Perceptions of the Zimbabwe Gold Currency (ZiG) as a Panacea to Economic Stability

- Lawrence Dumisani Nyathi

- Japhet Mutale

- 80-91

- Feb 13, 2025

- Economics

Perceptions of the Zimbabwe Gold Currency (ZiG) as a Panacea to Economic Stability

Lawrence Dumisani Nyathi1 and Japhet Mutale2

1Lecturer, Department of Banking & Economic Sciences, National University of Science and Technology

2Economist, Homelink Pvt Limited (Subsidiary of Reserve Bank of Zimbabwe)

DOI: https://dx.doi.org/10.47772/IJRISS.2025.915EC006

Received: 29 December 2024; Accepted: 07 January 2025; Published: 13 February 2025

ABSTRACT

This study investigated the perceptions and reactions of Zimbabwe’s economic agents regarding the Zimbabwe Gold Currency (ZiG) as a potential solution for achieving economic stability. The research employs a primary data approach, collecting information from 295 out of a possible 300 respondents through structured questionnaires administered via face-to-face interviews, town hall focus group and emails over a 14-day period. Respondents represent diverse economic sectors, including SMEs, manufacturers, informal businesses, and individual consumers, predominantly in all 3 Matebeleland Provinces which included rural and urban markets. Major findings reveal that while some economic agents especially exporters and manufacturers support the local currency for its potential to boost production and competitiveness, significant skepticism persists. Factors undermining confidence in the ZiG currency include policy inconsistency, selective usage, lack of trust in monetary authorities, and macroeconomic instability. Respondents highlighted government mismanagement of fiscal priorities, rampant speculation, and limited efforts to formalize the economy as further challenges. The study identifies several policy measures to stabilize the ZiG currency, such as engaging the private sector, promoting policy consistency, prioritizing developmental expenditure, addressing debt overhang, and eliminating selective administrative enforcement. The findings underscore the necessity of a multistakeholder approach to restore economic fundamentals and build confidence in the currency. These insights contribute to the discourse on monetary reforms and economic stability in Zimbabwe.

Keywords: Zimbabwe Gold Currency (ZiG), economic stability, monetary reforms, policy inconsistency, macroeconomic instability, currency skepticism, developmental expenditure, debt overhang, formalization, town hall focus group.

INTRODUCTION

Money has evolved significantly from its origins in ancient societies to its modern form. Early societies used diverse objects as money, such as cocoa in Mesoamerica, whale teeth in Fiji, and carved stones on the island of Yap, often imbuing these items with spiritual and ceremonial significance (Gentle, 2021; Laum, 1924). Metal currencies emerged in Babylon around 2000 BCE, with the first standardized coins created by the Kingdom of Lydia in the 7th century BCE. In China, spade-shaped bronze coins appeared over 2,600 years ago. Precious metals like gold and silver were commonly used for high-value coins due to their scarcity and divisibility, while less valuable materials like bronze and copper served smaller transactions. Paper money was first introduced in China under Emperor Zhenzong (997–1022 CE) (Kramer, 2021; Tikkanen, 2023).

Modern economies transitioned to fiat money, issued solely by central banks without the need for tangible backing. This shift, central to contemporary capitalism, followed the collapse of the Bretton Woods system in the mid-20th century, ending centuries of gold-based monetary systems. The Classical Gold Standard, established in the 19th century, had previously dominated international monetary systems but proved unsustainable in the face of geopolitical and economic changes. Zimbabwe’s monetary history reflects ongoing struggles with hyperinflation, currency instability, and eroded public trust. In 2024, the government introduced the Zimbabwe Gold Currency (ZiG), backed by gold reserves, to restore confidence and stabilize the economy. Drawing lessons from historical monetary systems, this initiative aims to combine the credibility of gold-backed currencies with the flexibility of modern financial policies. This paper explores public and expert views on the feasibility of ZiG as a solution to Zimbabwe’s economic challenges.

Research Objectives

- To assess the level of public and expert confidence in ZiG.

- To explore whether ZiG addresses key economic issues like inflation, currency depreciation, and fiscal discipline.

- To evaluate the challenges and risks associated with implementing a gold-backed currency in Zimbabwe.

CURRENCY DEVELOPMENT IN ZIMBABWE

In an effort to stabilise macroeconomic fundamentals, the Zimbabwean government has introduced the domestic currency six times. Since independence in 1980, the Zimbabwean economy has had a turbulent history with its currency, including several changes and redenominations (Chitambara, 2022; Techzim, 2024). The Zimbabwean dollar was introduced in 1980 to replace the Rhodesian dollar. The Zimbabwean economy has been characterised by mismanagement, macroeconomic instabilities, policy inconsistency, and overspending (Ndlovu, 2018). As rising inflation started to affect the purchasing power of the Zimbabwe dollar, high denominations—the $500 and $1,000 banknotes—were issued between 2001 and 2005 (Makochekanwa, 2019).

In May 2003, the government of Zimbabwe tasked the Cargill Cotton Group to issue emergency bearer cheques to cotton farmers. Cargill issued these cheques due to a shortage of money caused by high annual inflation (Chipika, 2015). The Reserve Bank later issued special traveller’s cheques on 8 August 2003 with six denominations ranging from $1,000 to $100,000. On 26 September 2003, the Reserve Bank of Zimbabwe (RBZ) issued bearer cheques with denominations of $50,000 and $100,000, with the $1 million denomination planned for September 2006 (RBZ, 2006).

On 1 August 2006, the banknotes of the second dollar replaced the first dollar, with denominations ranging from $5,000 to $500 million issued in the second quarter of 2008. Agrocheques were issued in denominations ranging from $5 billion to $100 billion (Makochekanwa, 2019). By 1 August 2008, the banknotes of the third dollar were printed. Moreover, on 2 February 2009, banknotes of the fourth dollar (ZWL) were introduced (Ndlovu, 2018).

In February 2009, the Zimbabwean dollar was effectively abandoned due to hyperinflation, and the country adopted multicurrency systems, including the US dollar, South African rand, Euro, and Botswana pula (Techzim, 2024). By 2016, the Reserve Bank of Zimbabwe introduced a new currency called the “bond notes,” which were meant to supplement the US dollar, which was in shortage and fast disappearing. However, the bond notes soon lost value, leading to a shortage of cash and rising black-market exchange rates (Chitambara, 2022).

In June 2019, Zimbabwe introduced a new currency, the Zimbabwean RTGS dollar, which was pegged to the US dollar at a rate of 1:1. The Zimbabwe dollar consisted of electronic and paper notes. However, the new currency soon lost value due to inflation, which rose to 800% year-on-year (Makochekanwa, 2019). In March 2020, the Zimbabwean government introduced the Zimbabwe dollar (ZWL) as the country’s new currency, with denominations of $1, $5, $10, $20, $50, $100, and $500.

As part of the new monetary measures to stabilise the exchange rate and ease demand for foreign currency, the Reserve Bank of Zimbabwe in March 2021 announced the Zimbabwe dollar auction system. Under this system, the central bank auctioned foreign currency to businesses and individuals at a fixed exchange rate. However, the auction system failed to curb inflation and ease demand for USD in the market; instead, speculative tendencies increased and perpetuated market indiscipline (Chitambara, 2022).

In February 2023, the Zimbabwean government introduced a new monetary policy called the Zimbabwe dollar (ZWL) liberalisation. Under this policy, the central bank announced that the ZWL would no longer be pegged to the US dollar, and market forces would determine the exchange rate. This was done to attract foreign investment and boost economic activity, according to the apex bank. However, the ZWL lost almost 100% of its value against the US dollar. By the beginning of April 2024, the rate stood at ZWL50,000: 1 USD (Techzim, 2024). The Zimbabwean government then abandoned the ZWL and adopted a gold-backed currency called the Zimbabwe Gold Currency (ZiG).

The introduction of the Zimbabwe Gold Currency (ZiG) was an attempt to tackle inflation and foster predictability in the exchange rate. Above all, it marks the sixth attempt for the country to introduce a local currency. ZiG stands for Zimbabwe Gold, a currency backed by gold and other precious metals of the land (Techzim, 2024).

The Zimbabwe Gold currency ushered in a stable economic environment with low inflation and predictability. All stakeholders have unanimously agreed that the success of the ZiG currency rests solely on the discipline and policy consistency of the Zimbabwean government. However, the parallel market remains prevalent, despite occasional crackdowns by the government, as these activities are deemed illegal. The lack of trust in the official currency system has driven the persistence of such informal markets. Moreover, the devaluation of the Zimbabwe Gold just a couple of months after its release has caused skepticism about the future of the currency (Chitambara, 2022; Techzim, 2024).

Case Studies of Gold-Backed Currencies Globally

Gold-backed currencies have historically provided monetary stability by anchoring currency value to a tangible asset like gold. The classical gold standard (1870–1914) exemplified this approach, with major economies, including the United Kingdom and the United States, maintaining fixed exchange rates linked to gold reserves. This system fostered low inflation and fiscal discipline by limiting money issuance to a country’s gold holdings (Bordo & Kydland, 1995). However, its collapse during the interwar period highlighted its limitations, particularly during economic crises. Events like World War I and the Great Depression exposed the system’s rigidity, leading nations to abandon it for more flexible monetary frameworks (Eichengreen, 1996).

More recently, countries like Switzerland maintained partial gold backing for their currencies, enhancing credibility and stability. However, by 2000, Switzerland fully transitioned to fiat money, reflecting a global shift away from commodity-backed systems to allow for more monetary policy flexibility (Stoffels & Neumann, 2009). These examples demonstrate that while gold-backed systems enhance trust and inflation control, they can hinder economic responsiveness during crises. For Zimbabwe, the proposed Zimbabwe Gold Currency (ZiG) draws lessons from such systems. While ZiG could restore stability by leveraging gold’s credibility, the country must mitigate risks of inflexibility and ensure robust institutional frameworks for effective reserve management. Transparent policies and lessons from past failures are crucial for its success.

LITERATURE REVIEW

The literature review contextualizes the study by exploring the theoretical underpinnings, historical developments, and empirical findings relevant to the Zimbabwe Gold Currency (ZiG). It provides insights into monetary theory, trust in currency systems, and the historical and empirical frameworks underpinning the potential impact of gold-backed currencies on economic stability.

Theory

The Classical Gold Standard Theory

The study follows the classical gold standard rooted in medieval European monetary practices, evolved into a hallmark of modern economic systems. Initially, state institutions managed coin minting, sometimes delegating this authority to local entities. Coins derived their value from fluctuating metal prices and often coexisted with coins from other nations. Bills of exchange and early banknotes, such as those issued by Venice’s merchants and later by institutions like the Bank of Genoa and Stockholms Banco, laid the groundwork for modern currency systems (Britannica, 2024; Le Goff, 2012).

Central banks, originally privately owned, gained prominence, eventually becoming pivotal to monetary systems. These banks issued notes redeemable in gold, ensuring trust in currencies. However, capitalism’s rise necessitated monetary reforms. For example, the prohibition of interest, upheld by Pope Innocent III and later supported by Martin Luther, was abandoned as Pope Pius lifted the ban in 1830 to align with capitalism’s demands (Kurkliński, 2017).

England pioneered modern monetary policy, adopting bimetallism in 1717. This system, which fixed the value of gold and silver coins, faced challenges, including Gresham’s Law, where the undervalued metal was withdrawn for non-monetary uses. A bank run in 1797, fuelled by false invasion rumours, led England to suspend precious metal redemption, prompting debates about monetary systems without commodity backing. While John Fullarton argued for the feasibility of inconvertible notes, David Ricardo advocated for gold-backed currencies to prevent misuse (Fullarton, 1845; Ricardo, 1821). Two schools of thought emerged in the monetary policy debate. The Currency School, drawing on the quantity theory of money, emphasized strict gold backing to prevent inflation. Figures like Ricardo (1824) and Friedman (1948) advocated for full reserves, aiming to grant central banks control over money supply. In contrast, the Banking School, led by Thornton (1802) and Fullarton (1845), argued for flexibility, suggesting that money supply aligned with production would not cause inflation. They proposed the real bills doctrine, emphasizing economic activity as a guide for monetary policy (Heine & Herr, 2003; Herr, 2024).

Both schools had limitations. The Currency School’s reliance on the quantity theory of money overlooked complexities in money supply dynamics, while the Banking School underestimated inflation risks during economic booms. These debates culminated in compromises within the Peel Act, which balanced gold backing with limited discretionary powers for the Bank of England. Despite these measures, the role of bank deposits grew, shifting monetary practices away from strict gold adherence (Keynes, 1933; Herr, 2024). By the late 19th century, the gold standard became a global system. Countries like Germany, Sweden, and the USA joined, stabilizing exchange rates and reinforcing gold as the monetary base. Gold discoveries in California and South Africa supported this expansion. Under this system, banknotes were freely exchangeable for gold at fixed rates, with central banks maintaining strict conversion policies. This regime established the pound sterling as the dominant currency and London as the financial center. However, the gold standard collapsed with World War I in 1914, ending its global dominance (Herr, 1992; Heine & Herr, 2022).

The Classical Gold Standard exemplifies the interplay between trust, monetary stability, and economic policy. While it provided a foundation for modern financial systems, its inflexibility and reliance on gold supply highlighted challenges in adapting to dynamic economic environments.

Monetary Theory

Furthermore, this study follows the Monetary Theory as propounded by Bordo & Schwartz (1997). The proponents argue that the gold standard, a monetary system where a currency’s value is directly linked to a fixed quantity of gold, historically stabilized currency values by imposing strict monetary discipline. This system limits governments’ ability to print money beyond their gold reserves, preventing inflationary policies and ensuring fiscal restraint. The researchers further point out that the gold standard enhances currency credibility by reassuring markets of its stability. By tying currency value to a tangible commodity, it mitigates inflation and speculative risks while promoting long-term price stability. According to Eichengreen (1996), this system bolstered trust in currencies, particularly during economic uncertainty, by discouraging devaluation attempts.

However, the gold standard’s rigidity has been criticized, particularly during economic crises. It constrained central banks’ ability to implement counter-cyclical policies, often exacerbating economic downturns and deflation. For instance, during the Great Depression, adherence to the gold standard deepened global economic suffering as countries faced constraints in adjusting their money supply to economic needs (Kindleberger, 1986). This inflexibility has led most nations to abandon the gold standard in favour of more adaptable monetary systems.

Zimbabwe’s gold-backed currency exemplifies the challenges of implementing such a system in developing economies. Limited gold reserves and volatile global gold prices create difficulties in maintaining the necessary backing, potentially undermining currency stability. While the gold standard historically offered benefits like currency credibility, its practical application in modern economies, particularly those with limited reserves and high volatility, remains challenging.

Trust and Confidence in Currency

Currency stability hinges on trust in the central bank’s ability to maintain sound monetary policies and fiscal discipline (Mishkin, 2021). In economies like Zimbabwe, plagued by hyperinflation and currency instability, restoring trust is crucial for economic stabilization. Zimbabwe’s hyperinflation, driven by policy inconsistency and fiscal mismanagement, eroded public confidence in the local currency (Hanke & Kwok, 2009). To rebuild trust, a gold-backed currency can serve as a psychological anchor, signalling commitment to monetary stability. Gold, viewed as a reliable store of value, offers a tangible benchmark that mitigates fears of devaluation and inflation.

However, the success of such a system depends on transparent management of gold reserves and consistent enforcement of monetary policies. Herr (2024) emphasizes that mismanagement or insufficient reserves could undermine the credibility of a gold-backed system. Zimbabwe’s economic history shows that trust in a currency requires more than just asset backing; it depends on broader economic policies like controlling inflation and ensuring fiscal discipline. Corruption and policy inconsistency have historically hindered Zimbabwe’s efforts to stabilize its currency, rendering asset-backed systems ineffective (Hanke & Kwok, 2009).

Restoring public confidence in Zimbabwe’s currency demands a multifaceted approach. While gold backing can enhance trust, it must be coupled with sound economic governance, policy transparency, and measures to address inflationary pressures. Without these, even a gold-backed currency may fail to stabilize the economy and regain public trust.

Zimbabwe’s Monetary Reforms: Lessons learnt from other countries

Zimbabwe’s predominantly informal economy, with 28% of respondents engaged in informal businesses, presents challenges to the circulation and adoption of the ZiG currency. This mirrors the experiences of Nigeria and India, where over 70% of the workforce operates informally, and making monetary policy interventions less effective (Medina & Schneider, 2018). Formalization strategies, such as South Korea’s tax incentives and promotion of digital payments, have proven effective in integrating informal sectors into formal economies (Kim & Lee, 2017). Zimbabwe could adopt similar approaches to enhance the impact of the ZiG currency.

The study also shows how the ZiG currency could improve manufacturing and export competitiveness. According to Cheung et al. (2018), who discovered that the Yuan’s undervaluation increased the worldwide competitiveness of Chinese exports, this is consistent with China’s use of a controlled exchange rate to maintain export growth. However, this potential is undermined by Zimbabwe’s inconsistent policies. Tan’s (2021) analysis of Singapore’s experience with pegging its currency to a trade-weighted basket highlights the significance of consistent policies in fostering investor confidence. Zimbabwe has to think about implementing comparable policies to stabilize its currency.

Zimbabweans’ loss of confidence in the ZiG currency is comparable to what happened in Argentina and Venezuela, where hyperinflation and unpredictable policy choices damaged confidence in local currencies. While Corrales (2020) emphasizes Venezuela’s inability to control inflation and speculation, Díaz Alejandro (1985) blames Argentina’s currency crises on inconsistent policies and a lack of budgetary discipline. Rwanda, however, provides a different illustration of achievement. Mutebile (2021) credits fiscal restraint, transparency, and coordinating reforms with long-term development objectives for Rwanda’s regained currency credibility. In order to rebuild confidence in the ZiG currency, Zimbabwe should adopt Rwanda’s strategy.

Ghana and Malaysia can teach us how to stabilize the ZiG currency. According to Frimpong & Adam’s (2017) analysis, fiscal measures, such as cutting back on government spending and giving priority to productive industries, helped to lessen Ghana’s 2014 currency crisis. According to Athukorala (2001), Malaysia’s response to the Asian Financial Crisis by tying the Ringgit to the US dollar and managing liquidity also contributed to stability. As suggested by Keynesian economic theory, Zimbabwe’s excessive expenditure on unproductive imports, like $3 billion on cars, may be diverted into funding manufacturing (Keynes, 1936).

Zimbabwe’s access to international financial markets is further restricted by its USD 21 billion debt burden. Similar difficulties were encountered by Greece during the Eurozone crisis. According to empirical research by Arghyrou & Tsoukalas (2011), Greece has successfully used foreign assistance and debt restructuring to win back investor trust. On the other hand, Jefferis (2020) points out that Botswana has been able to maintain a stable currency and low debt levels thanks to its careful debt management. To stabilize the ZiG currency, Zimbabwe might look into debt restructuring and adopt Botswana’s budgetary restraint. In order to rebuild trust and stabilize its currency, empirical data emphasizes that Zimbabwe must address macroeconomic fundamentals, lessen policy contradictions, and learn from global experiences.

Implications of Commodity-Backed Currencies on Financial Systems in Developing Economies

Commodity-backed currencies tie a nation’s money supply to physical assets like gold or oil. This approach offers potential benefits for stabilizing financial systems, particularly in developing economies prone to inflation and currency devaluation. Linking a currency’s value to a tangible asset reduces the risks of excessive money printing and inflationary pressures, fostering monetary stability (Bleaney & Greenaway, 2001). For resource-rich nations, this strategy can enhance confidence in the currency and discourage fiscal indiscipline.

However, commodity-backed systems also present significant risks. Frankel (2010) found out that the vulnerability of such systems to global commodity price volatility. Fluctuations in commodity prices can lead to instability in the currency’s value, complicating policymakers’ ability to address domestic economic needs. For instance, a sharp decline in global demand or prices for the backing commodity could destabilize the economy, particularly for countries heavily reliant on a single resource.

In Zimbabwe’s case, leveraging gold to back the ZiG offers both opportunities and challenges. Gold-backed currencies can mitigate inflation and restore trust, especially given Zimbabwe’s hyperinflationary past (IMF, 2009). Gold’s historical reputation as a safe-haven asset can act as a psychological anchor, signalling monetary stability (Hanke & Kwok, 2009). However, the adequacy of Zimbabwe’s gold reserves is a critical concern. Limited reserves and global gold price fluctuations could undermine the sustainability of a gold-backed currency.

Studies done by Mpofu (2020) and Zicchino & Hozz, (2019) posits that successful implementation requires strong institutional governance and transparent reserve management. Zimbabwe’s history of monetary policy mismanagement and public mistrust underscores the importance of addressing these issues. The lack of trust in the government and central bank could hinder adoption of the ZiG unless robust measures are taken to ensure credibility and transparency

While on the same note, Zicchino & Hozz (2019) argue that integrating a gold-backed currency into the global financial system poses significant challenges. Zimbabwe must navigate the complexities of international trade and finance, as most transactions are based on fiat currencies. Fluctuating gold prices could further complicate currency stability, affecting Zimbabwe’s ability to engage effectively in global markets. Lessons from Venezuela’s oil-backed cryptocurrency highlight the risks of inadequate governance and public skepticism, which led to limited adoption and credibility issues.

Generally, Zimbabwe’s exploration of a gold-backed currency draws on historical and empirical lessons from its own experiences with hyperinflation, dollarization, and de-dollarization. While commodity-backed currencies can stabilize inflation and enhance trust, they require robust governance, adequate reserves, and public confidence to succeed. For Zimbabwe, the ZiG offers a potential solution to its monetary challenges but must be implemented with transparency, credible reserve management, and institutional reforms to avoid repeating past mistakes. By learning from other countries’ experiences, particularly Venezuela’s failed attempts, Zimbabwe can address the risks of volatility, reserve inadequacy, and governance issues, ensuring the Zimbabwe Gold’s sustainability and effectiveness.

METHODOLOGY

The study adopts a qualitative research which hinges on primary data. 300 respondents were randomly across Matebeleland towns and respondents were selected through face to face interviews, town hall focus groups and emails. Town hall focus group method was employed for respondents in Matebeleland South and North. Town hall focus group was adopted because it would constitute teams of like-minded or similar people or single individuals who had a soul purpose to improve economic conditions of their town or country. Further these respondents also indicated that they would like to attend at the same time and such methods usually accommodate such scenarios. Note only minimizing bias of face to face interviews (Zuckerman-Parker M and Shank G , 2008). In Matebeleland South respondents were drawn from towns such as Gwanda, Filabusi, Plumtree, Beitbridge, Kezi, Maphisa, Makhado and Esigodini while Matebeleland North respondents were drawn from Lupane, Hwange, Nkayi, Tsholotsho, Binga and Bubi. Meanwhile, in Bulawayo respondents were from the central business district (CBD and the small and medium enterprises (SMEs) along 6th avenue, Sekusile Market and Entumbane markets to fill in questionnaires as well as with the industrial players across all sectors. Data was collected for 14 day period from 14 November to 30 November 2024. Structure questionnaires were used to collect information from the respondents. The use of structured questionnaires was necessary as the researcher wanted to obtain as much comparable and objective information regarding respondents’ reactions and perceptions as possible. This also ensured the data collected was specific and precise. Data was then analysed by means of simple excel spreadsheets.

RESULTS AND FINDINGS

This section provides the major findings of the study as analysed from the responses which were provided by the interviewed economic agents. The findings provide summarized views, reactions and perceptions of the majority stakeholders, thus ensuring anonymity of the respondents’ names or particulars.

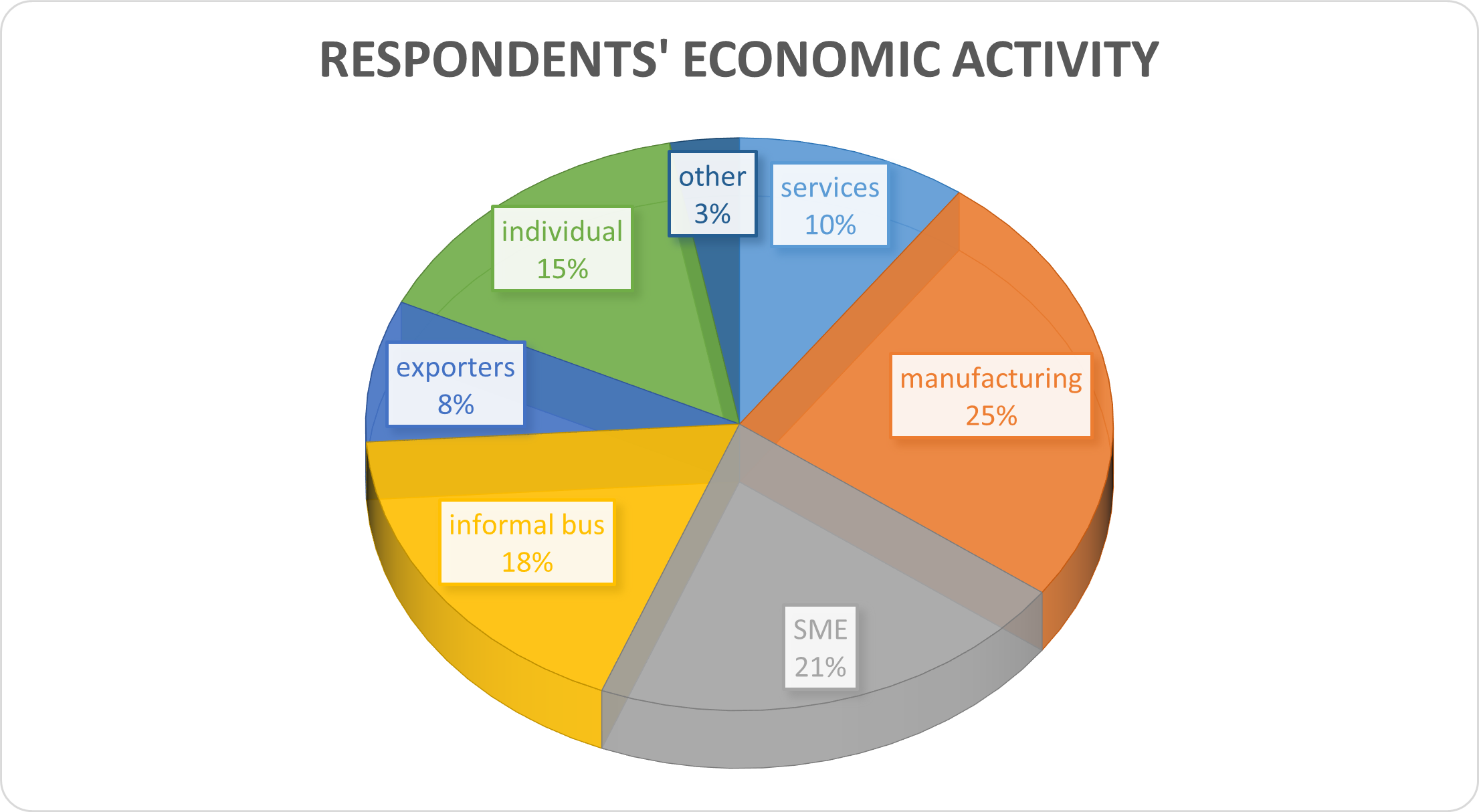

Nature of respondents’ economic activities

With regards to characteristics of the respondents, the response rate was 98.3% given that all various primary methods of 295 interviewed respondents accomplished to provide answers which were usable for the analysis. According to the survey results depicted in figure 1 below 18 % (52 out of 295) were informal businesses, SMEs had 21% (62 out of 295), while manufacturing and individual had 25% and 15% respectively. Services were also 10% (29 out of 295). Meanwhile, exporters 8% (25 out of 295) and lastly, others 3% (8 out of 295) accounted for the total sample.

Figure 1: Nature of respondents’ economic activities

Source: primary data, 2024

The response rate was 98.3% given that 295 out of a possible 300 interviewed respondents managed to provide answers which were usable for the analysis. According to the survey results depicted in Figure 1, manufacturing sector responses were the highest 25% (75 out of 295), while 21% (62 out of 295) of the respondents were for small medium enterprises (SMEs). Informal business had 18% (52 out of 295) respondents and individual consumers recorded 15% accounting for (44 out of 295) respondents. Service providers were accounted for 10% (29 out of 295). Respondents from exporters were 25 and accounted for 8%, while others had 8 responses which is 3% of the total surveyed sample.

Zig currency needed for the economic growth

The research revealed that the local unit is needed to boost economic growth and production among companies in Zimbabwe. 20% of the respondents that is exporters 8% and manufacturers 25% respectively, interviewed indicated that they need the local unit in economic circulation because it boosts production and most importantly that they remain competitive among their regional pairs as their products are affordable on the foreign market. Furthermore, the availability of the domestic currency reduces costs in production of local goods hence affecting the pricing of the locally manufactured goods. The central bank’s tight monetary policy plays a role with raised interest rates pegged at 35% encouraging more Zimbabweans to use the ZIG currency for higher returns.

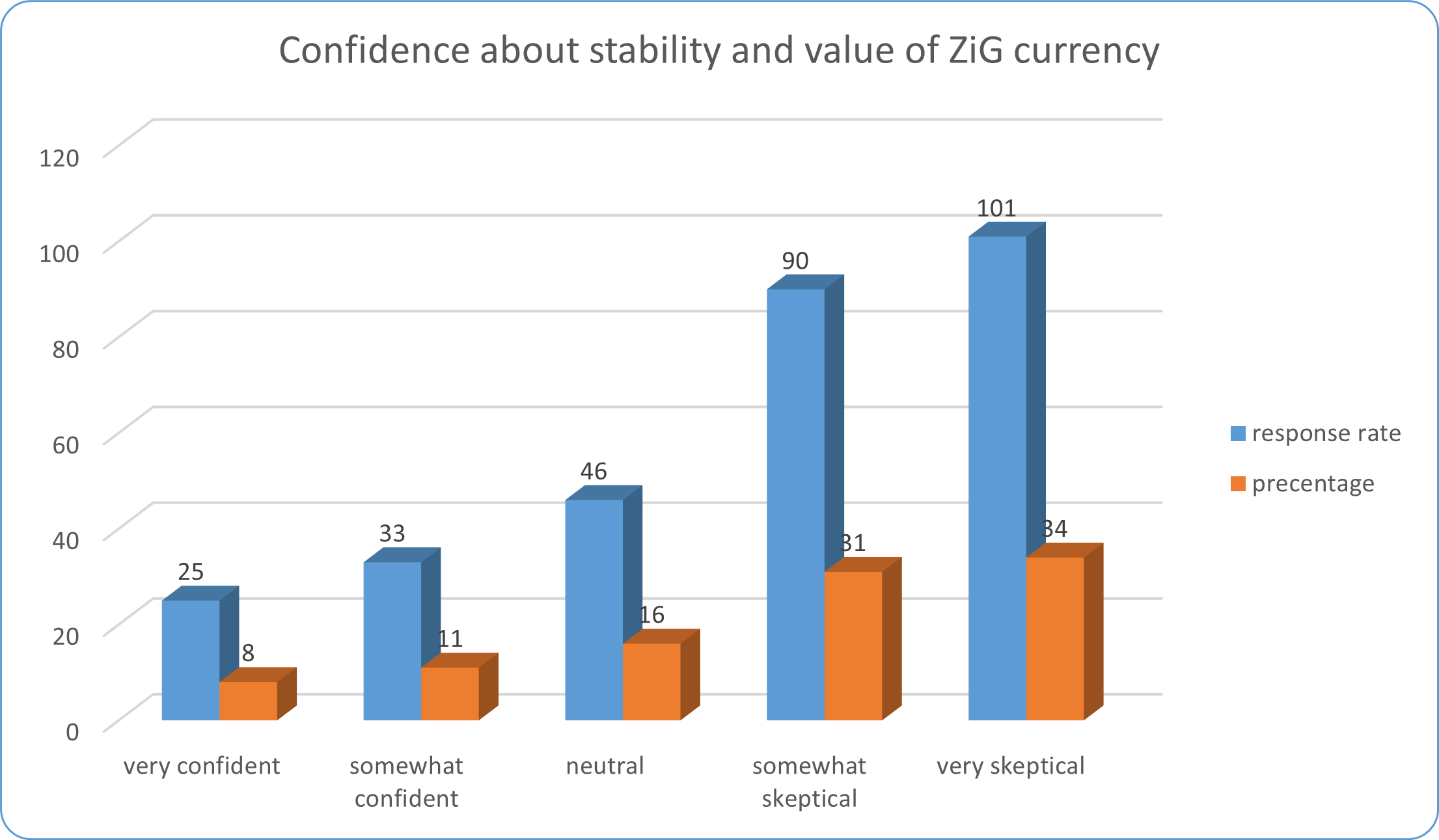

Why economic agent don’t have confidence with the ZiG currency

Table 1: Confidence of the ZiG Currency to restore Economic Stability

Source: Primary Data, 2024

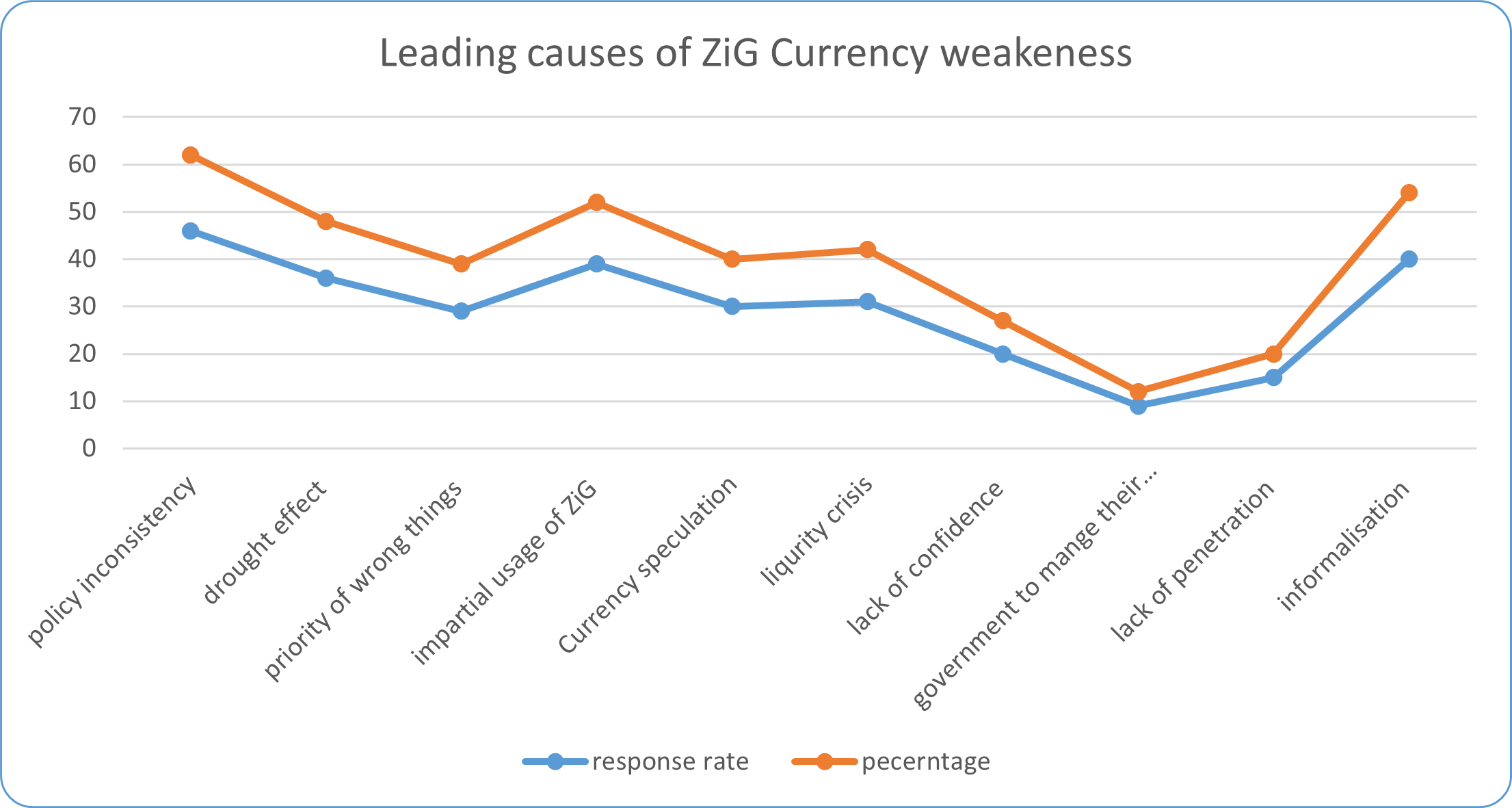

The research revealed that the ZiG currency started well when it was introduced into circulation during the month of April 2024. However, monetary authorities have also have had a role to play for the destabilisation of the ZiG currency. The results of the study reveal that economic agents are somewhat skeptical to very skeptical of the ZiG Currency to restore macroeconomic fundamentals. Amongst the major reasons are shown in figure 2 below.

Figure 2: Factors Leading to Weakening of the Domestic Currency

Source: Primary data, 2024

The study revealed that ZiG Currency is affected by many bottlenecks so that it doesn’t stabilise. 46 respondents out 295 (16%) cited policy inconsistency as major driver of currency weakening in Zimbabwe. One respondents said, “When the ZiG Currency was introduced earlier this year, RBZ assured that the exchange rate will be tracking the value of gold. However, devaluation is being implemented when gold prices have reached their highest which could by norm the ZiG Currency has appreciated its exchange rate. The devaluation led to a spike of inflation and have left many businesses to grapple with eroded balance sheets”. One of the business executives echoed that, “To plan using the local currency is to plan to fail”. Further, 40 respondents out 295 respondents (14%) echoed that ZiG performance was hampered by informalisation of the economy. According to (CZI, 2024) 80 percent of the economic activity are being controlled by dominant informal sector. The informal sector rejects the local currency in favour of the foreign currency. The study also reveals that as long as there is impartial usage of the ZiG currency it defeats the whole purpose of the dedollarisation process. Eversince the introduction of ZiG currency in April 2024, fuel, passports and other licences are sold exclusively in foreign currency. This creates high demand of US Dollar to purchase these goods and services.

While on the same note, 11% of the respondents echoed that weakening of the ZiG currency is attributed to wrong priories of the government of Zimbabwe and currency speculation respectively. Government should effortlessly address macroeconomic instability rather than buying cars and fuel for top government executives. Moreso, drought effects 12 %, liquidity crisis 11% also weighed negatively on the performance of the currency. 20 respondents out of 295 respondents (7%) said that generally Zimbabwean population lacked confidence in transacting with domestic currency. Workers when paid quickly offload local currency to big retail super markets and quasi-government institutions like city council and some is offloaded to the parallel market in exchange of USD balances. Moreover, 9 respondents out of 295 (3%) respondents apiece indicated that government was failing to manage their expenses. Lastly, 15 out of 295 respondents (5%) revealed that ZiG lacked penetration for circulation across Matebeleland region. Majority of the economic agents don’t know the new currency. Economic agents in Tsholotsho, Gwanda, and Beitbridge and Filabusi towns largely transact using the South African rand. The rand currency is most preferred mostly due to proximity of economic agents to South Africa, Botswana and Namibia were they procure their wares for trade and consumption.

Measures that can be adopted by government to stabilise the local unit

The research also revealed several ways that government of Zimbabwe can adopt so as to stabilise the local unit.

- There is need to formalise the economy. Zimbabwe economic activities are predominantly informalised. This is real threat to the impact of the currency as the informal sector doesn’t transact using the local unit.

- There is need for the government of Zimbabwe to engage private sector in addressing challenges that ZiG. The administrative enforcement being carried out by the government of Zimbabwe have largely left the private sector as enemies towards currency reformation process.

- Government of Zimbabwe need to adhere to policy consistency. When the ZiG currency was introduced its exchange rate was deemed to track the yellow metal and other precious metals which has reached its highest value for the year……, however its devaluation done recently has left economic players doubting the significance of the ZiG currency.

- ZiG currency exchange rate won’t stabilise up until government effectively addresses its selective usage amongst economic agents. Since being introduced into the economic system, the ZiG currency doesn’t buy fuel and other government services such passports and other licences with the government of Zimbabwe. These commodities have been sold exclusively in US Dollars.

- Government should also priotize its spending patterns. Government of Zimbabwe is called to priotize developmental economics limiting spending on cars for top government executives and fuel allocations. In 2024 alone, Zimbabwe spent an approximated USD3 billion on cars that are imported from Japan, US, Germany and UK. Such revenue can be channelled to revival the motor vehicle value chain locally and also served as production finance to fund productive sectors of the economy thus anchoring the local unit.

- Further, the local unit won’t survive due to debt overhang affecting the country. According the Ministry of Finance and Economic Development (MoFED, 2024) debt and restructuring office, Zimbabwe’s debt now stands at USD21 billion. Such a huge amount is blocking the country to source new global finance and limited participation to capital markets as well.

- Government of Zimbabwe needs to holistically address rampant informalisation which is spreading throughout the economy. There is constructive policies that incentive formalisation process of SMEs and strengthen the value chains of formal business to allow acceptance of government policies and monetary reforms to penetrate the economic system.

- Lastly, government of Zimbabwe should wean away administrative enforcement that it’s carrying out. Economic literature has proved that a strong currency is born through restoring economic fundamentals rather than pursuing administrative enforcements.

CONCLUSION AND POLICY RECOMMENDATIONS

The study explored the perceptions whether the Zimbabwe Gold Currency (ZiG) is the panacea for Zimbabwe’s economic stability. The analysis was carried out through primary data collected in a structured questionnaire was administered to 145 economic agents within the first seven days after the announcement of the devaluation of the exchange rate of the Zimbabwe Gold Currency. The study revealed that a domestic currency was needed to boost production especially by exporter and manufacturers, the study also revealed the factors that leading to weakening of domestic unit and it also indicated several measures that government of Zimbabwe can adopt to stabilise the Zimbabwe Gold currency.

Policy recommendations

Taking into account major findings summarised above, the success and stabilisation of the ZiG currency should be a collective multistakeholder approach of all economic agents in Zimbabwe. Above all, the government of Zimbabwe should ensure that it addresses all economic fundamentals that are a prerequisite for any good currency to stabilise and gain traction chief among them is confidence.

REFERENCES

- Arghyrou, M. G., & Tsoukalas, J. D. (2011). The Greek Debt Crisis: Causes and Policy Responses. Economic Policy.

- Athukorala, P.-C. (2001). Crisis and Recovery in Malaysia: The Role of Capital Controls. Asian Economic Journal.

- Bleaney, M., & Greenaway, D. (2001). The Impact of Terms of Trade and Real Exchange Rate Volatility on Investment and Growth in Sub-Saharan Africa. Journal of Development Economics, 65(2), 491–500.

- Bordo, M. D., & Kydland, F. E. (1995). The gold standard as a rule: An essay in exploration. Explorations in Economic History, 32(4), 423-464.

- Bordo, M. D., & Schwartz, A. J. (1997). The gold standard and related regimes: Lessons for the twentieth century. University of Chicago Press.

- Britannica. (2024). Gold Standard. Retrieved from Encyclopedia Britannica Online.

- Cheung, Y.-W., Chinn, M., & Fujii, E. (2018). China’s Exchange Rate Policy and Its Implications for Global Trade. Journal of International Money and Finance.

- Chigumira, G., & Moyo, M. (2020). “Economic Resilience in Zimbabwe: Lessons from Currency Crises.” Zimbabwe Economic Policy Analysis Unit (ZEPARU) Report.

- Chipika, S. (2015). Understanding Zimbabwe’s economic challenges: Lessons from the past. Zimbabwe Economic Policy Analysis Unit.

- Chitambara, P. (2019). “The Informal Economy and the Challenges of Policy Implementation in Zimbabwe.”. Labour & Economic Development Research Institute of Zimbabwe (LEDRIZ) Working Paper.

- Chitambara, P. (2019). The challenges of de-dollarization in Zimbabwe. Development Southern Africa, 36(6), 872-886.

- Chitambara, P. (2022). Zimbabwe’s currency crisis: Exploring the dynamics of hyperinflation and policy failures. Harare Economic Research Institute.

- Corrales, J. (2020). The Collapse of Venezuela’s Bolivar: Lessons in Currency Reform. Latin American Perspectives.

- Díaz Alejandro, C. F. (1985). Exchange Rate Misalignment in Developing Countries. World Development.

- Eichengreen, B. (1996). Golden Fetters: The Gold Standard and the Great Depression, 1919–1939 . Oxford University Press.

- Frankel, J. A. (2010). The Natural Resource Curse: A Survey” . National Bureau of Economic Research Working Paper Series, No. 15836.

- Friedman, M. (1948). “A Monetary and Fiscal Framework for Economic Stability”. The American Economic Review, 38(3), 245–264.

- Frimpong, J. M., & Adam, A. M. (2017). Currency Crisis in Ghana: Causes and Mitigation Strategies. West African Journal of Economic Policy.

- Fullarton, J. (1845). On the Regulation of Currencies. London: John Murray.

- Garten, J. E. (2021). The global financial system: The impact of the Nixon shock . HarperCollins.

- Gentle, M. (2021). The history of money: From bartering to Bitcoin . Financial Histories Publishing.

- Goldfajn, I., & Rigobon, R. (2000). “Hard Currency Pegs and Economic Stability in Emerging Markets.”. World Bank Economic Review, 14(3), 367–391.

- Hanke, S. H., & Kwok, A. K. F. (2009). “On the Measurement of Zimbabwe’s Hyperinflation”. Cato Journal, 29(2), 353–364.

- Hanke, S. H., & Kwok, A. K. F. (2009). On the high inflation of Zimbabwe, 2007–2008. Cato Journal, 29(2), 349-358.

- Heine, M., & Herr, H. (2003). The European Monetary Union. Springer.

- Herr, H. . (2024). Global monetary systems and the role of commodity-backed currencies. . Oxford University Press.

- Herr, H. (1992). “The Global Gold Standard and Its Consequences”. Journal of Economic Perspectives, 6(1), 157–174.

- Herr, H. (2024). Monetary Economics: Theory and Policy. Palgrave Macmillan.

- International Monetary Fund (IMF) . (2023). Zimbabwe: Article IV Consultation—Staff Report. . Washington, DC: IMF Publications.

- Jefferis, K. (2020). Fiscal Policy and Debt Management in Botswana: Lessons for Africa . African Journal of Public Policy.

- Keynes, J. M. (1933). “The Means to Prosperity”. London: Macmillan.

- Keynes, J. M. (1936). The General Theory of Employment, Interest, and Money. Macmillan.

- Kim, J., & Lee, H. (2017). Informal Sector Formalization and Economic Growth in Developing Economies. Development Policy Review.

- Kindleberger, C. P. (1986). The World in Depression, 1929–1939. University of California Press.

- Kramer, D. (2021). Ancient Chinese currency and its impact on global trade. Cultural Exchange Press.

- Kurkliński, W. (2017). “Money and Morality: The Catholic Church’s Doctrine and Modern Monetary Systems”. Journal of Religious Economics, 10(3), 200–220.

- Laum, B. (1924). Heiliges Geld: Eine historische Untersuchung über den sakralen Ursprung des Geldes [Sacred money: A historical study on the sacred origins of money]. Mohr Siebeck.

- Le Goff, J. (2012). Money and the Middle Ages: A Study in Economic History. Columbia University Press.

- Makochekanwa, A. (2016). The Impact of Currency Reforms on Zimbabwe’s Economy: A Case for De-Dollarization. African Economic Research Consortium (AERC) Research Paper No. 317. Retrieved from https://aercafrica.org

- Makochekanwa, A. (2019). Monetary policy and hyperinflation: A case study of Zimbabwe’s currency crisis. Journal of African Economics, 28(3), 301-322.

- Medina, L., & Schneider, F. (2018). Shadow Economies Around the World: What Did We Learn Over the Last 20 Years? International Monetary Fund.

- Ministry of Finance and Economic Development (MoFED). (2024). Zimbabwe’s Economic and Debt Report: Fiscal Challenges and Opportunities. Harare: Government Printers.

- Mishkin, F. S. (2021). The economics of money, banking, and financial markets (12th ed.). Pearson Education.

- Moyo, S., & Yeros, P. (2011). “Economic Reforms and Structural Challenges in Zimbabwe.”. Review of African Political Economy, 38(127), 289–302.

- Mpofu, M. (2020). De-dollarization in Zimbabwe: Challenges and prospects. Journal of African Political Economy, 15(2), 45-59.

- Mpofu, T. (2020). “Gold as a Stabilizing Anchor: Zimbabwe’s Monetary Challenges”. Journal of African Economic Policy Studies, 12(3), 122-137.

- Mutebile, E. T. (2021). Fiscal Discipline and Currency Stabilization: The Rwandan Case. . African Development Review.

- Ndlovu, T. (2018). The Zimbabwean dollar: Causes and consequences of currency collapse. International Monetary Review, 45(2), 150-164.

- Reserve Bank of Zimbabwe (RBZ). (2006). Annual monetary policy statement. Harare: Reserve Bank of Zimbabwe.

- Reserve Bank of Zimbabwe (RBZ). (2024). Monetary Policy Statement April 2024: Progress on Currency Reforms. Harare: RBZ Publications.

- Ricardo, D. (1821). Principles of Political Economy and Taxation. London: John Murray.

- Stoffels, H., & Neumann, K. (2009). “The Swiss Experience with Gold-Backed Currency”. Swiss Journal of Economics, 45(3), 198–210.

- Stoffels, P., & Neumann, R. (2009). The role of gold in the global financial system . Economic Review, 44-56.

- Tan, K. (2021). Currency Pegging and Policy Stability: The Singapore Dollar Experience. Economic Insights Quarterly.

- Tavuyanago, B., & Mutasa, F. (2019). “Challenges of Currency Reforms in Hyperinflationary Economies: Insights from Zimbabwe.”. Southern African Journal of Economic Studies, 15(4), 123–135.

- Techzim. (2024). Zimbabwe Gold Currency (ZiG): Will it succeed? Retrieved from https://www.techzim.co.zw.

- Thornton, H. (1802). An Enquiry into the Nature and Effects of the Paper Credit of Great Britain. London: Hatchard.

- Tikkanen, A. (2023). The evolution of money: From stone currency to digital assets. World Economic Review.

- Zicchino, L., & Hozz, A. (2019). Commodity-backed cryptocurrencies: The case of Venezuela. Journal of Digital Finance, 2(1), 8-24.

- Zuckerman-Parker M and Shank G . (2008). The Town Hall Focus Group: A New Format for Qualitative Research Methods. . 13(4), 630-635. Retrieved from http://www.nova.edu/ssss/QR/QR13-4/zuckerman-parker.pdf