Manufacturing and Structural Transformation Competitiveness in Algeria : An Analysis Through Key Statistics

- MELLAB Kahina

- 4519-4536

- Mar 24, 2025

- Economics

Manufacturing and Structural Transformation Competitiveness in Algeria : An Analysis Through Key Statistics

MELLAB Kahina

Research Center in Applied Economics for Development-CREAD -Algeria

DOI: https://dx.doi.org/10.47772/IJRISS.2025.9020357

Received: 15 February 2025; Accepted: 19 February 2025; Published: 24 March 2025

ABSTRACT

The article aims to use key statistics to gain a deeper understanding of the evolution of the manufacturing industry as a pivotal phase in the process of structural transformation within the Algerian economy. By examining these statistics, we will explore how the manufacturing sector has progressed and its role in the broader economic shift from agriculture to industrialization. Additionally, comparisons will be made to highlight the changes and developments in Algeria’s industrial landscape over time, providing insights into how this sector contributes to overall economic growth and competitiveness.

Keywords : Algeria, structural transformation, manufacturing industry, competitiveness, economic growth.

INTRODUCTION CONCEPTUAL FRAMEWORK OF STRUCTURAL TRANSFORMATION

Traditionally, the expressions “structural change” or “structural transformation” refer to the industrialization and tertiarization of the productive structure, which was previously dominated by the agricultural sector. During the second half of the twentieth century, structuralist economists such as Lewis (1954), Myrdal (1957), Rostow (1959), Kuznets (1966), and Kaldor (1967) presented analytical approaches to economic development as a process of structural transformation. These authors studied the mechanisms enabling traditional, wholly agricultural economies to transform into modern industrialized economies.

In this context, economic development is mainly understood as a process of economic modernization driven by the reallocation of production resources from a low-productivity sector (the traditional agricultural sector, which relies on traditional technology with diminishing returns) to a high-productivity, increasing-returns sector, namely modern industry. The accumulation of human and physical capital—common to all countries, despite their initial differences—conditions both the pace of structural transformation and the growth of the industrial sector. Over time, this process expands and evolves to include new factors emerging from the external environment, which can foster productivity growth, particularly institutional changes (such as ownership, for example) and regional shifts in the industrial production structure.

Other studies have linked structural transformation with geographical economics, particularly urbanization (as structural transformation between sectors is essential for understanding changes in population distribution) and inequality (or poverty). For instance, Gollin and Rogerson (2014) analyzed the impact of transport costs on agricultural productivity and its implications for the size of this sector. High transport costs penalize the economy in two ways : they reduce agriculture to a subsistence activity serving only final consumption, and at the same time, they increase production costs in the non-agricultural sector.

Demand side

Structural change is the result of various exogenous factors. In fact, the production structure, or Gross Domestic Product (GDP), is influenced by changes in domestic demand (Engel’s effect) and changes in export demand (expansion of exports, shifts in the composition of export demand). Furthermore, technological evolution alters lifestyles and consumption patterns, which in turn affect the structure of production. This is evident in the shift of employment from agriculture to industry, driven by the low income elasticity of demand for agricultural products. At a later stage, the role of the services sector becomes more prominent as the share of services in consumption increases significantly.

Supply side

The neoclassical view (Lucas, 1993 ; Harberger, 1998), among others, interprets the growth miracle as a miracle of productivity, with structural change being a means to reallocate productive resources (labor and capital) to more efficient uses. Differences in marginal productivity and productivity growth across sectors lead to the movement of input factors from low-productivity sectors to those with higher productivity. Much research from the supply-side perspective has focused on explaining the relationship between factor reallocation and productivity growth. In other words, these specific development models explain structural transformation as an endogenous process in response to the accumulation of factors that increase wealth, as well as sectoral demand properties and production functions.

Initially, Leamer (1987) proposed the “cones of diversification.” Then, within the framework of factor specialization theory, Schott (2003) revived the debate on these diversification cones by modeling the relationship between export diversification, capital accumulation, and income. However, comparative advantages change in relation to capital accumulation and the diversification cones. These elements determine successive specialization sequences, which are associated with changes in factor endowments.

From the 1980s onwards, modern theories of international trade and endogenous growth in an open economy filled this gap by proposing models linking the three notions : factor endowments, evolution of the productive structure, and economic growth

The Heckscher-Ohlin-Vanek (HOV) model on international trade predicts that the productive structure has a high level of aggregation (labor-intensive vs. capital-intensive sectors). According to the authors, several diversification cones may exist for countries that hold the same factor proportions, identical factor prices, and similar product sets. The theory thus confirms that net exports are linear functions of factor endowments.

In fact, the possibility of producing a variety of goods depends on the improvement of factor endowments. In practice, an economy with differentiated production factors can have competitive, diversified specialization. Therefore, export and production diversification depend on the accumulation of factor endowments and are compatible with the theory of comparative advantage.

According to Lectard (2017), in the first stage of structural transformation, or the first cone of diversification, an economy holds and exploits its initial comparative advantage ; it exports labor-intensive but low-skilled products. As economic development progresses, a country accumulates capital and transitions to the second stage of development. In this second cone of diversification, the country specializes in capital-intensive exports such as “machinery and transport equipment.” The shift to this cone is explained by significant diversification, typically in the automobile industry. As the economy accumulates more capital, it moves to the third cone and specializes in more sophisticated products, such as the chemical industry. When a country reaches the fourth cone of diversification, its productive structure becomes concentrated again, focusing on a small number of highly sophisticated and more complex products.

According to the author’s analysis, the logic of the diversification cones model suggests that as a country advances in development, even transitioning from one cone to another, the country diversifies its export basket further. This indicates that old specializations fade in the first stage and then decrease in the second stage, with the sophistication of existing products.

Lectard (2017) defines structural transformation (ST) as a process of diversification and sophistication of exports resulting from the accumulation of capabilities, ensuring that a country enters a virtuous circle of sustainable transformation over time. According to LEWIS (1954), structural change is the availability of conditions for transferring surplus labor from the traditional sector to a modern sector. Structural transformation is the reorientation of economic activity from low-productivity sectors to high-productivity sectors. For Kuznets (1966), structural transformation is the reallocation of economic activity from agriculture to non-agricultural sectors (manufacturing and services) that accompanies the process of modern economic growth. According to the author, modern economic growth is a process of technological innovation, marked by a sustained increase in productivity and the standard of living of the population. For Kuznets (1971), in modern economic growth, the sovereign state must act “as a center for exchanging necessary institutional innovations, as an agency for resolving conflicts between interest groups, and as a major entrepreneur for the socially required infrastructure.”

To define the policy of structural transformation, it is necessary to go further. Linear interpretations of the progression from primary sectors to secondary or tertiary sectors are evident in several recent works. The study by McMillan and Rodrick (2011) analyzes the relationship between structural change and productivity growth. They suggest that overall productivity growth can be achieved through productivity increases within sectors through capital accumulation, technological transformation, industrial rationalization (less productive firms disappear, while the remaining firms shed surplus labor), and other means, on one hand, and on the other hand, through the movement of resources from less productive activities to more productive ones. What should be retained from this definition is that structural transformation consists of two complementary elements: (i) the upgrading and strengthening of new, more productive activities, and (ii) the shift of resources from traditional activities toward these new activities, which enhances overall productivity. The absence of the first element prevents the economy from taking off, while the lack of the second means that productivity gains from leading sectors do not diffuse throughout the rest of the economy.

Thus, the African Development Bank (AfDB) in 2013 defines structural transformation as an intersectoral reallocation of economic activity from low-productivity sectors to those with higher productivity, thereby enabling sustained, strong, and inclusive growth. According to the AfDB, the process of ST is generally characterized by at least two stylized facts: (i) the increase in the share of the manufacturing and high-value-added services sectors in GDP, coupled with a sustained decrease in the share of agriculture; and (ii) the decline in the share of agricultural employment and the transfer of workers to other, more productive sectors of the economy.

The UNECA, in its 2017 report on Africa, adds three more stylized facts: a redeployment of economic activity from rural areas to urban areas; a demographic transition that ensures a shift from high growth and mortality rates (common in underdeveloped and rural areas) to low growth and mortality rates (associated with better health standards in developed and urban regions), and increasing urbanization. The work of Lin (2011) on economic development, for example, links structural change to the acceleration of industrialization and urbanization, along with technological innovation and capital accumulation. This constitutes the new characteristics of industrialization.

Finally, we can say that modern structural change is manifested in the improvement of the performance of production factors, the densification and modernization of infrastructure networks, the development of institutions, changes in attitudes and values, and an upward movement of the entire social system. From these definitions, we learn that several economic forces contribute to transforming the economy’s structure. In particular, public policymakers make economies increasingly attractive and competitive for investment. For this reason, structural transformation is a development issue that requires a very thorough diagnosis. Public, fiscal, and monetary policies play a key role. Therefore, the main policies derived from this definition are threefold: industrial innovation policies, technological policies, and competitiveness policies.

For a country to become competitive, industrial and technological policies targeting innovation must be combined with policies incentivizing and facilitating business operations. These policies are, in fact, prerequisites for joining Global Vale Chains (GVCs).

The Contribution of Different Sectors to the Structural Transformation Process

While the existing literature predominantly focuses on the manufacturing sector, is it the sole viable path for structural transformation and industrial development ? How can the primary and tertiary sectors also contribute to this process ? This section aims to explore the roles of the manufacturing, services, and primary sectors in driving the acceleration of structural transformation.

Empirical studies provide additional insights to those of Hausmann (2007), who centered on the sophistication of the export basket of goods. These studies underscore the significant role of the services sector in the broader development process. Notably, Rahul Anand, Saurabh Mishra, and Nikola Spatafora (2012), in an IMF working paper, highlighted the pivotal contribution of services to structural transformation. They further posited that the concept of sophistication extends beyond goods to encompass services as well. Over the last decade, services have substantially increased their share of global GDP, now accounting for approximately 70% of total output. The question arises: can the services sector emerge as a key driver in developing countries? The aforementioned authors sought to assess the evolution of exports of resources and manufactured goods from a new perspective, investigating whether countries are exporting similar products or engaging in entirely new economic activities. In this framework, exports are classified into four categories: “classic products,” “marginal products,” “disappearing products,” and “emerging products.”

Tableau n °1. Definition of “Classical”, “Marginal”, “Disappearing”, and “Emerging Products”

| Revealed Comparative Advantage (RCA) | ||

| 1990-94 2005-09 | ||

| Classical | >1 | >1 |

| Disappearing | >1 | <1 |

| Marginal | <1 | <1 |

| Emerging | <1 | >1 |

Source. Rahul Anand, Saurabh Mishra, and Nikola Spatafora (2012),” Structural Transformation and the Sophistication of Production”, IMF Working Paper.

A “classic” product refers to one for which a country has consistently demonstrated a revealed comparative advantage (RCA) across both subperiods. Specifically, the product’s share in the country’s total merchandise exports exceeds its share in global cross-border exports at both the beginning and the end of the sampling period. In contrast, “marginal” products are those for which the country has never exhibited an RCA. “Disappearing” products are those for which a country had an RCA at the beginning but not at the end of the period, while “emerging” products are those for which the country developed an RCA only by the end of the sampling period.

Additionally, the study examined the primary composition of export baskets in countries with low, middle, and high incomes, distinguishing between primary commodities and manufactured goods, and analyzing how these compositions evolved over two periods: 1980–2009. The results show that the share of manufactured goods in exports has increased substantially over time in high-income countries. By the end of the period, manufactured goods accounted for 90% of China’s exports. In contrast, primary commodities still represented 90% of Sub-Saharan Africa’s (SSA) exports.

Exports of manufactured goods from SSA, however, grew only slightly, from 7% of total exports in the 1980s to 13% by 2009. In other low-income countries, the share of manufactured goods in total exports actually declined over time, falling to just over 20%. Thus, while the export baskets of high-income countries are dominated by manufactured goods, those of low-income countries and SSA continue to be largely composed of primary and resource-based products.

The study further disaggregated exports of resources and manufactured goods into subcategories to provide a more detailed understanding of the export baskets of different regions. The export profiles of rapidly growing high-income countries differ markedly from those of low-income countries and SSA. In particular, for both low-income countries and SSA, natural resource exports are primarily composed of classic products, with very few emerging products. By 2009, emerging natural resource products, which these countries had previously lacked specialization in, made up 11% of SSA’s total exports.

How can the manufacturing sector contribute to structural transformation ?

Since 1950, a substantial body of theoretical and empirical research on economic development (Rodrik, 2008, 2009) suggests that the manufacturing industry holds significant potential for stimulating structural transformation. The expansion of manufacturing activities results from an interaction between demand- and supply-side factors. On the one hand, it generates income, employment, and demand, while on the other, it drives productivity gains that, in turn, foster income and demand growth.

As Kaldor (1966) highlights, the key characteristic of the manufacturing sector lies in its capacity to increase productivity and income. He observes that a high growth rate in manufacturing is associated with an increased rate of overall economic growth and total economic output. Consequently, income per capita is a monotonic function dependent on the level of development within the manufacturing sector, before it begins to decline. In this regard, Felipe and Estrada (2008) argue that this relationship evolves over time and takes on a U-shape. Furthermore, Rodrik (2006) confirms a monotonic relationship between manufacturing and economic growth.

What, then, makes the manufacturing sector so unique, and what are the arguments in favor of its expansion? The literature offers several answers to these questions. First, the manufacturing sector is closely connected to other sectors of the economy. Manufactured goods can serve both as final consumption products and as inputs for other sectors, creating complementarities and intersectoral linkages (Hirschman, 1958; Rosenstein-Rodan, 1943).

It is entirely plausible that, through production, investment, knowledge, and income linkages, the gains made by the manufacturing sector can spill over into the broader economy. However, the strength and importance of these linkages are crucial. For example, one sector might be strongly linked to another, yet the latter may contribute little added value to the economy. The concepts of upstream and downstream linkages, therefore, apply primarily to key sectors of the economy and influence industrial policy.

Hirschman (1958) explains that the expansion of production helps establish both upstream (e.g., automobile production stimulates investments in steel production) and downstream linkages (e.g., steel production boosts the emergence of an automobile industry). These intersectoral linkages—whether within the manufacturing sector or across other sectors—are pivotal. According to UNIDO (2009), intersectoral linkages emerge when efficiency gains and knowledge diffuse from manufacturing to primary sectors and services.

Regarding income, the effects of linkages arise when industrial development is accompanied by rising wages, contributing to a virtuous cycle through links to consumption. These effects can also be driven by public revenues (including fiscal linkages), leading to increased government spending. This, in turn, stimulates demand and GDP growth. Such income linkages create a self-reinforcing process of industrialization, boosting domestic demand and thereby promoting GDP growth.

It is important to note that the manufacturing sector offers advantages in terms of price elasticity and income elasticity. According to Engel’s law, as per capita income decreases, a larger share of income is spent on agricultural goods. As income rises, demand shifts from agricultural products to manufactured goods, thus encouraging manufacturing production. Moreover, the price elasticity and income elasticity of demand for consumer goods further stimulate manufacturing output. If industrialization succeeds, domestic demand for manufactured goods will be met. However, if a country does not industrialize, it will be forced to import manufactured goods. Given the significant price and income elasticities of the manufacturing industry, imports of manufactured goods can lead to foreign currency shortages and balance-of-payments difficulties.

Investments also create linkages when they are directed toward production capacity, entrepreneurial projects, and the expansion of manufacturing activities within a branch or enterprise. Additionally, when these investments trigger further investments in other sectors or firms that would otherwise not occur because profitability in a specific manufacturing project often depends on prior or parallel investments in related activities these spillover effects are significant.

Second, the manufacturing sector generates increasing static and dynamic economies of scale. Mass production leads to a reduction in costs for firms, meaning that unit costs decrease when production is scaled up. Specialization paves the way for a finer division of labor, and with accumulated production, firms learn to produce more efficiently. Furthermore, dynamic economies of scale can be harnessed when capital accumulation is accompanied by the use of increasingly advanced technologies, learning-by-doing, and knowledge development.

Third, manufactured products generate spillovers, offering opportunities for innovation and technological advancements in primary sectors, such as agriculture. Szirmai (2012) provides data on capital intensity between 1970 and 2000, demonstrating that in developing countries, this intensity is clearly lower in agriculture compared to manufacturing, making structural transformation toward the latter sector beneficial.

Fourth, manufacturing production requires modern technologies. Due to rapid capital accumulation rates, there is frequent adoption of new equipment and machinery. Moreover, it is increasingly evident that learning and innovation also play a role in the services sector, as well as in knowledge-based sectors (e.g., biotechnological applications in agriculture or ICT applications in services).

How can the services sector contribute to structural transformation ?

Since the 1990s, there has been significant focus on the revolution in information and communication technologies (ICT) and the advent of the internet era, which has brought about three global forces often referred to as the 3Ts (technology, transportability, and tradability). These developments have led to the emergence of various services and agro-industrial sectors, including horticulture, which share similarities with the manufacturing sector. As noted by Newfarmer, Page, and Tarp (2018), industries such as tourism, agro-industry, horticulture, transportation, and ICT are creating job opportunities and enabling faster structural transformation, particularly in Africa.

Similar to the manufacturing sector, these “industries without smokestacks (IWOSS)” exhibit characteristics akin to manufacturing, such as exchangeability, negotiability, and the benefits derived from technological progress. Their costs depend on economies of scale, agglomeration, networks, and labor division. Additionally, they offer high value-added per worker and absorb a substantial number of moderately skilled workers.

Moreover, service exports are no longer merely an input in trade in goods; they are increasingly becoming a final export consumed directly and are not subjected to many of the trade barriers that physical exports must overcome. According to Dasgupta and Sing (2005), some modern services, such as those leveraging ICT, can have positive effects on structural change, much like those traditionally associated with the manufacturing sector in terms of increasing productivity, employment, and the creation of linkages through international trade. Modern services include business processing, accounting, consulting, education, remote access services, medical record transcription, entertainment, production services, design, and marketing. This means that the services sector encompasses a much wider range of activities, from consumer services, which typically require little qualification and have low productivity, to business services that use highly skilled labor and involve high technological intensity.

As export-based industrialization becomes more challenging, the potential for service-driven growth has garnered significant interest, particularly in many developing countries where growth has been slower, while other nations have successfully embraced this path. In the absence of a solid manufacturing base, there are few countries where services—being highly heterogeneous sectors—play a central role in accelerating structural transformation.

According to UNIDO (2013), the significant contribution of services to employment might be due to statistical illusions, as many activities (e.g., cleaning and security services) are outsourced by businesses to specialized providers. Furthermore, the contribution of services to job creation and productivity depends on the composition of the sector. In terms of service categories, productivity is highest in sectors like financial services, real estate, insurance for businesses, communications, transport, and warehousing, compared to other service sectors like trade, hospitality, and food services. The first category of services requires a highly skilled workforce, while the latter can be outsourced by manufacturing industries.

Baumol’s (1967) study negatively assessed structural change towards services, formulating a two-sector model in which the first sector has constant labor productivity, while in the second sector, labor productivity grows cumulatively at a constant compounded rate. Baumol concluded that the opportunities for productivity growth in the services sector are limited, and thus the increasing share of services in production would lead to a slowdown in overall productivity growth. In the paper “Asia’s Productivity Performance and Potential: The Contribution of Sectors and Structural Change,” Bart van Ark and Marcel Timmer (2003) confirmed Baumol’s study in East Asia, noting that the negative impact of services on overall productivity in these countries was partly offset by the fact that productivity levels in some service sectors (e.g., ICT) are higher than in industry.

Low-productivity services, such as hospital services, can create jobs but result in minimal gains in overall productivity. However, the high productivity of certain service translates into rapid industrial productivity growth and higher wages and income. In India, services have played a substantial role as inputs to manufacturing activities, with the conclusion that India could diversify its economy by strengthening interactions and interdependencies between services and the dynamic manufacturing sector, eventually reaching maturity. Like India, Brazil experienced a remarkable increase in its revealed comparative advantage in business services during the 1990s. The import-substitution policy of both countries led to heavy investments in higher education institutions. The interaction of these skills with technological changes created a new comparative advantage in business service exports. For instance, Brazilian companies such as Odebrecht developed services for large turnkey construction projects, driven by an attractive domestic market, access to national public procurement markets, and other implicit subsidies. Despite the reduction in implicit and explicit subsidies for Brazilian construction companies due to austerity measures, skills endowments (and institutions that generate skills) in engineering, architecture, and other technical services remain the foundation of Brazil’s growing professional service exports.

In some African countries, there has been a shift of labor from the manufacturing sector to services, which grew by an average of 12 percentage points between 2000 and 2012. However, the added value from services in Africa largely comes from low-productivity services.

From this, it follows that in countries where industrialization has stalled at a low level of manufacturing value-added, services have less of a chance to contribute to driving structural transformation. This is further compounded by the low per capita income, which cannot generate demand for consumer services requiring high levels of technology and qualifications, nor by the fact that the manufacturing industry has not yet reached the stage that would encourage business services to contribute to manufacturing sector productivity growth.

However, developing countries can still leverage service exports by exploiting their static resources (e.g., tourism endowments such as historical sites). The tourism sector, for instance, whose exports are an important component, can be a source of employment and foreign exchange, and even create upstream linkages with the manufacturing sector. For the tourism sector to develop and contribute to overall productivity in the economy, appropriate infrastructure is essential. In fact, infrastructure services can provide intermediate inputs for all economic sectors. This growing importance of services in all economic activities, known as “servicification,” facilitates production and exports throughout production processes, particularly at the administrative and production stages (e.g., control and engineering functions, as well as the stages of installation and pre-sales).

How can the primary sector contribute to structural transformation ?

Through various linkages with the production of raw materials, several countries have initiated their industrialization process. Consider, for example, Malaysia, Chile, and Indonesia, which have managed to ease their external constraints. In contrast to countries rich in natural resources, which still face challenges related to the “resource curse,” whereby an abundance of natural resources discourages structural change, these countries have succeeded by efficiently managing these resources and maintaining fiscal discipline. It is not enough for a state to simply collect resources; they must be used effectively. Additionally, annual expenditures must not exceed total natural revenues.

While the goal of transformation is to reduce the share of the primary sector in GDP and employment, this sector can create a dynamic interaction between the production and export of raw materials, diversifying the economy and driving the manufacturing sector forward. Downstream, the primary sector can have links to the local manufacturing sector as a source of raw materials. In many resource-rich countries, this sector is considered industrializing. Upstream, this sector can create linkages with local services and goods that are needed as inputs.

Furthermore, net exports of raw materials generate foreign exchange earnings, which a country can use to finance imports of intermediate goods and equipment necessary for developing manufacturing capacity and modernizing the technological capabilities of the sector, while reducing reliance on foreign borrowing. Additionally, revenues from gas, mining, and oil resources are crucial for the state budget, thus enabling public investments and the provision of public goods. These public goods include education, vocational training, research and development, the development of new, more sustainable infrastructures, and business services. In this context, Henn, Papageorgiou, and Spatafora (2013) state that an increase in the standard deviation of institutional quality improves its quality by 0.3. Public spending can finance economic diversification while attracting additional private investment. Assuming that public funds are well allocated to an economic policy with incentives (such as structural reforms or promoting investments), it is important to remember that historical development take-offs in low-income countries have been accompanied by significant increases in productivity in major economic sectors : industry, agriculture, and services.

Since domestic markets are relatively small, the diversification of production and exports is part of the same process. That is, the diversification of domestic production and foreign trade are usually interconnected. Therefore, diversification measures should not be limited solely to trade transactions but should also focus on the domestic sector.

In summary, structural transformation is primarily about a country’s ability to produce a variety of manufactured goods and services, and then its ability to market them (i.e., from production diversification to export diversification). You cannot export what you do not produce. Diversification of production can not only generate growth benefits but also reduce growth volatility, as new goods and services will eventually be exposed to different demand and supply shocks compared to existing goods and services.

According to the IMF’s estimates (2016) for the WAEMU region, the benefits of diversification are significant. For example, a 1 percentage point increase in labor from agriculture to manufacturing (while keeping sectoral levels constant) leads to a 1.1% increase in production due to the large gap in labor productivity between the two sectors. In fact, a 1% increase in agricultural productivity (assuming resource reallocation is constant) generates a 0.3% increase due to the concentration of labor in this sector. This highlights the importance of GDP distribution in developed countries where industrialization is progressing positively.Haut du formulaire

Bas du formulaire

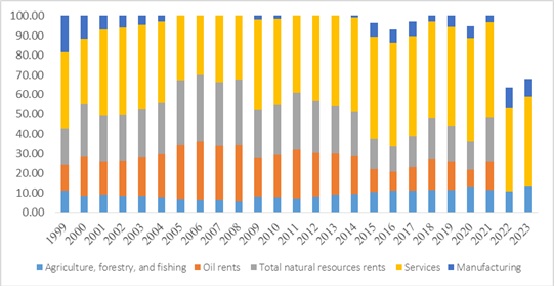

Graph 1. Sectoral Share in Gross Domestic Product in Algeria

Source. World Bank.

Focusing on Algeria’s manufacturing industry, the data reveals a concerning downward trend over the years, significantly limiting the country’s capacity to integrate into global value chains. From a robust contribution of 44.98% of GDP in 2000, the manufacturing sector has sharply contracted, reaching just 9.30% in 2023, signaling a considerable loss of industrial capacity and global competitiveness. This decline is most pronounced in key sub-sectors such as chemicals, textiles, and machinery and transport equipment. Chemicals, which once made a more substantial contribution to manufacturing value-added, now represents only 0.39% of total manufacturing output. Similarly, the textiles and clothing industry, which had accounted for 20.91% of the manufacturing value in 1974, now contributes a mere 0.88%. Machinery and transport equipment has also seen a dramatic reduction, dropping from 5.08% in 1974 to 0.60% in 2023. Although other manufacturing still holds the largest share, it is mainly composed of low-value-added industries, contributing over 87% in recent years. This over-reliance on labor-intensive, low-tech industries stifles Algeria’s ability to diversify and produce higher-value goods that are essential for entering global value chains. Modernizing the sector, especially by investing in high-tech and medium-tech manufacturing, is crucial for strengthening Algeria’s integration into international trade and fostering sustained economic growth. Without a more competitive and technologically advanced manufacturing base, Algeria faces challenges in capturing high-value markets and contributing meaningfully to regional and global supply chains. The ongoing lack of innovation and modernization in manufacturing makes it difficult for Algeria to fully capitalize on opportunities within the global economy, preventing the country from diversifying beyond its reliance on oil and gas exports.

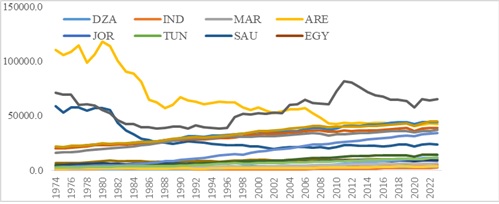

Graph 2. GDP per capita (constant 2015 US$) in selected countries

Source. WDI

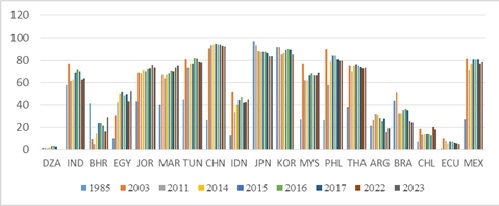

Graph 3. Manufactures exports (% of merchandise exports)

Algeria’s low percentage of manufactured exports, which has seen a significant decline from 1.51% in 1985 to 1.34% in 2003 and further decrease there after, can be explained by several key factors, especially when compared to other countries:

- Dependence on oil and gas exports: The Algerian economy is heavily reliant on oil and natural gas exports, which make up a large portion of its foreign exchange earnings. This dependence on natural resources has led to an underdevelopment of the manufacturing sector. For comparison, countries like China (91.88% in 2023) and India (63.55% in 2023) have seen substantial growth in their manufactured exports, driven by significant investments in industrialization. While Algeria’s focus on hydrocarbons limits its industrial development, countries like Tunisia (77.66% in 2023) and Morocco (74.75% in 2023) have been successful in boosting their manufacturing exports, indicating the importance of a diversified industrial base.

- Lack of investment in industry: Although Algeria has implemented some economic reforms, the country has historically lacked substantial investments in industrial sectors, limiting the growth of its manufactured exports. In contrast, China‘s robust manufacturing sector has led to exponential growth in its manufactured exports, rising from 26.43% in 1985 to 91.88% in 2023. Similarly, Malaysia (68.39% in 2023) and Thailand (72.97% in 2023) have been able to develop a strong industrial base, benefiting from both local and foreign investments.

- Economic and political instability: Algeria has experienced periods of political instability, particularly during the civil war in the 1990s, which disrupted the investment climate and slowed industrial growth. This contrasts with the steady growth observed in countries such as Japan (83.56% in 2023) and South Korea (89.27% in 2017), where stable political environments have fostered industrialization and strong export growth in manufactured goods. While Algeria has made some strides in economic stability, the political environment still poses a challenge for long-term industrial development.

- Lack of diversification: Unlike other emerging countries that have focused on industrialization and export diversification, Algeria has not managed to develop a diversified industrial base to boost its manufactured exports. For instance, Mexico (78.19% in 2023) has increased its manufactured export share steadily, largely due to its participation in trade agreements like NAFTA. Countries like Brazil (24.09% in 2023) and Argentina (18.95% in 2023), while heavily reliant on raw materials, have still managed to increase their share of manufactured exports compared to Algeria.

- Global competition: On the global stage, Algeria faces strong competition in the manufacturing sector, particularly from countries like China and India, which have heavily invested in their manufacturing sectors, making it more difficult for Algeria to compete globally. Additionally, nations like Indonesia (44.71% in 2023) and Philippines (79.50% in 2023) are also emerging as key players in manufacturing exports, showing how Algeria’s lack of competitiveness in this sector limits its global market share.

In summary, Algeria’s low share of manufactured exports is largely due to its reliance on hydrocarbons, lack of investment in industrial sectors, economic and political instability, and the absence of policies promoting industrial diversification. Compared to countries like China, India, Malaysia, and Tunisia, which have successfully developed robust manufacturing sectors, Algeria’s economic structure and focus on natural resources have hindered its ability to compete in the global manufactured goods market. To increase its manufactured exports, Algeria will need to invest in structural reforms, encourage industrialization, and diversify its economy.

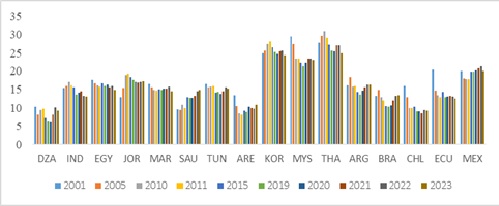

Graph 4. Manufacturing, value added (% of GDP) in selected countries

The data provided demonstrates the evolving role of the manufacturing sector across several countries and its fluctuating contribution to GDP over the years from 2001 to 2023. In countries with emerging economies, such as India (IND) and Thailand (THA), manufacturing has seen a substantial role in driving industrialization and growth, although these nations experienced some decline in recent years. India, for instance, has seen a slight dip in the manufacturing share from 15.3% in 2001 to about 12.9% in 2023, signaling shifts in the economic structure, possibly due to a greater focus on the service sector.

On the other hand, South Korea (KOR), an industrial powerhouse, consistently maintains a significant share of manufacturing in GDP, showcasing its strength in high-tech industries and manufacturing. South Korea’s contribution remained between 24-28% over the period, indicating its stable industrial base despite global economic fluctuations. Malaysia (MYS) and Thailand (THA) have similarly maintained strong manufacturing sectors, with Malaysia’s contribution dropping slightly over time but still remaining significant at about 23% in 2023. Contrastingly, countries like Egypt (EGY), Algeria (DZA), and Brazil (BRA) have seen considerable declines in manufacturing’s share of GDP. For example, Egypt’s contribution dropped from 17.7% in 2001 to 14.9% in 2023, while Algeria’s declined from 10.3% in 2001 to just 9.3% in 2023. This decline could be indicative of a shift toward other sectors such as natural resources or services, or potentially the result of economic challenges like political instability or lack of investment in manufacturing. Countries such as Morocco (MAR) and Tunisia (TUN) have shown relatively stable contributions over time, albeit with some minor fluctuations. Morocco’s manufacturing share remained close to 15% in 2023, and Tunisia’s contribution stayed around 15% for much of the period, reflecting ongoing industrial development in these economies.

Finally, Latin American countries like Argentina (ARG) and Mexico (MEX) exhibit varying trends. Argentina’s manufacturing sector showed a decline in the earlier part of the period, although it remained steady around 15% of GDP in recent years. Mexico, on the other hand, experienced some growth in the sector, particularly from 2015 onward, with the share of manufacturing rising to about 20% by 2023.

In conclusion, the data highlights the complex and varied role of manufacturing in different countries. While advanced industrial nations like South Korea maintain a strong manufacturing presence, many developing economies face challenges in sustaining industrial growth, as seen in the fluctuating shares of manufacturing in GDP. These trends may indicate shifts towards services or natural resources and reflect the broader global economic changes and structural transitions occurring in these nations.

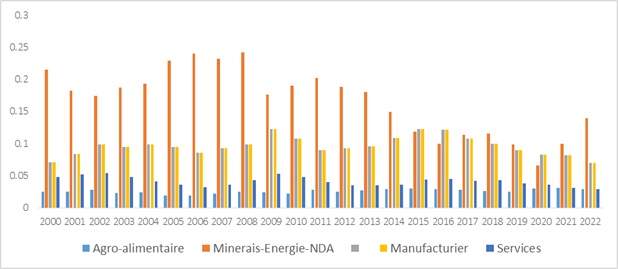

Graph 5. Degree of Openness in Algeria (as a % of GDP)

Source. WDI

Countries with a high degree of openness are more likely to participate actively in Global Value Chains (GVCs), as they gain access to global markets and resources, enabling them to specialize in specific stages of production, such as assembly or raw material supply. Openness also facilitates a shift in industrial structure, where developing countries may focus on labor-intensive tasks, while developed nations concentrate on high-value-added activities like R&D, design, and management. Moreover, open economies attract foreign direct investment (FDI), which further integrates them into GVCs through multinational corporations seeking cost advantages and global market access. While openness makes countries more vulnerable to global disruptions, it also offers resilience, as GVCs allow firms to adapt by relocating production and sourcing. Ultimately, a high degree of openness promotes deeper integration into GVCs, driving economic growth, industrial development, and specialization in global manufacturing networks.

The analysis of Algeria’s manufacturing sector, in relation to its degree of openness and integration into global value chains, highlights the challenges the country faces in diversifying its economy. Although Algeria has initiated a gradual opening since the 2000s, this dynamic has remained relatively weak, especially in terms of the manufacturing sector, which has not experienced sufficient growth to reduce its economic dependence on hydrocarbons. The manufacturing sector’s share of GDP has remained below 0.1% for much of the last two decades, and it has even declined since 2015, indicating that the country’s integration into global value chains is limited. Several factors explain this weak manufacturing performance, including heavy reliance on oil and gas exports, which continue to dominate the economy and attract investment, as well as slow industrialization that has not been sufficiently supported by appropriate structural reforms. Barriers to integration into global value chains include outdated infrastructure, low competitiveness due to a lack of advanced technology and human capital, and issues related to bureaucracy and the business climate.

Moreover, foreign direct investment (FDI) in the manufacturing sector has remained limited due to rigid regulations, a lack of diversification in local industries, and economic instability. As a result, Algeria has not been able to diversify its exports, and the integration of its manufactured goods into global value chains remains marginal. This lack of industrial diversification is a major obstacle to the structural transformation required to shift from an extractive economy to a more diversified, innovative, and competitive one. The current situation shows that deep economic reforms, focusing on improving infrastructure, education, innovation, and investment attractiveness, are essential to enhance global economic integration and stimulate the development of the manufacturing sector.

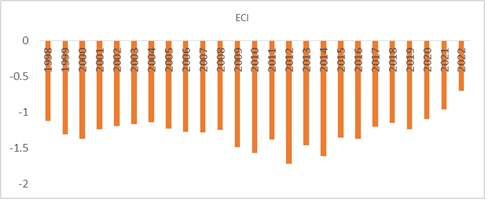

Graph 6. Economic Complexity in Algeria 1998-2022

Source. OEC

Economic Complexity, a rank of countries based on how diversified and complex their export basket is. Countries that are home to a great diversity of productive know-how, particularly complex specialized know-how, are able to produce a great diversity of sophisticated products.

The complexity of a country’s exports is found to highly predict current income levels, or where complexity exceed expectations for a country’s income level, the country is predicted to experience more rapid growth in the future. ECI therefore provides a useful measure of economic development.

The Economic Complexity Index (ECI) for Algeria from 1998 to 2022 shows an economy that was initially under-diversified and heavily reliant on oil and gas exports, with ECI values consistently negative, ranging from -1.12 to -1.49 from 1998 to 2010. Although the ECI slightly improved between 2011 and 2015, it remained generally low, reflecting an economy with limited complexity. However, from 2016 onwards, a gradual improvement was observed, reaching -0.7 in 2022, suggesting successful but slow efforts towards diversification. Algeria appears to be progressing toward a more diversified economy, but it still remains largely dependent on traditional sectors, requiring further reforms to increase its economic complexity.

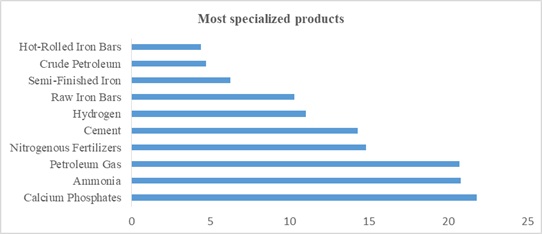

Graph 7. Most Specialized Products by RCA Index

Source. OEC

The graph shows the RCA trade values of various products, indicating their level of specialization in global markets. Products like Calcium Phosphates (21.82), Ammonia (20.78), and Petroleum Gas (20.7) have the highest values, suggesting they are more specialized, likely due to their niche markets or specific industrial demand. Nitrogenous Fertilizers (14.8) and Cement (14.28) are moderately specialized, with broad global demand but less concentration. Hydrogen (11), while important, is somewhat less specialized. On the other hand, products like Raw Iron Bars (10.28), Semi-Finished Iron (6.26), Crude Petroleum (4.7), and Hot-Rolled Iron Bars (4.41), being more basic materials, show lower RCA values, indicating they are less specialized, with high competition and broader markets.

The analysis suggests that chemical products and gases tend to be more specialized, while raw materials like iron and petroleum are more common commodities in global trade. However, Algeria does not hold a comparative advantage in manufacturing, limiting its ability to integrate into global value chains. The country’s reliance on raw material exports, without a strong manufacturing base, prevents it from capturing higher value-added opportunities in international trade.

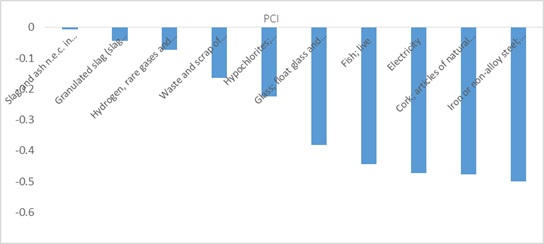

Graph 8. Most Complex Products by PCI

Source. OEC

The highest complexity exports of Algeria, according to the Product Complexity Index (PCI), are slag and ash n.e.c. in chapter 26 ; including seaweed ash (kelp) (-0.0068), Granulated slag (slag sand) from the manufacture of iron or steel (-0.043), Hydrogen, rare gases, and other non-metals (-0.072), Waste and scrap of paper and paperboard (-0.16), and hypochlorites ; commercial calcium hypochlorite ; chlorites ; hypobromites (-0.22). The PCI measures the knowledge intensity of a product by considering the knowledge intensity of its exporters.

This highlights the manufacturing industry’s role in Algeria’s export structure and its relationship to structural transformation. The low PCI values for these products suggest that while they are important exports, they are less knowledge-intensive compared to more complex products. This points to an industrial sector in Algeria that may still be in the process of structural transformation, shifting from raw material-based exports to more sophisticated, knowledge-intensive industries. Improving the complexity of exports would require advancements in technology, innovation, and skills development, allowing Algeria to transition toward higher-value, higher-complexity manufacturing and export activities.

Graph 9. Exports in Algeria (2023)

Source. WDI

In 2023, Algeria’s total exports amounted to $52.4 billion, positioning the country as the 57th largest exporter globally. Over the past five years, Algeria has seen a significant increase in its export value, growing by $10.3 billion from $42.1 billion in 2018 to $52.4 billion in 2023. This growth reflects a dynamic shift in Algeria’s trade patterns, both in terms of value and the types of goods being exported.

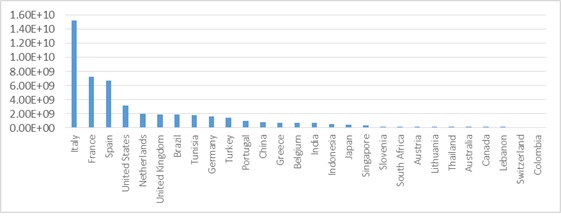

Breakdown of Exports by Sector

The leading exports from Algeria are energy-related products, primarily fossil fuels, which dominate the country’s export portfolio. Petroleum gas stands out as the top export, with a value of $27.2 billion in 2023. Crude petroleum follows closely, contributing $14.1 billion to the total exports. This heavy reliance on hydrocarbon exports highlights Algeria’s status as a key energy supplier, particularly to European markets.

Additionally, refined petroleum ($5.7 billion), nitrogenous fertilizers ($1.34 billion), and cement ($517 million) are also among the country’s top exports. The presence of nitrogenous fertilizers suggests a diversification within the chemical and agricultural sectors, albeit still within products tied to the energy sector, considering fertilizers’ reliance on natural gas for production.

Trade Partners and Export Destinations

Algeria’s export destinations reflect its geographical and historical trade relationships, with European countries taking the lead in importation. Italy is the largest importer of Algerian goods, receiving $15.2 billion worth of exports. Italy’s role as a major European energy hub likely contributes to its position as the primary market for Algerian petroleum products. Following Italy, France remains a significant trading partner, with exports to this country amounting to $7.29 billion. France’s long-standing ties with Algeria, as well as its reliance on energy imports, further solidify this trade relationship.

Spain, another European country, imports $6.73 billion worth of Algerian goods, further illustrating Algeria’s strong trade connections with Southern Europe. The United States and the Netherlands round out the top five destinations, importing $3.14 billion and $2.04 billion respectively. These markets tend to import a mix of energy products, including petroleum and natural gas, as well as potentially some of Algeria’s other industrial exports, such as fertilizers and cement.

Graph. Destinations of Algerian Exports in 2023

Source. WDI

Implications for Algeria’s Economy and Trade Strategy

Algeria’s export profile is heavily weighted towards energy exports, which makes the country vulnerable to fluctuations in global energy prices and demand. The dominance of petroleum and natural gas in its exports underlines the importance of maintaining and expanding its energy production capacity. However, the recent export growth also signals some diversification within Algeria’s export basket, with a modest increase in non-energy exports like fertilizers and cement.

Given the competitive energy market and the transition to renewable energy in many parts of the world, Algeria may benefit from further efforts to diversify its economy by increasing exports in high-value-added sectors, such as manufacturing, technology, and agriculture. To reduce its reliance on energy exports, Algeria could focus on enhancing its industrial base, improving technological capabilities, and creating value-added products. Expanding trade relationships beyond traditional European partners and exploring emerging markets, particularly in Asia and Africa, could also help secure future growth for Algerian exports.

In conclusion, while Algeria’s export sector is currently dominated by energy products, its ongoing growth in export value indicates a positive trajectory. For continued success, the country must balance its strong energy exports with efforts to diversify its export portfolio and expand trade relations on a global scale.

CONCLUSION

This article has explored Algeria’s manufacturing and structural transformation competitiveness, focusing on key export statistics and their implications for the country’s economic future. The country’s economic structure remains heavily reliant on the hydrocarbon sector, with petroleum and natural gas products constituting the bulk of its exports. However, recent trends in export diversification, especially in the areas of nitrogenous fertilizers and cement, indicate that Algeria is making strides toward enhancing its industrial base.

Algeria’s manufacturing sector faces several challenges, including low technological intensity in its exports, as indicated by the Product Complexity Index (PCI). The reliance on energy exports, particularly low-value-added products like crude oil and gas, limits the potential for economic diversification. Moving forward, Algeria’s ability to achieve structural transformation will depend on its efforts to foster innovation, improve technological capabilities, and invest in skill development within its workforce. Policies that encourage private sector development, increase manufacturing capacity, and integrate renewable energy technologies could help accelerate this transition.

Moreover, Algeria’s current trade patterns suggest a continued strong relationship with European markets, especially Italy, France, and Spain, while also presenting opportunities to explore emerging markets in Asia and Africa. By diversifying its export portfolio and creating value-added products in non-hydrocarbon sectors, Algeria could reduce its vulnerability to external shocks, particularly in the face of global energy market fluctuations.

In conclusion, Algeria’s competitiveness in manufacturing and structural transformation is evolving but faces significant hurdles. To ensure sustained economic growth and competitiveness, the country must focus on advancing its industrial sector through technological innovation, capacity building, and global market diversification.

Algeria’s path toward enhancing its manufacturing sector and achieving structural transformation can be better understood by comparing it with other successful models of industrialization and diversification. Notably, countries such as Malaysia and South Korea present valuable lessons in transitioning from resource-dependent economies to advanced industrial economies.

Malaysia’s successful transformation from a primary commodity exporter to a more diversified economy offers valuable insights. By heavily investing in manufacturing industries, particularly in electronics and machinery, Malaysia managed to reduce its reliance on raw materials. The country’s strategic focus on education, technology transfer, and infrastructure development, coupled with proactive industrial policies, allowed it to diversify its exports significantly. Algeria can take a page from Malaysia’s playbook by fostering a robust manufacturing sector, creating incentives for technology-driven industries, and improving the skillset of its workforce.

South Korea, which once faced similar challenges in transitioning from a resource-dependent economy, is another relevant comparison. By investing in heavy industries like shipbuilding, steel, and automobiles, alongside continuous research and development (R&D) efforts, South Korea was able to shift towards high-tech and value-added industries. The country also prioritized creating a conducive environment for private sector growth, fostering innovation, and investing heavily in higher education. Algeria could draw inspiration from South Korea’s emphasis on high-tech sectors and innovation-driven growth.

While Algeria has made strides in sectors like fertilizers and cement, it still lags behind countries like Malaysia and South Korea in terms of industrial competitiveness and export diversification. Recognizing these challenges, Algeria must adopt a similar multi-faceted approach investing in education and skill development, enhancing technological capabilities, and creating a favorable business environment to foster innovation and private sector engagement.

International organizations such as the World Bank and UNCTAD have acknowledged Algeria’s potential for structural transformation, particularly in its efforts to diversify the non-hydrocarbon sector. However, achieving global competitiveness in manufacturing will require continued policy reform, infrastructure development, and fostering industrial partnerships, much like the strategies employed by Malaysia and South Korea. While Algeria has made progress, it is essential for the country to adopt and adapt successful elements from other industrializing nations. With the right strategies and investments, Algeria can significantly enhance its competitiveness in manufacturing and move towards a more diversified and sustainable economic future.

Targeted Policy Recommendations for Algeria:

- Infrastructure Development: Propose initiatives to upgrade critical infrastructure, including transport networks (roads, rail, ports) and utilities (electricity, water supply), that can reduce operational costs for manufacturers and increase connectivity for exports.

- Public-Private Partnerships (PPPs): Recommend creating a more favorable environment for PPPs, which could include tax incentives, risk-sharing mechanisms, and streamlined regulatory processes to attract private investment in public infrastructure projects.

- Incentives for Foreign Direct Investment (FDI): Suggest policies like tax breaks, reduced tariffs on machinery and technology imports, or establishing special economic zones to attract foreign investors, particularly in high-value manufacturing sectors such as automotive, electronics, and renewable energy.

South Korea’s Industrial Policy: Highlight how targeted government support, such as technology transfer, R&D funding, and industrial clusters, helped South Korea develop a robust manufacturing sector. Germany’s Dual Education System: Demonstrate how Germany’s vocational training programs, combining in-class education with on-the-job experience, have created a highly skilled workforce that supports advanced manufacturing industries.

China’s Special Economic Zones (SEZs): Show how China used SEZs to attract FDI and develop export-driven manufacturing, which could offer insights for Algeria as it seeks to diversify its economy away from oil dependency.

Sociopolitical Analysis:

Political Stability and Governance: Analyze how political stability (or lack thereof) can influence the policy environment for industrialization, and propose reforms to improve transparency, reduce corruption, and create a more predictable business climate.

Social Inclusion and Labor Market Dynamics: Address the role of education and workforce development in supporting industrialization. Consider how to ensure that Algeria’s youth population, which represents a large proportion of the workforce, is equipped with the necessary skills for manufacturing jobs.

Engaging with Local Stakeholders:

Collaboration with Local Experts: Involve local economists, business leaders, and policymakers to incorporate perspectives on Algeria’s unique challenges and opportunities. This could be done through interviews, surveys, or roundtable discussions.

Industry-Specific Feedback: Engage with leaders from key industries (e.g., textiles, food processing, or electronics) to identify specific obstacles they face in the local environment and how tailored policies could address those concerns.

By integrating these elements, the paper would offer a comprehensive, multifaceted approach to industrialization in Algeria. It would not only provide actionable policy proposals but also demonstrate a deeper understanding of the unique challenges facing the country, backed by global examples and local expertise.

BIBLIOGRAPHY

- Lewis, W. Arthur (1954). Economic Development with Unlimited Supplies of Labour. Manchester School, 22(2), 139–191.

- Myrdal, Gunnar (1957). Economic Theory and Underdeveloped Regions. London : Gerald Duckworth & Co.

- Rostow, W. W. (1959). The Stages of Economic Growth : A Non-Communist Manifesto. Cambridge University Press.

- Kuznets, Simon (1966). Modern Economic Growth : Rate, Structure, and Spread. Yale University Press.

- Kaldor, Nicholas (1967). Strategic Factors in Economic Development. Cornell University Press.

- Gollin, Douglas and Rogerson, Richard (2014). Productivity and Transport Costs in Agricultural Development. Review of Economic Dynamics, 17(4), 692–705.

- Lucas, Robert E. (1993). Making a Miracle. Econometrica, 61(2), 251–272.

- Harberger, Arnold C. (1998). The Selection of Efficient Production Techniques in Developing Countries. In Productivity Growth in Developing Countries (pp. 51–80). University of Chicago Press.

- Leamer, Edward E. (1987). Paths of Development in the Three-Factor Model of Heckscher-Ohlin. Journal of Political Economy, 95(5), 961–979.

- Schott, Peter K. (2003). One Size Fits All ? Heckscher-Ohlin Specialization in Global Production. Journal of International Economics, 60(1), 53–76.

- Lectard, Thomas (2017). Cones of Diversification and the Evolution of Structural Transformation. Journal of Economic Development, 42(1), 83–103.

- McMillan, Margaret and Rodrik, Dani (2011). Globalization, Structural Change, and Productivity Growth. In Structural Change and Economic Growth (pp. 17–39). The World Bank.

- African Development Bank (AfDB) (2013). African Structural Transformation : Drivers and Challenges. AfDB Publication.

- United Nations Economic Commission for Africa (UNECA) (2017). Economic Report on Africa : Industrializing in Africa. UNECA.

- Lin, Justin Yifu (2011). New Structural Economics : A Framework for Rethinking Development and Policy. World Bank.

- Anand, Rahul; Mishra, Saurabh; Spatafora, Nikola (2012). The Role of Services in Structural Transformation: New Insights from Emerging Markets. IMF Working Paper No. 12/170.