impact of monetary policies on Nigeria’s unemployment, which if not checked will continue to hinder the success of the fight against poverty in the nation.

Philip (2016) examined the effect of macroeconomic policies on unemployment and poverty rates in Nigeria from 1980 to 2013 with implication to achieving inclusive growth. The paper adopted the Ordinary Least Square (OLS) technique. The study observed that among macroeconomic policy variables only exchange rate significantly influenced unemployment rate while only fiscal policy significantly influenced and poverty rate. This implies that present macroeconomic policies in Nigeria do not guarantee the attainment of inclusive growth in Nigeria. The contribution of the paper is that to achieve inclusive growth that guarantees high employment and reduced poverty rate, there is the need for a re-examination of macroeconomic policy management in Nigeria.

Sunday et al., (2016) investigated the link between unemployment and monetary policy in Nigeria using a vector autoregressive (VAR) framework for the period 1983q1 – 2014q1. The paper investigates the effect of structural change by identifying three structural breakpoints and incorporating them into the VAR model as dummy variables. The results show that a positive shock to policy rate raises unemployment over a 10 quarter period. In addition, all the variables used as proxy in the model jointly Granger cause unemployment, implying the existence of a dynamic relationship between monetary policy and unemployment in Nigeria.

Theoretical underpinning

The Keynesian school held that monetary policy is a major instrument of macroeconomic management. They stressed the necessity role of government’s controlling bodies in stabilizing the country at full employment. They opined that this goal is attained by controlling the level of total demand to attain full job for the country. Thus, the government in order to attain full employment can as well increase taxes on goods and services that are not domestically produced as a way of increasing earnings. Also, the government can give tax holiday to domestic entrepreneur thus promoting increase in export volume to pay for increased imports, in that regard promoting and enhancing domestic production and job creation.

The Keynesian went further to submit that employment relies on aggregate demand; demand promotes output; output on the other hand generates earning while earning provides job. In that regard, they saw the nexus between monetary policy and joblessness as a vicious circle reason being that he saw employment as a function of income. Therefore, Keynes (1934) emphasised that effective demand is what is required to combat depression and joblessness.

METHODS AND MODEL SPECIFICATION

These papers empirically examine the impact of monetary policy on unemployment rate reduction in Nigeria, and because it is a cause and effect relationship which sees an existing situation and looking back in time for causal agent, the research design is the ex-post facto design.

This paper uses time series data which covered a period of 24 years from 2000 to 2023. The research made use of secondary data on monetary policy and unemployment. The researcher sources relevant data which were obtained from the Central Bank of Nigeria Bulletin and Nigeria Bureau of Statistics data records.

This paper adopts Autoregressive Distributed Lag (ARDL) model for more accurate and robust estimations and also because it gives the long run estimation without losing the short run properties. The paper is therefore justified in terms of the model adopted. The ARDL-bound testing approach accommodates the presence of both I(0) and 1(1) variables or combination of both, Pesaran et al., (2001). Also, it is justified by capturing more variables as regressors, which are M2, INF, MPR and UNEMP. The fundamental assumption of the model of the paper is time series stationarity. Thus, since economic time series are non-stationary, the paper avoided spurious results by utilising ADF test.

The model is specified thus:

Following the example Chukwuemeka (2022), this research constructed an empirical model to investigate the influence of monetary policy and unemployment rate in Nigeria. The equation 1 presents the model used by Chukwuemeka (2022).

UNEMP = f(PRIME, MRR, EXR) Eqn. (1)

UNEMP is the Unemployment rate, PRIME is the Prime rate, MRR is the Minimum rediscount rate EXR is the Exchange rate. The present work established a unique model by implementing certain alterations to Equation 1. The research included money supply, inflation and monetary policy rate. Therefore, the mathematical expression employed for this investigation is precisely defined in Equation 2.

UNEMP = f(M2, INF, MPR) Eqn.2

Where

UNEMP is the Unemployment rate, M2 is the money supply, INF is the inflation rate and MPR is the monetary policy rate.

Explicit stated

UMP = βo + β1 M2 + + β2INF + β3MPR +Ut2 Eq.3

Where 1a 2a, 3a, and 4a are the coefficient of UNEMP, M2, INF and MPR respectively, while 0a represents the constant value called intercept or constant.

Data Presentation and Analysis

This section presents the data utilized in the paper and the results of the analysis conducted to understand the impact of monetary policy on unemployment reduction in Nigeria. The analysis includes descriptive statistics, unit root tests, the specification of the ARDL model, and the interpretation of the estimated short-run and long-run relationships.

Table 1: Summary of Descriptive Statistics for the Variables

| UMP | MS | INF | MPR | |

| Mean | 4.186042 | 9.213739 | 13.37500 | 16.88647 |

| Median | 3.810500 | 9.546256 | 13.40000 | 16.90279 |

| Maximum | 5.700000 | 10.78854 | 22.90000 | 24.85000 |

| Minimum | 3.507000 | 6.778167 | 5.400000 | 11.48313 |

| Std. Dev | 0.701321 | 1.258255 | 4.538915 | 2.941262 |

| Skewness | 1.079961 | -0.538975 | 0.241621 | 0.234310 |

| Kurtosis | 2.611613 | 1.927766 | 2.436433 | 4.000966 |

| Jarque Bera | 4.816112 | 2.311663 | 0.551130 | 1.221538 |

| Probability | 0.089990 | 0.314796 | 0.759143 | 0.542933 |

Source: Researcher’s computation, using E-views 12, 2025

The above table 1 shows that MPR had the highest mean of 16.88647, followed by the INF 13.37500, then MS had a 9.213739, the least is UMP with a mean value of, 4.186042. Also the median descriptive statistics shows that MPR, had the highest value of 16.90279, followed by INF with a value of 13.40000. The least median value was 9.546256, followed by UMP, 3.810500. The highest maximum value was MPR with a figure of 24.85000, followed by the INF 22.90000, the least maximum value is 10.78854 which is MS, followed by 5.700000 of UMP. The variable with the highest minimum value is MPR, with a value of 11.48313, followed by 6.778167 of MS. The variable with the least minimum value is INF, with a value of 5.400000, followed by 3.507000 of UMP. The variable with the highest standard deviation is INF with a value of 4.538915, followed by MPR with a value of 2.941262 and MS of 1.258255. The variable with the least standard deviation is UMP with a value of 0.701321.

Table 2: Summary of Unit Root Test Results

| Variables | ADF | ||

| ADF Values | Critical Values | Order of Int. | |

| UMP | -4.035745 | -3.690814 | 1 |

| MS | -4.333468 | -3.632896 | 1 |

| INF | -3.043853 | -2.998064 | 0 |

| MPR | -5.285046 | -3.632896 | 1 |

Source: Researcher’s computation, using E-views 12, 2025

Table 2 shows the stationary test of the variables used in this study and the results revealed that the variables were integrated at order one 1(1) except for inflation which shows unit root at level. Unemployment rate shows unit roots at first difference and money supply (MS), monetary policy rate (MPR) show at first difference. This implies that they were stationary at the first difference. Therefore, the paper went further to test for the long-run relationship by testing the co-integration using the autoregressive distributed lag model error correction test.

Table 3: Summary of Bound Test

| F-Bounds Test | Null Hypothesis: No levels relationship | |||

| Test Statistic | Value | Signif. | I(0) | I(1) |

| F-statistic | 11.62055 | 10% | 2.01 | 3.1 |

| k | 3 | 5% | 2.45 | 3.63 |

| 2.5% | 2.87 | 4.16 | ||

| 1% | 3.42 | 4.84 | ||

Source: Researcher’s computation, using E-views 12, 2025

The test result obtained from the study cointegration test revealed that the F-statistic value (11.62055) exceeds both the lower (I(0)) and higher (I(1)) critical values of 2.45 and 3.63, respectively, at the 5% significance level. The stud therefore rejects the null hypothesis of a long-term association at the 5% significance. It is therefore concluded that the variables are co-integrated, indicating a long-term equilibrium link between monetary policy and unemployment from 2000 to 2023.

Table 4: Summary of ARDL-ECM

| Variable | Coefficient | Std. Error | T. Statistics | Probability |

| D(UMP(-1)) | -2.373669 | 0.410249 | -5.785919 | 0.0012 |

| D(KMS) | -5.983415 | 0.774945 | -7.721079 | 0.0002 |

| D(INF) | 0.222881 | 0.031475 | 7.081108 | 0.0004 |

| D(MPR) | -0.514125 | 0.062485 | -8.227945 | 0.0002 |

| R-squared | 0.933166 | |||

| Adjusted R-squared | 0.851479 | |||

| Prob(F-statistic) | 0.000000 | |||

| Long run ARDL | ||||

| Variable | Coefficient | Std. Error | T.Statistics | Probability |

| KMS | 0.326431 | 0.021986 | 14.84733 | 0.0000 |

| INF | 0.188417 | 0.022876 | 8.236546 | 0.0002 |

| MPR | -0.083055 | 0.016958 | -4.897763 | 0.0027 |

Source: Researcher’s computation, using E-views 12, 2025

In the above table, which is a test for the ARDL-ECM, it can be seen that ratio of unemployment rate contributed negatively and significantly to economic growth, in the period as captured by its coefficient value of -2.373669 and a p-value of 0.0012. Further, it was found that money supply contributed negatively to economic growth as captured by its negative coefficient values of -5.983415 and a p-value of 0.0002 which was statistically significant under the period of investigation. Inflation rate with a positive coefficient of 0.222881 and a p-value of 0.0004 means that there is a positive and significant relationship with economic growth during the period. The variable of MPR was seen to be negatively associated with the coefficient value (-0.514125) with UMP meaning that there is a negative relationship between MPR and unemployment. Also, the P-value of the F-statistics of the model is significant indicating a goodness of fit of the model. Furthermore, R-squared of 0.933166suggests that about 93% of variation in INF is explained by the model while 7% is explained by variables outside the model.

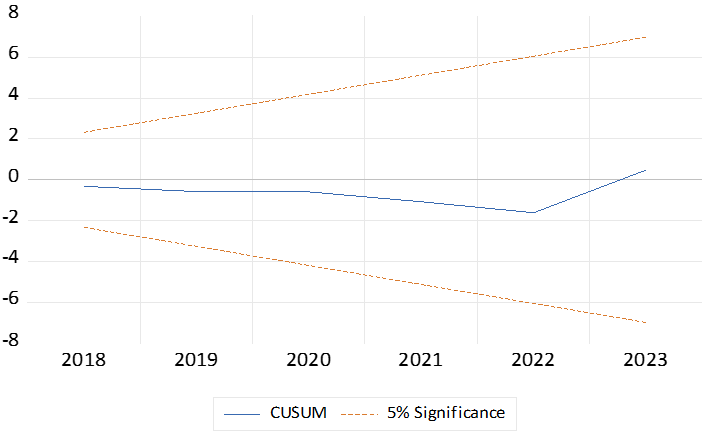

Cusum Test

Figure 1: Cusum Test

The results of the CUSUM test indicate that the model is well-fitted, as the test line remains within the upper and lower bounds throughout the sample period. This outcome suggests that the coefficients in the model are stable over time, meaning the relationships between the variables do not change significantly during the period under study. Stability in the model’s coefficients is crucial, as it implies that the model’s predictions are reliable and consistent across different time frames, without being influenced by potential structural breaks or sudden changes in the underlying economic conditions. This reinforces the credibility of our findings, showing that the model we have constructed is robust and dependable for explaining the relationships between the variables in question.

Table 5: Diagnostic test

| Test type | F-Statistics |

| Heteroskedasticity Test | 0.6453 |

| Breusch-Godfrey Serial Correlation LM | 0.0877 |

Source: Authors compilation, 2025 (Eviews-12)

The diagnostic test result indicates that the residuals of the ARDL specification are not affected by auto-correlation, heteroskedasticity or misspecification.

Table 6: ECM Result

| Variable | Coefficient | Std. Error | T. statistics | Probability |

| CointEq(-1)* | -2.373669 | 0.284270 | -8.350049 | 0.0002 |

Source: Authors compilation, 2025 (Eviews-12)

From the above result ECM is statistically significant, although greater than one and negative which shows a high adjustment speed exist in the longrun from the short run of the model.

DISCUSSION OF FINDINGS

From the result presented in Table 4 of the estimated long-run coefficients using the ARDL approach, it showed that the coefficient of broad money supply is positive and significant at the 5% level of significance. Hence, an increase in broad money supply would reduce unemployment. Broad money supply as earlier defined includes currency in circulation, demand deposit, savings and fixed deposits as well as other assets that are in spendable form. Economic theory posits that an increase in money supply will raise the domestic price level to a larger degree in the long-run, thus lowering the unemployment rate of labour and capital. The result of this study is in sharp contrast with the findings of Bassey (2017) that showed that the relationship between broad money supply and unemployment rate is positive and negative money supply growth shocks. However, the results show that money supply plays a vital role and showed that there is a significant pass-through effect of the money supply growth to unemployment rate in the long-run, this is in collaboration with the submissions of Sanz-Bas (2011). In real terms, once the amount of money supply in circulation is higher than the level of total output of the economy, it is seen as excess money supply; it does so through the control of the base money made up of currency and coins outside the banking system and deposits of banks with the Central Bank of Nigeria. In addition, the Central Bank of Nigeria regulates money supply based on the knowledge that there is a stable relationship between the quantity of money supply and economic activity.

This paper found that monetary policy rate (MPR) has significant negative impact on unemployment rate in Nigeria. This is confirmed by the ARDL regression result as presented in table 4, the coefficient of the monetary policy rate variables is -0.083055, and the p-value of the population parameter (t-stat) for monetary policy rate (MPR) is (0.0027), this implies that 1 percent increase in the monetary policy rate decreased the unemployment rate by 0.8% within the period under study. This result is in consonance with the findings of Aliu (2022) which examined the effectiveness of monetary policy in stimulating economic growth in Nigeria between 1990 and 2019 and found that there is negative influence of monetary policy rate on the rate of unemployment. The increase in monetary policy rate seems to escalate unemployment rate, this is the justification for the negative correlation and influence. Importantly, the two key policies for achieving full employment are fiscal policy and monetary policy. Fiscal policy can be seen as the use of government collected taxes and expenditure to influence the aggregate spending in an economy which is the crucial cause of unemployment (Oloye, 2012). In Nigeria, despite several fiscal policy measures, used by government to curb unemployment, yet the issue has been on the rise. Statistically, unemployment rate rose sharply from 3.9% in 1998. This ugly upward spree continued till 2011 when unemployment peaked 23.9%. Although downward trend was observed in 2012, 2013 and 2014 as unemployment recorded 10.6% 10% and 7.8% respectively, a sharp reversal was experienced in the following years as unemployment recorded 9.9% and 12.1% and 23.1% in 2017 and 2018 respectively. As at 2020, unemployment rate rose to 33.7 (NBS, 2020).

The coefficient of inflation was positive and significant according to the findings of this paper. The Philips curve shows the inverse trade-off between inflation rate and unemployment. If unemployment is high, inflation will be low. If unemployment is low, inflation will be high. The Phillips curve shows that lower unemployment can only be achieved through expansionary policies, which increases the money supply and lead to higher inflation. The derived results show that the Philips curve hold in Nigeria by inflation having a positive and significant relationship with unemployment during the period of investigation, this is in contrast with the findings of Eyone et al., (2024) who found a negative and insignificant association with unemployment.

CONCLUSIONS AND RECOMMENDATIONS

This paper examined the impact of monetary policy on unemployment reduction in Nigeria from 2000 to 2023. Basically, there are three major specific objectives to shape the discussion of the findings of this study- (i) to investigate the impact of broad money supply, inflation rate and monetary policy rate on unemployment rate in Nigeria. From the tested hypothesis, the null hypothesis was rejected (P (0.0002). It was concluded that there is a significant impact of money supply, inflation rate and monetary policy rate on unemployment in Nigeria. This implies policy measure that would promote and sustain the monetary policy aggregate that will help reduce unemployment in Nigeria. This calls for sound monetary policy to promote macroeconomic stability, manage inflation and promote sustainable growth. This would involve designing policies to help control the fluctuations in employment levels, prices and production. The coefficient of money supply is positive and significant. This implies that an increase in broad money supply would reduce unemployment. In conclusion to objective two, to investigate the impact of inflation on unemployment reduction in Nigeria, it was shown from the result that inflation rate has a positive and significant relationship with unemployment, this implies monetary authorities to adopt a monetary stance that will reduce inflation and/or create and sustain an enabling environment for entrepreneurs and innovation that can unlock the full potential of Nigerians by empowering to build and grow their business through availability of reduced inflation; which invariably means that investors can buy so much more with the money they have i.e, value thus, boosting the activities of the investors, hence reduction in unemployment in Nigeria. Inflation rate has positive and significant relationship with unemployment. This implies that inflation rate has the structural potential to reduce unemployment if kept at a stable and single digit.

In consonance to objective three, the increase in monetary policy rate seems to escalate unemployment rate, as this reduces the amount of credit or loan available to investors who are willing to borrow money to do business. Thus, from the findings of this paper monetary policy rate has a negative but significant relationship with unemployment; for MPR to be significant during the period of investigation implies that the monetary authorities needs to adopts policies that will reduce drastically MPR rate to enable money or credit to be accessible or available to individuals and investors, thus reducing unemployment. The coefficient of monetary policy rate was negative and significant. This implies that a decrease in monetary policy rate will would reduce unemployment.

On the basis of the empirical findings the following recommendations are proffered;

- The money supply should be increased significantly by the central bank of Nigeria so that there will be money in the economy, this will lead to increase in employment, poverty reduction, improve standard of living amongst others.

- Monetary policy authorities should ensure that there is a significant fall in inflation rate which will lead to an increase in the growth of the economy.

- It is therefore recommended that to curb unemployment using the interest rate channel, the monetary authority (Monetary Policy Committee) should ease the MPR by a higher magnitude compared to the magnitude that is required to tighten it for the purpose of price stability.

REFERENCES

- Abayomi, O., (2022). Macroeconomic Setting in Nigeria; Post-Graduate Lecture Series, Department of Economics, Bingham University, Karu, Nasarawa State.

- Adeagbo, M. O. (2021). Monetary policy and economic growth nexus in Nigeria. Ianna Journal of Interdisciplinary Studies, 3(2).

- Aganga, O. (2010). Rising Unemployment Rate is Unacceptable – Goodluck Jonathan. Business Facts and Figures Magazine September, 15.

- Aliu, T. I. (2022) Effectiveness of monetary policy in stimulating economic growth in Nigeria. International Journal for research in social science and humanities (IJRSS).

- Amasomma, D. (2015). The efficacy of monetary policy variables in reducing unemployment in Nigeria, International Finance and Banking, 2(2), 52-71.

- Attan, J.A., Effiong, U.E. &Okon, J.I. (2019). Is monetary policy a veritable tool for tackling the problem of unemployment in Nigeria? International Journal of Educational Research and Management Technology 4(4): 13-29.

- Bassey, K.J. (2017). Money supply growth and unemployment rate in Nigeria: Investigating a long-run relationship using asymmetric ARDL approach. West African Journal of Monetary and Economic Integration. West African Monetary Institute, 17(1), 45-60.

- Blair, F. (2023). Economies from the Top Down: new ideas in Economics and the Social Sciences.

- Chinonye E. O. (2022). The impact of fiscal and monetary policy on unemployment rate in Nigeria (1981- 2020), Eco Res & Rev, 2(3), 226-235.

- Chukwuemeka N. (2022). Monetary policy and unemployment rate in Nigeria, World Journal of Advanced Research and Reviews, 15(03), 248–255.

- Effiong, U.E., Ekpe, J.P. & Udofia, M.A.(2022) An empirical examination of the influence of private sector credit on unemployment in Nigeria. International Journal of Academic Multidisciplinary Research, 6(9), 187-199.

- Effiong, U.E., Udofia, M.A., & Ekpe, J.P. (2022). Labour underutilization and output degeneration in Nigeria: Empriical evidence from a traditional production function. International Journal of Academic Management Science Research, 6(8), 38-54.

- Ekwe, E. I. (2018). The impact of monetary policies on Nigeria’s unemployment: Lessons for Poverty Reduction in Nigeria, Equatorial Journal of Finance and Management Sciences, 3 (1):1-16.

- Ekwe, I.E. (2018). The impact of monetary policies on Nigeria’s unemployment: Lessons for poverty reduction in Nigeria. Equational Journal of Finance and Management Sciences, 3(1), 1-16.

- Eyone, A.U ., Kalu, C.U., Metu, G.A &Maduka, D.O. (2024). Monetary Policy Pass-Through to Unemployment Reduction in Nigeria, Journal of Social Sciences & Humanities, 9(2).

- Fasanya, I.O., Onakoya, A.B. & Agboluage, M.A. (2013). Does monetary policy influence economic growth in Nigeria? Asian Economic and Financial Review, 3(5), 635-646.

- Gideon G. G. & Paul T. I. (2020). Measuring the asymmetric pass-through of monetary policy rate to unemployment in Nigeria: Evidence from Nonlinear ARDL, Nigerian Journal of Economic and Social Studies, 62(3).

- Gideon G. G. & Paul T. I., (2020). Measuring the asymmetric pass-through of monetary policy rate to unemployment in Nigeria, Nigerian Journal of Economic and Social Studies, 62(3).

- Linus, E., Nse-Abasi, I. E., &Itoro, M. I., (2024). Monetary policy measures and unemployment dynamics in Nigeria, African Banking and Finance Review Journal (ABFRJ), 13(13).

- National Bureau of Statistics (2019) Reports. www.nigerianstat.gov.ng.

- Ndife, C. F. (2020). Impact of Monetary Policy on Economic Growth of Nigeria. African Scholar Publications & Research International, 18(7) ISSN: 2276-0732.

- Nigerian Economic Summit Group, (NESG) 2018.

- Nwamuo, C. (2022). Monetary policy and unemployment rate in Nigeria: An empirical investigation. World Journal of Advanced Research and Reviews, 15(3), 248-255.

- Nwosa, P. (2016). Impact of macroeconomics policies on poverty and unemployment rates in Nigeria: Implications for attaining inclusive growth. ActaUnivDanubiusEconomusa12: 114-126.

- Ogunmade, O. (2013). $600bn Stolen by Nigerian Elite since Independence. ThisDayLIVE. www.thisdaylive.com/article/$600bnstolen-by-nigerian-elite.

- Okeke, I. C. & Chukwu, K. O. (2020). Effect of monetary policy on the rate of unemployment in Nigerian economy, Journal of Global Accounting 7 (1).

- Okeke, I. C. & Chukwu, K. O. (2021). Effect of monetary policy on the rate of unemployment in Nigerian economy. Journal of Global Accounting, 7 (1).

- Okeke, I.C. & Chukwu, K.O. (2021). Effect of monetary policy on the rate of unemployment in Nigeria economy (1986-2018), Journal of Global Accounting. 7(1), 1-13.

- Okoro, A. S. (2015). Impact of monetary policy on Nigeria Economic Growth. Prime Journal of Social Sciences, 2 (2), 195-199.

- Onwuka, C.E. (2022). The impact of fiscal and monetary policy on unemployment rate in Nigeria (1981-2020). Journal of Economic Research and Review, 2(3), 226-235.

- Onyeiwu, C. (2012). Monetary policy and economic growth of Nigeria. Journal of Economics and Sustainable Development, 3 (7), 1-21.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approach to the analysis of level relationships. Journal of Applied Econometrics, 16 (2), 289-326.

- Philip N. (2016). Impact of macroeconomic policies on poverty and unemployment rates in Nigeria, implications for attaining inclusive growth, Acta Universitatis Danubius, 12(6).

- Sanz-Bas, D. (2011). Heyek’s critique of the general theory: A new view of the debate between Hayek and Keynes, The Quarterly Journal of Austrian Economics, 14(3), 11-25.

- Sunday N. E., Garba A. M., Mary O. A. A., Kufre J. B., Suleiman F. O., Deborah G. O., & Francisca O., (2016). Monetary policy and unemployment in Nigeria: Is there a Dynamic Relationship? CBN Journal of Applied Statistics,7(1(b).

- Udude, C.C. (2015). Monetary policy and balance of payment in Nigeria (1981-2012), Journal of Policy and Development Studies, 9(2), 14-26.

- Ufoeze, L., Odimgbe, S.O., Ezeabalisi, V.N. &Alajekwu, U.B. (2018). Effect of monetary policy on economic growth in Nigeria: An empirical investigations. Annuals of SpiruHaret University. Issn: 2393-1795.

- Zhou, Y. Y. (2021). Monetary Policy and Unemployment—A Study on the Relationship Exists in the United States. Open Journal of Social Sciences, 9, 306-322. https://doi.org/10.4236/jss.2021.94024.