Inflation and Macroeconomic Performance in Nigeria

- Ekekwe, Mary Obiageli.

- Njoku, Ndubuisi Felix

- 2186-2199

- Jul 31, 2024

- Economics

Inflation and Macroeconomic Performance in Nigeria

1Ekekwe, Mary Obiageli., 2Njoku, Ndubuisi Felix

1Department of Economics, Ignatius Ajuru University of Education, Rivers State, Nigeria.

2Department of Economics Michael Okpara University of Agriculture Umudike, Abia State, Nigeria.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.803159S

Received: 11 June 2024; Accepted: 22 June 2024; Published: 31 July 2024

ABSTRACT

In Nigeria, high inflation has been one of the major challenges facing the nation’s economy. This has necessitated the re-evaluation of the impact of inflation on the nation’s macroeconomic performance between 1981 and 2022. The data utilized were sourced from the secondary sources like Central Bank of Nigeria Statistical Bulletin 2022 and United Nations Conference on Trade and Development Report. The inflation rate, exchange rate, and interest rate served as independent variables, while per capita income and gross fixed capital formation (proxy for private investment) served as the dependent variables. The outcome of the unit root tests showed that all the variables were not stationarity at level, but became stationary after first difference which informed the use of Error Correction Model (ECM) test approach. The results from the per capita income model, revealed that an increase in inflation rate, exchange rate and interest rate erodes the value of the per capita income of the citizens. The result from the private investment model, showed that an increase in inflation rate, exchange rate, and interest rate reduces the level of private domestic investment. The policy implication of these results is that negative impact of inflation on these key macroeconomic indicators suggests that high or volatile inflation rates can hinder economic growth and development. The paper therefore recommends amongst others, that the central bank should adopt appropriate monetary policies aimed at controlling inflation rates within acceptable levels. This may involve adjusting interest rates, managing money supply, and employing other monetary tools to stabilize prices. Furthermore, government should prioritize fiscal discipline and prudent spending to avoid excessive budget deficits that can fuel inflationary pressures and allocate funds towards productive investments and infrastructure projects that stimulates economic growth without exacerbating inflation.

Key Words: Inflation Rate, Per Capita Income, Private Investment

INTRODUCTION

Inflation is a crucial economic indicator that measures the rate at which economic prices increase over time. High levels of inflation can have detrimental effects on the macroeconomic performance of Nigeria. These effects include eroding the purchasing power of consumers, reducing investment and savings, distorting resource allocation, and creating uncertainty in the business environment. One possible cause of inflation in Nigeria is the excessive growth in money supply. This can lead to an increase in aggregate demand, which puts upward pressure on prices. However, inflation in Nigeria can also be driven by external factors such as oil price changes, which significantly impact the country’s economy. The inflationary trend in Nigeria has been persistent over the years, with single-digit inflation maintained for only a limited period. During periods of high inflation, the Nigerian government has implemented measures such as effective monetary policy, fiscal prudence, and exchange rate stabilization to curb the rising inflation rate (Onifade et al., 2020). These measures aim to strike a balance between stimulating economic growth and maintaining price stability. However, the effectiveness of these measures has been debated (Okoye et al., 2019). Some economists believe that in less developed economies like Nigeria, the effectiveness of monetary policy in reducing inflationary pressure may be limited due to the underdeveloped financial markets and lack of diverse financial instruments (Korgbeelo & Nwiado, 2021).

Inflation is the rate at which the general level of prices for goods and services in an economy is rising over time, leading to a decrease in the purchasing power of a currency. It is often expressed as a percentage and measured on an annual basis. Inflation reflects the erosion of the real value of money, as the same amount of currency buys fewer goods and services over time. Central banks and policymakers generally aim to maintain a moderate level of inflation, as low and stable inflation is considered conducive to economic stability. Mild inflation encourages spending and investment, while deflation (negative inflation) can lead to economic stagnation as consumers and businesses postpone purchases in anticipation of lower prices in the future. Various factors contribute to inflation, including increased demand for goods and services, supply shocks, and changes in production costs. Economists distinguish between different types of inflation, such as demand-pull inflation and cost-push inflation, depending on the underlying causes. Managing inflation is a key consideration in monetary policy, and central banks use tools like interest rates to influence the level of inflation in an economy.

In Nigeria, high inflation has been one of the major challenges facing the nation’s economy. The inability of the government to proffer a lasting solution to this problem indicates the inevitability of inflation in the economy; hence, it shows that the government lacks the power to eliminate the persistent rising prices of goods and services in the domestic economy (Taiwo, 2011). Inflation in Nigeria can be traced to 1950s, though not prevalent then. Scholars have argued that during an inflationary period, domestic currency finds it difficult to act as a medium of exchange and a store of value without adversely affecting the output level, income distribution, and employment level of the country (CBN, 1984). Inflation leads to currency depreciation and a rise in foreign exchange rates. This is the case of the Naira as it has depreciated over time against the US dollar and other major foreign currencies. For example, the naira exchange rate was ₦0.61 per US dollar in 1981 and depreciated to ₦2.0206 to a dollar in 1986. In 1991, the exchange rate depreciated to ₦9.9095 per dollar, and further depreciated to ₦21.886, ₦111.9433, ₦128.6516, ₦153.8616 and ₦199.268 in 1996, 2001, 2006, 2011 and 2015 respectively. However, the corresponding rate of inflation in 1981 stood at 20.8% in Nigeria; and in 1986, the inflation rate declined to 5.7%, and increased to 13.0% in 1990. By 1996, the rate of inflation again rose to 29.3%; in 2001 and 2006, the rates of inflation were 18.9% and 8.2% respectively; and it was 10.8% and 9.0% in 2011 and 2015 respectively (CBN, 2015). More so, the growth rate of real gross domestic product (RGDP) in 1981 was -20.4%; in 1986, the growth rate of RGDP rose to 1.9%, and declined to 0.01% in 1991. By 1996, 2001, 2006, 2011, and 2015, the growth rates of the RGDP were 4.1%, 9.8%, 6.0%, 7.4% and 3.9% respectively (CBN, 2015). As of May 31st, 2023, the inflation rate in Nigeria has reached 22.22%, which marked an increase from the 22.04% recorded at the end of the 1st quarter. This surge represents the highest inflation rate witnessed in the country over the past 20 years.

In the words of Taiwo (2011), inflation in Nigeria has become a major threat to economic activities, especially on workers whose standard of living declines continuously. The inflationary factors traced to Nigeria’s high inflation include continuous hikes in petroleum prices and exchange rate depreciation/devaluation. These increases in the two variables (the price of petroleum and exchange rate depreciation) have been blamed for the increases in transportation costs, input materials, foodstuffs, rents, and goods and services coupled with the exchange rate depreciation in Nigeria. Inflation in an economy can be measured using the consumer price index approach and the wholesale or producer price index approach. The period-to-period changes in wholesale or producer price index are used as direct measures of inflation, though not the best measure of inflation in Nigeria. The Central Bank of Nigeria (CBN) often adopts monetary policies to achieve price stability, as well as sustainable economic growth. According to Sani and Abdullahi (2011), the monetary authorities in an attempt to achieve the overall inflation objective of the government via effective monetary management, sets intermediate and operating targets that are in line with the targets for GDP growth, inflation rate, and balance of payments. Yet, despite all the monetary policies adopted by the monetary authorities to reduce high inflation in Nigeria, the rate of inflation in the country is still high with the standard of living of the citizens decreasing continuously. It is against this background that this paper investigates the effect of inflation on the macroeconomic performance in Nigeria for the period of 1980-2023.

The broad objective of this paper is to re-evaluate the effect of Inflation on the macroeconomic performance in Nigeria from 1981 to 2022. Specifically,

- To ascertain the effect of Inflation rate, Exchange Rate and Interest Rate on Per Capita Income in Nigeria.

- To investigate the effect of Inflation rate, Exchange Rate and Interest Rate on Private Domestic Investment in Nigeria.

- To analyse the trend of Inflation rate in Nigeria.

The paper is structured as follows: Section one is the introduction, section two consists of the related literature review, while section three highlights on the research method adopted. Sections four and five present the data presentation and analysis; the summary, discussion of the findings of paper and policy recommendations. Also included are the contributions of the study to already body of knowledge and limitation of the study.

EMPIRICAL LITERATURE REVIEW

Nookhwun and Waiyawatjakorn (2024) assessed the impact of flexible inflation targeting on macroeconomic performance in ASEAN-5 countries. The study aimed to analyze how adopting inflation targeting frameworks influenced inflation levels, economic growth stability, and the functioning of the financial system. The study utilized a difference-in-difference approach to compare the macroeconomic outcomes of countries that adopted inflation targeting frameworks with those that did not. The findings indicated that flexible inflation targeting in ASEAN-5 countries led to lower levels and volatility of inflation, more stable economic growth, and a well-functioning financial system. The study recommended the importance of reducing inflation levels and volatility, promoting stable economic growth, and ensuring the efficient functioning of the financial system as key objectives of flexible inflation targeting. Ahmed (2024) investigated the impact of inflation and exchange rates on the balance of payments. The study focused on analysing the relationship between inflation, exchange rates, and the balance of payments. By examining these economic variables, the research aimed to provide insights into how inflation and exchange rate fluctuations can influence a country’s balance of payments position. The study utilized a descriptive, analytical, and standard approach. The study findings indicated that an increase in inflation rates leads to a rise in the exchange rate deficit, subsequently causing a deficit in the balance of payments. The study also highlighted that high prices can result in a decrease in the volume of real money, leading individuals to convert their interest-bearing financial assets into cash. The study recommended implementing effective monetary policies to control inflation rates and stabilize exchange rates can help mitigate the negative impact on the balance of payments. Fitri and Syamsuri (2024) addressed theoretical gaps related to Indonesian inflation and its impact on economic growth. The study is focused on analysing the relationship between inflation and economic growth specifically in the context of Indonesia. The method employed in the study is a literature review to gather and analyze existing information, theories, and studies on inflation and economic growth in Indonesia. The study emphasizes the importance of stable and low inflation for economic growth in Indonesia. The study recommended for Indonesia to continue moving towards stability, quality, and sustainability in its economic policies. Bilall and Sadiku (2023) investigate the impact of inflation on financial sector performance in Western Balkan countries. The study aims to understand how macroeconomic factors like inflation, GDP growth, government expenditure, trade, and lending interest rates affect credit to the private sector. The research methodology includes panel regression models such as OLS, OLS robust, Fixed effects, Random effects, and Generalized method of moments (GMM) to analyze the data provided by the World Bank and the Central Banks of the Western Balkan countries from 2002 to 2021. The findings indicated a positive correlation between domestic credit to the private sector and inflation, while broad money shows a negative correlation with inflation in Western Balkan countries. The study recommended that policymakers to monitor and adjust lending interest rates in response to inflation levels, as fluctuations in inflation can influence the cost of borrowing and lending, affecting overall financial sector performance. Therefore, interest rate policies should be adaptable to inflation dynamics. Ogini (2022) examined the effect of selected macroeconomic variables on per capita income in Nigeria. Specifically, the study aims to determine the effect of money supply, exchange rate, interest rate, inflation rate, and unemployment rate on per capita income in Nigeria. The study employed econometric techniques, including Descriptive Statistics, Augmented Dickey Fuller for unit root, and the Autoregressive Distributive Lag (ARDL). Granger causality test and cointegration analysis were also used to investigate the existence of long-run relationships. The findings revealed that money supply, exchange rate, interest rate, inflation rate, and unemployment rate have significant policy effects on the standard of living of an average Nigerian in both the short run and the long run. The study concludes that selected macroeconomic variables have been effective policy instruments that largely influence per capita income in Nigeria. Based on the objective and findings of the study, the study recommended for an expansionary monetary policy to increase money supply, safeguarding the value of the domestic currency by reducing interest rates to encourage credit and boost productivity. Oluwole and Ushie (2022) evaluated the effect of interest rate liberalization on investment in Nigeria. The study used Autoregressive Distributed Lag (ARDL) and bound test for the long run Co-Integration. it was found that interest rate had an insignificant and negative effect on domestic investment, while savings and lending rate had a positive and significant effect on domestic investment in Nigeria. The study concludes that interest rate plays a significant role in the economy and recommends enhancing the investment position of the nation for sustainable growth and development. Wanjiru, Mutur, and Njeru (2021) evaluated the effect of selected macroeconomic variables on the growth of domestic private investment. The study used a time series quarterly data spanning 1997 to 2018. Autoregressive Distributed Lag (ARDL) model was adopted to examine if changes in select macroeconomic variables determine the growth of domestic private investment in Kenya. The long-run cointegrating model estimated showed that private domestic investment varies significantly and negatively with the central bank rate and the commercial lending rate. However, an increase in the money supply increases the level of investment. Moderate inflation is also found to be critical in increasing the level of investment. The study suggested that monetary policy conduct is essential in driving private domestic investment. Onwubuariri, Oladeji and Bank-Ola (2020) evaluated the impact of inflation on Nigeria’s economic growth over the past four decades. The study employed the Autoregressive Distribution Lag (ARDL) model and the Error Correction Model (ECM) to analyse the data. The result showed that inflation has negatively affected economic growth in Nigeria over the years, while interest rate maintains a positive relationship with economic growth. Government consumption is found to be insignificant in the growth of the economy. The study suggested that measures should be put in place by the Central Bank of Nigeria (CBN) through the Monetary Policy Committee to reduce the rate of inflation to the barest minimum. Ogu, Adagiri, and Abdulsalam (2020) sought to determine the impact of inflation and interest rate on economic growth in Nigeria. The study adopts the Ordinary Least Square (OLS) regression technique. The study found that inflation has a positive but not significant impact on economic growth in Nigeria. On the other hand, interest rate has a negative and significant effect on economic growth in Nigeria. The study recommended implementing efficient tax policies, policies to support consumers, and achieving a one-digit interest rate. Mogaji, Falade, and Ogundipe (2020) examined the interrelationship between inflation, interest rate, and domestic investment in Nigeria. The study employed the Augmented Dickey Fuller (ADF) and Phillip Peron (PP) unit root tests, Johansen Co-integration, and the Auto-Regressive Distributed Lag (ARDL) approach. The result revealed that the previous performance of domestic investment and inflation rate increased domestic investment, while interest rate and public expenditure reduced it. The study recommended that the government should formulate policies to encourage local investors by spending more on infrastructure and implementing regular interest rate reforms to discourage large disparities between lending and deposit rates. Ezeibekwe (2020) examined how changes in the inflation rate affect the ability of monetary policy tools to stabilize the Nigerian economy and stimulate investment. The study applied the Vector Error Correction Model to analyze the relationship between inflation rate, interest rates, money supply, and investment in Nigeria. The empirical results suggested that the impact of interest rates on investment depends on the level of the inflation rate. The effect of interest rates on investment gets weaker as the inflation rate increases. On the other hand, the impact of the money supply target on investment does not depend on the level of the inflation rate. The study highlighted the importance of considering the inflation rate when using monetary policy tools to stimulate investment. It also emphasizes the need to deepen the scale, capacity, and efficiency of open market operations in Nigeria. The study recommended that the Central Bank of Nigeria should work on improving the participation and reducing transaction costs in open market operations. They also suggest making different financial instruments available to enhance the effectiveness of monetary policy in stabilizing the economy and stimulating investment. Oniore, Gyang, and Nnadi, (2016) analysed the link between exchange rate fluctuations and private domestic investment in Nigeria. The study employed descriptive statistics and econometric methods. Simple averages of descriptive statistics and the Error Correction Model (ECM) technique within the Ordinary Least Square estimation are used to analysed the data. The findings suggested that the depreciation of the currency and interest rate do not stimulate private domestic investment activities in Nigeria. On the other hand, infrastructures, government size, and inflation rate have a positive effect on private domestic investment. The research highlights the need for appropriate policies to appreciate the value of the naira, reduce borrowing and lending charges, and create a stable macroeconomic environment to boost private domestic investment. The study further recommended that monetary authorities adopt appropriate policies to appreciate the value of the naira, reduce borrowing and lending charges, and create a stable macroeconomic environment to boost private domestic investment. Khalid, Khursheed and Mohi-u-Din (2015) analysed the impact of inflation on per capita income in emerging economies, specifically focusing on the BRICS nations. The study employed a regression model to analyse the data from 1999 to 2011. They used the data from five major emerging countries, namely India, Brazil, South Africa, China, and Russia, which are members of BRICS. The results of the study showed that inflation did not statistically influence per capita income in India, Brazil, and South Africa. However, in China and Russia, inflation was found to have a statistically significant impact on per capita income. Therefore, the study concluded that a change in the inflation rate may not necessarily lead to a change in per capita income.

Based on the survey of extant of literatures so far reviewed, there seems to be divergent views amongst scholars. Thus, this paper deviates from them by utilizing per capita income and private investment as macroeconomic performance indicators due to their ability to provide nuanced insights into the economic well-being and growth prospects of a nation. While indicators like economic growth, balance of payments, unemployment, interest rate and exchange rates which dominates the literatures are certainly important, they often reflect broader trends in the economy and may not capture the intricacies of income distribution and the dynamics of private sector participation.

Furthermore, the present study extends its scope to 2022 to capture the current trends and effect of inflation and to proffer appropriate policy direction that is in tandem with the global trend, which none of the reviewed literatures covered.

METHODOLOGY

3.1 Theoretical Framework

This study is anchored on the Neo-Classical Growth Theory developed in the mid-20th century by economists such as Robert Solow, Trevor Swan, and others. This theory emphasizes the role of technological progress and savings/investment decisions in determining long-term economic growth. Inflation can distort saving and investment decisions by reducing the real return on savings and distorting investment decisions. Over time, this can negatively affect per capita income growth and private investment levels. it emphasizes the importance of technological progress as a primary driver of long-term economic growth. Technological advancements allow for increases in productivity, which, in turn, lead to higher levels of output and income over time.

3.2 Model Specification

To examine the effect of inflation on the Nigeria’s macroeconomic performance, the study modifies the model developed by Onwubuariri et al., (2021) whose model is specified thus:

GDP = f (INF, INT, EXR, GOV) (3.1)

Where; GDP = Gross Domestic Product INF = Inflation Rate RINT= Real Interest Rate EXR = Exchange Rate GOV = Government Consumption Expenditure f = functional relationship.

From equation (1), the formula is further stated in an econometric form as: 𝑅𝐺𝐷𝑃 = ∝0+∝1 𝐼𝑁𝐹 +∝2 𝐼𝑁𝑇 +∝3 𝐸𝑋𝑅 +∝4 𝐺𝑂𝑉 + 𝜇 (3.2)

Where: ∝0 = Intercept of relationship in the model ∝1 – ∝5 = Coefficients of each independent or explanatory variable 𝜇 = Stochastic or Error term

This present study will extend the above equation to incorporate macroeconomic indicators such as Per Capita Income and Private Domestic Investment as the dependent variables thereby informing a two-sector model, specified thus:

PCI = f (INF, EXR, INT) (3.3)

GFCF = f (INF, EXR, INT) (3.4)

The functional forms of models for this present study are expressed below:

PCI = f (INF, EXR, INT) (3.5)

GFCF = f (INF, EXR, INT) (3.6)

The multiplicative forms of equations (5) and (6) are stated as:

![]() (3.5)

(3.5)

![]() (3.6)

(3.6)

Mathematically, the exact form of equation (7) and (8) could be expressed in the linear form:

![]() (3.7)

(3.7)

![]() (3.8)

(3.8)

Where : PCI = Per Capita Income ; INF= Inflation Rate ; EXR= Exchange Rate ; INT= Interest Rate ; GFCF= Gross Fixed Capital Formation (Proxy for Private Investment) ;![]()

3.3 Estimation Technique and Procedure

The study utilized, the Error Correction Mechanism (ECM) to examine the effect of the independent/control variables on the dependent variables. To establish whether long-run relationship exists among the variables or not, co integration tests were conducted by using the multivariate procedure developed by Johansen (1988) and Johansen and Juselius (1990) for both the Trace statistics and maximum eigenvalues.

RESULTS AND DISCUSSION

4.1 Preliminary Analysis

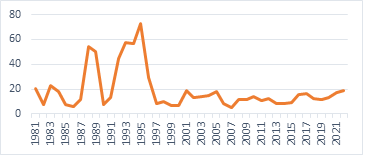

Nigeria has experienced significant fluctuations in inflation rates over the past few decades due to various economic, political, and social factors.

Between 1980s and 1990s, Nigeria faced high levels of inflation, largely attributed to factors such as poor fiscal management, excessive money printing, and political instability. Inflation rates often soared to double or even triple digits during these periods, severely eroding the purchasing power of the Nigerian currency, the Naira. In the early 2000s, Nigeria implemented various economic reforms and stabilization measures aimed at curbing inflation and stabilizing the economy. These efforts, including fiscal discipline and monetary policy adjustments, led to a gradual decline in inflation rates. Despite some periods of relative stability, inflation remained a challenge for Nigeria throughout the mid-2000s to the 2010s. Factors such as fluctuations in global oil prices (Nigeria’s primary export), currency devaluation, and economic shocks contributed to inflationary pressures. In the latter part of the 2010s and leading up to 2022, Nigeria experienced fluctuations in inflation rates. The economy grappled with challenges such as lower oil prices, foreign exchange shortages, and security concerns in certain regions. These factors, coupled with structural issues within the Nigerian economy, contributed to inflationary pressures.

Figure 1 Inflation Trend in Nigeria between 1981 and 2022

Source: The Author’s Computation (2024)

4.1.1 Descriptive Statistics

This shows a summary of statistics: the mean, median, maximum, minimum, standard deviation, kurtosis, and Jarque-Bera values for the variables under consideration. Table 1 below shows the mean value of PCI, INF, EXR, INR and GFCF are 7.52, 18.9, 3.65, 22.4 and 7.71 respectively. INF has the highest level of discrepancy, as shown in the standard deviation result. This means that inflation has become more volatile and unpredictable. PCI shows the lowest level. Skewness is a measure of the rate of asymmetry or discrepancy of the variables. Accordingly, EXR, INR, and GFCF have long left tail. This is because the variables exhibit negative values, while PCI, and INF are positively skewed. Kurtosis measures the peakedness and flatness of the series. The result shows that only INF is leptokurtic relative to their normal distribution because the value is greater than three, while PCI, EXR, INR and GFCF are platykurtic because their kurtosis values are lesser than 3. Jarque-Bera statistical test indicates the normally distributed variables as it measures the differences in skewness and kurtosis. The result shows that Jarque-Bera statistic rejects the null hypothesis of no normal distribution for all the variables. Thus, it is concluded that they are all normally distributed.

Table 1: Descriptive statistics of variables

| LOG(PCI) | INF | LOG(EXR) | INR | LOG(GFCF) | |

| Mean | 7.529177 | 18.92119 | 3.658569 | 22.47357 | 7.714573 |

| Median | 7.459675 | 12.94500 | 4.746733 | 22.46500 | 7.922833 |

| Maximum | 7.896553 | 72.84000 | 6.054392 | 36.09000 | 11.08563 |

| Minimum | 7.253470 | 5.380000 | -0.494296 | 10.00000 | 4.467516 |

| Std. Dev. | 0.238362 | 16.46575 | 2.016111 | 6.075259 | 2.021731 |

| Skewness | 0.266209 | 1.877648 | -0.818188 | -0.231169 | -0.205456 |

| Kurtosis | 1.395112 | 5.436276 | 2.427688 | 2.678688 | 1.804415 |

| Jarque-Bera | 5.003485 | 35.06596 | 5.259220 | 0.554747 | 2.796977 |

| Probability | 0.081942 | 0.000000 | 0.072107 | 0.757772 | 0.246970 |

| Sum | 316.2254 | 794.6900 | 153.6599 | 943.8900 | 324.0121 |

| Sum Sq. Dev. | 2.329472 | 11115.95 | 166.6528 | 1513.260 | 167.5832 |

| Observations | 42 | 42 | 42 | 42 | 42 |

Source: Authors’ Computation (2024) from e-view 10

4.1.2 Unit Root Tests

4.1.3 Unit Root Test Result for Per Capita Income Model

As shown in Table 2 below, the series showed that all the variables were not stationary at level. But became stationary after 1st difference. There was no autocorrelation problem amongst variables; hence, the ECM model can capture the long-run relationship among variables.

Table 2. ADF and PP Unit Root Test Result for Model One

| Variables | ADF Statistics Level | AD Statistics First Difference | PP Statistics Level | PP Statistics First Difference | Order of Integration |

| PCI | -1.164446 | -4.102933” | -0.495746 | -4.102933” | I (1) |

| INF | -3.048567 | -5.910682” | -2.915627 | -10.68364” | I (1) |

| EXR | -2.192124 | -5.419436 | -2.523348 | -5.419436 | I (1) |

| INR | -2.899830 | -7.105924 | -2.769105 | -8.998565 | I (1) |

Source: Authors’ Computation (2024) from e-view 10

4.1.4 Co integration Test

To ascertain a long-run relationship among the variables in the presence of the maximum Eigenvalues and trace statistics, the Johansen cointegration techniques was applied.

Table 3. Unrestricted Co integration Rank Test (Trace)

| Hypothesized No. of CE(s) | Eigenvalue | Trace Statistic | 0.05 Critical value | Prob ** |

| None * | 0.689140 | 72.24816 | 47.85613 | 0.0001 |

| At most 1* | 0.271291 | 29.79707 | 25.51161 | 0.0252 |

Trace test indicate 2 cointegrating eqn(s) at the 0.05 level. * denotes rejection of the hypothesis at the 0.05 level. ** Mackinnon – Haug – Michelis (1999) p-values

| Unrestricted Co integration Rank Test (Maximum Eigenvalue) | ||||

| Hypothesized No. of CE(s) | Eigenvalue | Trace Statistic | 0.05 Critical value | Prob ** |

| None * | 0.689140 | 46.73655 | 27.58434 | 0.0001 |

| At most 1 * | 0.271291 | 21.13162 | 12.65924 | 0.0252 |

Source: Authors’ Computation (2024) from e-view 10

Note: Max – eigenvalue test indicates 2 Cointegrating eqn(s) at the 0.05 level, * denotes rejection of the hypothesis at the 0.05 level, ** Mackmnon – Haugh – Michelis (1999) p values.

From the results as presented above, both the trace statistics and maximum eigenvalues showed traces of cointegrating – long-run relationship at the 5% level of significance. In order words, there exists a long-run relationship between per capita income and inflation, exchange rate, and interest rate within the reviewing period. The Error Correction Model Ordinary Least Square (OLS) are presented below. These results show the adjustment of the long run equilibrium to the short run dynamics

Table 4 Dependent Variable: DLOG(PCI)

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| D (INF (-1)) | -0.000963 | 0.000347 | -2.771573 | 0.0102 |

| D (INF (-3)) | -0.001602 | 0.000388 | -4.125661 | 0.0003 |

| DLOG (EXR) | -0.066458 | 0.015721 | -4.227233 | 0.0003 |

| DLOG (EXR (-3)) | 0.061524 | 0.016867 | 3.647585 | 0.0012 |

| D (INR) | -0.001756 | 0.001273 | -1.379864 | 0.1794 |

| D (INR (-3)) | -0.001745 | 0.001172 | -1.488907 | 0.1485 |

| ECM (-1) | -0.012207 | 0.002961 | 4.123104 | 0.0003 |

| R-squared | 0.719567 | Mean dependent var | 0.014419 | |

| Adjusted R-squared | 0.600922 | S.D. dependent var | 0.035796 | |

| S.E. of regression | 0.022614 | Akaike info criterion | -4.488450 | |

| Sum squared resid | 0.013296 | Schwarz criterion | -3.971317 | |

| Log likelihood | 97.28055 | Hannan-Quinn criter. | -4.304458 | |

| Durbin-Watson stat | 2.196589 | |||

Source: Authors’ Computation (2024) from e-view 10

From the result as presented above, the third period lag of inflation have negative and significant impact on the per capita income. This suggests that a one unit increase in inflation rate leads to a 16 unit decrease in per capita income. A negative and significant relationship is observed between exchange rate and per capita income. A one percent increase in exchange rate resulted in a 66 percent decrease in per capita income. The interest rate has a negative and insignificant relationship with per capita income. In other words, one unit increase in interest rate leads to a reduction in per capita income in Nigeria. These results are in tandem with economic theory and conforms to the present economic realities. The rising inflation rate has eroded the purchasing power parity by the fall in the value of the per capita income of the citizens. These results are in line with the findings of Ogini (2022) and Onwubuariri et al., (2020) who asserts that inflation, exchange rate and interest rate have significant policy effects on the standard of living of an average Nigerian in both the short run and the long run. The Error Correction Coefficient, estimated at -0.012207 is significant and negative as expected, showing the rate of adjustment to equilibrium. The Adjusted R-Squared showed 0.600922, depicting that 60% variation in per capita income (standard of living) is explained by changes in inflation rate, exchange rate and interest rate. This further justifies that fact that the rising inflation rate significantly contributes to the fall in the standard of living in Nigeria.

4.1.5 Unit Root Test Result for Private Investment Model

As shown in Table 5 below, the series showed that all the variables were not stationary at level. But became stationary after 1st difference. There was no autocorrelation problem amongst variables; hence, the ECM model can capture the long-run relationship among variables.

Table 5. ADF and PP Unit Root Test Result for Model Two

| Variables | ADF Statistics Level | ADF Statistics First Difference | PP Statistics Level | PP Statistics First Difference | Order of Integration |

| GFCF | -0.576631 | -4.204850” | -0.247030 | -4.187835” | I (1) |

| INF | -3.048567 | -5.910682” | -2.915627 | -10.68364” | I (1) |

| EXR | -2.192124 | -5.419436 | -2.523348 | -5.419436 | I (1) |

| INR | -2.899830 | -7.105924 | -2.769105 | -8.998565 | I (1) |

Source: Authors’ Computation (2024) from e-view 10

4.1.6 Co integration Test

To ascertain a long-run relationship among the variables in the presence of the maximum Eigenvalues and trace statistics, the Johansen cointegration techniques was applied.

Table 6.Unrestricted Co integration Rank Test (Trace)

| Hypothesized No. of CE(s) | Eigenvalue | Trace Statistic | 0.05 Critical value | Prob ** |

| None * | 0.635600 | 71.02517 | 47.85613 | 0.0001 |

| At most 1 * | 0.450811 | 30.64505 | 29.79707 | 0.0398 |

Trace test indicate 2 cointegrating eqn (s) at the 0.05 level. * denotes rejection of the hypothesis at the 0.05 level. ** Mackinnon – Haug – Michelis (1999) p-values

| Unrestricted Co integration Rank Test (Maximum Eigenvalue) | ||||

| Hypothesized No. of CE(s) | Eigenvalue | Trace Statistic | 0.05 Critical value | Prob ** |

| None * | 0.635600 | 40.38012 | 27.58434 | 0.0007 |

| At most 1 * | 0.450811 | 23.97251 | 21.13162 | 0.0194 |

Note: Max – eigenvalue test indicates 2 Cointegrating eqn(s) at the 0.05 level, * denotes rejection of the hypothesis at the 0.05 level, ** Mackmnon – Haugh – Michelis (1999) p values.

From the results as presented above, both the trace statistics and maximum eigenvalues showed traces of cointegrating – long-run relationship at the 5% level of significance. In order words, there exists a long-run relationship between per capita income and inflation, exchange rate, and interest rate within the reviewing period. The Error Correction Model Ordinary Least Square (OLS) are presented below. These results show the adjustment of the long run equilibrium to the short run dynamics.

Table 7 Dependent Variable: DLOG(GFCF)

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| D (INF) | 0.001749 | 0.001562 | 1.120110 | 0.2725 |

| D (INF (-3)) | -0.004471 | 0.001856 | -2.408751 | 0.0231 |

| DLOG (EXR) | 0.121605 | 0.075308 | 1.614772 | 0.1180 |

| DLOG (EXR (-1)) | 0.140641 | 0.075362 | 1.866206 | 0.0729 |

| DLOG (EXR (-2)) | -0.065769 | 0.078808 | -0.834557 | 0.4113 |

| DLOG (EXR (-3)) | -0.168989 | 0.078642 | -2.148829 | 0.0408 |

| D (INR (-3)) | -0.009938 | 0.005315 | -1.869842 | 0.0724 |

| ECM (-1) | -0.006404 | 0.019698 | -0.325099 | 0.0476 |

| R-squared | 0.472761 | Mean dependent var | 0.171129 | |

| Adjusted R-squared | 0.277487 | S.D. dependent var | 0.137402 | |

| S.E. of regression | 0.116793 | Akaike info criterion | -1.219629 | |

| Sum squared resid | 0.368296 | Schwarz criterion | -0.745591 | |

| Log likelihood | 34.17295 | Hannan-Quinn criter. | -1.050970 | |

| Durbin-Watson stat | 1.926721 | |||

Source: Authors’ Computation (2024) from E-view 10

From the result as presented above, the third period lag of inflation have negative and significant impact on the private investment. This suggests that a one unit increase in inflation rate leads to a 4 unit decrease in private investment. This implies that inflation erodes private domestic in the long run. A negative and significant relationship is observed between exchange rate and private investment. A one percent increase in exchange rate resulted in approximately 17 percent decrease in private investment after a three-period lag. The interest rate has a negative and insignificant relationship with private investment. In other words, one unit increase in interest rate leads to a reduction in private investment in Nigeria. These results are in tandem with economic theory and conforms to the present economic realities. The rising inflation rate has eroded the purchasing power parity through the increase in interest rate, that invariably affects the level of borrowing for private investment. The fall in the value of naira in relation to the dollar, has made our export very expensive and has left our domestic economy dominated with imported goods, thereby hindering the growth of our private domestic investments due to worsening exchange rate system. These results are in line with the findings of Ogini (2022), Onwubuariri et al., (2020), Oniore et al., (2016) and Wanjiru et al., (2021), and Wanjiru et al., (2021) who assert that inflation, exchange rate and interest rate have significant policy effects on the standard of living of an average Nigerian in both the short run and the long run. The Error Correction Coefficient, estimated at -0.006404 is significant and negative as expected, showing the rate of adjustment to equilibrium. The Adjusted R-Squared showed 0.277487, depicting that approximately 27% variation in private investment is explained by changes in inflation rate, exchange rate and interest rate. This further justifies that fact that the rising inflation rate significantly affect the level of private investment in Nigeria, although is a slow variation.

4.1.7 Model Diagnostic Test

The reliability of the model has been demonstrated by applying a series of diagnostic tests to meet the requirements for the quality of residual. Table 8. provides the model diagnostic test.

Table 8. Diagnostic Test Results Model One

| Hypothesis | Test Statistic | Cal. Stats | Prob. | Remark |

| Residual Normally Distributed | Jacque Bera (JB) | 1.219418 | 0.543509 | Accepted |

| No Serial Correlation | Breusch Godefrey (BG) | 5.441717 | 0.0612 | Accepted |

| Homoscedasticity | Breusch-Pagan Godfrey | 0.322990 | 0.9777 | Accepted |

| No Specification Error | Ramsey-RESET | 0.384284 | 0.5409 | Accepted |

Source: Authors’ Computation (2024) from e-view 10

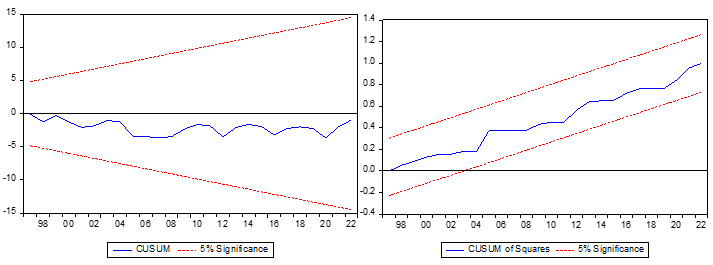

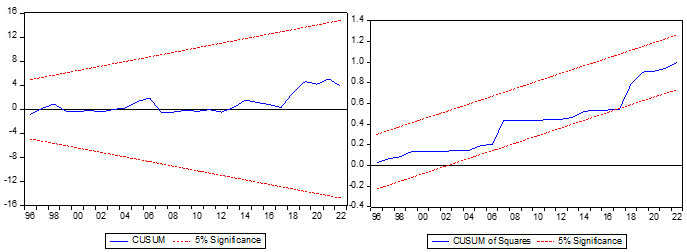

Drawing from the Gaus-Markov theorem, the estimates are declared as the Best Linear Unbiased and Efficient (BLUE) estimators and is therefore are useful for policy inference for both models. There were no sign of heteroscedasticity or auto correlation of residuals was found in the analysed model. The auto correlation LM test rejects the null hypothesis that there is no serial correlation. As shown in the figures of 2 and 3; 4 and 5, neither the recursive residuals or CUSUM of squares plot cross the 5 percent critical lines, there it was concluded that the estimated parameters are relatively stable, well specified and robust for policy analysis.

Fig.2 Fig.3

Table 9. Diagnostic Test Results Model Two

| Hypothesis | Test Statistic | Cal. Stats | Prob. | Remark |

| Residual Normally Distributed | Jacque Bera (JB) | 3.061492 | 0.216374 | Accepted |

| No Serial Correlation | Breusch Godefrey (BG) | 0.167578 | 0.8467 | Accepted |

| Homoscedasticity | Breusch-Pagan Godfrey | 0.280013 | 0.9845 | Accepted |

| No Specification Error | Ramsey-RESET | 0.410641 | 0.5273 | Accepted |

Source: Authors’ Computation (2024) from e-view 10

Fig.5 Fig.6

Source: Authors’ Computation (2024) from eview-10

4.2 Policy Implication

The policy implications of the empirical results have also been noted. From the per capita income model, inflation rate has negative and significant impact on the per capita income. Furthermore, from the private investment model, inflation rate has negative and significant impact on the private investment. This implies that inflation erodes private domestic investment in the long run. A negative and significant relationship is observed between exchange rate and private investment. The interest rate has a negative and insignificant relationship with private investment. The negative impact of inflation on these key macroeconomic indicators suggests that high or volatile inflation rates can hinder economic growth and development.

CONCLUSION AND POLICY RECOMMENDATIONS

5.1 Conclusion

Based on the findings of the study, it is evident that inflation rate has a detrimental effect on the macroeconomic performance indicators of per capita income and private investment within the country. This negative impact highlights the importance of maintaining stable price levels to foster economic growth and prosperity.

5.2 Policy Recommendations

From the empirical evidences, the following policy suggestions are offered:

- The central bank should adopt appropriate monetary policies aimed at controlling inflation rates within acceptable levels. This may involve adjusting interest rates, managing money supply, and employing other monetary tools to stabilize prices.

- The government should prioritize fiscal discipline and prudent spending to avoid excessive budget deficits that can fuel inflationary pressures and the allocation of funds towards productive investments and infrastructure projects to stimulate economic growth without exacerbating inflation.

- Implementing structural reforms aimed at enhancing productivity, efficiency, and competitiveness across various sectors of the economy can help mitigate the adverse effects of inflation

- Maintaining a stable and competitive exchange rate regime to enhance investor confidence and mitigate inflationary expectations associated with currency depreciation.

5.3 Contribution to Knowledge

This study utilized per capita income and private investment as macroeconomic performance indicators due to their ability to provide nuanced insights into the economic well-being and growth prospects of a nation. While indicators like economic growth, balance of payments, interest rate and exchange rates which dominates literatures are certainly important, they often reflect broader trends in the economy and may not capture the intricacies of income distribution and the dynamics of private sector participation. Per capita income reflects the average income earned by individuals in a country, providing a measure of the standard of living and income distribution within the population and gives policymakers a sense of how prosperity is distributed among citizens and can inform policies aimed at reducing income inequality. Private investment reflects the level of confidence among businesses and investors in the economy’s future prospects and is also an indicator of innovation and productivity growth within the economy. When businesses invest in new technologies, equipment, and infrastructure, it can lead to long-term improvements in efficiency and competitiveness which necessitated the Neo-Classical Growth Theory developed in the mid-20th century by economists such as Robert Solow, Trevor Swan, and others, that emphasizes the role of technological progress and savings/investment decisions in determining long-term economic growth.

5.4 Limitation of the Study

We are aware that the Nigerian economy is highly susceptible to external shocks such as oil price volatility. The data we employed might not have fully captured the effect of such external factors, and distinguishing their impact from domestic inflationary trends can be challenging.

REFERENCES

- Bawa, S., & Abdullahi, I. S. (2014). Threshold Effect of Inflation on Economic Growth in Nigeria. 3(1), 43–56.

- Bilalli, A., & Sadiku, M. (2023). THE IMPACT OF INFLATION ON FINANCIAL SECTOR PERFORMANCE: EVIDENCE. FROM. WESTERN BALKAN COUNTRIES. 18(2), 74–89. https://doi.org/10.2478/seeur-2023-0071

- Central Bank of Nigeria (2015). The Nigerian financial system, in briefs, 1997 special edition, CBN, Abuja

- Chisti, K. A., Ali, K., & Sangmi, M.-. ud.-. din.. (2015). Impact of inflation on per capita income in emerging economies: evidence from brics nations. 2(2). https://doi.org/10.18488/JOURNAL.66/2015.2.2/66.2.34.39

- Ezeibekwe, O. F. (2020). Monetary Policy and Domestic Investment in Nigeria: The Role of the Inflation Rate. 34(1). https://doi.org/10.2478/EB-2020-0010

- Fitri, W. S., & Syamsuri, A. R. (2024). The Impact of Inflation on Indonesia’s Economic Growth. 1, 1. https://doi.org/https://doi.org/10.5281/zenodo.11157994

- Jonathan, O., Gyang Oniore, E., & Nnadi, K. U. (2016). The Impact of Exchange Rate Fluctuations on Private Domestic Investment Performance in Nigeria. 7(3), 07–15. iosrjournals.org

- Korgbeelo, C., & Nwiado, D. (2021). Monetary Policy Instruments and the Control of Inflation in Nigeria: A Time-Series Analysis. 3(2), 71–80. https://doi.org/DOI: 10.36346/sarjhss. 2021.v03i02.006

- MOGAJI, O., FALADE, A. O. O., & OGUNDIPE, S. A. (2020). Inflation, Interest Rate and Domestic Investment in Nigeria: Auto-Regressive Distributed Lag (ARDL) Approach. 2(8), 516–525. https://doi.org/DOI: 10.35629/5252-0208516525

- Mohamed, A. M. A. (2022). The impact of macroeconomic indicators on inflation in Sudan during the period from 2000-2022. 288–311. https://doi.org/https://doi.org/10.31272/IJES2024.80.E17

- Nookhwun, N., & Waiyawatjakon, R. (2024). Flexible Inflation Targeting and Macroeconomic Performance: Evidence from ASEAN. 1–36.

- Ogini, P. (2022). Selected Macroeconomic Variables and Per Capita Income in Nigeria. 10(2), 7–20.

- Okoye, L, U., Olokoyo, F, O., Ezeji, F, N., Okoh J, I., & Evbuomwan, G, O., (2019); Determinants of the behaviour of inflation rate in Nigeria. Investment Management and Financial Innovations, 16 (2) PP 25-36

- Oluwole, F. O., & Ushie, P. O. (2022). Interest Rate Liberalization and Investment in Nigeria: An ARDL Approach. Volume 2(Issue 1), 31–40.

- Onifade, S.T., C¸ evik, S., Erdogan, S., Asongu, S. & Bekun, F. V. (2020). An empirical ˘ retrospect of the impacts of government expenditures on economic growth: new evidence from the Nigerian economy. Economic Structures 9(6). https://doi.org/10.1186/s40008-020- 0186-7

- Onwubuariri, S. E., Oladeji, S. I., & Bank-Ola, R. F. (2021). Inflation And Economic Growth in Nigeria: An ARDL Bound Testing Approach. 3(1), 277–290.

- Wanjiru, M., Muturi, W., & Njeru, A. (2021). Money Supply, Inflation Rate, Exchange Rate and Growth of Domestic Private Investment in Kenya. 59(2), 68–84.