Internal Control as an Aid to Accountability in the Public Service: A Case Study of Ibarapa East Local Government, Oyo State.

- Bolaji, Saudat Adewumi

- 1195-1209

- Mar 13, 2024

- Education

Internal Control as an Aid to Accountability in the Public Service: A Case Study of Ibarapa East Local Government, Oyo State.

Bolaji, Saudat Adewumi

Adeseun Ogundoyin Polytechnic, Eruwa, Ibarapa, Oyo State. Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.802084

Received: 10 July 2023; Revised: 15 July 2023; Accepted: 19 July 2023; Published: 12 March 2024

ABSTRACT

Internal Control System (ICS) is the process by which private or public organization governs its activities for effective and efficient operations, reliability of her financial accountability and compliance with applicable laws and regulations. This paper investigated how the implementation of ICS has aided the performance, accountability, transparency and efficient management of resources in the public service in which Ibarapa East Local Government was used as a case study.

It is a survey research design and both primary and secondary sources of data were explored. The data were gathered through questionnaire, interview, source document, official gazette, circulars and local magazine (The Ibarapa News), and from key stakeholders, government officials, employees and community representatives.

The data were analysed using Descriptive Statistics, the Statistics Process Control (SPC) charts and the non-parametric test – the Chi-Square.

Findings revealed that the administrative and accounting internal controls strategies were perceived as normal even with the non-autonomous status of all local governments in Nigeria and also well implemented in line with the council’s management culture and other elements of internal control processes. All the null hypotheses were rejected. The Chi-square X 2c = 23.045 > X 2t = 14.067; degree of freedom (df) being 7 and at 0.05 level of significant. All the control conditions on the Statistical Process Control (SPC) chart were at Upper Control Limit (UCL) except for the Risk Assessment and Exposure influenced by ethnic social problems of banditry and other crisis. The paper concluded that ICS has aided accountability of the Local Government through efficient and prudent resource management, transparent and financial integrity, internal and external audits, prevention of misappropriation of funds, enforcement and compliance with legal and regulatory requirements, as well as risk management and mitigation. Ultimately, the study has contributed to the improvement of public sector performance, service delivery, and public trust in Ibarapa East Local Government in particular, Oyo State Local Government Service Commission in general.

The study recommended that Ibarapa East Local Government should prioritize the strengthening of internal control mechanisms to enhance accountability by establishing clear lines of responsibility, providing adequate training to staff members, implementing regular internal and external audits, and fostering a culture of transparency, gender balance, and ethical behavior and quick report to resolve communal crisis.

Keywords: Internal Control System, Accountability, Administrative Control, Accounting Control.

INTRODUCTION

Internal Control is a plan of an organization, the procedures and records concerned with the safeguarding of assets and the reliability of the financial records.

Olowolaju and Ibukun-Falayi (2016) described a system of internal control as one in which the financial policy established by the management to carry out the business of that organisation in an orderly and efficient manner, ensuring adherence to management policies, and safeguarding the asset as well as completeness and accuracy of that records.

Internal Control Systems (ICS) are found in all areas of any enterprise – private and public, in production, administrative and store keeping functions. They are designated to mitigate risks, prevent fraud, theft, errors and misstatements in financial statements. ICS are to ensure accuracy and reliability in financial information and to maintain compliance with laws and regulations, promote efficiency in operations and facilitate the achievement of an entity’s goals.

Sanusi and Mustapha (2015) claimed that the recent global pressure on corruption and management of public funds is the major factor that necessitates the implementation of good ICS in every organization. Federal, State down to the Local Governments in the public service are to ensure financial accountability and transparency in the management of fund at their respective level.

The International Organisation of Supreme Audit Institution (INTOSAI) described accountability as a process whereby an organization are held responsible for the decisions and actions including the stewardship of funds, fairness and all aspects of performance. In Nigeria public service, the above description is otherwise especially at the Local Government Level. Whereas, local government system in Nigeria unlike its counterpart at State or Federal level lacks autonomy which is a symbol of independence. Due to this lack of autonomy, Local Governments are exposed to external and internal controls. The concern of this paper is on internal control and its primary role in the system of local government to ensure it watches over the council’s asset, ensures the lack of misappropriation of the council’s resources, proper authorization of revenue and expenditure, proper books of accounting records kept are to monitor expenditure, investigate misconduct in finances, inspect books of account etc. Also as a result of lack of autonomy, the 774 Local Governments in Nigeria have performed poorly or rather below expectation. Okoye (2006) maintained that Local Governments all over the world have a lot to contribute to the economic development process of their country. Obi (2001) also argues that the arrangement whereby, the internal auditor works directly under the Chairman is fraught with obvious problems. One wonders how independent an internal auditor can be when he receives his salary from the Local Government Council.

From the above, it can then be asked that how can internal control be effectively implemented to aid the performance and accountability of the local government administration granted that their autonomy still subsist and the issues of independence and confidentiality in Local Government auditing are in the hands of Local Government Authority. And how can the impact of internal control policies and procedures be felt among the rank and files of the local government which is devoid of politics, and any form of social crisis?

RESEARCH QUESTIONS

- What is the perception of stakeholders on the effectiveness of internal control framework of checks and balances as instituted by Oyo State Government on transparent financial management?

- How has the internal control strategy of potential auditing and accountability in Local Government Service in Oyo State been implemented?

- What is impact of the Internal Control policies and procedures in the administration of Local Government at the grassroots level.

OBJECTIVES OF THE STUDY

The broad objective of this study is to examine how internal control could aid the performance and accountability in the public service of Oyo State. Therefore, the specific objectives are posed thus:

- To evaluate the perception of stakeholders about the effective implementation of internal control framework of checks and balances as instituted by Oyo State Government on transparent financial management in the Local Government Public Service.

- To provide an understanding of the status of the application of the systems of audit and internal control in the public service

- To examine the impact of ICS policies and procedures on the performance and accountability of Ibarapa East Local Government in Oyo State.

RESEARCH HYPOTHESIS

Ho1 Stakeholders in Local Government administration in Oyo State perceived ICS as an aberration in view of their non-autonomous status.

Ho2: Internal Control Strategy of potential auditing and accountability in Local Government Service in Oyo State has not been efficiently implemented.

Ho3: Internal Control policies, procedures and processes have no impact on the performance and accountability of Local Government official activities.

BRIEF HISTORICAL BACKGROUND OF IBARAPA EAST LOCAL GOVERNMENT

Ibarapa East Local Government with its headquarters at Eruwa was established 1989. It covers an area of 705.78sqkm2 of land with the estimated population of over 120,220 according to 2006 Nigeria Census figure. The Local Government is classified as sub urban Local Government. It is bounded in the West by Ibarapa Central Local Government, in the East by Ido Local Government while it’s bounded in the North and South by Iseyin and Odeda Local Government in Ogun State.

The Local Government consists of multi-ethnic nationalities; though predominantly Yorubas, the presence of other nationalities is equally felt in the Local Government Area such as Fulanis, Igbos, TIVs, Jukuns among others.

The economic life of the Local Government is dependent on Agriculture. The local government area has admirable tropical climate which favours the growth of both food and cash crops. Agricultural sector provides income and employment opportunities for over seventy-five (75) percent of the populace. As a result of this, the local government encourages and facilitates agricultural empowerment and developmental initiatives. This explains why the area is a hub to so many Agro-Allied investments. Among the agro-allied companies located in the area are: – Nico Oil Palm Plantation, Zartech, Global-West, Obasanjo Farms among others. Aside this, the local government is housing two institutions of higher learning namely; Adeseun Ogundoyin Polytechnic, Eruwa and Oyo State College of Education, Lanlate.

Other mercantile activities noticeable among the people of the area include trading and cloth weaving. The local government is blessed with towns and villages among which are: Eruwa, Lanlate, Okolo, Maya, Temidire, Idi-Ope, Adeagbo, Elere, Onirope, Akete, Obanese, Alapa, Lagaye, Abule Baale, Ijesa, Babamogba etc. Currently, Ibarapa East is having ten (10) Political wards.

Figure 1: Map of Oyo State showing the Ibarapa Local Government Areas

Figure 2: Map of Oyo State showing the Ibarapa East Local Government Area

LITERATURE REVIEW

Conceptual Review

Basic Principles of an Internal Control System

True Tamplin (2023) described the conceptual framework of the principles, necessity, attributes, accounting and limitations of ICS in the following ways:

That an Internal Control System should be designed to meet a firm’s specific informational needs thus, the system can range, from a simple manual-system to complex computerized on-line system with remote terminals spread across the entire country.

Whether manual or computerized, the accounting system must process information efficiently, accurately, and on a timely basis. At the heart of any well designed accounting system is a well-thought-out internal control system.

He further stressed that one of the principal responsibilities of management is to protect the assets under its control, ensure the accuracy and reliability of its accounting records, and see that its policies are carried out efficiently. Internal control is the organizational plan, including specific methods and procedures that management develops to meet these responsibilities. Specifically, Internal control is formally defined as: “the plan of organization and all of the coordinate methods and measures adopted within a business to safeguard its assets, check the accuracy and reliability of its accounting data, promote operational efficiency, and encourage adherence to prescribed policies.”

A strong internal control system will contain both administrative and accounting controls.

Administrative controls include the plan of organization and the procedures and records that are concerned with the decision making processes leading to management’s authorization of transactions. That is, management uses administrative controls to ensure that its policies and procedures are carried out.

Accounting controls are the plan of the organization and the procedures and records that are concerned with safeguarding the assets and the reliability of the financial records.

These controls are more specific and are designed to ensure that:

Transactions are executed in accordance with management’s general or specific authorization.

Transactions are recorded as necessary (1) to permit the preparation of financial statements in conformity with Generally Accepted Accounting Principles (GAAP) or any other criteria applicable to such statements and (2) to maintain accountability for assets.

Access to assets is permitted only in accordance with management’s authorization. The recorded accountability for assets is compared with the existing assets at reasonable intervals and appropriate action is taken with respect to any differences.

For an organization, whether public or private to have a sound system of internal control, both administrative and accounting controls must be present.

The administrative controls provide the overall framework in which the specific accounting controls operate.

If management is not interested in maintaining administrative controls, specific accounting controls cannot ensure that the organization’s assets are being safeguarded.

Tamplin (2023) emphasized that internal controls are necessary because accounting systems are designed and run by people and people can make errors.

These errors may be either true mistakes or deliberate actions. There have been numerous instances in which large corporations have restated their financial reports because of inadvertent errors in the accounting records. Therefore it is mandated that there should be an act purposely for the maintenance of a strong system of internal control. Furthermore, the act should require that the system of internal control should limit the use of corporate assets for the purpose designated by management and that the accounting records be compared with the assets owned by the organisation.

Regarding the attributes of an ICS, Tamplin (2023) pin-pointed that the design of an internal control system and the procedures utilized should be tailored to the firm’s specific needs.

However, a well-designed internal control system will center on a properly designed accounting system and include sound personnel and personnel practices and the separation of duties. Tamplin (2023) therefore listed the following attributes of an ICS:

- A Well-Designed Accounting System: A strong internal control system is difficult to implement without a well-designed accounting system. The accounting system should provide accounting controls over the firm’s assets, liabilities, revenues, and expenses.

- Sound Personnel and Personnel Policies: Any internal control system is dependent on the people who run it. Individuals should be placed in positions commensurate with their abilities. Good personnel policies include the rotation of people in key positions, the requirement that all employees take an annual vacation, and the bonding of individuals who handle cash or other liquid assets. Bonding means checking employees and insuring the company against theft by them.

- Separation of Duties: Should be a clear separation of duties within the accounting function. That is, those individuals who have responsibility for and control over a particular asset should not also account for it. For example, the individual in the organization who handles cash receipts should not also handle accounts receivable or prepare the bank reconciliation. This makes it more difficult for one individual to steal the company’s assets.

Conditions for a Functional Internal Control System

It has been re-instated by many scholars that to have a functional internal control system in place, several key conditions or components should be considered. These conditions help to ensure the effectiveness, efficiency, and reliability of internal controls within an organization. The main conditions for a functional Internal Control System are:

Control Environment: The control environment sets the tone for the organization and influences the mindset and behaviors related to internal controls. It includes factors such as management’s commitment to integrity, ethics, and competence, as well as the establishment of a positive and accountable organizational culture. The control environment provides the foundation for effective internal controls (Kuo-Tay and Ronald, 1992).

Risk Assessment: Organizations should identify and assess the risks they face in achieving their objectives. This involves understanding potential internal and external risks, evaluating their likelihood and potential impact, and prioritizing them based on their significance. A robust risk assessment enables the organization to design and implement appropriate control activities to mitigate identified risks. (Gamage et al, 2014)

Control Activities: Control activities are the specific policies, procedures, and actions that are established to mitigate risks and achieve control objectives. These activities should be designed to address identified risks and should encompass a range of preventive and detective controls. Examples include segregation of duties, authorization and approval processes, physical safeguards, and IT controls. Control activities should be properly documented, communicated, and consistently applied throughout the organization. (Gamage et al, 2014)

Information and Communication: Reliable and timely information is essential for effective decision-making, monitoring, and control. Organizations should have systems and processes in place to capture, record, process, and communicate relevant information. This includes establishing clear channels of communication, ensuring the accuracy and completeness of data, and providing appropriate reporting to management and relevant stakeholders.

Monitoring: Monitoring activities are essential to assess the effectiveness of internal controls over time. Regular monitoring involves ongoing evaluations, reviews, and assessments to identify control deficiencies, detect deviations from established controls, and ensure the timely resolution of issues. Monitoring activities may include internal audits, management reviews, self-assessments, and periodic evaluations of the internal control system.

Information Technology (IT) Considerations: In today’s digital age, organizations need to consider IT controls as an integral part of their internal control system. This includes securing IT infrastructure, protecting data integrity, implementing access controls, ensuring system availability, and addressing IT-related risks and vulnerabilities.

Documentation and Documentation Retention: Proper documentation is crucial to support the design, implementation, and effectiveness of internal controls. Organizations should document their control environment, risk assessment processes, control activities, and monitoring activities. Additionally, maintaining appropriate documentation retention policies ensures that relevant records and evidence are retained for the necessary periods.

Gamage et al, (2014) concluded that by addressing these conditions, organizations can establish a functional internal control system that helps mitigate risks, safeguard assets, promote compliance, and improve overall operational effectiveness and efficiency. It is important to regularly assess and enhance the internal control system to adapt to changing circumstances and evolving risks within the organization.

Types of Internal Control System

According to Business Times, (Monday, November 13, 2000) quoting Kelvin (1999), the types of internal control systems that exist in an organization include:

(a) Preventive Controls: These controls are designed to prevent errors, fraud, or other undesirable events from occurring. They include segregation of duties, proper authorization and approval processes, physical security measures, and IT access controls.

Several other types or categories of Internal Control Systems that organizations can implement to address different aspects of their operations and mitigate various risks are:

(b) Detective Controls: Detective controls are implemented to identify errors or irregularities that have occurred. They help detect deviations from established policies or procedures and enable timely corrective action. Examples include regular reconciliations, exception reporting, and periodic internal audits.

(c) Corrective Controls: Corrective controls are put in place to address identified issues or errors. They are activated after an error or problem is detected to rectify the situation and prevent similar occurrences in the future. Examples include adjusting entries, disciplinary actions, and process improvements.

(d) Directive Controls: Directive controls provide guidance and instructions to employees to ensure that they follow established policies and procedures. These controls may involve documented guidelines, manuals, or standard operating procedures that outline the expected behavior and actions.

(e) Compensating Controls: Compensating controls are alternative measures implemented when an ideal control is not feasible or cost-effective. They help mitigate risks when primary controls are inadequate or unavailable. For example, if segregation of duties is not possible due to limited staff, compensating controls could include additional reviews or oversight.

(f) IT Controls: Information Technology (IT) controls focus on the security, integrity, and availability of information systems and data. These controls aim to prevent unauthorized access, data loss, system failures, and other IT-related risks. Examples include user access controls, network security measures, backup and recovery processes, and software change management.

(g) Administrative Controls: Administrative controls are management policies and procedures that provide overall guidance and direction to the organization. They include activities such as strategic planning, budgeting, performance evaluations, and ethical guidelines.

Sanusi and Mustapha (2015) quoted Singleton et al (2005) who studied (a), (b) and (c) above confirmed that preventive controls can to prevent error, omission or malicious act from happening. Detective controls can detect and occurrence of an omission or error or malicious act. While corrective controls help to minimize and identify the cause of a problem as well as to correct errors arising from such problem. Internal control system therefore, can provide an independent appraisal of the quality of managerial performance in carrying out assigned responsibilities for better revenue generation. Fadzil et al (2008) correlates effective internal control system with the organization success in meeting its revenue target. And Omolehinwa, (2003) proposed a principle that good governance in any organization is a function of effective system of internal control. According to Miller (2007), the study concludes that poor internal control leads to asset misappropriation, corruption, fraud in financial statements.

THEORETICAL REVIEW

Agency Theory

Agency relationship according to with Jensen and Meckling (2003) is “an agreement in which one or many groups employ one more group (the agent) to carry out some obligations in their behalf as well as allow them (agents) to make choices” (give making decision authorities to the agent). According to Eisenhardt, K. (1989), agency notion stresses on solving twofold problems escalating from agency relationship: agency issues and threat division problem. An agency problem occurs while interests of the principal and the agent result to conflict; this will lead to complications. In contrast, the issue of risk sharing occurs while the principal and the agent take diverse risk approach. If these kinds of agency conflicts persist, then their comparative significance will be vague. One might picture the steadiness at an inner optimal as in the trade-off theory. Though, the details of conflicting venture encouragements can result in compound harms, as advocated by Berkovich & Kim (1990). Eventually dynamic agency models such as Morrellec (2004) and Atkeson & Cole (2005) and dynamic trade-off are likely to go a long distance towards closing theoretical gaps between the various approaches to leverage.

Attribution Theory

The attribution theory examines the use of information in the social environment to explain events and behaviors (Schroth and Shah, 2000). Reffett (2007) asserts that when evaluators believe more people would have acted differently in a given circumstance, they attribute responsibility for an outcome to the person. So, failure to detect internal control on revenue generation by auditors when it is their duty, imply the auditors are negligent. Auditors are more likely to be sued when they fail to detect common misappropriations that would result to decreased revenues (Bonner et al. (1998). It is so because evaluators believe that the fraud could have been detected by other auditors.

In short, attribution theory calls for auditors to report on the effectiveness of firm’s internal control. When fraud occurs, auditors should be held accountable (Reffett, 2007).

Reliability Theory

This theory proposes the probability that a system will execute its functions in a given time (Gavrilov and Gavrilova, 2001). As far as reliability theory goes, units of a system of internal control include parts which are interwoven, and every unit requires a definite measure of success. The success or an eventfulness of a component defines its state. When a component exists in a successful state, it is said to be reliable. Additionally, the whole internal control unit system entails two values – success or failure. Despite the prevalence of tractability of reliability theory with respect to evaluation and design of system of internal control in research literature, there has not been any application of the workings of the theory of reliability. (Kinney, 2000). Organizational management and external editors remain the two users of reliability theory of the highest probability. As stated by Kinney (2000) in Ndungu (2014), there is need to garner as much evidence to support a professional stance in the manner of external audit. The central aim of internal control systems is risk control and assessment. Such prevents a material error from leading to losses on account of poor control or preventive measures. Greater cost is involved with losses following when the systems of internal control are weak.

RESEARCH DESIGN AND METHODOLOGY

The aim of this work is to discuss and investigate the various methods that have being employed as internal control in the administration of Ibarapa East Local Government in Oyo State. The technique and sources of data collection as well as method of analyzing data are described here. The objective of this is to provide authority-based method for this research.

RESEARCH DESIGN

The research employed a descriptive and survey research design to assess the effectiveness of internal control in the financial uprightness of officers and subordinates towards effective accountability of public office. It is therefore qualitative and quantitative in outlook.

TARGET POPULATION

The population of this study is the entire staff in all the departments of Ibarapa East Local Government Area. For clarity the departments were grouped according to: Accounts Department, Administrative Department and the Internal Audit Department. The study used the total number of staff in Ibarapa East Local Government. The Local Government consist of two towns (Eruwa and Lanlate) which has the population of 280 members of staff.

Table 1: Population of Ibarapa East Local Government Staff

| DEPARTMENT | POPULATION |

| ACCOUNTS | 100 |

| ADMINISTRATION | 120 |

| INTERNAL AUDIT | 60 |

| TOTAL | 280 |

SOURCE: Author’s field survey 2023

SAMPLE AND SAMPLING TECHNIQUES

Sample procedures are the method used in drawing sample from population which gives a sample size for the study.

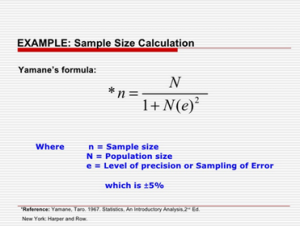

By using sample size determination according to Taro Yamane (1967) the researcher was able to determine the sample size of the study as follows:

Figure 3; Taro Yamane (1967) Sample Size Determination

n = N/1+N (e) 2 where

n= Sample size

N = Population Size

e = limit of tolerance error/level of precision

n = 280/1+ 280 (0.05) 2

n = 280/1+ 280 (0.0025) 2

n = 280/1+ 0.7

n = 280/1.7

n = 164.70588

Sample size = 165 approximately

METHOD OF DATA COLLECTION

In undertaking this study and because of the nature of the research, the researcher collected his data through primary and secondary sources.

Primary sources: These were mostly collected from questionnaires survey, personal observation, interviews and inspection of some documents of the local government. The last three, inspection, interview and observations had to be used in order to lower the level of bias that may have resulted in the responses supplied by respondents to the questionnaire and to improve or allow for unbiased view for effective and required conclusions.

Secondary sources: Mainly obtained from the review of available documents and work of many experts in this field. Some of these books, documents, news magazines (Ibarapa News), journals, periodicals, official gazette etc. contributed greatly to the review of related literature and data collection for this study.

The choice of this form of data source was employed because they would help to unveil the efficacy of internal control as an aid to accountability. It would expose difficulties that have obstructed the effective application of this function by public and private organization. The objectives of various aspects of internal control as an aid to accountability would come to light with these data sources.

VALIDITY OF THE INSTRUMENT

To ensure the validity of the instrument used about two people were approached for their comments. One person being at the top cadre, and another one of the management team. They were asked to examine the instrument with regard to its relevance to the study, technically and clarity of the items in describing the importance and implementation strategy of internal control as an aid to accountability in the public sector. Furthermore, in ensuring the validity of the instrument used, the questionnaire was highly structured and contains and close-ended items needed to elicit the needed information, comparing from the oral interviews.

PRESENTATION AND ANALYSIS OF DATA

Data collected were analysed using Descriptive Statistics, the Statistical Process Control (SPC) chart and Chi-Square, all these are apart from Taro Yamane (1967) statistic that was used to determine the sample size which resulted in 165 respondents out of the entire Ibarapa East Local Government staff used for this study.

Table 2: Questionnaire Respondent by Department

| Department | Number Distributed | Number Returned | Number Not Returned | % of Number Distributed |

| Accounts | 60 | 50 | 9 | 36.4 |

| Administration | 70 | 64 | 0 | 42.4 |

| Internal audit | 35 | 35 | 0 | 21.2 |

| Total | 165 | 156 | 9 | 100 |

Source: Field Survey 2023

Table 3: Questionnaire Respondents by Sex

| Gender | Frequency | Percentage (%) |

| Male | 62 | 40% |

| Female | 94 | 60% |

| Total | 156 | 100% |

Source: Field Survey 2023

Table 4: Questionnaire Respondents by Age-Range

| Gender | Frequency | Age Range |

| Male | 62 | 35 – 65 years |

| Female | 94 | 30– 45 years |

| Total | 156 | – |

Source: Field Survey 2023

above implied that the local government staff are female dominated, but males are of age than female staff. All these staffs are however literate and hold qualifications not below Primary School Leaving Certificate. Some senior staffs that headed some units have post graduate degree in relevant administrative and accounting areas.

The measures of central tendency and dispersion were computed to describe evidences from the staff on compliance and conformity as well as other conditions of internal control strategies.

The administrative and accounting internal controls were implemented under the following conditions with their corresponding sample mean:

- Segregation of duties with standard operating procedures ( ‾X = 27.82)

- Integrity, ethics and competence ( ‾X = 30.11)

- Clear channels of communication (‾ X = 28.24)

- Risk assessment (‾ X = 16.01)

- Authorization and approval processes. (‾ X = 32.14)

- IT infrastructure and data protection policies (‾ X = 26.67)

- Documentation and Documentation Retention Policies (‾ X = 30.00)

- Monitoring – internal audits, self-assessment and periodic. (‾ X = 27.30)

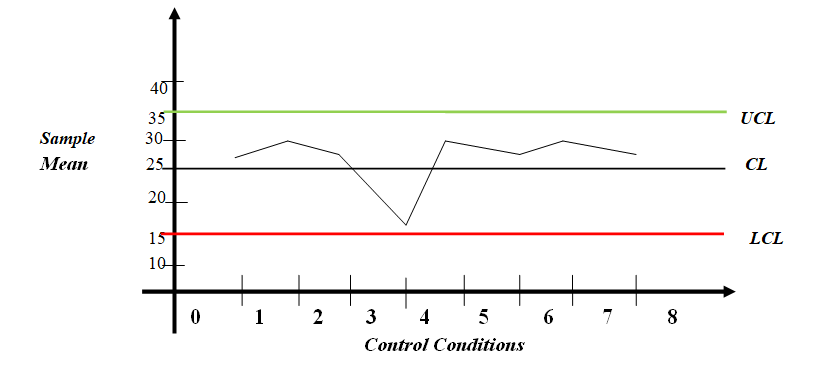

The mean and standard deviation of the responses to the above control conditions were computed within three (3) quantitative quarterly consecutive periods of time. They are described in the below SPC chart (Figure 4). Here the mean compliance rate, error rate, risk exposure, control effectiveness index, control monitoring frequency and trend analysis were measured to evaluate the control performance across different periods for improvement or deterioration in the internal control system.

From the data analysed, all these control measures were normal, remarkable, consistent and proactive overtime except for the risk assessment and exposure.

Figure 4: Control Conditions Chart

Note: UCL = Upper Control Line; CL = Centre Line; and LCL = Lower Centre Line

The potential risk of the Local Government was not due to ineffective internal control neither economic recession of the state, but due to Fulani herdsmen pastoral activities with bundles of conflicts such as crop destruction, water pollution, sexual harassment, land encroachment, cattle theft, banditry, etc. Hitherto, the researcher had employed the Monte Carlo simulation in which other surrounding Local Governments were affected by similar issue.

The Chi-Square analysis was based on the frequency of the agreement mode on a five-point scale with the observed and expected frequency discrepancy measured relatively to the various question items associated with each of the above control conditions (1-8). All the null hypothesis were rejected since X 2c = 23.045 > X 2t = 14.067; degree of freedom (df) being 7 and at 0.05 level of significant. This implied that, stakeholders are aware of the importance and purpose of internal control system in the public service and accountability is their watch-word. The effectiveness of the application of internal control strategy has a great impact on the administrative and accounting departments of the Ibarapa East Local Government of Oyo State regardless of the non-autonomous status of Local Government all overall the country

SUMMARY, CONCLUSION AND RECOMMENDATIONS

Summary of Findings

The study revealed the following:

- The administrative and accounting internal controls strategies were perceived as normal even with the non-autonomous status of all local governments in Nigeria

- The internal controls framework was well implemented as instituted by the Oyo State Government through the Local Government Service Commission and that there is need to keep the tempo of Internal Control System in the administrative, accounting and audit departments in the Local Government public service.

- Channel of communication to the subordinates should be improved especially on segregation of duties, authorization and approval processes. Official documentation and retention policies should be maintained regardless of local ethnic diversity.

- Overall monitoring and evaluation of individual job activities should be kept up at more periodic time-frame as possible.

- Most government ministries observed risk assessment and fraud-related risks procedures as functionality of internal control of their ministries or locality. The mechanism for mitigating critical risks need much attention since the area under study is not risk exposure-prone. Adequate and regular security should be provided against job hazard and unprecedented ethnic crisis

Conclusion

This study demonstrated that, whatever aspect one perceived public sector accountability, its principles are based on the fact that the recognition of the need for an organization to develop a strong internal control orientation particularly to its internal and external environment cannot be over-emphasized owing to its role in the public sector. It shows clearly that public sector could fail in its responsibility if there is lack of strict adherence to internal control processes. The hope of an effective internal control in Nigeria is now being placed in the hands of public officers, aided by accountable system audit and internal control systems to ensure that public services are delivered economically and efficiently.

Recommendations

The study recommends the following:

- The Ibarapa East Local Government should prioritize the strengthening of internal control mechanisms to enhance accountability by establishing clear lines of responsibility, providing adequate training to staff members, implementing regular internal and external audits, and fostering a culture of transparency, gender balance, and ethical behavior and quick report to resolve communal crisis

- The study further recommends that the governing body, possibly supported by the audit committee, should ensure that the internal control system is periodically monitored and evaluated. The actual assessment can be executed by the Local Government Board.

- All government ministries should transparently report on the structure and performance of their governance, risk management, and internal control system in their various reports to internal and external stakeholders, such as through their periodic accountability reports or on their website.

REFERENCES

- Adamu, S. O. (2008). Statistics for Beginners (1st ed.). Evan Brothers Plc.

- Adeoye, M., & Adeoye, E. (2014). “Drift of risk assessment on prevention of fraud in banks and financial institutions in Nigeria,” . Computing, Information Systems, Development Informatics & Allied Research Journal, 5(2), 13–28.

- Adetula, D. T., Balogun, S., Uwajeh, P., & Owolabi, T. (2016). Internal Control System in the Nigerian Tertiary Institutions. Innovation Management and Education Excellence Vision 2020 [Review of Regional Development to Global Economic Growth.]. 4505–4508.

- Akosile Akindele Iyiola, & Oladipo Oluwafolakemi Fasesin. (2013). A Comparative Assessment of Internal Control System in Public and Private Universities in South-West, Nigeria. Research Journal of Finance and Accounting, 4(13), 25–33.

- Badmus O. & Ebegbe (2003), Auditing and Investigation Theory & Practice. COSO (2013) framework.

- Retrieved from https://www.pwc.com/us/en/forensicservices/publications/assets/pwc-new-internal-control-frameworklitigation-counselperspectives.pdf

- Chenhall, B. N. (2003). Auditing and investigations (1st ed.). BON Publications.

- Cookey, A. E. (1998). Research Methods (1st ed.). Abbot Books Limited.

- Donald , K. K. ., & Delno, L. A. T. (2009). Proposal and Thesis Writing :an Introduction (1st ed.). Pauline Publications Africa.

- Emasu, S. (2007). Public financial management – Concepts and Practices, ACCA. International Public Sector Bulletin. , 3(7), 6–10.

- Fadzil, F. H., Haron, H., & Jantan, M. (2008). Internal Auditing practices and internal control system. Managerial Auditing Journal, 20(8).

- Financial Management Manual: Establishing and Maintaining a System of Internal Control. (2005). http://dev.wi.gov/grants.Fmm/B4INTL.com.htm

- Flesher, D. L. (2017). Internal Auditing Standards and Practices. A one – semester course. The Institute of Internal Auditors, Inc. USA.

- Gupta, P. P. (2001). Internal Audit Reenginering: Survey, model, and best practices. The Institute of Internal Auditors Research Foundation.

- Horgren, G. N. (2015). New Public Management and Accrual Accounting Basis for Transparency and Accountability in the Nigerian Public Sector. Journal of Business and Management, 16(7), 104–113.

- Jeremiah, O. (2013). Ethics, Transparency and Anti-corruption Practices, an Approach (1st ed.). Clear Lines Publications.

- Kisanyanya, A. (2018). Internal Control Systems and Financial Performance of Public Institutions of Higher Learning in Vihiga Country, Kenya. Journal of Business and Management, 20(4), 31–41.

- Kwanbo, L. M. (2009). Behavioural Accounting: A Means to Curb Corruption, a Window on Nigerian Local Government Councils. Journal for Forensic Accounting – Managerial Auditing Journal, 20(8), 844–866.

- Miller, D. K. (2007). Documenting Internal Controls from theory to implementation. http://cocubo.org/pdf/2007/chigo.

- Moraa, A. (2013). The Impact of Internal Control Systems and Financial Performance: The Case of Health Institutions in Upper West Region of Ghana. . International Journal of Academic Research in Business and Social Sciences, 7(4), 684–696.

- , U., & International Organization of Supreme Audit Institutions. (1980). Public Auditing Techniques for Performance Improvement. New York : United Nations.

- Ndegwa, T. (2013). Internal Controls for Small Business. Business Management Journal. Melbourne, Australia.

- Obi, V. A. O. (2004). Local Government Practice in Nigeria (1st ed.). Fulladau Publishing Company. Nsukka, Nigeria.

- Okpara, F. O. (2004). Public Sector Accounting. Journal of the Association of National Accountants of Nigeria.

- Olowolaju, M., & Ibukun-Falayi , R. O. (2016). Evaluation of Effectiveness of Internal Control System in Small Business Organizations in Ekiti State of Nigeria. European Journal of Business and Management, 8(31).

- Omolehinwa, E. (2001). Government Budgeting in Nigeria. Pumak Nig. Ltd, Lagos. https://edubirdie.com/examples/literature-review-on-internal-controls-and-revenue-collection

- Oshisami, K. (2015). Government Accounting and Financial Control (1st ed.). Evan Brothers Plc, Ibadan.

- Rezaee, Z. (2002). Financial Statement Fraud: Prevention and Detection. New York Willey.

- Sanusi, F. A., & Mustapha, M. B. (2015). The Effectiveness Of Internal Control System And Financial Accountability At Local Government Level In Nigeria. International Journal of Research in Business Management , 3(8), 1–6.

- Sebbowa, B. B. K. (2009). The Role of Internal Audit Functions in Organization.

- Singleton, A. J., Singleton, T. W., Boogna, G. J., & Lindquist, R. J. (2006). Fraud auditing and forensic accounting (3rd ed.). Wiley.

- Tamplin , T. (2023). Internal Controls. https://www.financestrategists.com/accounting/accounting-concepts-and-principles/internal-controls

- Transparency International Corruption Perceptions. (2006). http://www.transparency.org/policyresearch/surveys.indices/cpi/2006

- Venables, J. .S . R., & Impey, K. W. (1991). Internal Audit. (3rd ed.). UK: Butterworths . https://edubirdie.com/examples/literature-review-on-internal-controls-and-revenue-collection