Monetary Policy and Inflation in Nigeria: Unraveling the Threshold Puzzle

- IRIABIJE Alex Oisaozoje

- Christopher Nyong Ekong

- Paul Atanda Orebiyi

- 77-91

- Apr 25, 2024

- Economics

Department of Economics, University of Uyo, Ikpa Road, PMB 1017, Akwa Ibom State, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804006

Received: 16 March 2024; Accepted: 23 March 2024; Published: 25 April 2024

ABSTRACT

In this study, we investigated the threshold effects of monetary policy on inflation using two policy tools (monetary policy rate and money supply) for Nigeria from 1980 to 2021. Country specific data on inflation and monetary policy variables controlled with literature specified variables were analyzed using threshold autoregression (TAR). We found a threshold level of 13.69 units and 11.19 units respectively for monetary policy rate and money supply growth capable of making monetary policy management behave differently in inflation control. As an instance, we found that within the periods when policies are below and above the threshold levels (Monetary policy rate, exchange rate and Money supply), only monetary policy rate and money supply growth will be statistically efficient in curtailing inflation in Nigeria. Exchange rate management is only effective in periods of low policy rate regimes. We recommend, among other things, that monetary policy management strive to keep inflation in the economy in line with policy threshold strength for effective price stability.

Keywords: Monetary Policy, Inflation, Low regime, High regime, Threshold Autoregression (TAR), Nigeria.

JEL Classification: E0, E5, E6

INTRODUCTION

Monetary policy and inflation dynamics represent two critical pillars of economic management, each playing a pivotal role in shaping the economic landscape of nations. In the context of Nigeria, a country with a diverse and rapidly evolving economic milieu, the interplay between monetary policy and inflation has become a subject of heightened significance. This paper endeavors to delve into the intricate relationship between monetary policy measures and inflationary trends in Nigeria, with a specific focus on unraveling the threshold puzzle that lies at the heart of this complex economic dynamic.

Nigeria, as one of the largest economies in Africa, has witnessed a myriad of economic transformations in recent decades. Against a backdrop of demographic shifts, globalization, and technological advancements, the nation’s monetary policy has been continually adapted to address emerging challenges and foster sustainable economic growth. Simultaneously, inflation, as a persistent economic phenomenon, has demanded astute attention from policymakers, given its potential to erode purchasing power, disrupt economic stability, and hinder long-term development.

The threshold puzzle in the context of Nigeria’s monetary policy and inflationary trends refers to the boundary beyond which policy interventions cease to be effective in mitigating inflation or maintaining price stability. Unraveling this puzzle requires a nuanced exploration of the intricate channels through which monetary policy tools influence inflationary pressures and the identification of critical thresholds that delineate the efficacy of these measures.

In the Nigeria’s macroeconomic management, the pursuit of price stability and economic growth has been influenced by two major policy thrusts. The structural adjustment programme (SAP) implemented in 1986 marked a significant shift, transitioning from a regulated framework to a self-market regulatory stabilization approach. This shift had a transformative impact on inflation and policy tools, leading to a notable increase in macroeconomic indices, including a surge in inflation rates. For example, the inflation rate, which stood at 16% in 1980, experienced a historical peak of 61% in 1988 and 77% in 1994. Financial prices also exhibited double-digit growth during these periods

In 2004, Nigeria witnessed a shift in economic policy focus towards inclusive domestic growth potentials, notably through the implementation of the National Economic Empowerment and Development Strategy (NEEDS). This shift had a discernible impact on macroeconomic performance. Under NEEDS, economic stability parameters underwent significant changes. Inflation, for instance, maintained much lower double-digit values, stabilizing at approximately 12% in 2005 and remaining below 14% in 2010. Financial prices, including the monetary policy rate, also stabilized at single-digit figures, registering 8% in 2007 and further decreasing to 6% in 2010.

Rising inflationary pressures in the economy are seen as hindering development, prompting debates on the balance between supporting the poor and advocating for development planning. Studies by Bassey and Ekong (2019), Amaning and Seidu (2020), and Asuquo (2012) present varying perspectives on the issue.

The persistent increase in the general price level is viewed as a significant macroeconomic challenge, causing uncertainty. In Nigeria, inflation has exhibited fluctuations, notably in 1983 (39%), 1988 (61%), and 1989 (45%). During these periods, the effectiveness of the monetary policy rate in curbing inflation appeared limited, fluctuating between a maximum of 26% (1993) and a minimum of 6% (1980-81). However, post-1995, the monetary policy rate demonstrated heightened efficacy in controlling inflationary pressures until 2021, where inflation peaked at 18.55% in 2016.

However, beyond 1995, monetary policy rate seems to be very effective in controlling inflationary pressure up until 2021. Within the period, inflation peaked at 18.55% (2016). At what policy level is inflation anti-stabilizing or vice versa? This study aims to determine the optimal threshold for the monetary policies/inflation relationship, critical for achieving government price stabilization objectives. The research seeks to explore the behavior of inflation under two regime switches and identify any traceable threshold relationship between monetary policy and inflation in Nigeria.

LITERATURE REVIEW

Conceptual Reviews

Monetary policy: Monetary policy constitutes specific measures enacted by the central bank to regulate the value, supply, and cost of money in an economy, with the overarching aim of achieving the government’s macroeconomic objectives. These objectives encompass economic growth, price stabilization, balance of payment equilibrium, employment generation, among others (Ezeanyeji, Obi, Imoagwu, and Ejefobihi, 2021).

According to Friedman (1968), monetary policy involves actions taken by monetary authorities, typically the central bank, to influence monetary and financial conditions by controlling the availability and cost of credit. The broad goals include sustainable output growth, price stability, and maintaining a healthy balance of payments position. Key instruments of monetary policy, such as the monetary policy rate, play a pivotal role in regulating dynamic economic variables that impact the prices of goods and services and, consequently, the value of money.

Inflation: Inflation, defined as the continuous increase in the general price level of goods and services in an economy, is a key focus of monetary policy. The erosion of the purchasing power of a currency resulting from rising inflation is considered detrimental to economic growth and development. Both economic and non-economic factors contribute to inflation. Milton Friedman’s monetarist argument posits that monetary factors primarily drive inflation, while Fisher’s proposition suggests that the expansion of the monetary supply elucidates the inflation rate. Inflation can also be caused by demand factors, where aggregate demand exceeds supply, cost factors such as rising production costs, or profit motives under specific market conditions. Non-economic factors, rooted in structural inefficiencies in areas like capital formation, institutional frameworks, labor force, production levels, agriculture, and unemployment structures, can also contribute to inflation.

Since the onset of the COVID-19 pandemic in late 2019, global inflation has been on the rise due to factors such as supply chain disruptions, labor shortages, surging commodity prices, and changes in consumption patterns. In 2022, world consumer prices rose to 8.8 percent, the highest since 2008, driven by higher commodity prices and persistent supply-side constraints exacerbated by the Russia-Ukraine conflict. This surge in global inflation is anticipated to have cascading effects on developing economies (Funjika, Mwila, and Mulenga, 2023).

Money supply: The quantity theory of money serves as a framework for comprehending price changes in relation to the money supply within an economy. Essentially, the theory posits that any increase in the money supply leads to a corresponding increase in the general price level, and conversely, a decrease in money supply results in a decline in prices. An implication of this theory is that the value of money is contingent on the available money supply. Therefore, an augmented money supply diminishes the value of money due to the resultant increase in inflation rates, consequently reducing purchasing power. Fluctuations in money supply alter the equilibrium between money supply and demand, influencing new equilibrium positions and prices that offer valuable insights into core price developments in Nigeria (Omanukwue, 2010).

Monetary Policy rate and Inflation

Figure 1: Inflation and Policy Rate in Nigeria(1980-2021)

Source: Authors

Figure 1 illustrates the correlation between the monetary policy rate and the price level in Nigeria spanning from 1980 to 2021. Early in the study period, inflation exhibited volatile fluctuations, notably in 1983 (39%), 1988 (61%), and 1989 (45%). Further spikes in inflation occurred between 1992 and 1995, with a minimum rate of 49% in 1992 and a maximum of 77% in 1994. During these periods, the monetary policy rate appeared ineffective in curbing inflation, fluctuating around a maximum of 26% in 1993 and a minimum of 6% in 1980-81. However, post-1995, the monetary policy rate demonstrated increased efficacy in controlling inflationary pressures, with inflation peaking at 18.55% in 2016 and reaching a single-digit minimum at 5% in 2007. The Central Bank of Nigeria has historically identified similar periods of high inflation, exceeding 30%, adversely impacting economic growth since the early 1970s (CBN, 2009)

Figure 2: Inflation and Money Supply in Nigeria(1980-2021)

Source: Authors

However, such contracting strength must be interpreted with caution. A consideration of the money supply/inflation relationship using the money supply growth rate reveals that most of the inflation offshoot in the economy cannot entirely be explained away from money supply (Figure 3). Infact, fluctuations in inflation grew side by side with fluctuations in the growth rate of money supply throughout the period. Money supply growth grew from 6% in 1981 to 14% in 1983. It further grew from 12% in 1984 to nearly 33% 1988 and peaked for the entire period in 63% in 1992. Incidentally, this peak paralleled the period of sustained high inflation (1992-1995). Ezeanyeji, Obi, Imoagwu and Ejefobihi (2021) confirmed that the growth of money supply is always correlated with the high inflation episodes because money growth was often in excess of real economic growth. Similarly, an analogous trend emerges when examining the relationship between inflation and money supply, as depicted in Figure 2. Notably, post-2005, efforts to moderate money supply have effectively mitigated inflationary pressures, a trend observed until the year 2021.

Figure 3: Inflation and Money Supply growth in Nigeria(1980-2021)

Source: Authors

The observed decline in inflationary pressures should be approached with caution, as an examination of the money supply/inflation relationship, specifically through the money supply growth rate (Figure 3), indicates that a significant portion of inflation in the economy cannot be solely attributed to changes in money supply. Fluctuations in inflation closely paralleled the variations in the growth rate of money supply throughout the analyzed period.

Money supply growth exhibited notable increases, rising from 6% in 1981 to 14% in 1983. Subsequently, it surged from 12% in 1984 to nearly 33% in 1988, reaching its peak at 63% in 1992. This peak coincided with a period of sustained high inflation from 1992 to 1995. Ezeanyeji, Obi, Imoagwu, and Ejefobihi (2021) affirmed a correlation between money supply growth and episodes of high inflation, emphasizing that money growth often surpassed real economic growth.

Theoretical Literature

Numerous empirical studies have relied on the theoretical framework proposed by Fisher (1911) to elucidate the intricate connections between monetary policy and inflation. Researchers including Henry and Sabo (2020) and Ezeanyeji, Obi, Imoagwu, and Ejefobihi (2021) have incorporated Fisher’s specifications into their analyses. In its most straightforward expression, Fisher’s specification takes the form of a mathematical representation, serving as a foundational element in studies exploring the dynamics of monetary policy and inflation

MV=PY (1)

In equation (1), M is money supply; Y is gross domestic output; P is the general price level and; V is the velocity of circulation of money.

Equation (1) opines that under certain conditions, notably the constancy of V and Y, fluctuations in money supply produces an equal and opposite influence in the general price level. As Henry and Sabo (2020) outlined, the proportional relationship implies that a permanent increase in money growth leads to an equal increase in the rate of inflation over time.

The Fisher’s effect also give evidence to the existence of a long-term relationship in monetary policy and price stability. In its predictive form, Fisher’s effect links changes in domestic interest rate to domestic inflation baring inflation expectations thus;

it−πt=b1+ρ1t (2)

Where, i is norminal interest rate; π is inflation rate; p is real interest rate; b is an integer; t is time.

The standard view is that changes in short-term interest rates primarily reflect fluctuations in expected inflation inferring that they have predictive ability for future inflation. Mishkin (1992) and Funjika, Mwila and Mulenga (2023) have independently measured the Fisher parity in an effort to estimate inflation gap.

Monetary policy enters the aggregate demand function according to the Taylor’s rule

rt=pt-1+(1−p)(gππt+gyyt) (3)

Where rtis nominal interest rate, p captures the degree of policy inertia, gπ and gy measures the response of monetary policy to movements in inflation πt and the output gap ytrespectively. Accordingly, monetary authorities target the interest rate rtin the economy through policy adjustment to affect both price and output at appropriate levels (Kwapil and Scharler, 2006; Ekong and Ekong, 2022).

Empirical Reviews

Several studies have investigated the complex relationship between monetary policy and inflation across different countries and time periods.

Mehrara and Behzadi-Soufiani (2015): Investigated the nonlinear impact of monetary and fiscal policies on inflation in various economic regimes in Iran from 1990 to 2013. Used a threshold regression approach and identified a quarterly threshold for monetary and fiscal effects on Iranian inflation. Concluded that monetary policy had a greater impact on inflation during periods of low growth, highlighting its significance in inflation-regime switching.

Wauk and Adjorlolo (2019): Explored the relationship between inflation, monetary policy, and economic growth in Ghana from 1982 to 2017. Used the autoregressive distributed lag model (ARDL) and found that combined, monetary policy and inflation insignificantly dipped economic growth. Attributed this weakness to government interference in the central banking system, advocating for increased central banking independence.

Yusuf (2020): Examined the effectiveness of the monetary policy rate in curbing rising inflation in Nigeria from 1981 to 2019. Utilized cointegration and Granger causality analysis, revealing that a percentage rise in the policy rate increases inflation by nearly 4 percent. Suggested that the Central Bank should clearly communicate its policy objectives to effectively manage monetary policy variables.

Henry and Sabo (2020): Investigated the impact of monetary policy management on inflation in Nigeria from 1985 to 2019. Applied Fisher’s theoretical underpinnings to an Autoregressive Distributed Lag model, finding that the monetary policy rate and exchange rate reduced inflation, while inflation rose with increasing money supply. Suggested that reducing money supply could alleviate inflationary pressure.

Diaz-Roldan, Prats, and Ramos-Herrera (2021): Investigated the redefinition of monetary policy to lower the threshold at which monetary policy mitigates at zero bound. Utilized a dynamic panel threshold model for 19 countries in the Euro Area from 1999 to 2019, finding that inflation gap and output gap influenced short-term interest rates differently above and below a threshold.

Ezeanyeji, Obi, Imoagwu and Ejefobihi (2021): Examined the impact of monetary policy on inflation control in Nigeria from 1980 to 2019. Found unclear or insignificant impacts of both money supply and exchange rate on inflation control in Nigeria in the short and long run. Recommended efficient monetary policies to create a favorable environment for investment.

Hashemi-Dizaj, Hazeri-Niri, and Samadzadeh (2022): Investigated the effect of monetary policy on inflation in developed and developing countries from 1990 to 2019. Found varying policy magnitudes on inflation between developed and developing countries, emphasizing the need for income diversification away from oil in developing economies.

Funjika, Mwila, and Mulenga (2023): Explored the effect of monetary policy on inflation in Zambia, utilizing quarterly data from 2012 to 2022. Applied a Vector Error Correction Model and found strong impulses of monetary policy on inflation, suggesting its effectiveness. Recommended continued supply-side efforts to support monetary policy in targeting inflation reduction.

Ntshangase, Sheunesu, and Kaseeram (2023) examined spillover effect of US unconventional monetary policy on inflation in emerging markets after the 2007/2008 financial crisis and during COVID-19. Used a panel vector autoregression analysis for twelve emerging markets, finding statistically significant spillover impulses to both inflation-targeting and non-inflation-targeting economies.

Summary of Literature

The extensive review of existing literature reveals a rich landscape of studies investigating the intricate relationship between monetary policy and inflation. These studies, conducted across diverse countries using varied methodologies, have produced mixed results, underscoring the complexity of this economic dynamic. The adoption of inflation targeting by countries, providing a policy corridor for a targeted variable, has been a common theme. Notably, studies employing the Vector Error Correction Model have consistently shown supporting evidence for the links in the policy-inflation nexus.

Given the nuanced findings and the need for context-specific insights, this study aims to contribute significantly to the literature by investigating the threshold effects of monetary policy on inflation in Nigeria. Utilizing two key policy tools, namely the monetary policy rate and money supply, the research will cover the period from 1980 to 2021.

METHODOLOGY

The foundation for many studies in threshold analysis can be traced back to the work of Khan and Senhadji (2001), who adapted the panel methodology introduced by Hansen (2000). While early applications were primarily in debt and growth analysis, recent trends indicate a growing use of threshold analysis in various fields of finance (Omotosho, Bawa, and Doguwa, 2016; Bawa and Abdullahi, 2011). This methodological approach has expanded to include studies in diverse financial contexts (Houngb´edji and Bassongui, 2023; Diaz-Roldan, Prats and Ramos-Herrera, 2021; Mehrara and Behzadi-Soufiani, 2015).

We follow the specification by Omotosho, Bawa and Doguwa (2016) and Mehrara and Behzadi-Soufiani (2015) with some modifications as

for (σt≤∁σt>∁)

In equation (4) πtis inflation as the dependent variable; ϑ0is the relationship specific effect between inflation and monetary policy; ϑidenotes policy effect impacts on inflation; xitis monetary policy tools that affect inflation; ϵtis the stochastic error term; σtis the threshold variable and ∁ is the threshold value; ϑ1is regime switch parameter for policy changes; and σtwdenotes policy changes between regimes. Expanding equation (4) to take care of our specific interest give us;

In equations (5) and (6), ϑ1 represents the effect of monetary policy (in this case monetary policy rate (mpr) and Money supply (ms)) when the nominal policy tool is greater than the threshold value. This is the high policy regime. Equally, ϑ2is the effect of monetary policy when the threshold value is greater than the nominal policy tool value (in this case monetary policy rate (mpr) and Money supply (ms)). This period is the low policy regime. mpr∗ and ms∗ represents the iteration values selected for the process. σtmpr is a policy dummy that obeys the following rule, σtmpr= 1 if mprt>mpr∗ or σmpr= 0 if mprt<mpr∗. σtmsalso observe the same rules for money supply.

The optimal threshold point for each monetary policy tool is determined by iterating equations 5 and 6, using different values of monetary policy threshold levels. The optimal threshold is identified at the point where the Sum of Squared Residuals (SSR) of the iterated regressions is lowest. Data for the study are annualized data collected from the central bank of Nigeria data base and are defined in Table 1 below.

Table 1: Definition of Variables

Our choice of variables for the study is in line with other scholars (Houngb´edji and Bassongui, 2023; Diaz-Roldan, Prats and Ramos-Herrera, 2021; Mehrara and Behzadi-Soufiani, 2015) on the subject. All variables are subjected to prediagnostic analysis as stationary test among others. We used the augmented dickey fuller test and the Phillip Perron test analysis for our study.

DATA ANALYSIS AND DISCUSSION OF FINDINGS

Table 2 describes the statistical properties of the variables for the study. It shows that all the variables in the study except gross domestic product were positively skewed. We also noticed that all variables exhibited acceptable level of peakness except for money supply that was relatively flatter. The dependent variable exhibited the highest value in the system even as gross domestic product has the lowest value in the system. All variables in the system were multivariate normal with interest rate possessing the highest level of normality in the system.

Table 2: Descriptive Statistics of the Variables

Table 3 outlines the systemic associations between and among the variables in the study. Generally, it shows that positive associations in the system are only enjoyed between policy rate and interest rate with the dependent variable at close range. However, and possibly in line with theory, monetary growth and gross domestic product exhibited negative associations with the dependent variable with the strength of weakness that deepens from money supply to gross domestic product. Interest rate also had positive relationships with monetary policy rate and gross domestic product at positive difference of 0.21 units. Interestingly, the two policy variables considered in the study (money supply and monetary policy rate) are at negative variants to each other. Exchange rate exhibited negative relationship with the dependent variable and others except gross domestic product. Generally, the correlation matrix suggests that while an increase in monetary policy rate may elevate inflationary pressure, money supply growth tends to alleviate such pressure. The empirical evidence will further substantiate these findings.

Table 3: Correlation Matrix

In other to avoid spurious relations between the dependent variable and the explained variables we test for the stationarity properties of the variables and present the results in Table 4. We relied on the stationarity strength of Augmented Dickey Fuller (ADF) test and the Philips Perron (PP) test. Our result shows that all our variables were multivariate stationary. While gross domestic product (gdpt), monetary policy rate (mprt) and interest rate (rt) were stationary at levels; inflation rate (πt) and money supply growth (mst) and exchange rate (exct) were stationary after first difference.

Table 4: Unit Root Test

Next, we examined the existence of structural disturbances in the policy price stabilization chain. We relied on the sequential F-statistic methodology and found that the null hypothesis of no structural disturbances should be rejected (Tables 5 and 6). Thus, there exist at least one structural break in the inflation-policy chain under acceptable level of significance.

Table 5: Threshold test

Thus, there are traceable threshold points in the inflation-monetary policy chain made possible after policy lags. In the transition model selection, both monetary policy rate and money supply growth were nonlinearly transitory at lag (-3) (Figure 4). Both transitory threshold variables possess minimum residual sum of squares (RSS).

Table 6: Threshold test

* Indicates significance at 5% Source: Authors

With the transition model we proceed to the estimation of our threshold function and presented the results in Tables 7 and 8. Table 7 discusses the behaviour of inflation when monetary policy transit beyond a certain threshold (in this case 14. 31 basis point). Table 8 presents the behaviour of inflation when money supply switches from a threshold parameter of 11.14 basis point.

Table 7: Threshold Results

Source: Authors

Table 7 reveals that the direct marginal effect of monetary policy rate when inflation is below the threshold level of monetary policy is negative (nearly 17% at every 10% rise in the threshold variable (policy rate)) and statistically significance at 1% level of significance. Equally, the marginal effect of money supply growth when monetary policy transit below the threshold value is negative and statistically significant to price stability at 5% level of significance. In the same vein, exchange rate management was effective in managing inflation when mpr was below the threshold mpr and statistically significance.

In the period of high regime of policy rate (when monetary policy rate exceeds the threshold) both monetary policy rate and money supply growth produces statistically significant reducing effect on inflation of say 9% and 7% approximately to 10% rise in the duo. Within the period also, exchange rate management raise inflation within the period. The implication here is that while monetary policy rate and money supply growth may be inflationary stabilizing in both policy regimes, exchange rate management is only inflation stabilizing in low policy regimes. Amaning and Seidu (2020) also found similar behaviour of monetary policy rate on inflation in the Ghanaian economy in a non-threshold investigation.

The non-varying threshold variables used as control variables in the system showed that both interest rate and gross domestic product had statistically significant impact on inflation. However, while interest rate will increase inflation within the period, GDP reduces inflation in the country. This could be expected in line with developing economies’ experiences of low national income with rising financial prices. Our model shows that over 90% of variations of inflation are accountable to variations in monetary policy variables when monetary policy rate was treated as the threshold variable.

Table 8: Threshold Results

Source: Authors

Table 8 presents the results of the threshold regression with money supply growth as the transitory variable. In the low money supply regime, where money supply growth is below the threshold level 11.19, both monetary policy rate and money supply growth deepened inflation. Infact, increasing money supply by 1% will more than raise inflation by 1.9%. This has implication for monetary policy management. Raising money supply growth and monetary policy rate in low regime money supply period will only intensify the inflationary pressure in the economy. Equally, raising mpr by 1% will raise inflation by 0.2% and statistically significance. Our result shows that only exchange rate management will be effective in managing inflation when money supply in below the threshold level. Clearly, a 1% rise in exchange rate management dipped inflation by nearly 4% and statistically significant.

Conversely, in the high regime of money supply (money supply growth greater than 11.19), both monetary policy rate and money supply growth are inflation reducing while exchange rate is not. While the strength of reduction runs from monetary policy rate (3.77 in absolute term) to money supply growth (1.24 in absolute term) a greater impact on the economy came from monetary policy rate management to money supply growth management. Again, this is a pointer to the fact that in high regime of money supply, both monetary policy rate and money supply management will reduce inflation in the economy than exchange rate management. The control variables in the study exhibited consistent performance in both episodes, with only the parameters differing. This finding aligns with results obtained by Mehrara and Behzadi-Soufiani (2015) for the Iranian economy, where non-oil revenues were identified as efficient influencers of inflation in the country.

The results show that over 86% of variations in inflation was as a result of monetary policy management when money supply growth was gauged on a threshold of 11.19.

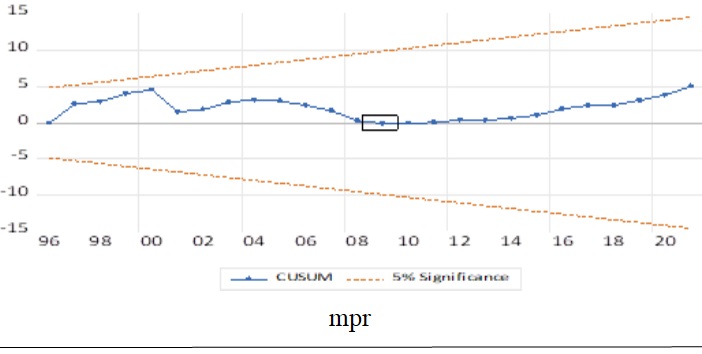

Figure 5: Model Stability results

Source: Authors

Figure 6: Model Stability results

Source: Authors

Our stability checks relied on the cumulative powers of CUSUM test where the cumulative effect of monetary policies (policy rate and money supply) is shown to be reliable at the normal 5% level of acceptance as inflation travels within the +(-) 2 standard deviation spectacles (Figure 5). Beyond the significance, Figure 5 also showed the possible inflexion point and time in the threshold framework. For monetary policy rate, the relationship turns nonlinear in 2008 and for money supply growth, it turned in 2008. Overall, the conclusion reached from the parameter estimates are reliable.

CONCLUSION

In this study, we investigated the inextricable relationship between monetary policy and inflation in Nigeria using data from 1980 to 2021 under threshold estimation. We showed that the major framework for monetary policy/inflation relationship is the traditional quantity theory of money among others. After prediagnostics sample data preparations, and estimations, we showed that the monetary policy variables investigated (monetary policy rate and money supply growth) switches around 13.69 and 11.19 basis points respectively.

Within these thresholds, monetary policy variables behave differently in inflation management drive of the macroeconomy. For instance, within the low money supply regime when money supply growth is below the threshold level, both monetary policy rate and money supply growth deepened inflation. Beyond this point, both monetary policy rate and money supply growth are inflation reducing. However, while the strength of reduction runs from monetary policy rate (3.77 in absolute term) to money supply growth (1.24 in absolute term) a greater impact on the economy came from monetary policy management to money supply management.

RECOMMENDATIONS

In order to achieve effective price stability, we advise that monetary policy management measure inflation management in the economy in accordance with policy threshold strength.

Based on our findings, we also suggested that, under high money supply regimes, money supply control and policy rate management should be undertaken as they will lower inflation in the economy more than exchange rate management. The goal of the monetary policy rate should be to target inflation in both high and low monetary policy regimes. This is due to the fact that both regimes’ monetary policy rates exhibit indications of successful inflation management.

To reduce inflation, the central bank should find workable ways to reduce the amount of money in the system and enhance its utilization of the monetary policy rate. Prior to implementing policies, the Central Bank should evaluate them, especially with relation to changes in the money supply and monetary policy rate.

REFERENCES

- Amaning, E. O. and Seidu, A. N. (2020). A Monetary Analysis of Ghana: Examining the impact and the causal relationship between Monetary Policy and Inflation in Ghana, American Journal of Economics, 4 (1,1): 1- 14.

- Amoah, B. and Mumuni, Z. (2008), “Choice of Monetary Policy Regime in Ghana, Working Paper, Monetary Policy Analysis and Financial Stability Department, WP/BOG-2008/07

- Asuquo A. (2012). Inflation accounting and control through monetary policy measures in Nigeria, Journal of Business and Management, 1(2):53-62.

- Bassey, G. E. and Ekong, U. M. (2019). Energy Consumption and Inflation in Nigeria: An ARDL Cointegration Approach, Energy Economics Letters, 6(2): 66-83.

- Bawa, S. and Abdullahi, I. S. (2011). Threshold Effect of Inflation on Economic Growth in Nigeria, CBN Journal of Applied Statistics, 3(1): 43-63.

- Central Bank of Nigeria. (2006). How does the Monetary Policy decisions of the Central Bank of Nigeria affect you? Part Two, Nigeria, Central Bank of Nigeria.

- Central Bank of Nigeria (2009). Annual Report and Statement of Account (December 2009): Central Bank of Nigeria Bulletin.

- Diaz-Roldan, C., Prats, M. A. and Ramos-Herrera, M. C. (2021). Redefining monetary policy rules: A threshold approach, Plus One, 16(5): 1-13.

- Ekong, C. N and Ekong, U. M. (2022). Monetary Policy and Industrial Sector Performance in Nigeria: Measuring the Extended Impact on the Economy, Journal of Applied Financial Econometrics, 3(2): 97-131.

- Ezeanyeji, C. I., Obi, C. O., Imoagwu, C. P. and Ejefobihi, U. F. (2021). Monetary Policy and Inflation Control: The Case of Nigeria, European Journal of Management and Marketing Studies, 6(2): 128-150.

- Fisher, I. (1911). The Purchasing Power of Money: Its Determination and Relation to Credit, Interest and Crises, Augustus M. Kelly, Publisher, London.

- Friedman, M. (1968). The Quantity Theory of Money. International Encyclopedia of Social Sciences. London, Corwell Collier and Macmillan, Inc. Vol. 10: 10487-10511.

- Funjika, P., Mwila, C. and Mulenga, P. (2023). Monetary Policy and Inflation in Zambia, available online at https://custom.cvent.com, date visited 12.07.2023.

- Garriga, A. C. and Rodriguez, C. M. (2020). More Effective Than We Thought Central Bank Independence and Inflation in Developing Countries, Economic Modelling, 85:87-105.

- Hansen, B. E. (2000). Sample Splitting and Threshold Estimation, Econometrica 68:575–603.

- Hashemi-Dizaj, A., Hazeri-Niri, H., and Samadzadeh, S. (2022). The impact of monetary policy on inflation in oil developing countries and developed countries, Journal of Development and Capital, 7(2): 213-232.

- Henry, E. A. and Sabo, A. M. (2020). Impact of monetary policy on inflation rate in Nigeria: Vector Autoregressive Analysis, Bullion, 44(4): 78-90.

- Khan, M.S. and Senhadji, A. S. (2001). Threshold Effects in the Relationship between Inflation and Growth, IMF Staff Papers, Vol. 48.

- Kwapil, C. and Scharler, J. (2006). Limited Pass-Through from Policy to Retail Interest Rates: Empirical Evidence and Macroeconomic Implications. Monetary policy and the Economy Quarter, 4(6): 26-36.

- Mehrara, M. and Behzadi-Soufiani, M. (2015). The Threshold Impact of Fiscal and Monetary Policies on Inflation: Threshold Model Approach, Journal of Money and Economy 10(4): 1-27.

- Mishkin, F. S. (1992). Is the Fisher effect for real?: A reexamination of the relationship between inflation and interest rates. Journal of Monetary Economics, 30(2), 195–215.

- Ntshangase, L. S., Sheunesu Z. and Kaseeram, I. (2023). The Spillover Effects of US Unconventional Monetary Policy on Inflation and Non-Inflation Targeting Emerging Markets, Economies, 11(138): 1-15.

- Omanukwue, P. N. (2010). The Quantity Theory of Money: Evidence from Nigeria, Central Bank of Nigeria Economic and Financial Review, 48(2): 91-107.

- Omotosho, B. S. Bawa, S. and Doguwa, S. I. (2016). Determining the Optimal Public Debt Threshold for Nigeria, CBN Journal of Applied Statistics, 7(2): 1-25.

- Wauk, G. and Adjorlolo, G. (2019). The Game of Monetary Policy, Inflation and Economic Growth. Open Journal of Social Sciences, 7: 255-271.

- Yusuf, S. T. (2020). The Effectiveness of Monetary Policy in Controlling Inflation in Nigeria, an unpublished research project submitted to the department of Economics, Baze University, Abuja-Nigeria, retrieved at https://portal.bazeuniversity.edu.ng, date visited 13.07.2023.